Abstract

Major assets such as buildings, infrastructure and defence systems are long term investments that require many outsourced sustainment activities to maintain satisfactory performances over their service life. When multiplied by the number of years that the sustainment is planned to be undertaken, the contracting cost is high. Many business processes are established to govern these asset sustainment activities and eventually become the source of inefficiency. This paper analyses the performance of these processes using a performance driven approach. Combined with input data of requests for engineering change in similar assets, this paper evaluates a new business process redesigned from an existing process to achieve significant savings in total cost of ownership as well as improving other non-financial performance indicators.

Keywords

Introduction

Sustainment is a term that is commonly used by defence organisations meaning activities that provide services such as maintenance, engineering, supply, configuration management, replenishment of consumable items and disposal, in order that the asset can be operated at its best possible condition. 1 These activities are equally applicable to non-defence environments. When a building is in use, many associated services which are often categorised in terms of facilities management, operations and maintenance are established. These services work closely with external sustainment service providers in ‘architecture, engineering, construction’ and are integrated with the building’s life cycle management. 2 Sustainment activities also have broader implications. De Almeida and Borsato 3 examined the impact of recycling and depletion of resources in sustaining operations while minimising the impact on the environment and the economy. Kulakov and Baronin 4 investigated new concepts in energy efficiency from the building’s life cycles perspective with the aim to improve both construction and operational costs.

Nowadays, many operations support and maintenance services are outsourced. When considering the number of years that sustainment activities are planned to be undertaken, the contractual value is high. Coles 5 reviewed sustainment requirements on a set of major asset and concluded that the total sustainment cost was more than double the initial cost of the asset. Therefore, asset owners are pushing for ‘value for money’ when evaluating procurement contracts. 6 Assessment of contracts in terms of ‘value for money’ for procurement of the asset is often based on cost benefit analysis on the whole asset life cycle. 7 Likewise, sustainment contracts are treated as a type of procurement of services. Procurement of sustainment services is usually separate from asset procurement due to funding arrangement. 8 Under the same ‘value for money’ assessment criteria, a ‘whole of life’ costing approach is required for sustainment works that span over a large part of the project life cycle. 9

Due to long term commitment, asset owners setup many business processes to govern these asset sustainment activities in order to ascertain good operational outcomes. After analysing three sets of projects, McLay et al. 10 found that five key constructs were required to ensure a service-support project to be effective in the project life cycle. The five key constructs were: (1) customer and humanistic driven innovation, (2) primary performance drivers, (3) learning from valued resources, (4) focus on quality planning and return on investment, (5) stakeholder collaboration. They recommended a facilities condition audit on whether these five key constructs existed as the first step in determining if the newly awarded sustainment contract would be viable and beneficial.

Unfortunately, pre-contract audit using specific assessment constructs does not necessarily guarantee good sustainment outcomes. 11 Instead, Suttell 12 recommended that Total Cost of Ownership (TCO) would be the best benchmarking parameter to make decisions on sustainment contracts. Similarly, Duran et al. 13 proposed a decision framework applying TCO as an overall performance indicator and incorporating the cost of spare parts management for assessing the life cycle costs of physical asset. Palmer et al. 14 applied TCO assessment of three types of electric vehicles, i.e. conventional hybrid, plug-in hybrid and battery electric vehicles in three countries, UK, USA and Japan. The study highlighted the influence of institutional policies on market share of electric vehicles in these countries. Application of TCO in these researches was primarily focused on acquisition of the asset and evaluated from the owner’s perspectives.

However, use of TCO to guide planning of sustainment activities to achieve contractual goal could be misleading. The strategy of defence organisation to reduce sustainment costs was to suppress demand of sustainment services as well as increase competition for short term contracts, but TCO increased as a consequence. 15 Mohamad et al. 16 combined the TCO approach with lean manufacturing to facilitate the decision making in ascertaining sustained processes in the system. Costs associated with efforts of implementing lean and waste management are in certain aspect related to sustainability of the system but since manufacturing is an ever evolving process (to suit customers’ needs), the TCO indicator was mixed with objectives other than system sustainment.

Sustainment activities, by its nature, is a type of service businesses. In contrast to goods trading businesses, service businesses operate on service-dominant logic as the foundation of business strategy which was initially published by Vargo and Lusch. 17 The concept attracted tremendous interests in both academia and industry. 18 Subsequent research highlighted nine propositions for service-oriented businesses to adopt in order to compete successfully. 19 Subsequently, the service-dominant logic has become one of the core concepts of a new business model known as Product-Service Systems (PSS). 20 Freiling and Dressel 21 examined the adoption of TCO by small and medium-sized companies. The study was based on a service-dominant logic and found that the model could be constrained by relational factors in business-to-business markets. Researches related to these service contracts were more marketing focus (promoting the advantages of service design) rather than optimising the sustainment system. Two research questions arise.

TCO was initially used to compute accumulation of project costs in whole of life of projects. 22 Is TCO an appropriate performance indicator to be used in assessing sustainment contracts? Does it represent the baseline information reflecting a plan for sustainment activities for years to come?

If TCO is suitable for evaluating sustainment contracts, how can TCO be applied to drive the design of sustainment system for better ‘value for money’? Can it be used as an objective function to guide development of a ‘value for money’ sustainment system?

This paper explores answers to these questions. For question 1, TCO has been used to characterise that asset acquisition project is value-for-money for the customer. The research question 1 raised here is for different type of project, viz, sustainment of asset. The nature of sustainment is different from asset acquisition. The rationale for this question is to establish TCO as the foundation concept that covers sustainment costs and revenues opportunities for the life of the sustainment contract. Therefore, it is necessary to carry out thorough literature review to determine (a) what is the most commonly acceptable meaning of TCO and its models, (b) what do we do with TCO models in the context of sustainment, (c) Are there any TCO models are specially designed for sustainment contracts. Following positive finding from question 1, question 2 is to explore what type of evaluation methodology needs to be done. The nature of sustainment contract is to solve evolving issues arising from operations, new system requirements, changed environment. Although the term ‘value-for-money’ is literally acceptable in commercial world, quantification of ‘value’ against monetary amount varies between people. With a better established TCO model from answering question 1, the ‘value’ can be assessed by the proposed process design evaluation methodology proposed for answering question 2.

The rest of the paper is structured as follows. The section ‘literature review’ searches for prior researches that are relevant to answers to these questions so as to identify the gap. The section ‘research methodology’ establishes the theoretical basis for this study. The methodology is applied to a ‘case study’ section with analysis results that illustrate how the methodology works for evaluating sustainment contracts.

Literature review for TCO models

In order to investigate if TCO is suitable for assessing sustainment activities, we focus our literature review effort on literature that identify and define parameters constituting TCO. This will help us to understand characteristics of TCO for answering question 1. Major research databases ScienceDirect, Proquest and Emerald Insight are used. Our search focus here is on research articles with two characterising keywords in our paper title, i.e. sustainment and total cost of ownership.

We realised from interactions with other researchers and industrials that the term ‘sustainment’ is not commonly understood. Hence, we started with the keyword ‘sustainment’. ScienceDirect returned 26,222 articles. Returned publications contained keywords ‘sustainability’, ‘sustainable’, ‘sustained’ but no exact match of the keyword ‘sustainment’ was found. Sustainability refers to the ‘quality of being able to continue over a period of time’. 23 This definition is different from the meaning of sustainment as discussed at the start of this paper. Proquest returned 3,646 articles. We glanced over 200 articles but could only identify 5 related to our definition. Singh and Sandborn 24 focused on balancing life cycle cost of sustainment versus obsolescence so as to optimise design process. The other four articles 25 –28 were authored by military personnel and dealt with policy and procedural issues in sustainment. Emerald Insight returned six articles. Four of them were related to social and product marketing issues. Of the two relevant papers, Evans and Steeger 29 studied the time of military deployment required to sustain operational readiness. Mathaisel et al. 30 studied and documented best practices in maintenance, repair and overhaul (MRO) in military environment. Research literature related to evaluating sustainment activities on an asset is rare. This keyword search has not only proved our observation, but also highlighted the need to examine the relationship of service business with engineering sustainment requirements.

