Abstract

Contextualizing in the digitalization of personal finance (e.g., mobile banking), the present research explores how financial decisions made on smartphones (vs. laptops or tablets) are more likely to be shortsighted, manifesting in being unwilling to save for retirement, referring to recent information while making financial decisions, and opting for instant but smaller rewards. We trace the effect to smartphones’ affordance of ubiquity, an attribute that allows users to satisfy various needs with considerable flexibility of time and space and prompts users to seek instant gratifications. We also rule out potential alternative factors that might account for this effect, including haptic gratification, direct-touch effect, task difficulty, thinking style, concentration, and the hedonic usage of the devices by users. Furthermore, we demonstrate that prompting users to deliberate on their decisions successfully attenuates the effect. Implications for the development of interventions are discussed.

Introduction

We can sell stocks, borrow money from a friend and cash out our 401(k)'s … My concern is that these so-called smartphones could encourage decisions that are not so smart, especially when it comes to our finances … We might neglect the long-term consequences of our behavior.

For many, the term “banking” may no longer mean planning a trip to a town center or a queue in front of the counter, but particular apps on their smartphones. Mobile banking has been worshipped as a convenient tool. Traditional banks such as HSBC drive customers to mobile banking in their cost-cutting moves (Ng, 2020), while new banks such as Monzo and Revolut are digital-only. In the United States, more than 50% of the customers who have adopted mobile banking actively use mobile banking (Crowe et al., 2019). Facilitated by mobile banking and other similar financial apps, most financial activities (e.g., making a deposit, taking out a loan, and making investments) take place on mobile devices especially through smartphones (Frost, 2020). By March 2020, 776.08 million people adopt mobile transactions in China (Daxue Consulting, 2021) so that the value of apps in emerging markets is expected to exceed $870 billion in 2026 (Maynard, 2022).

Contextualizing the unstoppable trend of digitalization in the domain of personal finance, the present research aims to further our understanding of the consequences entailed by making financial decisions on mobile devices, especially smartphones. Adopting mobile devices has been found to increase impulsivity and decrease deliberative decision-making (e.g., Schwartz, 2011; Seeger et al., 2018; Shen et al., 2019; Xu et al., 2016; Zhu & Meyer, 2017). For example, purchases made via mobile channels are positively associated with product returns, implying the likelihood of error-prone purchase decisions in the mobile internet environment (Seeger et al., 2018). Mobile devices with a touchscreen, compared with desktops, have been found to increase the likelihood of hedonic food consumption because of the “direct-touch” effect (Shen et al., 2016). In addition, people are more likely to make virtuous decisions (e.g., volunteering) on paper rather than on a digital device because the choices in the former context appear to be more authentic (Touré-Tillery & Wang, 2022).

In this research, we take a closer look at the relationship between mobile device use and its undesirable consequence in an important but ill-informed domain—financial decision-making (Aren & Hamamci, 2021; Sahi, 2017). In addition, this research is grounded in the notion that all “screens” do not equally influence users’ behavior. Specifically, we propose that smartphones should be differentiated from other mobile devices such as laptops and tablets, because of its high affordance of ubiquity—it is expected to satisfy the users’ needs anywhere and anytime. Such high levels of ubiquity will further increase the likelihood of shortsighted financial decision-making.

Ubiquity implies that people's needs are expected to be addressed without the restrictions of time and space (Balasubramanian et al., 2002; Barnes, 2002; Watson et al., 2002). Although they are common features shared by almost all versatile and mobile devices, smartphones are more portable and ubiquitous than other devices such as laptops (Barnes et al., 2019; Gao et al., 2009; Kim & Garrison, 2009; Okazaki et al., 2009). Smartphones instantly satisfy a variety of needs ranging from retrieving and seeking information, shopping, social networking, work, to entertainment. These qualities of smartphones indicate why smartphone use could sometimes be synonymous with streamlined experiences, quick solutions, instant gratification, and feel-good indulgence, which are often the opposite of well-thought-through decision-making that requires patience, deliberation, and long-term planning.

The ubiquity of smartphones has been argued to account for behaviors such as smartphone overuse and addiction (Barnes et al., 2019; Marciano et al., 2021; Panova & Carbonell, 2018) as well as impulsivity (Jung et al., 2019; Melumad & Pham, 2020; Sanbonmatsu et al., 2013; Wang & Tchernev, 2012). However, potential downstream effects in the domain of financial decision-making have not yet been fully examined (Aren & Hamamci, 2021; Sahi, 2017). This research question is important given that more and more financial activities are completed on smartphones. In the present research, we investigate how smartphones, compared to laptops and tablets, are more likely to result in shortsighted decision-making among users in broadly defined financial domains, ranging from saving for retirement, investing in funds, to choosing rewards. We propose that the effect is mediated by the level of ubiquity. We discuss the theoretical framework in the following section.

Theoretical framework

Ubiquity as a defining attribute of smartphones

The demarcation and scope of the term mobile devices could sometimes be ambiguous. In the present research, we use the term to refer to portable and versatile devices that allows users to connect to the Internet to satisfy a variety of needs via apps, software, and access to webpages. It excludes devices such as basic cellular phones, e-book readers, smart watches, or desktops. Among all the mobile devices, smartphones are the most dominant in terms of market share. Since the launch of the iPhone in 2007, the amount of smartphone users has been booming. According to the report of Bankmycell (2022), in the year 2022, 6.648 billion people in the world have smartphones, which accounts for 83.96% of the world's population. Meanwhile, global smartphone users are estimated to reach 7.516 billion in 2026 (O’Dea, 2021).

Smartphones have several unique attributes that have the potential to significantly shape users’ behaviors. For example, users are more likely to self-disclose on smartphones than on laptops because smartphone users experience greater psychological comfort and concentrate more on their communication tasks (Melumad & Meyer, 2020). The touchscreens on smartphones have also been argued to induce affect-laden choices such as chocolate cakes (vs. fruit salad) because the sensation of touch mentally simulates interactions with products (Shen et al., 2016).

