Abstract

Business models have received increasing attention in both academic and managerial communities. However, little attention has been paid to how business models change in response to extreme events. This topic is of critical importance since failure to achieve adaptation in a timely manner can lead to negative consequences such as a significant decrease in firm value or bankruptcy. This study explores how the business model paradigm of the Portuguese footwear industry changed following China’s entry into the World Trade Organization in 2001. The empirical results suggest that the shock acted as a trigger for change for the Portuguese footwear firms which reflected in the adoption of a new business model characterized by speed and flexibility in the manufacturing process, faster response to customer needs and, in specific cases, in downward integration through the creation of own brands selling directly to final consumers. This result, however, was not the outcome of a sudden change but rather the consequence of a planned adaptation strategy led by a key industry actor that acted as a network orchestrator coordinating the actions of the Portuguese footwear firms. The implications of these findings as well as directions for future research are discussed in the last part of this study.

Introduction

The footwear industry consists of all firms active in the production of all types of men’s, women’s, and children’s shoes. This is a very complex industry with a fragmented value chain in which large companies coexist with smaller and more specialized firms. During recent years, the industry has experienced a stable rate of growth and, according to recent forecasts, this trend is expected to continue going forward. Specifically, in 2015, the global market reached a value of US$270,136 million, showing a compound annual growth rate (CAGR), in the period 2011–2015, equal to 5.2%. 1 Similarly, for the period 2015–2020, the expected CAGR is forecasted to be 5.8%, driving the industry to a value of US$358,583 million by the end of 2020. The largest segment of the industry is represented by women’s footwear, accounting for 53.9% of the total value. Men’s footwear, instead, accounts for a further 28.1% and, finally, the children’s segment covers the remaining 18%.

More interesting data come out from a geographical segmentation of the market. The Asia-Pacific zone accounts for 33.7% of the global market, reaching a value of US$91,163 million in 2015 and showing a CAGR of 9.4% during the period 2011–2015. In comparison, the European and US markets cover 28.3% and 24.9%, respectively, reaching values of US$79,437 and US$67,253 million in 2015. The main reason behind these interregional differences can be traced in the economic and financial crisis that affected more heavily US and European consumers over the period of analysis. As a consequence, Asia-Pacific countries have started relying increasingly less on exports and more on their domestic markets. This trend is expected to lead to a greater share of the global growth of consumer spending in the emerging markets in the coming years. In Europe, although growth remained weak, the market has seen some acceleration recently. Further increase is expected for the next 5 years, moving the CAGR from the current 1.3% toward 2.7%. United Kingdom, Germany, France, Italy, and Spain account for almost 60% of the European market with the first two countries expecting the highest growth.

The competitive environment is reflected in these figures especially from the point of view of the relationship with the final consumer. In fact, looking at the footwear retailing, the industry is highly fragmented, even if the market is dominated by large retail groups with a high degree of rivalry. One of the main competitive factors is represented by price. In fact, since it reflects the quality of the final product, pricing strategy is the principal mean to segment the market and draw niches of consumers. Moreover, like any other industry based on design and creativity, styles and brands are very useful instruments to compete with rivals on the market. The traditional footwear delivery, based on two seasons, is radically changing toward the fast-fashion environment. Although consumers recognize the value of a brand and the heritage of some firms acting in the industry, they are increasingly buying shoes on impulse and expect to see a more rapid change of assortment with diversity. Therefore, managerial efforts are turning on devising strategies that enable products to be created, manufactured, and delivered based on “real-time” demand. 2

All these aspects are reflected in the business model concept that aims to understand how to create and deliver value for customers, generating, at the same time, value for the firm. 3 In other words, business models help to transform the top management’s strategic decisions in operative actions. More recently, the business model concept has progressively attracted the attention of researchers and managers due to its increasing importance in coping with turbulent environments such as the footwear industry. Consequently, the business model is not only seen as the instrument to design value creation and distribution processes, but it also represents the means to plan and execute adaptation strategies. As such, it has been used to analyze firms’ reactions to competitors’ strategies or to adjust product characteristics to changing market preferences or consumers’ behavior. 4 Nevertheless, to the best of our knowledge, this conceptual framework has not been properly developed to analyze the response of firms to exogenous shocks such as financial and economic crises or disruptive changes in the competitive environment. This article aims at filling this gap by focusing on one of the most significant events that hit the industry in the past decades: the entry of China into the World Trade Organization (henceforth WTO) at the end of 2001.

In order to study the effects of this rare event on the footwear industry business model, using both archival and survey data, a rich longitudinal analysis of the Portuguese footwear industry is conducted over a period of more than 20 years. This is a particularly interesting setting for several reasons. Portugal is a country with a long tradition in the footwear industry, mainly producing leather shoes destined to foreign markets with Europe being the main target of such exports. Moreover, although Portuguese footwear manufacturers, similar to other countries such as Italy and Spain, are small- and medium-sized, their average size is higher than the average of footwear manufacturers in the European Union. Finally, focusing on a localized territorial scope—such as Portugal—allowed us to analyze the local competitive environment more thoroughly and define the boundaries of our analysis.