On the contrary, the search for ‘total cost of ownership’ has good returns. Our goal is to investigate if there are significant variations of the TCO model used in different application areas. ScienceDirect returned 406 articles. Twenty-four articles contained the exact keywords on the title. Hartman et al. 31 focused on factors of offshore manufacturing ‘beyond’ TCO and deemed irrelevant in this search. Morssinkhof et al. 32 and Dumortier et al. 33 studied the marketing effects of providing TCO to customers. These articles did not have quantified TCO information.

Proquest returned 10,927 articles. We further focused on articles related to economic models, model and decision making. We glanced through over 200 of the results and found 5 duplicated with ScienceDirect returns. Twenty-four articles contained the exact keywords on the title. Ellram 34 reviewed taxonomy of TCO research. Colson et al. 35 discussed pollution compliance requirements for air fighters and made reference to TCO as a factor. Fitzgerald 36 made a qualitative comparison of TCO outcomes between education and commercial sector and concluded that the TCOs for schools were generally lower. Roda et al. 37 reviewed different TCO models and concluded that new TCO models would be necessary to support specific asset life cycle study. Wouters et al. 38 argued how TCO can improve governance of a company. Maltz and Ellram 39 examined modified version of TCO to TCR (Total Cost of Relationship) for logistics operations. These articles did not provide a computable TCO model.

Emerald Insight returned 11 articles. Ellram 40 studied TCO implementation in seven companies. The author found that TCO models varied between companies. The author concluded that individual companies should adapt their own model. Zachariassen and Arlbjørn 41 illustrated that TCO should be differentiated between companies due to difference in relationships and cost drivers. Again, these two articles used TCO as a management tool but no detail computational information was given.

To identify which cost items are critical to evaluating sustainment activities, we reviewed literature related to servitisation. In recent years, PSS emerged as a common strategy for original equipment manufacturers (OEMs) to extend their business to services after commissioning. 42 Baines et al. 43 performed a clinical review and identified three types of PSS: (1) Product-oriented PSS, (2) User-oriented PSS, (3) Result-oriented PSS. The authors concluded that PSS is a special case in servitisation where the service elements of a product are offered an integral part of a business. Sustainment services are post commissioning services in PSS. Expanding into PSS business model depends on the complexity of the asset and presents significant challenges to the OEM. 44 It is logical to apply TCO to PSS, but using TCO as a performance indicator for sustainment contract valuation would require further investigation.

This literature survey shows that the content of TCO varies between industry sectors, which highlights the importance for engineers and managers to harness precise knowledge of this type of service businesses.

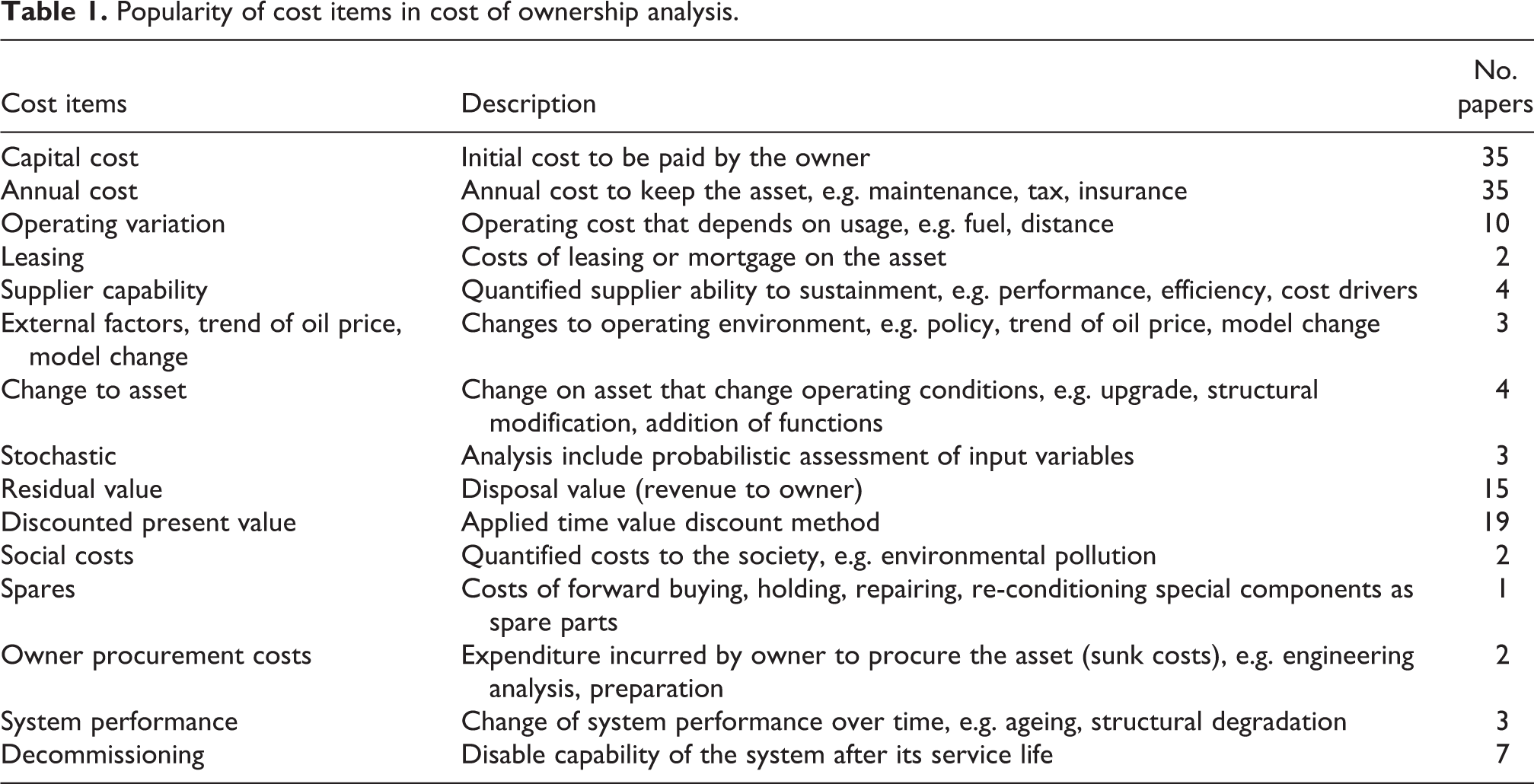

From these literature searches, Table 1 is compiled to classify different types of TCO model to guide our next investigation.

Popularity of cost items in cost of ownership analysis.

From Table 1, it is clear that capital cost and annual cost are essential items in any TCO model, with one exception due to the investigation context. Residual value, operating variation and discounted present value are common cost items and most noticeable in more recent researches. The remaining parameters are occasionally used, depending on application. Hence, apart from the five main cost items, TCO models can be customised to suit specific part of the project’s life cycle.

Literature review for what to do with TCO model for sustainment

Assuming a TCO model that reflects more accurately the characteristics of sustainment activities, answer to question 2 is on how this model should be used to assist evaluation of sustainment contracts. Braun et al. 45 analysed a contract-based relationship for value co-creation and gain-sharing between two companies for sustainment (maintenance) services. After 5 years of good results for both parties, the relationship was terminated. The authors found that even valuable contracts could be terminated because changes in business processes could affect trust between parties.

