Abstract

To maintain competitiveness, businesses need to upgrade their operational performance and financial performance more efficiently and effectively in order to control uncertainty and costs. The purposes of the study are to (1) investigate the relationship between three dimensions, namely integration, flexibility, and performance; and (2) examine the mediating effects of supply chain flexibility. This research collected annual reports from the Indonesian basic and chemical industry from 2014 to 2017. Content analysis was used to extract information from companies’ annual reports, and hierarchical analysis examined the hypotheses. The results show that external information integration positively influences both reactive and proactive flexibility. Furthermore, proactive flexibility significantly affects financial performance and operational performance. Moreover, both reactive and proactive flexibility have positive mediating effects on the connection between external information integration and operational performance. Lastly, reactive flexibility positively mediates external information integration’s effect on financial performance. As the market has been becoming more competitive, this study provides important insights for decision-makers. This study contributes to the knowledge of the Indonesian basic and chemical supply chain by considering both financial and operational performance, especially as these performance indexes measure different dimensions.

Keywords

Introduction

Globalization leads to market volatility. 1 This is caused by the interrelations among countries’ economies, whereby the economic conditions in one country can affect those in other countries. International businesses or trade practices are those most directly impacted by unpredictable market changes. During cross-border transactions, political conditions, technological development, business culture, and business communications are considered. 2 Furthermore, fierce competition also forces firms to synchronize operations such as supply, production, and marketing internationally. 2 Therefore, knowledge of how to design the supply chain strategy has become crucial in helping firms stay competitive. The supply chain can be defined as the linkage among value chains. 3 A firm with effective supply chain capabilities can significantly help decision-makers to anticipate problems, and to find a dynamic solution when the problems have already occurred. 4 Therefore, firms need to be flexible in their supply chain in order to quickly respond to problems arising from the market. 5

According to Vickery et al., 6 supply chain flexibility (SCF) is the combination of supply chain management (SCM) theories and an added “flexibility” dimension. In the supply chain field, the term “flexibility” is the ability of firms to enhance their supply chain effectiveness, and thereby boost their performance. 7 Some studies found that firms need SCF to stay competitive under market uncertainty by enhancing the company’s financial performance and operational performance. 8,9 However, before developing effective SCF strategies, firms in the supply chain have to share the information and standardize the operations process. Swink et al. 10 stated that strategic integration could provide managers of how to determine the recipe of flexibility or cost dimensions. Ataseven and Nair 11 found that supply chain integration would influence the performance of flexibility.

There are different interpretations of integration in the existing literature; this has made the definition ambiguous. According to Wang and Wei, 12 vertical integration improves SCF through higher information visibility. Töyli et al. 13 stated that there are two kinds of integrations often used in previous studies: information integration and operation integration. Information integration represents the information shared among supply chain members, whereas operation integration refers to the collaborative activities in the work processes. 14 Blome et al. 8 defined integration as internal and external knowledge transfer, which positively affects SCF. For both information and operation integration, the key is to have effective communication through the sharing of information internally and externally. Therefore, in this study, we focus on information integration and divide the term into external information integration (EII) and internal information integration (III).

Resources and capabilities are essential for companies’ effective SCM. 15 The resource-based view concept (RBV) can be seen as a suitable structure for investigating organizations’ pathways for obtaining sustainable competitive benefits, by focusing on their resources and capabilities. 16 We distinguished SCF into two terms, which are reactive supply chain flexibility (RSCF) and proactive supply chain flexibility (PSCF). RSCF refers to how the company adjusts to the changes in the external environment. 17 On the other hand, PSCF is defined as how a firm uses its resources and capabilities to influence external environment expectations, and how the particular industry should fulfill them. 18 Thus, determining how companies respond to market uncertainty, whether through PSCF or RSCF, should be based on the elaboration of RBV. 19 Higher SCF in a company would result in better operational performance because the firms would have a better ability in adjusting to (reactive) and predicting (proactive) market uncertainty. 14 A quicker response to the market also results in better operational performance, which in the future will enhance both the firm’s operational and financial performance. 20

Although a body of researches has focused on the relationship between integration, flexibility, or even capability and complexity, few studies specified both types of information integration (EII and III) and SCF (RSCF and PSCF). Furthermore, taking into consideration both operational and financial performance in the analysis which lacked in the previous research would add beneficial insights to the existing literature. Thus, this research provides an extended framework for the stream of relevant research. This research has several objectives. First, it investigates how EII and III affect PSCF and RSCF. Second, the study examines the influence of supply chain flexibility (PSCF and RSCF) on companies’ operational and financial performance. Last, it identifies whether PSCF and RSCF can mediate EII and III in companies’ operational and financial performance.

