Abstract

Who gets what in portfolio allocation, and how does it matter to coalition partners’ legislative support in presidential systems? I propose that portfolios are not all alike, and that their allocation as well as the support for the president's agenda depends on the particular distribution of assets within the executive. The portfolio share allocated to coalition parties is weighted by a measure of importance based on the assets controlled by the ministry in question, such as policies, offices, and budgets. Once the weighted allocation of ministries has been identified, the results show that: 1) the president concentrates the most important ministries in their own party, mainly considering the policy dimension; 2) the positive relationship between portfolio allocation and legislative support remains, with the importance of specific dimensions being considered; and, 3) coalition partners do not respond differently in terms of legislative support in light of the different assets’ distribution within the portfolio allocation.

Introduction

Government formation means translating electoral results into executive power. Governments may be formed by a single party or by multiparty coalitions. If the latter occurs, everything becomes more complex and government formation thus becomes a negotiation over who gets what.

For a long time, the discussion on coalition formation was considered typical of the literature on parliamentary systems. This was a consequence, first and foremost, of the widespread notion that presidentialism and coalitions were incompatible, whether because the president does not have incentives to share power or because parties do not have access to the main prize, the presidency (Mainwaring 1993). However, when comparing different political systems, Cheibub, Przeworski, and Saiegh (2004) found that multipartism generates cooperation incentives for coalition governments in both parliamentary and presidential systems. While the institutions are different, the motives for coalition formation are similar. Thus it is now necessary to expand the discussion, and to thereby understand the incentives that actors have to form coalitions in both of these political systems.

In presidential ones, the president forms coalitions to build legislative support for their agenda (Amorim Neto 2006). The terms of the exchange would be the following: parties commit themselves to support the president's legislative agenda while the president reciprocates by distributing ministries for the parties. Coalition government represents an equilibrium, because it formalizes the agreement and institutionalizes the exchange between actors – thereby overcoming the negative situation in which the president negotiates with each legislator individually (Raile, Pereira, and Power 2011). From the point of view of coalition partners, the deal would be beneficial because controlling ministries means access to the executive's decision-making process – wherein parties can now influence policy decisions, budget allocations, and political appointments too.

The goal of this article 1 is to evaluate to what degree the terms of this agreement are actually honored; that is, how the president allocates portfolios and how much this affects legislative support received from coalition parties. The analysis of how coalitions actually govern is particularly important for presidential systems. In this respect, results observed therein may differ substantially from in parliamentary ones. First, because in parliamentary systems proportionality is the rule – something very distant from the reality of presidential ones, where the president is always the formateur – incentives thus exist to maximize each's share of the prize. Second, because in parliamentary systems once in the coalition party support is taken as a given – since the same parties sit in the very cabinet where the deal is made. In presidential systems, parliament is also a relevant locus where decisions are made (Laver 2006) and, especially in Latin America, parties are not always seen as programmatic (Mainwaring 2001; Nicolau 2006). This means that legislative support for the president's agenda is less predictable (Amorim Neto 2000; Pereira and Rennó 2003).

I would like to thank the participants of the Comparative Presidentialism course at the University of Oxford, especially Timothy Power and Paul Chaisty for their comments and suggestions. I would also like to thank the participants of the Political Institutions panel of the 10th Meeting of the Brazilian Political Science Association (Associaçâo Brasileira de Ciência Política, ABCP) and the anonymous reviewers and editors of JPLA for their valuable comments and revisions.

The focus here is on the specific attributes concerning portfolio allocation, and how this affects the executive–legislative relationship in presidential systems. For this, it is assumed that ministries are not all alike and that these differences must be evaluated regarding the degree to which they reflect the various assets controlled by the executive. I argue that the number of ministries alone is not sufficient indication of the gains of coalition parties in portfolio allocation. I propose a measure of importance based instead on the ministries’ assets, an approach that incorporates key policy, budget, and office dimensions. The “policy” one refers to the number of legislative initiatives proposed by the ministry; “budget” refers to the total and to the investment budget controlled by the ministry; and, the “office” dimension refers to the number of discretionary office positions allocated within the ministry.

These dimensions reflect the main political motivations for government participation: policy, office, and votes. Political parties may seek influence over policy, and for this controlling a ministry – with substantial participation in the drafting of legislation - would be relevant. Politicians may also be interested in the office itself, and in the possibility of patronage with the appointment of political cronies in the administration; for this, occupying a ministry with a large number of political appointment positions would be preferable. Last, political parties may be interested in cultivating the electoral support of voters; the use of public expenditures and holding a ministry with a massive budget would directly serve this purpose.

In sum, politicians may be motivated by policy, office, or votes - and portfolio allocation serves all of these desirable ends. However, ministries taken individually do not serve all of these purposes equally at the same time. One ministry may be policy relevant while only controlling a small budget, and this is why we need to take into account the differences in the importance of respective ministries.

I use a weighted payoff for this importance, to identify the president's decision on who gets what in portfolio allocation and to also explain the coalition's support for the executive's legislative agenda. I revisit the traditional argument about the proportionality rule in portfolio allocation (Gamson 1961; Amorim Neto 2006), and about the positive relationship between portfolio allocation and legislative support (Amorim Neto 2000). The main argument proposed here is that the president's strategy in portfolio allocation and the effect of that portfolio share on legislative support varies according to the specific distribution of assets within the executive. This happens because of the respective incentives that exist for the president and for coalition partners. Regarding the president, the goal is to minimize the risk of policy drift – thus concentrating government coordination and policy formulation within their own party. From the coalition partners’ point of view, meanwhile, they can more easily claim credit for geographically targeted policies than for more diffuse governmental ones that would instead be directly attributable to the president.

From this it is expected that the president will allocate a disproportionate share of portfolios to co-partisans, especially considering the high-value ministries in the policy dimension, and will distribute esteemed portfolios per the budget dimension more evenly. Concerning legislative support, it is expected that the larger the gain within the executive, the greater the support in the legislature. However, following the main argument, this effect is expected to be more acute when it comes to the portfolio share weighted by budgetary importance.

I constructed an original dataset to address these questions with information regarding the Brazilian case, for the period of 1999–2014. The justification for the case study is that it is a starting point for the construction of little-explored measures and innovative tests for hypotheses. First, I describe the relative importance of the different ministries. Then, I analyze who gets what in portfolio allocation in the current Brazilian coalitional presidentialism. Last, I test the effect of portfolio allocation on legislative support, using the measure of coalition discipline toward the government.

The main contributions of this article are threefold. First, it is shown how presidents distribute portfolios via considerations of the different assets that the respective ministries control. To do this, I present a measure of portfolio importance based on objective indicators and not survey data, as is usually done in the parliamentary systems literature; this reveals that ministries may be valued for different reasons. Second, it is demonstrated that coalition partners are not treated equally and that the president allocates a disproportionate share of portfolios to co-partisan ministers. This concentration is especially acute when considering the policy importance of ministries. Third, I revisit established arguments in the literature and show that the positive relationship between portfolio share and coalition discipline holds when we consider the differences in importance of the respective ministries.

The rest of the article is organized as follows: in the next section, I present the theoretical framework for the argument and propose a new indicator of portfolio importance. This is done to show how presidents distribute ministries, and to test the effects of the exact distribution of ministries on legislative support. Following on, the empirical data and methods are presented. Then the results, and lastly the conclusion.