Roda and Garetti 46 maintained that integrating TCO into decision processes could prevent decision makers from undertaking investments which might appear cheaper in acquisition but ended up being significantly more expensive in total cost over the entire life cycle. Since the duration of TCO evaluation is basically the service life of the asset, decision for long term sustainment contracts needs to balance the risk of inappropriate contractor capability against expected performance when executing the service contract. 47

Aguilar-Saven 48 proposed a classification framework that helped system engineers to decide what business process analysis tools should be used to analyse a structure describing logical order and dependence of activities. The objective was to produce a set of related activities that could be of value to a customer. However, the author admitted that description of the available business analysis tools in terms of purpose, scope and usage were still inadequate.

Rauch et al. 49 proposed a framework for managing the distributed network of supplies to improve agility and sustainability of the system. Geissdoerfer et al. 50 used empirical data in US and Europe to study the effect of standardisation of the total life cycle cost models. They concluded that standardisation could enable more strategic advantage in purchasing decisions. Further cost savings were expected by calculated measures of selecting suppliers and determining optimal order quantities. 51 Unfortunately, contracts for sustainment activities were still costing billions to the asset owners. 52,53 Apart from setting up organisational structure with right attributes and managing supply chains effectively, there is a need to analyse every possible source of costing in the life time of the asset before engaging with suppliers for long term service contracts. It is evident that TCO models are particularly useful for service life requirements.

Since 2000, there is increasing research interest in methodologies, techniques and tools to support the design or redesign of business processes. 54 To meet many challenges in through-life-support businesses, structured and defined methods are essential while the system continues to adopt state-of-the-art technologies. 55 Vanwersch et al. 56 argued that redesign of business processes could have a huge potential in terms of reducing process costs and throughput times, as well as improving customer satisfaction. Therefore, changes in business processes is frequently required to improve business performance.

Boehm et al. 57 found that many organisations used separate budgets for system development and system life cycle support. This usage led to sub optimising system architectures and designs to minimise development costs, which in turn resulted in inflexible, hard-to-modify systems and higher overall costs for the system’s owners. An easy-to-understand indicator that can support decision on the process is the overall performance of the system, which should be analysed quantitatively. 58 Management decision regarding changes in process should not be considered lightly.

However, engineering business process in sustainment activities is not limited to the original equipment manufacturer of the asset. The service provider can be a third-party engineering organisation which gains access to the asset’s intellectual property through the asset owner and can re-engineer the asset. A review of the work by Ng et al. 59 showed that sustainment of complex engineering assets comprises on-going operations support, continuous upgrades, services, logistics, maintenance and repairs. In some cases, due to regulatory and institutional requirements, special procedures are also required for decommissioning. 60

The requirement for decommissioning an asset is mostly due to environmental considerations. Kaiser and Liu 61 estimated the total cost of decommissioning 53 offshore deep water oil wells to be $2.4 billion. The decommissioning work included removal of platform and associated facilities, plugging and removal of seafloor obstacles. Suh et al. 62 surveyed 162 nuclear decommissioning cases. The major factors affecting safety in decommissioning operations were plant’s operating history and duration, decommissioning funding and experience, waste facilities. Anifowose et al. 63 examined 19 oil and gas projects in Nigeria. The lowest work quality in these projects were in the areas of environmental impact prediction and project closure. The ability to decommission an asset properly for many organisations is doubtful. Sjöblom and Lindskog 64 investigated decommissioning cases of four old nuclear research and development facilities. They found that while budget had been prepared by the ‘polluter pays’ principle, decommissioning funds were still not available when the plants were decommissioned.

Apart from end of life decommissioning work, sustainment activities include support for operating the product. High value products are increasingly equipped with sophisticated monitoring systems to assist sustainment of system performance. Li et al. 65 reviewed approaches of product health monitoring systems with low-cost sensor networks and smart algorithms in rail industry. They concluded that inertial sensors were the most popular due to their advantages of low cost, robustness and low power consumption. Acharya and Han 66 reviewed systems and technologies used in Integrated Vehicle Health Monitoring in defence asset market. The systems were able to collect and analyse data concerning variations in operation and damages so as to decide appropriate actions even under hostile and harsh environments.

Maintenance and repairs involve availability of spare parts. To minimise the risk of stock out, product configuration are increasingly being used for asset procurement on ‘commercial-off-the-shelf’ or ‘military-off-the-shelf’ basis. Modgil and Sharma 67 investigated the impact of total productive maintenance (TPM) and total quality management (TQM) practices on operational performance and their inter-relationship. They found that these practices could help to reduce the cost of operation in terms of reduced scrap and less defective products. Based on these reviews, a TCO model should include elements for evaluating sustainment activities related to decommissioning, system change and spares.

From these literature, analysing processes in managing sustainment activities with an aim to make the processes more efficient appear to be a viable solution to plan sustainment activities that have a lot of repetition over time. The remaining part of the question is what analysis would be suitable.

Sustainment TCO model

Table 1 shows that there is no standard formula for TCO calculations. A more formal but not restrictive definition is necessary. To develop a computational model, we examine some TCO literature in detail. Ministry of Business, Innovation and Employment 68 in New Zealand presented a simple formula for calculating TCO. Broadly speaking, the method is to research, estimate and calculate all costs and benefits over the whole-of-life. Humphries and McCaleb 69 compared options for forming the fleet and evaluated TCO costs including new purchases, residual value, utilisation, maintenance, repair, fuel, downtime opportunity, depreciation, capital, over a 6-year cycle with Net Present Value (NPV) of the cash flow for each of the cases. Ritsma et al. 70 defined TCO as the total costs during the lifetime of a product taking into account costs of capital expenditure, costs of operation and costs of end of life.