The current research focuses on another important attribute of smartphones—ubiquity (Okazaki & Mendez, 2013), which refers to how a device can be used almost anytime and anywhere to address various needs. Ubiquity manifests in four dimensions: continuity, immediacy, portability, and searchability (Okazaki & Mendez, 2013). Continuity refers to the state or quality of being “always on” (Kleijnen et al., 2007; Okazaki & Mendez, 2013). This is enabled by wireless communication technology, which allows users to address tasks and events seamlessly as they arise. Immediacy refers to the time at which an action can be performed, or the perceived amount of time between an action and its consequences (Crano, 1997). For example, mobile devices enable users to access information and receive responses quickly. Portability refers to the extent to which a device is light and small enough for users to carry for an extended period (Barnes, 2002; Bruner II & Kumar, 2005; Junglas & Watson, 2006; Kleijnen et al., 2007), and affects the usefulness and effectiveness of information search and communication (Garfield, 2005). Finally, searchability refers to the ability to conduct a thorough examination of available information and choices (Pascoe et al., 2000).

Compared with other mobile and versatile devices, smartphones afford a higher level of ubiquity (Barnes et al., 2019; Gao et al., 2009; Jung et al., 2019; Kim & Garrison, 2009; Okazaki et al., 2009; Okazaki & Mendez, 2013) for three reasons. First, smartphones provide various functionalities, such as internet access and various apps. The comprehensive functionalities increase users’ reliance on smartphones to satisfy various needs, ranging from social networking, shopping, work, studying, accessing information, to entertainment. Second, smartphones are highly portable (Melumad & Meyer, 2020), allowing their functionality to be accessed virtually anytime and anywhere. Finally, companies develop new functionalities in smartphones to respond to consumers’ demands, which further enhances smartphones’ ubiquity (Jung et al., 2019). While the affordance of multifunctionality has been argued to increase impatience (You et al., 2022), we argue that ubiquity better captures the essence that accounts for the significance of smartphones because the functions that are exclusive to smartphones and thus differentiate them from other devices, if any, are exactly those that render smartphone use as ubiquitous (e.g., making emergency calls, navigating). In the next section, we discuss how the attribute of ubiquity may lead to biased decision-making.

Ubiquity increases short-sighted financial decision-making

The effect of ubiquity on users has been documented in a handful of studies, mostly revolving around how ubiquity promotes the use of and dependency on smartphones (Jung et al., 2019; Zhang et al., 2021). For example, the fact that smartphones are reassuring presences for many is partly because of their high ubiquity (Melumad & Pham, 2020). Ubiquity may also explain why smartphones are more indispensable than other mobile devices. For example, in the USA, where 85% of the population own at least one smartphone, 15% of the adult population are “smartphone-only” internet users (Pew Research Centre, 2021) and approximately 50% of smartphone users regard it as something that they “could not live without” (Perrin, 2017).

The high level of ubiquity has not only strengthened the users’ dependency on smartphones, but has also changed the way users think and behave while using them, especially in terms of entailing shortsightedness, impulsivity, and seeking instant gratification (Jung et al., 2019; Melumad & Pham, 2020; Sanbonmatsu et al., 2013; Wang & Tchernev, 2012). For example, the adoption of mobile devices has been found to increase users’ impulsive behaviors in online dating, manifested in more log-ins, reading more information, and sending more content (Jung et al., 2019). The availability to purchase tickets anywhere and anytime with mobile devices has also increased users’ desire for such purchases (Bauer et al., 2007). In contrast, multitasking across devices, which is common in today's mobile internet environment, is positively correlated to self-reported impulsiveness (Sanbonmatsu et al., 2013; Wang and Tchernev, 2012), while limited processing resources increase the likelihood of affect-laden choices, such as chocolate cakes (vs. fruit salad) (Shiv & Fedorikhin, 1999). In addition, heavier users of mobile devices show weaker tendencies to delay gratification and greater inclinations toward impulsive behavior (Wilmer & Chein, 2016). Importantly, while the ubiquity of media and other information and communication technologies leads to impulsivity, the effect can be prominent along with users’ learning to associate the devices with particular affective and behavioral responses, so that using ubiquitous devices itself triggers an always-on mentality and a rather impulsive fashion of future usage (van Koningsbruggen et al., 2017)

To date, as summarized in Supplementary Appendix A, the downstream effects related to ubiquity and impulsivity have mainly been documented in the forms of excessive engagement, hedonic consumption, and unplanned buying (Benartzi, 2016). In the present research, we extend the scholarship to an ill-informed domain that witnesses many psychological biases—financial decision-making (Aren & Hamamci, 2021; Sahi, 2017). We focus on financial decision-making because it is increasingly prevalent for people to engage in financial activities such as purchasing, retailing, and making investments on smartphones (Crowe et al., 2019; Daxue Consulting, 2021; Frost, 2020). We propose that making financial decisions on smartphones, rather than laptops or tablets, causes people to focus more on immediate or short-term benefits while neglecting long-term consequences, leading to shortsighted decision-making.

It is noteworthy that in our empirical study design, we compare the effect of smartphone use with that of laptop use or tablet use for two reasons. First, while smartphones are perceived to be the most ubiquitous among mobile devices (Barnes et al., 2019; Gao et al., 2009; Kim & Garrison, 2009; Okazaki et al., 2009), laptops could be on the opposite end of the spectrum of ubiquity while tablets should be in the middle. Thus, including laptops and tablets as contrasts in the design of empirical studies helps us to detect the effect of ubiquity in influencing financial decision-making. Second, smartphones, laptops, and tablets are included in our empirical studies to mirror the real-world personal finance experience where these devices are often necessary to access all functionalities. In the USA, for example, more than half of adult smartphone owners use mobile banking services (Benartzi, 2016). However, apps for mobile banking often come with only crucial features while online banking enables access to more potential features. In other scenarios, one may need both devices to complete certain tasks—one trying to make a transnational fund transfer through the webpage may be prompted to generate a security code using apps on a smartphone. This may also explain why laptops have often been adopted as the comparison group while investigating the effects of smartphone use (e.g., Melumad et al., 2019; Melumad & Meyer, 2020).