Portfolio Allocation in Coalition Governments: Sharing Power, Building Support

The literature on portfolio allocation in parliamentary systems is extremely well developed, and can be divided into two approaches: demand-based and proposer-based models (Ansolabehere et al. 2005). Demand models are the ones that predict portfolio allocation proportionality based on Gamson's Law, while proposer ones identify the formateur's advantage (Rubinstein 1982; Baron and Ferejohn 1989). While formal models predict a disproportional gain by the formateur, empirical analyses show an impressive proportionality regarding portfolios and legislative seats, “one of the highest nontrivial r-squared figures in political science (0.93)” (Laver 1998: 4). This is considered the “portfolio allocation paradox” (Warwick and Druckman 2001, 2006).

One of the aspects that may help us to understand the process of coalition formation better, and to resolve this disconnect between formal models and empirical results, is the features that differentiate ministries – or portfolio salience. Ministries are not all alike, and that needs to be taken into consideration in proportionality and formateur advantage calculations. Beyond a whole body of literature that establishes government as composed of entirely homogenous parts, where the decision to be made is exclusively about the number of ministries that each party will control, these models identify differences between ministries – establishing that parties have different preferences for different ministries, thus affecting the aggregate gain of coalition partners (Laver and Hunt 1992; Warwick and Druckman 2001).

Regardless of the measure used, once the coalition is formed and portfolios have been allocated, legislative support for the government is taken as given until internal conflicts cause the deal to be renegotiated. This happens because “countries with parliamentary regimes are NOT governed by their parliaments, but by executive coalitions supported by Parliament” (Laver 2006: 6). Responsible party government is usually assumed, and since the cabinet is the decision-making locus, legislators need to stay loyal to the various parties if they wish to be a part of the government or to keep their own party in the coalition. Therefore, party discipline or the supporting of the government's agenda is not a fundamental issue – except when focusing on the amendment of bills (Martin and Vanberg 2011) or on the monitoring of coalition partners (Carroll and Cox 2012).

How do these questions over portfolio allocation and legislative support develop in presidential systems? Are these coalitions formed in the same way, obeying the same calculations, and generating the same outcomes? In presidential systems, the head of state and government is directly elected and has a fixed term. This has an important implication for coalition formation and governance: the president is always the formateur, and that status is defined exogenously with a pre-determined duration.

Since for Gamson (1961) proportionality in portfolio allocation is only observed if no participants have veto power or are otherwise mandatorily included in every possible coalition, proportional allocation is not to be expected. This is because “where one member has veto power, there is no alternative to his inclusion; he could no longer be expected to demand only a proportional share of the payoff’ (Gamson 1961: 377). For that reason, proportionality would not be observed in presidential systems and, according to this rule, this would furthermore not be a surprise – rather a direct effect of the institutional design of such regimes.

Portfolio allocation in presidential systems is centered on the president's strategy of not only building up legislative support but also of minimizing the risk of policy drift (Martínez-Gallardo and Schleiter 2014). This is because ministries are delegated to coalition partners, but the president still has final responsibility for the government. This concern with coalition governance is fundamental, since coalitions in fact govern – that is, they formulate policy, allocate the budget, and implement directives.

Another significant difference herein as compared to parliamentary systems is in the executive–legislative relationship, where both cabinet and parliament are important decision loci (Laver 2006). Also the responsible party government ideal, usually assumed in parliamentary systems, is not observed in presidential ones – particularly in Latin America. therefore, the generation of legislative support becomes more complex and variable according to the specific context. In this regard, coalition formation is only one of the possible explanations - with distributive politics being a viable alternative for the president in their endeavors to maintain governability in a context of parties that are not very programmatic and of legislators behaving individualistically.

Regarding coalition formation and the construction of legislative support, Amorim Neto (2000) shows that the more proportional a party's gain in the share of ministries, the higher the degree of its adherence to the executive's agenda in parliament. This demonstrates that the nominal status of coalition government alone does not solve all the issues with building legislative support in presidential systems. How the portfolio allocation is actually made and how exactly deals are struck are what truly matter.

An alternative option for building legislative support in presidential systems is distributing pork in individual vote negotiations (Ames 2003). The individualistic nature of political behavior, mainly a consequence of the electoral system, makes representatives receptive to this type of strategy given that particularistic spending is associated with better chances of electoral success (Pereira and Mueller 2004; Pereira and Rennó 2003). Legislative support is constructed in the day-to-day life of the executive- legislative relationship, without an accompanying institutionalized, long-term deal.

Raile, Pereira, and Power (2011) argue in favor of integrating both strategies – coalition formation and pork distribution – via what the authors call pork goods and coalition goods. These are imperfect substitutes: “Coalition goods establish an exchange baseline, while pork covers the ongoing costs of operation” (Raile, Pereira, and Power 2011: 324). The president would have a toolbox to deal with parties far from the responsible party government ideal observed in parliamentary systems, and to maintain governability in a highly fragmented context.

However, one question remains unanswered: What exactly are “coalition goods”? By opposing pork and coalition goods, the authors – even if implicitly – associate the latter with a more ideological concern and the former with an electoral interest among the representatives. Nonetheless we still know little about what precisely the ministries, which represent the operationalization of these coalition goods, offer to the parties that comprise the coalition. That is, we know little about what assets each ministry offers, how these benefits are distributed among coalition partners, and how this specific carving up affects legislative support from these partners in parliament.

The ministries represent access to the policy-formulation process in the executive. There is a specialization in issues within each ministry, such that who controls the ministry oversees also a sizeable number of decisions. Normally, who actually runs these organizations has agendasetting power in policy propositions – or at least is consulted in their formulation. Ministries are also responsible for implementing policies and for budget allocation. Thus they may perform several roles in the executive's decision-making processes, from policy formulation to the allocation of distributive policies, including appointments in the administration. Because of this, I propose here an integrated approach to these topics – one in which coalition goods, or ministries, are valued by the assets that they control. Parties look to integrate the government so as to have access to the benefits that a ministry may offer in influence over policy, political appointments, and budget distribution. I thus analyze systematically which specific assets each ministry controls, to map how presidents distribute ministries and how the exact apportioning of these affects the coalition's subsequent legislative support.

The first step here is to establish that ministries are not all alike; that is, they control different assets that can have varying appeals. If ministries are not entirely homogenous, then the parties’ gain is different according to which particular ones it is that they control. The second step then becomes constructing a measure of importance capable of simultaneously capturing the different relevant aspects, objectively and systematically, so that results can be tested and potentially replicated in other contexts elsewhere too.

The matter of differences between ministries has already been reasonably explored in parliamentary systems, in the form of salience measures. These yardsticks of portfolio salience usually take the form of expert surveys, asking questions about the exact value of different cabinet positions (Laver and Hunt 1992; Warwick and Druckman 2001, 2005). These measures have been very useful for testing hypotheses about coalition formation and governance. However, they have also revealed a number of limitations. First, these are expert surveys – and the respondent's judgment may be contaminated by the portfolio-allocation process itself (Browne and Feste 1975; Bucur 2018). Second, these surveys ask very generic questions about the value ascribed to a specific ministry, and thus do not explain why these ministries are valued differently or indeed the variety of reasons why a particular ministry might be important.

Concerning presidential systems, portfolio salience is a matter of discussion and certain a priori classifications. Abranches (1988) argues that ministries do not have the same political worth, and may be differentiated into coordination ministries and clientele or spending ministries. For Amorim Neto (2000), in the real world of politics not all ministries are alike. Moving on to the classifications provided for empirical tests, Escobar-Lemmon and Taylor-Robinson (2005) identify ministries as having high, 2 medium, 3 and low 4 prestige. The same authors (2009), analyzing the career paths of female ministers, also offer a classification based on the issue area dealt with. They thus demarcate ministries into “feminine policy domain” 5 and “masculine policy domain.” 6

Defense and Public Security, Finance and Economy, Foreign Affairs, and Government/ Interior.