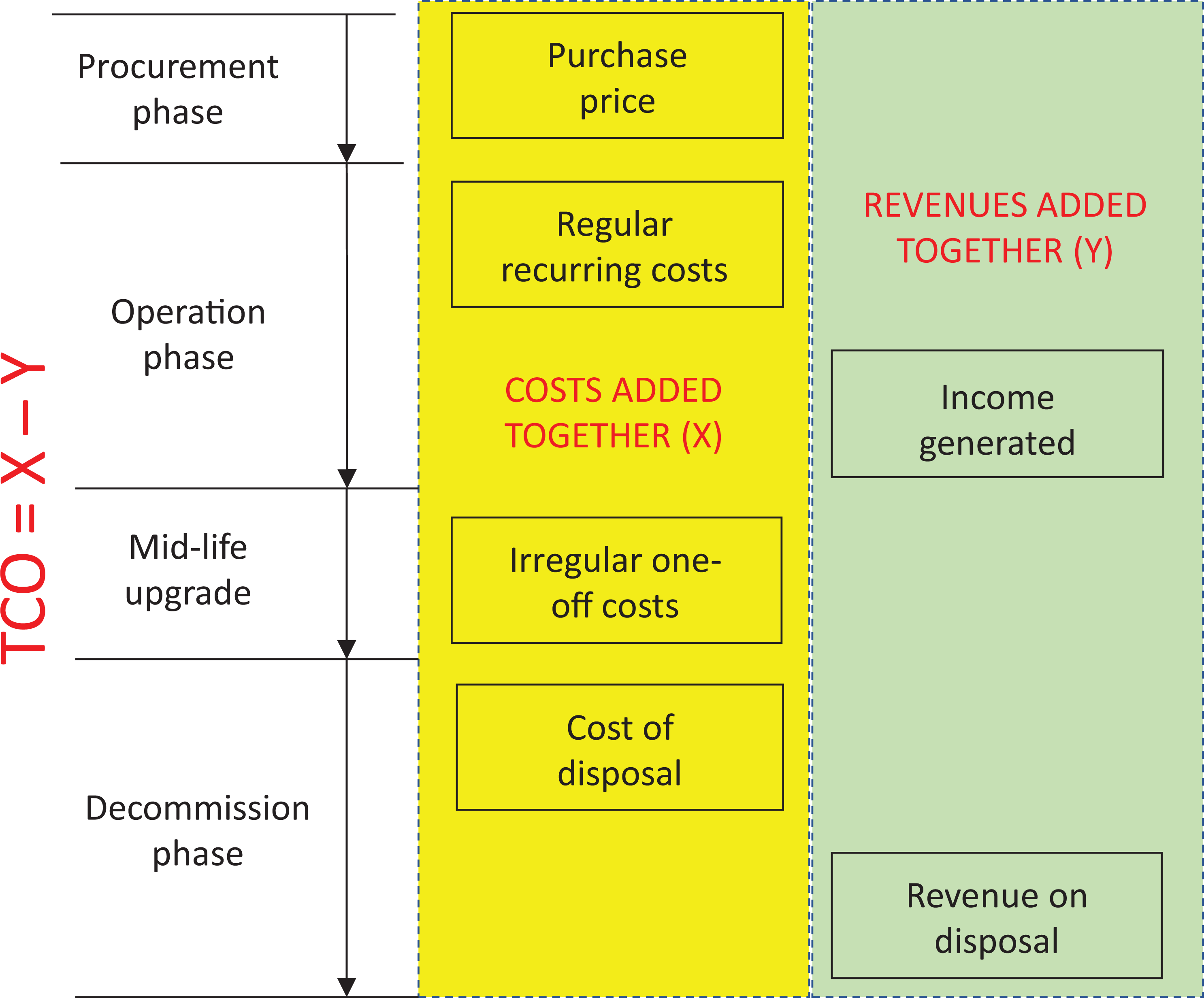

Boudreau and Naegle 71 represented TCO as a set of ‘costs as independent variables’ (CAIV). The variables are distributed in distinct phases along a life cycle time line (Figure 1).

CAIV TCO model.

The focus of CAIV is to establish cost targets based on affordability and requirements and then to manage to those targets, thereby controlling TCO. This model presents a high-level representation of sustainment activities in three phases. Therefore, we propose to adopt this model but further enhance it with the following details:

In the decommissioning phase, cost of decommissioning will be mandated to be included and appropriate funding should be retained and inflated from present value.

System upgrades and changes (due to adjusted operational requirements) are major sustainment activities that are difficult to forecast. Sufficient budget should be allocated, with reference to past experience in other comparable assets for the mid-life upgrade phase.

Operation phase is the time when the asset is put into regular wear-and-tear scenario. Costs related to management and usage of spares will be costed according to recommended spare parts reliability data.

Hence, the TCO model defined in this research can be represented by equation (1):

where A = Purchase price − one-off payment to the seller for acquiring ownership of the asset. B = Regular recurring costs − expenditures that are required to operate, maintain, adopt, support proper use of the asset while in possession. C = Irregular one-off costs − expenditures that are used to upgrade or make engineering changes for new application of the asset. D = Cost of disposal − expenditures that are required to prepare decommissioning and final disposal of the asset (with due consideration on environmental impact).

These costs are offset by two possible revenues: E = Income generated − through contractual agreement to secure payment for efficiency, bonus meeting target indicators, sharing of cost savings. F = Revenue on disposal − income by scrap sale or reusable components on the asset.

All cost items are discounted as present value.

The CIAV model has the advantage of being generic and can be expanded hierarchically to incorporate the essential features of TCO in Table 1. The relationships of the generic categories are also defined in equation (1). This definition is an essential step to form the foundation of subsequent process design analysis.

Sustainment activities will span over years. To understand what analysis could be done on sustainment processes, we examine literature on process improvement. Pearce et al. 72 used TCO to represent the sum of present value of all direct, indirect, recurring and non-recurring costs incurred over its anticipated life cycle of a facility, infrastructure or assets. The Capability Acquisition and Sustainment Group of the Department of Defence 73 in Australia developed a programme requiring the contractor to monitor and report on productivity improvements arising from optimisation of existing work practices, processes and procedures. Consequently, contractors were forced to establish continuous improvement programme in order to compete for the contract.

Moreover, TCO computation becomes complicated when these service activities require responsibility sharing of many suppliers, where each participant in sustainment activities had their own standard operating processes. Bacchetti et al. 74 applied TCO calculation to a highly energy-intensive equipment, an aluminium melting plant. Their TCO model showed that the capital expenditure incurred by the seven companies under investigation accounted for only 3–5% of TCO. To reduce the complexity of sustainment processes in the product’s life cycle, it would be much better to use more expensive, large size, centralised but energy efficiency furnaces. Degraeve et al. 75 computed TCO for a company to exploit different procurement options.

In terms of what to do for supporting decisions on business process reengineering, Choudhari and Gajjar 76 proposed that computer-based simulation could be used as a tool for manpower planning in maintenance services. Alabdulkarim et al. 77 developed a discrete event simulation model to mimic complex maintenance operations with different monitoring levels (reactive, diagnostics, and prognostics. Computer-based simulation has been proved to be one of the most effectiveness analysis methods for supporting decisions in designing manufacturing systems, particularly those with intelligence built into decisions of individual machines. 78 Parameters such as arrival rates or service intervals were modelled, giving insight into process bottlenecks and suitable alternatives.

Adoption of simulation analysis conforms to the stochastic cost analysis done in some literature as shown in Table 1.

Hence, the following systematic approach is adopted in our case study: The baseline contractual requirements are established from data stipulated in the sustainment contract. These data include personnel, organisation structure, expected cost items (classified according to sustainment TCO model), problem reports (historical data). These data are used in the simulation model to establish a comparative baseline for next steps. The processes for carrying out sustainment activities are analysed. Deficiencies of the existing system are identified. New processes are proposed and the effect of change is simulated. Once the new processes are proved successful from simulated TCO outcomes, further change is made to optimise the sustainment system. The new system is also simulated to see how significant the effect can be.

The simulation software used in this research is ARENA. 79

Establishment of baseline scenario for the case study

The sustainment activities-oriented TCO model has been applied to evaluate a sustainment contract in defence industry. This project has been managed by one of the authors. Due to confidentiality reason, the information presented in this paper has been sanitised so that the project itself cannot be identified, but the characteristics of the project for TCO analysis remains intact.

The case study baseline scenario consists of 50 personnel responsible for delivering the defined engineering support and sustainment activities. The team is made up of the following disciplines providing the core services defined under the contract.

