Abstract

Managing risks is very significant for microfinance institutions (MFIs) to guarantee their financial soundness, to achieve their social objectives and then to encourage donors and investors to participate in microfinance industry financing. Risks impacts on MFIs differ considerably which make their prioritizing a highly important task to figure out the candidate risks to be mitigated or tolerated. This article provides a clear picture of the most serious risks affecting the microfinance sector in Morocco. We used an approach that combines the interval-valued intuitionistic fuzzy sets (IVIFSs) and the technique for order of preference by similarity to ideal solution (TOPSIS) method to deal with the lack of sufficient statistical data and the subjectivity of the experts’ judgement in risk rating. A sensitivity analysis was also conducted to show the impact of criteria weights on the decision process and to examine the robustness of the model results.

Introduction

Microfinance refers to the provision of financial services to the poor who have limited access to traditional banking services with the aim of reducing poverty. 1,2 Several studies showed the positive impact of having access to microfinance services on the living condition of the poor. 3 Other studies suggested that the original mission of microfinance institutions (MFIs) was not always respected. 4 Steinwand 5 reported that MFIs face many risks that threaten their social mission and their long-term viability. This risks’ classification differs significantly from one author to another. According to Goldberg and Palladini, 6 microfinance risks, which can be examined internally or externally, 6,7 can be classified into three categories: financial risks, operational risks and strategic risks. La Torre 8 classifies them into financial risks, business risks and process risks. Lascelles et al. 9 found that microfinance risks can be grouped into three baskets: client risks, service provider risks and market environment risks. In this study, microfinance risks are grouped into financial risks, operational risks and strategic and institutional risks. Based on the literature database and discussion with some practitioners in the field, the elements of each group are given in Table 1.

Risks in microfinance.

Fernando et al. 12 sustained that a comprehensive approach that covers all kinds of risks is fundamental for MFIs whatever their ownership type; NGO, cooperative or a specialized MFI. MFIs need to manage the probability and the potential severity of risks adequately to guarantee both their sustainability and outreach as well as to gain the confidence of donors, investors, lenders and borrowers. 5,12

According to Goldberg and Palladini,

6

Steinwand

5

and Liew and Lee,

21

the steps of the risk mitigation process can be set as follows: Identifying the risk profiles; Prioritizing, assessing and defining the most important risks; Designing policies and procedures to mitigate those risks; Assigning responsibilities; Testing the effectiveness and evaluating the results; and Improving the adopted policies when necessary.

Oluyombo and Olabisi 7 added that the influence of risks on MFIs varies considerably, hence, every single risk needs to be handled according to its appropriate importance. In that context, risks prioritization can be very helpful for MFIs. The aim of this study is to provide a clear picture about the exposure of Moroccan microfinance sector to risk. Obtaining sufficient data about all kinds of risks in Moroccan microfinance sector is not possible. To tackle this challenge, we adopt an expert-driven approach; we managed to prioritize risks in microfinance sector using the interval-valued intuitionistic fuzzy TOPSIS.

In many real life problems, the decision makers’ judgement is vague and uncertain due to the lack of sufficient information, the time pressure or the difficulty to differentiate between alternatives. Yadav et al. 22 confirmed that fuzzy logic is a successful way to deal with this challenge. It is more appropriate for expressing the logical relations related to human expression. 23,24 Nevertheless, Velasquez 25 showed that providing an exact value of the degree of membership for an element may be difficult; there may be a hesitation degree between the membership and non-membership. A decision maker (DM) may express his/her opinion, while he/she is not so sure about it. 26 In such situations, the intuitionistic fuzzy set (IFS) can be the best choice. It can successfully tackle this hesitation degree as it allows DMs to express their opinions using both membership and non-membership degrees and then to accurately assess alternatives in a decision problem. 27 The IFS 28 is an extension of the fuzzy set theory. 29 It is characterized by a membership, non-membership and hesitation functions. Boran et al. 30 noted that it may be more practical in deciding under uncertain conditions. The intuitionistic fuzzy logic has been used in several areas such as suppliers’ selection, economics, environmental studies, management, marketing, social, medical and pattern recognition. 25,30,31

Despite its advantages, according to Xu and Cai, 32 it is difficult to express the values of the membership function and the non-membership function as exact numbers in IFSs. However, it may be easy to specify their ranges. That explains the usefulness of interval-valued intuitionistic fuzzy set (IVIFS) introduced by Atanassov and Gargov. 33 A distinguishing feature of IVIFS is that the values of the membership and non-membership functions are intervals rather than exact numbers.

