Abstract

In investment decision-making, money's moral attributes vary based on principal source and profit method. This study investigated the effects of immoral money on intertemporal investment choices. Studies 1 and 2 show that perceived immorality of principal sources or profit methods increased preference for smaller-sooner (SS) options. A guilt-mediated effect was demonstrated, suggesting guilt aversion as an SS preference mechanism. Study 3 explored the joint effects of the morality of principal sources and profit methods on guilt and investment choices. When both aspects were immoral, individuals engaging in immoral profit methods preferred SS more, and those investing moral principal via immoral methods felt guiltiest. These findings implicated that maintaining the morality of the principal source and profit methods can promote long-term investment. The present study also highlights the vicious cycle of shortsighted behavior (e.g., eco-unfriendly behavior), where money with moral flaws would aggravate future shortsighted decisions.

Introduction

The morality of money refers to the ethical considerations surrounding the use and distribution of money (Walsh & Lynch, 2008). It is usually shaped by cultural, social, and religious factors, and can have a significant impact on individual's financial behavior. The previous studies on the morality of money sought to understand the complex relationships between money, morality, and social justice, and to develop frameworks for responsible and equitable financial practices (Haynes, 2012; Ouma, 2018; Singh, 2019; Walsh & Lynch, 2008; Watanabe, 2017). In real life, money can take on an immoral character in various ways, including through illegal income (such as money laundering and theft) and unethical earnings from industries lacking social responsibility (such as environmental destruction or resource waste). In this study, we concentrate on immoral money generated in eco-unfriendly investment.

Currently, sustainability issues are receiving greater consideration. According to Bloomberg (2022), investment considering the impact of environmental, social, and governance (ESG) factors surpassed $35 trillion in 2020, up from $30.6 trillion in 2018 and $22.8 trillion in 2016, to become a third of the total global assets in management. However, unsustainable investments such as those in environmentally hazardous industries are still conducted on a relatively large scale. For example, according to the European Environment Agency (2023), industrial air pollution in Europe costs society between €277 and €433 billion in 2017, which is equivalent to approximately 2–3% of the European gross domestic product (GDP).

In this article, we aimed to explore the impact of money immorality (caused by environment pollution) on individual's intertemporal investment decision-making and the underlying psychological mechanism.

Immoral principal sources and profit methods in investment

Principal and profit are two primary financial categories that influence investment decision-making. As a currency, money itself has no connection with morality. However, when principal is linked to its sources and profit is linked to the means used to earn it, money can become associated with morality. The sources of principal represent different morality levels, such as earned honestly, gained accidentally, or obtained improperly. Profit methods also vary in how they connect to morality, relative to environmental friendliness, credibility, and social responsibility.

In fact, enormous amounts of funding from immoral sources exist in every country/economic system. The most widely quoted figure showing the extent of money laundered is the International Monetary Fund's (IMF) “consensus range” of 2% to 5% of global Gross Domestic Product (GDP), made public by the IMF (Camdessus, 1998). In addition to the use of immoral money as investment principal, investment projects with moral defects exist as a means for earning profits in investment markets in all countries. According to the Global Sustainable Investment Alliance, at the start of 2016, sustainable investments constituted only 26% of assets that are professionally managed in Asia, Australia and New Zealand, Canada, Europe, and the United States (Bernow et al., 2017).

Environmental pollution is one of the most common ways through which ordinary individuals encounter the immoral attributes associated with money. Many businesses, driven by the pursuit of profit, often neglect their environmental responsibilities. Such environmentally unfriendly behaviors by businesses can evoke a sense of immorality among both employees and consumers (Ab Wahab, 2021; Lin et al., 2016). Consequently, when people receive wages from environmentally irresponsible companies or invest in such companies, this sense of immorality transfers to the money through “moral contagion” (Nemeroff & Rozin, 1994), thereby influencing their investment decision-making behavior.

Once the money involved in investment is attached to immorality in terms of principal sources or profit methods, the consideration of money morality derived from it may influence subsequent investment decision-making. A previous study found that people are less likely to accept money with a negative moral history and feel concerned about possessing stolen money (Tasimi & Gelman, 2017). Additionally, people are less motivated to earn dirty money than clean money, and they believe that dirty money has less purchasing power than clean money (Stellar & Willer, 2014). A dilemma exists in regard to dirty money—whether to accept dirty money and, if yes, how to use it (Siegel et al., 2022; Tasimi & Gross, 2020). In this study, we mainly focus on how the perceived immorality of money (in particular, related to environmentally polluting industries) affects people's intertemporal investment decisions.

Intertemporal decision-making in investment

Investment activities usually involve both intertemporal and risky decision-making. Merton, one of the 1997 Nobel laureates in economics, argues that the core of financial theory is to investigate how economic agents allocate and utilize their resources under uncertain environments, including across both time and space. Accordingly, time and uncertainty are considered to be key factors that influence financial behaviors. In many cases, investors must make choices between smaller-sooner (SS) and larger-later (LL) gains, which is also termed intertemporal decision-making (Frederick et al., 2002).

Past research on intertemporal choice has mainly stressed the influence of three kinds of factors, including option attributes (e.g., magnitude of payoff, length of delay), individual traits (e.g., discounting tendency, time perspective, construal level), and situational factors (e.g., interest rate, inflation, financial crisis) (Frederick et al., 2002). Among those factors, the length of delay and cost and benefit have been considered crucial components of intertemporal choice and are of particular interest to researchers (Liang & Liu, 2011).

Nevertheless, the effects of money morality on intertemporal decision-making behavior have received little, if any, attention within the economic field. Former decision-making models, such as the expected utility (EU), prospect theory (PT), and discounted utility (DU) models, have deemed money morally irrelevant or neutral, and the influence of moral connectedness or ethical factors of money on decisions is rarely considered. Meanwhile, normative economic theory suggests that money holds “source independence” or “fungibility,” which means that the value of equal money from different sources should be identical and interchangeable (Thaler, 1990). In other words, the source of money should make no difference to the value of said money (Staddon & Horner, 1989; Von Neumann & Morgenstern, 1947). Regarding the moral consideration of the means by which a project or company makes money, rational decision theorists will not consider this, instead holding the view that investment decisions are made rationally and selfishly and that financial considerations rather than moral considerations should dominate investment decisions. However, previous research on ethical investment indicates that investment decisions are influenced not only by financial benefits but also by additional factors, such as attitudes and moral considerations (Cohen et al., 2022; Hofmann et al., 2008; Michelson et al., 2004). To better understand the intertemporal decision-making behaviors of individuals in the real world, the concept that money has elements of morality should also be considered.

Therefore, the purpose of the present study is to shed light on the influence of immoral principal sources and profit methods on intertemporal choices in investment activities. Specifically, supposing that someone has a sum of principal to invest, the question is whether its immorality will affect his or her preference for the SS or LL outcome. Similarly, if someone decides to invest in a project or company, the question is whether its immorality will make him or her myopic. This study intends to reveal the effects of money immorality on intertemporal decision-making and to reconsider the fundamental economic assumption of source independence and fungibility.

Effects of money morality on intertemporal decision-making: The perspective of moral emotion

The concept of “moral contagion” was proposed in 1994 (Nemeroff & Rozin, 1994) and states that objects can transfer their moral or immoral essence to another object merely through contact. Past research has found that the effects of negative moral contagion are significantly stronger than those of positive moral contagion (Eisenberg, 2000; Malti & Latzko, 2010). For example, when people acquire earnings from environmentally hazardous enterprises, the immorality of the enterprises will contaminate this income in the mind of the receiver. Furthermore, the immorality connected with this income will contaminate the people who earn it. Thus, negative moral emotions are likely to be produced.

Emotional responses to receiving money can become associated with the money itself in the form of an “affective tag” (Levav & McGraw, 2009). When people spend money that has a negative affective tag, they may first attempt to avoid purchasing products, the consumption of which may intensify their negative feelings (Luce, 1998). Second, recipients of this type of money are more likely to choose virtuous or utilitarian purchases to launder or “cleanse” the money of its negative affective tag. Similarly, when confronted with morally tainted money, people seek to cleanse the tainted money rather than strive for more general moral redemption (Park & Meyvis, 2013). People tend to use immoral money for morally acceptable purposes to reduce the perceived immorality of the money. We therefore predict that in intertemporal decision-making, the SS option will be preferred when investing immoral money to mitigate the negative affective tag or to avoid reinforcing negative feelings that would come from investing the immoral money long term.

