Abstract

We use non-performing loan ratio and insolvency risk to measure bank risk and construct panel data regression models to examine the effects of the interbank market rate, central-bank rate and bank-level lending rate on bank risk in China. Empirical results show that interbank market rate and the central-bank interest rate are positively correlated with bank risk, while the bank-level lending rate is negatively correlated with bank risk. We also analyse and explain the difference between the effects of the US interest rates and China’s interest rates on its own bank risk. Finally, we put forward some policy implications.

Introduction

Financial imbalances and economic fluctuations often result from the fact that soft monetary policy (a low interest rate) frequently leads to excessive credit expansion. Many central banks have adopted a low interest-rate regime over an extended period to ward off potential recessions after the burst of the dot-com bubble. Continuously low interest rates can lead to a boom in asset prices and securitized credit and can induce banks to take on increasing risk. 1 Although it is difficult to state that low interest rates have been the root cause of the 2008 international financial crisis, it could have contributed to its build-up. Hence, the impact of interest rates on bank risk has become a focal point of the debate in theory and practice since the 2008 international financial crisis. 2,3

The effects of interest rate on bank risk belong to the contents of the relationship between monetary policy and financial stability. But they are different from each other. Oosterloo and deHaan discussed in detail the relationship between monetary policy and financial stability. 4 However, we concentrate on the effects of interest rates on the bank risk. About the effects, there is very limited theoretical support and empirical evidence so far. 1

In theory, some literatures explain several channels by which interest rate affects bank risk. 5,6 (1) ‘Asset valuation’ channel: A reduction in the interest rate boosts asset and collateral values, which in turn can modify banks’ estimates of probabilities of default, loss given default and volatilities and stimulate banks to take risk. (2) ‘Search for yield’ channel: Low interest rates cause banks’ target revenue to decline, which stimulates banks to invest in high-margin and high-risk areas or financial instruments. (3) ‘“Asset substitution’ channel: The decline in interest rates will lead to a low proportion of safe assets in the bank assets portfolio. Risk-neutral bank will increase the demand for risky assets until a new equilibrium arises in the ratio of safe assets and risky assets. (4) ‘Constant leverage’ channel: Commercial banks target constant leverage ratio. Low interest rates will boost assets prices. Bank equity will increase and banks will respond to the fall in leverage by increasing their demand for risky assets. This reaction reinforces the initial boost to asset values and so on. This will bring about a more fragile banking system that is more exposed to negative shocks to asset values and thus riskier.(5)’Central bank communication’ channel: If the central bank has transparent policy and credible commitment, low interest rate is an implicit commitment that will induce collective moral hazard. Low interest rates mean loose monetary and regulatory environment, which stimulates banks to take risk. (6) ‘Asset-liability mismatch’ channel: When interest rates are low, banks can only absorb short-term deposits. The mismatch between short-term deposits and long-term project finance tends to high leverage. The more leveraged banks are, the higher the risk of failure is. (7) ‘Habit formation channel’: If interest rate is low, investors tend to consume more and expected credit spread is high. Thus, investors loan more from the bank or invest in high-risk financial instruments, which results in higher bank risk. In addition, some studies suggest that interest rate has an uncertain effect on bank risk. The impact of interest rate on bank risk depends on many factors that affect the mutually countervailing forces. The effect of interest-rate changes on bank risk may change over time, the banking system or different characteristics of the bank. 1

Some conflicting findings can be seen from the present empirical research. Some researchers draw the conclusion that low interest rate leads to an increase in bank risk, and high interest rate can prevent the accumulation of bank risk, 7 –12 while other studies indicate that low interest rate may reduce bank risk and high interest rate may increase bank risk. 13 –15 Interestingly, Thakor, López et al. ) and Jiménez et al. document an uncertain effect of interest rate on bank risk. 16 –18 The interest rate has a smaller impact on the risky assets of the banks with more capital, but a bigger effect on the banks with more off-balance business. Different banks can make the heterogeneous reaction on interest-rate changes, and banks with high capital adequacy rate and income diversification perform more radical in taking risk. However, Özşuca and Akbostancı found that large, liquid and well-capitalized banks are less prone to risk-taking. 19

