Abstract

Demographic ageing poses severe challenges to the sustainability of public pension systems in Europe. Many member states rely heavily on pay-as-you-go arrangements, which, combined with longer life expectancy and relatively low retirement ages, are generating persistent pension deficits. Traditional reforms, such as increasing the retirement age, raising productivity or adjusting benefits, have proven politically difficult due to deficit bias, the problem of political agency and widespread loss aversion. This article argues that, in addition to such measures, the EU’s capital markets union could play a central role in addressing pension shortfalls. By fostering deeper financial integration, the capital markets union could enhance investment opportunities, promote growth and reduce the vulnerability of member states to the sovereign-bank ‘doom loop’.

Keywords

Introduction

The future finances of EU member states are in trouble. That is, if you take the projections of pension deficits seriously. Demographic changes combined with pay-as-you-go provisions will lead to large and persistent shortfalls in state-provided pensions. Dealing with this will be an important issue for many years to come.

This article traces the causes of the pension shortfall and moves from there to a vision for future developments. Specifically, I will focus on the potential for the capital markets union (CMU) to play a role in improving investment opportunities, increasing economic growth and mitigating financial market stress in times of crisis.

The problem: a large pension shortfall

Pensions are expensive. In the social model of most European countries, life after the period of paid work is one in which pension funds, the state or any other institutions are expected to pay retirement benefits. These benefits need to be high enough to sustain a reasonable living standard.

Pensions in most countries are high enough. Although pensioners in most countries are not as well-off as those in the Netherlands, a retired person in a European country can be expected to get by without having to work. People do work in retirement, and usually for their own good and that of others. But in all but exceptional cases, this is not necessary for survival.

Although the replacement rate of a typical pension plan is not 100% of the final wage, people get by because costs are lower in retirement. Commuting, lunches and other costs are gone. And there is time to do ‘housework’, maintaining and repairing things yourself. People suffer a bit of a consumption shock around retirement (Banks et al. 1998), but they adjust fairly quickly once they have adapted to the new situation.