Agriculture, Fisheries, and Livestock, Construction and Public Works, Education, Environment and Natural Resources, Health and Social Welfare, Industry and Commerce, Justice, Labor, Transportation, Communications, Information, and Planning and Development.

Children and Family, Culture, Reform of State, Temporary and Transient Ministries, Science and Technology, Sports, Tourism, and Women's Affairs.

Children and Family, Culture, Education, Health and Social Welfare, and Women's Affairs.

Agriculture, Fisheries, and Livestock, Construction and Public Works, Defense and Public Security, Finance and Economy, Foreign Affairs, Government/Interior, Industry and Commerce, Labor, Science and Technology, Transportation, Communications, Information, Environment and Natural Resources, Justice, Planning, Sports, and Tourism.

Analyzing coalition governance, Martínez-Gallardo and Schleiter (2014) establish a subgroup of “core portfolios” as the ones central to the government's sound functioning. Explaining ministerial turnover, Camerlo and Perez-Linan (2015), meanwhile, classify ministries into categories of “policy” (ministers in charge of macroeconomic management and specific policy areas such as education, health, and labor), “politics” (ministries engaged in domestic politics such as the Ministry of the Interior and the Ministry of the Presidency), and “external” (ministries engaged in international issues such as foreign affairs and defense). Even though researchers usually agree that cabinet positions are not all alike and present some a priori classifications for them, to the best of my knowledge there have been no attempts to date to measure portfolio salience systematically and objectively within presidential systems. I propose such a measure now being undertaken, that based on observable indicators.

Such indicators are useful for two reasons: First, they are objective, transparent, comparable across time, and replicable in different contexts. Second, objective indicators show that ministries can be important for varying reasons when compared across different dimensions. To describe the difference in importance between ministries, I explore the three core drivers that motivate political actors vying for electoral success: influence over policy, political appointments, and budget allocation respectively.

The choice of these variables is loosely guided by the argument that political parties facing hard choices make decisions, as noted earlier, based on three primary considerations: policy, office, and votes (Strøm and Müller 1999). I argue that political actors will consider these three factors when facing a decision about which ministries to control, and that these drivers can be translated as in effect being the different assets that a ministry holds. The policy driver can be seen as having influence over the policy-formulation process, precisely through participation in the drafting of policy initiatives in the executive. The office driver can be seen as control over political appointments, which can be used to award political allies and also as patronage. Last, the votes driver can be seen as having control of a large budget, which can be used to target voters in personalistic elections - such as the ones held with an open-list proportional representation rule.

With these measures of portfolio importance in hand, it will be possible to provide more precise answers to certain fundamental questions related to portfolio allocation. I argue that the president takes into consideration the governance implications of this portfolio allocation. These ramifications underpin both the construction of legislative support and also the risk of policy drift. Both the president and coalition partners seek influence over governmental decisions. However, the institutional design of presidential systems makes the incentives for the president and coalition partners differ. The president is the only representative elected in a national district. Also, the personalization of politics in presidential systems makes the president identifiable as the responsible person for national politics as well as for national-level outcomes. Despite the multipartisan nature of coalition governments, in presidential systems the president will remain the primary responsible individual for governmental decisions. For this reason, the president will have incentives to concentrate a disproportionate share of ministries within their party, appointing co-partisan ministers, as a way to keep decisions under control.

This effect is especially acute when we consider the most important ministries concerning policy formulation.

From coalition partners’ point of view, they are not directly responsible for governmental decisions since there is no binding agreement in government formation in presidential systems similar to the ones celebrated in parliamentary systems. Considering that coalition partners might find it challenging to claim credit for national policy, and taking into account also the incentives of an electoral system that brings to power legislators with an open-list proportional mode of rule, we can expect that coalition partners will be more interested in distributive policies. This would happen because coalition partners can now claim credit for policies with a concentrated geographical impact that can furthermore be attributed to a coalition partner, and not to either the government as a whole or to the president individually. The reasoning behind this argument is the same as that presented in the literature on distributive politics within legislatures.

I revisit the traditional argument on the proportionality rule (Gam- son 1961; Amorim Neto 2006) by proposing that presidents will have incentives to allocate a disproportionate share of ministries to loyal ministers. This will be expressed in the mode of a “formateur advantage.” However, considering that these ministries are not all alike, I expect that this concentration will be more pronounced when the policy relevance of the ministries is considered. On the other side, we expect that the president will reward coalition partners with the ministries that they are more directly interested in – namely the more important ones concerning the budget dimension, since these resources can be used to gain electoral advantages. From all of this I formulate the following hypotheses:

Presidents will allocate the largest share of portfolios to co-partisan ministers as compared to coalition partners.

The effect of co-partisanship will be greater considering the policy-weighted share of portfolios.

The effect of co-partisanship will be smaller considering the budget-weighted share of portfolios.

These hypotheses concern the who gets what question, and show how the specific assets that a ministry controls are relevant to the portfolio- allocation game. However, coalition politics in presidential systems do not end with portfolio allocation. Because of the separation of powers, coalition parties have enough autonomy in the legislative arena to react to these deals made in the executive. For this reason, I revisit the debate on the relationship between portfolio allocation and coalition partners’ legislative support.

The expected positive effect of portfolio allocation on legislative support has long been established, and indeed empirically tested (Amorim Neto 2000). The larger the gain, the greater the legislative support. However, this empirical association, despite its consistency, is perpetually accompanied by an important question: What would happen to the results if the differences between ministries were considered? It is expected, even considering the different facets controlled by the ministries, that the greater the share of portfolios controlled by the party, the larger the subsequent payback – in the form of legislative support for the president's agenda. This hypothesis means that the coalition agreement works with both sides on delivering what was promised.

The larger the weighted share of portfolios, the greater the legislative support for the president's agenda.

However, it is also expected that the different dimensions of portfolio importance will matter in the calculations. I anticipate that the effect of portfolio allocation on legislative support will be larger when the portfolio share is weighted by its budgetary importance. This follows the reasoning that when coalition partners control ministries with significant participation in the federal budget, they would be able to extract rents from government participation and would reciprocate by supporting the president's legislative agenda. This hypothesis is meant to compare the effect of different assets’ distribution on coalition support.

The effect of the budget-weighted share of portfolios on legislative support for the president's agenda is greater than the other dimensions’ effects.

Technically, H1 and H4 mean a simple effect. H2, H3, and H5 are pertinent in comparing the difference between coefficients of the policy, office, and budget dimensions of portfolio importance. I also consider as relevant certain factors that explain legislative behavior: ideological proximity, the electoral cycle, the term of office, and the president's popularity. It is expected that the greater the ideological distance between the coalition party and the president, the weaker the support for the president's agenda. Also, the closer to the end of the term it is, the less support there will be for the president's agenda; and, when the president is in their second term, there will also be weaker support for their agenda. Finally, the higher the popularity of the president, the greater the legislative support that they enjoy. The next section presents a specific case study, the relevant data, and the research techniques used.

Case, Data, and Methods

To test the five introduced hypotheses, I propose the analysis of a particular case study. I believe that such a study is an important first step toward addressing as yet unexplored questions, prioritizing their validity – considering that data limitations may thwart the validating of new hypotheses, and the constructions of new empirical measures from a comparative perspective.