The empirical outcomes highlight how the shock acted as a turning point that led Portuguese footwear producers to a relevant change in their business model, stressing features such as speed and flexibility in the manufacturing process, quicker response to customer preferences, and, in specific cases, the development of new product lines based on the creation of own brands offered directly to final consumers. The results point out to another important finding. The successful transition to a new business model in the post-shock era was not the outcome of a spontaneous adaptation process but rather the result of a planned transition orchestrated by a key industry actor, Portuguese Footwear, Components, and Leather Goods Manufacturers’ Association (APICCAPS).

Background

The business model concept has gained increasing popularity over recent years and has become a frequent object of study in management research. For instance, a search of academic articles using the term “business model” revealed 166 such articles between 1975 and 1994, and 1563 between 1995 and 2000. 5 Despite the proliferation of studies on business models, there is still lack of consensus on what a business model is. One of the first definitions of the term business model was proposed by Timmers who defined it as “an architecture for the product, service and information flows, including a description of the various business actors and their roles; a description of the potential benefits for the various business actors; a description of the sources of revenues” (p. 2). 6 Later, definitions focused mainly on identifying the components of a business model. For example, Osterwalder and Pigneur argue that a business model can be described as a canvas through several basic building blocks that cover some of the main areas of a business, such as customers, offer, infrastructure, and financial viability that illustrate how a company intends to make money. 7 Similarly, Johnson et al. identify four elements of a business model (i.e. customer value proposition, profit formula, key resources, and key processes) that, when they work together, create and deliver value for customers. 8 Recent surveys of the literature on business models indicate that discrepancies in the uses of constructs, definitions, and operationalization are still present. 9

One possible approach to solve the puzzle of which definition should be adopted is to choose the definition that best fits the empirical context in which a business model is analyzed. A finer-grained distinction could be, for instance, made by choosing which components of a business model to analyze based on industry characteristics. For instance, in a study of airline business models, components were identified starting from the business model conceptualization of Osterwalder and selecting among the nine components identified by this author the ones that would best describe an airline business model. 3 This filtering process led to the selection, and in certain cases, renaming of the six most suitable components, including value proposition, revenue streams, network, distribution channels, fleet structure, and alliances. 10 Thus, a context-specific definition of a business model promises to provide a more precise identification of which elements or components should be considered in the analysis on a case-by-case scenario.

In this study, we follow the definition of business model proposed by Zott and Amit who proposed a relational view of business models, defined as the structure, content, and governance of transactions. 11 This definition is particularly suitable for the analysis of the relationships chain that involves manufacturers, distributors, and consumers. Specifically, given our interest in exploring business models in the footwear industry, we look at different models of production that can be described along a continuum having “scheduled-based production” and “ready-fashion” at the two opposite ends and “fast-fashion” or “semi-planned production” in the middle. Building on previous research, 12 we adopt a definition that stresses the following elements as necessary parts of a business model: (1) market performance (measured in terms of total turnover), (2) customers (viewed as geographic target markets), (3) placement strategies to reach target markets, and (4) costs borne by firms.

Business model adaptation and exogenous changes

Gradually, research on business models has been moving from a static to a dynamic view of business models. In other words, instead of describing a business model in a particular moment of time, scholars have begun to examine how business models evolve, change, and reconfigure over time. While this nascent stream of literature has been focusing mainly on business model innovation, other terms have started to appear such as “evolution,” “reconfiguration,” and “adaptation.” 13 –15 While innovation, when attached to business models, is defined as the process by which firms actively innovate their business model to disrupt market conditions, the focus of this article is on how business models change in response to an external trigger. These changes have been defined as business model adaptation, that is, the process by which firms align their business model with a changing environment. 15

The idea that firms respond to external stimuli by changing or reconfiguring their strategy and practices is well established in the literature. With respect to business model adaptation in response to external stimuli, previous research has analyzed how business models adapt to changes in the competitive environment and changes brought by new technologies. 16,17 Other studies have linked changes in business models to unusual events or shocks. For instance, using a large sample of Norwegian firms across several industries, Saebi et al. studied how managers introduced changes in their business models such as increasing sales efforts to new customer segments in the aftermath of the 2008 financial crisis. 15 Using a qualitative approach, Bogers et al. studied business model evolution by looking at one single firm in the airline industry. 18 Despite using distinct methodological approaches, both studies reached the conclusion that business models are not immune to external changes.