Managers (Project, Hardware, Software, ICT, Systems and Installation)

Systems Engineers

Hardware Engineers

Software Engineers

Communication Engineers

Logistic Engineers

Installation Technicians

Senior Design Engineers

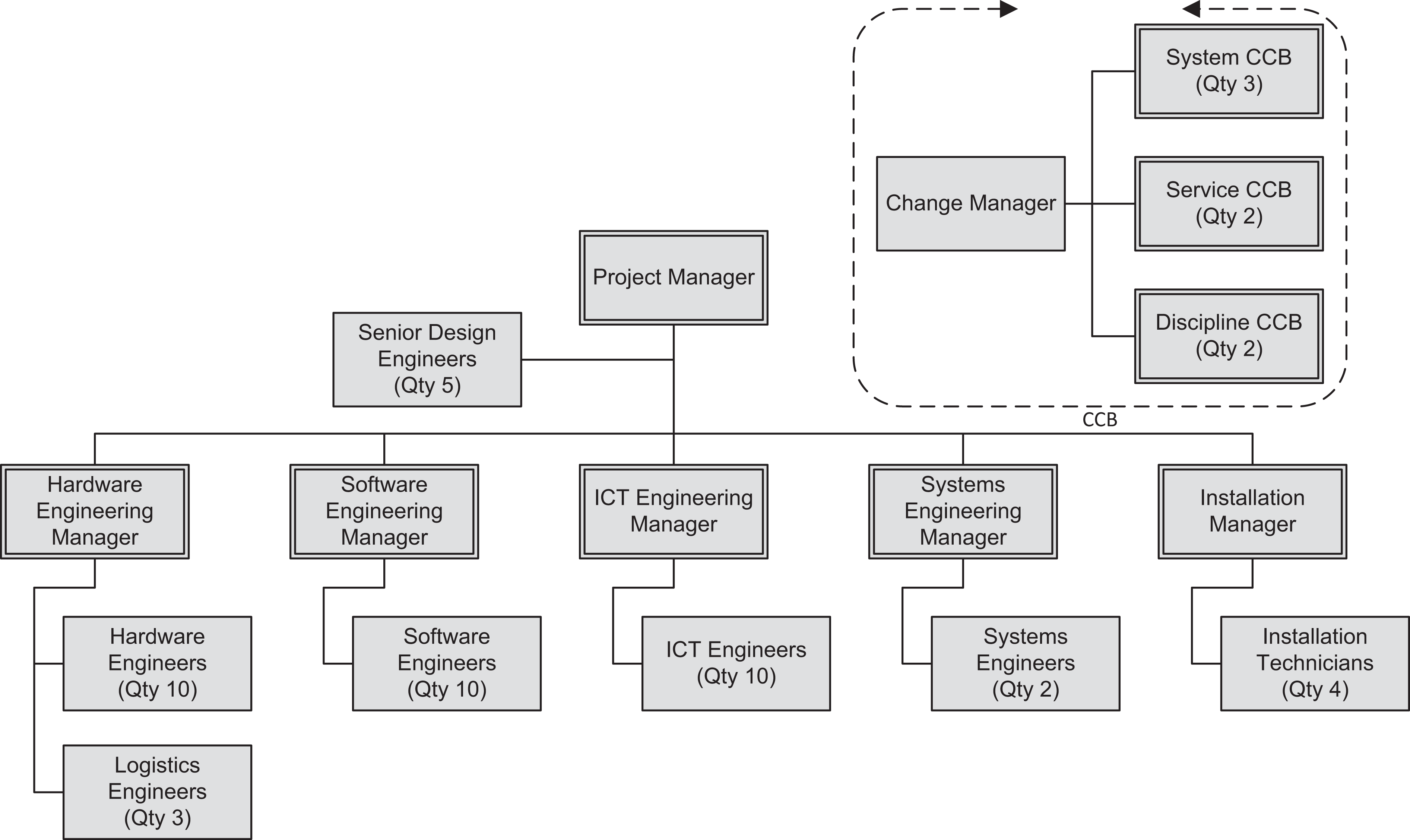

The team’s organisational structure is shown in Figure 2.

Engineering sustainment organisation.

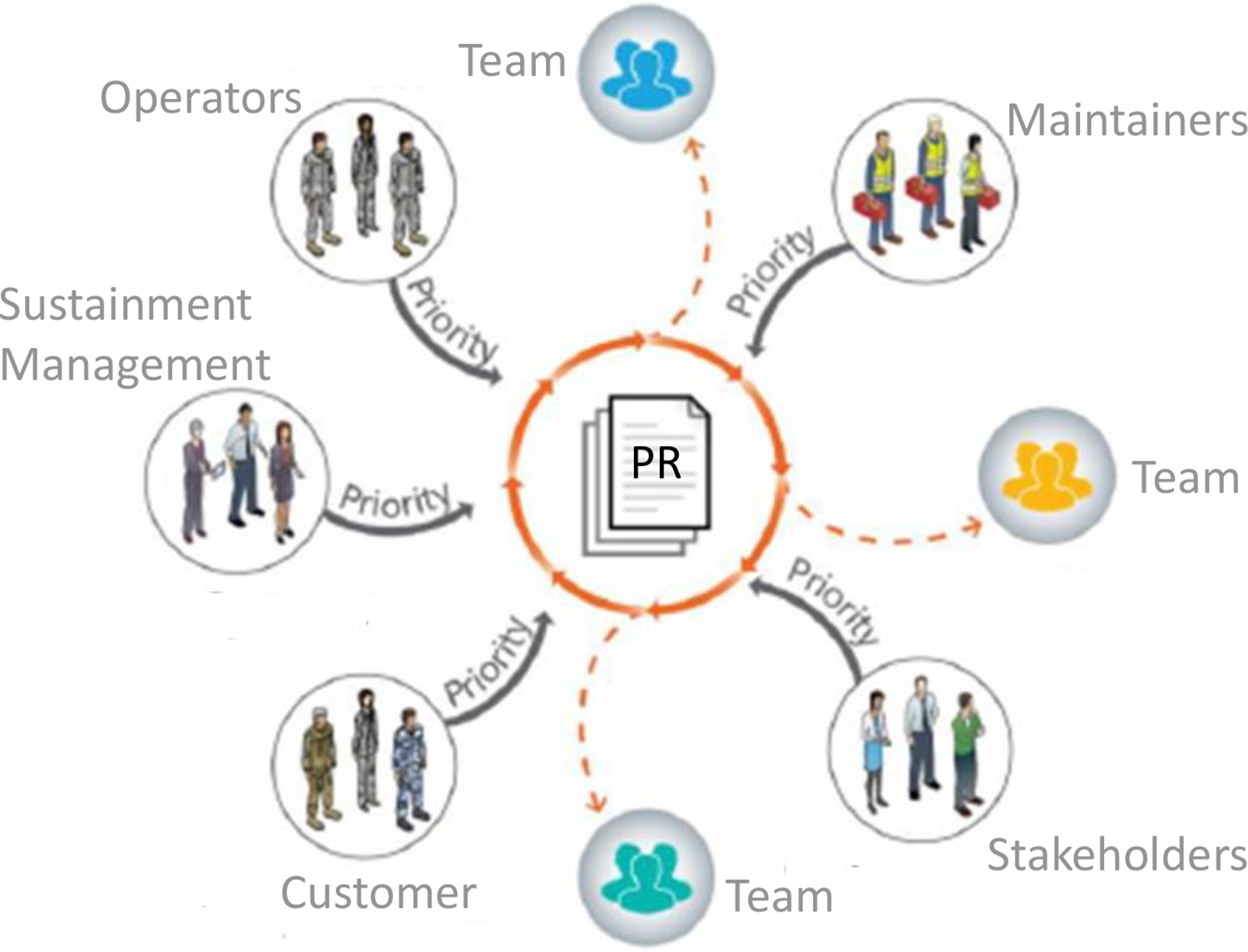

Each of the personnel branches in Figure 2 (under a manager) is a ‘team’ capable of carrying out sustainment activities on its own, or in collaboration with other teams. The existing process for handling engineering change activities on the asset can be described as ‘scattered competing priorities’ process allocating tasks to these teams (Figure 3).

Existing process for handling activities arising from problem reports.

Sustainment activities are initiated by any of the stakeholders (customers, sustainment management, operators, maintainers, other stakeholders) filing a Problem Report (PR). All PRs are treated ‘with priority’, in effect, equal priority in the system. Coordinated by the Project Manager, the PRs are allocated to one of the teams.