The TOPSIS 34 is one of the most popular methods in multi criteria decision making (MCDM) techniques. 30,35 It allows the identification of alternatives with the shortest distance from the positive ideal solution and the longest distance from the negative ideal solution. 25 Borjalilu and Ghambari 36 mentioned that despite its usefulness to several areas of knowledge, MCDM still cannot fully match imprecise and incomplete information. However, its flexibility allows benefiting from the other theories of decision.

Combining IVIFS with TOPSIS can have an enormous chance of success in assessing risks in microfinance sector as it can both tackle the vagueness present in MCDM problems and the hesitation present in the decision makers’ knowledge. 22

The remainder of this article is organized as follows: The second section provides a brief description of the IVIFS. The third section presents the concept of intuitionistic fuzzy TOPSIS. In fourth section, the proposed approach is implemented for risks assessment in Moroccan microfinance sector. Finally, a conclusion and some perspectives are given in the fifth section.

IVIFS: A theoretical background

Several studies have been conducted on the IVIFS, which include and not limited to the operations of IVIFSs, the correlation between IVIFSs, the aggregation operators of IVIFSs and so on. 27

Definition 1

Let X be a set of the universe, the fuzzy set A is defined as

Definition 2

For a set X, the IFS is defined by:

A great value of

Definition 3

Let X be a set of the universe, and D [0,1] be the set of all closed subinterval of [0,1]. An IVIFS A is defined as:

The intervals

where

The hesitation degree of an IVIFS A is given as follows

From definition 1, 2 and 3, we can demonstrate that the crisp sets, fuzzy sets and IFS are special cases of IVIFS,

37,38

indeed if

Crisp sets, fuzzy sets and IFS are special cases of IVIFS. IFS: intuitionistic fuzzy set; IVIFS: interval-valued intuitionistic fuzzy set.

Definition 4

An interval-valued intuitionistic fuzzy number (IVIFN) is denoted

Let

Definition 5

Let

Two IVIFNs If S (A) < S (B), then A < B

If S (A) > S (B), then A > B

If S (A) = S (B) and:

H (A) = H (B), then A = B

H (A) > H (B), then A > B

H (A) < H (B), then A < B

The larger the value of the score function S (A), the larger is the IVIFN A. The larger the H (A) is, the higher the degree of accuracy of IVIFS A is, and vice versa. The score function and accuracy function are like the mean and variance in statistics. 26

Interval-valued intuitionistic fuzzy TOPSIS

The interval-valued intuitionistic fuzzy TOPSIS is a systematic approach that can be summarized in eight steps:

Step 1: Identify the evaluation criteria, alternatives and decision makers

Let

Step 2: Construct the decision matrix for each expert

To estimate their judgements on alternatives, the

Step 3: Aggregate the decision matrices of all decision makers

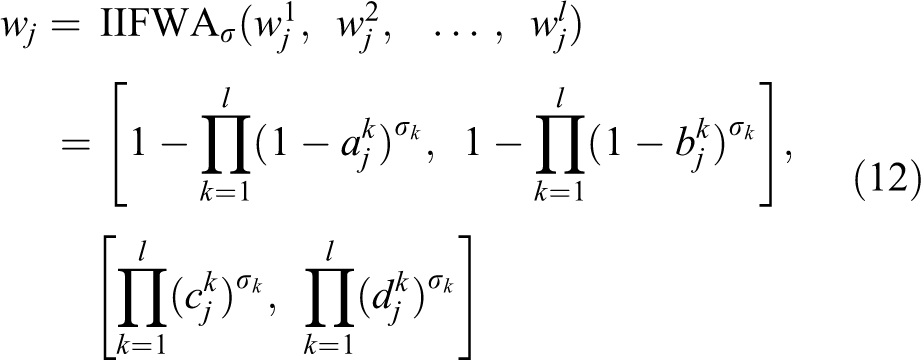

Choosing the appropriate aggregation procedure of decision makers’ opinions is fundamental in the MCDM process. 40 In that context, several operators have been developed 31,39 such as interval-valued intuitionist fuzzy weighted averaging (IIFWA) operator, interval-valued intuitionist fuzzy ordered weighted averaging operator, interval-valued intuitionistic fuzzy ordered weighted geometric operator, interval-valued intuitionistic fuzzy weighted geometric operator and interval-valued intuitionist fuzzy hybrid aggregating operator. In this article, the IIFWA operator is chosen.

Let

Let D =

Step 4: Assign the weights for criteria

Let

The weights set W of all criteria can be given as follows:

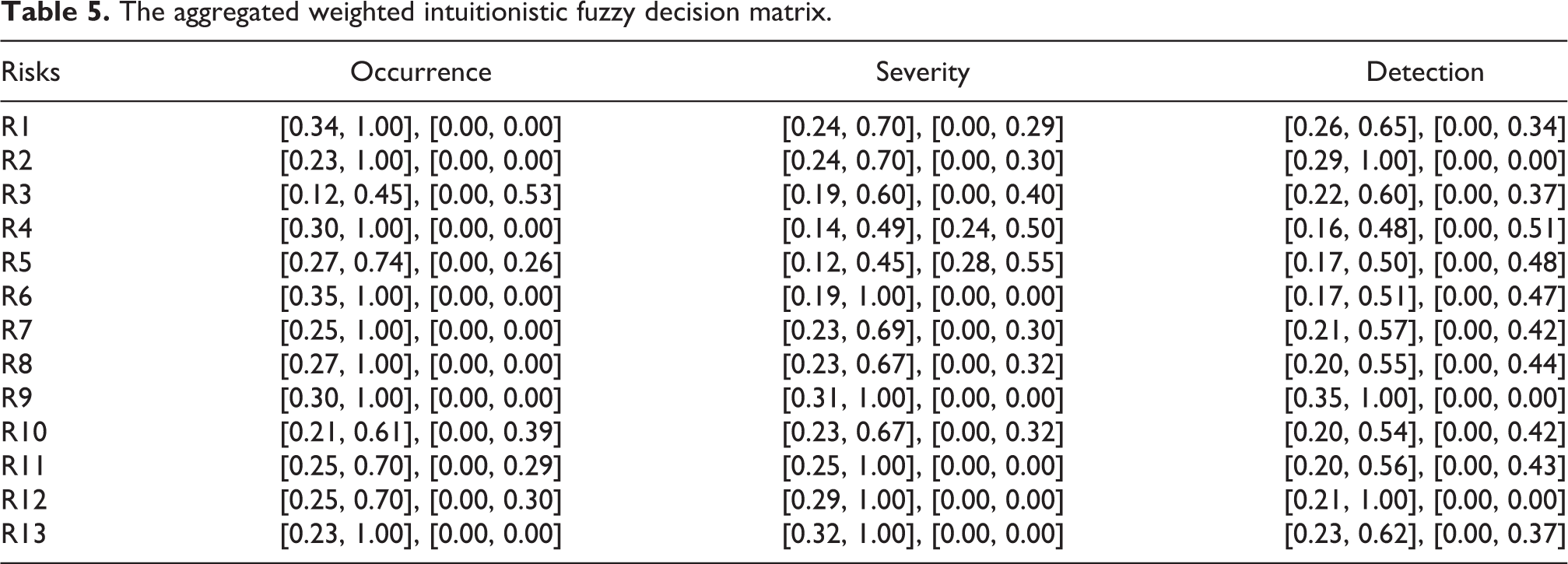

Step 5: Establish the aggregated weighted intuitionistic fuzzy decision matrix

Xu and Jian 31 define the aggregated weighted intuitionistic fuzzy decision matrix as