The limited amount of studies linking business model adaptation to the external environment calls for more studies in this domain. This topic is of critical importance as failure to adapt business models on time can result in diminished returns and, in extreme cases, in bankruptcies and firm death. An interesting opportunity is provided by the possibility to study how and if new business model paradigms emerge in the aftermath of exogenous events. Previous research has documented that disruptive changes, such as in case of exogenous shocks, interrupt equilibria making it possible for novel organizational mutations, intentional or random, to take hold. 19 Subsequent periods of flux endure until a dominant design emerges. This punctuated-equilibrium perspective studies firm evolution as being composed of two distinct and recurring phases: (1) long periods of quasi-equilibrium, during which firms make small changes in structure and activities and 2) brief periods of disequilibrium, during which deep change can take place. 19,20 In light of these theoretical developments, we posit that business model adaptation could result in the establishment of a new and shared dominant business model paradigm following a shock.

Business model adaptation and central network actors

What is the role of networks in the process of business model adaptation? This is an important yet understudied question since firms are embedded in networks made of competitors, collaborators, suppliers, and institutions, among others that affect firm strategy and behavior. 21 Thus, we argue that the choices firms make with respect to their business models may be influenced by their networks (i.e. the ties they maintain with other actors). While networks emerge and develop as actors make choices about whom to connect with and what to transact without being guided by any specific actor, other networks are intentionally shaped by one or more actors. 22,23 Evidence of this latter form of networks has been found, for instance, in supply chain networks as well as in entrepreneurial networks and innovation networks. 24 –27 Orchestrated networks are characterized by the presence of key agents also known as network “orchestrators” that “act as a broker to plan and coordinate the activities of the network as a whole.” 22

Orchestration can take two separate forms—closed- or open-system orchestration—depending on the role played by the central network agent. 28 Closed-system orchestration is the set of purposeful and deliberate actions undertaken by key agents to coordinate and harness “the dispersed resources and capabilities” (p. 659) of network members. 29 These key agents are typically self-interested and have as a primary goal the maximization of their own benefit. Such actors are often referred to as hub firms or anchors 30 and can be found in R&D consortia as well as government-sponsored programs. In an open-system orchestration, instead, central actors in the network are mainly focused on supporting members’ dispersed and largely independent search for new business opportunities rather than trying to extract value from members as in the case of closed-system orchestration. Business incubators and associations of small- and medium-sized enterprises are examples of open-system orchestration.

Finally, previous research has indicated that orchestration should be considered as a set of evolving rather than static actions. 31 However, the same authors consider network orchestration as an endogenous process where the orchestrator works to address emergent dilemmas disregarding the possibility that action could also be triggered by external and episodic events. This, we believe, is an important limitation which we address here by proposing that the ability of an orchestrator to influence the evolution of an industry network is also driven by external changes.

Data and methods

This research aims to explain how the business model paradigm of the Portuguese footwear industry changed in the face of an exogenous rupture in the system: China’s entry into the WTO in 2001. To do so, we build on a case-based method that is particularly suitable for understanding poorly understood phenomena 32 with multiple and complex elements that evolve over time. 33 Our choice of a longitudinal approach with a single case study 32 is grounded in the fact that this approach is particularly suitable for studying the evolutionary processes of business models. 13 Our study extends over the period 1995–2016, although our main focus is on the years preceding and following China’s entry into the WTO in 2001. We identify three subperiods that reflect our interest in exploring changes in business models before (1995–2001), during (2002–2005), and after (2006–2008) the shock.

We draw on several data sources that include both survey data as well as data obtained from APICCAPS’ annual reports, and EUROSTAT. Financial and accounting information was obtained through the Sistema Anual de Balances Ibéricos (SABI) database which holds accounting data on Iberian companies. SABI’s data are available only from 2002 onward which does not allow us to compare the pre- and post-shock results in terms of market performance. However, this should not be a problem as previous studies have also limited their analysis to post-shock effects. 15 These data are then confronted with the results from the quarterly business conditions survey that has been administered to the members of APICCAPS on an ongoing basis since 1995. We have therefore access to both primary and archival data which allows us to triangulate different sources effectively.

We chose the Portuguese footwear industry for our case study for several reasons. First, the firms populating the Portuguese footwear industry were not immune to the significant changes that took place in the external environment following China’s entry into the WTO in 2001 and reacted to them by modifying the way they delivered and captured value (i.e. their business model), making it an ideal context in which to study how shocks affect structure and strategy. Second, this setting is attractive because orchestration processes were central to how firms reacted to the shock, thus illustrating how business associations add value for their members. 32 Finally, several contributions have used the broader fashion industry as an empirical setting, 2,34 including contributions focusing specifically on business models in the footwear industry. 12

The Portuguese footwear industry

Although footwear production has a long tradition in Portugal, in the last 20 years, the industry went through a profound transformation and is often presented as one of the Portuguese economy’s success stories. Footwear now accounts for more than 6% of the country’s manufacturing employment and almost 4% of Portuguese exports. Portuguese footwear exports have the third highest unit price among the world’s leading exporters, after Italy and France. This is partially explained by Portuguese specialization in leather footwear which is an expensive material compared to other countries, such as Spain, that export a higher proportion of rubber, plastic, or textile shoes. Around 95% of the Portuguese footwear manufacturers’ production is destined to foreign markets, with Europe being the main target of such exports.

