Abstract

One the largest cases of kleptocracy is attributed to the 1Malaysia Development Berhad (1MDB) scandal involving the former Malaysian Prime Minister, Najib Razak. As a result of the pressure to pay the debt, Najib signed multiple inflated infrastructure loans from China in 2016. This study analyses the manipulation of Public Service Bargains as a critical variable influencing the foreign loan decision-making of the kleptocrat leader. It concludes that Najib's manipulation strategies transformed the established Trustee-type to kleptocratic-type bargains in Malaysia's foreign loan decision-making process. The post-Najib's restoration of Trustee-type bargains under the new Malaysian government, followed by a series of successful renegotiations with China, attest to the significance of the Public Service Bargains system on the foreign loan decision-making process. This analysis also contributes to the wider discussion on the critical side of China's Belt and Road Initiative amidst a global call for good governance.

Introduction

The 1Malaysia Development Berhad (1MDB) scandal, associated with the former Malaysian Prime Minister Najib Razak, is regarded as one of the largest cases of kleptocracy. From 1MDB's funds, as many as 3.5 billion USD were siphoned off by Najib. Out of this amount, more than 700 million USD ended up in his private bank account and more than 1 billion USD were laundered in the United States (Brown, 2018; Case, 2017; Milner, 2017; US Department of Justice, 2016; Wright and Hope, 2018). In 2015, 1MDB had accumulated a debt of 11 billion USD—over a period of five years—and was on a verge of defaulting on its payment. This is when Najib Razak turned to China's capital and soft loans for help. Under Beijing's Belt and Road Initiative (BRI), Najib took multi-billion-dollar loans for supposed infrastructure projects in 2016. While there are other legitimate Chinese investments in Malaysia (Abadi, 2019; Liu and Lim, 2019; Tham, 2018), Najib's 2016 deals cannot be considered a part of those investments.

Following the defeat of Najib Razak in the May 2018 general election, the Chief of the Malaysian Anti-Corruption Commission (MACC), Latheefa Koya, revealed that the loans and funds obtained from China were redirected into 1MDB to pay RM1.2 billion of its staggering debt through Chinese contractors and intermediary (The Edge Markets, 25 October 2018). Involvement of the Chinese Industrial and Commercial Bank of China in facilitating the transactions to pay off 1MDB's debt was later exposed by the Special Advisor of the new Finance Minister, Pua (2020). However, most studies on 1MDB and Najib Razak have focused on the domestic Malaysian political struggle (Case, 2017; Gabriel, 2018), financial perspective (Jones, 2020), or media reporting (Nazmi and Helmi, 2016); research has not been conducted on kleptocracy as a variable influencing the foreign loan decision-making process to understand the critical connection between the 1MDB scandal and Najib Razak's deals with China in 2016. In addition, most of the literature on the subject has neglected the role of top bureaucrats in the foreign loan decision-making process. This lacuna is the result of the treatment of bureaucrats as insignificant in the literature on kleptocracy vis-à-vis kleptocratic executive leaders since most of them emerged in institutionally weak Third World countries (Acemoglu et al., 2004; Andreski, 1968; Rose-Ackerman, 1999). However, this was not the case with Malaysia. It emerged as the new ‘Asian Tigers’ economy during the peak of ‘Asian Miracles’ in the 1980s, with highly professional bureaucrats at the apex of its administration (Daud, 2020; Embong, 2008; Gomez and Jomo, 1999; World Bank, 1993). The Malaysian bureaucracy was based on its colonial heritage, i.e. a merit-based British model of public administration system (Esman, 1972; Funston, 2001; Mansor and Noriza, 2015; Sarji, 1996; Siddiquee et al., 2019). In fact, Case (2017) elaborates that Malaysian bureaucrats possessed ‘significant technocratic capacity’, a group that ‘issues bonds and borrows internationally, operates state-invested banks and corporations, and adequately regulates macroeconomic policy’ to the extent that ‘defaults on government debt have been assiduously avoided and credit worthiness protected’ (Case, 2017, 637). To this end, the present analysis addressed the following question: How did Najib Razak's 1MDB scandal affect Malaysia's foreign loan decision-making?

This study fills this gap by not only assessing the role of a kleptocratic leader in the 1MDB scandal and the deals with China in 2016, but also the role of Malaysian bureaucrats in the decision-making process. Therefore, kleptocracy is identified as an independent variable affecting the Public Service Bargains (PSB) that consequently influence the dependent variable, foreign loan decision-making process, under a kleptocratic regime. Each of the variables is elaborated separately before a ‘kleptocratic bargains’ model for explaining foreign loan decision-making is developed. The analysis begins by theorizing the impact of kleptocracy on foreign loan decision-making. The following section discusses the combination of Public Service Bargain insights and political manipulation in the decision-making process to explain the kleptocrats’ use of two manipulation strategies, i.e. exclusion and inclusion, against other bureaucrats to achieve their foreign loan objectives. The next section elaborates the 1MDB scandal, followed by a discussion on three 1MDB-related loans from China: East Coast Rail Link (ECRL), Trans-Sabah Gas Pipe (TSGP), and Multi-Product Pipeline (MPP). The analysis reveals how Najib bypassed other influential actors, such as the Second Finance Minister and the Economic Planning Unit bureaucrats—while leveraging his loyalists at the Ministry of Finance and 1MDB—to fulfil his objectives to cover 1MDB's debt. Finally, a series of renegotiations between the new Malaysian government and China post-Najib Razak, and the implication of this case on China's BRI scheme are also discussed. For this purpose, along with secondary data, information has also been obtained through extensive interviews with five informants who have been directly involved in Malaysia's foreign loan decision-making process. The participants included a senior official at the Economic Planning Unit (EPU), a former senior official at the Ministry of Finance, a former Investment Director of Khazanah (the Malaysian sovereign wealth fund), a senior officer from the Malaysian Ministry of Foreign Affairs, and the fourth and seventh Malaysian Prime Minister Mahathir Mohamad.

Kleptocracy, Public Service Bargains, and Foreign Loan Decision-Making

Kleptocracy

The term ‘kleptocracy’ was first coined by Andreski (1968) as ‘a ruler or top official whose primary goal is personal enrichment and who possesses the power to further this aim while holding public office’ (Andreski, 1968, 92–109). In ‘kleptocratic’ regimes ‘the state is controlled and run for the benefit of an individual, or a small group, who use their power to transfer a large fraction of society's resources to themselves’ (Acemoglu et al., 2004, 1). A kleptocrat exploits their office to siphon off public funds into their own pocket (Andreski, 1968; Rose-Ackerman, 1999). In the context of the rise of post-Bretton Woods offshore financial systems following the end of World War II, kleptocracy became transnational with the emergence of intermediaries such as bankers, real estate brokers, accountants, lawyers, wealth managers, and public-relations agents helping kleptocrats to steal from people, hide their dirty money abroad, and spend that money in other countries (Bullough, 2018; Cooley et al., 2018).