where

So

Step 6: Determine the IVIF-PIS and the IVIF-NIS

Let J 1 be the benefit criteria and J 2 be the cost criteria. The interval-valued intuitionistic fuzzy-positive ideal solution (IVIF-PIS) denoted I+ and the interval-valued intuitionistic fuzzy- negative ideal solution (IVIF-negative ideal solution [NIS]) denoted I− are given as follows

where

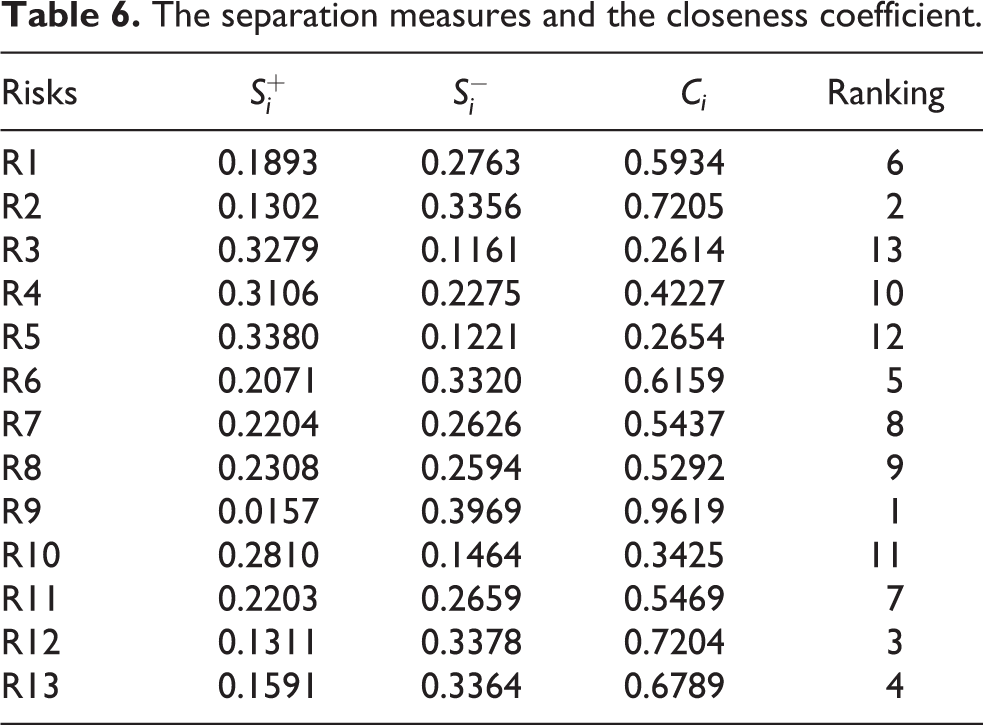

Step 7: Calculate the separation measures

Several distance measures were proposed to calculate the separation of each alternative from the IVIF-PIS and the IVIF-NIS 27,38,39 such as the Hamming distance, the normalized Hamming distance, the Euclidean distance and the normalized Euclidean distance. In this article, we adopt the normalized Euclidean distance. Therefore, the separation of each alternative from the IVIF-PIS and the IVIF-NIS is given as follows

Step 8: Determine the closeness coefficients and rank the alternatives

The closeness coefficient of the alternative (risk) Mi is defined as

where

The alternatives are classified according to their Ci , in our case, the risk (alternative) with the highest Ci is presented as the most serious one.

Risk assessment in Moroccan microfinance sector

The Moroccan microfinance sector, considered as an international model since 2007, 41 faced a serious crisis in 2008 due an uncontrolled growth. 42 To respond to this crisis, a stringent prudential regulation was adopted by the national central bank and, furthermore, the MFIs are becoming more concerned with risk management. 15 The microfinance sector in Morocco includes 13 MFIs also known as Moroccan Microfinance Associations with about 1 million beneficiaries of which three; Al Amana, Attawfik and Al baraka, concentrate 95% of the market share. 15 Bennouna and Tkiouat 43 noted that the main product offered is microcredit, they also highlight that the Moroccan MFIs do not have the right to collect saving due to their associative status.