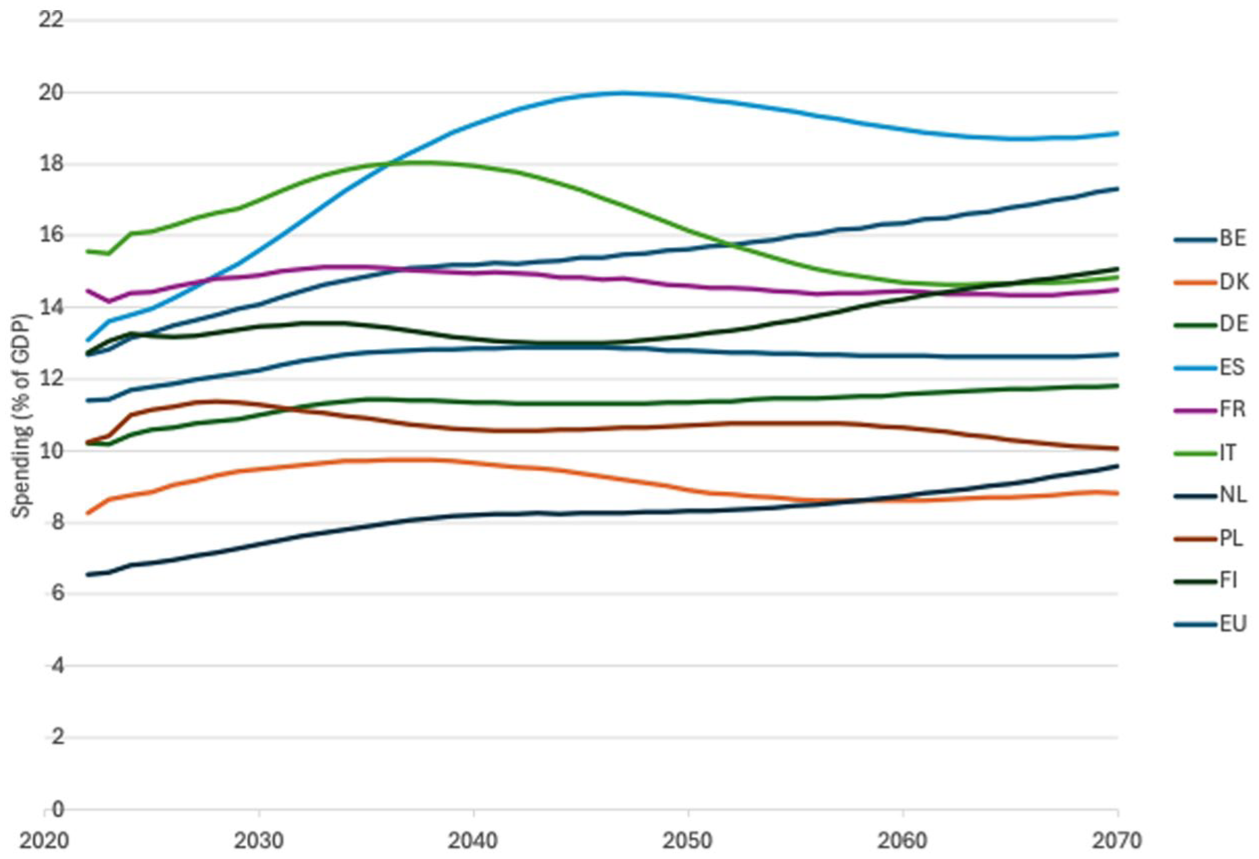

The bad news is that public pension costs—the spending by governments on providing retirement benefits—are rising. Figure 1 documents the projections for the rising costs in a selection of European countries.

Projections for public pension costs 2022–70.

The reasons that costs are rising differ from country to country and depend on the extent to which pension plans are funded (Pape 2023). The shortfall countries have pension systems through which retirement benefits are mostly state-provided. The benefits received by pensioners are paid from the contributions of the working population. In pension jargon this is called ‘pay-as-you-go’ (PAYG), as the state pays the pensions as it goes along through time. No capital is set aside, and no investment returns accrue that could pay for future pensions.

In countries with low expenditures, a PAYG system is combined with a funded system of occupational pensions. The pension funds provide capital to businesses, and the investment returns contribute to the affordability of retirement incomes. Countries with funded pension plans have relatively stable government expenditures which are not expected to rise much in the future.

It is not merely the way they provide pension benefits that characterises the countries with a projected shortfall in the PAYG system. They also suffer from a relatively low retirement age, and unemployment is usually higher. This is a triple problem: an out-of-pocket expenditure for the state, a long retirement period and a low base of workers to pay the necessary taxes.