In view of the fact that sub-prime mortgage crisis in the United States has exerted an impact on China, 20 it is significant to study the effects of interest rates on bank risk in China and compare the difference of the effects between United States and China. Our study constructs the panel data regression models to examine the effects of the interest rates on bank risk in China from 2001 to 2012. Our study differs from other studies in several ways. First, we test empirically the effects of the interbank market rate (market-oriented interest rate), the central-bank rate (officially set interest rate) and the bank-level lending rate rather than one interest rate on bank risk in China. Second, we compare and analyse the difference between the effects of US interest rates and China’s interest rates on its own bank risk. Our study thus provides meaningful policy guidance in implementation in China. The results also provide useful information to policymakers in emerging markets in designing their monetary policy.

The rest of the paper is organized as follows: The section ‘Econometric model and data’ proposes the empirical model and data analysis approach. The section ‘Econometric analysis and results’ elaborates the identification framework embedded in the core model and the corresponding results. The section ‘Concluding remarks and policy implications’ draws the conclusions and puts forward the policy implications.

Econometric model and data

We construct a panel regression model to study the effects of interest rates on bank risk as follows:

where the risk variable, RISK, of bank i at time t is a function of interest-rate variables (RATE), a set of bank-level control variables (ASSET, Capital Adequacy Ratio (CAR) and Return on Assets (ROA)) and macroeconomic control variables (Gross Domestic Product (GDP)). α represents the constant term. βj (j = 1,2 …, 5)denotes the parameters. ∊it means the random disturbance. ln is natural logarithm.

Before carrying out the empirical analysis, we should discuss the variables used and the data set. We use annual (from 2001 to 2012) data of all 16 Chinese listed banks whose assets account for over 65% of the assets of Chinese banking industry in 2012. The sample contains the five large commercial banks, eight joint-stock commercial banks and three city commercial banks. Among those, the large commercial banks include the Industrial and Commercial Bank of China , the Agricultural Bank of China , the Bank of China , the China Construction Bank and Bank of Communications ; the joint-stock commercial banks include China International Trust and Investment Corporation (CITIC) Bank, Everbright Bank of China, Huaxia Bank, Pingan Bank, China Merchants Bank, Shanghai Pudong Development Bank, Industrial Bank and China Minsheng Banking Co.; the city commercial banks include Beijing Bank, Nanjing Bank and Ningbo Bank.

Table 1 provides descriptive statistics for all the variables used in the empirical analysis. Table 2 reports correlation coefficients between these variables. According to Damodar, 21 if zero-order correlation coefficient of each two regressors is over 0.8, the multicollinearity problem will be a severe problem. Correlations in our study are in acceptable levels as shown in Table 2. In what folows, we analyse the choice of our dependent, explanatory and control variables.

Descriptive statistics.

NPL: non-performing loan; INS: insolvency risk; S3: 3-month national interbank market rate; C1: the RMB 1-year benchmark deposit rate; DL: the bank-level lending rate; CAR: Capital Adequacy Ratio; ROA: Return on Assets; GDP: Gross Domestic Product.

Correlation matrix.

GDP: gross domestic product; ROA: return on assets.

Bank risk

We proxy the dependent variable – the bank risk using the ratio of non-performing loans (NPLs) to total loans and insolvency risk (INS). Data for both the variables are obtained from Almanac of China’s Finance and Banking and the website of every commercial bank.

The ratio of NPLs to total loans is a very helpful ratio used widely for analysing credit risk and equals the sum of substandard, doubtful and loss loans divided by total loans. As an indicator of credit risk, a bank’s NPLs respond to the quality of its assets, hence a good representative of the overall status of the financial security. Once the loan quality collapses, the mark-to-market value of the bank asset drops immediately following the increasing bad loans. Therefore, a high ratio of NPL exposes the bank to more credit risk, whose mean value is 4.905 in this scenario.

