Abstract

Censored demand data reduce forecast accuracy, and the common separation of forecasting from optimization often leads to suboptimal seat allocations and diminished revenue in airline revenue management. This study proposes an integrated framework that jointly addresses demand unconstraining, forecasting, and capacity control, with performance assessed through simulation. Using historical data from a major Chinese airline, we evaluate Expectation–Maximization (EM) and Projection Detruncation (PD) unconstraining methods combined with Expected Marginal Seat Revenue (EMSR) heuristics. Our results underscore the critical importance of demand unconstraining, with PD outperforming EM. Compared to the airline’s experience-driven approach, the integrated framework delivers substantial improvements in both revenue and decision quality. Notably, even a simple, tractable optimization model, when paired with properly unconstrained and updated forecasts, captures most of the benefits of full integration.

Keywords

Introduction

Revenue management (RM) is a core function in the airline industry, aiming to maximize revenue through the coordinated use of seat inventory control and dynamic pricing. These strategies rely critically on two interdependent components: accurate demand forecasting and effective capacity control. However, existing research and practice often treat these components in isolation, leading to potential inefficiencies in revenue performance. To address this limitation, this study develops an integrated framework that unifies demand forecasting with updating mechanisms and control policy optimization, thereby enhancing total expected revenue through adaptive and data-driven decision making.

The primary contribution of this research is the development of a comprehensive system that integrates demand estimation and optimization methods within a unified framework. The proposed system is evaluated through simulation experiments designed to assess its effectiveness under realistic operating conditions. By systematically comparing different combinations of forecasting and control techniques, the study identifies configurations that yields superior performance and provides insights into addressing key challenges in airline revenue management, including forecasting uncertainty, dynamic demand patterns, and capacity constraints.

The model is developed using extensive sales and operational data from a major airline, providing a rich foundation for analyzing customer demand and market dynamics. Each RM component is rigorously tested in simulation to ensure methodological rigor and practical relevance. The insights from this evaluation are expected to support airline revenue managers in selecting effective tools and strategies for integrated decision making.

The remainder of this paper is organized as follows. We begin with a review of the related literature. Next, we describe the data and basic assumptions underlying our modeling approach. We then present the integrated framework of demand estimation and optimization, followed by the results of the simulation experiments and a discussion of their managerial implications. Finally, we conclude with the key findings and potential directions for future research.

Literature review

This research builds on two primary areas of study: demand unconstraining and forecasting, and seat allocation for a single flight leg. The first area focuses on estimating true demand from censored sales data, while the second involves optimizing seat allocation for multiple fare classes. Both are critical for airline revenue management.

Demand unconstraining and forecasting

Airline ticketing systems often fail to capture the full extent of customer demand. This issue, known as demand truncation, arises from inventory controls that restrict the availability of lower-fare tickets and from capacity limits. For example, when a low fare class is closed, the demand from customers who would have purchased it goes unrecorded. Similarly, once a flight is sold out, any additional demand is not observed.

The observed sales data are censored, requiring techniques to recover the true demand. As reviewed by, 1 these methods can be categorized by application: single fare classes (e.g., Expectation–Maximization, Booking Profile, and Life Table algorithms2–4), multiple fare classes (e.g., Q-Forecasting 5 ), and multiple flights?. 6 This study concentrates on models that treat fare-class demands as independent, a standard assumption in single-leg forecasting.

In industry practice, simpler methods like the Pick- up increment model 7 are common due to their stability and ease of use. More sophisticated methods like Hybrid Forecasting, 8 differentiate between price- sensitive leisure travelers and service-oriented business travelers. This segmentation helps distinguish between independent and more complex, correlated demand patterns. Recent work has shown that data-driven methods can substantially improve unconstrained demand estimation and forecasting. For example, Price et al. 9 apply Gaussian process regression to recover unconstrained demand paths, demonstrating the flexibility of nonparametric Bayesian models for capturing complex temporal patterns. Carmona-Benítez and Nieto 10 propose a single-class unconstraining framework that combines time-series decomposition, bootstrap resampling, and machine-learning predictors to estimate the true “market size” for an origin– destination pair. Fan et al. 11 develop a support-vector- regression approach for flight-level demand forecasting, further illustrating how modern machine-learning tools can enhance predictive accuracy. Together, these studies highlight the promise of integrating statistical decomposition and machine learning when reconstructing censored demand and motivate our exploration of hybrid, data-driven unconstraining techniques.