Most of the literature on kleptocracy is devoted to the impact of kleptocratic activities on the domestic economy and social well-being of the impoverished population (Acemoglu et al., 2004; Andreski, 1968). Rose-Ackerman (1999) defined a kleptocrat as ‘a stockbroker or a real estate agent who makes money from turnover’, (Rose-Ackerman, 1999, 118) wherein he can ‘extract a share of the gains from any type of transaction involving the state and thus may support the privatization of some firms while supporting the nationalization of others’ (Rose-Ackerman, 1999, 118). However, there is yet to be an account on the impact of kleptocracy on a state's foreign loan decision-making process.

Manipulating Public Service Bargains

There are two dominant groups in the decision-making process, the executives (president, Prime Minister, cabinet and junior ministers) and the bureaucrats (departments, ministries, or central agencies). Among the available works on executive-bureaucrats interaction in the decision-making process (Aberbach et al., 1981; Bach and Wegrich, 2020; Peters, 1988; Svara, 2006), the Public Service Bargains (PSB) framework—developed by Hood and Lodge (2006)—provides a systematic understanding of the nature of power relations between both groups. Hood and Lodge (2006) define PSB as an explicit or implicit agreement between political executives and bureaucrats wherein the former normally expects some degree of political loyalty and competence from the latter in the decision-making process, while the bureaucrats normally expect to gain autonomy in the decision-making processual structure. Two types of bargains exist between these groups: agency and trustee bargains. In the former, bureaucrats are regarded as the political masters’ servants, while in the latter, they function autonomously. In essence, bureaucrats under trustee bargain possess a higher degree of autonomy wherein they ‘exercise discretion in a way that is not subject to commands or control from elected politicians’ compared to their counterparts in countries that practice agency bargains (Hood and Lodge, 2006, 25).

Hood and Lodge (2006) indicated that ‘cheating’ or manipulative behaviour are among factors other than wars, regime change, revolution, and long-term evolutionary processes that can alter the establish system of bargains. This section conceptualises the emergence of ‘kleptocratic bargains’ in established PSB as the result of kleptocrats’ manipulative strategies, eventually affecting the foreign loan decision-making process. This analysis argues that manipulation of the established PSB occurs when one or both sides of the bargain attempt to alter the established foreign loan decision-making process to suit their policy preferences. Some scholars have argued that individuals operating in a group context are often driven to alter the group's structure and processes to enhance the strength of a preferred policy option (Hoyt and Garrison, 1997, 249). This applies directly to kleptocrats. Under the guise of their kleptocratic interests—whether the demand to settle foreign debt or pressure from foreign investigation—a kleptocrat can easily accept external support, even though it may be damaging to the taxpayers’ money. Consequently, a kleptocrat undermines the bureaucrats’ autonomy in the foreign loan decision-making process to pursue or protect their interests.

Literature on the relation between bureaucracy and corruption (Dahlström, 2015; Dahlström et al., 2012) and their autonomy vis-à-vis the executives (Brehm and Gates, 1999; Carpenter, 2001) explain manipulation from the bureaucrats’ perspective. Hypothetically, a bureaucrat can either cheat or deliver according to their portfolio. Hood and Lodge (2006) explain that a bureaucrat is considered as ‘delivering’ their job when they execute specific tasks related to their public office, and a deviation from this is regarded as manipulation. Additionally, bureaucrats can be considered as manipulative if they join the kleptocratic executive's bandwagon to plunder public coffers instead of safeguarding them. This is in line with Dahlström’s (2015) analysis on bureaucrats’ involvement in ‘grand corruption’, wherein despite enjoying top public service and a high salary, few elite bureaucrats compromised their bargains and cooperated with their executive's corrupt practices. However, in some cases, instead of conforming with the kleptocrat, bureaucrats are able to forge political alliances to uphold their preferred policy and agenda against their executive political masters (Allison and Zelikow, 1971; Carpenter, 2001; Wilson, 1989).

This study incorporates Hoyt and Garrison’s (1997) strategies of political manipulation, i.e. inclusion and exclusion, to understand kleptocrats’ strategies to manipulate the established Public Service Bargains system according to their preferences. Hoyt and Garrison (1997) have argued that the executive possesses an upper hand in deciding who participates in the decision-making process; this is because those who are involved are likely to influence the process, including the number and nature of proposed solutions, definition of the solutions, and the relative strength of factions (Hoyt and Garrison, 1997, 253). Thus, the ‘exclusion’ strategy refers to the deliberate alteration of the composition of decision-making actors to include only those with shared interests and sympathetic viewpoints. The ‘inclusion’ strategy represents an attempt to diffuse the influence of opponents by packing the meeting(s) of actors involved in decision-making with additional like-minded participants (Hoyt and Garrison, 1997; Yukl and Tracey, 1992).

Therefore, a combination of kleptocracy and political manipulation gives rise to a third type of bargain, ‘kleptocratic bargains’. Under this bargain, both groups include those who benefit and those who lose from kleptocracy. For example, kleptocratic executives form alliances with compromised bureaucrats while excluding and bypassing non-corrupt executives and non-compromised bureaucrats. There are several indicators to measure the degree of inclusion or exclusion, as well as the pace and intensity by which these strategies are undertaken in foreign loan decision-making process. In terms of the degree of inclusion strategy, there are three indicators: first, most (not all) of the actors who are being involved in the decision-making process have no formal, established bureaucratic authority; second, they are reporting directly, and most of the time only, to the kleptocrat; and third, they performed their role in the decision-making process in a non-transparent manner, without accountability to the relevant bureaucratic body nor to the public. On the other hand, actors who are involved in the exclusion strategy are those with formal authority as established under the Trustee-type bargain and possessed technical expertise. In terms of the pace and intensity of both inclusion and exclusion strategies, the indicators are speed of execution, rank of the excluded bureaucrats, and amount involved in the foreign loan deals. The operationalisation of kleptocratic bargains vis-à-vis the foreign loans decision-making process is explicated in the following section.

Kleptocratic Bargains and the Foreign Loan Decision-Making Process

Small, developing states generally use different options to secure foreign capital, for example, foreign loans, foreign direct investment (FDI), foreign portfolio investment, and divesting equity and nonfinancial assets (International Monetary Fund, 2013; Nunnenkamp, 1989). Usually, such states prefer FDI over other options due to the higher financial risks and political risks involved with foreign debt inflows and nonfinancial assets divestment, respectively (Katzenstein, 1985; Lin and Sosin, 2001; Magcamit, 2016). High interest rates and the pressure to comply with ‘structural adjustment’ like privatisation and austerity programs, have often been cited as imminent threats of foreign loan (Edwards, 1983; Orelus and Chomsky, 2014a). Privatization/de-nationalization or divestment of strategic assets is often followed by the fall of debt-ridden leaders and regimes in Third World countries (Orelus and Chomsky, 2014b; Pepinsky, 2009). This phenomenon has been observed in countries with weak institutions and inefficient bureaucracy, such as countries in Latin America, Sub-Saharan Africa, and Suharto's Indonesia (Edwards, 1983; Pepinsky, 2009); however, the sudden increase in Malaysia's foreign loans from China in 2016—amidst Najib Razak's 1MDB scandal—was a puzzling incident.