Taken together, we hypothesize that while making financial decisions, people who do so by using smartphones are more likely to make shortsighted financial decisions if compared to those using laptops or tablets, and this difference is mediated by the different levels of ubiquity. The formal hypotheses are as follows.

Moderation of deliberation

Shortsighted decisions often result from a lack of deliberation (Hofmann et al., 2009; Milkman et al., 2008; Miller et al., 2003; Thorndike, 1966; Whiteside & Lynam, 2001). Deliberation refers to slow cognitive processes involving consciousness and consuming cognitive resources (Gigerenzer & Gaissmaier, 2011; Wilson & Schooler, 1991). It prevents ill-informed decision-making by enabling people to evaluate all alternatives, consider potential negative consequences of impulsive decisions, mentally operate action plans for goal pursuit, and inhibit habitual responses (Hofmann et al., 2009; Veling et al., 2017). We therefore propose that the effect of smartphones on shortsighted financial decision-making can be eliminated by deliberation.

Alternative accounts

One may argue it could be factors other than ubiquity that account for the difference of effects on shortsighted financial decision-making between smartphone use and laptop use. In this research, we test four alternative factors that may mediate the relationship between device type and shortsighted financial decision-making. The first alternative account is task difficulty. Melumad and colleagues (2019) have found that because of the physically constrained nature of smartphones (vs. PCs), consumers generate briefer content and focus on the overall gist of their experiences while creating contents on smartphones (vs. PCs). The small screen of a smartphone may also increase the difficulty that users have processing the information on it, which further consumes their self-control and facilitates their shortsighted decision-making. However, it is also possible that because smartphones are indispensable for contemporary people, the users have got used to their features and can efficiently process information on them. We thus test whether users will perceive different levels of task difficulty on smartphones than on other devices and whether task difficulty will further mediate our proposed effect.

Second, smartphone use has been found to be associated with an experiential thinking style because of its touchscreen interface (Huang & Wang, 2019; Ma et al., 2020; Zhu and Meyer, 2017). Experiential thinking leads to the seeking of instant gratification, such as purchasing hedonic products (e.g., chocolate cakes) that are rewarding in the short term but harmful in the long run (Metcalfe and Mischel, 1999; Peck & Childers, 2006; Peck & Wiggins, 2006; Shen et al., 2016). We thus examine experiential thinking as an alternative factor.

Third, smartphones are often used for hedonic purposes (Leung, 2021). For example, the smartphone gaming market has now accounted for almost 50% of video gaming revenue worldwide (Clement, 2021). Such hedonism may spill over and influence consumers’ decision-making and is therefore an alternative factor to be examined in the present research.

Fourth, the extent of concentration required to operate smartphones may influence users’ decision-making. The relatively small keyboards and screens of smartphones imply that users must spend more time reading and generating content via the devices (Raptis et al., 2013), thus increasing users’ concentration while completing tasks on smartphones (Han et al., 2020; Melumad & Meyer, 2020). Such high levels of concentration may lead to a state of immersion and shortsighted decision-making. Concentration is examined as the last alternative factor.

Overview of studies

Five studies were designed to test the effect of smartphones on shortsighted financial decision-making. As shortsightedness shifts people's time orientation to emphasize present pleasure and rewards (Otterbring, 2019) so that new information is considered more important than old information irrationally (Aren & Hamamci, 2021), we designed the studies to examine whether people give more weight to temporally close rewards when they consider future rewards (Studies 1 and 2 on retirement savings) and to temporally close information when they look back (Studies 3 and 4 on the evaluation of existing information). We predict that those making decisions on smartphones (vs. laptops and tablets) will be less willing to save for retirement, more likely to prioritize recent, short-term financial information while evaluating funds, and prefer instant rewards while making intertemporal decisions.

Specifically, Study 1 examined whether American participants were less likely to increase the contribution rates of 401(K) plans when reading appeals and making decisions on smartphones rather than laptops (H1). Study 2 tested whether Chinese participants were less likely to save for retirement when making decisions on smartphones rather than tablets (H1). We also tested whether the effect is mediated by the users’ perceived task difficulty or their experiential thinking. Because smartphones and tablets are both equipped with touchscreens, this study rules out possible underlying mechanisms such as direct touch effect (Shen et al., 2016) and haptic gratification (Melumad & Pham, 2020). In Studies 3 and 4, we tested whether participants tended to rely on recent information (e.g., the performance of a fund on the previous day) when processing information about funds on smartphones rather than on laptops (H1). We also examined the mediating role of ubiquity (H2) in these two studies and tested three possible alternative factors: experiential thinking (Study 3), hedonic usage of the device (Study 3), and concentration (Study 4). Finally, in Study 5, we tested whether deliberative thinking attenuated the effect of smartphone use on shortsighted financial decision-making (H3).

The current research was approved by the ethics committee of the university of the corresponding author. The participants provided their electronic informed consent to participate in each of the studies. The original data and analysis syntaxes are available at https://osf.io/kcb3j/?view_only=46d3836420cc412aaf74190072357803.

Study 1: Making decisions about the 401(K) plan on smartphones versus laptops

Nowadays, many people do not have enough savings to retire, especially those workers in the “gig economy” who are responsible for their own retirement savings (Benartzi & Thaler, 2013; Hershfield et al., 2020). People face psychological hurdles to save money for the long term, even if they are aware of the necessity to plan for their retirement (Hershfield et al., 2020). As one's shortsightedness could be manifested in how they prioritize short-term interests over long-term saving goals (Hershfield et al., 2018; Liu & Aaker, 2007), in this study we measured participants’ willingness to save for the future to indicate their shorted-sightedness.