Recent work in inventory and demand forecasting, although often applied outside the airline context, offers valuable insights for airline revenue management. For example, Ho et al. 12 develops a demand driven storage allocation model for order picking. While the paper studies warehousing, it demonstrates how linking demand estimates with allocation decisions and operational constraints can improve overall performance. That perspective maps directly to seat allocation, where seats are the constrained resource and bookings are the demand to be fulfilled. Deep learning methods have likewise been used to combine prediction and operational decision making. Deng and Liu 13 proposes a deep learning pipeline that jointly forecasts demand, recommends inventory actions, and detects anomalies. Abbasimehr et al. 14 applies LSTM networks to demand forecasting and layers an optimization component to tune operational choices. These studies suggest that modern machine learning models can meaningfully improve forecasting accuracy and integrating forecasts with downstream decision processes produces measurable benefits. Although our model employs a classical parametric linear regression to generate explicitly normally distributed forecasts for EMSR input requirements, these studies provide strong support for the value of jointly modeling unconstraining, forecasting, and capacity control within a continuously updated pipeline.

Evaluating demand forecast accuracy is inherently difficult because true demand is unobservable. Fiig et al. 15 introduced a method applicable across fare structures to assess forecast performance. Building on this, our study uses actual airline sales data to unconstrain and forecast demand, while also evaluating predictive performance under the independent demand assumption.

Single-leg airline seat allocation

The study of revenue management began with work on overbooking models 16 and capacity allocation for two fare classes. 17 Littlewood’s rule, derived from the latter, became a foundational concept. Belobaba 18 extended this work to multiple fare classes and introduced the Expected Marginal Seat Revenue (EMSR) heuristic, which is now a standard industry tool.

Early seat allocation models assumed that customer demand for each fare class was independent and arrives sequentially, from the lowest to the highest fare. While this static, sequential-arrival model aligns with practical observations—such as leisure and price- sensitive customers typically booking earlier, and business travelers booking late, subsequent research introduced dynamic models where demand for different fare classes can arrive in random order, reflecting more realistic booking patterns.

The problem of allocating seats for multiple fare classes on a single flight remains a central topic. Recent work has produced both refined heuristics and dynamic programming based models to better accommodate realistic demand dynamics on a single flight. For instance, Korkmaz et al. 19 model dynamic fare class allocation under non-homogeneous Poisson demand and derive a fluid approximation to the stochastic dynamic program; their practical “look- ahead” pricing policy empirically approaches the DP optimum while remaining computationally tractable for single-leg applications. Balseiro et al. 20 study the single-leg problem in an algorithms-with-advice framework, formalizing how imperfect forecasts may be incorporated into online allocation rules and providing performance bounds that interpolate between model- based and worst-case approaches. Bai et al. 21 develops fluid approximations that account for high variance in arrival processes, improving approximation quality when classical Poisson assumptions fail and offering tractable policy design tools for volatile demand settings. Ertuğrul and Şahin 22 proposes EMSRtrc, an extension of EMSR that relaxes classical protection limits to control total revenue more directly, and shows empirical gains in several numerical experiments. Long and Belobaba 23 evaluates segmented continuous pricing and demonstrates how finer fare differentiation can increase revenue when implemented alongside realistic demand models. Together, these works support our emphasis on combining improved forecasts, approximation methods, and EMSR variants in a continuously updating pipeline.

While dynamic models more accurately capture customer behavior, their optimal policies—being both time- and state-dependent—are computationally demanding and difficult to implement in airline booking systems, which must deliver decisions within seconds to process high transaction volumes. Consequently, static models have been widely adopted in practice (e.g., Belobaba 18 ; Weatherford and Bodily 24 ). Nonetheless, static models can be adapted for dynamic use by updating demand forecasts and capacity control decisions more frequently. Recent research has advanced this integration; for example, 25 propose a single-leg RM approach that continuously updates forecasts and booking limits throughout the booking horizon. 25

Distinct from this work, our study develops a unified framework that integrates demand unconstraining, forecasting, and capacity control in a continuously updating process—thereby bridging two traditionally separate streams of research and offering a practically implementable solution for airline revenue management.