Figure 4 shows the steps through which the PRs are acted upon to completion. The assigned PR may sit in a queue until a resource (primarily an engineer with the right skills) is available to work on it. The resource completes a PR Investigation and reports to an Engineering Review Board (ERB) for approval of proposed work. There are several review points, particularly for sustainment works that require redesign of components, e.g. due to new usage or obsolete spare parts. The PR may be required to undergo rework, before it is eventually approved and accepted for installation/integration. The process and decision points are input into ARENA as the PR process model with timing and resources uncertainty data for simulation.

Process flow of PRs through ERB and engineering approvals.

The time that the PR takes to traverse the workflow is defined as the Time in Work and the PR Completion Rate is defined as the number of PRs completed per day. Based on the numbers of hours a PR takes to traverse the workflow, an associated cost per PR can be established. For setting up simulation analysis, the following parameters are quantified and reported:

Number of PRs completed per year

Average PR Time in Work

Resource utilisation

Total process cost

PR Cost

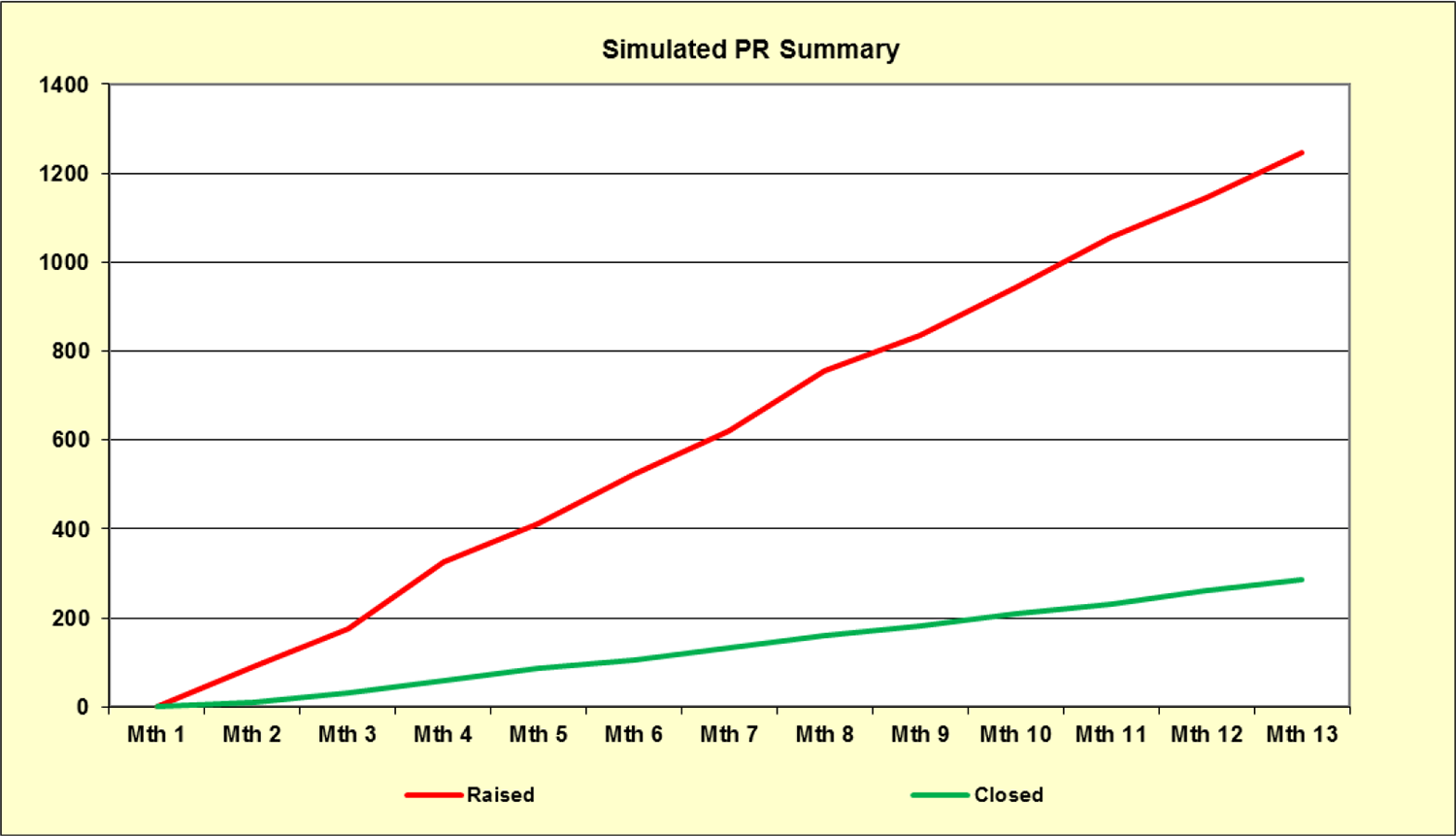

Statistics collected in the first 12 months of a similar sustainment contract showed that the rate of new problem reports (PRs) far exceeded the rate that PRs were completed and closed out (Figure 5). This means completion of PRs could not keep up with the demand for solution to problem reports and resulted in a huge backlog of problems that were not solved in time. This is a problem that will be investigated in step 2 of our systematic approach.

Real-world PRs in a similar sustainment contract.

To convert the real-world PRs data into the simulated environment, the number of PRs raised per month was used to create a histogram. These were entered into the ARENA Input Analyser and fitted to a Poisson process as input probability of a PR entering the sustainment system. The output of simulated input PRs is shown in Figure 6. By comparing the real-life data to the output of the simulation model, it can be seen that the model represents the trend of real-life PRs data reasonably well.

Simulated input PRs over the sampling period.

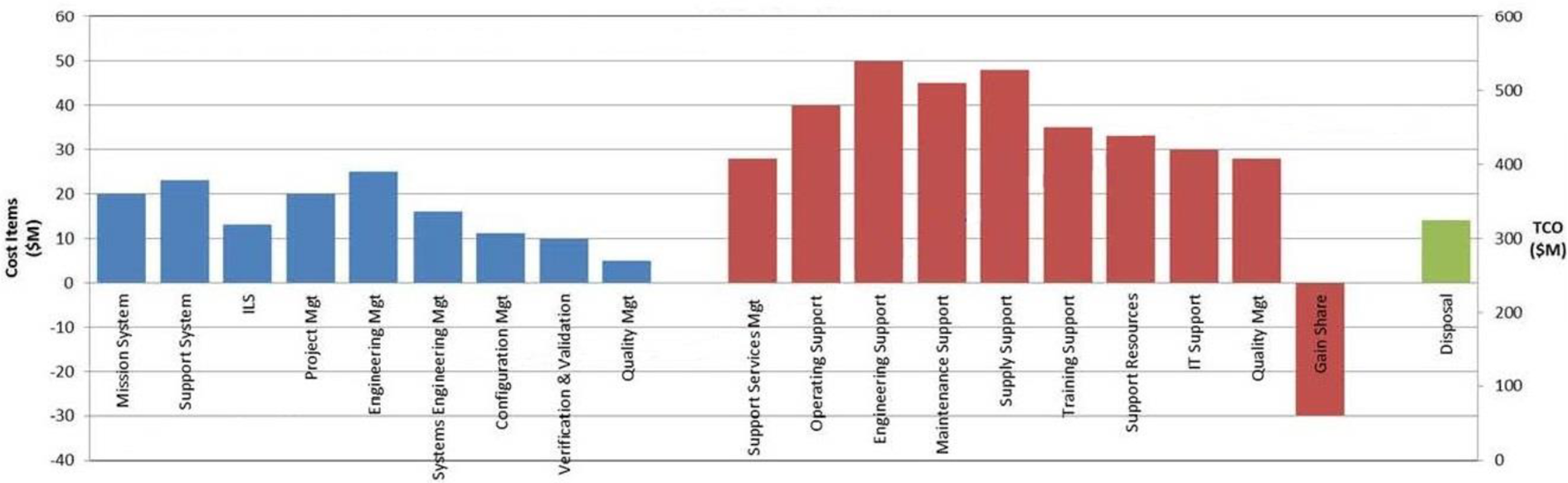

The case study sustainment contract has a period of 24 years, based on a team of 50 personnel as shown in Figure 2 and nominally costing $100 per hour per resource. The sustainment activities included in the simulation can be summarised according to the six types of costs outline in equation (1) as shown in Figure 7.