This research makes two contributions. First, we provide meaningful insights for the existing stream of research by exploring the association between the different dimensions of information integration, flexibility, and performance in the Indonesian context. Second, we clarify the strength of the linkages between information integration, flexibility, and performance, which are unclear in previous studies.

The remainder of the research is organized as follows: Section 2 discusses the related research and the research hypotheses. Section 3 comprises the data collection procedure and research methodology; then, section 4 presents the results and discussion of this research. Conclusions, research limitations, and suggestions for further research are stated in Section 5.

Literature review and conceptual framework

Supply chain information integration (SCII)

The elements of business process integration form parts of the SCM; these include services, provision of products, and information that adds value for stakeholders. Such integration occurs from the design to the delivery process, starting from suppliers through end customers. 21 SCII is a concept of connecting and redefining objects through information sharing. 22 Moreover, SCII takes place during data transactions, so that supply chain allies can enable inter-organizational and intra-organizational information-sharing strategies. 23,24 Knowledge and information sharing are usually defined as intangible resources 25 ; these are critical players for integrating two-way information flows. 23,26

SCII mainly includes two dimensions, known as III and EII. 14,27 –29 III and EII represent different roles in the context of SCII. III denotes the degree to which companies can arrange their organizational activities into cooperative, synchronized, and controllable procedures, to satisfy customers’ demand. 30,31 Based on the resource bundling point of view, this is the use of information systems to exchange real-time information, such as inventory or transportation status, for intra-organizational purposes. 32,33 By facilitating the information exchange across different departments, a joint decision on product design, process management, and manufacturing planning can be made if there is sufficient time and money. 34 Therefore, the purpose of III is to enable departments and functions within a company to exchange standardized information for better operations management.

By contrast, EII emphasizes the development of close and interactive relationships upstream and downstream in the entire supply chain; it is the degree to which corporations can collaborate with key supply chain partners externally. 35 Suppliers would be involved in the product development phase, by providing the capability, quality, and cost of the manufacturing process. In addition, customers can provide feedback on product features, pricing strategies, or other inputs. Thus, the benefits, including cost reduction, customer satisfaction improvement, quality enhancement, and lead time reduction, can be generated from integrating the information from suppliers and customers. 36 Both perspectives are critical in allowing supply chain partners to act collaboratively, and to maximize the value of the supply chain. 37

Supply chain flexibility (SCF)

SCF is one of the important elements for creating or preserving a competitive advantage. 38 Swafford et al., 39 explained that the degree of flexibility present in the manufacturing and distribution/logistics processes significantly impacts the supply chain agility of a firm. Five components of SCF can be identified, namely: volume, product, distribution, access, and new product introduction. 6 Moon et al. 5 summarized SCF as sourcing, operating system, distribution, and information flexibility. To achieve a flexible supply chain, Stevenson and Spring 40 provided a comprehensive review and summarized five components that should be included: grid flexibility, re-configuration flexibility, active flexibility, potential flexibility, and network alignment. Although previous studies have provided different definitions of SCF, ultimately it can be explained as how quickly the supply chain reacts to demand and the business environment. 41

SCF is correlated with activities such as facility structure management, transportation management, material handling, and inventory management. 42 Moreover, flexibility is the capacity to make modifications when there is a lack of information from complicated and uncertain business environments. 43 SCF also covers dimensions which include the shared responsibility for multiple tasks along the supply chain, and which indirectly influence companies’ clients through aggregated supply chain agility. 44