Although Portuguese footwear manufacturers, similar to other countries such as Italy and Spain, are mostly small- and medium-sized, their average size is 26 employees which is higher than the average of footwear manufacturers in the European Union. The Portuguese footwear industry is prevalently located in the north of the country and is organized into two geographic clusters separated by some 80 km: the towns of Felgueiras and Guimarães forming one and the towns of Feira, São João da Madeira, and Oliveira de Azeméis forming the other. These two clusters account for about 75% of the sector’s employment and exports. This geographic concentration has been a key strategic advantage for the industry, allowing for an easier access to services and materials needed for the production, a faster diffusion of knowledge, and the creation of both formal and informal networks.

Most Portuguese footwear firms specialize in shoe manufacturing itself, not being present in upstream or downstream segments of the industry nor on the related leather accessories industry. However, sometimes, especially in the case of larger firms, a few players have integrated downward, retailing shoes under their own brands. There are also several cases of quasi-integration, both upstream and downstream, with legally independent firms, owned by common shareholders, being present at different levels of the value chain. Figure 1 shows an overview of the vertical structure of the industry.

The vertical structure of the footwear industry.

Adapting to an exogenous shock

Between 1974 and 1994, the Portuguese footwear industry developed at fast pace: the number of companies increased by 143%, employment by 286%, production by 626%, and exports by more than 1600% (Table 1). Portuguese low-production costs, particularly labor costs, coupled with easy access to large markets resulting from proximity and, since 1986, membership in the European Economic Community, sustained this growth. These conditions guaranteed the international competitiveness of local producers and attracted foreign investment from countries such as the United Kingdom, Germany, Denmark, and France. The main value proposition of Portuguese firms, in this period, was to deliver long series at low prices for large global brands and retailers such as Marks & Spencer. Several international brands, such as Clarks (United Kingdom), Rohde (Germany), and ECCO (Denmark), had their own manufacturing facilities in Portugal, which were among the largest of the Portuguese footwear industry.

Overview of the Portuguese footwear industry evolution (1974–2014).

This state of affairs was disrupted by China’s accession to the WTO in 2001. China offered much lower labor costs and a productive capacity that Portugal could not match. Building on its economic reforms, China was able to rapidly expand trade and attract high levels of foreign investment, just like Portugal had previously done, but on a much amplified scale. Between 2000 and 2005, the Chinese footwear exports increased by 120%, raising China’s share of the world footwear market from 21.6% to 30.7%, and this trend continued in the following years. This put enormous pressure on European producers and particularly on Portuguese producers that saw their competitive advantage overturned.

We treat China’s entry into the WTO as an exogenous shock affecting the Portuguese footwear industry and study how Portuguese firms responded by implementing significant changes in their business model. The analysis of footwear business models is structured following the approach proposed by Pirolo et al. who define business model in this industry as a model that comprises four dimensions, namely market performance, customers, placement strategies, and costs. 12 Given our interest in understanding how and if the footwear business model changed in the aftermath of China’s entry into the WTO, we follow previous studies by focusing on each dimension individually before detecting an overall change in the business model. 35

China’s accession to the WTO had a double negative impact on the Portuguese footwear industry. On the one hand, Portugal lost appeal to large international buyers for whom the production cost economies obtained in Asia for large orders more than compensated any additional transportation costs. As a result, Portugal was no longer competitive for buyers looking for long series at low prices and the increased competition resulted in a decrease in Portuguese producers’ market share. On the other hand, several large foreign firms closed their factories in Portugal or significantly reduced their activity, and transferred them to Asia.