When people invest in enterprises or projects that earn profits through immoral means (e.g., environmentally hazardous enterprises), due to moral contagion, those who will receive the profit may become contaminated as well. Thus, immoral feelings and negative moral emotions can be easily induced in the face of contaminated money. Hence, decision-makers are likely to prefer smaller outcomes when investing in immoral projects, not only because profits obtained through immoral methods will lead to negative emotions but also because the investment itself and the continued involvement in immoral projects will induce negative emotions. To rid themselves of this anticipated negative emotional experience, investors prefer earlier rewards when investing in immoral projects.

Both immoral principal sources and investment projects can trigger negative moral emotions. Guilt is often regarded as a typical moral emotion resulting from moral transgressions (real or imagined), in which people believe that their action (or inaction) contributes to negative outcomes (Tilghman-Osborne et al., 2010). Decisions can be viewed as a conduit through which emotions guide everyday attempts at avoiding negative feelings (e.g., guilt and regret) and increasing positive feelings (e.g., pride and happiness), even when decision-makers do so without being aware of their emotions (Lerner et al., 2015). Thus, to avoid or alleviate guilt generated from immoral principal sources and investment projects, decision-makers will be more likely to prefer the SS option in intertemporal investment choices. In addition, prior research suggests that negative emotions lead to myopic decisions in intertemporal choices (Guan et al., 2015). Similarly, human beings often display much steeper discounting rates (which means preferring SS) in intertemporal choices after a stable negative emotion is induced by successive presentations of negative pictures (Augustine & Larsen, 2011) or a natural disaster (Li et al., 2011). Thus, guilt, a negative emotion produced when violating ethics, will play a mediating role and lead people to prefer the SS option in intertemporal investment.

In real-life investment decisions, the principal source and the profit methods often simultaneously present moral concerns. To better simulate real-life investment decision-making, we studied how both factors simultaneously influence people’s intertemporal decision preferences. As previously hypothesized, people would choose SS options to alleviate the guilt caused by immoral principal sources or profit methods. However, when profit method is moral, the impact of the morality of principal source on intertemporal investment decision preferences will diminish, as investing immoral principal into moral industries may evoke a sense of atonement. When profit method is immoral, the impact of the morality of principal source on intertemporal investment decision preferences will increase, as investing moral principal into immoral industries may intensify feelings of guilt.

Pilot Study 1: Intertemporal choice titration

To determine the effects of money morality on intertemporal decision-making about investments, the allure of SS and LL rewards needed to be balanced. This study ascertains the indifference point through a choice titration procedure, with the selected proportions of SS and LL options being similar under the control condition to avoid a ceiling effect.

Methods

A total of 85 non-psychology major participants were recruited from several general education courses (42 men, Mage = 22.83, SD = 2.23). The experiment was conducted using a paper-and-pencil test offline. Participants would receive a small gift as a reward upon completion of the experiment. The experimental protocol of all studies was approved by the Research Ethics Committee of Zhejiang University, and informed consent was obtained from all participants before they engaged in this study.

Following the choice titration method, a questionnaire was used to obtain the approximate subjective value of an outcome that was temporally distant in the future. Participants were given 11 pairs of choices between receiving ¥30,000 in two years (LL option) and receiving some money one year later (SS option); the value of the SS reward increased from ¥9,000 to ¥29,000 in ¥2,000 increments. Adjusting amount orders (ascending or descending) of the SS rewards were counterbalanced. Participants in the pilot study were given the following scenarios:

Pair 1. A: received ¥9,000 in 1 year B: received ¥30,000 in 2 years Pair 2. A: received ¥11,000 in 1 year B: received ¥30,000 in 2 years Pair 11. A: received ¥29,000 in 1 year B: received ¥30,000 in 2 years

The present subjective value was the value midway between the two varied neighboring rewards from which participants switched, consistently preferring the varying amount to consistently preferring the fixed amount (¥30,000). If participants consistently preferred option A or B in all 11 pairs, they would then be asked to estimate an amount that was psychologically equivalent to ¥30,000 in two years.

Results

Data from 8 of the 85 participants were dropped, as their preferences contained logic errors in the choice procedure (e.g., they preferred A to B when A weakly dominated B but preferred B to A afterwards when A strongly dominated B). The average SS outcome that was indifferent to the LL outcome was ¥17,600, rounded up to ¥18,000. Namely, participants’ subjective value of “receiving ¥30,000 in two years” was “receiving ¥18,000 in one year.” Thus, this amount could be used for intertemporal choices in the formal experiments.

Pilot Study 2: Morality assessment of principal sources and profit methods

Pilot Study 2 was designed to check the effectiveness of the manipulation for morality of principal sources and profit methods.

Methods

A total of 42 non-psychology major participants were recruited from several general education courses (11 men, Mage = 23.29, SD = 2.89). The experiment was conducted using a paper-and-pencil test offline. Participants would receive a small gift as a reward upon completion of the experiment.

A 9-point scale was used to assess the morality of principal sources and means of profit making to be used in the formal experiments. The two principal sources were (1) acquiring income from environmentally friendly enterprises and (2) from environmentally hazardous enterprises, and the two profit methods were (1) investing in environmentally friendly enterprises and (2) investing in environmentally hazardous enterprises. Environmentally friendly enterprises were described as those having adopted environmentally friendly technology for production and profit-making and those having a production process that has no pollution discharge and conserves resources; environmentally hazardous enterprises were described as those having adopted environmentally hazardous technology for production and profit and those having a production process that has pollution discharge and waste resources.

The following four statements were designed for the manipulation check, which was randomly presented to participants to counterbalance the possible sequence effect. Participants were asked to rate the morality of principal sources and profit methods on a 9-point scale from −4 (very immoral) to +4 (very moral).

Investing ¥100,000 principal in an environmentally friendly enterprise. Investing ¥100,000 principal in an environmentally hazardous enterprise. Acquiring ¥100,000 income from an environmentally friendly enterprise. Acquiring ¥100,000 income from an environmentally hazardous enterprise.

Results

Assessment scores of the moral principal source (M = 2.57, SD = 1.63) were higher than for the immoral principal source (M = −1.48, SD = 1.38), t(82) = 12.29, p < .001. Likewise, assessment scores of the moral profit method (M = 2.67, SD = 2.07) were higher than for the immoral profit method (M = −1.33, SD = 1.06), t(82) = 11.15, p < .001. Hence, it was effective to adopt these contexts in the formal experiments.

Study 1: Effect of the morality of principal sources on intertemporal investment decisions

In this study, the morality of principal sources was manipulated to investigate its effect on intertemporal investment decision-making and the mediating effect of guilt.

Methods

Participants

A total of 130 non-psychology major participants were recruited from several general education courses (58 men, Mage = 21.96, SD = 2.22). The experiment was conducted using a paper-and-pencil test offline. Participants would receive a small gift as a reward upon completion of the experiment.

Design and procedure

A between-subjects design was adopted with the morality of principal sources (moral vs. immoral) as independent variables and intertemporal investment preference for SS and guilt as dependent variables. Participants’ guilt tendency and time perspective were also measured to control for their potential influence.

Each participant was randomly presented with one of two versions of the experimental material. In the moral condition, participants were asked to imagine acquiring income from an environmentally friendly enterprise, while in the immoral condition, they were asked to imagine acquiring income from an environmentally hazardous enterprise. Participants rated their preference for Plan A or B on a 9-point scale from 1 (Prefer Plan A) to 9 (Prefer Plan B). Next, they rated their guilt about being paid by environmentally friendly or hazardous enterprises on a 9-point scale from −4 (very justified) to +4 (very guilty). Finally, the future time perspective scale (Zimbardo et al., 1997) and the Chinese version of the situational guilt inventory (Hu, 2008) were completed.

Materials

(1) Two kinds of intertemporal investment decision-making contexts were employed: investment principal that originated from either (1) environmentally friendly or (2) hazardous enterprises. An example instruction was given as follows: Suppose you work for a company that adopts environmentally hazardous technology for production and profit, whose production process has pollutant discharge and wastes resources. The company paid you a salary of ¥100,000 and you can use the money as principal for financial investment. Here, there are two alternative plans for you to consider:

Plan A: Redeeming your principal and reaping a profit of ¥18,000 in 1 year. Plan B: Redeeming your principal and reaping a profit of ¥30,000 after 2 years.