INS describes the likelihood that a bank will become insolvent because of its inability to service its debt. INS = SDROA/(ROA + EA), where ROA means return on assets, EA represents the ratio of the capital to asset and SDROA is the standard deviation of ROA. The lower the INS is, the more stable banks are. Higher INS reveals that banks have greater risk and are in more dangerous situation. In our sample, the mean value of INS equals 0.044.

Interest rates

With special emphasis on the interaction between interest rates and bank risk, various types of interest rates are taken into consideration to reach a comprehensive and exhaustive result: interbank market rate (market-oriented interest rate), the central-bank rate (officially set interest rate) and a bank-level lending rate. Data for the interest-rate variables is obtained from Almanac of China’s Finance and Banking and the website of People’s Bank of China (summary statistics are provided in Table 1). In particular, interbank market rate is the annual average of the 3-month national interbank market rate and the central-bank rate is the annual average of the Renminbi (RMB) 1-year benchmark deposit rate. The bank-level lending rate gives way to involving a lot more observations with respect to interest-rate variables. We adopt the ratio of interest income to total loans as the proxy of the bank-level rate. The average of this ratio is 4.387 in the worked sample, meaning that the loan is priced averagely at 4.378 by the bank when charging its customers.

Control variables

We have chosen several control variables for our regression analysis. Please see below for these variables definition and annotation and refer to Table 1 for the summary statistics.

To evaluate the effect of the macroeconomic environment status at the country level on bank risk, we utilize real GDP growth rate to be the key control variable. The data of real GDP growth rate come from DRCnet (The Information Website of Development Research Center of the State Council of China) Statistical Data Database System.

To realize a more-angles control on bank characteristics that might impact bank risk, a series indicators are screened as below (all required data are collected from Almanac of China’s Finance and Banking and the website of every commercial bank). ASSET represents size of the bank, which is measured by total asset of the bank. In the regression, we use the natural logarithm of total asset. Banks with the different sizes may have distinct motivation to engage in risky activities. CAR, as a measure of bank capitalization, is the ratio of capital to risk-weighted assets. Banks are expected to trade-off higher levels of equity capital for risky assets. ROA, the ratio of profits before tax to total assets, is used for measuring bank profitability whose impact on bank risk is ambiguous.

Econometric analysis and results

We construct three models in terms of the three interest rates to examine the relationship between changes in interest rates and bank risk. First, we select the NPL ratio as the dependent variable to establish three panel data regression model as follows:

where Y1, S3, C1 and DL denotes, respectively, NPL ratio, 3-month national interbank market rate, the RMB 1-year benchmark deposit rate and the bank-level lending rate (represented by the ratio of interest income to total loans). The meanings of other variables are the same with those of equation (1).

Then, we substitute the NPL ratio for INS to construct the following three-panel data regression models to test the robustness of the results:

where Y2 denotes INS. The meanings of other variables are the same with those of equations (2) to (4).