The article's goal is to build further knowledge on political systems characterized by multiparty presidentialism. In the Latin American context, presidential systems vary greatly when it comes to multiparty government formation. In Brazil, Chile, and Colombia all cabinets have hitherto been multiparty ones. For an article that explores portfolio allocation in a multiparty context, an extended period of coalition governments’ rule and variability in the composition of these are desirable characteristics. For these reasons, Brazil, Chile, and Colombia would be the natural candidates for a case study. Among these three cases, from a theoretical standpoint, the Brazilian one may be considered extreme (Seawright and Gerring 2008). Coalitions in Brazil have an average of 7.5 parties, a figure much higher than the ones observed in Chile (4.00) and Colombia (4.00) respectively (Freudenreich 2016). On this basis, Brazil was chosen as the case study as a way of exploring this pronounced variability in coalition formation.

The period analyzed is 1999–2014. These years encompass the administration of three separate presidents and four terms, including heads of state from distinclty different ideological leanings. The article, as noted, addresses the two research questions of who gets what and how does it matter. For this reason, there are two sets of dependent variables and accompanying analysis here.

To answer the question of who gets what, the dependent variables are the distribution of ministries weighted by three yardsticks of importance. I measure the significance of the ministries with the following variables then: policy, office, and budget. The policy dimension is seen as the ministry's participation in the formulation of the executive's legislative agenda, measured as the number of legislative initiatives authored by the ministry in question in a particular year. The office dimension is identified as the number of positions to be filled by appointment, in Brazil referred to as High-level Management and Advising (Direção e Assessoramento Superiores, DAS), within the ministry in a particular year. The source for this data is the Ministry of Planning. The budget dimension is taken as the ministry's total budget as well as also their investment budget for the year. The latter is included because it is the part of the budget that is used for distributive politics. The data for this is taken from the Financial Administration Integrated System (Sistema Integrado de Administração Financeira, SIAFI).

An important question concerning these variables is whether they are attributes of the ministry itself or rather only of specific ministers. I argue that these are in fact structural facets of the ministry, and not completely subject to the variation ensuing from the particular minister currently appointed to the job. To explain this point using concrete examples, I would contend that the Ministries of Planning, Finance, and justice are structurally important policywise. These are coordination ministries that are thus not relevant to budget allocation. This structural component states that these ministries will not suddenly become irrelevant in the policy dimension because of a change of minister at the helm.

The logic is that the president observes the a priori characteristics of the ministry and then appoints a minister according to the needs of the job, and not the other way around. To use another example, the Ministries of Local Affairs and National Integration are budget-relevant ones and not especially important with regard to policy formulation; this will not change with the appointing of a different head minister. Empirically, this can be seen by observing the confidence intervals of the respective measures. These do not vary that much, showing that even though there is a lot of ministerial turnover the importance of the bodies themselves remains relatively stable. 7

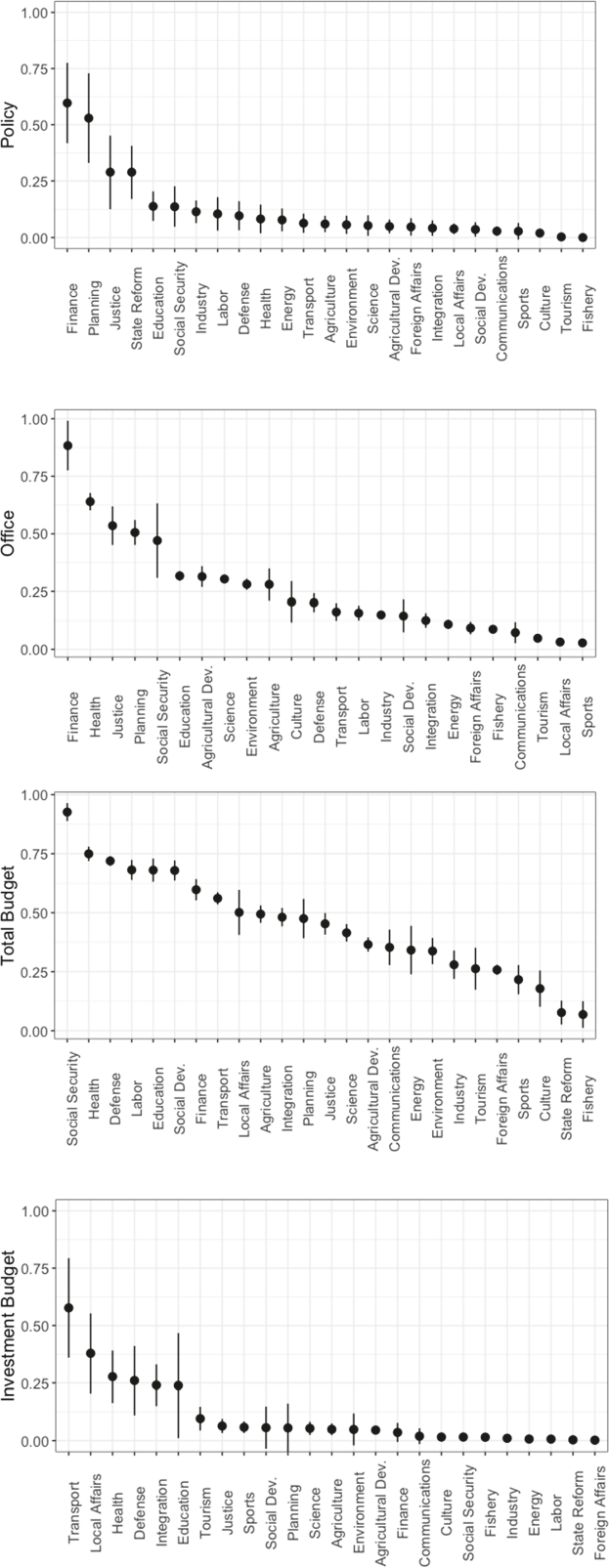

Means and confidence intervals for the policy, office, and budget measures can be seen in Figure 1 below.

Portfolio Importance: Policy, Office, and Budget Dimensions (1995–2014)

The goal here is to explore the relative gains of different coalition parties, when considering the importance of the ministries across different dimensions. To do this, I present separate regression models - each one with a measure of portfolio share weighted by importance. However ministries control policy, office, and budget assets simultaneously, while they are each analyzed separately here. To take into consideration this compositional nature of the data, I use a seemingly unrelated regression system. This approach is a particularly appropriate one when considering sets of dependent variables that show a contemporaneous correlation of errors, such as the importance-weighted portfolio shares used here (Philips, Rutherford, and Whitten 2016). The system solves this problem by assuming that the error terms are correlated across the different equations. 8

I present the simple OLS models in the Appendix.

The core idea behind this is that the president will concentrate the largest share of portfolios within their party, by appointing co-partisan ministers (in this article I consider nonpartisans as co-partisans of the president, since these ministers are expected to be loyal to the president). Also, I expect that this effect will be larger when we consider portfolio share weighted by policy importance. On the other hand, I anticipate that this effect will be smaller when considering the portfolio share as weighted by its budgetary importance. Summing up, the president will keep control of the largest share of portfolios but will be more willing to share the budget-important ministries with coalition partners. In these models, the status of being a member of the president's party or of being counted as other coalition partners is used as the leading independent variable. I also include the legislative seat share of the coalition parties as a predictor of portfolio share in the various models. Data comes from the Chamber of Deputies website.

For the second research question, how does it matter, my hypotheses concern the effects of portfolio allocation on coalition discipline when considering these different attributes. For this reason, the measures of portfolio share become the leading independent variables here. The dependent variable is measured as the coalition parties’ adherence to the stipulations of the government's leader in the Chamber of Deputies. Legislators cast their votes in roll calls. They are considered aligned with the government when they vote according to the position indicated by the government leader himself/herself. Party discipline is thus the aggregation of these individual votes in the form of a discipline rate. The data is observed by party and year, and the source for it is the Cebrap's Legislative Database (Figueiredo and Limongi 2001).

