Abstract

Traditional regulatory models of natural monopoly network utilities are designed to incentivise cost-efficiency, subject to the firm achieving a certain level of reliability. With the rise of decarbonisation as a key policy goal, facilitating innovation in electricity networks has become of vital importance. Innovation and cost-efficiency may overlap and exhibit the same risk profile. However, we show that when there is a difference in their risk profile, incentivising these two tasks using the same incentive scheme is ineffective. This means incentive regulations need to be enhanced with additional modules that take into account the level of risk to which companies are exposed to for their stage of innovation activity. We also demonstrate that the issue of risk can distort the outcome of a competitive scheme for allocating innovation funds when bidders are heterogeneous in their risk attitude and there is uncertainty about recovering initial investments needed to prepare the project proposal. Thus, competitive schemes need to be designed such that they factor in risk attitude heterogeneity among bidders.

Keywords

Introduction

The power grid needs to adapt to its changing operating environment during energy transition. The electrification of the heat and transport sectors, which are currently being pursued as a default strategy by many European countries, has serious implications for grid infrastructure. Without intervention, the combined electrification of heat and transport can cause the peak electricity demand of a developed economy to grow as much as 1 GW per year post 2030 (Energy Networks Association [ENA], 2017). This means electricity networks require more innovation to enable agility, control, automation and new operating and business models, both at the transmission and distribution network levels. The problem is even more critical at low voltages, because this is a place where most disruptive technologies are located and this area has traditionally been managed in a passive manner.

Innovation can be defined as a process through which new methods are created or alternative methods are adopted, with the aim of providing improved outcomes (The UK Regulators Network, 2015). In the context of infrastructure service businesses (such as electricity, gas and telecommunication networks), this can be expanded into technical innovations, process innovations and commercial innovations. Technical innovation occurs when existing technologies are improved or new technologies are introduced, so that goods and services can be delivered more efficiently and/or reliably. Process innovation relates to improvements in management and the operations of organisations in order to lower costs. Commercial innovation is the introduction of new business models to offer services that otherwise would not have been commercially feasible.

These all mean that the grid requires improving not only in technological aspects but also in organisational and business models dimensions. In recent years, efforts at the level of grid have largely been focused on dealing with issues such as renewable intermittency, congestion, load shifting and bidirectional flow in distribution networks. In the future, technological innovation at the grid edge will facilitate the development of markets for distributed resources, service-oriented business models and active distribution grid management (IRENA, 2019). Therefore, the role of the grid is evolving beyond just supplying electricity to consumers (Poudineh et al., 2015). There are multiple pathways here but one scenario envisions the electricity network as a platform that also maximises the value of grid edge technologies such as distributed generation, storage, energy efficiency, demand response and electric vehicles (EVs) (Küfeoğlu et al., 2018). A new paradigm (including a technical, regulatory and business model) is required at grid level to integrate disruptive technologies, find new ways of operating to meet customers’ expectations and facilitate grid edge transformation.

Innovation in the electricity industry has generally been sluggish, but it is even more so when it comes to the network segment. This is because the capital intensive network infrastructures exhibit natural monopoly characteristics that result from high economies of scale relative to market size (Joskow, 1996). Due to the absence of direct competition in these regulated industries, infrastructure providers rarely undertake the appropriate level of innovation activities to optimise their operation and improve the continuity and quality of their services. Therefore, innovation needs to be incentivised through economic regulation.

Traditionally, the regulatory regimes of network companies have been designed to incentivise cost reduction in the business-as-usual activities of firms (including provision of quality of service), and innovation was largely dealt with implicitly as part of cost reduction. An important difference between innovation and the business-as-usual activities of a network company is that innovation is not only costly but also risky as it does not always produce successful outcomes. The justification for incorporating innovations, despite these being risky activities, is that learning can be obtained both from successful and unsuccessful outcomes; it is thus rewarding in the long term despite being costly in the short run. However, regulatory models of network companies in many places are still efficiency-oriented rather than innovation-oriented. A recent report which analyses the regulatory models of distribution network companies in 20 European Union member states shows that in 2016 only seven countries had provided explicit incentives for innovation (Eurelectric, 2016).

This article addresses the issue of innovation in regulated electricity networks by asking the following key question: How to incentivise innovation, as a risky activity, in network utilities? We first analyse how regulated networks will behave when innovation and cost-efficiency are incentivised using the same incentive scheme. For this, we adopt the multitask moral hazard model proposed in Holmstrom and Milgrom (1991). We then evaluate the effect of risk attitude on the outcome of a competitive scheme for allocation of innovation fund using contest game introduced by Tullock (1980).

We demonstrate that incentive mechanisms that do not take into account the risk profile of innovation activities divert the attention of the network utilities from innovation to normal efficiency gain. This suggests that incentive regulation does not necessarily promote innovation, if the risk to which companies are exposed is not considered. We also show that a heterogeneous risk attitude among bidders can distort the outcome of a competitive allocation of innovation funds. We prove that a firm with a greater level of risk tolerance but a less valuable project can win a contest for innovation funds in competition with a risk-averse firm which has a more valuable innovation project. This means that the existence of competition alone cannot guarantee that an innovation fund will be allocated to the project with the highest value. At the end of the article, we suggest some alternative approaches to address issues mentioned above when dealing with innovation in regulated network companies.

The outline of this article is as follows. The next section provides a brief discussion of the need for technological, organisational and business model innovations in the grid segment of electricity supply industry. The third section analyses the issue of incentivising innovation through regulation using insights from economic theory. The fourth section discusses main options available to the regulator to encourage innovation, given the trade-off between risk exposure and insurance provision in tasks with uncertain outcomes. The fifth section provides concluding remarks.

Power grids and the need for innovation

The operating environment of electricity networks was largely unchanged during the 20th century, until the beginning of the new century when the importance of environmental policies rose in the agenda of policymakers around the world. As a result, the decarbonisation of the power sector became the focal point of environmental policies as it paves the way for further decarbonisation of the economy through electrification of heat and transport.

Electrification of the heat sector requires the use of highly efficient heat pumps. While these will impact the entire electricity network, their effect on the high-voltage transmission network will be much lower than on the low-voltage distribution grid, because its ability to alleviate their impact is much more limited. In the United Kingdom, for example, heat demand in the winter is around five times higher than electricity demand 1 ; this means a significant surge in the electricity demand and the consequent straining of national and local electricity grids, should electrification of the heat sector go forward (Love et al., 2017). Overall, four potential issues, at the national and local levels, can occur as a result of the mass deployment of heat pumps. The national-level issues, which exacerbate the need for capacity and flexibility in the system, are an increase in the peak demand and an increase in the ramp rate. At the local level, challenges are voltage drop beyond the statutory limits and insufficient thermal capacity of the low-voltage feeders and transformers.

Therefore, unless electricity networks are reinforced (both at transmission and distribution levels) electrification of the heat sector can be hampered by the inadequacy of existing infrastructures.

Electrification of the transport sector presents a slightly different problem. Through smart charging, part of the EV fleet can be accommodated in the existing network without any considerable reinforcement. For example, a recent study of the Spanish electricity system shows that off-peak charging can facilitate the roll-out of a large number of EVs – enough to represent a quarter of the current total car fleet in the country (Colmenar-Santos et al., 2017). Furthermore, EVs can be suppliers of various services to the grid through the vehicle-to-grid concept. Nonetheless, a full penetration of EVs in the electricity system would not be possible without a significant reinforcement of existing infrastructures.

Beyond decarbonisation, decentralisation is another major trend that changes the operating environment of the grid. Technological progress in the generation and demand-end sectors from the growth of intermittent and/or distributed energy resources to digitalisation and rise of new business models challenges the way which the centralised power grid is operated and regulated (Tuttle et al., 2016). In the future, networks are expected to be used in fundamentally different ways than the current model as a passive conduit. The overall theme is one of more intelligent network components throughout the power network, permitting more accurate, possibly automated, control operations under various conditions. For both transmission and distribution networks in the future, real-time wide-area situational awareness of grid status through advanced metering and monitoring systems is the trend. However, the increased amount of data created by smart grid devices and the increasingly complex models in which they are used can overwhelm the utilities if the underpinning data management ability and computing power have not been scaled up accordingly (Daki et al., 2017). Increasing incorporation of Big Data technologies and high-performance computing into the electricity network of the future is therefore expected.