Which plan do you prefer? Please circle the corresponding number on the 9-point scale below.

How do you feel about receiving ¥100,000? Please circle the corresponding number on the 9-point scale below. 1

(2) Chinese version of the situational guilt inventory (SGI)

A 37-item scale was used to measure guilt tendency (Hu, 2008). A sample item from this measure is “Please choose the degree of guilt you would have if you betrayed a friend.” Participants rated their feelings of guilt on a 4-point scale from 1 (Do not feel guilty) to 4 (Feel guilty). Higher scores are indicative of a higher participant guilt level (α = .69–.77)

(3) Future time perspective scale

Future time perspective was measured by this 11-item scale (Zimbardo et al., 1997). A sample item is “Every day should be planned in advance,” which was rated on a 5-point scale ranging from 1 (Never) to 5 (Very frequently). A higher score indicated more future time perspective (α = .76).

Results

Effect of the morality of principal sources on intertemporal investment decision-making

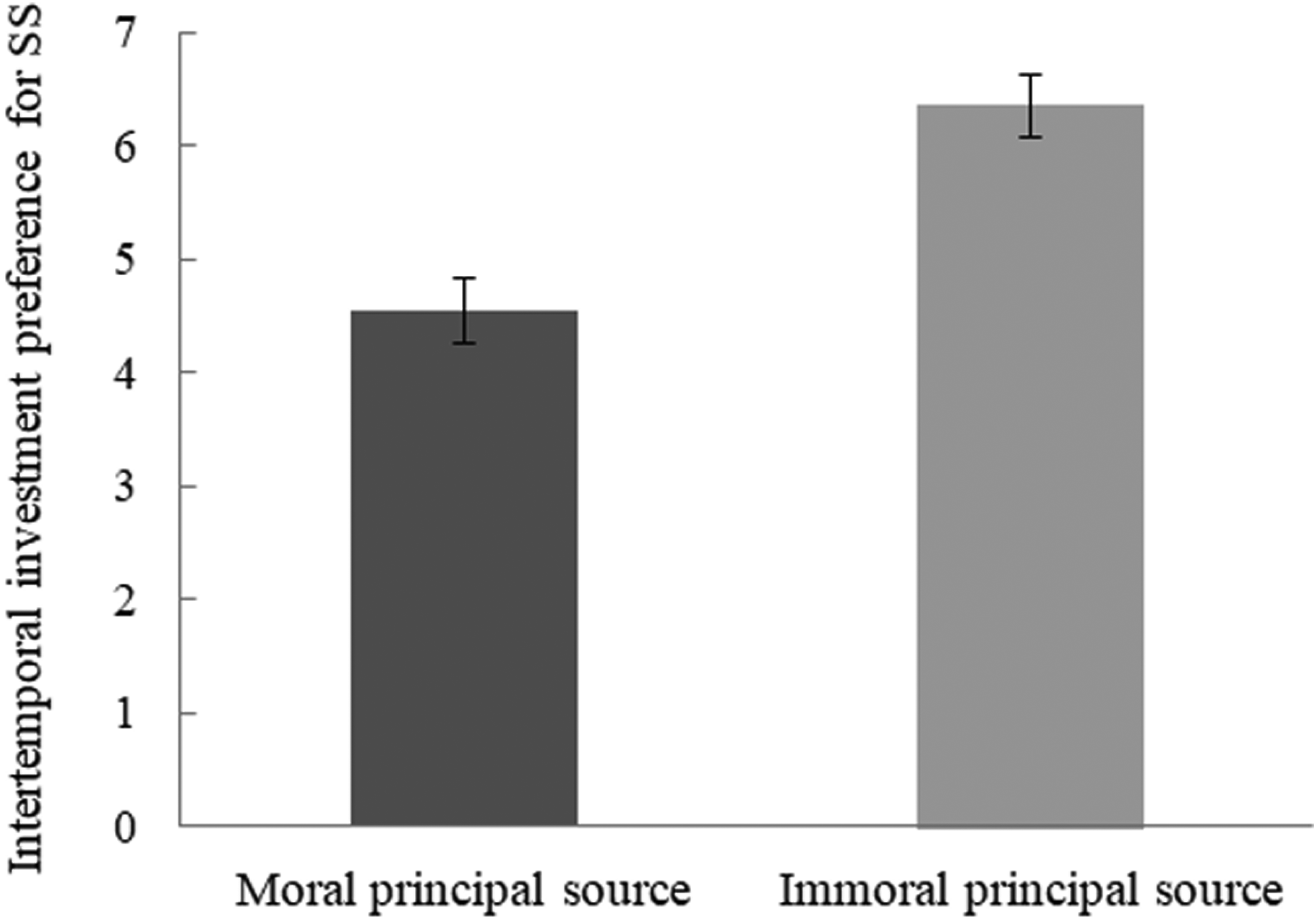

An analysis of covariance (ANCOVA) was conducted on the intertemporal investment preference for SS, with the morality of principal sources as an independent variable and future time perspective as a covariate. 2 The results revealed that the main effect for the morality of the principal source was significant: F(1, 127) = 18.59, p < .001, ŋp2 = 0.128. Participants using the immoral principal source (M = 6.37, SD = 2.44) chose the SS outcome more than participants using the moral source (M = 4.56, SD = 2.33; see Figure 1). Thus, H1 is supported.

Intertemporal investment preference for SS as a function of the morality of principal sources.