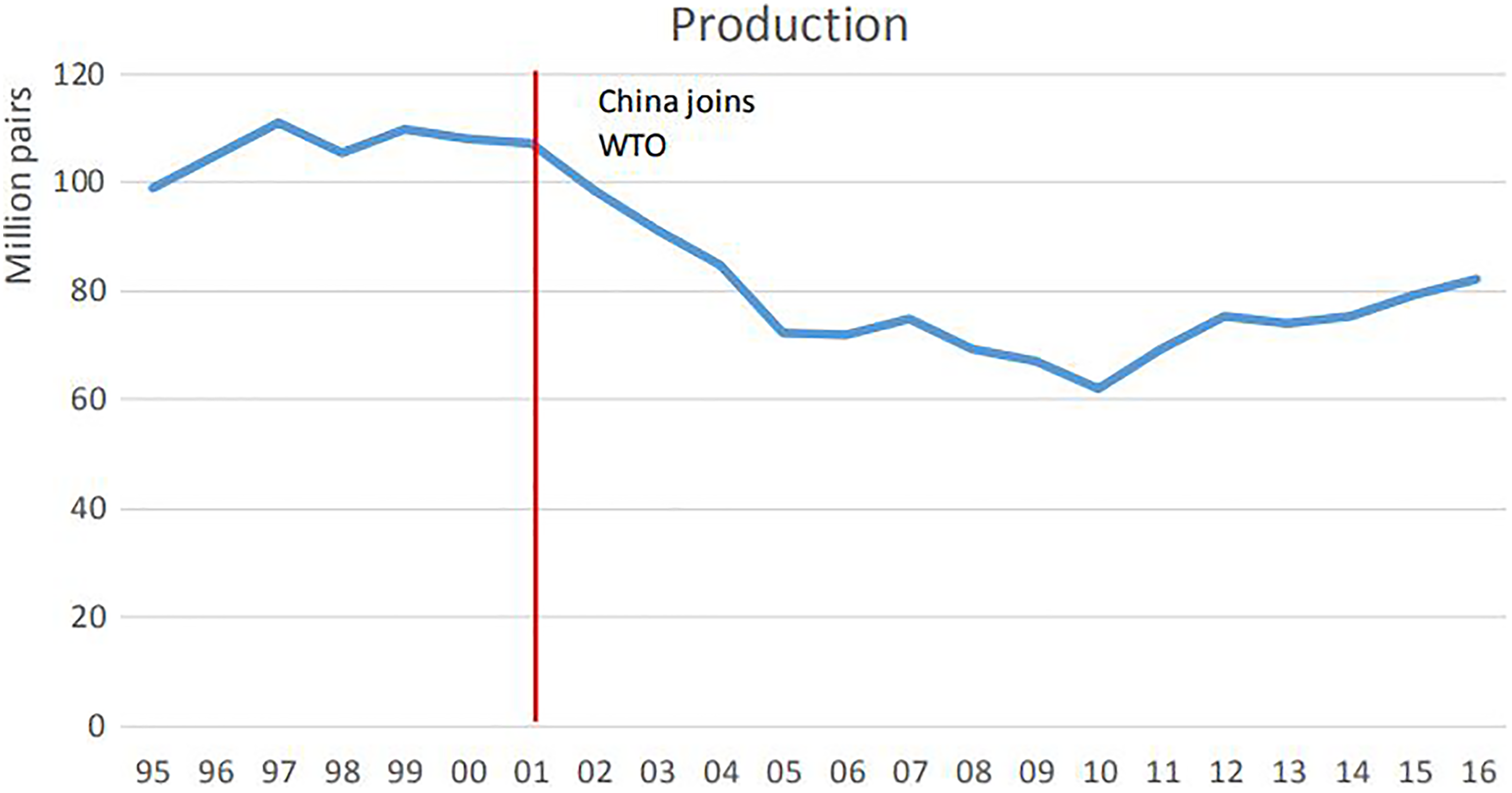

The impact of the shock on market performance is evident in the responses to the question “How were the business conditions for your firm in the previous quarter?” included in APICCAPS’ quarterly business conditions survey. The results (Figure 2) clearly indicate a sharp deterioration of perceived conditions between 2002 and 2005. However, this is followed by a recovery from 2006 through 2010—except for the immediate aftermath of the 2008 global financial crisis—and a relatively stable, predominantly positive, situation since then which is indicative that the Portuguese industry was able to reestablish its competitiveness on new grounds. A sharp decline in 2002–2005 is also visible when analyzing data on footwear production, in volume (Figure 3). The decline is followed by a milder fall up to 2010 and a clear recovery from then on. Recovery starts earlier, already in 2005, if the value of production is considered instead, as the unit price of Portuguese footwear has been growing consistently, which is further evidence that the industry was able to find a new successful business model. Data on footwear firms’ turnover and profit extracted from SABI, although only available from 2002 onward, show a pattern that is consistent with the previous results. The average turnover of the top 100 firms in the post-shock window was 30% higher than that in the shock period, while their average profit was 114 times higher. We performed several analyses using different sample sizes but did not find significant variations.

Quarterly business conditions of the Portuguese footwear manufacturers. WTO: World Trade Organization.

Annual production in pairs of the Portuguese footwear manufacturers. WTO: World Trade Organization.