Sustainment activities cost types (in million $).

Further examination into the sustainment activities in different phases, cost items can be identified from the Statement of Work of the sustainment contract. Figure 8 shows detail breakdown of the TCO cost items. Purchase price, income generated, cost of disposal, revenue on disposal are independent of time. They are one-off expenditure (or income) either at the start or end of asset life. On the other hand, the regular recurring costs and irregular one-off costs (spread over interval years during the asset’s service life) are affected by consumer price index and value discount over time. In addition to this, the Income Generated is estimated in conjunction with the customer in consideration of contractual mechanisms, such as painshare, gainshare, efficiency bonus. Similarly, the cost of preparing the asset for disposal needs to be estimated with experience of other similar defence assets.

Sustainment activities cost items (in million $).

Figure 9 shows the annual TCO of the asset over 24 years of sustainment contract period. An escalation rate, i.e. salary adjustment, of 2.25% per year has been applied. The TCO for this scenario is $358 M. The NPV can be calculated to give the TCO in today’s dollars. Assuming a discount rate same as the escalation rate of 2.25%, the TCO is calculated as $276 M.

Engineering support annual TCO model.

Performance data collected from the simulation run are shown in Table 2.

Baseline process simulation summary.

The queue data from simulation showed lead times for different detail processes are: Build Approval (49 days), Design Approval (48 days), Product Approval (49 days). These long waiting times conformed to the many user complaints that their problems were not attended to urgently. The Resource Utilisation data also showed high utilisation rates of Engineers, Managers and System Design Engineers (SDEs). These queues and the corresponding resource set represent the bottleneck in the system, which reflects why the Technicians have lower utilisation. Along with this, the process is considered expensive, which must be reduced in order for this service business to be competitive.

Process improvement investigation

The key to improve this case is management of PRs. Table 2 shows that the resources (engineer, managers, SDEs) are overloaded (almost 100% occupied all the time), whereas technicians have a lot of spare time. It is crucial to redesign the processes so that workload of the expert resources is reduced. A method suggested was the implementation of a triage process for PRs. The triage process has been commonly used in medical applications where patients are screened for their case urgency and treated with different priority. 80 Based on survey in medical applications, the triage is a reasonable solution for wait queue management. 81 This research therefore considered the same principle re-structuring for the basic starting point of sustainment activities, i.e. process of handling problem reports.

The triage process included prioritisation and assignment of workflows that are tailored based on scale and risk of the problem and its possible resolution. The process design rationale is to reserve critical resources to PRs that need their skills most. The process flow is illustrated diagrammatically in Figure 10.

Redesigned sustainment process for handling problem reports.

To implement this process, a position, Change Manager, is added to the sustainment organisation. The Change Manager will perform an initial analysis of all PRs and include the following responsibilities:

Identifying whether the proposal is an engineering issue

Performing initial Judgement of Significance (JoS)

Determining the type of change – critical, routine or non-routine

Identifying the system or discipline lead responsible for further development of the change.

Three Configuration Control Boards (CCBs) are also established to replace the single ERB. JoS (role 2 of Change Manage) determines how the PRs are assigned to the relevant CCBs according to their severity and effect on the system. For example, the System CCB manages all PRs assigned as Major. The Service CCB manages PRs that only affect specific services but not extending to system level operations. These PRs are classified as Minor. The Discipline CCB manages PRs that only affect specific Engineering Disciplines but not requiring one-off special changes. These PRs are classified as Routine. As a result, the case study baseline scenario is updated to include the position of Change Manager, as well as the establishment of the CCBs (Figure 11).

Redesigned organisational structure for the triage process.

To understand possible performance outcome of the new process, a process model is created in Figure 12. When a PR is raised, it is routed to the Change Manager who undertakes the tasks under the new process organisation. The PR is then routed to the relevant CCB depending on the assigned initial priority.

Model of the new process handling engineering change.

The key difference in this new process is the introduction of a triage streaming process that sparks three alternate workflows to most appropriate work teams. Each of the change workflows is modelled in detail to allow respective PRs to be simulated

Major change workflow

The Major Change Workflow is invoked for PRs that have a significant effect on the existing system baseline and requires approvals from the SDE, as well as acceptance from the customer. Figure 13 shows the detail Major Change Workflow process.

Detail of major change workflow process model.

Minor change workflow

The Minor Change Workflow is a cut down version of the Major Change Workflow process in that it removes the need for product acceptance from the customer (Figure 14). This is relevant for changes where there is an agreed condition of design acceptance delegated from the customer. This applies to PRs that are not implementing functionality required by a customer-initiated project, have a JoS determination of non-significant, do not have any identified safety implications and are not representing a major system build or new capability. This is a key enabler to a responsive and agile process to satisfy customer’s need quickly.

Detail of minor change workflow process model.

Routine change workflow

The Routine Change Workflow is severely cut down from Major Change Workflow process and only includes Component Development and Design Approval prior to the PR being implemented (Figure 15). This process is used for rapid changes such as network scripts or document updates to non-design related technical documentation.

Detail of routine change workflow process model.