The relationship between SCII and SCF

The relationship between SCII and SCF has been examined by numerous studies; however, the consistency of the results was not identified. Internal integration, which denotes the intra-organizational infrastructure for information sharing, requires the adaptive capabilities of organizations to enable information sharing and processing. 45 Wong et al. 46 argued that a higher degree of external integration would lead to better delivery and production flexibility. Juneho 47 revealed that internal management strategies and external supply chain integration positively affect flexibility and agility. Although scholars have stated that EII affects SCF positively. 12,14 , Chaudhuri et al. 48 found only internal integration affects SCF. Therefore, we argued that information integration would affect different dimensions of flexibility (passive and reactive). In addition, We examine both passive responses and reactive responses of organizations are sufficient measures of how they react to the dynamic external environment, in order to achieve sustainable competitive advantages. Therefore, we hypothesize that:

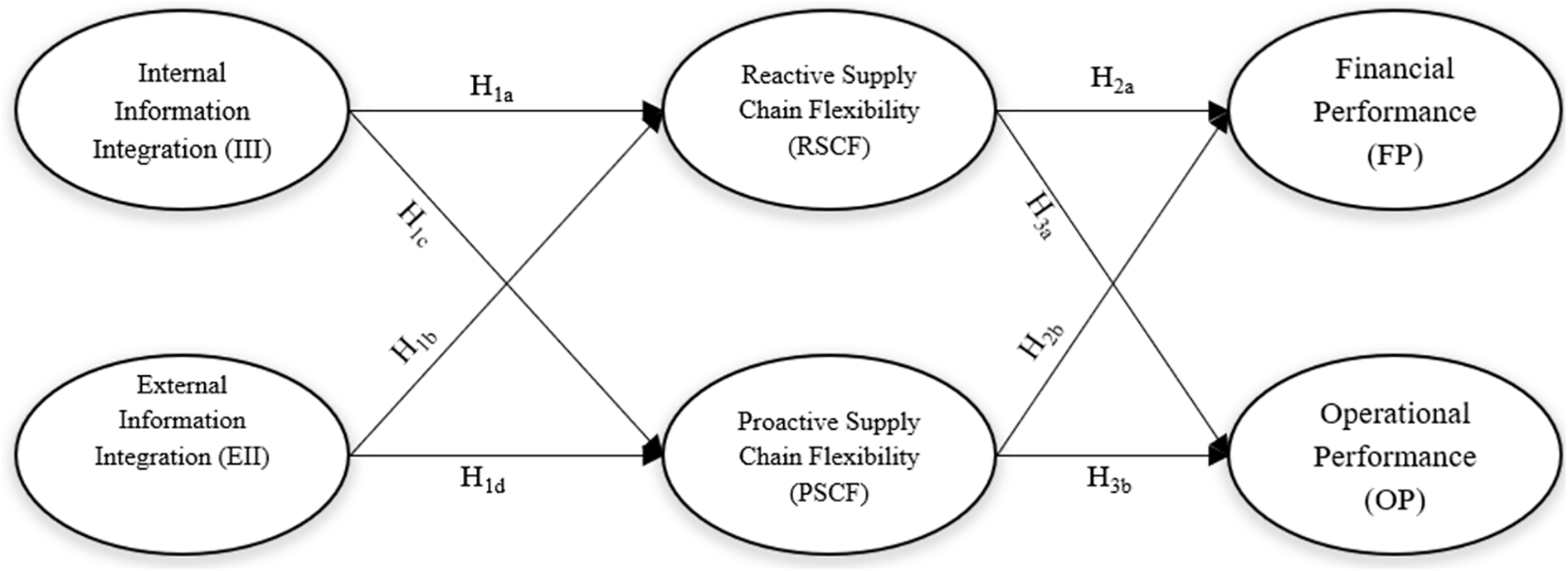

H1. SCII positively influences SCF: ▪ H1a: Internal Information Integration (III) increases Reactive Flexibility (RSCF). ▪ H1b: External Information Integration (EII) increases Reactive Flexibility (RSCF). ▪ H1c: Internal Information Integration (III) increases Proactive Flexibility (PSCF). ▪ H1d: External Information Integration (EII) increases Proactive Flexibility (PSCF).