It is argued that the established ‘Trustee-type Public Service bargains’ system in Malaysia has produced a consistent foreign loan policy, wherein the state's material gains are accumulated through equity shares and FDIs are attracted while maintaining the state's autonomy (Daud, 2020; Embong, 2008; Gomez et al., 2017; Lafaye de Micheaux, 2019). However, ‘kleptocratic bargains’ had hampered the foreign loan decision-making process to specifically serve their private material interests at the expense of the state's sovereignty, autonomy, fiscal position, and long-term debt.

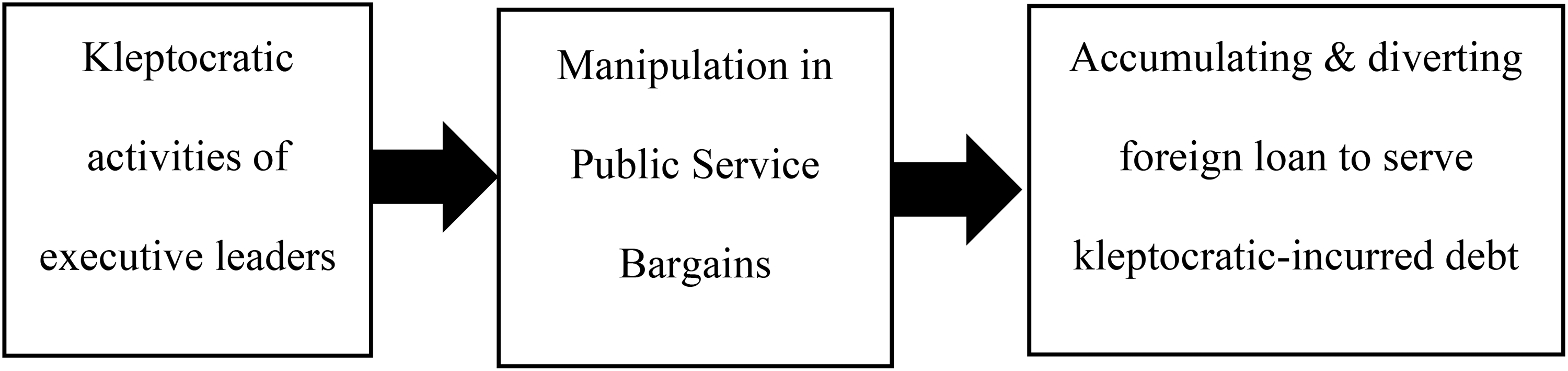

Both the agency and trustee pattern of executive-bureaucrat bargains are affected in the context of kleptocracy-incurred external pressure that directly affects—or even threatens—certain executives’ or bureaucrats’ interests. The push and pull incurred by kleptocracy can critically affect executives’ and bureaucrats’ interests, especially in terms of material consideration (Cooley et al., 2018). In such cases kleptocrats often face political and financial threats, such as foreign investigation and pressure to clear foreign debts, respectively. Consequently, in a ‘kleptocratic bargain’, the executives and bureaucrats may not always share the same assessment of external pressures. In fact, it is possible for one group to undermine their counterpart's threat assessments for the sake of preserving their interests. The differences in threat assessment of foreign loans logically compel those whose interests are threatened to abandon the established PSB system. This move is accompanied with the primary objective to change the state's foreign loan decision-making process. This is precisely where different manipulation strategies, elaborated in the previous section, come into play. On the one hand, internally, both exclusion and inclusion strategies alter the established system of bargains in the decision-making process. On the other hand, externally, decisions related to foreign loans can be altered. To that end, this model provides the following central assumption: when a political executive turned into a kleptocrat, a change in the Public Service Bargain can be expected to occur due to the inherent clash between the kleptocrat's private interest against the public interest supposedly guarded by the bureaucrats. Nevertheless, the manipulation strategy's capability of kleptocrats to achieve their interest defers depending on the actors involved in the decision-making process, the specific foreign loan in question, and their consequent implementation. To determine whether and how much the bargaining that has taken place causes a shift in the overall character of relations from the trustee type into an agency type of bargain, one can observe that such change has occurred once the bureaucrats are excluded from their key roles and functions that previously were their routine tasks, but at the same time they were not fired or terminated, nor was their formal job scope officially amended to portray the reduction in their authority. The theoretical model is illustrated in Figure 1.

The impact of kleptocracy on the foreign loan decision-making process.

Najib Razak's 1MDB scandal and Malaysia's foreign loan from China in 2016.

The proposed kleptocratic bargain model of foreign loan decision-making process implicates the following: kleptocracy and foreign loan decision-making process can be considered as endogenous variables, since they correlate with each other within the model. In contrast, the US pressure upon the kleptocrat, the Chinese willingness to provide loans and facilitate the loan diversion to serve the kleptocrat's debt through its bank and currency, are all treated as exogenous variables – entirely independent of the endogenous variables within the model. There is a caveat, however, since this model is applicable only in the context of a country with established Trustee-type bargains with the tradition of relatively autonomous bureaucracies. To that end, while its applicability might be limited, its predictability can be expected to be better.

The Making of a Kleptocrat: Najib Razak and the 1MDB Scandal

Having sketched the theoretical model of kleptocratic bargains in the foreign loans decision-making process, this section provides a brief account of 1MDB. It is a Malaysian state-owned strategic development corporation established by Najib Razak when he assumed premiership in 2009. Unlike the Khazanah, Malaysia's sovereign wealth fund, which is funded and invests on the government's behalf, 1MDB is regarded as a separate entity from the state (Gomez et al., 2017). While 1MDB has to find and invest its own funds, its loans are guaranteed by the government. 1MDB's Board Chairman, Wok Lodin Kamaruddin, has described 1MDB as a ‘strategic investment company’ that was ‘set up to drive the country's economy and long-term development’, driven by private sector thinking and practices (Case, 2017). Since its inception, 1MDB has rapidly raised its own funds through issuing bonds and borrowings. Nevertheless, the then Minister of EPU, Abdul Wahid Omar, had openly criticized 1MDB's business model; according to him the ‘model of low capitalization and huge borrowings’ was never sustainable (CNBC, 21 April 2016).

