Abstract

With the intention to analyze the effects of different board characteristics on the insurance companies’ performance, this research article explores the impact of board gender diversity and size on the performance of the insurance companies in Croatia. It analyzes the impact of characteristics of both boards, the board of directors and the supervisory board on corporate performance. The analysis, conducted using dynamic panel model, covers all insurance companies in Croatia operating in the 2007–2013 period. The main findings suggest that gender diversity at the top positions is not critical for financial success. Specifically, it is established that women acting as presidents of supervisory board deteriorate insurer’s performance measured by return on assets (ROA). This is also the case when more women are present in the board of directors. Moreover, the findings of the model measuring performance by both ROA and return on equity demonstrate that financial performance of insurance companies is negatively influenced by the number of members of the board of directors. The article upgrades the existing research by providing new support for the effects of board structure on performance in insurance industry, with specific reference to effects of gender diversity. Moreover, this study extends the existing literature in this field by introducing two corporate governance mechanisms in the analysis, that is, both the board of directors and the supervisory board. Furthermore, it is, to the authors knowledge, the first attempt to describe the effects of diversity in terms of gender on performance in the insurance sector.

Introduction

Corporate governance has a significant impact on performance, which has been one of the most studied issues in the last couple of decades. 1 More especially, composition of board of directors is one of the mostly investigated subjects within corporate governance studies, as this affects board decision-making processes, the way board performs its functions and roles, effectiveness of the board, and consequently firm financial performance. 2 –4

Traditionally, most of the corporate governance studies investigated factors such as the independence of the board members, 5 share of insiders on the board, 6 or board size. 7 More recently, board diversity, with particular emphasis on the gender of directors, has become an emerging topic of interest, especially after recent movements that bring legal requirements for greater women participation on board positions. 8 A central question is whether adding women to boards contributes to board role and task performance and ultimately corporate performance. 9 It is important to provide additional insight into board diversity and diversity in perspectives as it can influence various aspects of corporate behavior, as decision-making, boardroom behavior, board activities, and outcomes. However, in spite of many researches in this field, additional research is needed to gain a deeper knowledge about the benefits of board diversity. 10 Especially, we still lack a clear understanding on gender diversity impact, as gender diversity of the board so far has been relatively less examined field. 11 This is especially true for the insurance sector, where high-quality corporate governance is a relevant factor for ensuring its sustainability. Different corporate governance factors were found to have impact on performance, such as “recruitment policy, staff training and development, communication policy and performance evaluation.” 12 However, as some authors emphasize, 13 board diversity may also have an important role that should not be neglected.

Insurers play an important role in assuring general protection and security of their stakeholders while at the same time encourage economic growth. 14 Consequently, the relevance of the insurance sector and the nature of its business activities make its corporate governance mechanisms, problems, and activities industry-specific and distinct. In addition, the reduction of systemic risk, one of the basic goals of industry regulator, can be in collision with shareholder’s principal goal, the maximization of shareholders’ interest, that is, profit.

Monitoring is one of the basic activities of corporate governance related to the board of directors. 15 Most studies that investigate the impact of board structure on corporate performance in the financial sector, as it is usually the case, refer to banks. 16 –18 The insurance industry, as an object of analysis, is represented to a much lesser extent. 19 –21 Existing studies have mainly analyzed the connection among several different corporate governance mechanisms and performance of insurance companies. Still, as mentioned previously, they do not encompass an important feature of the boards that occupies the general public, that is, gender diversity. This article contributes to this field of research, by providing additional insights regarding gender diversity of boards and its influence on performance of insurance companies. Women in their business environment, as compared to man, show distinct styles, approaches, and perspectives in work. This eventually can have significant different influences on organizational outcomes, including corporate performance. Board size, as an additional element, can also be a significant predictor of performance, so its influence on the performance of insurance companies is explored as well.

Thus, through this research, we focus on the companies in insurance industry in Croatia and influence of two dimensions of board structure, that is, board size and board gender diversity on financial performance of these companies. Specifically, we will try to find an answer whether and how size of the board and diversity of the board in terms of gender impact financial performance of the insurance companies. The issue of gender diversity can be discussed from different aspects; however, through this article, we orient exclusively on the role that the board gender diversity has on performance of insurance companies.

This analysis has been conducted on the sample of Croatian insurance companies since most of the empirical research papers on this subject were done on the sample of organizations from developed economies, and studies in emerging and developing economies are still rare. 22,23 In this way, the findings of this study will contribute to the existing literature in the context of emerging insurance market such as Croatian due to the differences in its institutional and regulatory environment compared to developed countries.

The findings of this analysis will also be interesting in the context of the proposed (European Union) EU directive on improving the gender balance among nonexecutive directors of companies listed on stock exchanges which is meant to significantly increase the number of women on corporate boards throughout the EU by setting a minimum quota of a 40% presence of women among the nonexecutive directors of companies. Since this objective has already been imposed in legislative framework in many EU countries, it will be interesting to see whether this quota is justified in small and undeveloped Croatian insurance market.

