Abstract

The aim of this study is to investigate the effect of environmental management accounting information (EMAI) on the design process of environmental and sustainable products of Iraqi industrial companies. This process has five different sub-processes: research process, analysis process, conceptual design process, detailed design process and design production process. The study uses the quantitative approach as the questionnaire was designed and distributed to 87 quality managers, production managers, design managers and financial managers. The MANOVA analysis shows that EMAI has a positive and significant effect on three of these processes, namely research process, analysis process and detailed design process, while EMAI has an insignificant effect on conceptual design process and design production process. The study has practical implications for managers of industrial companies. The results provide practical and theoretical knowledge for design and production managers as well as senior management to plan the production of environmental or sustainable products.

Keywords

Introduction

Management accounting plays an important role in providing financial and non-financial information for decision-making. Such information allows decision-makers to make appropriate choices about the use of the organization’s resources and capabilities. This traditional role of management accounting has been useful in managing product design costs Varaniūtė et al., 1 management control systems Dahal, 2 financial and non-financial performance measures Bogićević and Krstić, 3 and other important aspects of performance measurement. This trend has given rise to a number of important accounting applications that are considered integral parts of the strategy of modern industrial and commercial companies in a highly competitive, complex and dynamic environment. These applications include activity-based costing, activity-based management, balanced scorecards, target cost, quality cost, managerial creativity; value management and shareholder value analysis Rasyid et al. 4

Due to the complexity of the business environment and the social role of industrial companies in terms of protecting the environment, reducing pollution levels, reducing carbon levels in the air and contributing to the sustainable development of society, industrial companies have been paying attention to environmental and sustainability issues and integrating them into accounting systems. This integration is known as environmental accounting (EA), or green accounting. 5

EA is not a new field; it dates back to the 1970s as reported by Khalid et al. 6 and has gone through different stages of development, reflecting the concern of accounting with contemporary and renewable environmental issues. This concern is evident in the integration of environmental information into the accounting system. 7 The main outcome of this integration is environmental management accounting (EMA) as a component of EA. Vinayagamoorthi et al. 8 stated that the objective of EMA is to provide decision-makers with accounting and non-accounting information that goes beyond the traditional management accounting system. Sari et al. 9 pointed out that EMA is the process of collecting and analysing information related to environmental costs in order to assist management in making decisions related to product design, process design and product pricing.

EMA has developed because it has a relationship with product design, especially for environmental or sustainability products. Some multinational companies have introduced products, such as environmental products, clean products, sustainable environmental products and environmental design products that have become popular and accepted by consumers worldwide. Hojnik et al. 10 pointed out that European consumers prefer to buy ecological products that take into account environmental design. However, Doorasamy 11 argued that the development of EMA is still slow, and it is used in different areas in industrial companies. Similarly, Varaniūtė et al. 1 argued that managers do not want to make large investments in the development of EMA systems for the long term because they believe that these investments are associated with high risks and uncertainties.

Research gap and problem

Al-Mahdawi and Abdul-Amir 12 diagnosed many environmental challenges facing the business environment in Iraq, including increasing environmental pollution, climate change, desertification, drought and high waste rates. There have been several attempts to use green production and the green economy to provide solutions to environmental problems. For example, Abdulhussain 13 examined the possibility of applying EA in Iraqi industrial companies and concluded that although there is an awareness of the importance of applying EA in this environment, this type of accounting is not applied due to several difficulties and limitations. Jaff et al. 14 concluded that the application of management accounting methods and environmental costs in cement firms is limited due to the fact that the majority of these firms do not use management accounting and environmental cost accounting. Al-Humairi 15 examined the method of integrating the traditional applied accounting system and the disclosure of environmental information by including such information in financial statements. Thabit and Abdulrahman 16 pointed out that EA is an important control tool for reducing environmental violations, harmful emissions and the cost of manufacturing products in the long run.