Indeed, five years after its inception 1MDB had defaulted on a payment to its bondholders. This was followed by the 2015 explosive revelation by the Wall Street Journal (WSJ) and Sarawak Report that more than 700 million USD from 1MDB's funds had been traced to Najib's private account (Case, 2017; Sarawak Report, 2015; Wright and Clark, 2015). Following his defeat in the 2018 election, Najib has been prosecuted in which the opening statement by the prosecutor Gopal Sri Ram was: “He [Najib] also caused amendments to be made to the articles of the company to place himself in sole control of important matters concerning the business and affairs of the company. In short, he was its plenipotentiary. Additionally, he was the chairman of the company's board of advisers. He used that position and that of Prime Minister and Minister of Finance to do certain acts and to exert influence over the board of 1MDB to carry out certain abnormal transactions with undue haste. The ultimate aim of the accused was to obtain gratification for himself. He succeeded in achieving that aim” (Astro Awani, 28 August 2019).

1MDB was later proven as a vehicle used by Najib to siphon off public resources and funds raised through his government-guaranteed bonds for the purpose of enriching himself – part of which he was sentenced to 12 years of jail, RM210 million fine, and instructed to pay RM1.69 billion in tax for offences related to abuse of power under Section 23 of the MACC Act 2009, three criminal breach of trust offences under Section 409 of the Penal Code (to serve 10 years for each count), and 10 years jail for each of the three counts of money laundering under Section 4(1)(b) of the Anti-Money Laundering, Anti-Terrorism Financing and Proceeds of Unlawful Activities Act 2001 (AMLATFPUAA) (Astro Awani, 2019; New Straits Times, 2020).

The list of luxury assets owned by Najib seized both in Malaysia and abroad has been documented by the Deputy Commissioner of Malaysian Anti-Corruption Commissioner (MACC) Mohamad (2019) as well as the US; epartment of Justice (2016). Among the long list of assets forfeited are Park Lane Hotel ($380 million), Time Warner Penthouse ($30 million), Park Laurel Condo ($33 million), Walker Tower Penthouse ($50 million), Viceroy L’Ermitage Hotel ($44 million), Beverly Hills Mansion ($31 million), Montalban House ($38 million), London Town House ($41 million), Red Granite Pictures’ investment in The Wolf of Wall Street ($100 million), Bombardier 700 Jet ($35 million), Van Gogh drawing ($5 million), and Monet Paintings ($92 million) (US Department of Justice, 2016). Eventually, the US Department of Justice (DOJ) launched a formal investigation and criminal lawsuits in 2016 and 2017, which sought to recover 3.5 billion USD stolen from 1MDB's funds between 2009–2015 in the form of assets found in the US through its Kleptocracy Asset Recovery Initiative.

Despite Najib's efforts to deny the US DOJ's charges, the financial reality had already hit 1MDB. The company had faltered on its debt payments in billions and the Najib-led government—as the guarantor of 1MDB—was desperately looking for foreign loans and capital to salvage 1MDB. The US DOJ's investigation revealed that one of the most pressing foreign debt pressures on 1MDB came from the International Petroleum Investment Corporation of Abu Dhabi (IPIC). For the acquisition of two power plants, 1MDB along with IPIC's subsidiary Aabar, had issued two 10-year bonds of 1.75 billion USD each in 2012. In this arrangement, 1MDB had to pay 1.37 billion USD to Aabar as a security deposit. However, IPIC had insisted that neither it nor Aabar received any payments from 1MDB, and the company that did—Aabar Investments PJS Ltd (Aabar BVI)—was not part of their group (The Edge Markets, 11 May 2017). 1MDB's delay in paying off IPIC's debt led to the devaluation of bonds issued by the Malaysian government, creating widespread political controversy (Sarawak Report, 2015). IPIC had declared that 1MDB had defaulted on its 1.1 billion USD debt and interest obligations (Reuters, 18 April 2016). IPIC's statement was considered as a bombshell since it confirmed the allegation that 1MDB had paid 3.5 billion USD to a British Virgin Islands shell company called ‘Aabar Investments PJS Ltd’ owned by Najib's close aid and advisor, Low Taek Jho (Jho Low), instead of the real IPIC-owned company, Aabar Investments PJS (Wright and Clark, 2015). After Najib-led government's collapse in May 2018, the ex-CEO of 1MDB, Shahrol Azral Ibrahim, testified in the High Court that in 2014, the company's funds had been embezzled in two tranches into the fake Aabar (The Edge Markets, 2 September 2020; Sinar Harian, 17 August 2020). Ultimately, Najib was desperate to cover the 1MDB's debts to IPIC, compelling him to apply for several loans disguised as mega infrastructure loans under China's BRI investment scheme.

Malaysia's 2016 Loans From China

East Coast Rail Link (ECRL) Contract to China Communication Construction Company

The largest loan secured by Najib Razak from China was procured four months after the US DOJ launched its official investigation on 1MDB in July 2016. During his visit to Beijing in November 2016, Najib awarded the RM55 billion ECRL project to the highly-controversial China Communication Construction Company (CCCC). The selection of CCCC as the project's main contractor was criticized as it was barred for eight years from conducting business on some World Bank projects because of a corruption scandal and played a leading role in building artificial islands in the South China Sea (Bogdanich and Forsythe, 2018). Since CCCC also does not produce trains, the later rolling-stock outsourcing can be questioned as ‘no formal indication has been made regarding the supplier of such vehicles for the ECRL’ (The Malaysian Reserve, 3 April 2017). At a staggering cost of RM91.67 million per kilometre, the project is considered as one of the most expensive interstate rail and cargo lines establishment in the world. It is also the largest rail link contract financed by Chinese loans under the Chinese BRI (The Edge Markets, 8 November 2016). Najib Razak had committed to pay a 3.5% interest rate with 85% loans from Chinese Export-Import (EXIM Bank) seven years after the construction started (Jomo, 2017). Also, amid the project's ‘uncertain’ impact and financial feasibility, the government's fiscal position could be ‘weakened’ if the project—amounting close to 8 percent of the country's public debt—‘fails to generate sufficient returns to service and repay the debt incurred’ (Lee, 2016).

Furthermore, most feasibility studies conducted for such a railway project in the East Coast in 1984 concluded that such a project was financially unviable (Jomo, 2017; Malaysiakini, 21 April 2019; Mohamad, 2017). An opposition MP, Tony Pua, exposed that the latest feasibility studies conducted by HSS Integration from 2009 to 2015 estimated that such a project would cost around RM30 billion, which is far from the RM55 billion figure announced by Najib (The Edge Markets, 15 November 2016). Furthermore, Najib's administration refused to make HSS's feasibility studies public. Eventually, the Sarawak Report exposed the details of Najib Razak's plan. The premier had inflated the cost of ECRL by billions with the consent of its Chinese counterpart to cover 1MDB's debt to IPIC (Sarawak Report, 2016). The testimony of Najib's close aid, Amhari Efendi, in the High Court during the 1MDB trial in September, 2019 and the WSJ's report on the ECRL backdoor deal in January, 2019 confirmed the accusation. While Najib was able to pay a part of 1MDB's debts to IPIC through the inflated cost of ECRL, China would clearly benefit massively in terms of strategic and economic returns from the project, at the Malaysian taxpayers’ expense (Abadi, 2019; Abadi, 2021; Jomo, 2017; Mohamad, 2017).