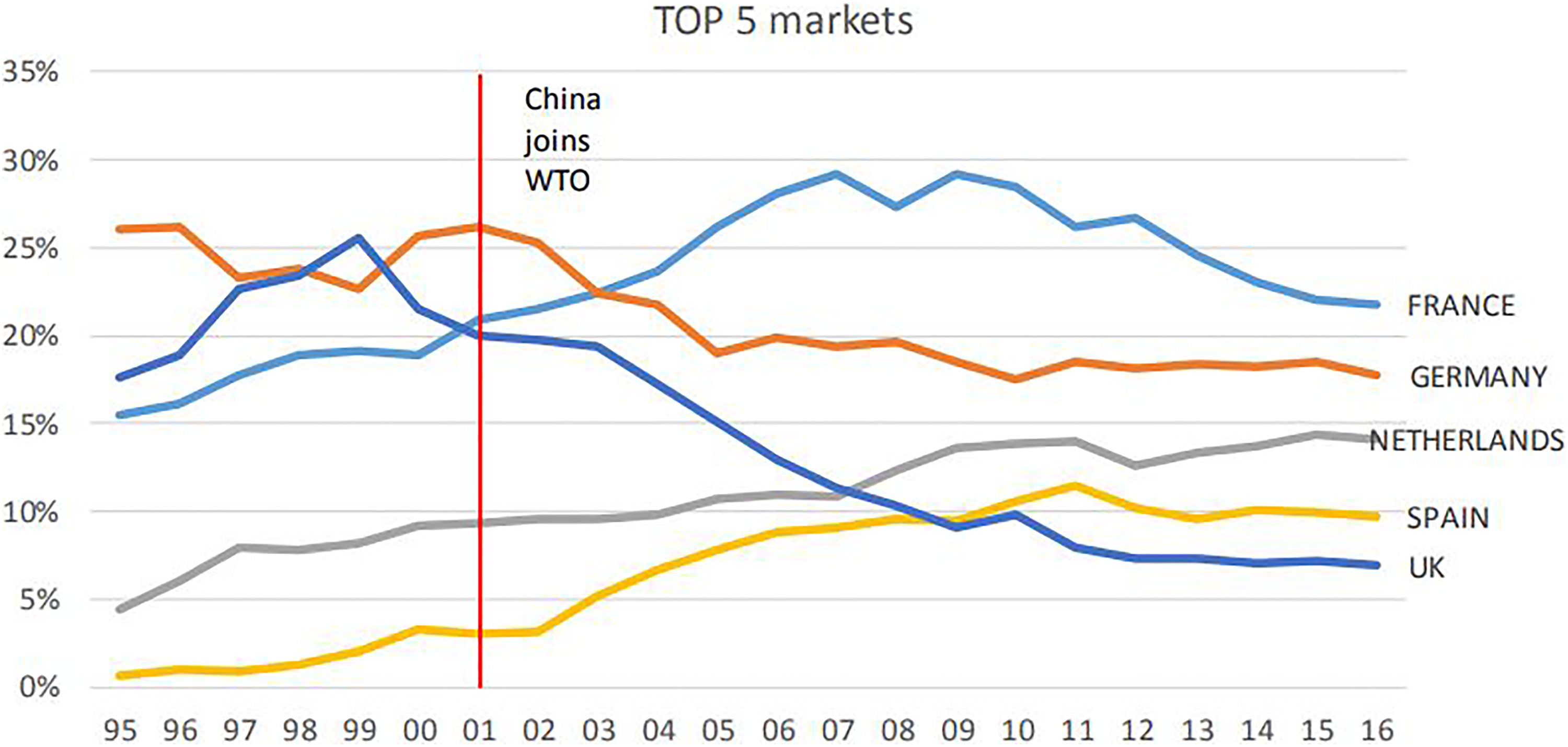

The impact of the shock is also clear in terms of geographic target markets. Portuguese footwear firms had been traditionally exporting to clients located in neighboring countries, confirming that geographical proximity facilitates buyer–supplier relationships. 36 The shock reinforced this behavior. In fact, the percentage of Portuguese footwear exports going to the European Union went up from 67% in the pre-shock period to 74% during the shock and 81% in the post-shock period. This result was also largely due to the increased Chinese competition that made it harder for the Portuguese firms to compete in large non-European markets such as the United States and because the competitive advantages that the Portuguese firms developed under the new business model were particularly effective at moderately short geographic distance. But, inside Europe, the relative importance of some markets changed quite dramatically. In 1999, one year before China joined the WTO, the United Kingdom was still Portugal’s largest export market and, together with Germany, represented almost half of Portuguese exports. By 2005, this was down to one-third and the United Kingdom had fallen to the third place among main markets (Figure 4). Besides the top 5 markets, exports to Denmark, another relatively important market, followed a similar trend. These results are directly justified by the closure or reduction of activity of the Portuguese factories of firms such as the United Kingdom’s Clarks, Germany’s Rohde, and Denmark’s ECCO, and by the fact that the United Kingdom and Germany became important buyers of Chinese footwear.

Top 5 markets for the Portuguese footwear manufacturers. WTO: World Trade Organization.

As these countries’ share in Portuguese exports fell, others’ have increased. More specifically, France became the main market for Portuguese footwear, with its share going from an average of 18% in the pre-shock period to 28% in the post-shock period. The Netherlands and Spain also gained considerable share. Being unable to compete head-to-head with the Chinese footwear producers in the supply of large orders, Portuguese manufacturers adapted their business model by focusing on market segments of lesser volume but of greater value added. Rapid response and flexibility in production, accepting very small orders, became key to their market positioning and were particularly relevant for nearby buyers such as those located in Spain and France. Portuguese footwear firms also invested considerably in the development of their own collections, instead of passively responding to buyers’ requirements, and some invested in the creation of their own brands. Additionally, they started competing for the orders of smaller retailers instead of the large international brands as done previously. By 2009, while the Portuguese export value was about 10 times smaller than the Chinese one, its average export price was about 8 times higher. 37