The relationship between SCF and supply chain performance

The capability of flexibility refers to the adoption of market changes and usage of the firm’s ability to precisely align internal resources with external demand. 49 This highly depends on the dynamic scanning of the external environment and involves a widespread exchange of information. 50 Therefore, SCF is correlated to internal resources such as operations, human resources, and information technology. 51

Gunasekaran et al., 52 explained that SCF is sometimes considered an index of firm performance. Performance is to measure how a corporation achieves the strategies efficiently and effectively. 53 Supply chain flexibility can lead to firms’ revenue growth, thus confirming that supply chain flexibility is a key component in the sustainable business strategy. 54 Firm performance (also called organizational performance) usually contains six dimensions, namely: Return on Investment (ROI), market share, the growth of ROI, sales, profit margin on sales, and overall competitive position. 55 A flexible supply chain should lead to higher profit margins and/or increased market share.

Nevertheless, companies should also take outcomes other than financial performance into consideration. Al-Tit 56 summarized the dimensions of organizational performance and identified three dimensions, named sales-based performance, organizational-based performance, and supply chain-based performance. These dimensions should be ultimately categorized into financial and operational performance. Angel and Perez-Perez 57 argued that SCF is correlated with meeting special customer specifications, decreasing the risk of out-of-stock, and reducing uncertainty in the production process. These improvements are correlated with operational efficiency, which is the productivity of an organization’s operations in obtaining the largest revenues (outputs) with limited resources (inputs). 14 Although flexibility can solve uncertainty problems, one of the ultimate goals of a company is to optimize its operational efficiency. 58 Therefore, we hypothesize that:

H2: SCF positively affects financial performance: H2a: Reactive flexibility (RSCF) positively influences financial performance. H2b: Proactive flexibility (PSCF) positively affects financial performance.

H3: SCF positively affects operational performance: H3a: Reactive flexibility (RSCF) has a positive effect on operational performance. H3b: Proactive flexibility (PSCF) has a positive influence on operational performance.

Previous research has found the positive effects of information integration on supply chain performance. 59 Niranjan et al. 60 indicated that information exchange would affect firm performance only if the relationship is mediated through flexibility. Therefore, We further examine how SCF mediates the relationship between supply chain information integration and supply chain performance.

H4: SCF has a mediating effect on the relationship between supply chain information integration and financial performance: ▪ H4a: Reactive flexibility (RSCF) has a mediating effect on the relationship between internal information integration and financial performance. ▪ H4b: Reactive flexibility (RSCF) has a mediating effect on the relationship between external information integration and financial performance. ▪ H4c: Proactive flexibility (PSCF) has a mediating effect on the relationship between internal information integration and financial performance. ▪ H4d: Proactive flexibility (PSCF) has a mediating effect on the relationship between external information integration and financial performance.

H5: SCF has a mediating effect on the relationship between supply chain information integration and operational performance: ▪ H5a: Reactive flexibility (RSCF) has a mediating effect on the relationship between internal information integration and operational performance. ▪ H5b: Reactive flexibility (RSCF) has a mediating effect on the relationship between external information integration and operational performance. ▪ H5c: Proactive flexibility (PSCF) has a mediating effect on the relationship between internal information integration and operational performance.

H5d: Proactive flexibility (PSCF) has a mediating effect on the relationship between external information integration and operational performance.

The theoretical framework is shown in Figure 1.

Research framework.

Methodology

This section describes the research design that is used to investigate the effect of EII and III, PSCF, and RSCF, on both the operational and financial performance of Indonesia’s basic and chemical companies that are listed in idx.com from 2014 to 2017, by using the content analysis approach.

Research design

Different industrial environments are expected to result in diverse integration practices and flexibility strategies, and these differences might cause inconsistency and bias in the results of empirical testing. Therefore, we narrowed our research sample to Indonesia’s basic and chemical companies. Another reason to select basic and chemical companies is that companies belonged to this sector provide raw materials and manufacture products. As a manufacturing-oriented country, it is beneficial to investigate the relationship between integration, flexibility, and performance of this sector. To test the several hypotheses stated in the previous section, we collected data from firms’ annual reports. There are two benefits of using annual report data. First, most companies disclose critical information about their company for their investors and stakeholders, including information that indicates companies’ information integration, SCF, and operational performance. 61 Furthermore, from the companies’ financial reports, we also can gather information on financial performance; such as from financial statements, notes to financial statements, or companies’ financial ratios. Second, the annual reports also include complete information on companies’ performance in one book period.