In addition to technology, the relevant organisational and business models are also improving. At the level of distribution networks, where most of these changes are happening, the core areas of operation have traditionally been investment in, and operation of, the network – maintaining the security of the system and technical data and, finally, loss management. With the integration of distributed energy resources and the need for more active management of grid operations, the role of distribution companies started to evolve from that of a distribution network operator to one of distribution system operator (DSO) (Poudineh & Jamasb, 2014). The difference between the two is that, under the DSO model, the distribution company assumes a role similar to that of the transmission system operator (TSO), but at a local level. Therefore, a DSO not only manages voltage and reactive power but also balances the distribution network to manage congestion in real time, using distributed resources, in coordination with the TSO (IRENA, 2019).

There are many pathways that electricity networks could take as their role in the power system evolves (ENA, 2017). For example, they can move towards further implementation of smart solutions to improve their efficiency or undergo more fundamental changes and become a neutral market facilitator with some system operator capability. In recent years, there has been a growing interest in the notion of the distribution system platform (DSP) as a future model for electricity distribution networks (Energy Institute, 2017). The aim of a DSP is to integrate new and innovative energy resources and allow them to compete with traditional centralised sources of energy on a level playing field. The shift in business model from network operator to platform provider may create possible alternatives to the need for building more physical network infrastructure.

In summary, these developments and advancements herald a change in the operation of electricity networks and highlight the importance of innovation, not only in technological dimensions but also in the business model and organisational aspects of power grid companies.

Economic incentive for grid innovation

Incentive regulation (such as price cap and revenue cap) was originally designed with the aim of improving the efficiency of natural monopoly infrastructures. The issue of innovation was often not dealt with explicitly in regulation, as it was assumed that the incentive for cost reduction also promotes innovation if such activities lead to long-term efficiency improvement (Jamasb & Pollitt, 2007). Therefore, the standard regulatory model of network companies incentivises only cost reduction or static efficiency gain, subject to firms meeting certain levels of reliability or quality of service (Giannakis et al., 2005). This is usually done through sharing with the firm a percentage of its cost reductions during the regulatory period. However, the risk profile of innovation efforts might be different from that of the normal activities of firms. This means that the conventional efficiency-oriented model of grid regulation is inadequate to stimulate innovation when there is a difference in the risk profile of these two activities. In this section, we first show the reason why a focus on cost reduction does not necessarily deliver innovation. We also examine the effects of risk in the context of competitive schemes for innovation funds. Finally, we review the regulatory options for explicitly dealing with innovation in the regulatory model of network companies.

The model adopted in this article is based on the standard contract theory and game theory. It is inspired by similar problems which have been investigated in the literature. For example, the moral hazard in individual contracts (Bolton & Dewatripont, 2005), the cooperation models through side contracts between agents in a principal–agent setting (Holmström & Milgrom, 1990; Itoh, 1993; Tirole, 1986), inducing competition in a monopoly environment (Bresnahan, 1997), risk and technology heterogeneities in contest games (Cornes & Hartley, 2003) and designing incentives to make agents more innovative (Manso, 2011). Our contribution here is the application of the existing economic theory to investigate incentive design for risky activities in the context of regulated electricity network companies. In the individual incentive contract, regulator incentivises regulated network utility to undertake risky and costly innovation activity as well as cost-reducing efforts. The contract is designed to address the problem of moral hazard when the firm is incentivised to undertake two tasks under the same incentive mechanism. The competition model is a rent-seeking contest game in which companies compete for innovation fund by submitting proposal for innovation projects to the regulator.

Incentive for innovation versus incentive for cost-efficiency: One regulation two tasks

Implementation of incentive regulation per se does not necessarily incentivise network companies to undertake innovation, especially when the objective of innovation is beyond cost-efficiency. This is even true when the objective of innovation is cost-efficiency but the way of achieving it is through implementation of less certain technologies and processes. We distinguish between innovation and normal efficiency gain based on the level of risks involved in these two activities: normal efficiency gain is assumed to be less risky than innovation efforts.

In order to investigate this, let’s consider the incentive regulation model in equation (1)

where z represents the allowed compensation of the firm for its innovation and efficiency gain efforts;

A firm can exert effort to reduce its costs as part of its normal operation, but cost reduction is not guaranteed. Therefore, we assume that the amount of cost reduction (x

1) is a function of effort of the firm (e

1) and a risk parameter (

The size of variance (

At the same time, the regulator aims to incentivise innovation as part of the regulatory model by allowing the firm to claim a share (

Similar to the previous case, there is uncertainty in the outcome of innovation activities, so we assume that innovation gain (x

2) is a function of the firm’s effort (e

2) and a risk parameter (

When innovation is motivated within the existing regulatory model of network companies, incentive regulation is supposed to fulfil an additional purpose – in other words, in addition to the normal cost reduction, the regulatory regime needs to incentivise the firm to carry out costlier and perhaps riskier innovation activities. This means that the optimum regulatory scheme in this case should not only allocate the risk and compensate the firm for its effort but also allocate attention between two tasks.

In order to analyse the behaviour of the firm under the regulatory regime presented in equation (1), we employ the multi-task moral hazard model proposed in Holmstrom and Milgrom (1991). Under this setting, the regulated firm chooses the vector of effort

The firm experiences the cost of

We assume the shape of the firm’s cost function (

The variance matrix in equation (4) allows for the possibility that the risk of two activities (innovation and efficiency) can be correlated. Likewise, the cost function in equation (5) allows for the possibility of shared technological features between efficiency and innovation activities. Apart from the fact that these assumptions can be reasonable, given that the two activities are conducted within the same firm with the same resources, and have similar purposes, being able to make general assumptions allow for general solutions which cover a wide range of possibilities.

In terms of the solution, the main aim is to understand the following:

What is the optimal level of

How do the optimal values for

How does the effort of a firm undertaking two tasks change with increased risk of innovation activity?

The regulator (namely the principal) is assumed to be risk neutral and obtain the gain (on behalf of consumers) equal to

Solving equation (1) on the basis of the aforementioned assumptions leads to an expression for the optimal share of firms from efficiency gain and innovation, as presented in equation (6), and to another for the optimal level of effort as in equation (7) (please see Appendix for the details)

Equations (6) and (7) reveal some interesting features on the structure of an optimal compensation plan for innovation and efficiency gain when they are treated similarly despite having different risk profiles. In order to understand what the implications of incentivising innovation under the regulatory model in equation (1) are, we carry out some simple simulation analysis.

Simulation of results

Subsequently we provide some simple simulated results under various scenarios with respect to cost structure and the uncertainty of outcome of two tasks. It is important to note that we do not give a technical interpretation to the numbers in the graphs presented in the following rather we want to show what happens to optimum incentive structure and effort, when innovation is more uncertain compared with the normal efficiency gain of the regulated firm. Therefore, it is the shape of graph (increase or decrease in the value of incentive coefficients and efforts) which of interest not the actual numbers which are arbitrary.