Globally, Tanc and Gokoglan 7 examined the sensitivity of Turkish industrial companies to environmental issues and EA methods within the scope of social responsibility accounting, as well as the applicability of these concepts in these companies and their impact on strategic management accounting. Ariffin 17 considered EMA an important innovation that must be applied by companies to allow them to identify methods of more efficient operations and better consumption of resources that can lead to positive environmental and economic performance. Varaniūtė et al. 1 examined how management accounting systems can be integrated with sustainability and concluded that this integration improves the performance of companies. Johnstone 18 stated that information on environment and sustainability is necessary for firms to support and develop environmental management control systems. Kelsall 19 discussed how EA is used for management purposes. In this regard, management starts to pay more attention to the accounting for ecosystem management and cost accounting for environmental materials.

Accordingly, the relationship between EMA and product design is not discussed in the literature. Therefore, this study aims to fill this gap by identifying the role of EMA information in the design and development of sustainable and environmental products. This research will determine how EMA can be integrated with the stages of the process of environmental product design, meaning how environmental and sustainability requirements are incorporated into the product design and development process.

This study makes several theoretical and practical contributions. First, it provides a theoretical framework for the relationship between the EMA information system and the process of environmental or sustainability product design and development. Second, the study provides a practical framework for using EMA information in the process of designing and developing environmental or sustainability products. Third, it enables design managers, production managers and senior management to plan the production of environmental or sustainability products. Fourth, it helps production, finance and design managers estimate the costs of producing environmental and sustainability products. Fifth, the study provides a practical guide for how to use EMA information at each stage of the design and development of environmental or sustainability products.

Literature review

The concept of environmental management accounting

Bennett et al. 20 defined EMA as an accounting system that generates, collects and uses financial and non-financial information to improve economic environmental performance and sustainable business. Doorasamy 11 mentioned that EMA is an integrated approach that combines financial and non-financial information to reduce the negative environmental impacts of business activities and increase the efficiency of material use. In the same framework, Vinayagamoorthi et al. 8 defined EMA as the process of collecting and analysing information about environmental costs for the purpose of making internal decisions on product design, process design and product pricing. Ariffin 17 stated that the role of EMA is related to the diagnosis, measurement and analysis of environmental costs and that it goes beyond traditional management accounting.

Wahyuni 21 concluded that EMA is useful in cost savings, product pricing, optimal use of resources, innovation, clean products, increasing value for investors and improving the company’s reputation. In examining the impact of environment and sustainability in management accounting, Varaniūtė et al. 1 identified how the management accounting system can absorb environmental and sustainability requirements, especially with regard to product development and integrating those requirements when developing environmental and sustainable products. The results showed that the integration process is the main driver of changes in management accounting, product development and improvement of company performance.

Particularly in environmentally oriented companies, the main aspect of an EMA system is the process of identifying, measuring and analysing environmental information regarding costs incurred by the company in order to improve environmental performance and provide necessary information for making decisions about company activities. This aspect aims at improving the environmental performance of companies and the quality of life in society.

The EA system appeared as a result of the failure of the traditional management accounting system to fulfil environmental requirements imposed by regulations and laws, as well as the voluntary orientations of companies in serving society and improving the environment and quality of life. Ariffin 17 argued that companies have found the solution to their environmental problems through the application of the EMA system, which has become an integrated approach that needs to be applied in companies carrying out environmentally harmful operations. Companies that implement the EMA system have been able to reduce the environmental impact of their operations due to their focus on managing environmental costs and improving the company’s environmental performance. 22 In addition, companies that have implemented the EMA system have started to use fewer resources and focus on environmentally friendly resources with less impact on the environment. 23 EMA also plays an important role in providing managers with necessary information about the costs and benefits related to environmental performance and environmental and sustainable products. EMA also plays an important role in the integration of day-to-day operational information that management needs to assess the company’s environmental status and its compliance with environmental requirements. 24

Furthermore, EMA provides the necessary measurements to track costs and revenues and build measures for assessing environmental and sustainable performance. 25 These measurements enable a company to plan costs and profits and assess the feasibility of manufacturing and providing environmental products from environmental, social and economic viewpoints. Székely et al. 26 believe that EMA will be able to integrate many activities within the framework of environmental manufacturing processes for the purpose of achieving environmental goals and requirements. Some of these activities are related to creativity in product design, process design and the recruitment of creative and exceptionally skilled human resources. Doorasamy 11 believes that EMA provides information about product pricing when costs associated with environmental products are involved. In other words, management accounting provides information about the price of a product that fulfils the characteristics of or complies with environmental requirements. From another perspective, EMA provides information about measuring the profits of environmental products, making the appropriate decisions about abandoning or continuing the production of an environmental product, redesigning in order to reduce costs, improving the environmental performance of the product and eliminating unnecessary costs.