Effect of the morality of the principal source on guilt

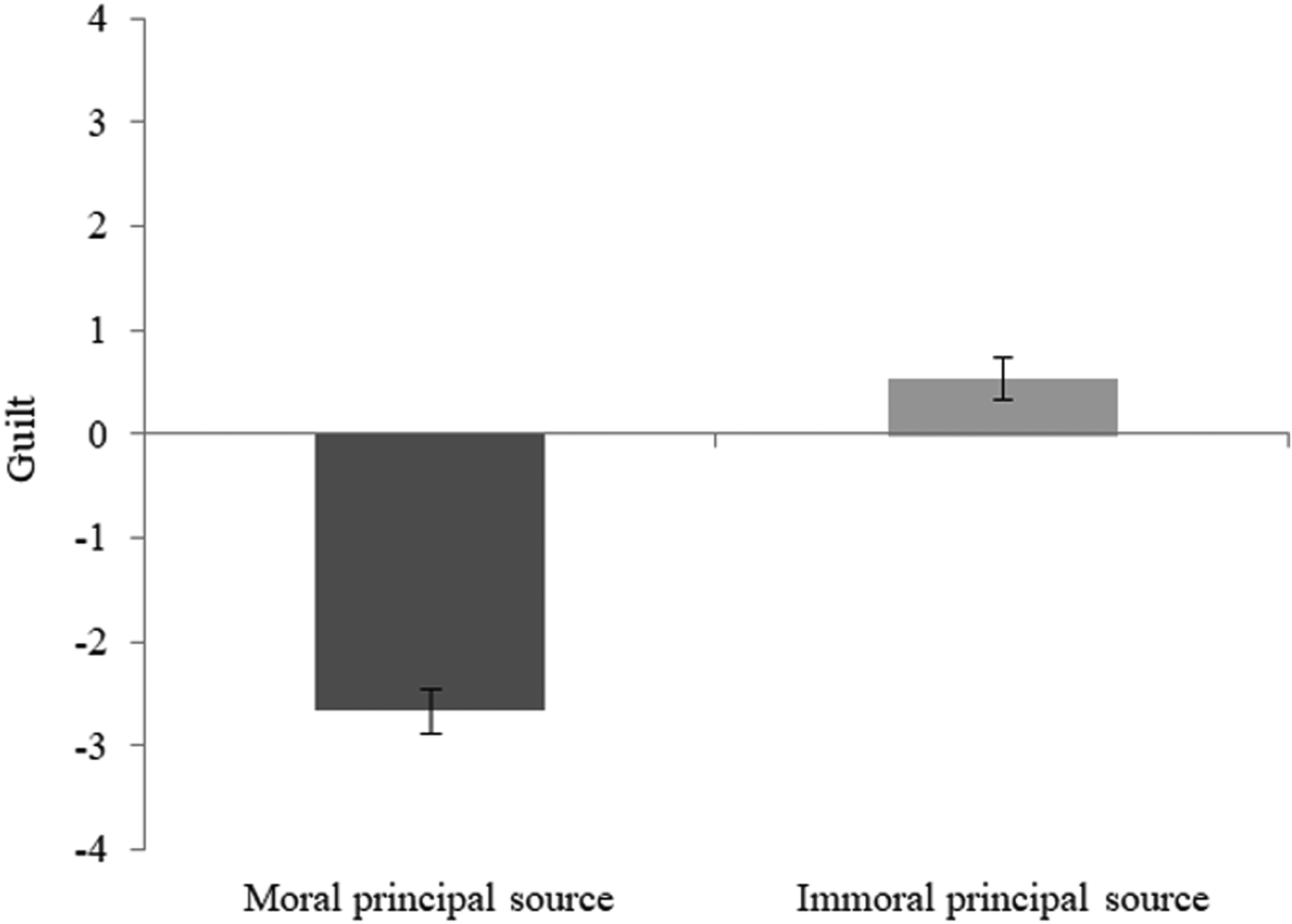

An ANCOVA was conducted on guilt, with the morality of the principal source as the independent variable and SGI score as a covariate. The results revealed that the main effect for the morality of principal sources was significant, F(1, 127) = 116.50, p < .001, ŋp2 = 0.478. Participants with money from an immoral principal source (M = 0.54, SD = 1.90) felt guiltier than those with money from a moral principal source (M = −2.67, SD = 1.55; see Figure 2).

Guilt as a function of the morality of principal sources.

The mediating effect of guilt

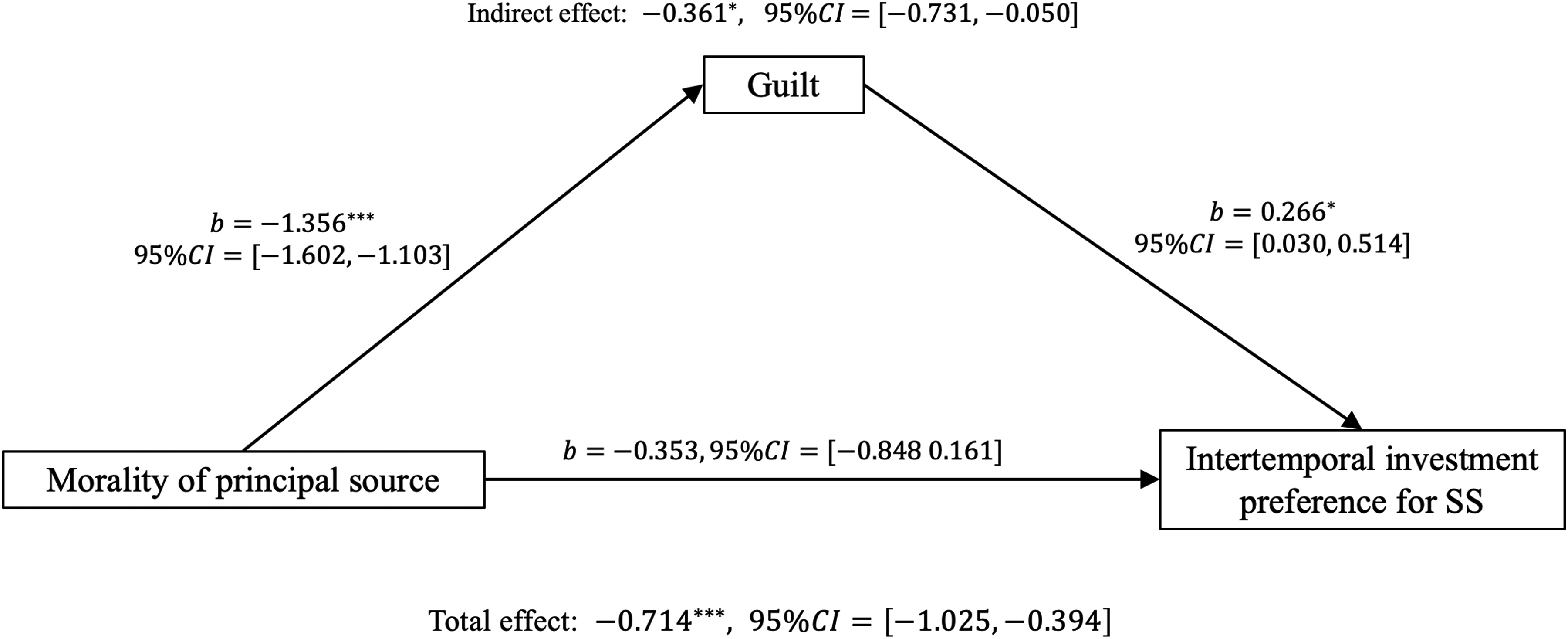

Following the bootstrap procedure (Preacher & Hayes, 2008), the morality of principal sources (1 = immoral principal source, 2 = moral principal source) served as the independent variable, guilt served as the potential mediator, and participants’ intertemporal investment preference for SS served as the dependent variable. Based on 5,000 bootstrap samples (biased-corrected percentile), the analysis revealed a significant total effect (−0.714, p < .001, 95%CI [−1.025, −0.394]), a significant indirect effect for guilt (−0.361, p = .018, 95% CI [−0.731, −0.050]) and an insignificant direct effect (−0.353, p = .105, 95% CI [−0.848, 0.161]). Thus, these results supported H3a. Figure 3 showed the standardized path coefficients and their significances.

Mediation analysis.

Study 2: Effect of the morality of the profit method on intertemporal investment decisions

In Study 2, the morality of the profit method was manipulated. We investigated its effect on intertemporal investment decision-making and the mediating effect of guilt.

Methods

Participants

A total of 127 non-psychology major participants were recruited from several general education courses (68 men, Mage = 21.88, SD = 2.38). The experiment was conducted using a paper-and-pencil test offline. Participants would receive a small gift as a reward upon completion of the experiment.

Design and procedure

A between-subject design was adopted, with the morality of profit method (moral vs. immoral) as the independent variable and intertemporal investment preference for SS and guilt as dependent variables.

The two versions of the experimental material are as follows: In the moral condition, participants were asked to imagine investing in an environmentally friendly enterprise, while in the immoral condition, they were asked to imagine investing in an environmentally hazardous enterprise. The remaining procedure was identical to that in Study 1.

Results

Effect of the morality of profit method on intertemporal investment decision-making