Trans-Sabah Gas Pipe (TSGP) and Multi-Product Pipeline (MPP) Contracts to China Petroleum Pipeline Bureau

The MPP involved a 600 km multi-product petroleum pipeline connecting Melaka and Port Dickson to Jitra, in northern Kedah and costing 4.53 billion yuan and RM2.53 billion, or approximately RM5.35 billion. The TSGP was a 662 km gas pipeline from the Kimanis Gas Terminal to Sandakan and Tawau, costing 3.08 billion yuan and RM2.14 billion, or approximately RM4.06 billion (The Star, 5 June 2018). Following Najib's defeat in 2018, the new Finance Minister, Lim Guan Eng, has discovered that 88% of the total funds for both the projects have been utilized but only 13% of the work has been completed (The Star, 6 June 2018). Both projects were ‘kept hidden’ under the red files, away from the scrutiny of most officials in the Treasury during Najib's premiership. Lim Guan Eng revealed that the ministry was shocked to discover that RM 4.71 billion and RM 3.54 billion for the MPP and TSGP projects, respectively, had already been paid to the China Petroleum Pipeline Bureau (CPPB) despite the fact that at the end of March, 2018, the projects had achieved only 14.5% and 11.4% completion, respectively. In total, RM 8.25 billion constitutes a staggering 87.7% of the projects’ total value, despite the average completion rate of only 13% and two years remaining on the contracts. This also marked another deviation in Malaysia's foreign loan decision-making process because it was based entirely on time-based milestones and not on progressive work completion milestones (The Star, 6 June 2018).

Najib Razak's Manipulation Strategies and Kleptocratic Bargains

In the established Malaysian foreign loan policy-making process, Malaysian executives, such as the Prime Minister and Finance Minister, provide a high degree of autonomy to their bureaucratic counterparts, such as the Treasury Secretary-General at the Ministry of Finance (MoF) and the Economic Planning Unit (EPU). This Trustee-type bargain results from the political-economic system that allocates foreign loan decision-making responsibilities to the following three central agencies: ‘Federal Treasury, which deals with budget and loan approval; EPU, which is responsible for government allocations and project approval; and Public Implementation Co-ordination Unit, whose function is to monitor and evaluate the performance of public enterprises in the country’ (Mohamad, 1995, 68). According to a senior EPU official, Malaysian executives allocated such autonomy to EPU to increase the local equity share vis-à-vis foreign ownership (Mehmet, 1986; Puthucheary, 1960). The institutional strength of Malaysian bureaucrats under the Trustee-type Public Service Bargains is recognized by Hood and Lodge (2006) and is well-documented in the developmentalist state literature on political economy (Daud, 2020; Embong, 2008). However, Najib's 1MDB scandal and subsequent deals with China altered this system from Trustee-type to kleptocratic bargains through a series of manipulations.

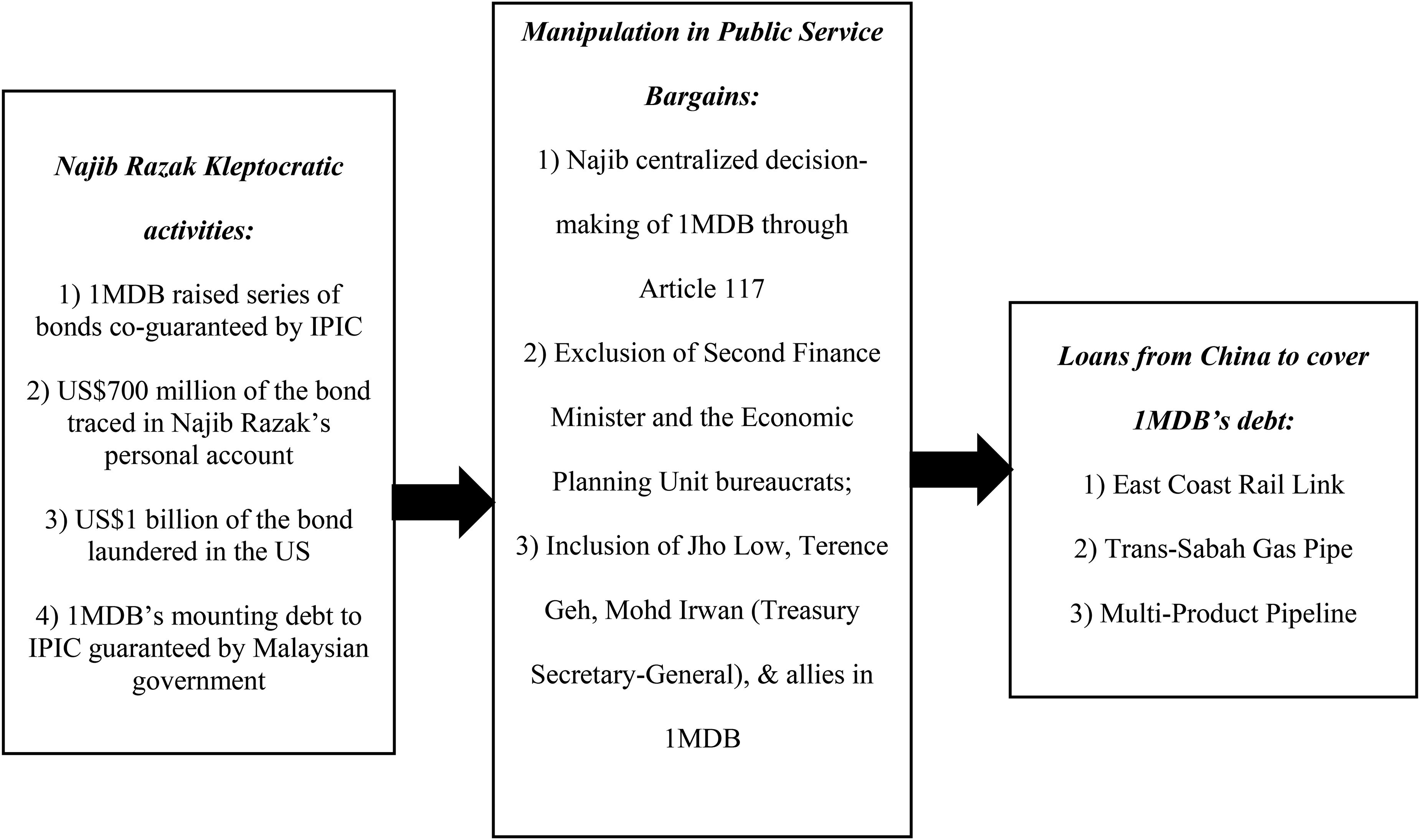

When Najib established 1MDB in 2009, he quickly ensured his complete control over the company, while at the same time excluding the senior bureaucrats – which was a departure from the conventional economic decision-making in Malaysia. While it was Mahathir (1981–2003) who started the tradition of the Prime Minister simultaneously holding the Finance Minister post, and monopolising key economic decision-making, Najib went further by excluding key senior bureaucrats while at the same time creating a vehicle like 1MDB with distinct decision-making authority. There was no major foreign loan taken by Mahathir that was proposed entirely without the input and consent by senior bureaucrats and that was signed as fast as those of 1MDB, along with strong objections by key EPU bureaucrats and the Malaysian Central Bank.