Accordingly, EMA plays a vital role in the success of a company’s environmental policy and its compliance with the environmental requirements imposed voluntarily by the organization or by environmental laws and regulations.

Product design process

Product design is one of the important processes in industrial firms. It requires the accurate analysis of structural requirements and other materials and requirements to determine the possibility of manufacturing and developing a product. 27

Ghimisi and Nicula 28 defined product design as all activities related to the creation and communication of information to transform data from multiple parties, including the market, into information and opportunities for the purpose of producing and presenting prototypes, initial specifications, designs and programmes. Cheng 29 defined product design as a creative, planned, step-by-step, purposeful and directed activity, where the design process refers to the process of developing the design and the order in which this process is carried out to achieve the design tasks.

Althuizen and Chen 30 viewed product design as a process of interactive and iterative sequential arrangement. This process requires an integrative design of the product life cycle — an exchange of information between designers from the beginning of the product design, taking into account all factors related to the product design process. This is in order to achieve the objectives of the design process in terms of improving quality, shortening the development cycle, reducing costs and protecting the environment. Chen 31 described product design as a series of interactive and iterative processes. In this process, the designer considers factors such as technology with a focus on product performance.

The product design process focuses on the need to integrate a number of aspects, such as manufacturing, assembly, inspection, materials and other process-related factors, including maintenance, environment, distribution and recycling. 27 Ginting et al. 32 emphasized this integration by pointing out that the product design and development process requires a holistic view of all aspects of the process and is not limited to one aspect rather than another. For example, technological products that require high technology should not neglect other aspects such as shape, weight and size.

Raffaeli et al. 33 focused on the role of designers in the product design and development process, noting that designers quickly learn about the production environment and try to obtain the necessary information for the design by using their experience in product design to simulate the requirements of the new design. However, it must be admitted that the designer cannot satisfy everyone, as experience alone is not enough. This is because the design process requires that designers have timely access to actual production data in order to design excellent professional products.

Stages of the product design process

The product design process encompasses the following stages:

Alli et al. 36 noted that the role of the EMA information system is highlighted in providing information about the availability of the potential to produce environmental and sustainable products by the company, information on the availability of machinery and equipment capable of producing environmental and sustainable products, information on the human potential to produce environmental and sustainable products and information on the internal environment suitable for producing sustainable environmental products. Therefore, this study’s first hypothesis was as follows:

There is a statistically significant positive correlation between the EMA information system and the research stage.

Tanc and Gokoglan 7 pointed out that the EMA system provides information related to the analysis of purchasing options for the machinery required to produce environmentally sustainable products. The company selects the machinery capable of producing the products it chooses and allocates efficient human resources capable of designing and producing environmental and sustainable products. Pratiwi et al. 22 stated that the company will be able to analyse environmental and sustainable products, determine the characteristics of each product and assess the impact of the products on the surrounding environment. In addition, the company must also identify and analyse the products that consumers want and that the company has decided to produce. Therefore, the second hypothesis was as follows:

There is a statistically significant positive correlation between the EMA information system and the analysis stage.

Within the framework of the EMA information system, Yuliarini et al. 35 argued that the company builds a set of procedures to start producing environmental and sustainable products, such as determining the types of environmental products required and the types of characteristics desired in each product. Thus, the company sets goals for each environmental product to be produced and identifies opportunities to change and improve the conceptual design and the resources required to produce each environmental and sustainable product. Therefore, the third hypothesis was as follows:

There is a statistically significant positive correlation between the EMA information system and the conceptual design stage.