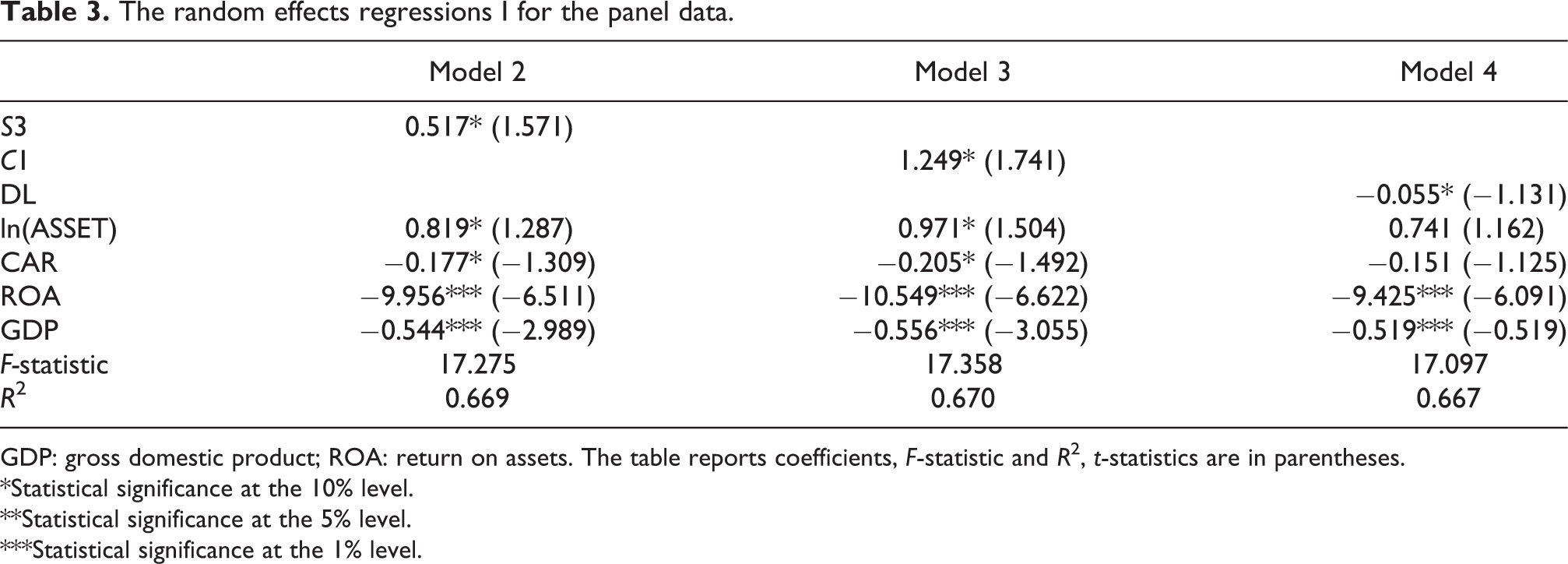

Based on the results of the Hausman test, we use the random effect model for the panel data to estimate equations (2) to (7). The results are reported in Tables 3 and 4. The two tables report coefficients and t-statistics (in parentheses). The symbols *, ** and *** denote, respectively, the statistical significance at the 10%, 5% and 1% level.

The random effects regressions I for the panel data.

GDP: gross domestic product; ROA: return on assets. The table reports coefficients, F-statistic and R2, t-statistics are in parentheses.

*Statistical significance at the 10% level.

**Statistical significance at the 5% level.

***Statistical significance at the 1% level.

The random effects regressions II for the panel data.

GDP: gross domestic product; ROA: return on assets. The table reports coefficients, F-statistic and R2, t-statistics are in parentheses.

*Statistical significance at the 10% level.

**Statistical significance at the 5% level.

***Statistical significance at the 1% level.

Effects of interest rates on bank risk

Interbank market rate

From the regression results of models 2 and 5, the 3-month national interbank market rate has a significant (at 10% level) and positive effect (0.517, 0.031) on bank risk. The possible reasons are as follows. When the 3-month national interbank market rate is low, the firms and commercial banks have a low cost of the liabilities (deposits or borrowings) to the residents, the interbank or central bank, which demonstrates that banks face likely low liquidity risk. On the contrary, when the 3-month national interbank market rate is high, commercial banks have a high-cost of the liabilities (deposits or borrowings) to the residents, the firms, the interbank or central bank, indicating that liquidity risk faced by banks is likely to be high.