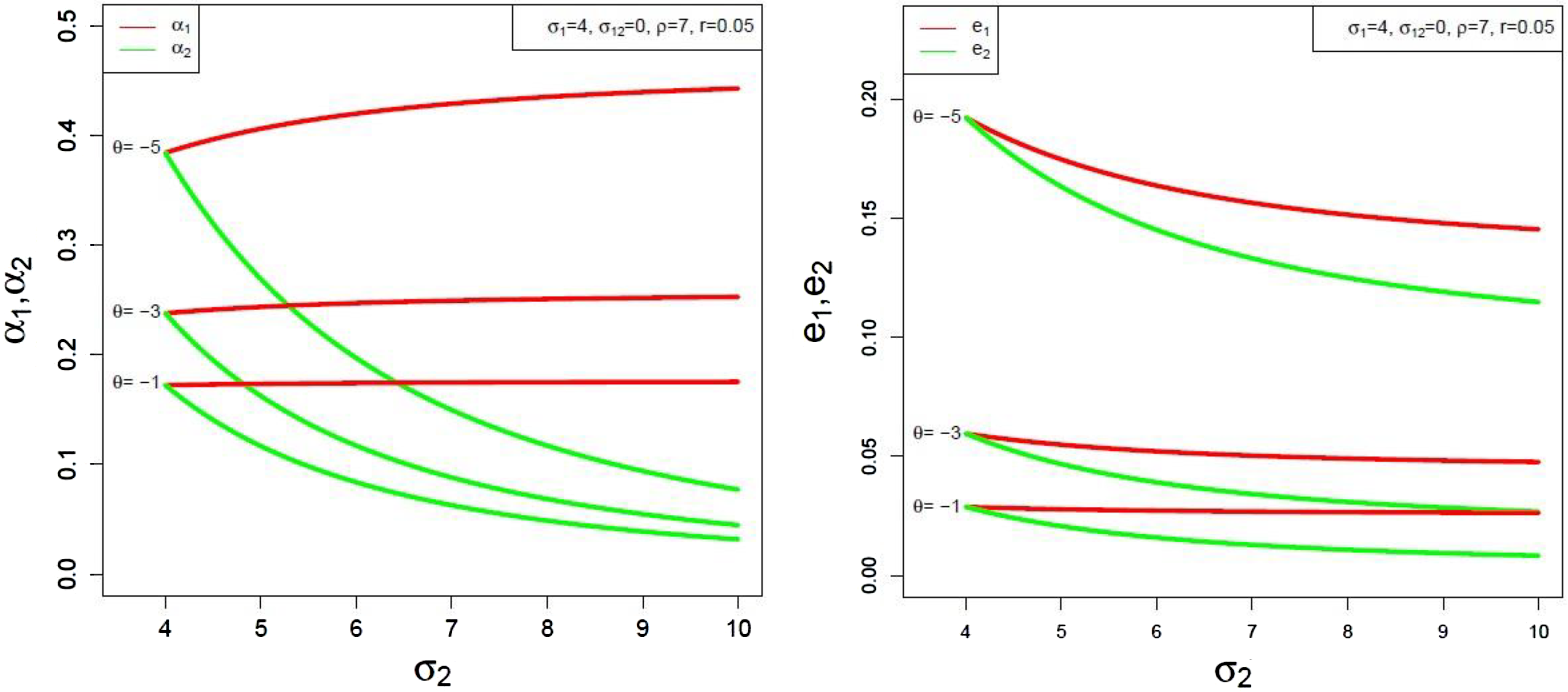

(i) In the first case, we assume that the risk profiles of the two tasks are independent (

The effect of increase in uncertainties of innovation on the optimal share of firm and its effort (when there is synergy between tasks).

As can be seen from Figure 1, when there is synergy between tasks, the increase in uncertainty of innovation has a slight increasing effect on the optimal share of the firm from its conventional efficiency gain (meaning that the compensation for efficiency needs to be based more on outcome) but a visible decreasing effect on that of innovation gain (meaning that compensation for innovation needs to reduce its reliance on outcome). This means that although the optimal shares of the two tasks start as being of similar magnitudes (when the risks are similar), they move in opposite directions as the risks of innovation increase. The effect is more visible at higher levels of synergies between two tasks.

Unlike the optimal shares of two tasks which move in opposite directions under this scenario, the level of effort for both activities reduces with the increase in uncertainties in the outcome of innovation effort. This suggests that when there is synergy between two incentivised tasks (innovation and efficiency), the risks associated with innovation negatively affect the effort not only of innovation but also of conventional efficiency gain. This is an indication of the distortionary effect of performance-based schemes for innovation under assumptions made about costs synergy and risk in this scenario. To ensure that our results are independent of the value chosen for θ, we have plotted the graphs for three values of θ. This is also the case in the subsequent cases.

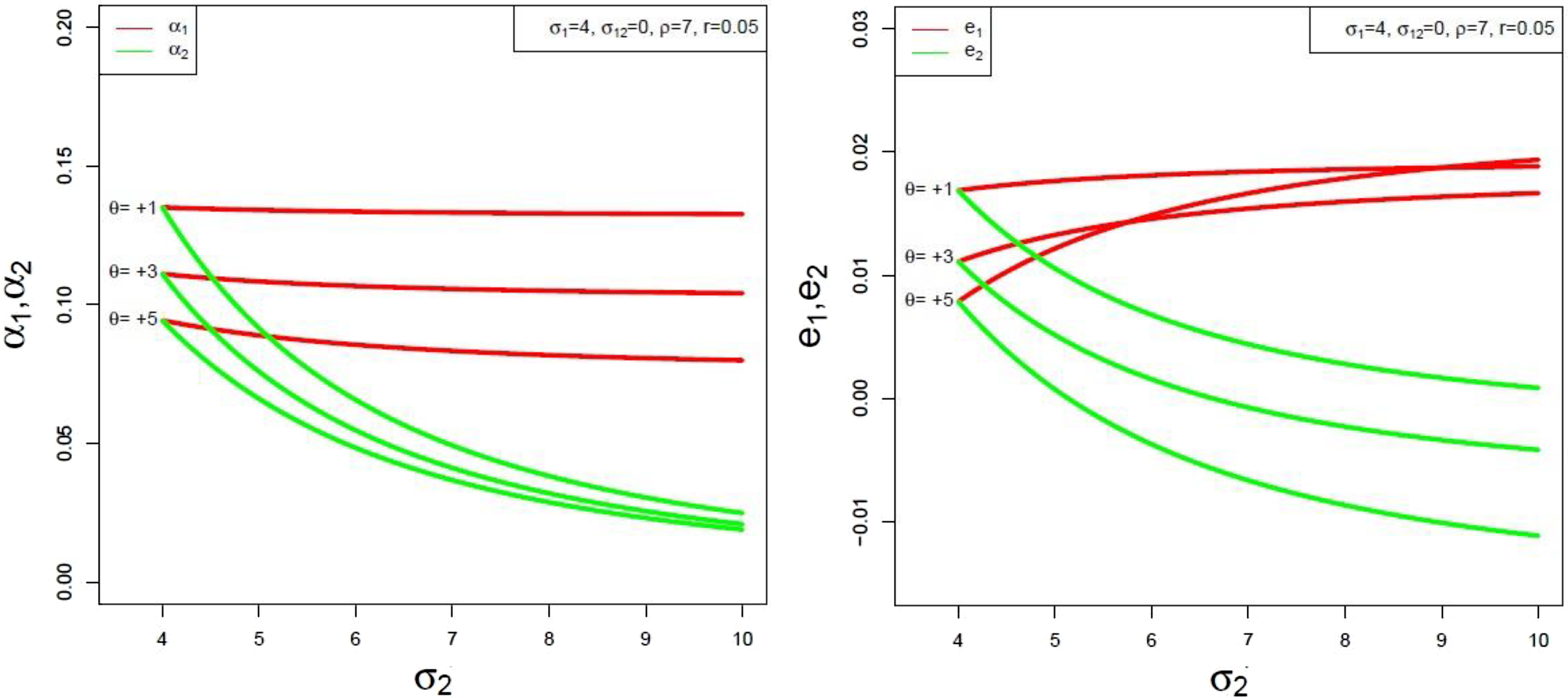

(ii) In the second case (similar to the first case) we assume that the risks of two tasks are independent (

The effect of increase in uncertainties of innovation on the optimal share of firm and its effort (when there is no synergy between tasks).

As can be seen from Figure 2, 2 an increase in uncertainty of innovation outcome leads to a reduction in optimal share of the firm from the outcomes for both efficiency gain and innovation achievement (this means that the regulator needs to reduce the reliance of compensation on outcome for both tasks). However, the optimal effort for the two tasks goes in opposite directions, and the two tasks will become substitutes. In other words, as the innovation becomes riskier, the firm diverts its attention from innovation to conventional efficiency gain activities. Thus, innovation effort will approach zero when it becomes sufficiently risky (the firm will only engage in normal cost-efficiency activities).