We recruited US participants who are already involved in the 401(k) plan, a retirement savings and investing plan in which employees can decide their contribution to their accounts. Participants were invited to read an appeal from their employers that asks them to increase their contribution rate for their 401(k) plan. The lower willingness to increment the rate indicates a higher level of shortsightedness. Participants made the decisions either on their smartphones or on their laptops. We predicted that participants would be less likely to increase the contribution rate while making the decision on the smartphones (vs. laptops).

Method

We recruited 200 US participants on Amazon Mechanical Turk via TurkPrime (Litman et al., 2017). Half of them were required to use smartphones to complete the study while the other half were asked to use laptops. We also use Qualtrics to record the device type used in order to confirm that all of the participants follow the instructions.

Two hundred one participants have joined the study. They first reported their demographic information, including gender, age, nationality, race, education level (1 = primary school or below; 2 = secondary school; 3 = high school; 4 = diploma or equivalent; 5 = associate degree; 6 = bachelor degree; 7 = master degree; 8 = doctoral degree or above), and entire household income (1 = less than $15,000; 2 = $15,000 to $19,999; 3 = $20,000 to $24,999; 4 = $25,000 to $29,999; 5 = $30,000 to $34,999; 6 = $35,000 to $39,999; 7 = $40,000 to $49,999; 8 = $50,000 to $59,999; 9 = $60,000 to $69,999; 10 = $70,000 to $79,999; 11 = $80,000 to $89,999; 12 = $90,000 to $99,999; 13 = $100,000 to $149,999; 14 = $150,000 to $249,999; 15 = $250,000 to $349,999; 16 = $350,000 or more; 0 = I don’t know).

In the demographic information measure, we also embedded a question: “Have you joined the 401(k) plan? (yes, no).” One hundred twenty-two participants (72 males; Mage = 42.30, SDage = 11.43; 57 used smartphone and 65 used laptop) reported “yes” and continued this study, while the other participants who had not joined the 401(k) plan completed another unrelated task.

Participants imagined reading the following reminder from their employers on their smartphones or their laptops, depending on the type of device that participants are assigned to use: Many financial advisors recommend saving more than 10% of your income for retirement. Remember to increase your savings rate over time. The sooner you can increase your contributions, the sooner you can have your money working for you. There's a higher 401(k) employee deferral limit for 2022, and now is the time to boost contributions.

Results

We conducted an ANOVA to compare participants’ likelihood to increase their contribution rate of 401(k) plan between the smartphone and laptop conditions. The results indicate that the participants were less likely to increase the rate while making decisions on smartphones (M = 4.14, SD = 1.78) than on laptops (M = 4.95, SD = 1.64; F(1, 120) = 6.90, p = .010, ηp2 = .05). The sample of 122 participants provided 69% power (given ɑ = 0.05) to detect a f of 0.2236. These results did not change after controlling for the participants’ gender, age, income, and education levels (F(1, 116) = 7.03, p = .009, ηp2 = .06). None of the control variables significantly predicts the participants’ willingness to increase the contribution rate (ps > .368)

Discussion

Study 1 provides preliminary evidence that American people are less likely to save for retirement while making decisions on smartphones than on laptops, supporting our hypothesis that smartphones may beget shortsighted decisions. In Study 2, we aimed to replicate this finding in a different population (i.e., Chinese).

Study 2: Retirement investment on smartphones versus tablets

In Study 1, we recruited US participants who have already participated in the 401(k) plan. In Study 2, we recruited university students in China and asked them to join an imaginary task and infer their willingness to save for a retirement plan. The lower amount saved indicates a higher level of shortsightedness. In this study, the participants use either smartphones or tablets to complete the study, which rules out the account that effect observed could be due to direct touch effect (Shen et al., 2016) or haptic gratification (Melumad & Pham, 2020). We also examined another two factors—namely, perceived task difficulty and experiential thinking.

Method

Students in a major university in China were recruited to participate in a survey. Half of them were asked to use their own smartphones while the other half were asked to use the tablets provided by the research team. We planned to recruit 200 participants and finally received 203 valid responses (48 males; Mage = 21.10, SDage = 3.12).

The participants first completed an imaginary task. Specifically, they were asked to imagine that they had graduated and joined a company, with a monthly income of RMB 10,000. One day, they receive a note from the company's finance department, which invites them to contribute a portion of their income into a pension scheme that guarantees 5% annual interest that can be withdrawn when they retire. Participants then report the percentage of income they are willing to contribute, which serves as the measure of shortsightedness.

We then used four items adapted from prior research (Hsee et al., 2015) to measure experiential thinking: “When making decisions on a smartphone/tablet, I carefully analyze the costs and benefits and don’t let emotions or subjective feelings influence my decisions”; “When making decisions on a smartphone/tablet, if one option makes me feel better and the other option helps me achieve my goal, I choose the latter option”; “When making decisions on a smartphone/tablet, I rely on objective metrics of options (data, description, etc.) rather than my gut feeling”; “When making decisions on smartphone/tablet, I focus on objective facts rather than subjective feelings” (1 = completely disagree, 7 = completely agree; α = .76). We used another three items adapted from prior research (Brunken et al., 2003) to measure perceived task difficulty:, “I feel that making the above decision on the smartphone/tablet was” (1 = very low stress / very easy / very simple, 7 = very high stress / very difficult / very complicated; α = .87). Finally, we collected the participants’ demographic information.