The new business model required a significant change in the commercial strategy of Portuguese footwear firms. In the past, these firms had mostly worked as subcontractors for a few large buyers that required little active commercial activity. This meant that often it would be the buying firm, or some intermediary working for it, that would contact the manufacturers asking for a particular order. Following the shock, instead, the Portuguese footwear manufacturers had to actively seek customers for their own collections which they did by stepping up international promotion initiatives (Figure 5). The number of companies attending international fairs as well as the number of international events with Portuguese presence almost doubled in the post-shock period compared with the pre-shock period. This finding confirms previous theoretical research arguing that managers are more motivated to take action and break inertia when confronted with uncertainty. 38

Commercial strategy of the Portuguese footwear manufacturers. WTO: World Trade Organization.

Additionally, many firms invested in creating new brands, such as the Lemon Jelly brand launched by Procalçado, or buying existing ones, such as the acquisition of the British Fly London by Kyaia. In terms of distribution, a large number of Portuguese footwear producers rely either on a private distribution network or on intermediaries, and very few brands use flagship stores to distribute their products, a pattern that is consistent with previous research in other contexts such as Italy. 12 Another aspect suggesting a more proactive posture of Portuguese footwear firms is their behavior in terms of protection of intellectual property, which has little tradition in the industry. In 2002, the Footwear Technological Centre of Portugal (CTCP) set up an office to assist firms on such matters, and in the following years, the registration of brands, models, and patents increased exponentially, as the Portuguese footwear brands became increasingly a desirable target for imitation and counterfeiting (Figure 6).

Registration requests supported by CTCP.

The available evidence does not suggest that the shock significantly changed firms’ cost structure. It might be suspected that the new business model, with average shorter orders and more demanding development and commercial activities, might have required higher labor costs as a percentage of turnover. However, our data do not confirm this. If anything, this percentage fell moderately in the post-shock period (2006–2008). Several factors may have contributed to this result. During the shock period, due to legal restrictions on layoffs, firms accumulated slack, which somewhat increased their labor costs. Slightly increased sales and exports in the post-shock period may therefore have allowed for a reduction of their weight on turnover. Confirming this, average labor costs again increased in 2009, when production fell anew. On the other hand, many of the foreign-owned firms that left Portugal in the shock period were, in relative terms, among the best-paying employers. By itself, their departure will then have led to a reduction in average labor costs. Further, their departure greatly reduced demand and increased supply in the footwear labor markets, changing the equilibrium to employers’ advantage.

In a nutshell, the Portuguese footwear industry responded to the external shock by embracing new competitive logics which consisted in the transition from a “passive” business model, in which firms responded to large orders placed by few large buyers such as international retail chains and multinational footwear brands that would specify the design of the shoes to be produced, to an “active” business model, in which producers develop their own collections to be sold mainly to small retails chains, either under producer brands or on “private label,” and compete mostly on quality, design, and rapid response. This change required the development of new competences in product development, operations, logistics, as well as commercial activities. As a result, production and exports have been growing consistently over the last 7 years. These endogenous changes, however, were coupled with several initiatives orchestrated by APICCAPS which together resulted in an effective adaptation on the part of these firms.

APICCAPS as a network orchestrator

APICCAPS, the Portuguese footwear manufacturers’ association, was created in 1975. A distinguishing feature of APICCAPS, among Portuguese trade associations, is that since its inception, it did not limit itself to be an advocate for the industry. Since 1978, every 5–7 years, the association has published a strategic plan for the Portuguese footwear industry that guides its activity and tries to orchestrate the efforts of an industry composed of more than 1000 firms. These plans are the result of widely participated processes in which the association spends considerable time and resources, with the benefit of increased legitimacy. In these 40 years, these plans have inevitably evolved but a few common themes remain and have set the course for the industry and the way it dealt with the external shock analyzed here: acceptance of competition, innovation, and internationalization. Unlike many of its counterparts, in Portugal and abroad, APICCAPS did not take a purely defensive stance toward foreign competition. Instead, it embraced competition leading to a Schumpeterian renovation process and tried to stimulate its members to prepare for challenges ahead. Innovation and international promotion have been two priorities in terms of its activity.

Innovation efforts are mostly conducted through CTCP in which APICCAPS participates. Through CTCP, the association has been promoting R&D programs through a model where, for each initiative, a consortium is created involving scientific institutions, technology producers, and potential users of the technology. A particularly successful initiative, for example, was the Portuguese Footwear Factory of the Future (FACAP) program between 1995 and 1999 that led to the development of multiple equipment for the industry. Anticipating problems ahead, the generation of solutions that would increase productive flexibility was a central goal of the program. FACAP was key to the development of water jet leather–cutting technology which was extremely significant for the increase in flexibility of Portuguese footwear manufacturers and, therefore, instrumental in the response to increased competition from Asia.