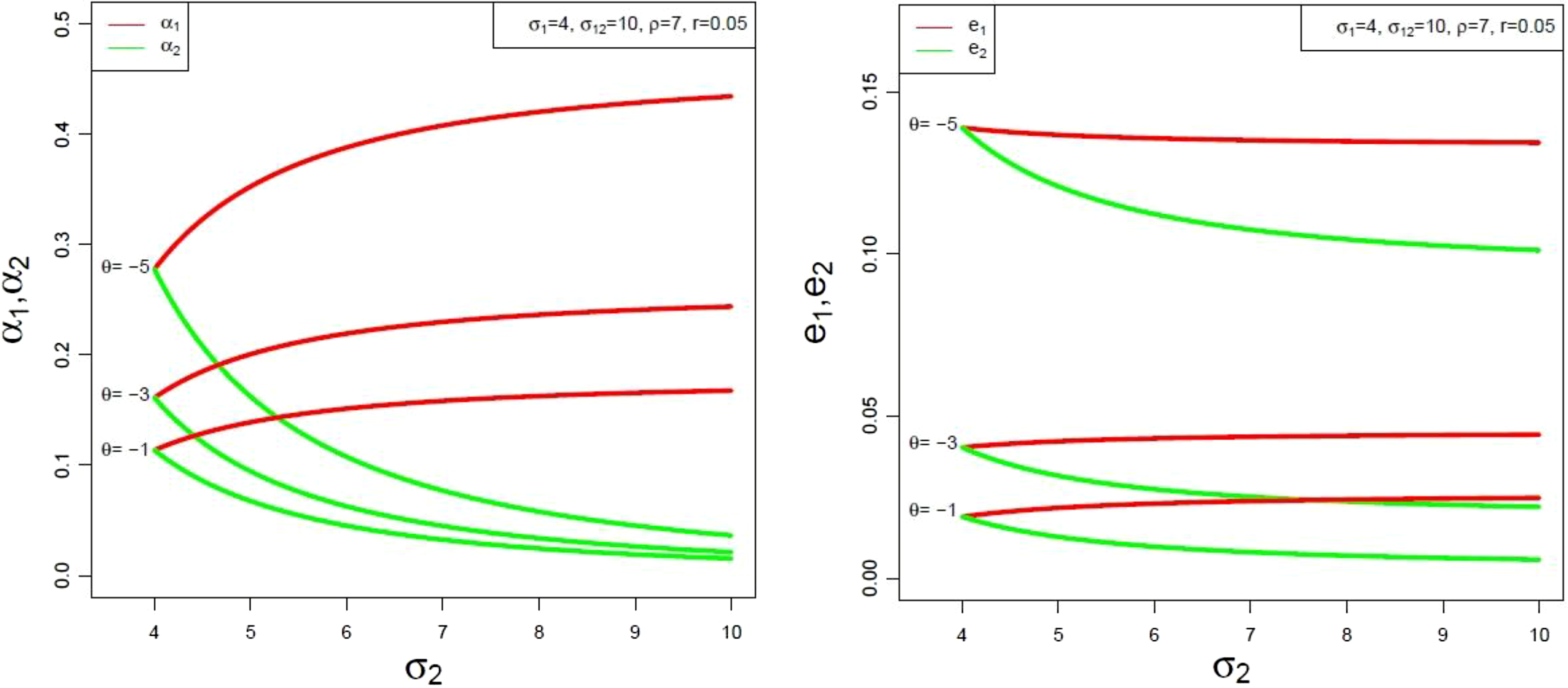

(iii) In the third case, we assume that uncertainties relating to the outcome of the two tasks are correlated (

The effect of increase in uncertainties of innovation on the optimal share of firm and its effort (when there is synergy between tasks).

As depicted in Figure 3, when there is synergy between the two activities and the risks associated with them are correlated, an increase in the risk of innovation activities reduces the optimal share of firm from innovation gain but increases it for efficiency gain (put another way, at higher levels of uncertainty, innovation incentive needs to be decoupled from outcome, whereas efficiency incentive needs to be more performance based). With regard to the effort of firm, higher innovation uncertainty leads to a reduction in the attention of the firm to innovation (attention to efficiency gain remains almost constant except in high levels of synergy that it may decline slightly). In this case, the regulatory model needs to increase the reliance of the compensation scheme on performance for efficiency gain and reduce it for innovation activity (i.e. innovation to be compensated mainly through a fixed sum).

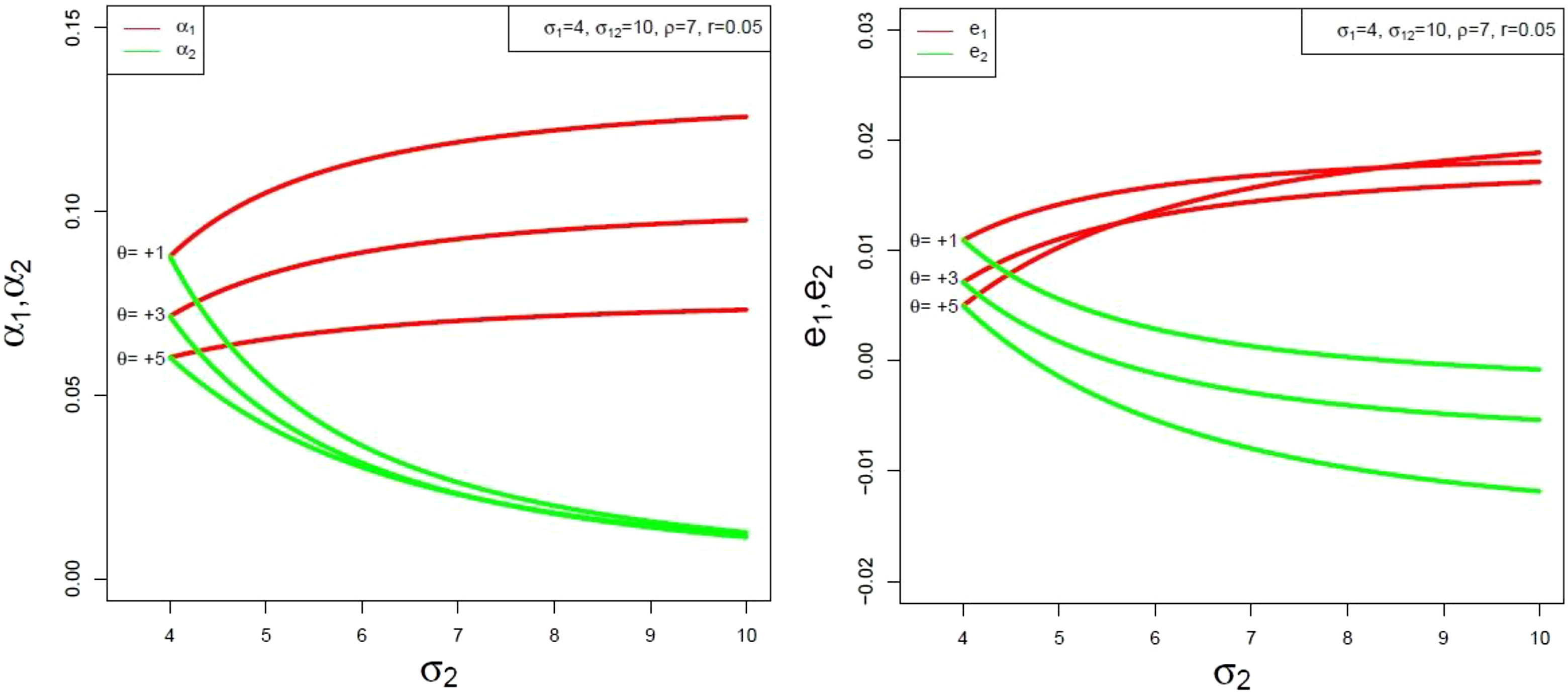

(iv) The fourth scenario assumes that the risks related to the two tasks are correlated (

The effect of increase in uncertainties of innovation on the optimal share of firm and its effort (when there is no synergy between tasks).

In case four, as shown in Figure 4, when the risks of the two activities are correlated but there is no synergy in their cost structure, an increase in the risk of innovation diverts the attention of the firm from innovation to normal efficiency gain (i.e. the effort on efficiency gain increases, whereas the effort on innovation decreases). The figure also shows that the optimum regulatory model in this case entails reducing the sensitivity of compensation for innovation to performance. Conversely, efficiency needs to be more performance based.

The four cases examined here cover almost all possible risk and technology relationships associated with cost-efficiency and innovation activities. In all cases, as σ 2 increases, it will become costly to induce the risk-averse utility to deliver the same level of effort thus the firm effort declines. With respect to α 2, also there is a similar story. It is affected through three channels. First, it decreases in risk aversion of the firm. Second, it decreases in how fast costs rise with effort as fast-rising costs will cause the agent to respond less to incentives, and hence, it is optimal to reduce them. Third, it decreases in noisiness of the link between output and effort (σ), because with a noisy process, sensitivity adds too much risk to the agent. Thus, when σ 2 increases, inducing even small level of effort requires a higher degree of insurance to the firm.