Court documents show that on 2 September 2009, Najib-controlled Ministry of Finance Inc. inserted Article 117 into the 1MDB contract which made Najib the sole stakeholder in making decisions related to the company's investments and gave him the power to overrule board decisions (The Edge Markets, 12 September 2019). This article replaced Article 9A, which gave the decision-making authority to the ‘Federal Government’, not the ‘Prime Minister’ (The Edge Markets, 17 October 2019). While officially 1MDB had a three-level corporate structure, including a management tier, a board of directors, and an advisory board, Najib Razak—as Prime Minister, Minister of Finance, and Chairman of 1MDB's advisory board—was the sole signatory of all 1MDB investments. The former chief executive officer of 1MDB, Shahrol Azral Ibrahim Halmi, revealed that the transfer of decision-making power from the federal government to the Prime Minister was made at Jho Low's advice.

During his premiership, Najib had appointed Ahmad Husni Hanadzlah as the Second Finance Minister (10 April 2009–27 June 2016), who had resigned from this post amid the 1MDB scandal. Five months later, in November, 2016, he and the ex-Deputy Prime Minister Muhyiddin Yassin—who was sacked by Najib—were investigated under the Sedition Act 1948 for allegedly revealing 1MDB's secrets (The Edge Markets, 8 November 2016; New Straits Times, 29 October 2016; Free Malaysia Today, 31 October 2016). This indicated Najib's use of inclusion and exclusion as manipulation strategies which is in contrast to the two PSB conditions: political loyalty and competence as argued by Hood and Lodge (2006, 5). Najib not only excluded those who are competent like the then-EPU Director-General Bivi Rahamat Yusof, but also the then Second Finance Minister Ahmad Husni Hanadzlah and Muhyiddin Yassin who was politically loyal to him prior to the 1MDB scandal. It must be noted that both Husni and Muhyiddin had been in Najib's Cabinet since his first day as a Premier. In addition, to support the ‘inclusion-exclusion’ argument, Najib had not sacked or replaced the then-EPU Director-General with a political loyalist to prepare his loan proposal to China. Instead, Najib gave the tasks to Jho Low and Amhari on an ad hoc basis. This is also the same in the case of Irwan Serigar who was appointed by Najib to sign the Suria Strategic Energy Resources Sdn Bhd (SSER) contracts with China barely a week after his appointment (see page 24).

An examination of the composition of actors involved in the decision-making process revealed two clear patterns. First, certain actors were usually involved in the discussion but excluded from the decision-making process. Second, those actors were deliberately excluded from the process by virtue of Najib's authority. In fact, even the CEO of 1MDB, Shahrol Azral Ibrahim Halmi, testified at the High Court in 2019 that he had been ‘discouraged’ from inquiring about matters that were not under his purview and ‘everyone within the company had worked in their own ‘silos’’ (The Malaymail, 21 October 2019).

Exclusion Strategy

Najib Razak had deployed the strategy of exclusion in the 2016 loans from China while he was being investigated by the US DOJ. The deals can be considered as the most controversial breach of the established Trustee-type bargains in Malaysia's foreign loan decision-making process. The EPU bureaucrats were excluded from the process of designing loan proposals and their advice and warnings against this loan were also rejected (MalaysiaKini, 21 April 2019). In the interview, a senior official described this exclusion as ‘unethical’, which ‘violated the procedure’, and something which was ‘not supposed to happen’ (Senior official at Malaysian Ministry of Foreign Affairs 2019). Daim Zainuddin, who was appointed as the Special Envoy by the new Malaysian government to renegotiate with China, further exposed this process of exclusion. He criticized Najib for pushing for the old ECRL project at a hefty cost of RM65.5 billion at the people's expense and ‘neglected good advice’ from the EPU bureaucrats. He emphasized: ‘Did the EPU not make clear its objections and concerns over the paper that was presented to the cabinet, and why were these objections and concerns ignored?’ (MalaysiaKini, 21 April 2019). In an interview, a senior EPU official revealed that the EPU Director-General ‘wrote a letter to object the Prime Minister's plan’ since the ‘facts and figures’ were against the plan (Senior EPU Official, 2020). This explains why Najib did not extend the then EPU Director-General Rahamat Bivi Yusoff's contract. The former Investment Director of the Malaysian sovereign wealth fund, Khazanah, described Rahamat Bivi Yusoff as ‘the bravest and strongest bureaucrats’ who dared to stand up against the Prime Minister's China deals (Former Khazanah Investment Director, 2019).

Additionally, the Malaysian parliament was excluded from the project altogether. Unlike other mega infrastructure projects in Malaysia that involved foreign companies, no Parliamentary approval was ever requested for the ECRL deals (The Edge Markets, 8 November 2016). In contrast to the establishment of special purpose vehicles that are ‘usually formed as a subsidiary of a big corporation with a strong built-up capital’ (The Malaymail, 8 November 2016), the one established to operate ECRL, known as the Malaysia Rail Link (MRL) was made in a rush with a mere budget of RM2.00. A former official at the Malaysian Ministry of Finance (2020) admitted in an interview that MRL was approved by the MoF, indicating Najib's control as the Finance Minister.

Another exclusion target as revealed by Tommy Thomas, the Malaysian Attorney General, was the Malaysian Central Bank (BNM):

‘Next, the source of financing the RM8 billion. Again, the Chinese connection: through EXIM Bank China. As SSER was borrowing massively from a foreign bank, the law required prior written approval from Malaysia's Central Bank, Bank Negara. The latter, not surprisingly, insisted that payments should be made by SSER to CPPB on work progress, and not on a fixed-time basis. This express term was imposed by Bank Negara in its approval letter to SSER. SSER's decision to openly defy Bank Negara's condition imposed on it can only lead to the conclusion that the absurd payment terms in the contracts were not a product of bad legal advice, oversight, negligence, or even woeful incompetence on the part of SSER's management, but rather the result of a deliberate and calculated decision made with the sanction of a voice more powerful than Bank Negara. Only one candidate exists: the Minister of Finance, Najib, who was also the Prime Minister’ (Thomas, 2021, 236–237).