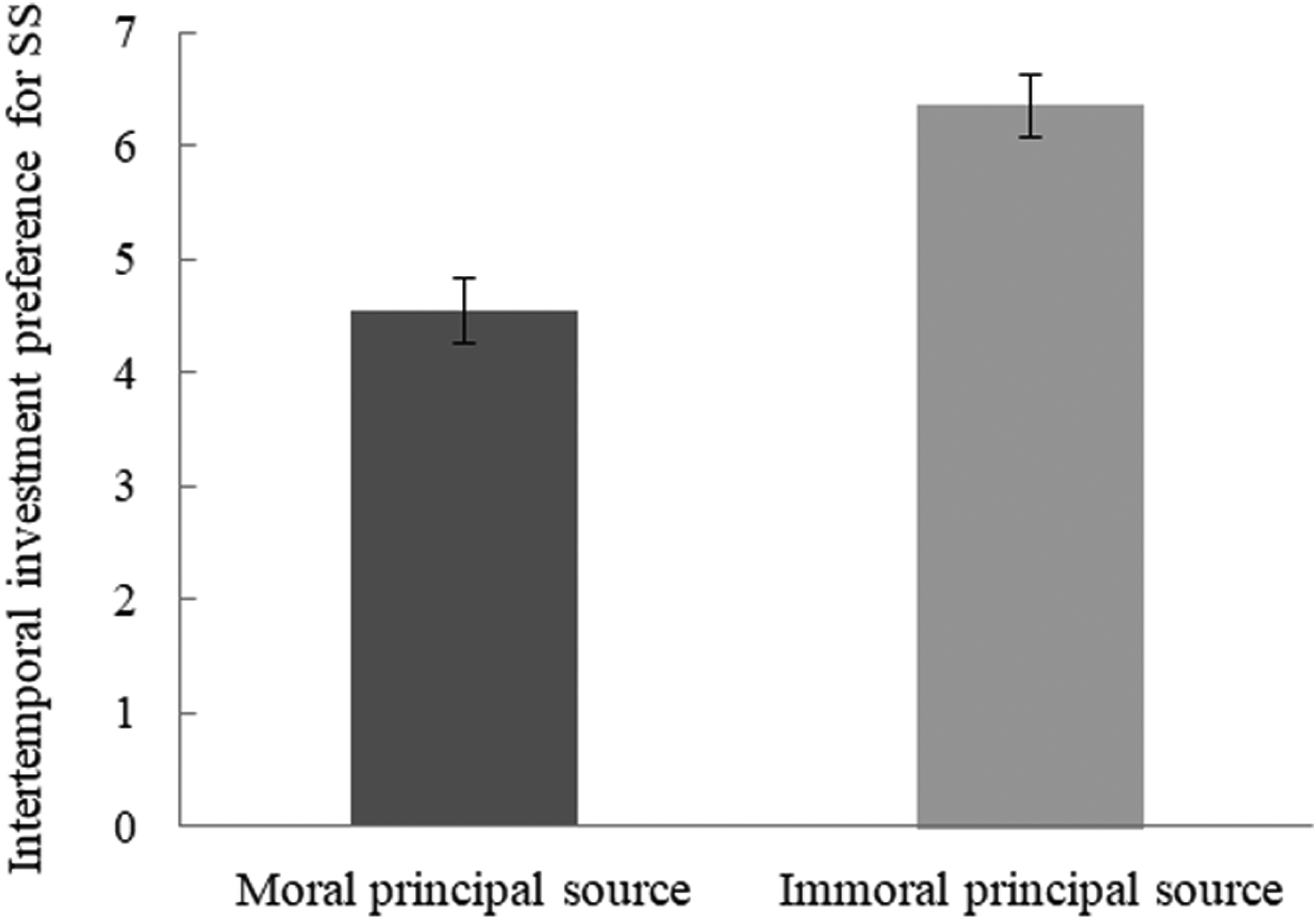

An ANCOVA was conducted on the intertemporal investment preference for SS, with the morality of profit method as an independent variable and future time perspective as a covariate. The results reveal that the main effect for the morality of profit method is significant: F(1, 124) = 17.11, p < .001, ŋp2 = 0.121. Participants who invested in an immoral company (M = 6.03, SD = 2.09) chose the SS outcome more often than those who were asked to invest in a moral one (M = 4.39, SD = 2.34; see Figure 4). Thus, H2 is supported.

Intertemporal investment preference for SS as a function of the morality of the profiting method.

Effect of the morality of profit method on guilt

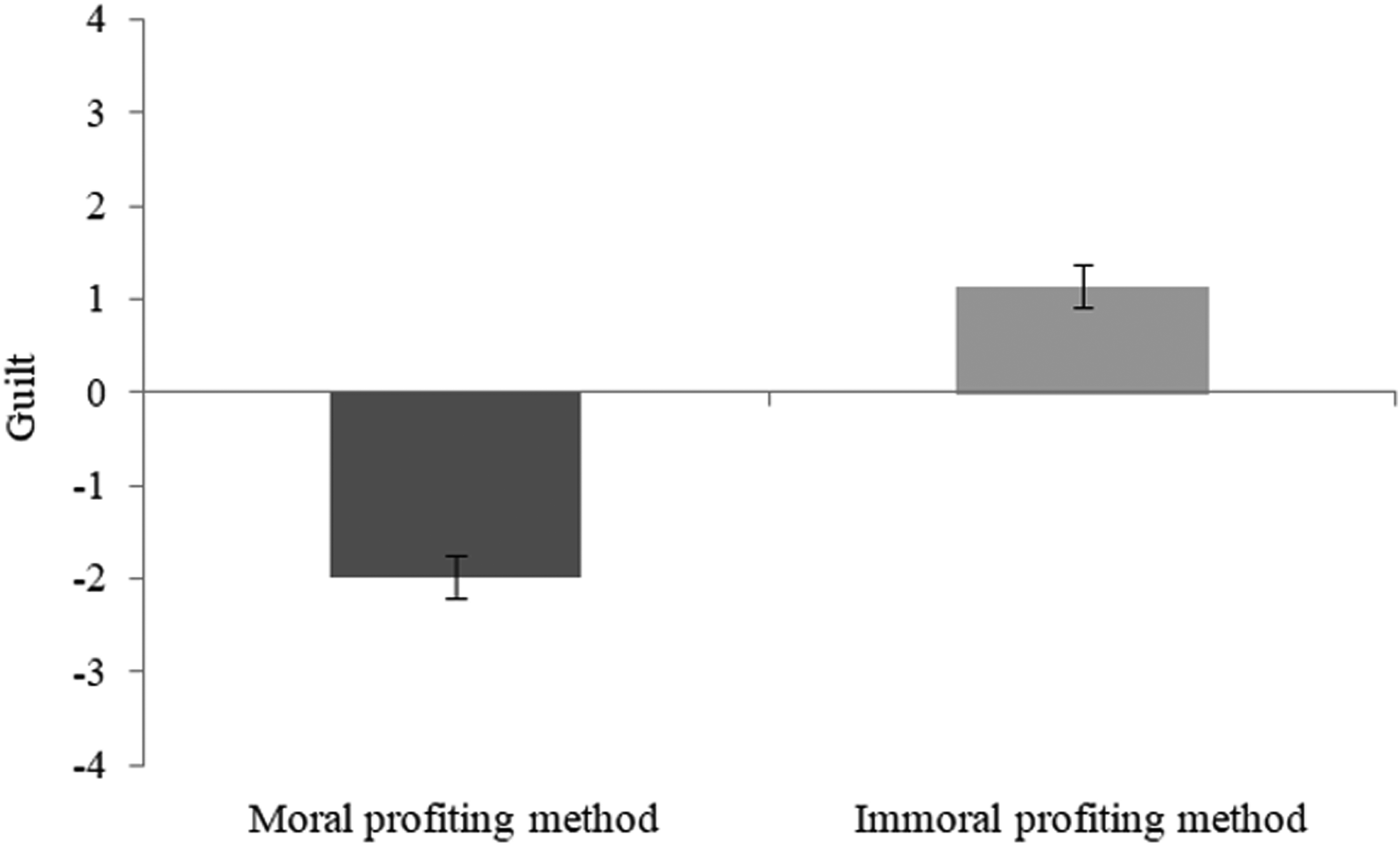

An ANCOVA was conducted on guilt, with the morality of profit method as the independent variable and SGI score as a covariate. The results reveal that the main effect for the morality of profit method was significant: F(1, 124) = 92.12, p < .001, ŋp2 = 0.426. Participants who invested in an immoral company (M = 1.14, SD = 2.17) felt guiltier than those who invested in a moral company (M = −1.98, SD = 1.36; see Figure 5).

Guilt as a function of the morality of profiting methods.