Results

We conducted an ANOVA to compare the portion of income that participants were willing to contribute between the smartphone and the tablet conditions. The results indicate that the participants were less willing to contribute while making decisions on smartphones (M = 12.56, SD = 8.87) than on tablets (M = 16.95, SD = 14.81; F(1, 201) = 6.57, p = .011, ηp2 = .03). The sample of 203 participants provided 69% power (given ɑ = 0.05) to detect an f of 0.1732. These results did not change after controlling for the participants’ gender and age (F(1, 199) = 7.75, p = .006, ηp2 = .04). None of the control variables significantly predicted the participants’ willingness to increase the contribution rate (ps > .124). In addition, the differences in experiential thinking (F(1, 201) = 0.36, p = .548) and in perceived task difficulty (F(1, 201) = 0.29, p = .592) between the two groups was nonsignificant.

Discussion

The first two studies provide preliminary evidence that people are less likely to save for retirement while making decisions on smartphones than on laptops or tablets, supporting our hypothesis that smartphones may beget shortsighted decisions. Study 2 also ruled out task difficulty and experiential thinking as possible accounts. In the next two studies, we further tested the hypothesis in a different financial domain (i.e., evaluating funds) and examined the underlying mechanism.

Study 3: Mediating role of ubiquity and alternative accounts

Study 3 was contextualized in another crucial function of smartphones—information seeking. We tested how college students evaluate financial information while making decisions using their own smartphones or laptops. Specifically, participants were provided with the performance of five funds that had fluctuated in value over the past year, but all declined recently. The participants imagined that they held these funds and were asked to indicate the extent to which the performance of the funds on the previous day (which represents the most recent performance of the funds) influenced their decisions on whether to sell the funds. Shortsightedness is indexed by their reliance on short-term information (Aren & Hamamci, 2021; Otterbring, 2019; Sahi, 2017), and we predicted that participants who use smartphones to make their decisions would rely more on the recent performance of the funds than those who use laptops. In addition, we tested whether the effect was mediated by the attribute of ubiquity, as well as two alternative accounts, experiential thinking and hedonic usage.

Method

One hundred sixty college students (55 males; Mage = 22.04, SDage = 2.48) were recruited via a Chinese online survey platform (www.credamo.com). They were randomly assigned to either a smartphone or a laptop between-subjects condition. The materials for the study were presented in Chinese. The participants were asked to complete a survey either on their own smartphones (smartphone condition) or on their own laptops (laptop condition). The data collection platform traced the type of device that each participant used, which ensures that all participants followed the instructions and completed the survey on the designated type of device.

Participants first completed a survey. Under the disguise of collecting information on habits of device users, we measured three possible accounts, including device ubiquity, participants’ experiential thinking while using the device, and the hedonic usage of the device. Adapted from existing literature (Melumad & Pham, 2020), we used three items to measure ubiquity: “When I need to use a smartphone/laptop, I can use it immediately”; “I can use my smartphone/laptop anytime and everywhere”; and “I can use the functions of my smartphone/laptop whenever I want.” We used three other items adapted from prior research (Novak & Hoffman, 2009) to measure experiential thinking: “While making decisions on my smartphone/laptop, I often rely on instincts”; “While making decisions on my smartphone/laptop, my decisions are often informed by my feeling”; and “While making decisions on my smartphone/laptop, I trust my hunches.” We also created two items to measure hedonic usage of the device: “I use my smartphone/laptop mostly to do something that makes me happy” and “I use my smartphone/laptop mostly to deal with work” (reverse item). Participants reported the extent to which they agreed with these statements on a 7-point Likert scale (1 = completely disagree, 7 = completely agree) and we averaged the scores to create indicators for all the variables (αubiquity = .84, αthinking = .83, αhedonic = .31).

Subsequently, participants read information on five funds that had fluctuated in value over the past year but all declined recently (see Supplementary Appendix B), either on their smartphones or laptops. The interface used to present the information was adapted according to the smartphone or laptop interface. We asked the participants to imagine that they held the five funds. They then reported the importance of the performance (i.e., return rate) of each fund on the previous day for their decisions on whether to sell the funds (1 = not at all, 7 = very important). We averaged the scores for the five funds to create an index of shortsightedness (α = .91), with higher scores indicating higher shortsightedness. At the end of the study, participants provided demographic information.