Data and assumptions

Data & scope

This study leverages sales data from a major Chinese airline to optimize revenue management on a business- travel-intensive route with eight daily flights. Using sale records from 2018 to 2019, we unconstrain demand, optimize booking control policies, and evaluate revenue performance via simulation for a representative flight.

Figure 1 shows cumulative booking curves for all flights, illustrating typical patterns: reservations are tracked daily from 60 days before departure, with the economy cabin spanning 17 fare classes (Y, K, M, etc.) across different pricing tiers and discount levels. Bookings accelerate sharply about 10 days before departure, providing insights into customer behavior that guide control strategies. Historical cumulative booking curves.

To ensure a clean single-leg analysis, we retain only non-stop, point-to-point departures and exclude code- share or interline legs, multi-leg itineraries, and external competitor fare feeds. Group bookings and corporate bulk contracts are removed from the unconstraining and forecasting pipeline. Cancellations and refunds are processed according to the carrier’s operational timestamps and treated consistently in the unconstraining step. The retained fields—including flight date, origin–destination pair, fare class, booking timestamp, fare paid, and inventory snapshots—support the unconstraining procedures, probabilistic forecasting, and EMSR-based capacity control experiments presented in this study.

Virtual class classes integration.

Model assumptions

The model is developed under several standard industry assumptions to ensure both methodological tractability and practical relevance. • Focus on the Economy Cabin: The analysis is restricted to economy-class passengers, excluding first and business classes. Demand in premium cabins tends to be more stable and constitutes a smaller share of total passengers. Revenue management research therefore emphasizes the more dynamic economy cabin, where the potential for revenue enhancement is greater. • Independent Demand Across Fare Classes: Demand for different fare classes is assumed to be independent. This assumption aligns with market segmentation strategies embedded in fare structures and underlies widely used demand estimation (e.g., EM, PD) and revenue management algorithms (e.g., EMSR), which have demonstrated practical effectiveness. • Exclusion of Cancellations, No-Shows, and Group Bookings: The model focuses exclusively on confirmed individual bookings and does not account for cancellations, no-shows, or group reservations.