In 2015, the BNM had recommended the Attorney General to initiate criminal prosecution against Najib-controlled 1MDB for breaches under the Exchange Control Act 1953 (ECA), stating that their investigations found that permissions required under the ECA for 1MDB's investments abroad were ‘obtained based on inaccurate or without complete disclosure of material information relevant to the bank's assessment of 1MDB's applications’ (The Sun Daily, 9 October 2015). Subsequently, BNM has revoked three permissions granted to 1MDB under the ECA for investments abroad totalling US$1.83 billion (RM7.55 million) and also issued a direction under the Financial Services Act 2013 to 1MDB to repatriate the amount of US$1.83 billion to Malaysia (The Sun Daily, 9 October 2015). However, the contract of the then BNM Governor Zeti Akhtar Aziz was not extended, while the services of the former Attorney-General Tan Sri Abdul Gani Patail, who was preparing to press charges against Najib, was terminated ‘due to health reasons’ (The Edge Markets, 16 May 2016).

Inclusion Strategy

Amid the pressure against his kleptocratic 1MDB's debts, Najib Razak employed the aggressive ‘inclusion’ manipulation strategy: a former Investment Director of the Malaysian sovereign wealth fund under the MoF revealed how Najib's aide, Jho Low, was ‘omnipresent in the Ministry of Finance’ and assisted Najib to ‘inflate the loans from China to cover 1MDB's loopholes.’ Najib also instructed several of his loyalists to abandon the established Trustee-type Public Service bargains. These included the appointment of a top bureaucrat, Irwan Serigar Abdullah, as the Treasury Secretary-General (involved in TSGP and MPP pipeline loans from China) and Abdul Rahman Dahlan, as the Economic Planning Minister (involved in the ECRL and pipelines decision). Jho Low's ally, Terence Geh (1MDB Director of Finance) was appointed as the project secretariat for all loans, including ECRL, TSGP, and MPP projects, from China in 2016 (New Straits Times, 4 September 2019). During the 1MDB trial, the ex-1MDB CEO, Mohd Hazem Abdul Rahman, testified that Jho Low was responsible for appointing the 1MDB board of directors, which can be considered as an inclusion strategy that secured Najib's proxies in the 1MDB financial decision-making process (Sinar Harian, 14 September 2020).

Najib's Special Officer, Amhari Efendi Nazaruddin, also exposed his inclusion manipulation strategies. Testifying at the Malaysian High Court on 4 September 2019, Amhari revealed that Najib had instructed him and Jho Low to secure the ECRL, TSGP, and MPP loans from China to bail 1MDB out of its debts during his ‘secret mission’ to Beijing to convince China to help pay 1MDB's debts. Amhari revealed that he went to China on 28 June 2016 and found out that Jho Low was also involved in the discussions with the Chinese parties. Amhari Efendi Nazaruddin testified: “The confidential instructions from Najib were made after the 1MDB fundraising issue was widely circulated. Najib directed me to China to represent him to confirm the economic relations of both countries including China-Malaysia investments. However, based on what Jho showed me through talking points and action plans, the deal and joint venture is an investment that will help repay 1MDB's bailout like 1MDB's debt repayment to IPIC” (The Edge Markets, 4 September 2019). The minutes from a series of a previously undisclosed meeting on 28 June 2016, reviewed by The WSJ in January, 2019, describe ‘a plan proposed by Malaysian officials for Chinese state companies to build two large projects with funding from Chinese banks’, referring to the ECRL and the TSGP-MPP projects, confirming Amhari's account. The document stated that those projects would provide ‘above market profitability’ to the Chinese state companies, and Xiao Yaqing, the Chairman of China's State-owned Assets Supervision and Administration Commission, stressed during the meeting that the public must believe ‘all initiatives are market driven for the mutual benefit of both countries’. Xiao also informed that he ‘cancelled all his key engagements in Beijing to attend’ the June 28 meeting because the matter ‘has been approved by President Xi Jinping, Premier Li Keqiang’ and another senior Chinese official (Wright and Hope, 2019).

The former CEO of 1MDB, Mohd Hazem Abdul Rahman, also testified that Jho Low and Najib Razak monopolised the financial decision-making process of the company to the extent that even he was not allowed to manage the company's funds abroad (Sinar Harian, 17 September 2020). If the ECRL was parked under the Najib-controlled special purpose vehicle, the MPP and TSGP projects were handled by another MoF subsidiary, SSER. Similar to ECRL, both projects were approved by the Cabinet on 27 July 2016, two days after they were presented. Both pipeline projects amounted to RM9.41 billion, which was awarded to the CPPB on 1 November 2016, following the signature of the then Treasurer-General, Irwan Serigar Abdullah, who was also the chairman of SSER (The Star, 6 June 2018). This is an example of kleptocratic bargains wherein Mohd Irwan Serigar was working with Najib Razak to cover 1MDB's debts through the SSER company—chaired by him—and which was responsible for both TSGP and MPP pipelines loans from China. The Malaysian Attorney-General emphasized: “Mohd Irwan Serigar bin Abdullah signed the construction contracts on behalf of SSER, a week after his appointment. As the principal director of SSER, he was required to exercise reasonable care, skill and diligence, when he signed the two contracts. It would have been impossible for him to have studied the documents, given the magnitude, complexity and phenomenal value of the contracts involved, and to have comprehended the true nature of SSER's obligations. Tan Sri Irwan is currently facing criminal charges in a 1MDB scandal-related fraud” (Thomas, 2021, 237). The finding is illustrated in Figure 2.

Post-Najib Razak: Trustee-Type Restoration, Renegotiation of China Deals, and Reflection on Belt and Road Initiative

Najib's 1MDB scandal was met with unprecedented resistance from the unified opposition bloc and international coverage of the issue. As a result, he lost the historic 14th general election of Malaysia (Nadzri, 2018). The magnitude of kleptocracy's negative impact on the Malaysian lives and economy was devastating: in May 2021, Finance Minister Tengku Zafrul noted that despite RM15.5 billion of 1MDB and SRC's debts had been repaid by the government, there remains more than RM42.3 billion in debts, comprising both principal and interest in which he later emphasized ‘Just imagine how many people we could have helped during this pandemic if this amount of nearly RM58 billion were available for use’ (The Star, 26 May 2021). He also condemned 1MDB, SRC, and SSER, as these projects ‘cannot generate income to finance their principal…have zero multiplier on GDP and contribute zero revenue to the government…. The government would have been able to foot the bill for the financial needs in the current crisis if it was not for 1MDB’ (The Edge Markets, 26 April 2021).