Results

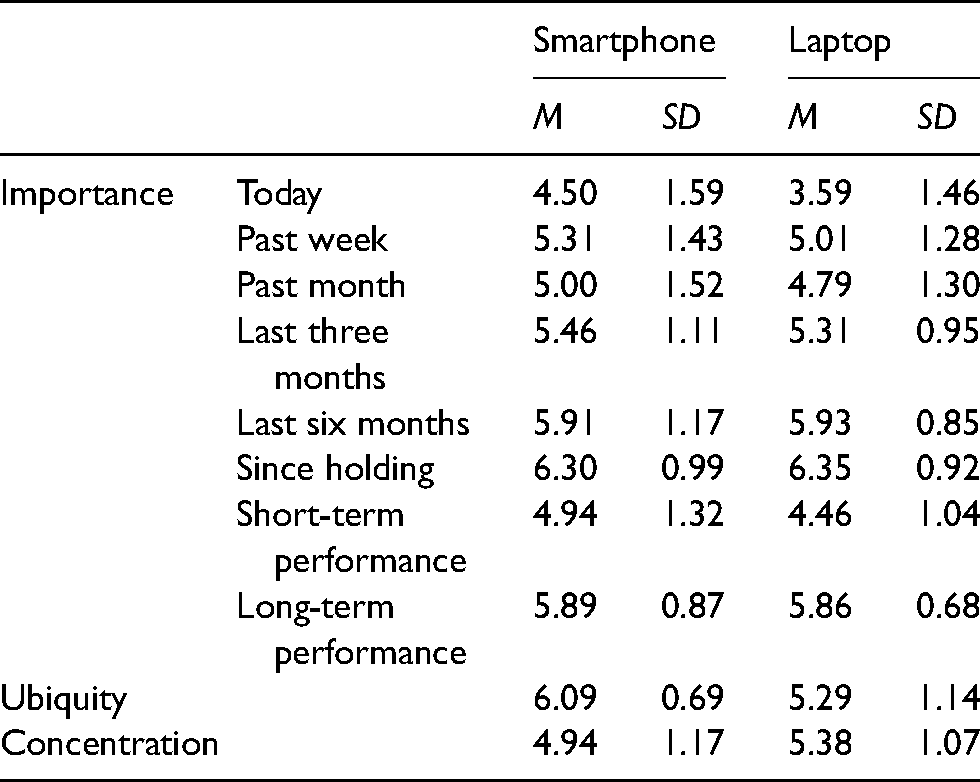

Table 1 presents the descriptive statistics. An ANOVA demonstrated that participants using smartphones considered the previous-day return rates more important (i.e., they were more shortsighted) while making decisions than those using laptops (F(1, 158) = 8.61, p = .004, ηp2 = .05). The sample of 160 participants provided 80% power (given ɑ = 0.05) to detect an f of 0.2236. In addition, participants reported higher levels of ubiquity (F(1, 158) = 13.37, p < .001, ηp2 = .08) and hedonic usage (F(1, 158) = 45.88, p < .001, ηp2 = .23) for smartphones than for laptops. The difference in experiential thinking between the two groups was nonsignificant (F(1, 158) = 2.45, p = .120).

Descriptive statistics of variables (Study 3).

We then used model 4 of PROCESS (Hayes, 2018) to test whether ubiquity, hedonic usage, and experiential thinking mediated the effect of device type on shortsighted financial decision-making. Upon inclusion of all three variables as mediators in the model, only the mediating role of ubiquity was found to be significant (see Figure 1), for which the 95% confidence interval (CI) excluded zero (95% CI of ubiquity = [0.0637, 0.3637], 95% CI of hedonic usage = [−0.3072, 0.1436], and 95% CI of experiential thinking = [−0.0206, 0.1325]). The results did not change when the three possible mediators were included in the model separately.

Results of the mediation analysis (Study 3).

Discussion

The above results reveal that smartphones are perceived to be more ubiquitous than laptops, and this attribute subsequently influences people's shortsighted financial decision-making. In addition, this effect is not mediated by users’ experiential thinking or hedonic usage of smartphones.

Study 4: Mediating role of ubiquity and concentration

Study 4 continued to examine the mediating role of ubiquity (H2) in the relationship between device type and shortsighted financial decision-making, and additionally tested an alternative mediating factor, concentration. Further, participants reported on the influence of information from a longer time span on their financial decisions. This addresses a shortcoming in Study 3, in which the importance of recent information was measured by a single item focusing on previous-day performance.

Method

One hundred sixty Chinese residents (68 males; Mage = 28.77, SDage = 5.78) were recruited from a Chinese online survey platform (www.credamo.com). They were randomly assigned to either a smartphone or laptop between-subjects condition. As in Study 2, participants were asked to complete a survey either on their own smartphones (smartphone condition) or on their own laptops (laptop condition). The materials for the study were presented in Chinese.

Participants first responded to a survey to provide information on device ubiquity and user concentration. We used the three items that were used in Study 2 to measure ubiquity (1 = completely disagree, 7 = completely agree; α = .79). We created two more items to measure users’ concentration while using the device: “While using my smartphone/laptop, I concentrate on what I am doing and do not pay attention to the surroundings” and “While using my smartphone/laptop, I am often immersed in what I am doing” (1 = completely disagree, 7 = completely agree; r = .64).

Subsequently, participants imagined holding a fund and read its information on either their smartphones or laptops (see Supplementary Appendix C). The interface on which the information was presented was adapted for smartphone and laptop screens, respectively. Participants read about the performance (i.e., the return rates) of the fund on the previous day, the previous week, the previous month, the previous three months, the previous six months, and since the fund was held. We asked participants how important each return rate was to their decisions on selling the fund (1 = not at all, 7 = very important). At the end of the study, participants provided demographic information.

Results

Table 2 presents the descriptive statistics. We used exploratory factor analysis to examine the structure of the reported importance of the six return rates, resulting in two factors. The first factor comprised the previous-day, the previous-week, and the previous-month return rates, and explained 41.08% of the variance with factor loadings ranging from .774 to .858. The second factor comprised the previous-three-months, the previous-six-months, and the since-holding return rates, and explained 25.3% of the variance with factor loadings ranging from .628 to .858. The average of the first three items was used as an indication of the importance of short-term performance (α = .78), and the average of the last three items was used as an indication of the importance of long-term performance (α = .67).

Descriptive statistics of variables (Study 4)

We then used a repeated-measures ANOVA to test the effect of device type on the importance of short- or long-term information, with device type as a between-subjects factor and the importance of short- or long-term information as a within-subjects factor. We found a significant main effect (device type: F(1, 158) = 4.18, p = .042, ηp2 = .03; information type: F(1, 158) = 136.80, p < .001, ηp2 = .46), showing that participants considered the return rates to be more important while using smartphones than while using laptops. They also considered long-term performance more important than short-term performance.

These main effects were further qualified by a significant interaction of these two variables (F(1, 158) = 4.91, p = .028, ηp2 = .03). The sample of 160 participants provided 94% power (given ɑ = 0.05) to detect an f of 0.1732. Participants considered short-term performance more important while making decisions on their smartphones than on their laptops (F(1, 158) = 6.37, p = .013, ηp2 = .04). However, the effect of device type was not observed for long-term performance (p = .813).