In this study, the risks in Moroccan Microfinance sector are evaluated by 10 risk analysts (decision makers) considered with equal expertise and selected from different Moroccan MFIs. Each risk is evaluated with respect to three criteria: severity (S), occurrence (O), and detection (D). 46 The decision maker is asked to assign weights for criteria and then to rate independently the different risks within the Moroccan Microfinance sector using the linguistic scales 37,44 (see Appendix 1). The decision makers’ judgements are then transformed into their corresponding IVIFNs.

Once the IVIF decision matrices for all decision makers as well as the weight corresponding to each criterion are established (see Appendix 1), we calculate the aggregated IVFI decision matrix (Table 2) and the aggregated IVIF weights (Table 3) using the IIFWA operator.

The aggregated IVIF decision matrix.

IVIF: interval-valued intuitionistic fuzzy.

The aggregated IVIF weights.

IVIF: interval-valued intuitionistic fuzzy.

In the next step, we calculate the IVIF-PIS, the IVIF-NIS (Table 4), the aggregated weighted intuitionistic fuzzy decision matrix (Table 5), the separation measures and the closeness coefficient (Table 6).

The IVIF-PIS and the IVIF-NIS.

IVIF-PIS: interval-valued intuitionistic fuzzy-positive ideal solution; IVIF-NIS: interval-valued intuitionistic fuzzy-negative ideal solution.

The aggregated weighted intuitionistic fuzzy decision matrix.

The separation measures and the closeness coefficient.