The mediating effect of guilt

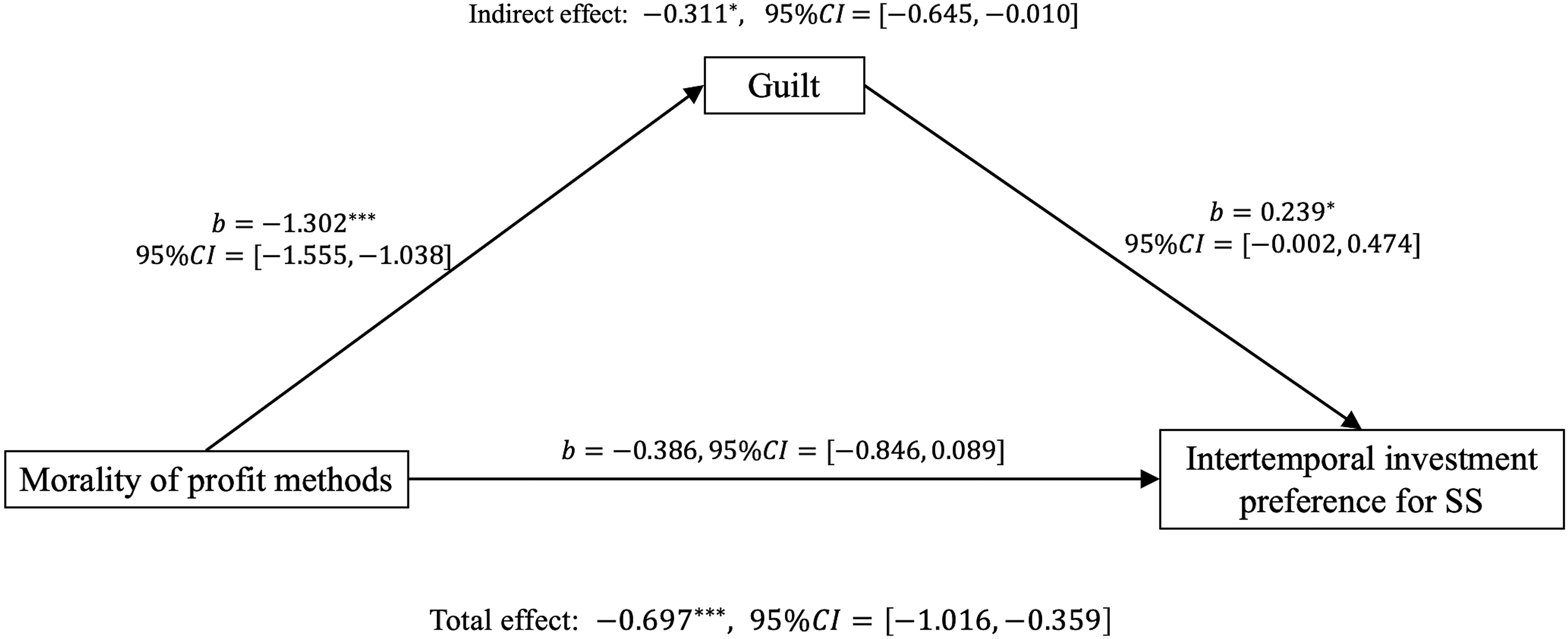

Following the bootstrap procedure (Preacher & Hayes, 2008), the morality of profit method (1 = immoral profit method, 2 = moral profit method) served as the independent variable, guilt served as the potential mediator, and participants’ intertemporal investment preference for SS served as the dependent variable. Based on 5,000 bootstrap samples (biased-corrected percentile), the analysis revealed a significant total effect (−0.697, p < .001, 95%CI [−1.016, −0.359]), a significant indirect effect for guilt (−0.311, p = .0311, 95% CI [−0.645, −0.010]) and an insignificant direct effect (−0.386, p = .072, 95% CI [−0.846, 0.089]). Thus, these results supported H3b. Figure 6 showed the standardized path coefficients and their significances.

Mediation analysis.

Study 3: The joint effect of the morality of the principal source and profit method on intertemporal investment decision-making

In Study 3, the morality of principal sources and profit methods were both manipulated, and we explored the interaction effect on intertemporal investment decision-making.

Methods

Participants

A total of 220 non-psychology major participants were recruited from several general education courses (112 men, Mage = 22.17, SD = 1.80). The experiment was conducted using a paper-and-pencil test offline. Participants would receive a small gift as a reward upon completion of the experiment.

Design and procedure

A 2 (principal source: moral, immoral) × 2 (profit method: moral, immoral) between-subjects design was adopted with the intertemporal investment preference for SS and guilt (invested income from Company A into Company B) as dependent variables.

Four versions of experimental materials were used (i.e., investment principal for intertemporal decision-making originating from environmentally friendly or hazardous enterprises that were invested in environmentally friendly or hazardous enterprises to earn profits). For instance, participants were asked to imagine acquiring income from an environmentally friendly enterprise (Company A) and then use this income as the principal to invest in another environmentally friendly enterprise (Company B). Participants had to choose between two financing plans offered by company B. The remaining procedure was identical to that in Study 1.

Results

Joint effect of the morality of the principal source and profit method on intertemporal investment decision-making

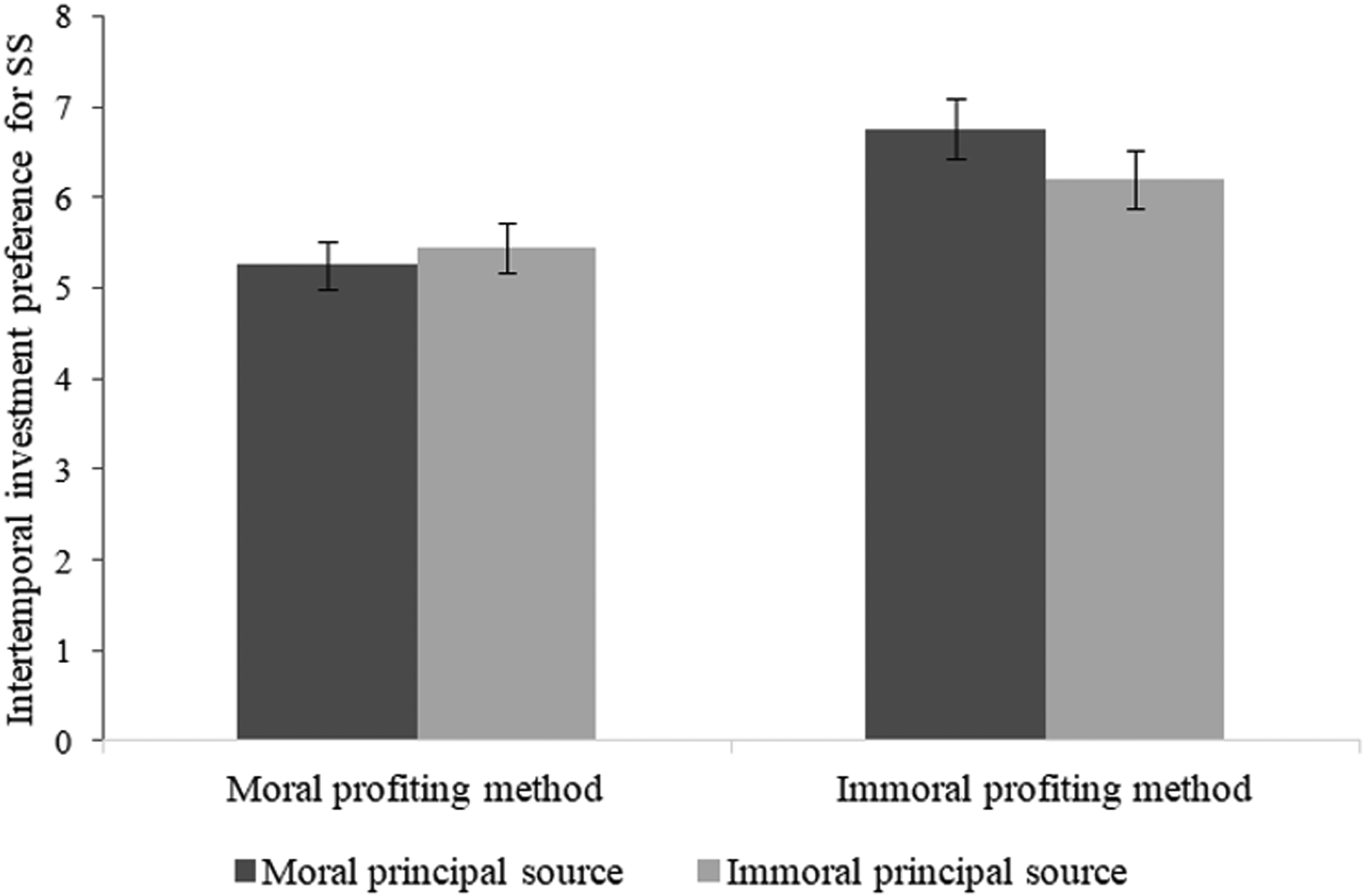

A 2 (principal source: moral, immoral) × 2 (profit method: moral, immoral) analysis of variance (ANOVA) was conducted on the intertemporal investment preference for SS. The main effect for the morality of the profit method was detected: F(1, 216) = 8.91, p = .003, ŋp2 = 0.040. Participants who invested in an immoral company chose the SS outcome more often than participants who invested in a moral one. However, the main effect for the morality of the principal source and the interaction between the morality of the principal source and the profit method was not significant: F(1, 216) = 0.24, p = .627, ŋp2 = 0.001 and F(1, 216) = 0.98, p = .324, ŋp2 = 0.005, respectively (see Figure 7). Therefore, H4 is not supported.

Intertemporal investment preference for SS as a function of the morality of principal sources and profiting methods.