Additional reason for this analysis lies in the fact that the Croatian economy has went through a long period of transition from a centrally planned to market-oriented one and had no preconditions for a greater degree of gender diversity development as some Western European countries had. In these former socialist countries, including Croatia, women mostly were not present in leadership positions in companies. This refers in particular to financial institutions such as insurance companies where leadership positions were commonly assigned to men. Therefore, we wanted to explore state and perspectives regarding representation of women as members of the board in the insurance industry in Croatia and whether there is a scientific basis for it in terms of its positive impact on companies’ financial performance. In addition, as some authors state, 24 national institutional features possibly affect the relationship between board size and performance. Therefore, by providing national specific examination on this relation, our results can be useful in deeper knowledge on the relationship between size of the board and company performance.

As regard to the existing knowledge in this field, this article primarily contributes by demonstrating the relevance and impact of board structure on corporate performance in the area of insurance industry with specific reference to how gender diversity as well as the board size affects insurance companies’ performance. Moreover, this study extends the existing literature in this field by introducing two corporate governance mechanisms in the analysis, that is, both board of directors and supervisory board. Furthermore, analysis is done on the sample of organizations from a developing economy, and it is, to the authors’ knowledge, the first attempt to describe the influence of gender diversity on corporate performance in the insurance sector.

The study is organized into following sections. After the introduction, the second section provides overview of main findings from the existing literature. Characteristics of the Croatian insurance market as well as the specifics of gender diversity in Croatian insurance market are given in the following section. Outline of methodology, including selection of variables, sample construction, and data sources as well as empirical methodology, is then presented. After reporting the results of the analysis, discussion of the relevant results and its implications, limitations, and possible future research streams are analyzed.

Board diversity and financial performance: Theoretical framework and hypothesis development

Existing research regarding financial sector has been largely focused on banks, so the knowledge on the influence of board composition on corporate performance in insurance industry is very scarce. Boubakri 25 emphasizes how “there is a rare international evidence on corporate governance impact on performance in the insurance industry compared to the literature on international corporate governance of typical public firms.”

Given that the main area of focus of our investigation is to determine whether there is an impact of board structure in terms of size and gender diversity on insurance companies’ performance, our initial aim was to cover with our literature review primarily those papers that examine the aforementioned characteristics. However, given the fact that the papers dealing with the topic of impact diversity in terms of gender on performance in the insurance industry is very scarce, first we give an overview of the literature that covers more general influence of gender diversity on corporate governance and performance. Then we develop our hypothesis to be tested on the sample of insurance companies in Croatia. This is followed by overview of selected existing researches on the relation between board size and insurer’s performance and development of hypothesis regarding board size and company performance.

Connection between diversity in terms of gender and company performance

Because of modern and postmodern cultural and social processes in the labor market, study of diversity at all organizational levels, and especially the top management positions, has received a special interest. When analyzing different impacts of variety on board functioning, it can be seen that social–psychological processes, such as the ones including “participation and interaction, the exchange of information, and critical discussion,” 26 will most likely influence board effectiveness. Among other sociodemographic factors, gender diversity has become a central focus of interest and has been recognized as a creator of value in corporate governance. 22,27

Regarding work environment and relationships at work, “an employee’s gender can illustrate differences in perception related to organizational structure, problem-solving style and view of work-related conflict,” 28 as well as to have significant effects on board inputs. 29 It has been recognized that women as opposed to man have different set of qualities, skills, and characteristics that can lead to their presence on the board create better results for the company. Various theoretical perspectives have tried to provide benefits of diversity and more especially benefits of a greater proportion of women on corporate governance and performance. Different arguments regarding gender diversity and its consequential influence on performance can be summarized into the following: (1) increased diversity of opinions in the boardroom that eventually results in heterogeneity of ideas, increased creativity, and innovation 30,31 ; (2) improving quality of decision-making as diversity influences problem solving and decision-making, as of variety of perspectives and alternatives provided 1,4,32,33 ; (3) gender diversity could lead to a better understanding of the markets that are also diverse in terms of gender, 34 especially as women are better suited to comprehend customer needs 35 ; (4) improving public image of a company 30,33,34 ; (4) bringing into boardroom helpful leadership qualities and skills attributed exclusively to women 36 ; (5) ensuring “better” boardroom behavior 30 ; for example, women are more likely to show greater attendance to board meetings than men, quality of monitoring is improved, 29 and communication is easier and more open among board members. 1,37