Integrated demand forecasting and capacity control optimization framework

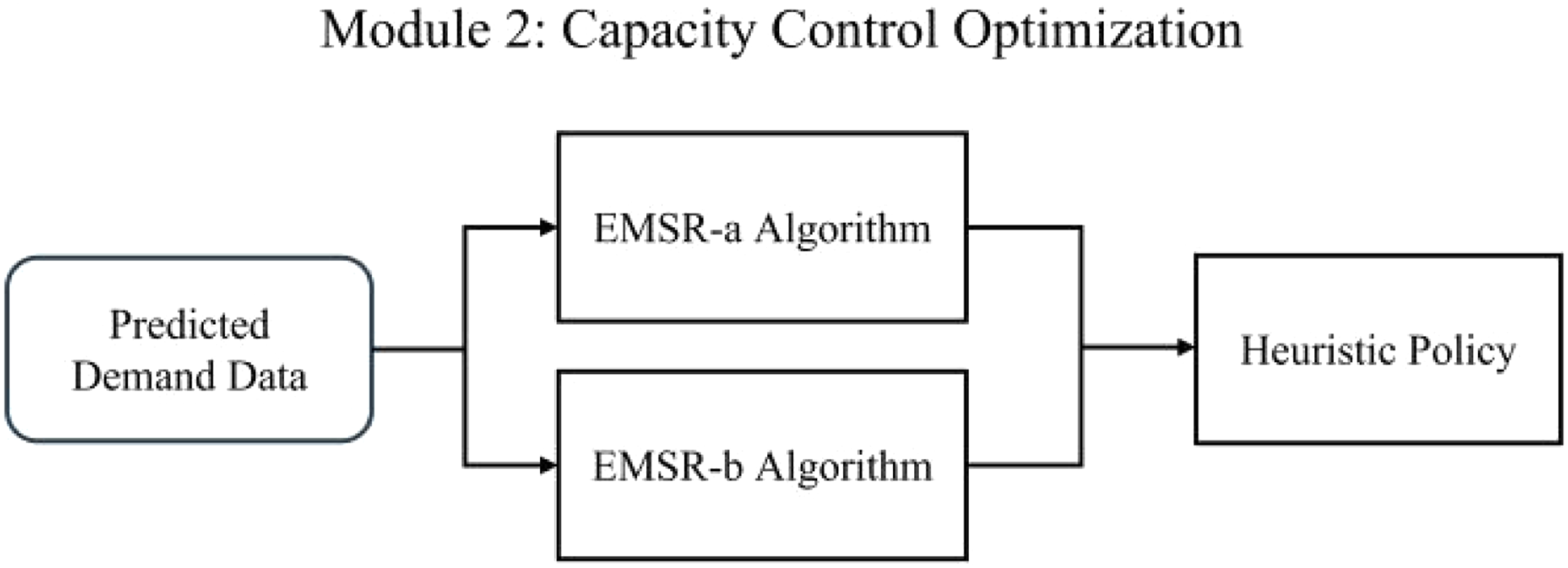

The framework of our model is shown in Figure 2. It is designed to improve decision-making by accurately forecasting demand and optimizing control policies. The model consists of four interconnected modules: • Module 1: Demand Forecasting: This module uses historical sales data to forecast future demand. Using advanced statistical techniques, it generates the demand predictions that are essential for the subsequent optimization modules. • Module 2: Capacity Control Optimization: This module uses the demand forecasts to develop and optimize capacity control policies. The goal is to refine operational strategies, such as seat inventory allocation, to maximize revenue based on the predicted demand. • Module 3: Performance Evaluation of Demand Forecasting: This module assesses the accuracy of the demand forecasts. Using various performance metrics, this evaluation helps refine the forecasting methods to ensure they are reliable and practical. • Module 4: Performance Evaluation of Control Policy: This module evaluates the effectiveness of the control policies developed in Module 2. By testing the policies under simulated conditions, we can refine them to be more effective and adaptable to changing market dynamics. Model framework.

Demand forecasting

Demand Unconstraining A critical preliminary step in the demand forecasting process is demand unconstraining, which differs fundamentally from conventional sales forecasting. Observed sales data represent censored demand, as they are influenced by inventory controls and capacity limitations (Figure 3). Consequently, sales figures for low-fare classes often underrepresent the true demand. This underrepresentation arises either from restricted access to low-fare tickets, resulting in “demand loss,” or from flights selling out, leading to “demand truncation.” Cumulative sales and actual demand.

Accurate estimation of true demand is essential for effective revenue management. Forecasts based solely on censored sales data systematically underestimate demand, which may lead to suboptimal capacity allocation and lower overall revenue.

In our approach, we assume that demand for each fare class follows a normal distribution. All fare classes except the highest-fare class are considered to have censored demand under typical circumstances. The highest-fare class is treated as censored only when the flight reaches full capacity. Therefore, our unconstraining procedure focuses on lower- and mid-fare classes and applies to the highest-fare class only in cases of capacity constraints.

EM algorithm

The Expectation-Maximization (EM) algorithm is an iterative method for finding maximum likelihood estimates in statistical models with unobserved (latent) variables. In our context, it is used to estimate the true, uncensored demand distribution from truncated sales data. The algorithm alternates between an expectation (E) step, which estimates the unobserved data, and a maximization (M) step, which updates the parameters of the demand distribution. This process is repeated until the estimates converge. We assume that the underlying demand for each fare class is normally distributed, and the EM algorithm helps estimate the mean and standard deviation of this distribution from the observed, censored sales data.

PD algorithm

The Projection Detruncation (PD) algorithm is another iterative method for demand unconstraining, similar to the EM algorithm. The main difference is in how it estimates the unobserved demand. Instead of using the conditional mean of the truncated distribution, the PD algorithm uses the conditional median or another quantile. A parameter, τ, controls the intensity of this estimation. A τ value of 0.5, which corresponds to the median, is a common choice. Adjusting τ allows for tuning the aggressiveness of the demand estimation, and the use of the median can make the method more robust to outliers compared to the EM algorithm.

Demand forecasting

For demand forecasting, the dataset is divided into a training set (January 2018– August 2019) and a test set (September–December 2019). As shown in Figure 4, we first reconstruct historical demand in the training set using either the EM or PD algorithm. The resulting unconstrained demand then serves to train a predictive model for future departures. Demand forecasting process.