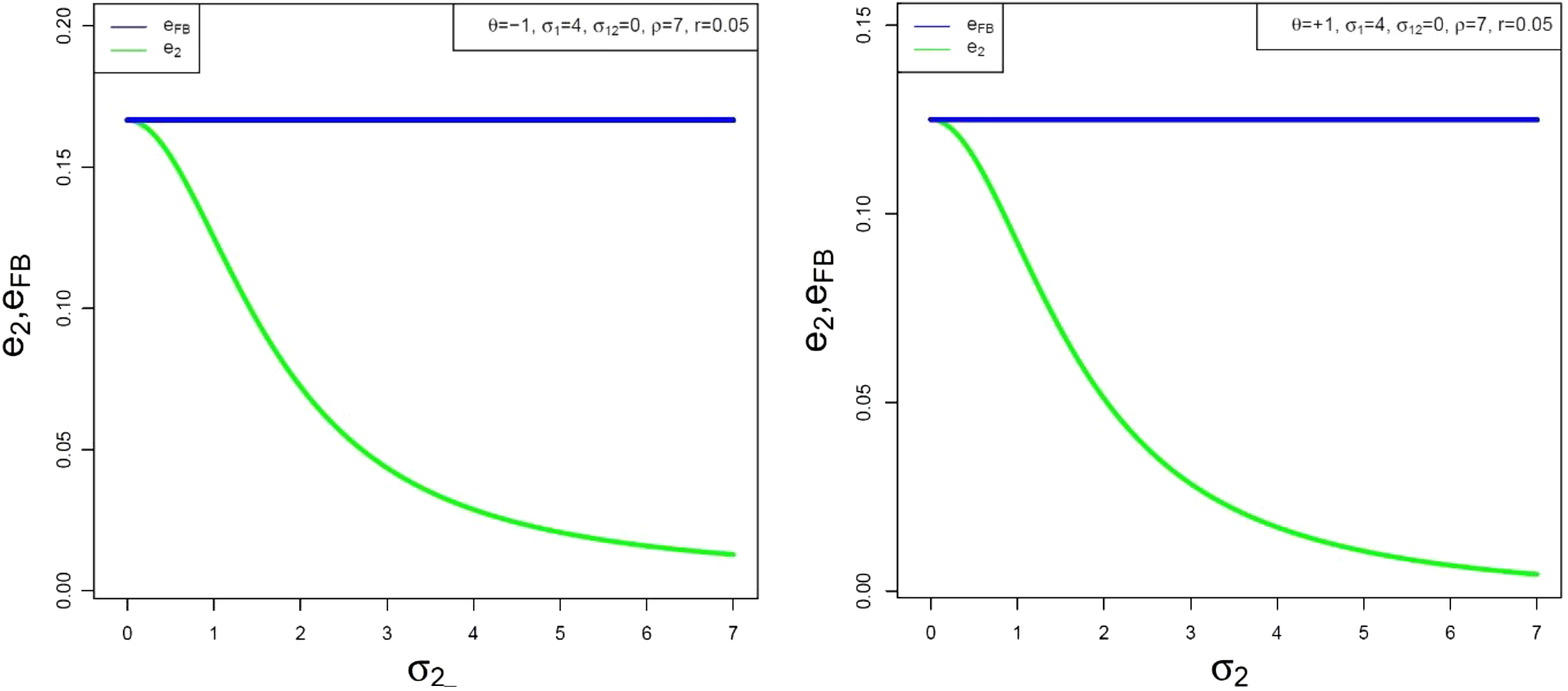

The uncertainty of innovation causes the second best level of effort (under information asymmetry) to diverge from the first best when the regulator is able to fully observe the effort and thus remunerate it at an amount that induces socially optimum level of innovation. The socially optimal level of effort

3

in this case is

Divergence between the first-best and second-best levels of effort when innovation outcome becomes more uncertain.

In all scenarios, the riskier innovation is the less effective becomes performance-based regulation of innovation. Put another way, the results show that performance-based incentive regulation is an effective approach only when the regulator deals with the less risky business-as-usual activities of the firm.

This means that the regulator cannot rely on efficiency-oriented incentive regulation to encourage innovation in network companies, without the introduction of additional modules that take into account the risk to which companies are exposed. Previous studies have argued that incentive regulation has resulted in the decline of R&D and innovation expenditure in the electricity sector (Jamasb & Pollitt, 2008). The nature of uncertainty of innovation requires the application of regulatory incentive mechanisms that take into account the risk of these activities. The message from this section of the article is that incentivising innovation through the same mechanism as efficiency gain does not lead to innovation, even if the objective of innovation is productivity, but with a higher degree of risk.

Competitive innovation funds and the problem of risk

The issue of risk is relevant irrespective of the way in which innovation is incentivised. In recent years, there has been an interest in the introduction of competitive approaches to allocate innovation funds more efficiently and to encourage innovation in network companies. Although these schemes can be designed in various forms, a common feature is that firms submit proposals for the innovation fund to the regulator. The regulator then evaluates these submitted proposals and allocates the funds to the best projects according to some criteria (such as the highest potential value for consumers/society and their impact on the government’s objective of decarbonisation). The source of these funds can be rate payers or tax payers (or a combination of the two). In the rate payer approach, an uplift is added to network fees to be collected from end user, and innovation fund is established, the resource from which will be allocated through a competitive process to the best projects (the regulator may or may not leverage these resources). In this way, electricity customers (rate payers) pay for the cost of innovation.

The competitive scheme for innovation funds is usually implemented for large and complex projects. The significance of the risk here is that preparing proposals for such projects is costly and usually requires the network firm to rely on outside resources. The cost of these resources is non-recoverable if the firm is not successful. Therefore, it is important to understand the implications of such a scheme and the way in which the risk attitude of the firms impacts the outcome of the competition in this context.

Suppose there are two firms operating in a regulatory environment where the total innovation fund available for allocation is

where

and where

In addition, we also assume that the firms’ risk preferences can be presented by a CARA utility function as follows

where

In terms of a solution, this is a simultaneous game of complete information, in the sense that each firm knows its own as well as its rival’s characteristics. The firms exert effort in order to maximise their expected gain from competition, given the uncertainty of outcome and the cost of the effort in preparing and submitting the proposal. We solve the maximisation problem of the firm and obtain the ratio of success probability for the two firms (