The joint effect on guilt

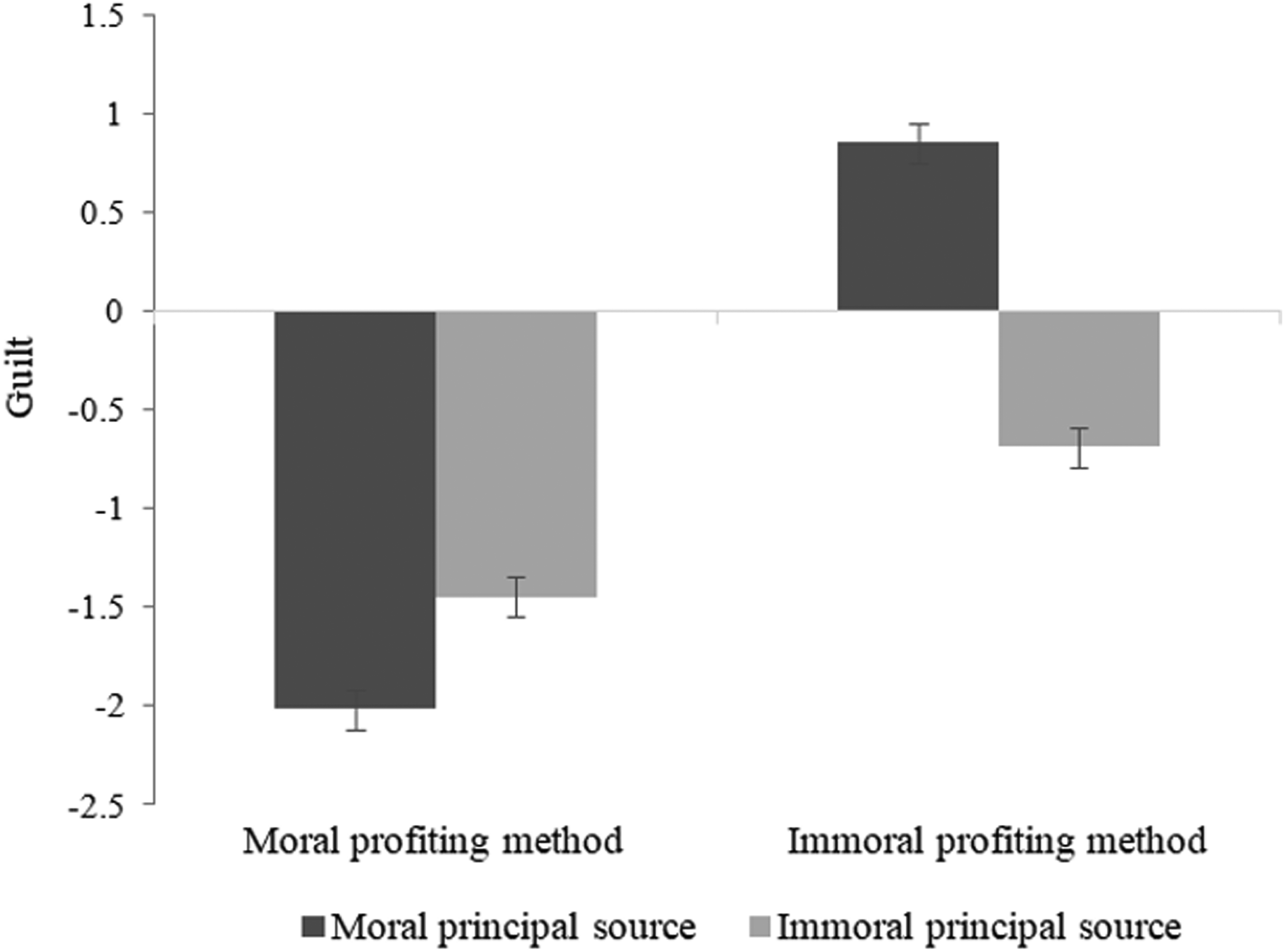

A 2 (principal source: moral, immoral) × 2 (profit method: moral, immoral) analysis of variance (ANOVA) of guilt yielded no significant effect for the morality of principal source: F(1, 216) = 2.45, p = .119, ŋp2 = 0.011. The main effect for the morality of profit method was significant: F(1, 216) = 34.61, p < .001, ŋp2 = 0.138. Participants who invested in an immoral company felt guiltier than those who invested in a moral one. The interaction between the morality of the principal source and the profit method was significant: F(1, 216) = 11.64, p < .001, ŋp2 = 0.051 (see Figure 8). Participants felt most guilty when investing moral principal in immoral projects rather than when both the principal source and the profit method were immoral.

Guilt as a function of the morality of principal sources and profiting methods.

The mediating effect of guilt

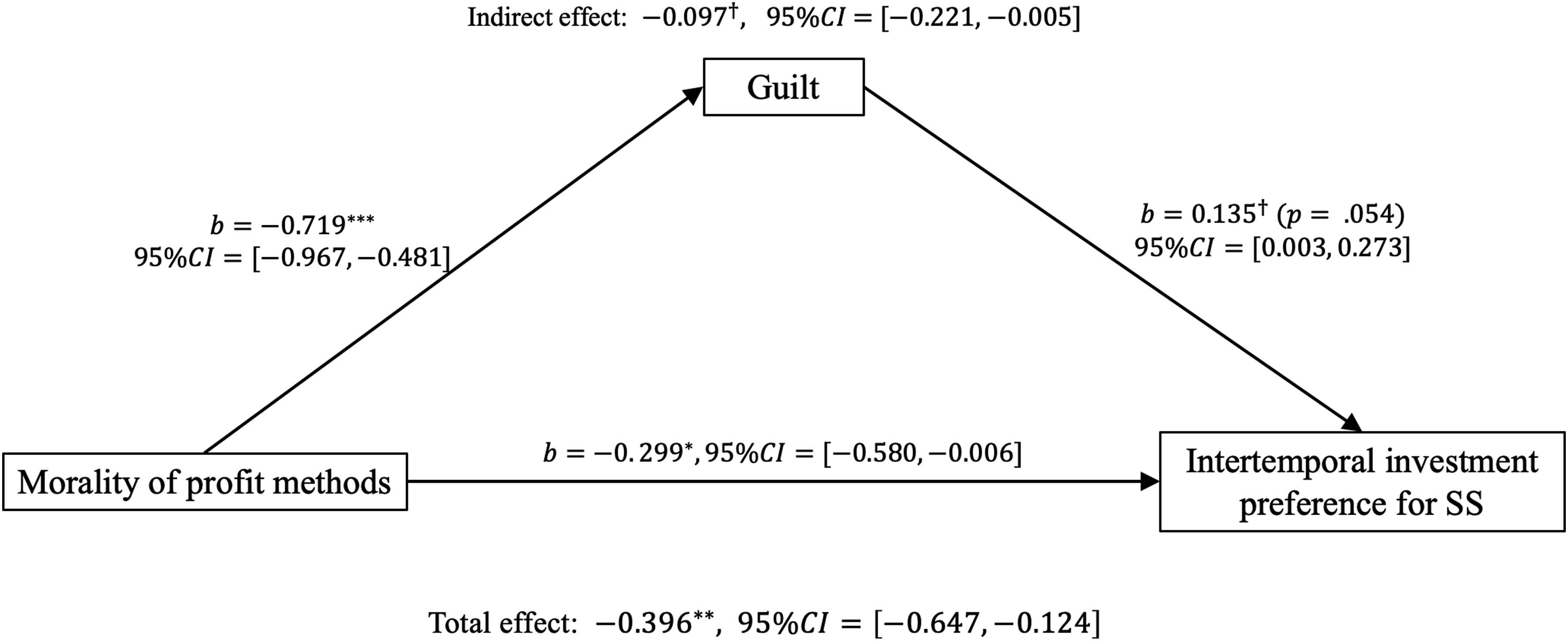

Since the main effect for the morality of the principal source and the interaction between the morality of the principal source and the profit method was not significant, we conducted a mediation analysis with the morality of profit method (1 = immoral profit method, 2 = moral profit method) as the independent variable, guilt as the potential mediator, and participants’ intertemporal investment preference for as the dependent variable. Based on 5,000 bootstrap samples (biased-corrected percentile), the analysis revealed a significant total effect (−0.396, p < .01, 95%CI [−0.647, −0.124]), a marginally significant indirect effect for guilt (−0.097, p = .068, 95% CI [−0.221, −0.005]) and a significant direct effect (−0.299, p = .033, 95% CI [−0.580, −0.006]). Figure 9 showed the standardized path coefficients and their significances.