However, as of diversity in opinions, more diverse boards have higher potential for conflicts and more time-consuming and less effective decision-making. 4,36 This can especially be a problem if a quick response is needed. Diversity within boards is also considered to constrain board efforts to take decisive action and strategic changes that need to be initiated as of environmental turbulence or poor performance. 31 Additionally, when it comes to decision regarding investment and financial activities, women show higher aversion to risk than man, which can eventually influence organizational decisions regarding resource distribution. 22

Consistent with conflicting results from a theoretical standpoint, prior empirical studies also did not provide conclusive answers and provide mixed results regarding impact of gender diversity on performance. For instance, some authors 22,38,39 report significant negative connection among gender assortment and performance. Interesting results are provided by Adams and Ferreira, 29 who also found negative relation, but only for firms with strong governance and monitoring. Similarly, Abdullah et al. 40 report how impact of diversity on performance varies with companies’ characteristic. Some authors found no significant relationship, indicating women proportion in boards to have neutral effect on firm performance. 41 –44 In contrast to the above, some authors 4,32,33,45,46 report a positive relation between gender variety and different measures of performance. As far as the studies in the financial sector, Pathan and Faff, 47 for instance, found negative connection between gender variety and banks performance. As to our knowledge, the only analysis of the impact of board variety on performance in the insurance sector done by Garba and Abubakar, 13 among other diversity variables, found positive influence of gender diversity on company’s performance.

As noted from above, prior studies’ results are not conclusive and the question of relation between gender diversity and financial performance undoubtedly requires additional investigation. Accordingly, we want to test this relation and propose the following hypothesis:

Connection between size of the board and company performance

One of the corporate governance factors that have been a subject of many interest is the size of the board of directors. As considering the board size, “there is a trade-off between additional value-added expertise or monitoring benefits and disadvantages stemming from the coordination problem.” 48 Although larger board size can facilitate board functions and provide more quality decision-making processes, they can ultimately have problems of coordination and communication leading to decline in board effectiveness and consequently firm performance. 24

Similar to results regarding relation of gender diversity and performance, evidence on the connection of board size and performance are also unclear. While some authors report a positive connection between board size and corporate performance, 49 some 50 found no evidence of that connection. However, most research findings indicate a negative connection of board size and performance, 24,51 finding evidence which supports the notion that higher performance is connected to boards with less members. 52

In the context of insurance sector and empirical evidence, the expected influence of board size on insurer’s performance is also vague and unclear. For instance, Connelly and Limpaphayom’s 48 empirical evidence indicates that while board composition is positively related to overall profitability, solely board size is not related. Wang et al. 53 gave similar results with “board size and presence of CEO duality having negative impacts on the efficiency performance of property-liability insurers.” Some authors found a significant relation among board size and profitability ratio, 54 as well as higher efficiency scores 19 and higher levels of cash holding, 20 if the board is larger. In contrary to the above, the study by Hsu and Petchsakulwong 55 shows ambiguous connection of board size and efficiency performance among insurers, similar to Hardwick et al.’s 50 study.

As seen, previous empirical results reveal unclear relations. However, in accordance with the majority of previous research, we expect to have a negative connection between board size and firm performance and accordingly state our second hypothesis:

Characteristics of the Croatian insurance market and gender diversity in the boardroom in Croatia

Management and supervision of a company may be a function of one mechanism, that is, a function of management board in a monistic system, or it can be separated into two separate bodies: board of directors and supervisory board in the dualistic system. Croatian insurance companies can freely choose between a monistic or dualistic board structures. According to the Croatian Insurance Act, 56 “an insurance company may stipulate, by virtue of articles of association, that it will have a management board instead of both a board of directors and a supervisory board.” However, in Croatian insurance industry, there is a clear prevalence of a two-tier system of corporate governance; that is, all insurance companies have dualistic board structure including both board of directors and supervisory board.

The Insurance Act 56 regulates work of boards, and according to it, an insurance company must have two members at the minimum in the board of directors who manage the operations and jointly represent the insurance company. More specifically, they need to ensure operations are done according to the law, monitor risks, ensure internal controls as well as process of internal audit, and ensure quality accounting system and procedures. In addition to the obligations of the board of directors, the supervisory board authorizes decisions of the board of directors related to business policy, reviews annual report and other financial statements and the finance scheme of an insurance company, and overlooks the setting-up and annual program of operations of the internal audit and concerns related to internal audit’s annual report. Moreover, Croatian Agency for Supervision of Financial Services together with Zagreb Stock Exchange has published Corporate Governance Code for issuers trading on the Zagreb Stock Exchange. The objective of that Code is to provide guidelines of good corporate governance culture and protection of primarily investors, but also other interested stakeholders.

The period from 2007 to 2013 was included in our analysis, and during this period, there were on average 25 insurance companies. According to the Croatian Insurance Act, 56 insurance companies can get authorization for providing solely life or solely non-life insurance business. However, the composite insurance companies that were established prior to this provision came into force can continue to operate in both segments. In the observed period, as it can be seen from Figure 1, composite insurers dominated the market.