Central-bank rate

From the regression results of models 3 and 6, the central-bank rate (the RMB 1-year benchmark deposit rate) has a significant (at 10% level) and positive effect (1.249, 0.072) on bank risk. The possible reasons are listed below. As a kind of monetary policy instrument, the low RMB 1-year benchmark deposit rate implies the economy is down. As the economy goes down, banks would not like to take risk in engaging in the more risky asset business, which is also unnecessary for banks with the reason that low interest rate basically means high interest-rate margin that implies high earnings on condition that loan-to-deposit spread is the main source of profits of the banks in China. Margin equals the bank-level lending rate (the ratio of interest income to total loans) less RMB 1-year benchmark deposit rate. Margin and RMB 1-year benchmark deposit rate have the reverse trend and their correlation is as high as −0.742. In view of the fact that deposit rate is not fully market-oriented, RMB 1-year benchmark deposit rate can be taken as the commercial banks’ own deposit rate. Therefore, banks face a lower risk of default. On the contrary, the high RMB 1-year benchmark deposit means the economy is up, banks would like to take risk in engaging in the more risky asset business to make large earnings, which is also necessary for banks with the reason that high interest rate basically means low interest-rate margin that implies declining earnings on condition that loan-to-deposit spread is the main source of profits of the banks in China.

Bank-level lending rate

In terms of the regression results of models 4 and 7, the bank-level lending rate (the ratio of interest income to total loans) has a significant (at 10% level) and negative effect (−0.055, −0.003) on bank risk, which is the same with the international mainstream viewpoints. Lower bank-level lending rate means lower interest on loans, which causes bank earnings decline. Hence, in order to complete its target revenue, the bank will be inclined to invest in high-risk areas or financial instruments, which increases the bank risk. Moreover, the lower ratio of interest income to total loans shows that some loans fail to be recovered and become NPLs, which causes a rising risk.

The difference between the effects of US interest rates and China’s interest rates on its own bank risk

As what has been mentioned above, both the 3-month national interbank market rate (market-oriented interest rate in China) and the RMB 1-year benchmark deposit rate (interest rate set officially in China) have a positive effect on bank risk, which is very distinct from the empirical findings of US that low interest rate increases the bank risk. The reason lies in the difference of the degree of interest-rate marketization, degree of development of financial market, attitude of the banking sector towards risk and financial consciousness of the residents between China and United States. Accordingly, there is also a great difference between United States and China in the effects of interest rates on bank risk by ‘asset valuation’ channel, ‘search for yield’ channel, ‘asset substitution’ channel, ‘constant leverage’ channel, ‘central bank communication’ channel, ‘asset–liability mismatch’ channel and ‘habit formation channel’ mentioned in the section ‘Introduction’. (1) In China, interest rates are still not fully market-oriented and have not fully played a role in China’s economy. China’s stock market is not perfect and there are more speculative activities in the stock market. Therefore, interest rates have an insignificant impact on asset prices in China. 22 Unlike the US where interest rate is fully market oriented, a decline in interest rates causes a significant rise in asset price. Therefore, asset valuation channel and constant leverage channel may be non-existent in China. (2) Most of China’s banks are risk averse. A case in point is the fact that many managers of banks are afraid of losing their positions if they take risk to induce the loss of bank under the circumstances of strict bank supervision and rigorous performance evaluation. Hence, even if lower interest rate leads to a decline in real revenue of safe assets, most of China’s banks do not increase the demand for risky assets and thus face low risk. Therefore, ‘asset substitution’ channel differs between United States and China. (3) Low interest rates mean really loose monetary environment, which may induce banks to take risk. However, China carries out a strict banking supervision. In addition, the level of risk management is not high in banking industry and the sound operation is the priority of the banks in China. So, most banks dare not take risk and their risky behaviour is less. Thus, China and United States differ in the role of ‘central bank communication’ channel. (4) In China, even if interest rates are low, residents also deposits with the reason that they dare not consume much under the imperfect social security system and dare not invest much in the undeveloped stock market. The residents are forced to retain the deposits, which makes banks’ supply of funds abundant. For example, China’s residents’ saving deposit in banks has been increasing since 1978 to 5.52 billion RMB at present. So ‘asset-liability mismatch’ risk of banks is low, which means low liquidity risk. Chinese residents have weak consciousness of taking risk and face a narrow choice of financial assets under the circumstances of undeveloped financial market. Therefore, there is a lower probability of the investment in high-risk financial products in terms of Chinese residents. Asset–liability mismatch channel and ‘habit formation channel’ are different between United States and China.