Mukwarami et al. 39 pointed out that the EMA information system should provide information related to internal decisions on the cost of converting the detailed design into a final product and the cost of making substantial changes to the final product. The EMA information system also provides information related to the company’s ability to evaluate the selected designed product from all angles and dimensions. Here, the company can reach the stage of maximization in relation to the expected benefits of the product. The company develops detailed procedures for the product in terms of structure; design features such as colour and size; and calculates the expected costs and benefits of each feature. Therefore, the fourth hypothesis was as follows:

There is a statistically significant positive correlation between the EMA information system and the detailed design stage.

Here, companies need to introduce new products faster than their competitors, before new technologies emerge, market changes occur and the complexity of production and products increases, which requires the creation of a broad knowledge base for engineers. 40 According to Huseno 41 the product launch decision includes what to launch, where to launch, when to launch and why to launch in the market, taking into account that although the product may be clear, it may fail due to the weakness of the product launch strategy. Here, if the new product launch strategy is in line with the actual market, the product launch will be successful.

Mukwarami et al. 39 stated that the EMA information system should provide information about the cost of converting the detailed design into a final product and the cost of making significant changes to the final product so that the designed product complies with the objectives set and environmental characteristics of each environmental and sustainable product, as well as the environmental and regulatory requirements in the environment in which the product will be produced and sold. Therefore, the fifth hypothesis was as follows:

There is a statistically significant positive correlation between the EMA information system and the final design stage.

Methodology

The research is based on a questionnaire that was developed for the purpose of this study. Face validity and content validity of the questionnaire were made. The responses were classified according to five (1–5) point Likert scale. The questionnaire includes two parts; the first part contains four items related to personal information; the second part contains 40 items related to the research variables. The questionnaire is used for the purpose of this study due to the limitation of secondary data disclosed by the companies in Iraq. On the other hand, as many departments are involved in the production of environmental and sustainable products because it is a multi-dimensional process, collecting data from all these participants is useful to improve the process and reach true conclusions about it.

Population and sample

Sample distribution.

aIn some firms, the design management is under the responsibility of quality management.

Research instrument: A survey questionnaire

Demographic data of respondents.

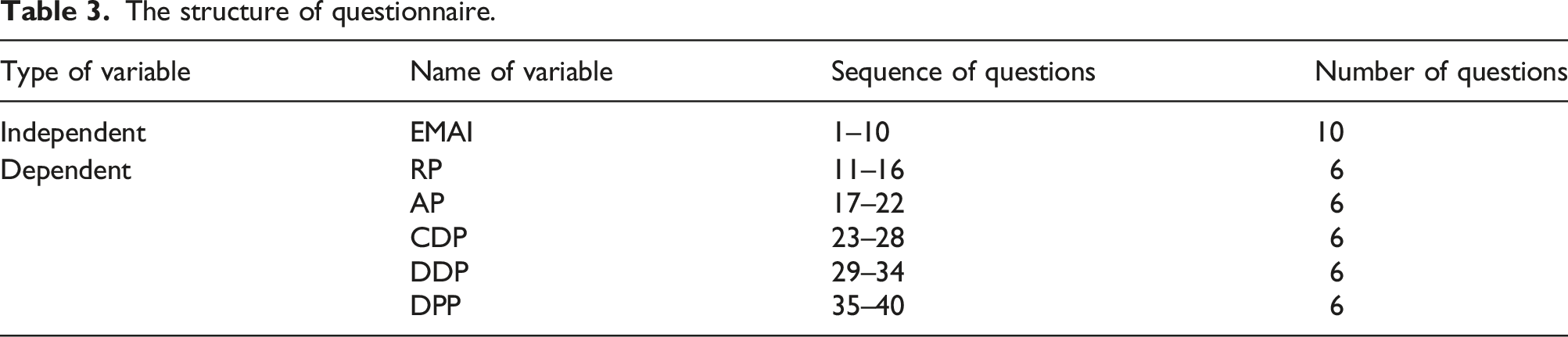

The structure of questionnaire.