Structure of the Croatian insurance market by type of insurance company. Source: Authors’ calculation.

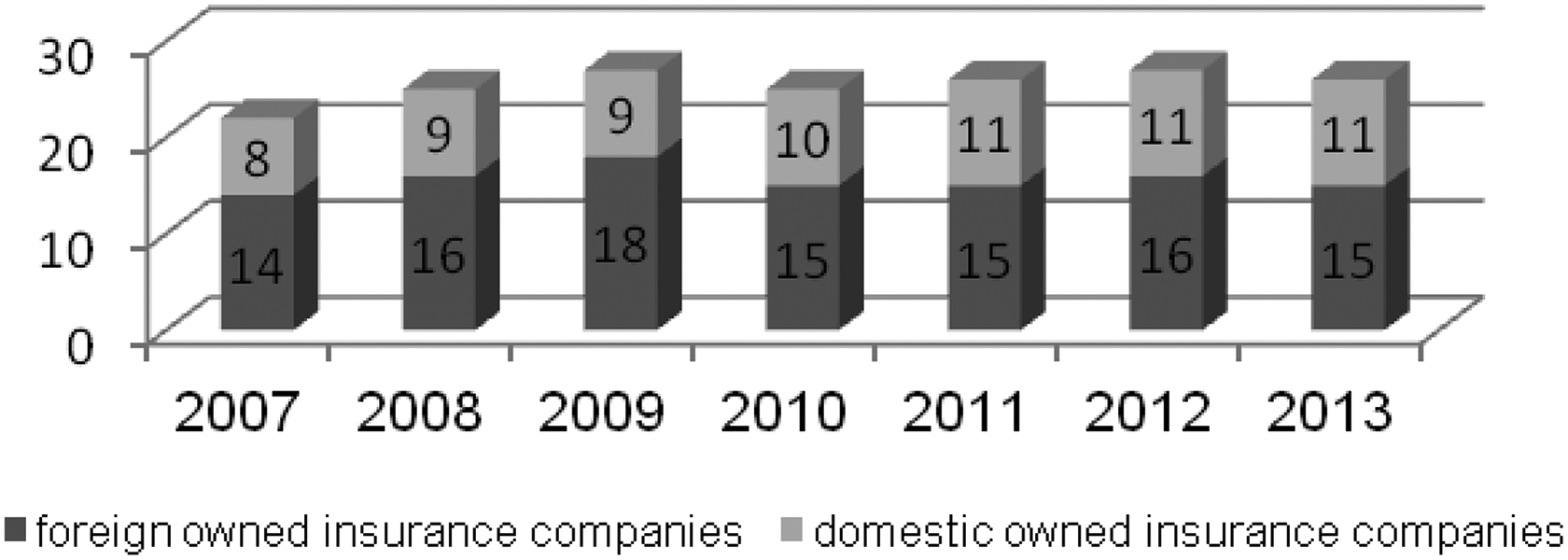

If an insurance company is controlled by non-Croatian shareholders that hold more than 50% of its equity, then it is considered to be foreign. As shown by Figure 2, share of foreign ownership is quite high. To be more specific, 61% of the insurance companies in the observed period were foreign owned.

Ownership of the Croatian insurance market. Source: Authors’ calculation.

Interesting to emphasize is that all of the insurance companies in Croatia are stock companies with only several of them publicly listed on the stock exchange.

Despite arguments in favor of gender diversity, it appears that segregation between gender still exists, and work situation is characterized by high horizontal and vertical segregation, 3 not just in Croatia, but also across the Europe. The legal status of women in Europe has, looking historically, progressed, but still effective equality is not present. It is possible to recognize many fields where gender gaps pertain. 57 This is especially the truth for the business and finance section, as documented by the European Commission. 58

According to the data from the European Commission 59 in most EU member states, although women present a significant proportion of the workforce, they remain to be less influential in the process of decision-making, especially at the top management hierarchy. As shown in Table 1, the situation is particularly disappointing in business leadership across companies registered in EU: In April 2015, women presented just 21% of board members, and in only 7% of the largest publicly listed companies, they occupied the position of board presidents.

Gender (in)equality in the decision-making bodies in the largest publicly listed companies (April, 2015).

Source: European Commission. 58

Gender equality is emphasized as a fundamental, central value of the Croatian Constitution and the basis for its interpretation, such as it is the basic principle of the acquis. Although in Croatia Gender Equality Act was enacted in 2003, a new version in 2008, there is still no legal framework which would prescribe, for example, a minimal number of women on companies’ boards. In addition to the Gender Equality Act, the Labour Act is another act to contain provisions for the prevention of gender discrimination in the field of work and employment. Still, the average representation of women as members of the board of directors in Croatia in the 2007–2013 period is about 15%. This is notably low considering the fact that women in Croatia constitute almost half of the total workforce (46% in 2013).