As mentioned above, we analyze annual reports by using the content analysis technique developed by Tangpong. 62 Content analysis is the methodology of transforming qualitative information into quantitative information through several coding procedures that have been previously determined. 63 It is an indirect approach to gain information from the subjects being studied; thus, it will not affect the behavior of those subjects.

Data collection procedure

First, we collected the annual reports from idx.com (IDX) and the companies’ official websites. IDX is the official Indonesian stock exchange bureau, which provides the information needed by investors, such as annual reports. The number of annual reports from each year is 53 companies in 2014, 55 companies in 2015, 62 companies in 2016, and 67 companies in 2017; this accounts for 74% of all companies in this sector over the entire period (2014–17). Thus, the total sample consists of 237 annual reports, before the data processing stage. From the annual reports, we extracted the current assets turnover (CAT) to measure the companies’ OP and companies’ profitability ratio (PR); this represented companies’ FP. We also extracted control variables from the annual reports used in this research; these are firm size (FS), firm age (FA), majority owner (MO), firm type (FT), and industry type (IT).

Second, since the sample used in this research consists of Indonesian companies, many of the financial reports are denoted in Rupiah as their reporting currency. Nevertheless, some companies have used the United States Dollar (USD) as their reporting currency. Thus, to make the unit consistent, we converted all the Rupiah data, such as current asset and main business income, into USD using the end-of-year currency. Current asset was used to measure the operational performance of firms; main business income was also employed as a measure of financial performance.

Third, we collected data to measure SCF, which is the mediator of the model. In order to obtain the SCF inputs, we coded some keywords, which are explained further in the next section. We identified the keywords or codes that commonly appeared in the directors’ reports of the companies. Next, we collected the integration inputs, from the annual report or a particular company’s official website.

Content analysis

The next step was to conduct the content analysis. As mentioned earlier, this method was used to gather SCF inputs. We performed the content analysis test according to the procedure established by Tangpong,

62

as follows: 1. Determining the recording unit

This research elaborated on the information which was stated in the annual director’s reports; This report usually states a company’s current business status or strategic planning.

2. Determining the content categories of coding

After determining the data source, in this step, we extracted the information from the director’s reports, regarding companies’ information systems, product flexibility, supply flexibility, manufacturing flexibility, and distribution flexibility.

Developing the coding rules

Each of the sub-sectors mentioned earlier has five measurement items, and each of the measurement items includes one or two coding content examples. For example, “increasing production equipment” and “improving production processes” are some of the coding contents used to measure the manufacturing flexibility.

4. Determining quantitative data

After the text constructs were determined, we explored how to quantify the data. For each measurement item, we scored 1 if the director’s company report contained information about the measurement item, and 0 otherwise. Thus, the maximum score of the company in one flexibility variable will be 5 if the company provides all the information about the measurement items, and the minimum is 0 if the items are not stated at all. Finally, we summed all the scores to give the final SCF score of a particular company’s flexibility.

Measures

Dependent variables

The dependent variables in this research are operational and financial performance, which are measured by CAT and PR, respectively. CAT was chosen to represent operational performance because this number is derived from the main business income divided by current assets. Operational performance indicates the productivity of companies’ operation management; it means the revenue that companies can earn from the limited resources owned. Thus, the higher the CAT results, the better the companies’ operational performance.

Furthermore, we followed Ojha’s 20 work to measure financial performance. We used the logarithm of companies’ total revenue for a particular year. Additionally, we used 1-year lagged data because the impact of RSCF or PSCF may not be evident in the same year.

Mediators

To derive the RSCF variables, we adopted the information on the operation and strategies of the firm in the particular years of the collected annual reports. However, for the PSCF, we measured according to the companies’ strategies that would be implemented in the following year. The detailed measurement items of RSCF and PSCF are listed in the Appendix 1.

Independent variables

The independent variables of this research are III and EII. We used a dummy variable to quantify the information. We scored 1 for companies that stated their information integration system usage, whether to provide information for their external parties (to measure the EII system), or an information-sharing system among organizations (to measure III). On the other hand, if the company did not have an information integration system, 0 was assigned.

Control variables

The control variables of this research are firm size, firm age, ownership, firm type, and industry type. Firm size is the natural logarithm of a company’s total assets. We gathered information on the number of employees from companies’ annual reports. Firm age is the period from the establishment date until the year of the annual report. Firm ownership measures the proportion of the first majority shareholder of the company. For firm type, 1 indicates a state-owned company and 0 denotes a privately owned company. Lastly, Table 1 shows a description of the variables.