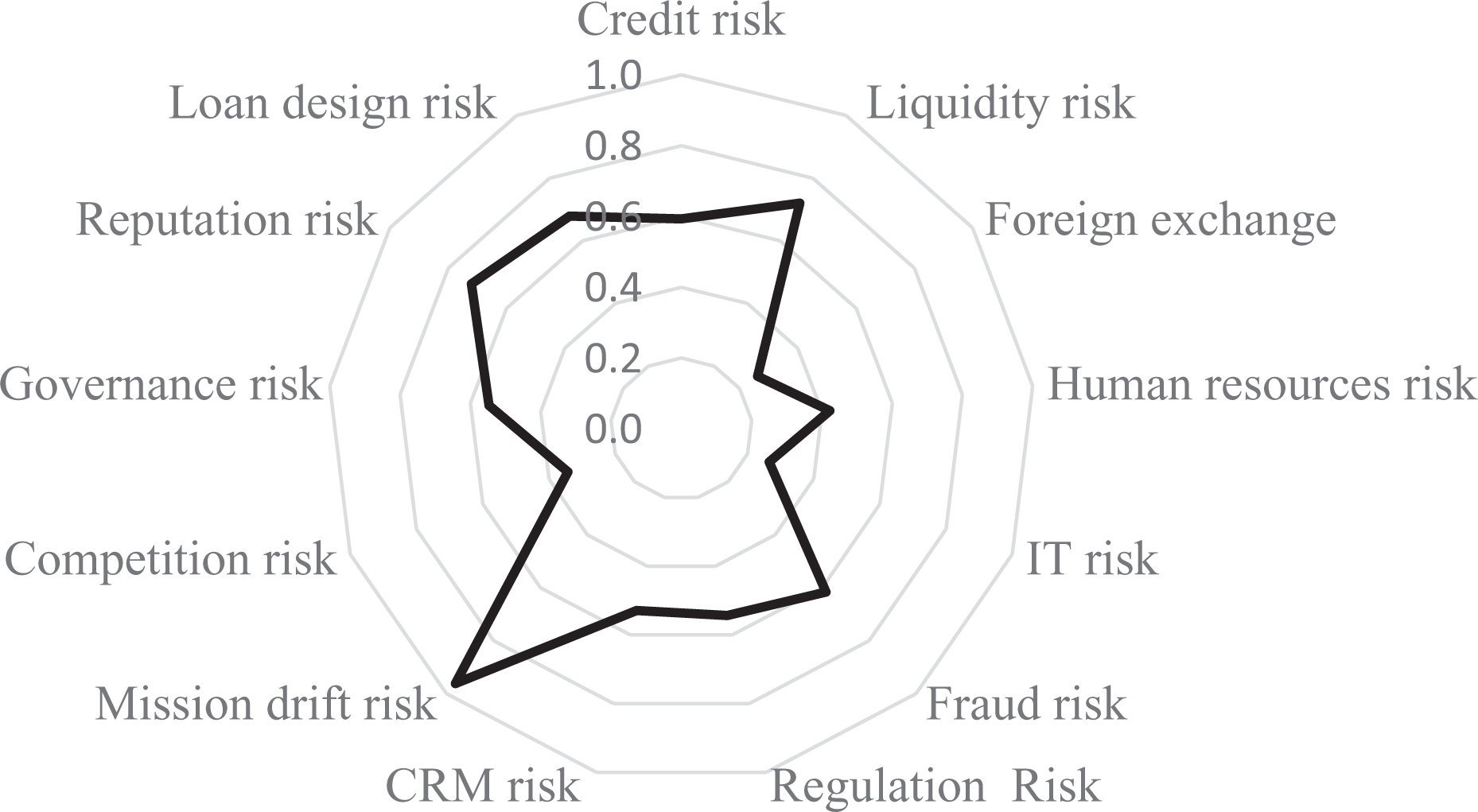

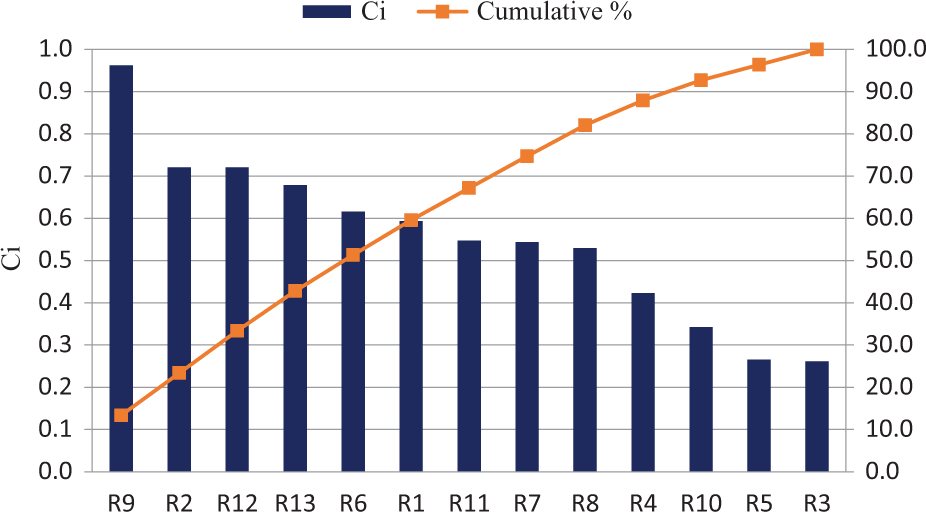

The representation of the closeness coefficients related to all risks is highlighted in Figure 2.

The closeness coefficients of all assessed risks. Source: Authors’ elaboration.

To show which risks the Moroccan MFIs need to focus on, the Pareto analysis is conducted. It is one of the six sigma and quality management tools that is highly recommended to identify where efforts should be focused to achieve the desired improvements. In our case, the Pareto diagram (Figure 3) suggests that the mission drift risk (R9), liquidity risk (R2), reputation risk (R12), loan design risk (R13) and fraud risk (R6) represent, respectively, 50% of the risks’ effect in the Moroccan microfinance sector.

Pareto analysis diagram. Source: Authors’ elaboration.