Data from Statistical Yearbook of the Republic of Croatia 2014, as presented by Table 2, show women dominate financial and insurance activities sector with 68.68% share. However, only a small portion of these women is holding a university degree (34.39%), a prerequisite for decision-making positions.

Women in business activities in Croatia in 2013.

Source: Statistical Yearbook of the Republic of Croatia. 60

If we take a closer look particularly at the insurance sector, as it can be seen from Figure 3, composition of board of directors in terms of representation of women as presidents of the board of directors in Croatian insurance companies varies widely across observed period, ranging from 19% to 37%. However, in the total observed period women acted as presidents of the board of directors in 27% of insurance companies on average.

Share of women as presidents of the board of directors in insurance sector in the 2007–2013 period (%). Source: Authors’ calculation.

The situation is more aggravated when we look at the proportion of women acting as presidents of the supervisory boards of the insurance companies in Croatia, which, in observed period, amounts to only 10%.

Methodology

Selection of variables

The variables used in the analysis are grouped into three categories including dependent variables, explanatory variables, and control variables. Table 3 provides a review of used variables.

Variables used in the research.

ROE: return on equity; ROA: return on assets.

Dependent variables comprise variables related to performance and include the measure return on assets (ROA) as well as the measure return on equity (ROE). As previously emphasized, most of the insurers operating in the Croatian insurance market are not listed companies; therefore, the authors followed Diacon and O’Sullivan 61 approach by using accounting measures of performance rather than market ones. Accounting-based measures present the management actions outcome and many authors 62 emphasize accounting-based rather than market-based measures of performance to be more suitable when analyzing the relationship between corporate governance elements and firm performance. Market-based measure, as Tobin’s q, is considered ambiguous when evaluating performance 63 as it is more oriented to future results and reflects expectations of the shareholders regarding future outcomes that can also be under influence of factors outside the managerial control. Thus, ROA and ROE, as accounting based measures, have been extensively used in the previous empirical research on board diversity and firm performance. 23,42,48,64 Since the aim of this research is to analyze the influence of several board characteristics on performance of insurance companies, profitability variable (ROA) was introduced in a model as a dependent variable. ROA is calculated by dividing insurer’s annual profits after tax by its total assets. Moreover, in order to ensure clear conclusion on subject analyzed and to diminish the influence of profitability measure used, an additional measure of profitability, that is, ROE variable, was included as a dependent variable. ROE is calculated as insurers after tax annual profits divided by its total equity.

Explanatory variables on board composition used in the analysis include gender diversity variables, that is, gender of the president of the board of directors (GPBD), share of women in the board of directors (Share_W_BDFM), and gender of the president of the supervisory board (GPSB). Variable gender of the president of the board of directors (GPBD) was introduced in the model as a dummy variable with 0 referring to male president and 1 referring to female president of the board of directors. Share of women in the board of directors (Share_W_BD) was calculated as total number of female members divided by the total number of members of the board of directors. Gender of the president of the supervisory board (GPSB) was also introduced to the model as a dummy variable with 0 referring to male president and 1 referring to female president of the supervisory board. Another variable regarding characteristics of the board is the size of the board of directors (LN_SIZE_BD), computed as natural logarithm of total number of members of the board of directors.

Control variables, size based on total assets (LN_ASSETS) and expense ratio (EXP), often controlled for in empirical research in the insurance field, were included to control for specific characteristics of insurance industry.

Company size is commonly reflected by different indicators, such as number of employees, level of sales, and assets.

65

Since these capture the same information, and due to the specific nature of the insurance companies, the author opted for the use of the natural logarithm of total assets. This is a proxy of company size, an approach implemented also in papers relating to insurance industry.

53,66

It is more difficult for smaller firms to write insurance premiums than for bigger ones. Furthermore, major insurance companies compared to smaller ones are expected to respond quickly to changes in the market, diversify the risks they accept in an effective way, employ more qualified labor power in an easier way, and in particular, benefit from the economies of scale concerning labor cost.

67

Expense ratio represents a variable often employed in studies dealing with determinants of insurance companies’ profitability. 68,69 Since expense ratio is cost ratio, its negative influence on performance is expected.

Sample construction and data sources

Although there are papers comparing board composition of mutual and proprietary insurance companies, 66 the sample consists only of proprietary insurance companies since all insurance companies operating in Croatia are fully independent stock insurers, with exception of one mutual that ceased to exist in 2002. Reinsurance companies were also excluded from the analysis, although at the time range covering this study, there was one reinsurance company active in the Croatian insurance market.

In terms of numbers, the research covers the entire market, that is, 25 insurance companies per year on average. It encompassed life, non-life, and composite insurance companies with an average of 10, 6, and 6 insurance companies per year, respectively.