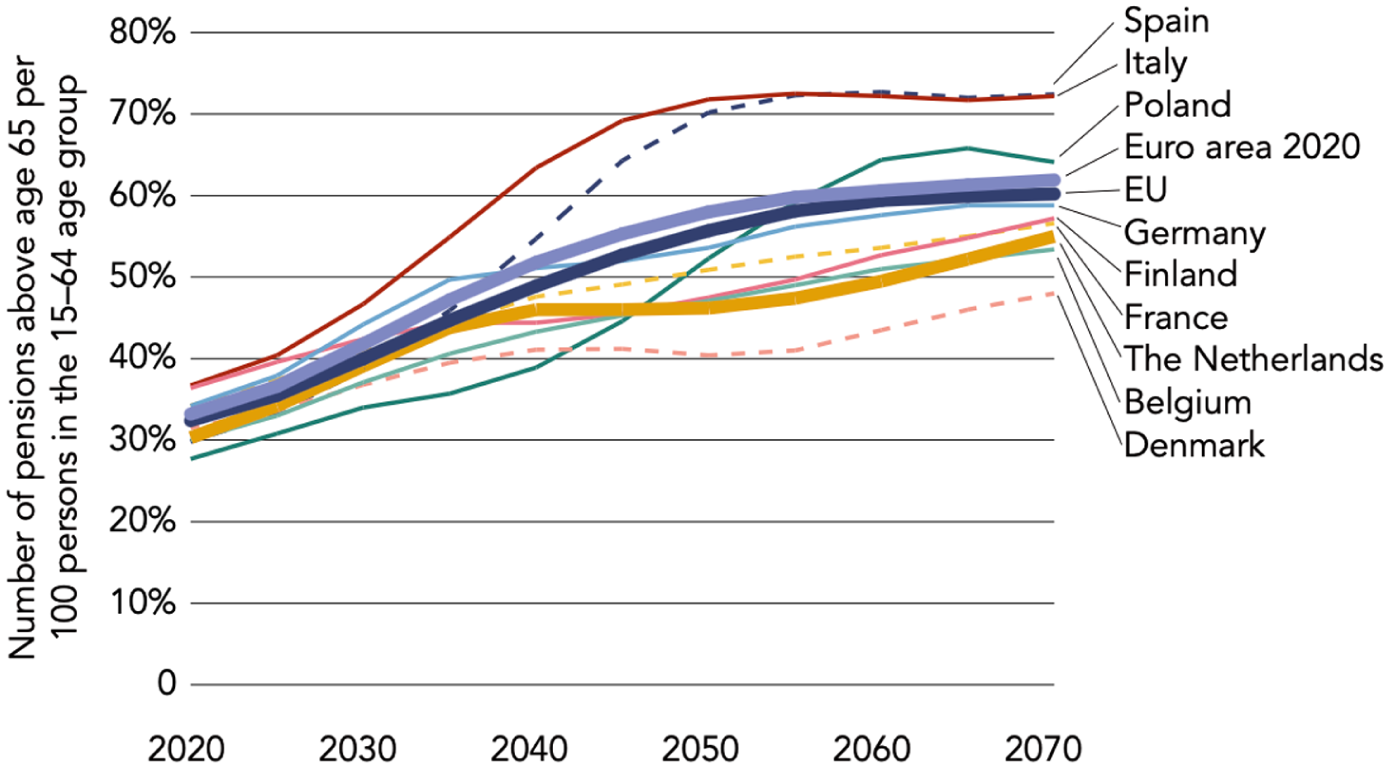

To add to the bad news, the situation in Figure 2 visualises just one element of higher costs in an ageing society. Depending on the country, other costs, such as healthcare, can pose a larger problem than the one presented by pensions. Figure 2 shows the ‘grey pressure’ as computed by the United Nations.

Estimated population pressure 2020–70.

The demographics shown in Figure 2 will lead to pressures on more than just the pension systems. For example, in the Netherlands the increase in PAYG payments is much smaller than projected healthcare cost increases. The predominant cost in the future will be expenditure on long-term care.

Origins of the pension problem

The pension problem has been known for decades. Why was it not solved earlier?

Three insights from the field of political economy can help us to understand the causes. First, it has been known for a long time that governments have a tendency to overspend. Most countries run a budget deficit, for most of the time (Alesina et al. 2008). This pattern, also called the deficit bias, is a result of political forces that, apparently, make it difficult to balance the budget. The deficit bias is also seen in the reluctance to undertake pension reform: the financial costs are in the future while the real political costs of reform are now. So, reform is postponed, and spending on other priorities can continue.

Second, there is political agency. Concrete and current spending projects can be communicated to voters easily. Far-away cost run-ups are much more difficult to communicate. Voters are limited in their ability to effectively monitor the state’s real financial situation. The demise of traditional parties in the centre of the political spectrum has made this problem more salient (Mair 2006). This is not to say that past generations of politicians found it easier to avoid deficits, but certainly the new generation is faced with new problems of legitimacy and agency.

Third, people are loss averse. In the words of Burton Malkiel, ‘a dollar loss is 2½ times as painful as a dollar gain is pleasurable’ (Malkiel 2014, 190). And since both politicians and voters are only human, they are both susceptible to this bias. The bias occurs because a ‘loss’ is coded against a reference point that can be arbitrary, anchored to some past event or expectations of the future (Kahneman and Tversky 1979).

The loss-averse bias is another factor that induces people to postpone painful interventions until they are really necessary (Vis 2009). Small losses, in particular, are the most avoided. This pattern precludes political interventions that are relatively small, such as raising the retirement age by a few months: the political costs are high, but the gains are slight.