In addition, participants reported higher levels of ubiquity (F(1, 158) = 28.50, p < .001, ηp2 = .15) and concentration (F(1, 158) = 6.13, p = .014, ηp2 = .04) for smartphone use than for laptop use. We used model 4 of PROCESS (Hayes, 2018) to test whether ubiquity and concentration mediated the effect of device type on the importance of short-term performance. Upon including these two variables as mediators in the model, only the mediating role of ubiquity was significant (see Figure 2), for which the 95% CI excluded zero (95% CI of ubiquity = [0.0554, 0.4335], 95% CI of concentration = [−.2289, .0253]). The inclusion of these two possible mediators in the model separately did not change the results.

Results of the mediation analysis (Study 4).

Discussion

This study replicates the finding of Study 2 that people accord higher importance to short-term information while making decisions on smartphones as compared with on laptops. This effect is mediated by the level of ubiquity of the devices, rather than users’ concentration. However, no difference was observed between smartphone users’ and laptop users’ reliance on long-term information and participants generally value long-term information more than short-term information. This is presumably because, in general, long-term information considerably influences one's judgment of fund performance, such that the effect of device type is eliminated.

Study 5: Attenuating the effect by increasing deliberation

Study 5 tested whether the effect of smartphones on shortsighted financial decision-making can be attenuated if participants think deliberatively. To achieve this, we required participants to pause for a certain duration while making their decisions. This method has been evidenced to be effective in terms of evoking deliberative thinking (Dijksterhuis, 2004; Dijksterhuis et al., 2006; Fazio, 1990; Friese et al., 2006; Veling et al., 2017). In contrast, time pressure often leads to unconscious and impulsive decisions (Chen et al., 2008). We predicted that prolonging the duration for deciding would decrease the effect of device type on shortsighted financial decision-making.

Informed by extant literature (Yao et al., 2017), we used intertemporal financial decision-making to measure impulsivity. Participants were asked whether they preferred receiving a payment immediately or later with extra compensation. Choosing immediate payment is an indicator of shortsightedness.

Method

One hundred sixty-one college students (26 males; Mage = 20.50, SDage = 2.52) at a major university in mainland China were recruited. Each participant was assigned to one condition in a 2 (device type: smartphone vs. laptop) × 2 (deliberation condition: deliberation vs. control) between-subjects design.

Participants completed the study in independent laboratory cubicles. They first completed an unrelated paper-and-pencil survey. Subsequently, they used either their own smartphones (smartphone condition) or laptops provided by the researcher (laptop condition) to provide demographic information. At the end of the survey, participants were informed that they would receive a payment of RMB 20 (approximately USD 3.11) for participating in the study, but that the researcher did not have enough cash and would like to invite some participants to volunteer to receive a delayed payment. They were told that the delayed payment would be provided in two weeks and the amount would be increased to RMB 23 (approximately USD 3.56).

Participants were then asked to indicate their preferences regarding these two payment options on a seven-point Likert scale (1 = prefer receiving 20 RMB immediately, 7 = prefer receiving 23 RMB two weeks later). In the deliberation condition, participants were asked to think carefully about the two options and were required to wait for at least 40 secs. to submit their responses. Such limitations were not imposed on the participants in the control condition. We reversed the responses so that higher scores indicate a stronger preference for receiving the payment immediately. All participants received RMB 20 at the end of the study.

Results

An ANOVA with device type and time condition as the independent variables and payment preference as the dependent variable revealed a significant interaction (F(1, 157) = 4.79, p = .030, ηp2 = .03). The sample of 161 participants provided 59% power (given ɑ = 0.05) to detect an f of 0.1732.

In the control condition, participants making decisions on smartphones (M = 5.10, SD = 2.11) were more likely to prefer receiving the payment immediately than those making decisions on laptops (M = 3.76, SD = 2.22; F(1, 157) = 7.98, p = .005, ηp2 = .05). This replicates our previous findings. In contrast, such a difference was not observed in the deliberation condition (Msmartphone = 3.77, SDsmartphone = 2.40 vs. Mlaptop = 3.90, SDlaptop = 1.80; F(1, 157) = 0.08, p = .781). Put in another way, deliberation decreased shortsighted financial decision-making in the smartphone condition (F(1, 157) = 7.63, p = .006, ηp2 = .05) and did not impact shortsighted financial decision-making in the laptop condition (F(1, 157) = 0.10, p = .757).

Discussion

These findings demonstrate that deliberative thinking attenuates the effect of smartphone use on shortsighted financial decision-making.

General discussion

Smartphones are more ubiquitous than other devices and are more likely to induce shortsighted financial decision-making among users. This effect can, however, be attenuated if users are prompted to think deliberatively. Five studies, including online and laboratory studies in the USA and China based on a variety of financial decision-making scenarios, provide converging evidence that supports our hypotheses. Study 1 shows that US citizens are less likely to increase contribution to their 401(k) plan when they make decisions using smartphones rather than laptops. Study 2 shows that Chinese university students are less willing to save for retirement when they make decisions using smartphones rather than tablets. Studies 3 and 4 demonstrate that while evaluating funds, people using smartphones (vs. laptops) are more likely to be influenced by recent information (e.g., the performance of a fund in the previous day or week). This effect is mediated by the high level of perceived ubiquity of smartphones as compared to other devices. In Study 5, by having users think deliberatively, the effect of device type on shortsighted financial decisions was successfully attenuated. In Studies 2 to 4, we also ruled out alternative factors such as perceived task difficulty, experiential thinking, hedonic usage, and concentration.

Theoretical and practical implications

Our findings yield theoretical contributions. First, we add to the scholarship of mobile devices and impulsivity by revealing that (1) device type matters, and that (2) impulsivity could be manifested in the domain of financial decision-making. The relationship of smartphone usage and shortsighted financial decision-making is explained by the perceived high level of ubiquity associated with smartphones. In other words, the underlying mechanism is psychological rather than behavioral, which is a departure from extant literature that discusses impulsivity from the lens of a preexisting disorder (e.g., Reed et al., 2015; Pérez de Albéniz Garrote et al., 2021). In addition, while extant literature has often accounted for the effect of smartphones by user–device relationship (e.g., Ward et al., 2017), the mechanism of ubiquity revealed in the present study shows that such an effect could be a byproduct of contemporary digital culture—the effect is derived from the collective, long-term pursuit of optimizing users’ experiences, which has generally been considered an ideal business goal to achieve (Bush, 2020; Jiang et al., 2013).