Data on gender of the president of the board of directors as well as of the supervisory board were taken from the various issues of the annual reports called Croatian Insurance Market 70 and Insurance and Reinsurance Companies in the Republic of Croatia 71 published by Croatian Insurance Bureau. Moreover, variables share of women in the board of directors and the size of the board of directors were calculated also using the information from the abovementioned source.

Data on size of the insurance company based on total assets as well as ROA variable were calculated based on the data obtained from annual reports published by Croatian Financial Services Supervisory Agency. 72

Moreover, variables ROE and expense ratio were calculated using the data from balance sheets and income statements of particular insurance company available on web pages of Croatian Financial Agency.

Empirical methodology

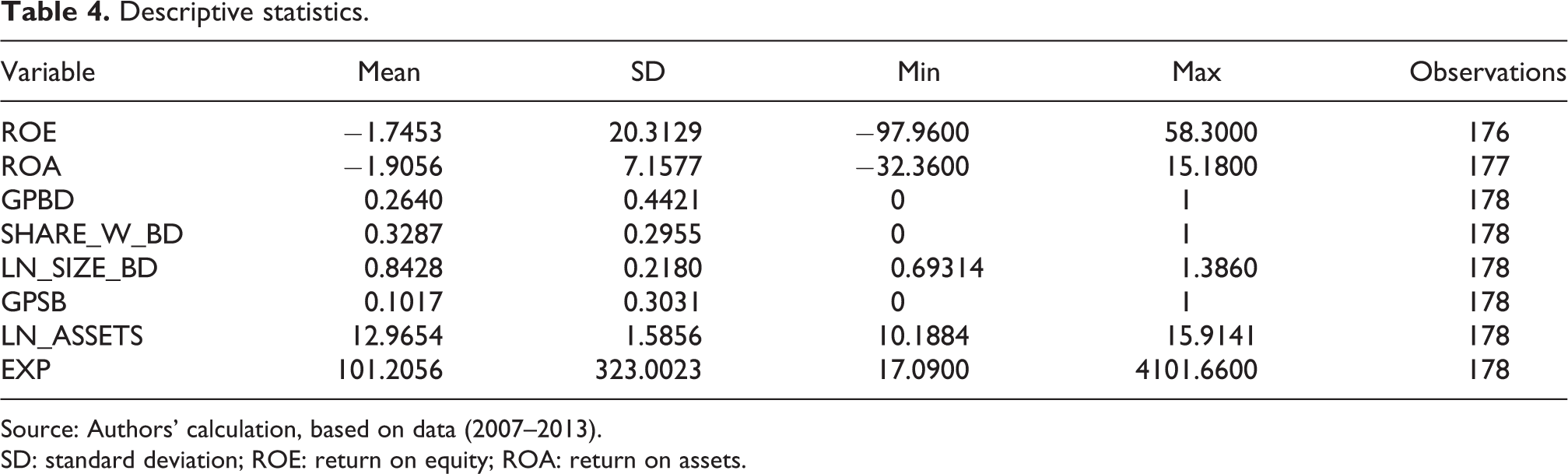

Descriptive statistics regarding dependent and explanatory variables covered by the analysis are provided in Table 4.

Descriptive statistics.

Source: Authors’ calculation, based on data (2007–2013).

SD: standard deviation; ROE: return on equity; ROA: return on assets.

A matrix giving the correlations between all pairs of variables, reported in Table 5, suggests high correlation between some of the variables. Therefore, special caution is given when including the variables in the model.

Pairwise correlation matrix.

Source: Authors’ calculation, based on data (2007–2013).

ROE: return on equity; ROA: return on assets.

Dynamic panel model was specified in the form

with yit being dependent variable whereas

Since the use of OLS estimator leads to biased and inconsistent parameter estimates, the use of generalized method of moments (GMM) estimator, introduced by Arrelano and Bond, 73 is more appropriate. Specifically, two dynamic panel data models with lagged levels of the dependent variable are estimated using Arellano and Bond two-step GMM estimator. In the first model, dependent variable is ROA, whereas in the second model, ROE is used as a dependent variable.

Validity of instruments used is tested by Sargan test, which tests for overidentifying restrictions. The Sargan statistic implies we cannot reject its null hypothesis, and thus can conclude that the moment condition is met and all instruments are appropriate. The autocorrelation tests of the residuals in first differences are m 1 and m 2 tests. The null hypothesis of the m 1 test assumes the nonexistence of the first-order autocorrelation of the residuals in first differences, whereas null hypothesis of the m 2 test assumes the nonexistence of the second-order autocorrelation of the residuals in first differences. Results of the m 2 test indicate that the nonexistence of the second-order autocorrelation of the residuals in first differences cannot be rejected; that is, they confirm the validity of the instruments.