The analyses are divided into three parts: first, I describe each ministry's measure of importance, and then present their exact distribution among the coalition parties – thereby answering the who gets what question. Then, second, I utilize the importance measures as independent variables, analyzing their effect on the coalition's discipline. As control variables, I include the electoral cycle (number of years until the next election), the term of office (zero for the first term and one for the second), popularity, and ideology. Ideology is measured with data taken from a survey with legislators presented by Power and Zucco (2009). Popularity is measured as the mean yearly approval of the president (percentage of positive ratings); data for this comes from Carlin et al. (2016).

Results

First, I outline the relative importance of ministries in Brazil accordingly to the policy, office, and budget dimensions introduced earlier. Then, I present how presidents allocate portfolios regarding their importance; in other words, who gets what in coalition governments. The point of this is to compare portfolio share by party status, whether from the president's party or alternatively other coalition partners, and also by seat share in the lower chamber. I then proceed to the testing of hypotheses. I initially examine the effect of the importance-weighted share of portfolios on coalition discipline, then test the moderating effect of that portfolio share on the impact of ideological distance on coalition discipline, and lastly scrutinize the difference in effect size between various specifications of importance weight.

Portfolio Importance

Are ministries all alike? To answer this question, I present the distribution of Brazilian ministries according to the policy, office, and budget indicators. The analysis below only includes cabinet ministries, thus not considering special secretariats located within the presidency. The decision to exclude such secretariats comes from the fact that most of these bodies do not have their own budget or personnel, and for this reason are not directly comparable to cabinet ministries. Another justification for this choice is that some of these bodies have very specific attributions, such as handling the president's communications, acting as the secret service, or overseeing institutional relations – for these reasons, they lie outside the scope of this article. Analyzing the whole period of 1999–2014, I present data on 25 different ministries. Figure 1 below presents the distribution of Brazilian ministries according to each of the variables discussed: policy, office, total budget, and investment budget.

The points are the averages for 1999–2014 and the bars, the standard deviations. 9

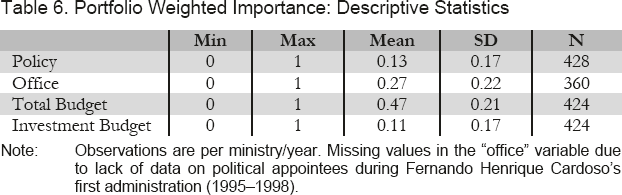

All variables were normalized to vary from zero to one, so as to make the comparison of the results easier. Table 6 in the Appendix shows the descriptive statistics.

In the policy dimension, the Ministries of Finance, Planning, and justice are the most important ones, while least important are the Ministries of Fishery, Tourism, and Culture. The distribution of the most important ones in this dimension shows the so-called political coordination ministries, and they are usually considered the government's core. In the office dimension, meanwhile, the order slightly alters, with the most important ones being the Ministries of Finance, Health, and Justice, while least important are the Ministries of Sports, Cities, and Tourism.

Regarding total budget, most important are the Ministries of Social Security, Health, and Defense. These ministries usually control resources that are termed rigid; that is, over which political actors do not have the political leeway to decide on their allocation. The least important with regard to this indicator are once again the Ministries of Fishery, State Reform (during its brief existence), and Culture. Still in the budget dimension, but now regarding control over the investment budget (which corresponds to the discretionary part of the budget, and where geographically concentrated expenditure originates from such sources as voluntary transfers and parliamentary amendments), most important are the Ministries of Transport, Cities, and Health and least so the Ministries of Foreign Affairs, State Reform, and Labor. Two out of the three most important ministries in this dimension are ones that typically do not grab our attention and that would not be considered relevant a priori. Nonetheless they are ministries that are highly valued by parties interested in controlling funds that can be allocated for electoral purposes.

Comparing the different dimensions, we see that particular ministries can be more or less important across them. However, something to be noted is that the standard deviations are not large within the given timeframe. This may be interpreted as homogeneity or consistency of ministry importance over time, and across different governments. 10 Given the ministries’ distribution presented in Figure 1, we can notice that their importance varies significantly – corroborating the preliminary assumption that ministries are not all alike. Table 1 presents the correlation matrix between the respective importance indicators.

Correlation Matrix: Importance Indicators

Note: These are Pearson correlation coefficients.

p-value <0.01,

p-value <0.05.

Note that this indicates that portfolio allocation is not completely endogenous to the government's preferences or indeed ministry-led, since it does not vary greatly over time.

Table 1 shows that the correlation between the different indicators of portfolio importance are not all as high as expected, when ministries are all homogenous parts of the cabinet. The highest correlations are between policy and office (0.643, p-value<0.01) and between office and total budget (0.437, p-value<0.01). The correlation between total budget and policy is low (0.179, p-value<0.01), and between policy and investment budget actually negative (-0.138, p-value<0.05). The correlation between office and investment budget is not statistically significant (-0.05) meanwhile. These results indicate that portfolios control different assets, and are important for varying reasons. This is why this information must be taken into consideration in portfolio allocation analyses of who gets what in the Brazilian political system of coalition presidentialism.

Who Gets What?

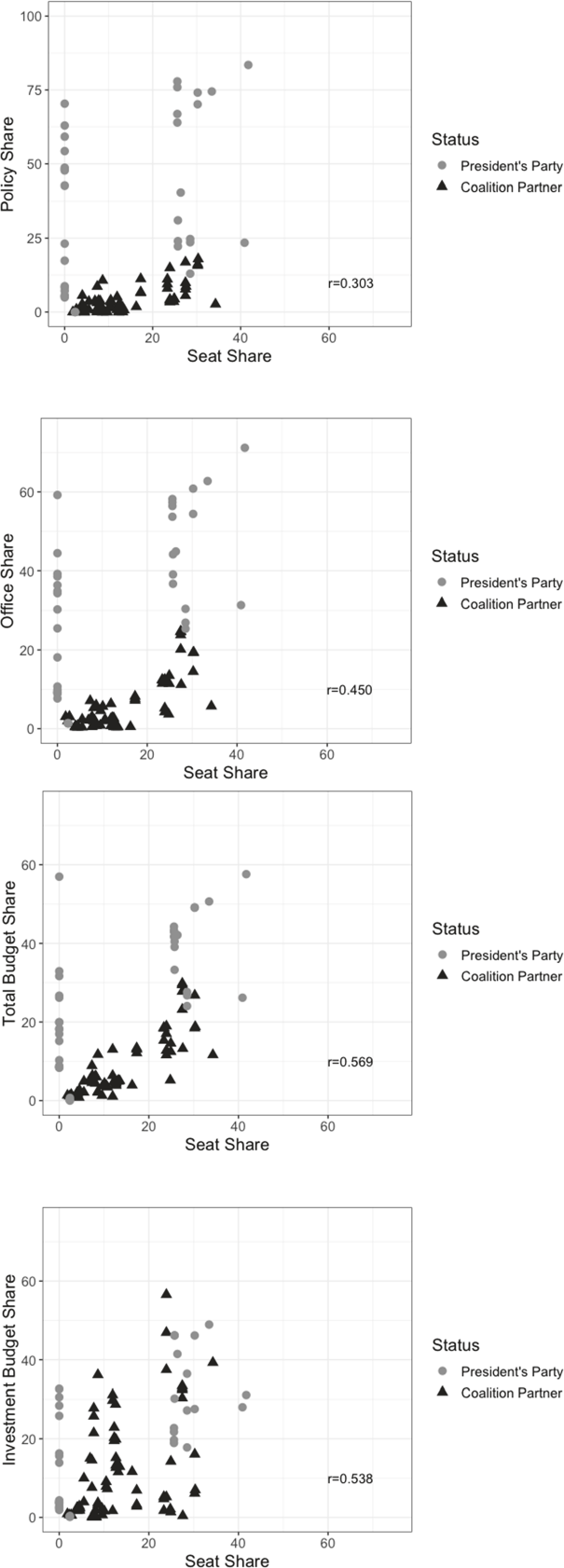

Figure 2 presents the relationship between the proportion of ministries and that of seats in the legislative, comparing the gain of the president's party with that of the remaining parties in the coalition across each of the dimensions of portfolio importance. In this analysis, I consider nonpartisan ministers as being from the president's party – since their loyalty is to the head of state. I first present the policy dimension, then the office one, and following on both respective indicators for the budget dimension. Each point in the graph indicates a party–year observation.