Description of the variables.

Research results and analysis

The objective of hierarchical regression is to interpret the influence of the independent variables on the dependent variable. The results of this test are also used to address the hypotheses that were developed in Section 2. To answer each of the hypotheses (H1, H2, H3, and H4), we developed four models that were further regressed using the hierarchical regression method, with SPSS 20. These models are: Model l: Reactive Supply Chain Flexibility (RSCF) as the dependent variable, and Internal Information Integration (III) and External Information Integration (EII) as the independent variables with five control variables. Model 2: Proactive Supply Chain Flexibility (PSCF) as the dependent variable, and Internal Information Integration (III) and External Information Integration (EII) as the independent variables with five control variables. Model 3: Financial performance as the dependent variable, and Reactive Supply Chain Flexibility (RSCF) and Proactive Supply Chain Flexibility (PSCF) as the independent variables with five control variables. Model 4: Operational performance as the dependent variable, and Reactive Supply Chain Flexibility (RSCF) and Proactive Supply Chain Flexibility (PSCF) as the independent variables with five control variables.

The results provide significant support for the effect of EII on RSCF (β = 0.517, p < 0.001). Moreover, the t coefficient also shows a positive sign. Thus, we can conclude that EII positively affects RSCF, which supports our H1b. On the contrary, since III is not significantly related to RSCF (β = 0.033, p > 0.5), H1a is not supported. PSCF is affected by both EII and III (β = 0.421, p < 0.001, β = 0.179, p < 0.005, respectively), which supports our H1c and H1d. None of the control variables has an impact on supply chain flexibility. Table 2 represents the effect of information integration on supply chain flexibility.

Regression results of models 1 & 2.

*p < 0.05; ** p < 0.01; ***p < 0.001

Table 3 below shows how PSCF and RSCF affect financial and operational performance. Financial performance is positively influenced by RSCF (β = 0.128, p < 0.05), while the effect of PSCF is not significant (β = 0.002, p > 0.5). Furthermore, two control variables have a significantly positive influence on financial performance, which are the firm size and majority ownership. This means that financial performance is also positively influenced by the company

Regression results of models 3 & 4.

*p < 0.05; ** p < 0.01; ***p < 0.001

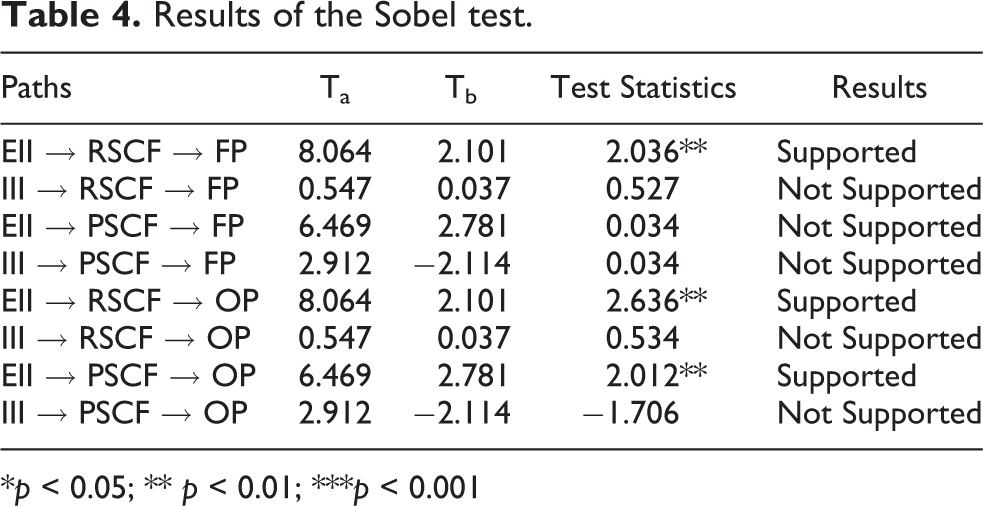

Furthermore, to investigate the mediating effects of RSCF and PSCF on the influence of EII and III on financial and operational performance, we considered the results by multiplying the beta coefficient from the t-test by the result for each related variable. If there is a negative sign we can conclude that there is no mediating effect, whereas a positive sign after the calculation shows that there is a mediating effect between variables. Figure 2 depicts the coefficient and the relationship between variables based on the previously developed research framework. In the results (Table 4), there is a mediating effect of RSCF on the relationship between EII and financial performance (p < 0.05). The results also show that the relationship between EII and operational performance is mediated by both RSCF and PSCF (p < 0.05, p < 0.05, respectively). In summary, only H4b, H5b, and H5d are supported.