For more than two decades, APICCAPS has been incentivizing and supporting its associates to develop international promotion initiatives. In the first stages of these efforts, when Portuguese firms had very little experience in dealing with international markets, this was done mostly through the organization of a professional fair in Portugal, MOCAP, through which the association tried to attract international buyers. Progressively, however, the focus was moved to the participation in fairs abroad. APICCAPS plays a dual role regarding these activities: on the one hand, it negotiates the Portuguese participation with the organizers, logistic providers, and other suppliers, allowing associates to benefit from increased bargaining power, and on the other, it tries to obtain external funding to support this sort of initiative. The main trigger to this shift has been once again China’s accession to WTO which increasingly made it clear that the presence abroad was more effective than attracting buyers to Portugal. Therefore, the industry stepped up its efforts abroad, by involving more firms in fairs and by including more fairs in the promotion programs (Figure 5). Such behavioral change was driven not only by the necessity to serve new markets but also by a higher recognition by these firms of the role that the association could play as a tertius iungens between Portuguese footwear companies and new clients. 39 Thus, the shock legitimated the role of APICCAPS as a network orchestrator as the Portuguese footwear companies realized the value of a higher level of embeddedness in the global footwear industry network compared to a more peripheral position. Figure 7 summarizes our findings by illustrating the coevolution of business models, the network orchestrator, and the external environment.

Illustration of the Portuguese footwear business model adaptation. Note: This figure is not based on actual measurements but rather meant for illustrative purposes.

Conclusion

Adopting a dynamic approach to the study of the business model, this article explored how business models change in response to variations in the competitive environments. More specifically, the results of the study indicate that, on the one hand, new relevant business models emerge in response to exogenous events that affect the industry and on the other hand, the emergence of these new business models may be influenced by the social structure in which firms operate. To explore these intuitions, the Portuguese footwear industry has been chosen as the empirical setting, analyzing how firms in this industry modified their business model when faced with a major exogenous event represented by the entry of China into the WTO in 2001.

The Chinese accession to the WTO can be considered a disruptive occurrence because it put significant competitive pressure on European footwear manufacturers, particularly impacting those that were highly exposed to international markets such as the Portuguese ones. This has led the Portuguese footwear companies to review their business model in order to cope with the price-based competition of Chinese producers. Among all the changes adopted by the Portuguese footwear producers, perhaps the most noteworthy is the adjustment made in their commercial strategy. Portuguese footwear producers, traditionally, responded to large orders placed by a few large international buyers. In the aftermath of the shock, this “passive” business model was replaced by an “active” model in which manufacturers put more emphasis on design and marketing activities with the goal to sell their products to small retailers and distribution chains. This process required the development of new competences in product development, operations, logistics, as well as commercial activities which was gradually achieved through the support of a key industry player—APICCAPS—that orchestrated the network of relationships inside the industry. In sum, this change in business attitude by the Portuguese footwear firms indicates that severe negative shocks require an equally strong response, based on an adaption strategy aimed to align firms’ business model with the changed competitive landscape in a rapid and effective way.

As with any research, this study comes with some limitations that outline the directions for future research. First, the nature of the exogenous shock we focused on in this study may pose some limitations to the generalizability of our results. Although China’s entry into the WTO took place in 2001, disrupting significantly the equilibria of the footwear and other manufacturing industries, this event and its consequences were to a high extent predictable. Thus, our results could represent an optimistic account of footwear firms’ ability to adapt their business models in the face of an exogenous shock. To that respect, it would be interesting to explore in this or other settings business model adaptation in the aftermath of an exogenous and unexpected event.

Second, it is important to underline that most of the Portuguese footwear production relies on the use of leather, corresponding to 80% of the pairs produced and to 90% of the production value in 2016, for example. Heavy specialization in high-quality materials has been a source of competitive advantage for Portuguese footwear producers in the past years and helped these firms weather the uncertainties in the post-shock period. Yet, new players such as Belgium and the Netherlands focusing on cheaper materials such as rubber are gaining momentum which may pose a threat for the Portuguese firms’ future growth. To that respect, two distinct business models are worth noting here. One, where manufacturers mainly export their own production and another where they reexport footwear imported from other sources. The latter model has been gaining momentum especially in countries that have limited manufacturing activity. Future studies may explore this additional challenge faced by countries such as Portugal or Spain that have a more consolidated manufacturing tradition.

Finally, the strengthening of its position outside the European markets should be seen as a priority for the Portuguese footwear industry as diversifying the markets served is a way to reduce the threats associated with future downturns. Recent data seem to confirm this trend as countries such as Australia and the United States have registered three-digit growth in 2016 compared to 2011. One example of a company that has heavily focused on nontraditional markets for the Portuguese footwear companies is the brand Josefinas for which the United States has become the biggest market representing 35% of the total sales. Future studies may explore the role that such pioneering firms play in the industry’s internationalization process in nontraditional markets.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.