Effects of the control variables on bank risk

From the results of regression, the effects of real GDP growth rate on bank risk are all significant and negative. This indicates that a fast pace of economic development will reduce the bank risk, probably due to the fact that the banks’ business operation is good and the revenue is stable under an up economic environment and the banks do not need to take risk to achieve a higher revenue.

The banks’ total assets have a positive and significant effect on bank risk with the probable reason that the banks with a larger size have a stronger motivation to engage in risky activities, leading to the greater risk.

Capital adequacy ratio is negatively correlated with bank risk, that is, the higher the bank’s capital adequacy ratio is, the lower the risk is. High capital adequacy ratio can curb excessive expansion of risky assets, protect the interests of depositors and other creditors and ensure banks to operate normally.

ROA has a negative and significant effect on bank risk, which shows that the enhancing profitability can effectively reduce the risk of banks.

Concluding remarks and policy implications

We select all 16 listed banks of China as a sample, use NPL ratio and INS to measure bank risk and establish panel data regression model to study the effects of interbank market rate (3-month national interbank market rate), the central-bank interest rate (RMB 1-year benchmark deposit rate) and bank-level lending rate (the ratio of interest income to total loans) on commercial bank risk. The empirical findings are as follows: 3-month national interbank market rate and RMB 1-year benchmark deposit rate are positively correlated with the bank’s risk. The ratio of interest income to total loans has a negative on the bank’s risk.

In view of the effects of the interest rates on bank risk, the following measures should be taken to ensure the financial stability and the effectiveness of monetary policy. First, applying interest rate and other monetary policy instruments simultaneously and synthetically is helpful for achieving price stability and financial stability synchronously. The ‘trade-off’ viewpoint holds true in China that monetary policy aiming at price stability is not necessarily helpful for financial stability and a trade-off relationship exists between price stability and financial stability. 4 From China’s experience, on the one hand, price stability can be achieved by enhancing the interest rate at the time of high inflation. On the other hand, the increase in the interest rate leads to the increase in bank risk according our empirical results. Therefore, the reserve requirement ratio (an administrative instrument), open market operation and other monetary policy instruments must be applied simultaneously and synthetically to ensure the financial stability and the effectiveness of monetary policy. Second, due to the fact that as a decision-making process, risk management involves considerations of engineering factors, 23 banks ought to pay much attention to the impact of the changes in interest rates on bank risk, establish a comprehensive early warning system of risk and construct the models by which commercial banks can assess risks caused by the changes in interest rates. Third, the monetary authorities should improve its reaction function and take the bank sector into macroeconomic decision-making model and strengthen the monitoring and analysis of bank risk and thus guard against financial imbalances. In addition, monetary and regulatory authorities must take into account the different effects of the different interest rates on bank risk and strengthen the coordination and cooperation so that some effective steps can be taken in advance to prevent the possible risk. Fourth, in view of the fact that the effects of interest rates on bank risk may change with the improvement of the degree of the interest-rate marketization, the perfection of financial market, changes of the banking sector towards risk and enhancement of financial consciousness of the residents in China, monetary authority or regulatory authority of China should concentrate on the changes in the effects of interest rates on bank risk, caused by financial reforms and institutional changes, and take steps in advance against the possible risk.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This article is financially supported by National Natural Science Foundation of China (grant numbers 71103048 and 71273224), Zhejiang Provincial Natural Science Foundation of China under grant no. LY16G030018, Project of Humanities and Social Sciences of Ministry of Education in China under grant no.14YJC790167 and Project of Educational Commission of Zhejiang Province under grant no. Y201432409.