Coefficient framework.

Results of the Sobel test.

*p < 0.05; ** p < 0.01; ***p < 0.001

Discussion and conclusions

Conclusions

The study investigated the relationship between supply chain information integration (internal and external), supply chain flexibility (reactive and proactive), and supply chain performance (financial and operational) in the Indonesian context. By elaborating and analyzing annual reports of basic and chemical companies in Indonesia, the study indicates that increasing external information integration would enhance the level of RSCF and PSCF, while enhancing the level of internal information integtation only affect PSCF. Moreover, enhancing the level of either RSCF or PSCF would also increase supply chain operational performance. Surprisingly, PSCF negatively affects operational performance. We found that PSCF illustrates the upcoming strategies that would be implemented in the next year. Therefore, it might only increase the assets as operational performance indicates the ratio between main business income and current assets. However, RSCF only mediates the relationship between EII and supply chain performance (both financial and operational) and PSCF only mediates the effects between EII and operational performance.

Theoretical implications

This study provides meaningful insights for the existing stream of research. First, we contribute to the theoretical implications of the association between information integration, flexibility, and performance, which can be illustrated by RBV. In RBV, competitive advantages rely on tangible and intangible resources. The companies in the supply chain have to obtain heterogeneous and immobile resources through information exchange with departments internally and other allies externally. Moreover, companies have to adjust and predict their operational strategies through tangible and intangible resources, in order to enhance their dynamic capabilities to respond to environmental changes. In other words, a company which can adapt to environmental changes would stay competitive, and the outcomes would eventually be reflected in financial and operational performance.

Another contribution of our study is to clarify the strength of the linkage between information integration, flexibility, and performance. For example, EII has a strong impact on both reactive and proactive flexibility. Nevertheless, the effect of III on reactive supply chain flexibility is not significant. We argued that most of the listed companies in the analysis had achieved information integration internally for years. A higher level of III adoption might not the contributor to enhance adaptive capabilities of these companies. Both reactive and proactive flexibility have a stronger influence on operational performance than on financial performance; this might indicate that flexibility is more related to the resource transformation ability of the companies. In addition, the effect of reactive flexibility on operational performance is stronger than the effect of proactive flexibility. In the study, financial performance measures how effectively a company can earn revenue. However, proactive strategies might need a longer period to reflect the results. In addition, revenues might be obtained from other dimensions not included in our study. Therefore, the linkage between proactive flexibility and financial performance is very weak.

Last, the results regarding SCF’s mediating effect on EII’s influence on operational performance also confirmed Yu et al.’s 14 finding. However, RSCF only mediates the effects of EII on supply chain performance. The information collaboration between supply chain members such as suppliers, manufacturers, distributors, retailers, and logistics providers should indicate a certain ability to deal with market uncertainty to improve financial performance.

Practical implication

The study also discusses important practical implications. The economy of Indonesia has been growing fast. As the upstream suppliers in the supply chain in Indonesia, any of the variations in this sector would significantly affect the downstream manufacturers and the customers. For example, the global competition and the fluctuation of global price commodities such as metals and chemical products have an impact on the basic and chemical industry. Moreover, the force of government environmental policies also affects the performance of the industry. For instance, the plastics and paper industries are sensitive to government regulations. The Indonesian government has banned the usage of single-use plastic bags. In addition, the imported recovered fiber has to meet a higher standard for contamination. The environmental policies would also affect how to select material in the product development phase. Thus, the basic and chemical industry has to be flexible to stay competitive. According to the collected data in our study, most of the companies have adopted III. Improving the information exchange and transparency among all supply chain partners effectively should be the second step to achieve higher performance. Additionally, a close and mutual collaboration in the supply chain is critical, to respond to market uncertainty and meet future market expectations. For example, the basic and chemical industry in Indonesia should adopt green manufacturing and green logistics to meet future market expectations. As long as the Indonesian government starts to regulate stricter environmental policies, reactive flexibility would be the priority in this sector to reach higher financial and operational performance.