Simulation of results

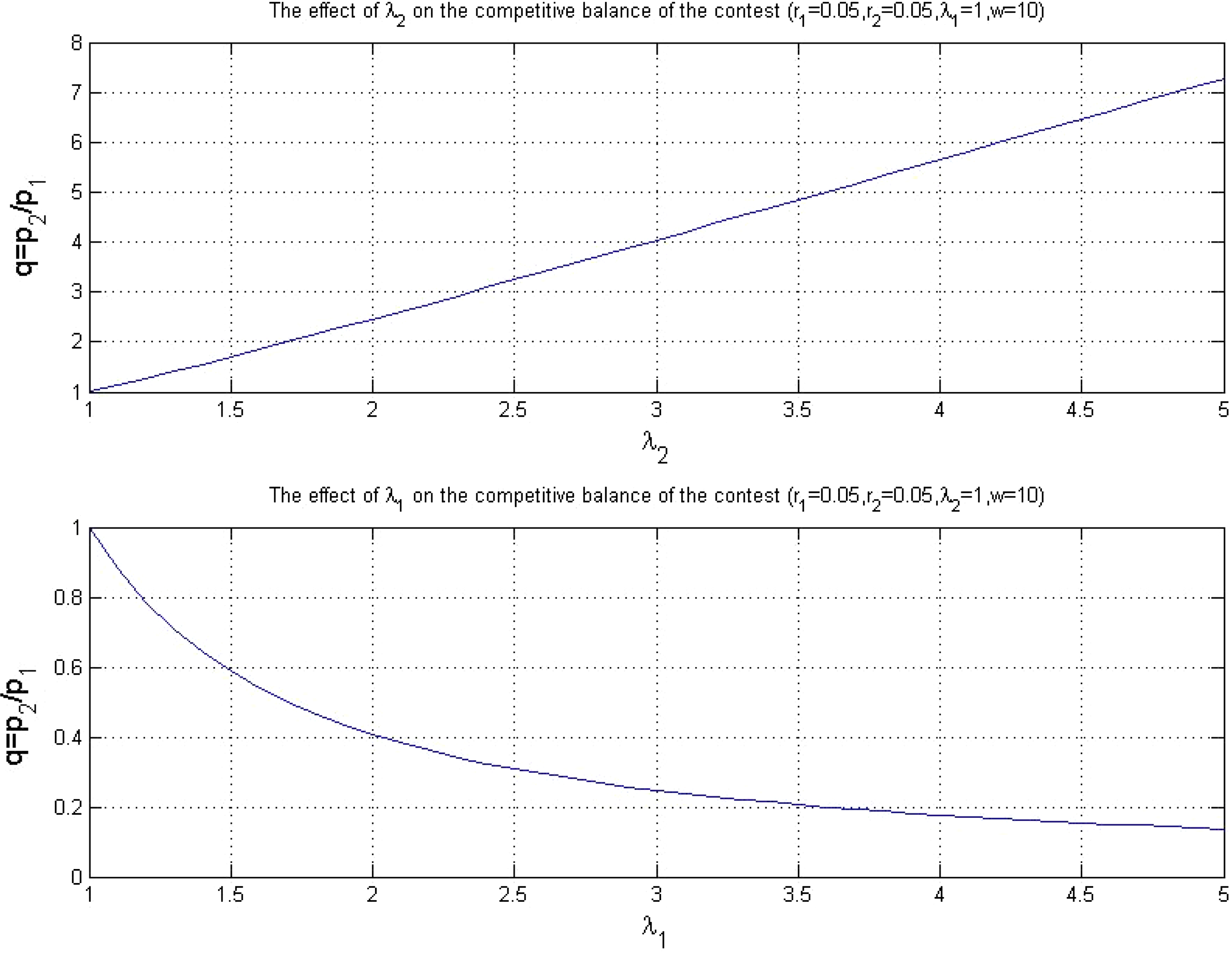

In this section, we simulate some results from the competitive innovation fund model that we presented in the previous section. First we investigate the effect of quality of idea (

The effect of λi – the coefficient representing the inherent quality of the idea – on the competitive balance of the contest.

However, the outcome of the innovation contest also depends on the effort of the firm in preparing the proposal, attending the panel of technical experts and responding to questions and providing the regulator with evidence about the impact and significance of its innovation project. The regulator may not be aware of all the benefits of the proposal, and thus, it is incumbent upon the network company to spend time and resources in order to make a strong case for its innovation initiative. However, not only are these efforts costly, but the outcome of the competition is uncertain. Faced with an uncertain outcome and unrecoverable initial costs in the case of competition loss, firms may show dissimilar levels of risk attitude (depending on their characteristics). The risk attitude, along with the quality of innovation, has an impact on the competitive balance of the outcome.

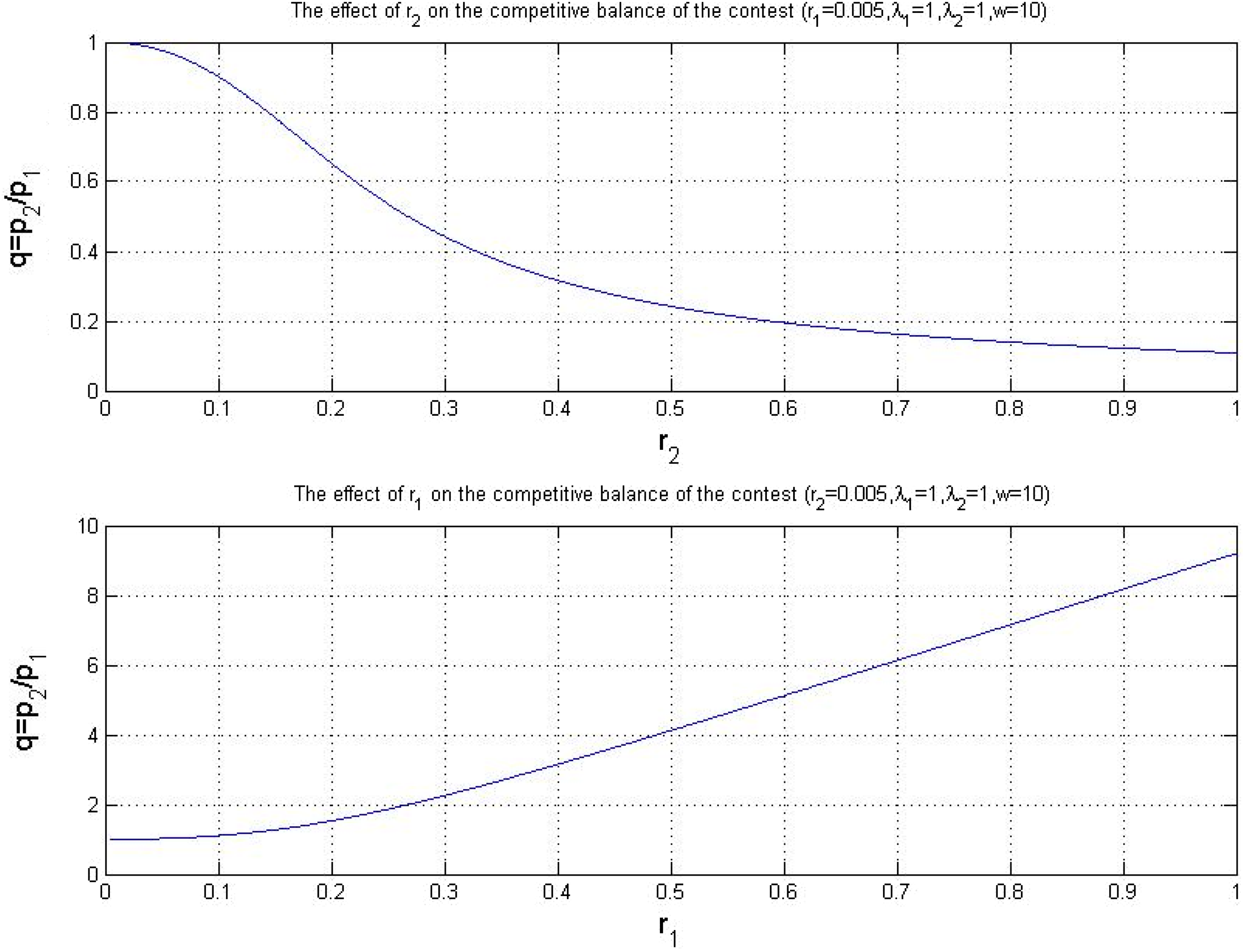

This result is depicted in Figure 7. It shows that when two rival firms have an innovation proposal of the same quality, the probability of winning the competition declines with an increase in the firm’s own level of risk aversion (upper graph) but it increases with a rise in the opponent’s level of risk aversion (lower graph). This happens because the less risk-averse firm is willing to sacrifice more resources in order to justify its proposal and convince the regulator of the value of its project, whereas the more risk-averse firm is acting in a conservative manner.

The effect of risk aversion of parties on the competitive balance of the contest (two projects have the same inherent quality of idea).