Portfolio Allocation and Seat Share: Policy, Office, and Budget Indicators

The president's party is overcompensated for in three out of the four indicators presented in the graphs above. That is, the president's party receives a disproportional gain in relation to its size in the legislative when considering the proportion of ministries as weighted by their importance in the policy, office, and total budget dimensions. Only in investment budget is distribution more equitable. The concentration of ministries within the president's party is particularly strong regarding the policy dimension, where the president controls almost all legislative formulation through their own party – sharing very little with the rest of the coalition partners.

Thus, when one considers the distribution of ministries weighted by the assets controlled, the government may be a coalition government but the effect of presidentialism is evident in the separating out of the president's party from the other ones in the coalition per their differentiated statuses. Another critical aspect in the distribution of ministries is the allocation of a significant proportion of them to nonpartisan ministers. This can be noticed in the distribution of ministers having zero proportion of seats in the legislative.

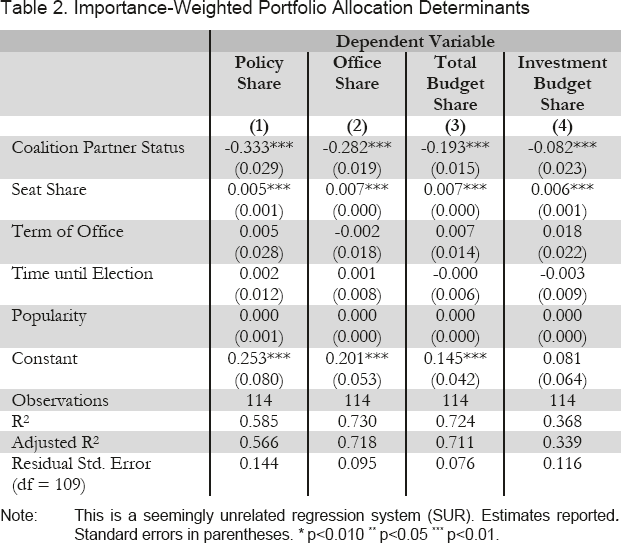

Analyzing the allocation of ministries weighted by the different dimensions suggests the following core pattern: the president concentrates the ministries that formulate policies within their own party, while more equitably distributing among the remaining coalition partners the ones that are stronger concerning budget allocation. This pattern may be explainable by the various incentives that exist for both the president and for coalition partners. Regarding the president, the goal is to minimize the risk of policy drift – thus concentrating government coordination and policy formulation within their party. From the coalition partners’ point of view, meanwhile, they can more easily claim credit for geographically targeted policies than for more diffuse governmental ones that would be directly attributable to the president himself/herself. To illustrate this pattern more clearly, Table 2 shows the regression models with each of the portfolio shares as dependent variables, and the status and seat share as the main independent ones. Regressions are linear models in a seemingly unrelated regression system. 11

Importance-Weighted Portfolio Allocation Determinants

Note: This is a seemingly unrelated regression system (SUR). Estimates reported. Standard errors in parentheses.

p<0.010

p<0.05

p<0.01.

Systemfit command of the “systemfit” R package.

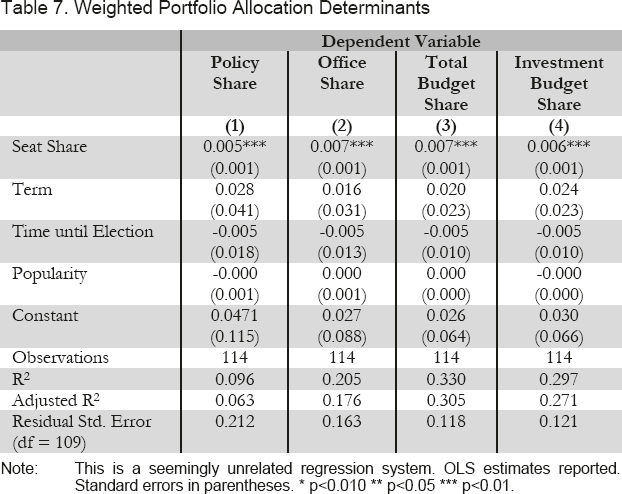

Table 2 reveals that no matter the specification of the dependent variable – meaning regardless of the specific weights applied, whether policy, office, total budget, or investment budget – coalition partners always receive a smaller share in portfolio allocation. This means that the president always prioritizes their own party therein, appointing mainly co-partisans to control ministries. In sum, coalition governments imply some power-sharing – but in presidential systems this power-sharing is done while a difference in status between the president's party and the other coalition partners still remains however. Notice that this result is observed even when keeping the legislative seat share constant. This means that the parties comprising the coalition are not treated indiscriminately. In theory, coalition parties should be compensated in direct relationship to their contribution to the coalition concerning seat share. However, in the eyes of the president, coalition parties are not all equal – and so co-partisan ministers are prioritized. To demonstrate that coalition partner status is the primary predictor, I give in the Appendix the same regression models but with this specific variable removed (Table 7). The variable of legislative seat share keeps its direction and significance, but the R 2 are significantly reduced: from 0.566 to 0.063 in the policy- weighted, from 0.718 to 0.176 in the office-weighted, from 0.11 to 0.305 in the total budget-weighted, and from 0.339 to 0.271 in the investment budget-weighted share.

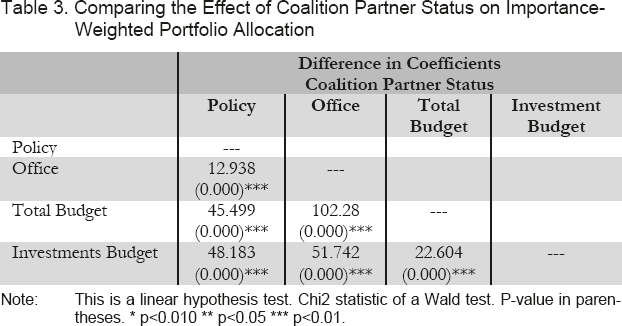

The results in Table 2 present evidence in support of H1, which states that presidents will allocate the largest share of portfolios to co-partisan ministers compared to coalition partners. However, to provide a formal test of H2 and H3 respectively, we have to compare the magnitude of the coefficients provided in Table 2. In the comparison of the absolute numbers, the effect of coalition partner status is the largest in the policy-weighted share (-0.333) and the smallest in the total budget-weighted (-0.193) and the investment budget-weighted (-0.082) ones. This provides evidence for the five hypotheses being true, since it was expected that the effect would be greater in the policy-weighted share of portfolios and smaller in the budget-weighted ones. However, to formally test these hypotheses, a significance test of the difference between coefficients is provided. 12

Linear hypothesis test of difference between coefficients. Linear-hypothesis command in the “car” R package.