The return of the former premier, Mahathir Mohamad, as the new Prime Minister restored the Trustee-type bargains system. He established a Council of Eminent Persons (CEP) including formidable bureaucrats with a technocratic background, such as: a UN-recognized economist, Jomo Kwame Sundaram; former Finance Minister and Economic Advisor to the Prime Minister Daim Zainuddin; former Central Bank Governor Zeti Akhtar Aziz; and Hassan Marican, the former CEO of Petroliam Nasional (Petronas) who turned it into a Fortune 500 company (Sukumaran, 2018). The CEP works in conjunction with bureaucrats from the EPU, Bank Negara (Central Bank), and Attorney General's Chambers (The Star, 4 June 2018).

Due to the restoration of the broken Trustee-type Public Service bargains, the new government immediately suspended, renegotiated, and even cancelled several deals with China made by Najib in 2016, making Malaysia the only country to do so (The Edge Markets, 12 April 2019; Mourdoukoutas, 2019a). Prime Minister Mahathir Mohamad eventually announced that the ECRL project would be continued at a much lower cost of RM44 billion (The Edge Markets, 12 April 2019). In addition, the CCCC agreed to refund some of the RM3.1 billion which was paid in advance by Najib Razak's government, and the participation of Malaysian contractors increased from 30 to 40 percent. The TSGP and MPP projects were cancelled, and the new government demanded the return of RM9 billion payment made to China by Najib's administration (Straits Times, 10 September 2018) along with 243.5 million USD that were seized from the China Petroleum Pipeline Engineering (CPP) bank account at HSBC Malaysia in July, 2019 (Reuters, 15 July 2019).

The new government also proceed to charge Najib Razak along with his allies, including Mohd Irwan Serigar (the Treasury Secretary-General), Jho Low, and Terence Geh, for the deals with China. In October 2018, Mohd Irwan Serigar and Najib Razak were jointly charged with six counts of criminal breach of trust (CBT) involving a sum of RM6.636 billion worth of government funds, including two charges totalling RM1.855 billion related to the ECRL, TSGP, and MPP pipeline projects (The Edge Markets, 25 October 2018). While MACC's findings proved the efficiency of Najib's kleptocratic bargains, it also highlighted the drawbacks of the Chinese BRI. China was willing to lend Najib overinflated loans for his kleptocratic-incurred debts, to further their interest in strategic infrastructure contract and profit from the lucrative interest rate (Doig, 2019; Jomo, 2017; Lafaye de Micheaux, 2019; Mahavera, 2016; Mourdoukoutas, 2019b; Pua, 2020; Wright and Hope, 2019). Tony Pua, the Special Advisor of the new Malaysian Finance Minister, has provided details of the Chinese role in facilitating their loans to serve the 1MDB's debt: “By May 2017, the then Prime Minister Dato’ Seri Najib Razak had signed the Phase I and Phase II of the East Coast Rail Link (ECRL) project with a total value of RM55 billion with China Communications and Construction Company (CCCC). By June 2017, Malaysia had paid CCCC RM1,931.4 million and another CNY17,320 million via a loan from China Exim Bank.

28 Aug 2017 – CNY7,279,500,000 transferred from Multi-Strategic Investments Limited, Hong Kong (MSIL) to Al-Asbah International General Trading, Kuwait (a company with USD1,350 paid up capital). MSIL is a wholly-owned subsidiary of Zhen Hua Engineering Co Ltd, which in turn is a wholly-owned subsidiary of CCCC.

28 Aug 2017 – CNY7,279,500,000 transferred from Al-Asbah International General Trading to the personal account of its sole shareholder, Sheikh Sabah Jaber Al-Mubarak Al-Hamad Al-Sabah.

30 Aug 2017 – CNY4,253,000,000 transferred from Sheikh Sabah to Silkroad Southeast Asia Real Estate Limited.

30 Aug 2017 – CNY4,253,000,000 was then transferred from Silkroad Southeast Asia to Sentuhan Budiman Sdn Bhd, a wholly-owned subsidiary of the Ministry of Finance holding the 1MDB Air Itam land.

30 Aug 2017 – CNY1,950,000,000 was transferred from Sentuhan Budiman to IPIC, Abu Dhabi as part of 1MDB's debt repayment agreement.

Between September 2017 to March 2018, the balance of the receipt in Sentuhan Budiman was used to service the interest of other 1MDB debts.

“Most critically, all of the above transactions were facilitated by Industrial & Commercial Bank of China. The billions of renminbi were transferred from ICBC Hong Kong to ICBC Kuwait to ICBC Kuala Lumpur to ICBC Abu Dhabi in a matter of 3 days. The transactions, carried out entirely in Chinese yuan, were obviously meant to circumvent anti-money laundering detection of US dollar transfers in the light of international scrutiny over 1MDB” (Pua, 2020).

Conclusion

This analysis enumerates the impact of kleptocracy on the foreign loan decision-making process of a developing country. It proves that kleptocrats are not necessarily unitary actors, especially in an established political system with a strong bureaucratic structure. Prior to the 1MDB scandal, the Malaysian executive delegated significant autonomy to their bureaucratic counterparts, under the long-established Trustee-type bargains system. However, after the incident, Najib devised a series of inclusion and exclusion manipulations strategies, against non-corrupt and non-compromised bureaucrats. This caused an alteration of the Trustee-type bargains system to a kleptocratic bargains system, leading to a massive accumulation of inflated loans from China to cover his 1MDB debt. The post-Najib Razak's restoration of Trustee-type bargains under the new Malaysian government, followed by a series of successful renegotiations with China, attest to the significance of the Public Service Bargains system on the foreign loan decision-making process.

In terms of policy implications, there are several political institutional reforms that must be implemented. First, there must be a separation between the Prime Minister and Finance Minister posts. Second, the Governor of the Central Bank needs to be freed from the Finance Minister's jurisdiction. Third, the parliament need to be empowered, for instance, through frequent supervision by the Public Account Committee (PAC) on the government's foreign loans. Fourth, a stronger whistleblower's protection act is needed to ensure the freedom of the public or bureaucrats to report violations against public interest Finally, the Attorney General and MACC need to be freed from the control of the Department of the Prime Minister to ensure their independence.

In addition, this analysis also critically evaluates China's BRI in assisting the kleptocrat. It traced Chinese assistance to Najib's schemes of misappropriating the 2016 loans to pay off 1MDB's debts to the IPIC through Chinese contractors and banks, with the approval of top Chinese officials. Therefore, this analysis provides a stepping-stone for future comparative studies on the role of China's BRI scheme vis-à-vis the foreign loans decision-making process by kleptocratic leaders in other BRI participant countries.

Footnotes

Acknowledgements

I would like to thank my supervisors at Leiden University, Kutsal Yesilkagit and Johan Christensen, Muhamad Takiyuddin Ismail from UKM, as well as the two anonymous reviewers for their very helpful comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Kementerian Pengajian Tinggi (KPT) Malaysia and Universiti Kebangsaan Malaysia (UKM) (grant number Grant GP-2019-K014994.).