In a previous work, Bennouna and Tkiouat 43 highlighted that the interest rates practiced in Morocco are high. Lamrani and Tkiouat 13 showed that the Moroccan MFIs suffer from aggressive collection practices, inadequate analysis of customers’ business and a lack of training and coaching of the MFIs staff. That can explain some of these study findings. On other side, our finding is contradictory with Gietzen 45 who held that generally, microfinance sector is facing minimal liquidity risk.

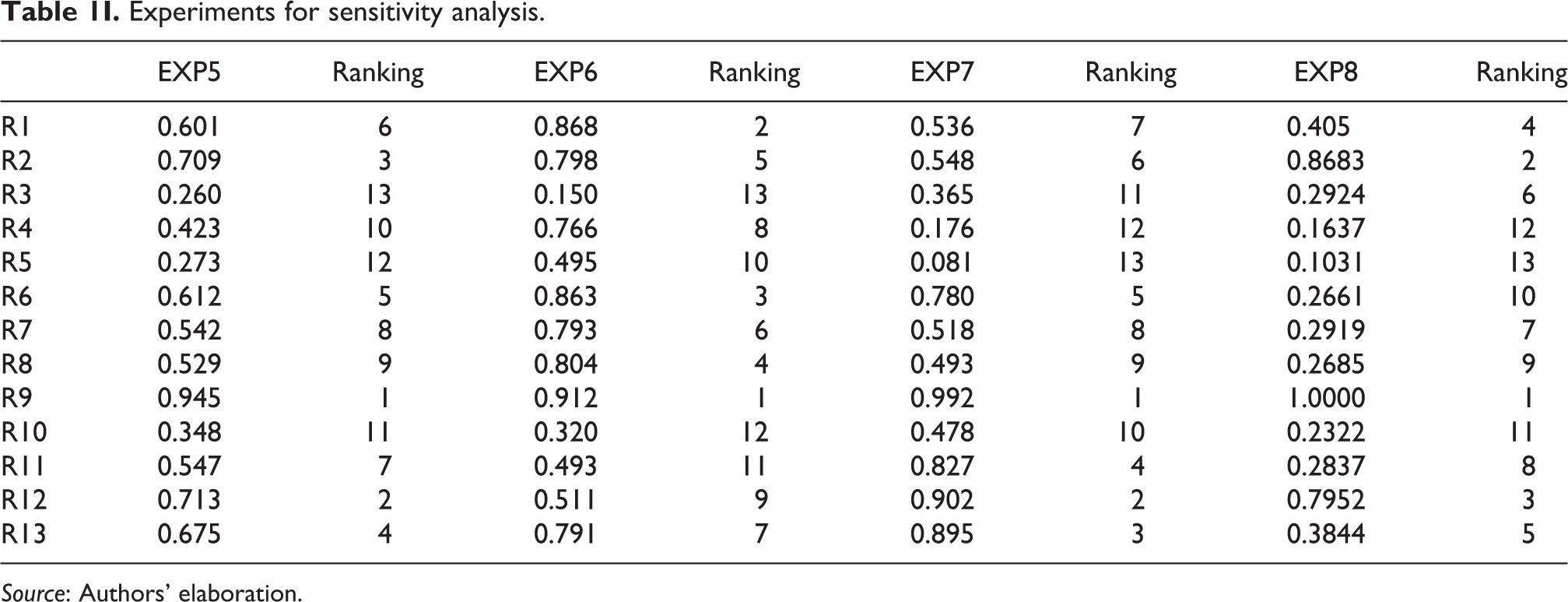

In order to validate the model’s results quantitatively, a sensitivity analysis is also performed, it can highlight the degree to which the criteria’ weights (denoted wj

for the criteria

EXP1: All criteria are considered very unimportant:

EXP2: All criteria are considered unimportant:

EXP3: The importance of all criteria is supposed medium:

EXP4: All criteria are considered important:

EXP5: All criteria are considered very important:

EXP6: The occurrence criterion is set as the very important, while the other criteria are supposed very unimportant,

EXP7: The severity criterion is set as the very important while the other criteria are considered very unimportant

EXP8: The detection criterion is set as the very important while the other criteria are considered very unimportant