Variable measurement and model specification

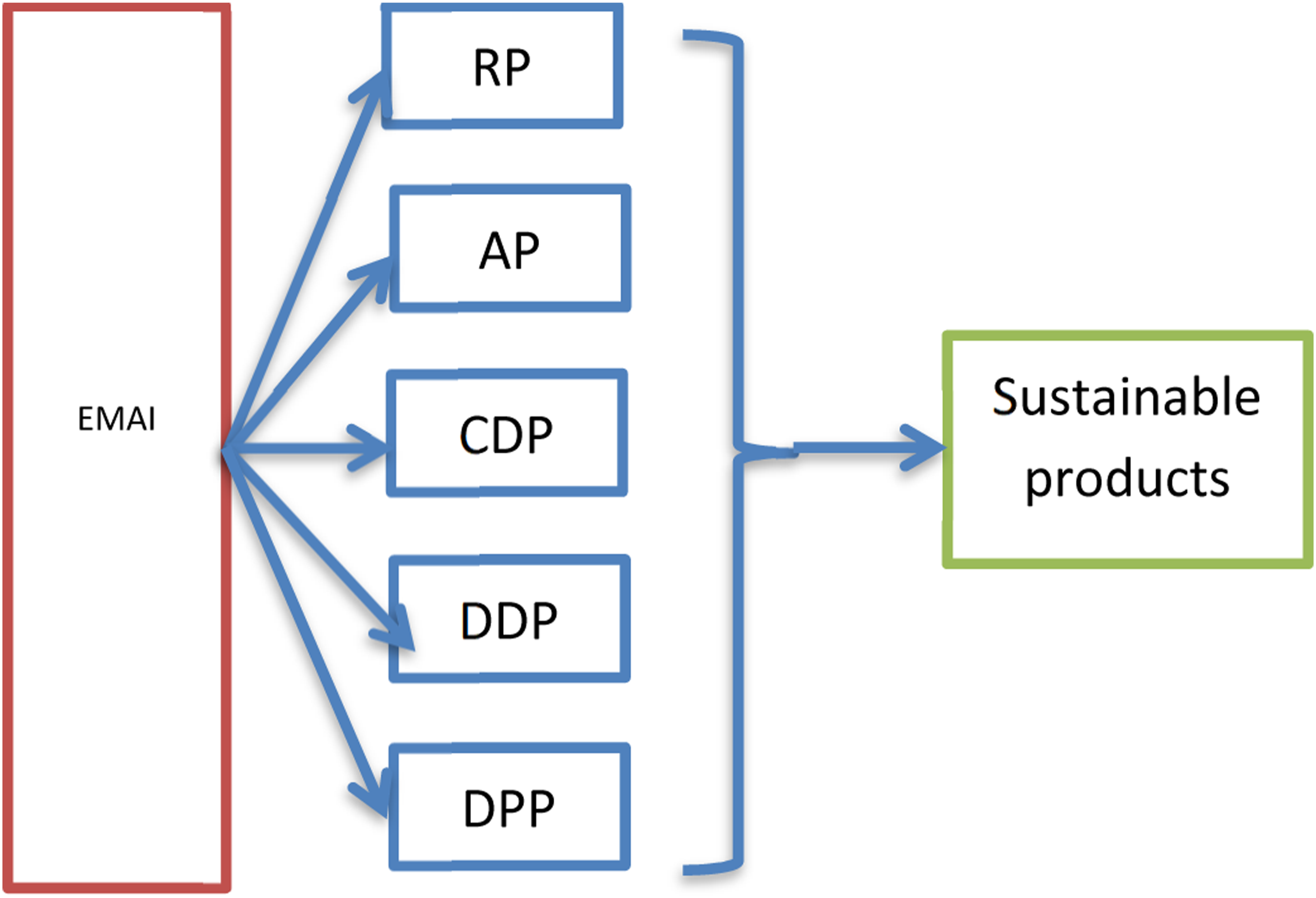

There are two variables in this study. Following the previous studies (e.g.,11,17,22,1 the independent variable is the environmental management accounting information (EMAI). On the other hand, the dependent variables are product design processes which include five sub-process; research process (RP), analysis process (AP), conceptual design process (CDP), detailed design process (DDP), and design producing process (DPP).42,1 In Figure 1, the relationship between the dependent variable and the independent variable is explored. Research model.