It is worth noting that, although factors including task difficulty, thinking style, hedonic usage, and concentration are ruled out as the underlying mechanisms, the participants’ levels of concentration and hedonic usage did vary between the smartphone and the laptop conditions. This may be due to (1) the rather utilitarian nature of financial decision-making, and (2) the characteristics of impulsive decision-making. To elaborate, the influence of hedonic usage of smartphones has been observed mainly when consumers choose between hedonic products and utilitarian products (Benartzi, 2016; Shen et al., 2016), but making financial decisions, especially the processing of financial information required in Studies 3 and 4, is arguably a utilitarian task that has little hedonic implication. Therefore, although the participants reported a higher (lower) level of hedonic usage for smartphones (laptops), this factor does not necessarily mediate the effect of smartphone usage on financial decision-making. Besides, although the participants tend to report a higher level of concentration while using smartphones (vs. laptops), this does not necessarily influence their shortsighted decision-making because shortsightedness manifests in prioritizing short-term interests, which is not directly predicted by concentration that mainly reflects the cognitive resources involved (Melumad & Meyer, 2020).

Second, previous exploratory studies (e.g., Suh & Hargittai, 2015) have compared mobile devices with non-mobile devices (laptop vs. desktop computers) and discussed how each shapes our behavior in unique ways. For example, the former poses more risks for privacy management because users tend to accidentally share posts to the public while using mobile devices. Our findings, however, reveal that effects may vary even within the category of mobile devices (smartphones vs. laptops; smartphones vs. tablets). This yields important practical implications as users may not always be aware of the varied nature across mobile devices, especially when the apps are often synced across mobile devices. Consumers should be informed that even if they are using the same apps, switching to devices other than smartphones may decrease the likelihood of shortsighted decision-making.

Our findings also yield three important practical implications for the development of interventions to facilitate rational financial decisions.

First, different devices may require different regulations even if they seem to share the same contents. For example, informed by our research, findings that deliberation successfully decreases the likelihood of shortsighted decision-making, certain users, especially those who are mentally vulnerable (Bush, 2020), may benefit from some “speed bumps” such as warning messages while performing transactions online. However, as retailers may be reluctant to address such requirements, authorities may stipulate that certain elements of friction be added to the smartphone versions of, for example, banking apps.

In addition, on-site promotional events that invite customers to user their personal devices—likely to be smartphones—to complete particular tasks should be regulated. For example, in the process of checking out, customers are often invited to download the retailer's app or to sign up for memberships online in order to receive rewards or discounts. This may lead to shortsighted financial decision-making, such as focusing on immediate perks at the expense of overlooking the terms and conditions statement and hidden costs. Where possible, consumes should be prompted to review legal documents on their laptops or be informed of the potential effect of making decisions on smartphones.

Finally, our research informs the communication of public policy in the trend where financial planning is no longer centralized by a “big government” in order to ease the burden on national pension funds. For example, in the recent reform of retirement pension management in China that encourages private retirement savings (i.e., the launch of the Chinese 401 (K)), eligible citizens should be encouraged to use laptops or tablets to access information and be prompted to deliberate before making decisions. While Study 2 of the present research revolves around the retirement scheme in China, the findings could be extrapolated to societies where citizens are less familiar with privatized financial systems and individuals learn to make decisions for their own insurance, pension, and investment.

Limitations and future research

Despite its theoretical and managerial implications, this research has several limitations that warrant the attention of future research.

First, while the effect of smartphones on shortsighted financial decision-making is driven by its affordance or ubiquity, one may argue that such effects may be challenged when smartphones are perceived to be less ubiquitous. For instance, among those who cannot use smartphones freely (e.g., soldiers and schoolchildren), or during a particular period when users may refrain from using smartphones (e.g., exam week for students), the effect we found might be attenuated. This also implies that devices other than smartphones may yield similar effects if they are perceived to have high-level ubiquity. For example, teenagers who own a tablet but not a smartphone may use the tablet ubiquitously and an effect on shortsighted decision-making could be observed even if there is no smartphone involved. Future research may examine the effect in these relatively unconventional scenarios to further illuminate the underlying mechanism.

Second, future research may examine whether the effect of device type on financial decision-making could be moderated by users’ financial literacy, or whether the findings may be extended to other domains, especially those related to prosocial behaviors. For example, after ordering food, customers are often encouraged to round up their bills at retailers such as McDonald's, where the extra payment goes to charities (Kelting et al., 2019). It may be worth investigating whether using smartphones rather than, for example, self-service kiosks increases the likelihood of such donations.

Finally, it is unclear whether there is a defining characteristic associated with the perceived high level of ubiquity of smartphones, especially when the line among mobile devices becomes blurred. For example, smartphones are now embedded with apps to help users to limit their screen time, rendering a lower level of ubiquity. Future studies may examine the positioning and consumers’ relations with multiple devices in further depth, to illuminate factors that define particular devices and account for ensuing user behaviors.

Supplemental Material

sj-docx-1-pac-10.1177_18344909221147782 - Supplemental material for Smartphone use increases the likelihood of making short-sighted financial decisions

Supplemental material, sj-docx-1-pac-10.1177_18344909221147782 for Smartphone use increases the likelihood of making short-sighted financial decisions by Tianran Wang, Wei-Fen Chen, Xue Wang and Xiucheng Fan in Journal of Pacific Rim Psychology

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Fundamental Research Funds for the Central Universities (grant no. 310422147) and the Fundamental Research Funds for the Central Universities, National Natural Science Foundation of China (grant no. 71832002).

Supplemental material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.