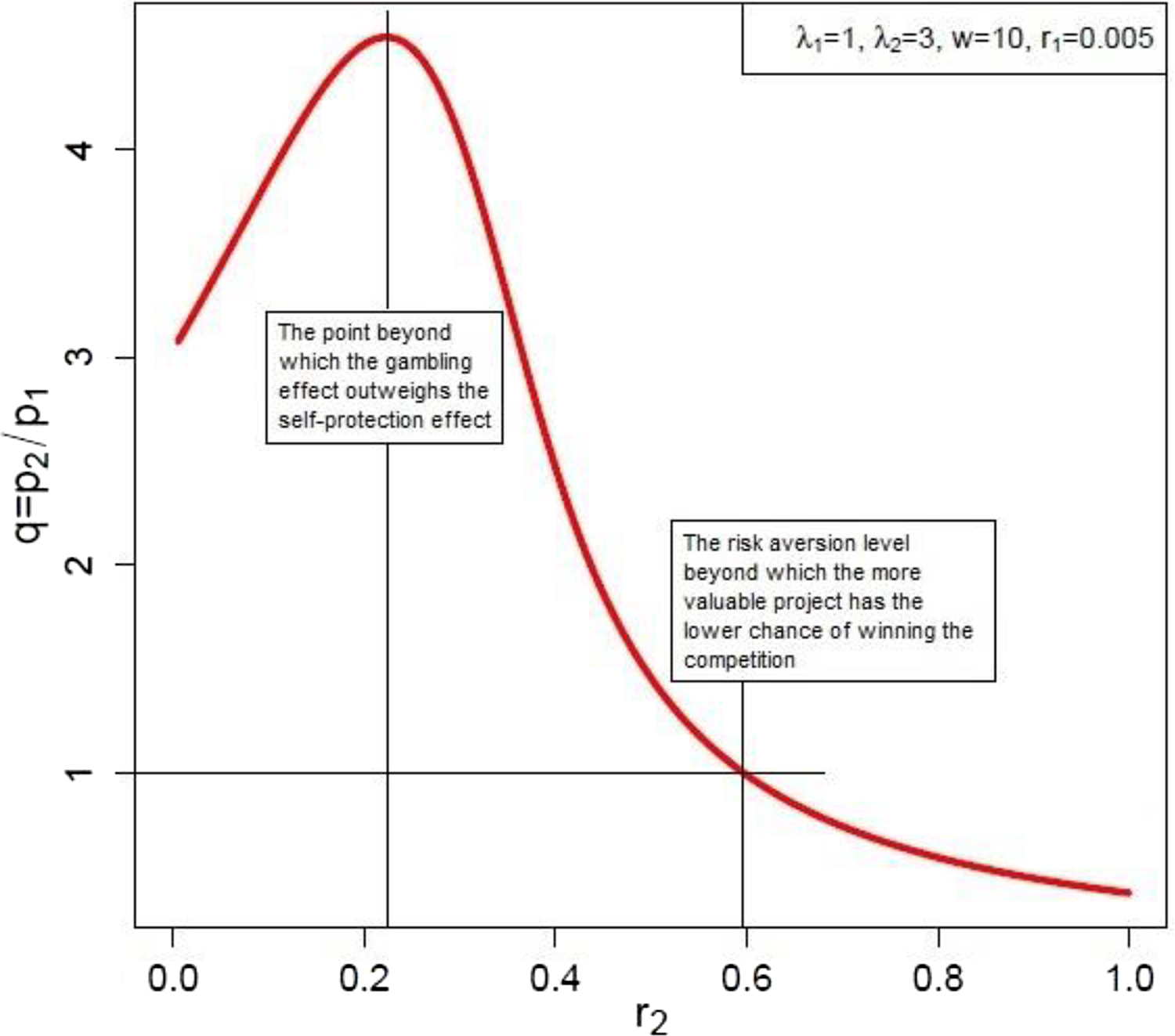

However, the effect of risk aversion on the competitive balance of the competition is not linear, as it depends on the initial quality of idea (

The effect of risk aversion on competitive balance when the firm which has the innovation project with higher potential value is also more risk-averse.

This result has important implications for the design of competitive innovations schemes, because it shows that the existence of a competitive innovation fund does not necessarily lead to the selection of more valuable projects, as the risk attitude of the firm plays a decisive role. Put another way, just by holding a competition (irrespective of how fierce the competition is), the regulator cannot ensure that an innovation fund will be allocated to the innovation idea that has the highest value in terms of consumer benefit and/or alignment with government objectives. This means that the competitive approach needs to consider the difference between risk attitudes of firms in the face of possible non-recoverable initial investments. The other point is that the size of fund in competitive schemes needs to be sufficiently large to justify a company’s initial investment, otherwise uncertainty of outcome may discourage the firm from participation in the scheme altogether. This is why competitive schemes have been used to allocate large amount of money to large projects.

Discussion

In this section, we offer some insights about addressing the issue of innovation under regulation based on the results of analysis made in the previous section.

There is no doubt that regulatory model of network companies should move away from a cost-efficiency-oriented approach to the one that includes additional instrument for longer term objectives (Cambini et al., 2014). There is a need for regulatory models that provide incentives to meet policy goals and remove disincentives inherent in traditional regulation for innovative solutions, while staying agnostic to the exact means of delivery.

Incentivising innovation efforts involves designing a compensation plan that determines how to share the risk of innovation efforts between a firm and its customers in an efficient manner. However, designing a scheme to encourage innovation, allowing the firm to have flexibility, while factoring in risk and information asymmetry, is not a trivial task. Information asymmetry exists because a regulator is usually unaware of innovation opportunities (in terms of cost reduction, service quality improvements or other objectives) available to the firm and also of how good the firm is at exerting effort to realise these potentials (in other words, the quality of the firm and the efforts of its managers are unobservable to the regulator). At the same time, the outcome of innovation efforts is uncertain, meaning that it is a risky undertaking.

Economic theory tells us that when the effort of the firm is unobservable, remuneration needs to be linked to the performance of the firm (at least partially) as this causes the firm to exert the optimal level of effort. This explains why performance-based regulation has been so popular in network industries. However, the same theory tells us that if the firm is risk-averse and the outcome of the task is uncertain, the compensation scheme needs to provide the firm with insurance for its cost recovery, otherwise the firm does not have the incentive to engage in the task. This suggests that regulation of innovation is a delicate task of balancing between incentive and insurance provisions for the firm.

In practical terms, the regulator has many options to address innovation, but not all of them necessarily result in an efficient risk sharing between network firms and consumers. The regulator can focus on inputs (innovation costs) or output (innovation outcome) or both (Bauknecht, 2011). In the input-oriented model, the regulator designs the incentive scheme based on the costs of innovation. In this way, innovation costs can be included in the regulatory expenses and be subject to the same regulatory restriction as other costs. For example, the regulator can include them in their benchmarking practice, to be compared with the costs of peers in the industry. Alternatively, the regulator can treat innovation costs differently by passing them directly to consumers or including them in the regulatory asset base of companies, which entitles the firm to a minimum rate of return. Rather than inputs, the regulator can focus on innovation output and devise the incentive mechanism such that the firm benefits from successful innovation. This can be done in various ways such as allowing for additional revenue under a regulatory model based on the value of innovation, extending the regulatory period and removing regulatory restrictions for a limited period (Bauknecht, 2011).

An input-based regulation of innovation costs (where innovation costs are treated separately) insures the firm against the downside risk of innovation, whereas an output-based regulation of innovation allows the firm to benefit fully from the value of a successful innovation. However, an input-based regulation, if not designed properly, can lead to inefficient expenditure, whereas an output-based regulation of innovation can expose the firm to undesired risks (Bauknecht, 2011). Furthermore, output-based regulation can run into the problem of verifiability and measurability (National Renewable Energy Laboratory [NREL], 2017). This is because innovation can be concerned with activities other than cost-efficiency gain – such as facilitating integration of distributed resources, improving quality of service or introducing new services, reducing environmental impacts, providing resilience for service provision, enabling new market models at the grid level and improving the business model of network companies (ENA, 2018). If the regulator cannot verify and measure innovation output, it cannot remunerate the company for its activities. The approaches that can be used to address this issue are as follows: using patents registered by the network firm as an indicator of output or defining innovation output ex ante (e.g. number of fast EV charging points or number of smart meters installed or the share of demand response/distributed resources used to defer grid capacity enhancement).

Whether a regulator should focus on input or output to incentivise innovation depends on several factors such as innovation direction (namely whether the regulator wants the firm to undertake specific tasks), the cost of monitoring input versus output and the risk attitude of the firm. If the regulator is interested in incentivising innovation in a particular area (such as smart grid), and inputs are observable, an input-based regulation can be used. This also holds when the cost of monitoring inputs is lower than that of measuring outputs, and when the firm is risk-averse so that it requires a higher level of insurance against innovation costs given the uncertain outcome of such activities.

An important point here is that the regulator needs to distinguish between types of innovation by network firms and apply incentive instruments appropriate for the phase of innovation and proportional to the degree of risk that the firm is exposed to. There are four stages of innovation that are relevant to regulated networks as follows: R&D; piloting; the introduction of new technologies/processes; and the commercial stage.

Risk mitigation is crucial for innovation activities that are at the early stages of the spectrum. In the case of R&D and piloting (risky undertakings), the regulator can reduce the risk of these activities by adopting an input-based scheme in which innovation costs are decoupled from outcome (e.g. these costs are directly transferred to consumers). However, this needs to be done on the basis of an ex ante rule which clearly determines which expenses can be included in innovation category. This is to avoid strategic behaviour in the form of cost transfer between cost categories.