For fare class i, let

For each fare class i, we fit a Lasso regression with the regularization weight λi, yielding the estimator:

The predicted mean demand for a test flight s with features

To obtain a variance compatible with EMSR, we estimate the class-level noise variance from the training residuuals

While advanced machine learning models (e.g., tree-based or neural network architectures) can provide accurate point forecasts of demand, estimating their predictive variance in a statistically consistent manner remains challenging. Most existing methods offer heuristic approximations rather than theoretically grounded variance estimates. Since the EMSR model requires explicit distributional inputs, specifically the mean and variance of demand, we employ the linear forecasting model, which provides closed-form and interpretable estimates of both quantities.

Capacity control optimization

With the forecasted demand, the airline applies capacity control optimization to allocate limited seat inventory across fare classes, with the objective of maximizing expected totoal revenue over a finite selling horizon. We consider a static demand environment in which demand for each fare class arrives in non-overlapping intervals, ordered from the lowest to the highest fare.

Let

Although dynamic programming provides the theoretical optimum Capacity control optimization process.

EMSR-a The EMSR-a algorithm extends Littlewood’s two-fare-class rule to multiple fare classes by sequentially applying the rule to all successive pairs of classes. At each stage

EMSR-b EMSR-b extends EMSR-a by incorporating both nesting and demand pooling effect across fare classes, thereby yielding more robust protection levels. An additional advantage of EMSR-b is its adaptability to rolling demand updates during the selling horizon.

In EMSR-b, protection levels are determined based on the aggregated demand of all higher-fare classes. Specifically, the protection level for fare class

Numerical results

This section outlines the practical application of our framework using the airline’s historical data. The process follows the first two modules of our integrated model: demand forecasting and heuristic optimization.

In Module 1, we begin by preparing the historical data. Sales records from January 2018 to August 2019 serve as the training dataset, while data from September to December 2019 is reserved for testing.

First, we apply the EM and PD unconstraining algorithms to the training data to estimate the true, uncensored demand for each virtual fare class. This step is crucial for correcting the distortions in sales data caused by booking limits and sell-outs.

With the unconstrained historical demand estimates, we then train a Lasso regression model to forecast future demand. The model predicts the mean and standard deviation of demand for each fare class for each day in the test period. The features used for prediction include time-based variables (such as the day of the week and month) and event-based indicators (such as public holidays) to capture demand variations.

In Module 2, the demand forecasts generated by Module 1 are used to optimize seat allocation. The predicted mean and standard deviation of demand for each fare class are fed into the EMSR-a and EMSR- b heuristic algorithms. These algorithms then calculate the optimal protection levels for each class, which define the number of seats to reserve for higher-fare passengers. The resulting set of protection levels constitutes the optimized control policy, which is then evaluated in the simulation framework.

Evaluation framework

Validating demand forecasts is challenging since true demand is inherently unobservable. To rigorously assess the performance of our forecasting and capacity control methods, we employ a Monte Carlo simulation–based evaluation framework. The number of independent simulation replications, N is adaptively determined to satisfy a predefined precision requirement, following the stopping rule described in the supplemental material.

In our experiments, we set the confidence level to 95% and the relative error γ to 0.01. The simulation for each flight sample continues until this condition is met, which typically requires approximately 5000 runs. This ensures that our results are statistically significant. The control strategies used in the simulation mimic those of the airline’s route managers, providing a realistic baseline for comparison.

As shown in Figure 6, we evaluate forecast effectiveness by comparing simulated sales and revenue with actual results. We use a dedicated test period (September to December 2019) not used for model training. We measure performance using the Mean Absolute Error (MAE) and Mean Absolute Percentage Error (MAPE) between simulated and actual outcomes. Demand forecasting evaluation process.

We compare three demand scenarios in our simulations: (i) a forecast based only on historical sales data (the baseline), (ii) a forecast based on demand unconstrained by the EM algorithm, and (iii) a forecast based on demand unconstrained by the PD algorithm. By comparing the results against actual data, we can determine which method best reflects real-world demand and quantify the value of demand unconstraining.

After identifying the most accurate demand forecast (the PD algorithm combined with linear regression), we use it to optimize control policies. We then compare our optimized policies (using EMSR-a and EMSR-b) against the airline’s actual policy. As outlined in Figure 7, we test these policies in the same simulation environment to estimate their expected revenues. The difference in revenue provides a clear measure of the effectiveness of our optimized strategies. Control policy evaluation process.