Results and discussion

Each model has three diagnostic tests and in both models the results of diagnostic tests are valid, with p values shown in Table 5. The parameter estimates of the dynamic panel model are provided in Table 6.

The parameter estimates of the dynamic panel models.a

ROE: return on equity; ROA: return on assets.

aStandard errors in parentheses.

* p < 0.1.

** p < 0.05.

*** p < 0.01.

Variable board of directors’ female members (SHARE_W_BD) significantly and negatively affects insurer’s performance measured in ROA, suggesting that the presence of larger number of women on boards constrains performance. This is however in line with previous research that also found negative relation. 22,38,39 Hereby, it is interesting to cite Galinsky et al. 74 how “diversity can also incite detrimental forms of conflict and resentment.” Or, as suggested by Alesina and La Ferrara, 75 diversity has decision-making and economic benefits but diverse groups run the risk of descending into detrimental conflict, which can derail growth. Similar to the findings in panel A model, adding more women in the board of directors (SHARE_W_BD) also has negative impact on insurer’s performance measured by ROE, although this impact is not significant. It is worth mentioning the paper by Smith et al., 33 which also found that the effect on firm performance of a higher ratio of women on top-level management positions and/or members of boards of directors varies from none to positive depending on the measure of performance. The similar pattern can be found in the paper by Dobbin and Jung, 42 which evidenced that while female directors can have a negative effect on Tobin’s q but at the same time have no effect on ROA.

The variable gender of the president of the supervisory board (GPSB) has negative impact on insurer’s performance measured with both ROA and ROE. However, when measuring performance with ROE, this influence is insignificant. The variable gender of the president of the board of directors has no statistically significant impact.

When looking at overall results, it is possible to conclude that the results do not confirm our first hypothesis that gender diversity will positively and statistically significant effect financial performance of companies in the insurance sector in Croatia.

Size of the board of directors (LN_SIZE_BD) and size of the supervisory board (LN_SIZE_SB) also appear to be important corporate governance factors influencing insurance companies’ profitability. Its negative sign in both models is consistent with other authors’ clarification that “coordination, communication, and decision-making problems increasingly hinder board performance when the number of directors increases.” 24 Small boards of directors are more effective and there are more coordination and communication problems connected with large board size. Furthermore, as stated by Wang et al., 53 “increased board size may be less cohesive and thus result in poorer performance.” The above results confirm our second hypothesis that board size will have a negative and statistically significant effect on financial performance of companies in the insurance sector in Croatia.

The control variable size based on assets (LN_ASSETS) is significant as well and, as expected, positively affects insurer’s performance. This is in accordance with findings by, for example, Stancic et al. 17 and Doğan, 76 to name a few. Hardwick et al., 50 analyzing organizations in life insurance industry and connection between board characteristics and profit efficiency, also found that larger firms have higher profit efficiency, suggesting this to be a consequence of their economies of scale and scope. However, they also found that, once “a firm becomes too large, the effect of size inflects possibly because of the increasing complexity of management.” Another control variable, expense ratio (EXP), as expected, has significant and negative impact on insurer’s performance. Lee 77 obtained the similar finding.

Conclusion

Board structure is a topic of interest in the recent corporate governance literature, but still lots of its aspect, such as board size and board diversity, still remain unclear and under-researched, with ambiguous empirical findings. Gender diversity especially is an intriguing question that has become even more important as of the labor market changes in the last couple of decades and increased participation and legal acquirements for inclusion of women on board positions. Insurance sector is especially underrepresented in the empirical research and additional empirical studies are needed to create additional knowledge on the board diversity and its influence on companies in the financial sector, and especially their financial performance. Motivated by the need to additionally explore this question, the article examines the influence of board size and board gender diversity on financial performance of the insurance companies in Croatia. Our analysis covered all insurance companies operating in Croatia in the 2007–2013 period and was conducted using dynamic panel model. Financial performance of the companies was assessed using ROA and ROE measures as dependent variables, while gender of the president of the board of the directors and of the supervisory board, share of women in the board of directors, and board size were used as explanatory variables. Size based on total assets and expense ratio were used as control variables.