Table 3 provides the significance tests, and furthermore shows that the differences in the magnitude of the effect observed in Table 2 are statistically significant. This means that, in fact, the effect of coalition partner status is larger in the policy-weighted share and smaller in the two budget-weighted ones. In sum, the president appoints co-partisans to the ministries most important to the government's own policy formulation. The Ministries of Finance, Planning, and justice will almost always be headed by a loyal minister, and are very unlikely to go to a coalition partner. This means that the president takes into consideration the importance of the ministry in question when deciding whom to delegate these powers to.

Comparing the Effect of Coalition Partner Status on Importance-Weiqhted Portfolio Allocation

Note: This is a linear hypothesis test. Chi2 statistic of a Wald test. P-value in parentheses.

p<0.010

** p<0.05

p<0.01.

Moving on to the budget indicators, we can see the increased participation of coalition partners – since the effect of coalition partner status is the smallest in these specifications. This indicates that, when deciding who gets what, the president usually shares the ministries that are most important concerning the budget dimension more equally with coalition partners. Summing up, the president always retains the largest share of portfolios, appointing co-partisan ministers. However this concentration is significantly smaller when we consider the budget-weighted portfolio shares.

This shows that portfolios are not all alike, and are furthermore not distributed among coalition partners equally. There is a clear division of labor, where the president keeps the policy-relevant ministries and shares the budget-relevant ones with coalition partners. Given this specific pattern of portfolio allocation, how do these circumstances affect legislative support for the president's agenda in Congress? That is, how does this precise distribution of ministries – considering the different assets controlled – affect the legislative behavior of the coalition's constitutive parties within the parliamentary arena?

The Power-Sharing Hypothesis: Party-Level Support

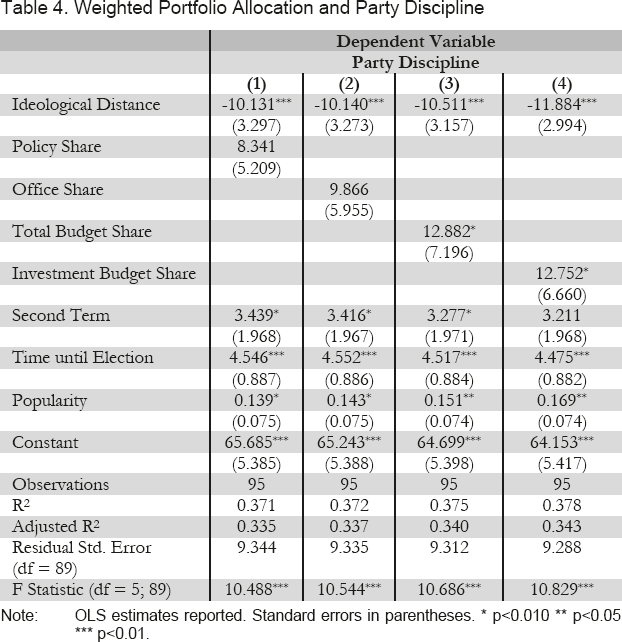

Table 4 presents the results of the effect of portfolio allocation on coalition discipline. The effect analyzed here is the size of the gain for each party weighted by the importance of the ministries. The results of the models show the positive relationship between portfolio share and coalition discipline. That is, in general, the larger the gain in the executive, the greater the support in the legislative arena. This result provides evidence in favor of H4, as well as the argument presented in the literature that portfolio allocation to coalition partners would be a way to “cement” the power-sharing deal and to establish legislative support for the president's agenda.

Weighted Portfolio Allocation and Party Discipline

Note: OLS estimates reported. Standard errors in parentheses.

p<0.010

p<0.05

p<0.01.

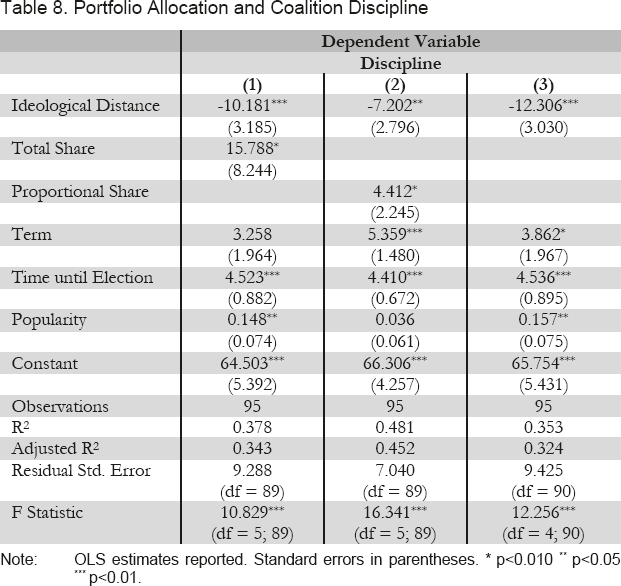

However this result is only statically significant when we consider the budget-weighted portfolio shares (Table 4, models 3 and 4), and even in these models the effect is significant only at the 10 percent level. This means that even though the relationship remains positive in all models, the positive relationship between portfolio share and party discipline might be mainly driven only by the distribution of budget-important ministries. The reduced level of significance, and the fact that two of the specifications do not show statistical significance, could be an indication of a measurement error or of some other problem – considering that the strong and positive relationship between portfolio share and legislative discipline is posited to be very stable in the literature. To demonstrate that this is not the case, Table 8 in the Appendix shows the effect of the simple measure of portfolio share (considering only the number of portfolios allocated) and also includes a measure considering proportionality in allocation (portfolio share as related to seat share). The results show that the significance remains at the 10 percent level.

These results perhaps indicate that the effect of portfolio share on legislative discipline is smaller and more unstable than usually believed. Also, they may show that another factor could be more important to explaining legislative discipline – in this case, ideological distance. Table 4 shows that the effect of ideological distance is negative, strong, and stable across different specifications. For this reason, I argue that portfolio allocation might be a secondary explanation for legislative support. To demonstrate this point, model 3 in Table 8 in the Appendix shows that the R 2 is not notably reduced when we remove portfolio share – meaning that this factor has only a limited effect on coalition discipline. Regarding the remaining variables included in the model, the president's popularity increases legislative support. For the time until the next election variable, the greater it is, the more extensive the coalition's support. Counterintuitively, party discipline was demonstrated to be stronger in the president's second term.

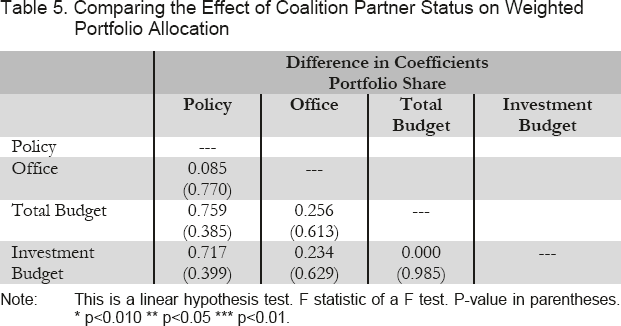

The results presented in Table 4 may suggest evidence for H5 being true, since the effect of portfolio share is significant only when we consider the budget-weighted ones. Also speaking in favor of H5 is that the R 2 of models 3 and 4 in Table 4 are the largest. However, the difference is only small. To formally test if there is a statistically significant difference between the coefficients, I implement the same linear hypothesis test between coefficients as presented above. Results are given in Table 5.