Mediation analysis.

General discussion

This study reveals the phenomenon that immoral money can lead to myopic behavior in future intertemporal investment decisions, and explains the reasons from the perspective of moral psychology: the immorality of money makes individuals feel guilty, and tendency of guilt aversion leads to a preference for myopic behavior. The results of Studies 1 and 2 indicate that both the principal source and profit method have similar effects on preference in intertemporal investment choice. That is, money immorality increases the possibility that investors will select the SS option. Study 3 further inspected the joint effect of the morality of the principal source and profit method. The result suggests that both principal source and profit method influence decision-makers’ preferences, but no interaction effect is found.

Money morality matters in intertemporal decision-making related to investments

When people were asked to use immoral principals in investing, they tended to choose projects with less reward over a short period of time rather than projects with a greater reward over a long period of time. However, that was not the case when people were asked to use principal from moral or neutral sources. We suggest that this is because people tend to launder or “cleanse” the immoral principal as quickly as possible through short-term investment to mitigate feelings of guilt. Preference for intertemporal investments differs due to the two principals (moral vs. immoral), which means that moral and immoral money are not the same and are therefore not fungible. We propose that these effects have two causes. First, moral and immoral money are deposited in different emotional accounts, a variant of mental accounting that categorizes money on the basis of the feeling it evokes (Levav & McGraw, 2009). Likewise, there may be a “moral account” that categorizes money based on its morality. Second, the morality of money could make a difference in the value of the money. Specifically, we would expect that money value includes two categories: economic value and emotional value. The economic value of moral and immoral money is the same; however, the emotional value is different, leading to different psychological values. The titrated decision-making pair is balanced in terms of economic value, but the intervention of the immoral attribute of money gives the SS option a smaller negative emotional value, so the preference for the SS option yields.

When people were asked to invest in immoral enterprises or projects, the morality of the reward in both the SS and LL options influenced intertemporal investment preference, which means there are certain limitations within former decision-making models (e.g., EU, PT, DU) that regard gains and losses as morally irrelevant or neutral. The different morality of profit methods results in different morality of the payoff matrix. Therefore, former models are not able to effectively describe and predict people's decision-making behaviors.

When people were asked to invest principal (moral/immoral) in enterprises or projects (moral/immoral), the main effect of the morality of profit method was significant, but not of principal source. Whether the principal source is moral or not, investors will prefer the SS option as long as the profit method is immoral.

Guilt aversion in investment decision-making involving moral concerns

Studies 1 and 2 further investigated the mechanism behind the effects of the morality of principal sources and profit methods on intertemporal investment decision-making. The preference for SS is shown to result from participants feeling guilty about immoral money (regardless of principal source or profit method) in the intertemporal investment choice task. As indicated by approach-avoidance motivation theory (Elliot, 2006), the avoidance motivation of guilt aversion would take advantage of approach motivation of earning more money in a long period, since decision-makers do not want to experience guilt over a long period. Therefore, they choose the SS option to avoid or alleviate that guilt. In decision-making involving moral factors, “guilt aversion” can be a decision rule or heuristic analogous to risk aversion and avoidance of uncertainty.

It is noteworthy that when the morality of the principal source and the profit method were combined in Study 3, the results showed that the morality of principal source exerted no significant effect on either preference for SS or guilt. However, profit methods significantly influenced preference for SS and the mediation effect of guilt was marginally significant. The morality of principal source seemed to be “ignored” by participants. We speculate that this is because when both principal source and profit method were considered simultaneously, participants focused more on profit methods (i.e., whether the invested enterprise is environmentally friendly or not). For participants, the profit method is more proactive, as it involves how to use the money, whereas the source of the principal is more passive, as it pertains to where the money was earned. “Moral agency” theory indicates that when people believe their actions are a result of autonomous choice, they feel a stronger sense of moral responsibility (Oshana, 2013). Nevertheless, principal source and profit methods do have an interaction effect on guilt. When principal source is immoral, people would like to invest in a moral profit method for moral cleansing and guilt relief (compensatory effect); when both principal source and profit method are immoral, the level of guilt would rise but only to a limited extent, because the immorality of principal source make people feel numb of the immorality of profit methods (numb effect). When principal source is moral, people would like to invest in a moral profit method to keep behavioral consistency (Mullen & Monin, 2016) and the level of guilt is of course the lowest (consistency effect); when principal source is moral but profit method is immoral, the moral consistency is broken negatively and the level of guilt is the highest (enhancing effect).

Implications and future directions

By investigating the influence of the morality of the principal source and profit method on investors’ preferences in intertemporal investment decision-making, the present study introduces the moral dimension of money in decision-making research, which has been neglected by traditional decision-making models (e.g., EU, PT, DU). We found that money morality, as a decision-making cue, affects individuals’ choice preferences, which expands current knowledge of the process of investment decision-making. In addition, our results challenge the concept of fungibility, that is, that the source of money should make no difference in the value of the money (Von Neumann & Morgenstern, 1947). The results of our experiments indicate that when using immoral principal to invest or when investing in immoral projects, decision-makers’ choices often deviate from choices made in moral situations. Thus, the results further challenge the fundamental assumption of source independence, in which the value of money from different sources is considered to be the same. Finally, the current study proposes a moral emotional mechanism, namely, guilt aversion or alleviation, to interpret the effects of money morality on intertemporal investment decision-making. Zhang et al. (2014) called for intensive study on the impact of guilt on subsequent behaviors, as well as on the relationship between many social activities and guilt. This study explores the influence of guilt on intertemporal investment decision-making, a crucial social activity, from the perspective of moral emotion.

This study holds significant practical implications. Although environmentally hazardous investments often result in negative ecological consequences, they continue to attract investors due to their potential for rapid, short-term economic gains. However, these investments not only yield immediate ecological harm, but the associated money also carries an inherent immorality. This leads investors to become more shortsighted in their future intertemporal investment decisions, generating further negative economic outcomes. As a manifestation of shortsighted behavior itself, environmentally hazardous investments perpetuate a vicious cycle of shortsightedness and unsustainable development. This serves as a valuable lesson for governments, businesses, and individuals. Governments should promote and establish a business environment that prioritizes investment morality, ensuring long-term sustainable economic development. Businesses should expedite their green transformation in pursuit of lasting investments, while individuals must carefully weigh moral factors, such as environmental impact, when making investment decisions to avoid shortsighted behavior.

This study has several potential limitations. First, alternative mechanisms behind immoral money and investment myopia should be further examined. The present study proposes a moral emotion mechanism, namely, guilt aversion or alleviation, to interpret the effects of money morality on intertemporal investment decision-making. Future research can continue to explore other possible mechanisms from different perspectives. For example, is it possible that the immorality of principal sources and profit methods could cause an underestimation of their value, resulting in a preference for SS? Second, there were indeed some extraneous variables in the experiment that could not be fully eliminated. Since we used environmentally unfriendly money as immoral money, participants may choose LL more because the terms (e.g., environmentally friendly) primed them to focus more on future considerations, or participants may choose SS more because of concerns over the potential collapse of such enterprise due to external policy influences. Future studies may improve the experimental design to eliminate these potential variables. Third, the present study only focused on how the immorality of money influences intertemporal decision preferences by affecting feelings of guilt. However, the differing monetary profits of SS and LL options might also influence guilt. Higher monetary returns could potentially reduce feelings of guilt. Future research could explore this issue further. Fourth, investment decisions are usually delayed and uncertain, resulting in characteristics of both intertemporal and risky decision-making. This study primarily stresses the effects of money morality on intertemporal investment decision-making. Future studies may shed light on the effects of money morality on other types of decision-making.

Supplemental Material

sj-docx-1-pac-10.1177_18344909241293834 - Supplemental material for Immoral money aggravates myopia in intertemporal investment decision-making

Supplemental material, sj-docx-1-pac-10.1177_18344909241293834 for Immoral money aggravates myopia in intertemporal investment decision-making by Zetong He, Wenjing Lin and Guibing He in Journal of Pacific Rim Psychology

Footnotes

Acknowledgements

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Ethics statement

This present study received ethical approval from the Research Ethics Committee of Zhejiang University.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Natural Science Foundation of China, STI 2030—Major Projects (grant number 71671162, 72071178, 2021ZD0200409).

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.