According to the relationship between the dependent variable and the independent variable, the following models will be tested in the study:

Note:

RP = Research process

AP = Analysis process

CDP = Conceptual Design process

DDP = Detailed Design process

DPP = Design Producing process

EMAI = Environmental Management Accounting Information

β = coefficient

α = constant

ε = standard error

The study uses MANOVA to test the hypotheses because it is the relevant test related to the model of this study. This statistical test is used when the study has one independent variable and more than one dependent variable. Also, the study uses ANOVA and Tukey analysis to find out the effect of demographic variables on both independent and dependent variables.

Results

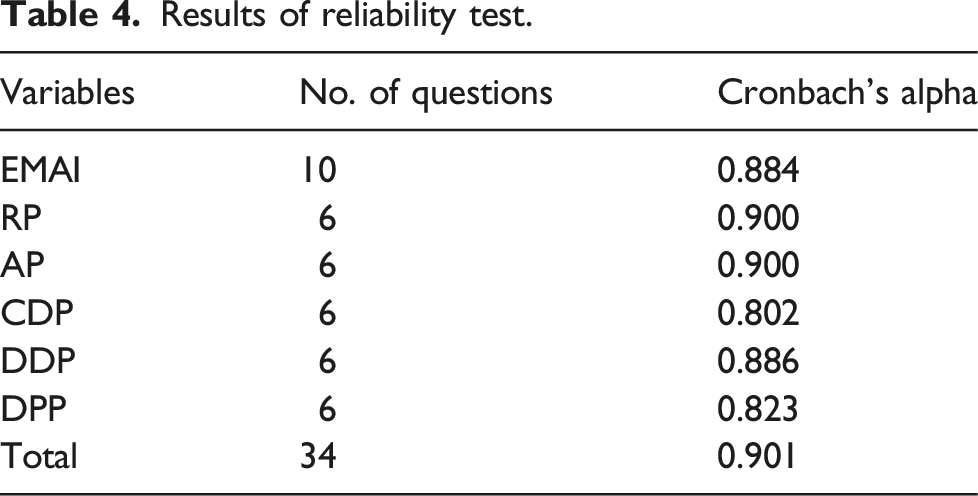

Result of construct assessment: reliability test

Results of reliability test.

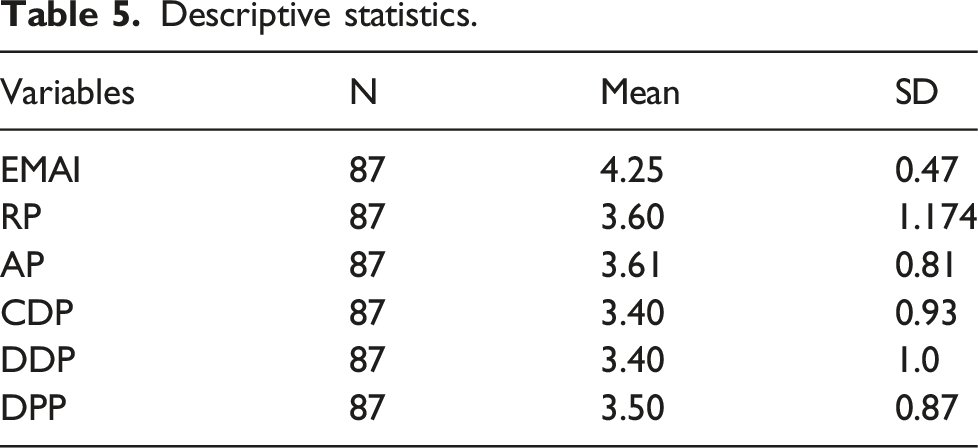

Descriptive statistics

Descriptive statistics.

The results of Table 5 show that the mean of the variables is between 3.40 and 4.25, which indicates that the industrial companies recognize the importance of these variables. The mean of EMAI is (4.25), which is high, indicating that the respondents believe that EMAI should receive a high level of attention when designing environmental and sustainable products. The respondents also gave a higher weight to the research and analysis processes than the other three stages due to their importance in the design of environmental and sustainable products.