Limitations and recommendations

Data availability is a limitation of this research. This research used financial reports of a sample of Indonesian basic and chemical companies that were listed in IDX from 2014 to 2017. However, a longer time frame and a larger sample may enhance the quality of the results. This research could not be extended to include data from earlier than 2014, because the latest data that we could access in IDX were for 2016, while other data were obtained from the companies’ official websites.

Furthermore, the Indonesian basic and chemical industry contains eight industry categories. We believe that a greater focus on certain industries, with an adequate sample size, is the best way to test all the hypotheses of this research. However, focusing on a more specific industry means decreasing the sample size for each year, which as previously mentioned, leads to the limitation of data availability. Thus, we suggest that if future research can access a longer period of available financial reports, the results will be more reliable.

Last but not least, we believe that comparing specific factors with other countries can be one of the future research directions. The objective of this research is to investigate the relationship between integration, flexibility, and performance of companies in Indonesia; however, the variable, flexibility, is a combination of manufacturing, product development, supply, and distribution. It would be beneficial to examine the effects of different flexibility dimensions on supply chain performance. Additionally, we argued that the importance of these dimensions would differ from the regional perspective. As this idea was not explored in this research, we, therefore, hope that further research can compare the results regionally.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Measurement of flexibility.

| Flexibility Names | Measurement Items | Related Studies | Coding Content Examples |

|---|---|---|---|

|

|

Ability to make product modifications effectively due to process correction or customer changing needs. | Yu et al. 14 | “changing the product design,” optimize the process design” |

| Ability to adjust the product mix effectively over time. | Yu et al. 14 | “new factories/plants construction,” “factory building expansion” | |

| Ability to manufacture a broad range of different products effectively. | Yu et al. 14 | “launching new product lines,” “product line replacement” | |

| Ability to adjust production volumes. | Moon et al. 5 | “improving production capabilities” | |

| Ability to change manufacturing facilities and processes. | Moon et al. 5 | “investing production equipment,” “changing production processes” | |

|

|

Simultaneously design products | Swafford et al. 39 | “item postponement strategy,” “optimize product structure” |

| Utilize the product differentiation strategy during product development. | Swafford et al. 39 | “extending the product lines,” “product differentiation at the development phase” | |

| Incorporate platform-based approach in R&D | Swafford et al. 39 | “collaborating between R&D and manufacturing,” “investing a new research center” | |

| The number of new products or services the company can create every year. | Moon et al. 5 | “developing new product series,” “providing new services” | |

| Change products and services mix | Moon et al. 5 | “adding value (additional services) to the products” | |

|

|

Number of available suppliers | Moon et al. 5 | “expanding the channels,” “alliance development,” “new supplier list” |

| The ability of major suppliers that provide products and services | Moon et al. 5 | “Controlling the cost of raw materials,” “raw material importing” | |

| Range of suppliers that provide major materials/components/ products. | Moon et al. 5 | “source of materials,” “supplier in another industry” | |

| Ability to add and remove suppliers. | Moon et al. 5 | “supplier selection,” “seeking collaboration,” “terminating the contract with supplier.” | |

| Ability to change suppliers to satisfy changing requirements | Moon et al. 5 | “supplier auditing,” “supplier relationship management” | |

|

|

The number of warehouses, loading capacity, and other distribution facilities. | Moon et al. 5 | “building new warehouses/distribution facilities” |

| Ability to add or remove carriers or other distributors. | Moon et al. 5 | “increasing the volume of chemical material,” “enlarging storage capacity,” “terminating the contract with distributor” | |

| Ability to change warehouse space, loading capacity, and other distribution facilities |

Moon et al. 5 | “warehouse expansion,” “enlarging storage capacity,” “investing loading equipment” | |

| Ability to change delivery modes/ schedules | Moon et al. 5 | “changing transportation modes/network/schedule” | |

| Flexibility in responses to request for changes in this relationship | Yu et al. 14 | “Expanding the distribution network,” “Establishing long term relationship with distributors” |