Comparing the Effect of Coalition Partner Status on Weighted Portfolio Allocation

Note: This is a linear hypothesis test. F statistic of a F test. P-value in parentheses.

p<0.010

p<0.05

p<0.01.

H5 states that the effect of the budget-weighted shares on legislative support is larger compared to the other effects. This happens because coalition partners are more interested in affecting distributive policies, and reciprocate for the influence over valuable resources in the legislative arena. However the comparison of coefficients does not show statistically significant differences, indicating that all effect variations are indistinguishable from zero. This means that the effect sizes are consistent, and can be considered the same across different specifications of the weighting of portfolio share. This result is a direct refutation of H5, showing that the greater the gain, the larger the support - and also that the effect size is the same across different types of gain.

The nonsignificant results present evidence that coalition parties do not react differently in the legislative arena on the basis of the specific assets controlled in the executive. The explanation for this result might be that coalition partners may be acquiring different assets in the executive.

However, once in the cabinet, coalition partners provide reasonable legislative support to the government. Sharing power does indeed build support. This result should not mean that coalition partners are office- seekers and exclusively motivated solely by getting into the cabinet. Taken together, the results presented here emphasize that preferences matter. For this reason, the president takes into consideration whom to appoint to important ministries; coalition partners, meanwhile, are also influenced by the ideological distance from the president and not solely by portfolio share.

Conclusion

I explored here the question of portfolio allocation in coalition presidentialism, focusing mainly on the as yet unsolved problem of the differences between ministries. Whether in the literature on coalition governments within parliamentary systems or adapted to the specific context of presidentialism, the debate always ends up coming back to the issue that not all ministries are alike. How, for example, does one compare the Ministry of Finance to the Ministry of Sports?

In many situations, ministries are so different in their attributes, prerogatives, and powers that their direct comparison makes no sense. There is debate about classifying ministries into political coordination and clientele ones respectively (Abranches 1988), and into more important ministries – or “core portfolios” (Martínez-Gallardo and Schleiter 2014). However these classifications usually respond to only intuitive or unsystematic criteria. If we do not know objectively how ministries are to be differentiated, how is it possible to understand portfolio allocation strategies implemented by the president or moreover to comprehend the effects that the specific allocations of these has on the behavior of the parties comprising the coalition?

This article has attempted to bring some fresh answers to these longstanding questions, presenting an original measure of portfolio importance based on three objective dimensions of the specific assets controlled: policy, office, and budget. Weighting the proportion of ministries allocated to coalition parties with these measures of importance, I have strived here to answer two interrelated questions: who gets what, or how does the president allocate ministries, and how does this matter, or what is the effect of the proportionalities in ministry distribution on coalition partners’ subsequent legislative support?

The results indicate that ministries are distinctly different, and that importance varies according to the specific dimension being evaluated.

That is, what is an essential ministry in policy formulation may not be the most important one in budget allocation meanwhile. This result highlights the relevance of asking not only how the ministries differ, but also according to which criteria exactly or in which specific dimension they do so. This is because an asset valued by one party may not be what is esteemed by another.

The results indicate that the president prioritizes their party when distributing ministries. The presented evidence has shown that the president allocates the largest share of portfolios to co-partisan ministers in all four specifications of the importance-weighted measures – policy, office, total budget, and investment budget. However the comparison of the specific attributes of the ministries and the effect of co-partisanship on portfolio allocation across different dimensions of importance has revealed that the president primarily concentrates on the ministries deemed most crucial when considering the issue of policy relevance, and is more willing to hand over the budget-relevant ones meanwhile. For this reason it can be concluded that power-sharing is limited within presidential systems, with the president's party keeping control over the most important ministries concerning policy formulation and building a coalition by sharing the budget-important ones with coalition partners.

The findings here also divulge that the larger the gain in the executive when it comes to the proportion of ministries controlled, the greater coalition partners’ legislative support. This result is consistent across all specifications of the gain made in the executive. However this effect is only statistically significant when considering the budget-weighted share. Nevertheless, when comparing the different importance-weighted shares, the results do not show variation between respective gains. This means that when it comes to coalition discipline, the effect on legislative support stays the same.

Taken together, the answers uncovered to the two research questions may be evidence of a possible coalition presidentialism dilemma. This is because at the portfolio-allocation stage of the game, the president takes into consideration the risk of policy drift and thus apportions more ministries to their co-partisans. However, when analyzing the explanatory factors for legislative support from coalition partners, it was found that portfolio allocation serves as an instrument to induce such support – even if only limitedly so. Consequently, while the president has incentives to concentrate ministries with close partners, that strategy may have negative effects on the legislative stage of the game – as the parties receiving little reward begin to vote against the government's various positions. There is a fine balance that the president must strike to make coalition presidentialism work: allocating ministries in a way that builds legislative support while at the same time minimizing the risk of being undermined by their coalition partners.

Footnotes

Appendix

Portfolio Weighted Importance: Descriptive Statistics Note: Observations are per ministry/year. Missing values in the “office” variable due to lack of data on political appointees during Fernando Henrique Cardoso's first administration (1995–1998). Weighted Portfolio Allocation Determinants Note: This is a seemingly unrelated regression system. OLS estimates reported. Standard errors in parentheses. p<0.010 p<0.05 p<0.01. Portfolio Allocation and Coalition Discipline Note: OLS estimates reported. Standard errors in parentheses. p<0.010 p<0.05 p<0.01.

Min

Max

Mean

SD

N

Policy

0

1

0.13

0.17

428

Office

0

1

0.27

0.22

360

Total Budget

0

1

0.47

0.21

424

Investment Budget

0

1

0.11

0.17

424

Dependent Variable

Policy Share

Office Share

Total Budget Share

Investment Budget Share

(1)

(2)

(3)

(4)

Seat Share

0.005

***

(0.001)

0.007

***

(0.001)

0.007

***

(0.001)

0.006

***

(0.001)

Term

0.028 (0.041)

0.016 (0.031)

0.020 (0.023)

0.024 (0.023)

Time until Election

-0.005 (0.018)

-0.005 (0.013)

-0.005 (0.010)

-0.005 (0.010)

Popularity

-0.000 (0.001)

0.000 (0.001)

0.000 (0.000)

-0.000 (0.000)

Constant

0.0471 (0.115)

0.027 (0.088)

0.026 (0.064)

0.030 (0.066)

Observations

114

114

114

114

R2

0.096

0.205

0.330

0.297

Adjusted R2

0.063

0.176

0.305

0.271

Residual Std. Error (df = 109)

0.212

0.163

0.118

0.121

Dependent Variable

Discipline

(1)

(2)

(3)

Ideological Distance

-10.181

***

-7.202

**

-12.306

***

(3.185)

(2.796)

(3.030)

Total Share

15.788

*

(8.244)

Proportional Share

4.412

*

(2.245)

Term

3.258

5.359

***

3.862

*

(1.964)

(1.480)

(1.967)

Time until Election

4.523

***

4.410

***

4.536

***

(0.882)

(0.672)

(0.895)

Popularity

0.148

**

0.036

0.157

**

(0.074)

(0.061)

(0.075)

Constant

64.503

***

66.306

***

65.754

***

(5.392)

(4.257)

(5.431)

Observations

95

95

95

R2

0.378

0.481

0.353

Adjusted R2

0.343

0.452

0.324

Residual Std. Error

9.288 (df = 89)

7.040 (df = 89)

9.425 (df = 90)

F Statistic

10.829

***

(df = 5; 89)

16.341

***

(df = 5; 89)

12.256

***

(df = 4; 90)