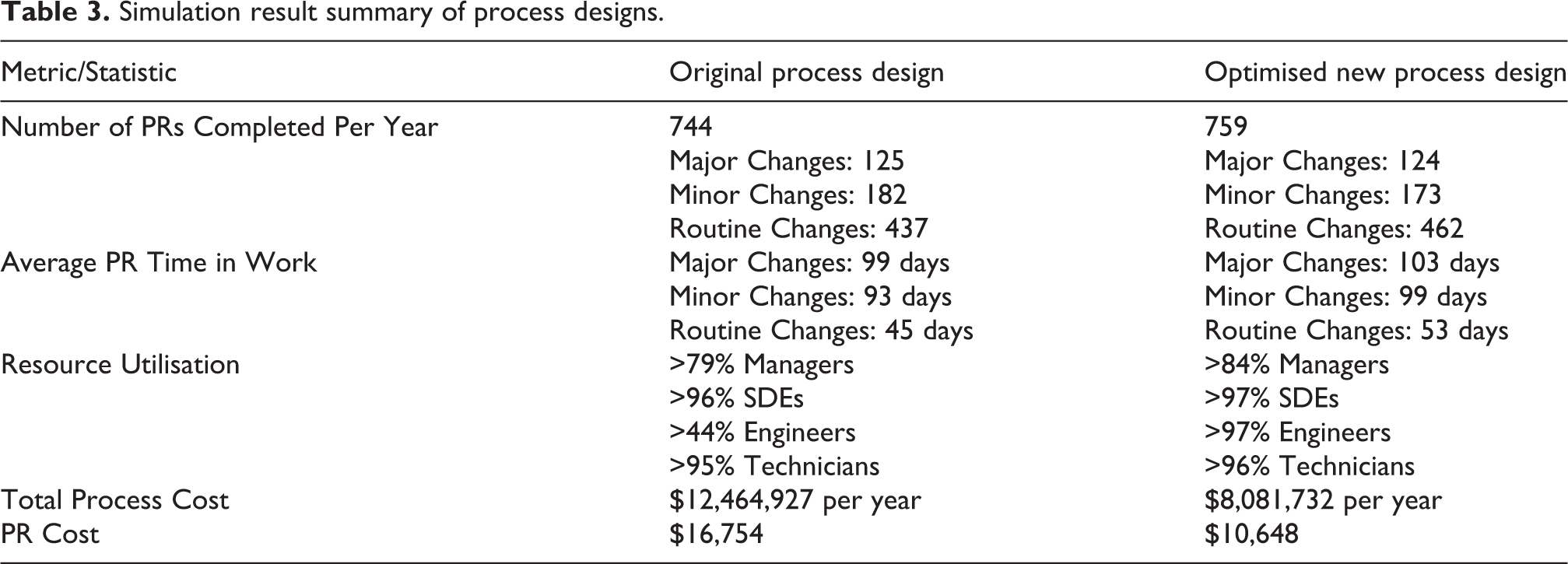

The question arising from this new process is: does it make the system more efficient? The model of the new process was simulated and produced results in the column heading ‘Original process design’ in Table 3. Please note that the column heading ‘Optimsed new process design’ will be discussed in next section ‘Optimised new process simulation’.

Simulation result summary of process designs.

What is interesting about the results is the two types of process cost. The Busy Cost is $6,849,590, with the Idle Cost $5,615,337. This corresponds to the utilisation of the resource Engineers, which is quite low at 44%. This demonstrates that there is sufficient capacity that can be capitalised on. This capacity provides the following options:

To deal with scenarios where the rate of incoming PRs increases, due to unexpected system faults or obsolescence

Headcount can be reduced to reduce TCO

Given that the SDEs are almost at capacity at 96%, an increase in PRs is not going to be possible. This suggests that a reduction in headcount is a possible way to maintain the current throughput and at the same time reduce TCO.

Optimised new process simulation

To find if the TCO can be reduced, the organisational structure and specialty in different work teams are examined. A slightly reduced headcount organisational structure as indicated by the downward arrows (next to the functional personnel box) as shown in Figure 16 is adopted. The system with the triage process is then simulated with the same PR inputs.

Reduced headcount organisational structure.

The new simulation run result with reduced personnel within the sustainment organisation is shown in the column heading ‘Optimised new process design’ in Table 3.

As can be seen by the metrics captured in Table 4, utilisation of the Engineers has been increased to 97%, which has resulted in the Idle Cost being reduced to $1,188,155. Also, by reducing the headcount, the overall cost has been reduced to $8,081,732. To go along with this, the number of completed PRs has been increased to 759 per year, leading to a reduced average PR cost of $10,648. The metrics indicate that the optimised process is operating very efficiently in comparison to the baseline and the initial triage processes.

Using the optimised triage process model, the TCO for the new sustainment process can be calculated. As shown in Figure 17, the net cost per year of the case study sustainment contract with a period of 24 years, and based on the reduced headcount organisation, the TCO for this scenario (using an escalation rate of 2.25% in base date dollars) is $265 M. The NPV value (discount rate same as escalation rate) is calculated as $206 M.

Sustainment contract analysis annual TCO model (reduced headcount).

It is further noted that comparing the results to the Baseline Process, the New Optimised Process has savings of 26% and 25% respectively as shown in Table 4. This level of savings is enormous.

TCO summary.

Discussion

The primary case study investigation in this paper is based on a defence asset (in billion dollars). Strictly speaking, some researchers may classify this analysis as ‘operation management through performance evaluations’. This classification can be either real-time, i.e. monitoring performance outcomes on a real-time basis, or, like this paper, analyse possible performance outcomes in a simulated environment. The need for computer simulation is that the sustainment contract is long duration, i.e. 24 years in the cases study presented here. Technologies employed in this asset are high-tech electronic and telecommunication systems. These equipment can become obsolete quickly, typically every 5 years. In 24 years, there are at least four cycles in which engineering change activities need to be done to upgrade the system to meet latest functional needs.

On the contrary, other types of asset have different length of life cycles. For example, upgrade of buildings will probably occur less frequently. However, irrespective of whether the building is old and classified as historical, new technological improvements are still necessary from time to time, probably every 10 years and with lower degree of alterations. Furthermore, building structures last much longer than 24 years. Future sustainment costs are even more unpredictable. The need for stochastic simulation to get a feel of what the TCO look like can be even more critical when deciding engagement of certain sustainment service providers. The methodology in this paper is definitely applicable to analyse the situation well.

The thorough literature review presented earlier leads to the adoption of a special sustainment-oriented TCO model. From academic’s perspective, this research process has allowed us to document how our keyword search can lead to research papers that give us hints on what are included or not included in sustainment TCO. However, computational details still require carefully investigation into specific papers. Subsequently, the research has demonstrated that by using a specially constituted TCO as a measure for long term sustainment contracts, process improvement analysis could be driven from a range of associated simulation outcomes. For example, analysis of the utilisation level of resources was demonstrated as a clue leading to introducing different PR handling processes so as to better utilise critical resources. There is slight increase in overhead for the sustainment team in this case study but the savings as a result of better use of experts to complete more important PRs is obvious. Intangible outcomes such as better customer satisfaction (faster problem solving) and reduced personnel costs without scarifying efficiency are also achieved. This finding has helped us to understand the characteristics of TCO based performance indicators can be used in analyses of real-world and simulated environments.

Judgement of success in the sustainment system is difficult without quantitative proof. It is not possible to carry out a ‘small scale’ physical experiment of sustainment work to gauge performance of sustainment contracts. Simulation approach has used in many researches of asset types but application to sustainment activities is difficult without a relevant sustainment TCO model to accumulate performance metrics. Building a process model, capturing past data and convert into simulation run inputs are not trivial. The case study has its special feature (such as use of real-world PR data) that may not be repeated in other sustainment contracts. However, future researches in this area should still be able to find the alternative triggering input to the simulation package. The challenge for the case study organisation is to implement simulated results in reality.

Conclusion

This paper explored answers to two questions:

Is TCO an appropriate performance indicator to be used in assessing sustainment contracts?

How can TCO be applied to drive the design of sustainment system for better ‘value for money’?

Answers to these two questions represent novel contribution to knowledge supporting evaluation of long term sustainment contracts.

For question 1, selection of an appropriate TCO model is critical to this analysis. A special sustainment-oriented TCO model using CAIV costing as the basis, supplemented with NPV computation, and adapted PR distribution function as input to the simulation run has been adopted. By thorough literature review in this paper, a more comprehensive list of cost and revenues items characterising TCO models has been established. In particular, the cost items resulting from sustainment activities can be collected from performance data of the sustainment system, in the form of number of completed PRs (jobs entering the system), utilisation of resources and different types of costings. The quantified outcomes become vital proof and form the basis of evaluating the process that governs cost-effectiveness and efficiency of long term sustainment contracts. Decision makers can then drive for more fundamental changes to the sustainment system.

For question 2, this research has combined support data in the initial period of the sustainment contract with potential variations that are unique in sustainment work. By a systematic step-by-step approach, the sustainment system process has been redesigned in order to achieve significant savings in TCO as well as improving other non-financial performance indicators. Once the model is created, the processes governing sustainment activities with different resources implication scenarios, TCO can be used as an objective function to examine and drive changes in sustainment process design. The savings computed in this research are indicative of the power of evaluating TCO. The need to extend the analysis objective to cover the duration of all sustainment activities necessitates simulation to be used with realistic industry experience and data. This systematic approach has not been found in other business process analyses of asset sustainment contracts

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.