On the one hand, Figure 4 shows that when all criteria are given the same weight (from EXP1 to EXP5), the risks ranking is relatively similar to the model findings (RES). We note that, for our case (RES), all criteria have a score function between 0.75 and 0.8 (see Table 3). On the other hand, the Figure 5 shows that whatever the importance given to the criteria, the mission drift risk (R9) still the most important one. It also indicates that when the occurrence criterion is considered as the most important (EXP6), the credit risk (R1) is coming in the second place, the fraud risk (R6) in the third place and the poor client relationship management risk (R8) in the fourth place. When the severity criterion is considered as the most important (EXP7), we notice that the reputation risk (R12) is coming in the second place, the loan product design (R13) in the third place and the governance risk (R11) in the fourth place. When the detection criterion is considered as the most important (EXP8), we notice that the liquidity risk (R2) is coming in the second place, the reputation risks (R12) in the third place and the credit risk (R1) in the fourth place. More details about sensitivity analysis are given in the Appendix 1.

Experiments for sensitivity analysis when all criteria are given the same weight (EXP1 through EXP5). Source: Authors’ elaboration.

Experiments for sensitivity analysis when criteria are given different weights (EXP6 through EXP8). Source: Authors’ elaboration.

Both the results of the model and the sensitivity analysis were not surprising for several microfinance practitioners, which can confirm their appropriateness.

Conclusion

Adopting a comprehensive approach that covers all types of risks is fundamental for MFIs in order to enhance both their financial sustainability and outreach. Unlike the focus on the credit risk in the microfinance literature, the aim of this article was to identify the potential risks that can have a negative impact on the microfinance industry in Morocco.

To deal with the unavailability of crisp data about all kinds of risks and the subjectivity of the experts’ judgement in the decision process, an IVIF-TOPSIS evaluation was implemented. The findings suggested that Moroccan MFIs need to take some corrective actions to reduce the mission drift risk, the reputation risk, the liquidity risk, the loan design risk and the fraud risk, respectively.

For future work, this study can be extended to include the dynamic interval-valued fuzzy numbers, 47 where decision information about risks is to be collected at different periods. In addition, as risks are interlinked, the correlation among them also needs to be studied.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was financially supported by the Islamic Development Bank.

Appendix 1

Experiments for sensitivity analysis.

| EXP5 | Ranking | EXP6 | Ranking | EXP7 | Ranking | EXP8 | Ranking | |

|---|---|---|---|---|---|---|---|---|

| R1 | 0.601 | 6 | 0.868 | 2 | 0.536 | 7 | 0.405 | 4 |

| R2 | 0.709 | 3 | 0.798 | 5 | 0.548 | 6 | 0.8683 | 2 |

| R3 | 0.260 | 13 | 0.150 | 13 | 0.365 | 11 | 0.2924 | 6 |

| R4 | 0.423 | 10 | 0.766 | 8 | 0.176 | 12 | 0.1637 | 12 |

| R5 | 0.273 | 12 | 0.495 | 10 | 0.081 | 13 | 0.1031 | 13 |

| R6 | 0.612 | 5 | 0.863 | 3 | 0.780 | 5 | 0.2661 | 10 |

| R7 | 0.542 | 8 | 0.793 | 6 | 0.518 | 8 | 0.2919 | 7 |

| R8 | 0.529 | 9 | 0.804 | 4 | 0.493 | 9 | 0.2685 | 9 |

| R9 | 0.945 | 1 | 0.912 | 1 | 0.992 | 1 | 1.0000 | 1 |

| R10 | 0.348 | 11 | 0.320 | 12 | 0.478 | 10 | 0.2322 | 11 |

| R11 | 0.547 | 7 | 0.493 | 11 | 0.827 | 4 | 0.2837 | 8 |

| R12 | 0.713 | 2 | 0.511 | 9 | 0.902 | 2 | 0.7952 | 3 |

| R13 | 0.675 | 4 | 0.791 | 7 | 0.895 | 3 | 0.3844 | 5 |

Source: Authors’ elaboration.