For innovation activities that are related to the two later stages (introduction of new technologies/processes and commercialisation), the regulator can adopt an output-based regulation, if the risk of these activities are of the same order of normal activities of firm. If the outcome of innovation at these stages is are to be an efficiency gain, a revenue-sharing mechanism has proved to be an effective tool. This is because cost reduction can be verified and measured; sharing a percentage of cost reduction (resulting from innovation) with a company thus creates sufficient incentive and results in efficient risk sharing. However, if the outcome of innovation at these later stages is beyond cost-efficiency, the regulator can increase the cap, or remove the regulatory restriction, for a limited period on the basis of the successful deployment or commercialisation of the technology/process.

When the size of innovation projects is large, the incentives can be provided through a competitive mechanism. 4 This is specifically relevant to distribution network companies, given that the number of these grids is sufficiently high to make such competition feasible. As discussed in the previous section, one challenge of competitive schemes is that they expose the network firms to the risk of not recovering their initial investment in the preparation of innovation proposals, as the outcome of competition is uncertain. This risk can discourage firms from engaging in large innovation projects. One approach to dealing with this issue is that the cost of preparing innovation proposals, including the initial technical, economic and feasibility studies, is covered by a separate input-based mechanism. This means that the regulator can introduce small-scale funds for small-scale projects (whose costs can be recovered through the network tariff), and their results can be used in the bidding process for large complex funds in the competitive scheme. Another approach to address this issue is to adopt a two-stage competition process in which an initial evaluation provides an early indication of eligible projects before companies are invited for full submission.

The UK regulatory regime, RIIO (Revenue = Incentives + Innovation + Outputs), is an example of a model that is largely cognisant of the issues mentioned above. It was introduced to transition away from the traditional approach of simply rewarding capital investment in networks to an innovation and output-based regime with a system of rewards for achievement of specified goals and outputs (LARA, 2018). It also can serve as a model for other countries and regions (Payne, 2015).

The RIIO model incentivises network companies to undertake innovation through two mechanisms: (a) incentive as part of the price control review and (b) specific innovation stimulus package (Ofgem, 2010). Innovation as part of price control review is promoted through long-term ex ante output-oriented regulatory model where companies benefit from successful innovation. Innovation stimulus package, on the other hand, is designed to facilitate achieving a sustainable energy sector. It includes three different schemes: the network innovation competition (NIC), the network innovation allowance (NIA) and the innovation roll-out mechanism (IRM). The costs of incentives under innovation stimulus package is recovered through network tariffs, and companies will lose it if they do not use this fund.

As a form of incentive regulation, RIIO incentivises innovation as part of the price control review by defining a set of outputs and targets. The regulatory model is such that the firm has both financial and reputational motive in order to outperform these targets. The network companies need to report their performance to the regulator for each category of output and their revenue will be adjusted upward when they exceed the target and downward when they fail to meet the target. These rewards and penalties are not fixed but vary depending on case that incentives are provided for and reflect the marginal value to the consumer. An example of these incentives is the use of non-network solutions in distribution network congestion management which allows companies to retain a percentage of their costs savings.

A specific feature of RIIO model is that it applies a total costs approach and this directs the attention of firm to innovation rather than capital expenditure because network utilities are always entitled to a percentage of costs savings. The totex approach always treats a fixed percentage of total cost as capital expenditure and the rest as operational expenditure regardless of their actual share. This is to prevent the firm from only focusing on capital expenditure and widen the choice of firm for innovation as many of latest innovations in the network companies are not asset based (e.g. the use of demand response as an alternative to grid capacity upgrade).

Although price control review provides innovation incentive for network companies, however, most research, development and demonstration projects have uncertain outcomes and return (Ofgem, 2017). Furthermore, shareholders are often unwilling to fund speculative projects. In addition, commercialisation of projects that their benefits are linked to the decarbonisation of networks is often difficult. Therefore, the UK regulator has offered a time-limited stimulus package in order to help network companies to establish a culture, internal structures and third-party contracts to facilitate innovation. The innovation stimulus package covers 8 years (2015–2023) and provides innovation-specific incentive mechanism for network companies. One of the most important schemes in this package is NIC. Under this scheme, network companies compete annually for fund which allows them to develop and demonstrate new technologies or implement innovative commercial and operational arrangements.

The NIC addresses the risk of unrecoverable initial investments in the competition in two ways. First through initial screening process (ISP) and second through allowing network firms to recover their bid preparation and submission costs up to a certain level. The ISP provides an early indication of which project might be eligible for funding and thus reduces the risk that network companies spending resources and time to develop ineligible projects. In addition, for the projects that pass ISP stage, the network companies can use up to £175,000 or 5% of outstanding fund required (whichever is smaller) from their NIA in order cover costs of preparation and submission of bid (Ofgem, 2017).

The NIA is not competitive, and each company receives this fund as part of its price control review. This fund, which is equal to 0.5% of allowed revenue of the company (depending on the quality of project can be extended to 1%), is awarded to projects that have a direct improving effect on the operation of network licensees or the system operator and where feasible should involve RD&D in the area of product and process developments or adoption of new technologies and arrangements.

IRM allows network companies to receive further fund to undertake innovation within the regulatory period. This fund facilitates deployments of proven technologies. In order to receive this fund, companies need to submit a business case to the regulator that demonstrates the value of the project and benefit to the customers.

Conclusions

While the economics of low carbon generation technologies is fast improving due to a mix of policy and market-driven incentives, innovation in electricity networks has been relatively sluggish. This slow adaptation of electricity networks is challenging as they are key to the energy transition. Further electrification of the economy requires significant investment and innovation in the grid segment of the electricity supply chain.

Traditional regulatory models of network utilities are designed to incentivise cost-efficiency, with the assumption that network business is costly and the task of regulation is to lower these costs, subject to achieving a certain level of reliability. The main challenge of incentivising innovation is that it is not only costly but also risky. Therefore, an innovation-oriented regulatory model needs to factor in uncertainty in the outcome of innovation efforts.

The costs and risks of innovation effort can be borne by firms, be passed to consumers or shared between these two. If the regulator were able to observe the firm’s effort, incentivising innovation would be simple because the regulator could set the remuneration at a level equal to the cost of the efficient level of effort. However, in practice, there is information asymmetry between the regulator and the firm, which means that the remuneration of firms needs to be linked to the performance of the firm. But this is not straightforward. On the one hand, the regulator wants the firm to undertake innovation, but for this to happen, he needs to remunerate the firm for its costs when undertaking risky activity. On the other hand, the regulator does not want to distort the firm’s incentives by giving it full insurance for activities whose risks are actually manageable by the firm. The task of regulation is, therefore, to devise a scheme which balances risk sharing with incentives.

We show that incentive mechanisms that do not take into account the risk profile of innovation activities divert the attention of the network utilities from innovation to normal efficiency gain. This indicates the importance of differentiating between cost-efficiency and innovation in designing the regulation of electricity networks. A shift from traditional models of network regulation to new models – where innovation is the key part of the incentive structure – is crucial to facilitate the transition of the power sector. In relation to the design of an innovation-friendly regulatory scheme, the regulator needs to differentiate between types of innovation activities, as there is a different level of risk involved at each stage of innovation. When network companies engage in R&D and piloting, an input-based regulation (whereby the costs of these activities are decoupled from performance) has proved to be an effective approach. For less risky activities, such as the introduction of established technologies and processes, an output-based regulation that uses costs sharing or revenue cap adjustment leads to a more efficient risk-sharing mechanism.

The issue of risk in regulating innovation is not confined to the actual risk of outcome. The risk attitude of network companies is also decisive. If the scheme does not take this into account, a heterogeneous risk attitude among bidders can distort the outcome of a competitive allocation of innovation funds. We demonstrate that a firm with a greater level of risk tolerance but a less valuable project can win a contest for innovation funds in competition with a risk-averse firm which has a more valuable innovation project. The risk of losing their initial investment because of the uncertain outcome of competition can discourage network companies from entering into competition or spending resources to make a case for their project. An approach to address this issue is to adopt a two-stage competition process in which an initial evaluation provides an early indication of eligible projects before companies are invited for full submission. Regulator can also offer smaller funds to be used for projects whose technical/economic results can then be used in larger scale innovation proposals. This eliminates the risk of losing the upfront capital and puts network companies with different levels of risk tolerance on the same level in the competition process.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.