It is important to acknowledge the limitations of this framework. The simulation assumes that our demand and customer behavior models accurately represent reality. The evaluation is also specific to one route and time period, which may limit the generalizability of the findings. Finally, we compare our methods against an experience-based, static policy, and metrics like MAE and MAPE do not capture all aspects of forecast performance. These factors should be considered when interpreting the results.

Evaluation results

Demand forecasting evaluation results by simulated revenue.

Demand forecasting evaluation results by simulated class sales.

Having established that the LR+PD model provides the most accurate demand forecasts, we used these forecasts as direct inputs for the optimization module. The significant revenue lift just a result of superior optimization logic, but is fundamentally enabled by the high-quality, unconstrained demand data from the first stage. This demonstrates the synergistic value of our integrated framework, where forecast accuracy directly translates into more profitable control policies.

Control policy evaluation results.

Figure 8 provides a clear visual diagnosis for this 26% revenue gap. The managers’ policy consistently sets higher protection levels, reflecting a conservative, risk-averse strategy focused on guaranteeing seat availability for last-minute, high-fare passengers. While this approach minimizes the risk of turning away a high-fare customer, it leads to significant spoilage of a different kind: empty seats that could have been sold to mid-tier fare customers. Our EMSR-b model, informed by accurate demand forecasts, recommends lower protection levels. This represents a fundamental shift in strategy, correctly assessing that the risk of turning away a few high-fare passengers is outweighed by the near-certain revenue gain from selling more seats to Classes 2, 3, and 4. The 26% revenue improvement is the direct financial result of correcting this overly conservative stance. Protection levels for different class classes under route manager policy versus optimized policy.

Conclusions and future research

This paper presents an integrated airline revenue management framework that combines demand unconstraining, probabilistic forecasting, and capacity control optimization using real-world data. Simulation results demonstrate that unconstraining significantly improves forecast accuracy, which translates into more effective allocation strategies and higher expected revenues. Even simple EMSR-based booking rules recover most of the gains when fed with properly unconstrained forecasts, highlighting that input quality can be as critical as model complexity.

The framework provides a systematic, flexible approach for enhancing seat allocation decisions. By linking estimation and optimization, it clarifies how forecast errors propagate into control policies and offers a practical pipeline for incremental deployment. Airlines can implement the framework as a forecasting and decision-support module to generate recommended protection levels, improving seat utilization and revenue stability, especially on routes with sufficient historical data. Moreover, the approach supports controlled experimentation, allowing revenue management teams to evaluate forecast models, update frequencies, and EMSR parameters before scaling.

Despite its advantages, the framework has limitations. It focuses on single-leg operations and does not capture network effects, competitive interactions, or strategic responses, which can materially affect realized demand. Linear parametric forecasts assume stable relationships and normally distributed errors, which may be violated under extreme seasonal peaks or structural shifts. Data constraints—including group bookings, agent-mediated sales, and sparse covariates—can reduce unconstraining fidelity. Frequent updating also imposes computational and engineering demands, particularly under real-time latency requirements.

Future research can address these limitations by extending the framework to network settings, incorporating competitor pricing and market dynamics, and exploring alternative probabilistic forecasting methods such as Bayesian models, LSTMs, or Gaussian processes. Relaxing distributional assumptions through heteroscedastic or heavy-tailed models, applying robust optimization, and using online learning or bandit-style approaches to adapt EMSR parameters can improve resilience to model misspecification. Enriching input data with competitor fares, search signals, and corporate contract information can reduce censoring bias. Finally, field experiments with industry partners are needed to quantify revenue and service-level impacts under operational constraints and to calibrate engineering requirements for update frequency and latency.

Supplemental Material

Supplemental Material - Integrated demand forecasting and capacity control for segment-based airline revenue management

Supplemental Material for Integrated demand forecasting and capacity control for segment-based airline revenue management by Surui Wang, Kaiwen Wen, Jingying Lin, Haiying Pan, Lingshan Wu and Weifen Zhuang in International Journal of Engineering Business Management

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was partially supported by the Xiamen Airlines-funded project titled “Demand Forecasting and Dynamic Pricing for the Segment-Based Revenue Management”, as well as the National Natural Science Foundation of China, Grants No. 72072151.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.