As our theoretical overview has shown, it is widely recognized that when it comes to decision-making at top management positions, women are underrepresented worldwide. While employment of women in the insurance industry is high, they are poorly represented in leadership positions in this sector, especially in Croatia. One of the reasons arises from the Croatian political legacy and the environment that was not supportive for advancing women to leadership ranks. While there is still progress to be made toward achieving gender diversity in the boardroom of Croatian insurance companies, a positive shift in corporate culture on this issue is noticeable. This is not negligible given the Croatian historical and political background in which there was no private ownership, and men predominantly held the leading positions. However, the results of our research do not give additional support for incorporating more women in governance boards. On the contrary, it supports the view that gender diversity inhibits performance. To be more specific, our results indicate that adding more women on the board of directors will have a negative impact on insurance company performance measured by ROA and ROE, although this impact is significant only for ROA measure. Moreover, gender of the president of the supervisory board also has negative influence on performance measured used and has significant influence only when using ROA as a measure of performance. Interestingly, in both of our models, gender of the president of the board of directors has positive, however not significant, influence on performance measures. Consequently, we cannot confirm our first hypothesis. The results of the analysis do not speak in favor of greater gender diversity at the top positions in insurance industry since it is established that women acting as presidents of supervisory boards deteriorate insurer’s performance measured by ROA. This is also confirmed with the finding that making boards more gender diverse can decrease performance. However, as mentioned in the results section, this is in line with several previous researches that also found negative effects. Since this article does not provide evidence that women acting as presidents of the boards of directors nor supervisory boards improve insurer’s performance, the proposals for women’s integration in the top positions, as stated by Adams and Ferreira, 29 should be motivated by reasons other than improvements in governance and firm performance. Reasons can include, for instance, improvement in company image, greater understanding of the market, and promoting better boardroom behavior.

Still, we believe there are some possible explanations and implications for this negative effect. First, the negative link might be the consequence of the fact that women are preferentially selected for leadership positions in times of crisis (such as the period from 2007 that was the beginning of the world financial crises). As stated by Vongas and Al Hajj, 78 there is “the perception of women as being more empathic than men and, consequently, as capable of quelling certain crises.” Still, in these times of crisis, a much greater influence can be attributed to the economic and political situation that is beyond the influence of board members, and that is eventually leading to negative companies’ performance. Second, as stated, Croatia has traditionally male-dominated board of directors. For women, it may be difficult to assimilate fully to these boards, especially since women are usually given board committee assignments that have less instrumental impact on performance. 38 This implies that the mere presence of women at the board does not automatically improve performance. 29 Women should also be given appropriate assignments and tasks with greater influence on key board processes and eventually performance. And not just appropriate task, but also it may be that the number of woman on board itself and their qualifications can be an important factor. Some authors 8,79 found that a critical mass of three women on the board is necessary for women to have an impact. Going further, Smith et al. 33 found that women will have positive effect depending on their qualifications. In addition, board composition needs to adjust to different organizational characteristics and needs, for example, ownership structure, organizational life cycle, strategic orientation, and similar. 26

All of these previously mentioned reasons provide possible explanations for negative effects and provide implications for insurance organizations in Croatia. It is important to make a quality analysis of organizational needs and adjust its board composition suitably. Moreover, it implies that it is important to ensure women are integrated into boards and given assignments that can help them achieve their full potential and consequently can have influence on key board processes. As suggested by Dwyer et al., 80 adequately designed and encouraging working setting needs to be created for benefits of gender diversity to be fully achieved.

However, to fully understand gender, additional research needs to be done. Future research should analyze more deeply firm-level variables such as work practices and organizational culture 10 and additional ones that mediate among gender diversity of board of directors and firm performance. It would also be interesting to analyze dynamics among diverse board members and performance. Our article took only financial measure so future research should also include nonfinancial measures of performance to get a more detailed view on gender diversity influence on performance.

Results regarding board size confirm the preposition about the negative relationship between the size of the board and both measures of performance. This confirms our second hypothesis and supports the theoretical notion that smaller boards can have greater impact on board effectiveness and consequently firm performance also in the insurance market.

At the end, our research results need to be seen in light of certain limitations. First, we had a rather small period of analysis (2007–2013). Since the findings of the research may display the features of this period, larger period of analysis is needed which can be the possible venue of future research. As mentioned, this was the period when economic crises had significant effect on organizations financial performance. Having in mind the fact that crisis may have greater influence on performance than the number of women on boards, this aspect should be captured in future research. Furthermore, extending the sample by covering more countries in the analysis, focusing primarily on those with similar background and level of development with Croatian insurance market, might bring a valuable input on the issue. Since there might be some other factors influencing insurance companies’ performance that have not been employed in the model, future research might also address additional characteristics by including, for example, leverage, ownership, and gross written premium growth rates. Finally, it might be convenient to see the impact of gender diversity on performance, not only in top positions, that is, boards but in the insurance company as a whole. Also, there is a potential problem of time lag that can appear, as it, in some cases, takes more time for positive effects of adding more women to boards to reflect on financial performance.

Still, in spite of certain limitations, we believe this article upgrades the existing literature by providing new data on the impact of board structure on performance in the area of insurance industry. This study extends the existing literature in this field by introducing two corporate governance mechanisms in the analysis, that is, both board of directors and supervisory board. Our results can be helpful for academics but also practitioners, especially in the field of insurance. By providing results from not just industry but also national specific context, we believe our results can be useful in better understanding of gender diversity as well as the board size effects on performance in the insurance sector.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.