Correlation and multicollinearity

Correlation and multicollinearity.

aCorrelation is significant at the 0.01 level (2-tailed).

bCorrelation is significant at the 0.05 level (2-tailed).

The results of Table 6 show that there is a positive and significant correlation at 0.01 between EMAI and RP, AP, CDP and DDP, while the correlation between EMAI and DPP is positive and significant at 0.05. These results indicate that the increase in the information of environmental management accounting leads to the improvement of the process of designing sustainable and environmental products. On the other hand, Table 6 shows that there are no multicollinearity problems in the model as the correlations between the dependent variables are less than 0.80.

Regression analysis: MANOVA analysis

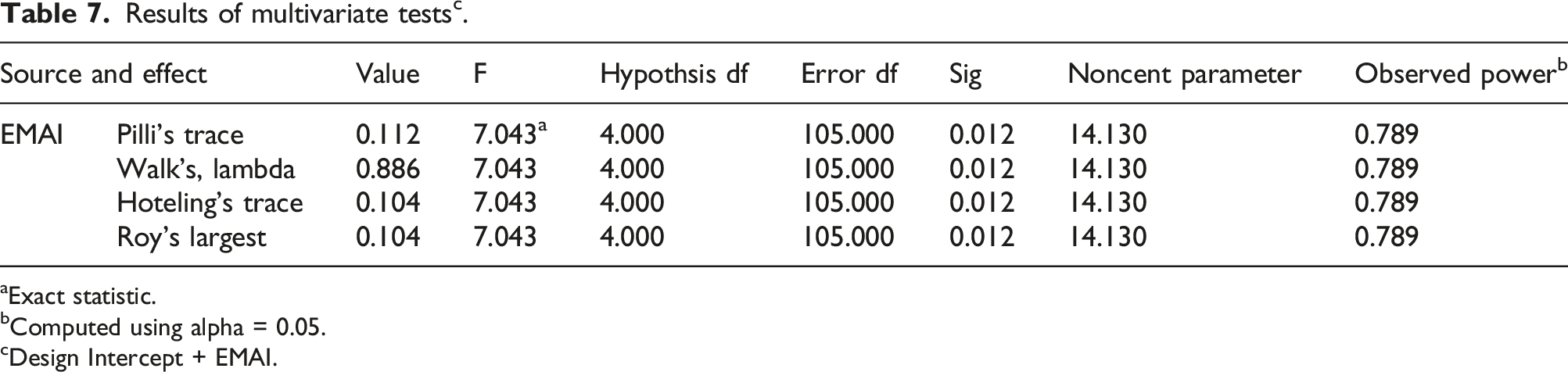

Results of multivariate tests c .

aExact statistic.

bComputed using alpha = 0.05.

cDesign Intercept + EMAI.

Tests of between-subjects effects (N = 87).

bComputed using alpha = 0.05.

The second part of the MANOVA analysis presents univariate tests of the effects of the independent variable on each of the different dependent variables, as in Table 8.

The results of Table 8 show that the EMAI has effects on RP, AP and DDP where the Sig values are less than 0.05. On the other hand, EMAI has no effect on the other two dependent variables; CDP and DPP. The observed performances for RP, AP and DDP (0.693, 0.609 and 0.594) are acceptable and they are better than the observed performances for CDP (0.169) and DPP (0.044). From the results, it can be concluded that EMAI is very important for the design of environmental and sustainable products in the early stages of this design process.

The effect of demographic variables

Results of effect of demographic variables (ANOVA).

Results of Tukey test.

a significant level 5%.

The results of Tukey test indicate that there is only one source of differences that is (5–10 years) as the mean is the highest (4.372) among the means of other years of experience.