The above mechanisms should not be read as excuses for politicians who have pushed finding solutions into the future. Politics is about making the choices necessary for current and future generations. Given the projected shortfalls, more should have been done to ensure that government finances are sustainable. However, these mechanisms outlined help to explain how hard these choices are and what forces are preventing the implementation of easy solutions. Politicians are representatives, and the will of the people has clearly not been in the direction of enacting painful reforms.

To make pensions sustainable in the longer term, a number of measures are available that could alleviate the stress in the system: raising the retirement age, raising productivity and labour force participation, cutting indexation or increasing taxes (European Commission, Directorate-General for Economic and Financial Affairs 2024). Sensible policies will be a combination of measures rather than any single action.

The CMU as a growth mechanism

In his 1933 paper ‘National Self-Sufficiency’, John Maynard Keynes argued that international trade and openness would benefit all nations. The exception was finance, an idea expressed in his famous quote, ‘above all, let finance be primarily national’ (Keynes 1933, 756).

It seems that the EU’s member states have heeded this advice. It has long been clear that the EU lacks a proper, functioning single market for savings and investment. The CMU has been on the agenda for a long time (Demertzis et al. 2021). It is necessary to improve financial stability and to finance high-growth sectors. This includes investments in emission-reducing technologies. European economies are mostly bank-based and must take a quantum leap in this respect.

The Letta report of 2024 made more concrete proposals on why the CMU is needed and what it should achieve (Letta 2024). It is needed because, in the EU, companies and financiers seeking to lend and invest across borders face more ‘capital frictions’ (i.e. obstacles) than they would in the US.

These capital frictions are not necessarily regulatory in character. Campos et al. (2025) show that in product market competition as well as financial market regulations, the harmonisation that has taken place in the EU has led to a decrease in the regulatory burden. However, most EU member states have forms of labour protection that hamper growth and innovation. This is not to say that US-style flexibility is necessary, but that attention is needed to the design of these policies. It is possible to have labour security and growth, but only Germany and the Nordic countries seem to have achieved this (Schoefer 2025, 47).

Also, non-tariff trade barriers are estimated by the International Monetary Fund (2024) to be as high as 44% for goods and 110% for services. These estimates have been arrived at by comparing the amount of intra-EU trade that takes place with what would be expected given similar economies, distances and so on. Apparently, EU member states trade much less with each other than we would expect. For a free-trade area like the EU, this is quite worrying and deserves more political attention.

The need for a CMU is shown in the recent refusal by the German government to allow the acquisition of Germany’s Commerzbank by the Italian UniCredit, although the anti-trust authorities had approved the plan (Reuters 2025). This is typical for the EU, a union in which cross-border banking firms are still rare (Montagner 2025).

Of course, EU member states need more than financing to raise productivity. The prospects of young people in some of the southern and eastern countries are not always hopeful, as the high youth unemployment shows. Labour market rigidities could be a leading cause of these abysmal statistics (Campos et al. 2025). Countries will have to make sensible changes to lower the cost of starting a business and competing with existing businesses. That this should be possible without having to become more ‘American’ by adopting the ultra-flexible labour laws seen in the US is shown by the performance of the Netherlands, for example (Schoefer 2025).

Preventing another doom loop

If the debt levels of EU member states keep rising at the current pace, partly caused by the pension obligation, it will be reflected in credit spreads. Rising credit spreads make government borrowing more expensive, which limits the ability of governments to honour their obligations. At the same time, banks’ balance sheets deteriorate because they hold government bonds from member states. This co-dependency between banks and governments is the ‘doom loop’ described by Gómez-Puig and Sosvilla-Rivero (2024).

The doom loop is not only a threat to financial stability, but it has also been a way for banks to artificially increase profits (see Acharya and Steffen 2015). Because governments are aware of their inter-relationship with the banking sector, banks have been able to count on this privileged position to fund themselves cheaply and to profit from the mispricing of risks in sovereign bonds. They can achieve greater returns at lower risk or decrease the risk on the existing levels of return. With a cheap lending facility provided by the European Central Bank in times of crisis, such constructions have come close to being a ‘money machine’. This is not good.