Discussion

The present research aimed to determine the role of EMA information systems in improving the design process of environmental and sustainability products in a sample of Iraqi industrial companies. These companies are trying to produce green and environmentally friendly products. In order to produce these products, it is necessary for companies to develop a management accounting information system that simulates the need for environmental and green information about the products, machines and equipment necessary to achieve this, as the traditional management accounting information system has failed to provide this type of information. On this basis, previous studies have pointed to the potential role of management accounting in providing financial and non-financial information for decision-making on the design of environmental products and in providing information at each stage of the product life cycle. The EMA information system evaluates the available alternatives for environmental products and collects information on the sales prices of each environmental product and its sales forecasts and costs. In terms of non-financial information, the EMA information system provides information about qualified human skills in dealing with environmental products, the environmental performance of the company, efficient use of materials in the manufacture of ecological products and information on trends and opportunities for improving the environmental performance of both the company and sustainable products.

This study has attempted to provide new practical evidence about the role of EMA information in improving the product design process in an industrial environment that requires such information for improvement of the manufacturing process for environmental and sustainable products. In alignment with prior studies (e.g.,29,30,39 the results of this study showed the importance of the EMA information system in improving the design process of environmental products, especially in the stages of research, analysis and detailed design, where there is a significant need for financial and non-financial information of an environmental nature, including environmental costs, compliance with environmental specifications and product structure, characteristics and specifications. In these three stages, the product image becomes physical and complete, and consequently, management will have a clear idea of the cost and structure of the product. All other processes that complete the design process will be routine and ordinary. Cheng 29 pointed out that in the research and detailed design stage, there will be a significant need for information by the designer to form an abstract image of a realistic product. In addition, management will have a clear picture of the production costs, expected production quantities and other expenses, selling prices and the marketing process of the product.

In the Iraqi industrial environment, there is a tendency for industrial companies to start the production of environmental and sustainable products in order to catch up with global development in this field, whereas environmental products and sustainability and development projects have become one of the most important features of the era.

Conclusions

This study is one of the few studies conducted in the Iraqi industrial environment. It aimed to analyze the role of environmental management accounting information in improving the design process of environmental and sustainability products. The study assumes that the improvement process requires identifying the information needed in all the different stages of the product design process, starting from the research stage to the production stage. The study has found that environmental management accounting information is important and necessary for making decisions related to improving the product design process. The importance of environmental management accounting information is clearly reflected in the research, analysis and detailed design stages, where the impact of such information was positive and statistically significant. This reflects the important role such information plays in making decisions related to product design, where the importance of information such as product costs, associated environmental costs, service costs and recycling is clear. In addition, the study find out that the years of experience as one of the demographic variables has effect on EMAI indicating that the respondents with more experience have more awareness about integrating EMAI in the production of environmental and sustainable products.

There are several practical implications of these findings that can serve management and designers. First, it visualizes the relationship between environmental management accounting information system and the process of designing and developing environmental or sustainability products, and the importance of building and designing an environmental management accounting information system in industrial enterprises. Second, in practice, the system provides financial and non-financial information for the purpose of improving the design and development of environmental or sustainability products. For example, this system integrates financial and non-financial information to consider most of the aspects related to the decision to design, improve or develop a product. Third, the research results provide practical and theoretical knowledge for design and production managers as well as senior management to plan the production of environmental or sustainable products. Fourth, the research results provide a practical guide on how to use environmental management accounting information system at each stage of designing and developing environmental or sustainable products.

However, the research results are subject to the following limitations: First, the information related to the construction of the research model and obtaining the results was obtained through a questionnaire addressed to a sample of production, quality, design, and finance managers. Therefore, the research results reflect their point of view and are difficult to generalize to all companies. Here, the study suggests the use of other tools to collect information, such as interviews or approved administrative records. Second, most of the companies surveyed do not currently produce environmental or sustainable products and do not have an environmental management accounting information system. As a result, the results of the research are only visions of the sample members and are not related to actual facts. Therefore, the study proposes to compare the results of the relationship between environmental management accounting information system in companies that produce sustainable products with those that do not. Third, the stages of product design are many and different from one company to another, so it is difficult to study all the stages of product design used by different companies. On this basis, this research examined the relationship between the environmental management accounting information system and the stages of product design as described in the relevant literature review in this field. In this regard, the present study suggests conducting a similar study using different stages of the ecological product design process.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.