The initial shock that exposed the existence of the doom loop was the US mortgage debt crisis of 2007–8, which led to the global financial crisis. This time, however, the initial shock could come from government debt. US debt levels currently exceed 110% of GDP, and the projected deficit for 2026 stands at 7%. Some European countries have similar levels of debt and deficits that are not coming down. An exception is Greece, which has sharply declining debt levels.

European sovereign spreads are still too sensitive to market frictions. For example, spreads have been rising recently due to the Dutch pension funds selling off around €125 billion of long-dated government bonds. They are preparing for a change in the pension system starting in 2026 (McDougall 2025). The fact that a few pension funds can produce such an effect speaks to the limited size of European debt markets and the need for more integration.

If the European banking system, or financial system as a whole, comes under pressure again, the value of financial assets will drop and the economy in its entirety will suffer. This makes it a dominant concern for the pension deficit. The deficit itself might not be affected directly by financial stress, but it will be an increasing burden on government finances. If growth remains low, the prospect of the pension shortfall will gain in significance.

Through the CMU, the likelihood of another doom loop could be greatly reduced. Banks would be more diversified geographically, both in their funding sources and in lending. They would depend less on the economic cycle in one country and more on the eurozone as a whole. And when a bank does get into trouble, governments would feel less need to save a national ‘champion’.

The fragility of the EU banking system in relation to Federal Reserve policy

At the height of the 2008–9 financial crisis, it was the US Federal Reserve that provided a backstop to Europe (a credit line in dollars) to save the European banking system. But of course, the US caused the financial crisis in the first place. All the same, the US was apparently needed. But this points to an inherent weakness in the European banking system. In times of crisis the US dollar is the reserve currency of choice, and people flock to it. And this, in itself, makes the European banking system fragile—beyond its current weakness and relatively low capital, low profitability, fragmentation and vulnerability to political interference.

In 2013 the swap line of the Federal Reserve to the European Central Bank became permanent, and the world is all the better for it (see Spielberger 2025). The US Federal Reserve has effectively become the liquidity backstop for the global financial system. However, with this global role comes greater responsibility. The actions of the current US government in raising tariffs for its former trade partners call into question that government’s commitment to global financial stability. This, and potential future actions that weaken the position of the dollar, could hasten the move from a unipolar (dollar) system to a multipolar currency system (Gensler et al. 2025).

Conclusion

Although Keynes believed that finance should remain national, he did acknowledge that change might need to happen. If it did, ‘It should not be a matter of tearing up roots but of slowly training a plant to grow in a different direction’ (Keynes 1933, 756). The message of the current article is similar. It has considered the potential benefits of the CMU for the looming pension deficits in a selected number of European countries: we need to grow in a different direction.

Pension shortfalls in many European countries appear to be entrenched. As long as they are not addressed, these projected shortfalls could be an impetus for a new debt crisis. It appears that the growth of government debt in the EU is already becoming unsustainable; it would start to become painful if interest rates were to rise. Another debt crisis could again start in the US, where deficits are at unprecedented peacetime heights. A small initial shock could lead to feedback loops in financial markets, where the projected pension shortfalls become relevant for sovereign spreads.

This article argues that pension concerns could be addressed in a way that benefits the current economy. It does not have to be a zero-sum game in which the gains of one generation (the elderly) are obtained at the cost of another (the younger). Developing a better capital market in the EU provides a win–win opportunity. The CMU would be able to unlock growth potential in the European economies, improve investment returns and increase the financial system’s capacity to deal with stress. It should be complemented by other reforms, but it will be an essential building block.

The economist Herbert Stein once said, ‘If something cannot go on forever, it will stop’ (United States, Congress, Joint Economic Committee 1986, 262). Stein was talking about the sustainability of the US debt. We should take seriously what has become known as ‘Stein’s law’ for the EU’s debt situation as well. We can only hope that policymakers do not waste the opportunity to improve intra-EU trade and capital flows before a looming crisis makes it necessary to do so under suboptimal conditions.