Abstract

The persistent shortage of critical medicines in the EU has emerged as a pressing challenge to public health. In response, the European Commission proposed the Critical Medicines Act in 2025, building on post-Covid strategies to enhance pharmaceutical resilience. The Act promotes domestic manufacturing, diversified supply chains and strategic partnerships with third countries. This article highlights, among other priorities, the importance of scrutinising every link in critical supply chains, fostering solidarity among EU member states and ensuring consistency across legislative frameworks. While these efforts will impose higher costs on citizens—both as patients and taxpayers—such costs could be largely offset by improvements in public health outcomes.

Introduction

At the onset of the Covid-19 pandemic, the globalised economy was jolted by a stark revelation of its vulnerabilities: supply chains, 1 once celebrated for their efficiency, proved ineffective due to a lack of resilience. Efficiency and resilience can coexist, but only as long as trade flows freely under the just-in-time model. However, when disruptions occur—whether accidental or geopolitical—the cracks become visible. Suddenly, for products long sourced from distant markets, domestic production has emerged as a strategic necessity in a world where political geography has returned with a vengeance.

In recent years, most EU countries have experienced shortages of critical medicines—those essential for the continuity of care and the protection of public health. This emergency has prompted the EU to draw lessons from the pandemic by adopting a new governance model to assess supply chain vulnerabilities and by proposing a new regulation aimed at strengthening resilience and stimulating domestic production.

This strategy is perfectly aligned with the spirit of ‘open strategic autonomy’, a concept introduced in the EU (European Commission 2021, 4). In response to the shortages of critical products experienced during the Covid-19 pandemic, the EU must now consider a multi-pronged strategy: boosting domestic manufacturing, redesigning the geography of supply chains through diversification and building strategic partnerships with third countries. After decades of prioritising efficiency, the focus must now shift towards resilience, that is, developing supply chains that can better withstand future shocks.

The shortage of medicine in the EU has worsened

Despite being home to one of the world’s leading pharmaceutical industries, the EU has been grappling with medicine shortages for years (PGEU 2019, 3–4). The Covid-19 crisis exacerbated the problem, as soaring demand for anaesthetics, antibiotics and muscle relaxants collided with supplier shutdowns, logistical bottlenecks and national stockpiling and export bans. Even after the end of the pandemic, the situation has not significantly improved: the percentage of European countries experiencing medicine shortages remained very high in both 2023 and 2024, and, for most medicines, a growing number of countries reported supply issues (PGEU 2024, 6; PGEU 2025, 6).

A survey on shortages (AEMPS and WP5 Beneficiaries 2024) identified that over 50% of reported shortages are caused by manufacturing issues, a category which includes shortages related to the availability of active pharmaceutical ingredients (APIs). 2 These shortages primarily affect generic medicines (or generics), 3 which account for 70% of those dispensed in Europe (Troein et al. 2024). Production of generics has increasingly shifted abroad, while the European pharmaceutical industry has focused on more profitable market segments. According to Fischer et al. (2023, 24) and the Chemical Pharmaceutical Generic Association (CPA 2025, 95), those segments are research and development (R&D), and products that require high-tech infrastructure, a skilled workforce and complex manufacturing processes. As a result, Europe’s dependence on third countries for less complex, high-volume, low-margin medicines, such as basic generics, has increased.

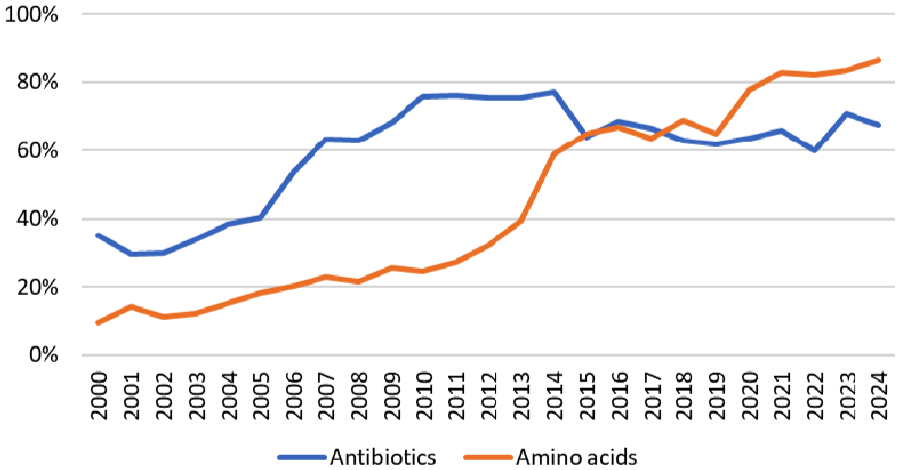

For instance, 80% of APIs and 40% of medicines sold in Europe originate from China and India. This dependency is particularly evident for antibiotics, 4 which top the list of medicines in shortage, and amino acids, which are essential to pharmaceutical manufacturing. According to Eurostat data, the EU has recorded a trade deficit in antibiotics since 2000 (the first year of available statistics) and in amino acids 5 since 2014. In 2024, 68% of the EU’s antibiotic imports and 86% of its amino acid imports came from China (Figure 1), underscoring the country’s growing role as a leading global exporter.

The EU’s import of antibiotics and amino acids from China (% of extra-EU27 imports).

As of today, for many critical medicines, China is the only country that hosts the whole industrial structure required for the entire supply chain within its territory.

The EU develops a new approach to governance to strengthen the availability of critical medicines

During Covid-19 the EU coordinated common solutions in a policy area—public health—that had traditionally been managed at the national level. In November 2020 the European Commission launched the European Health Union initiative (European Commission 2020), which granted the EU greater powers to act during cross-border health emergencies. This was followed in September 2021 by the creation of the Health Emergency Preparedness and Response Authority (HERA) (European Commission, Directorate-General for Health and Food Safety 2021). HERA was tasked with managing cross-border health threats and addressing Europe’s strategic dependencies on essential health-related goods, including medicines.

Since March 2022 the European Medicines Agency (EMA) has assumed expanded responsibilities to prepare for, prevent and manage public health emergencies. These include monitoring and reporting on medicine shortages. Within the EMA, the Medicines Shortages Steering Group was established to oversee supply and demand across the EU through a harmonised system for tracking shortages, export bans and manufacturer withdrawals.

Recognising the growing risk of disruptions to pharmaceutical supplies, in October 2023 the Commission proposed stronger coordination among national authorities (European Commission 2023). One key recommendation was publishing a list of essential medicines for which the EU must ensure a continuous and secure supply.

In December 2023 the EMA published the first Union List of Critical Medicines. These medicines consist primarily of the APIs used to treat serious conditions, often with limited or no therapeutic alternatives. The list includes mainly generic medicines across a broad range of therapeutic areas, including antibiotics. It is updated annually and currently contains 276 critical medicines. Once a medicine is designated as critical, it becomes essential to assess the vulnerability of its supply chain, that is, the weaknesses in production, sourcing or distribution that increase the risk of disruption. The goal is to identify potential risks so that appropriate EU-wide measures can be implemented to strengthen the supply chain and ensure resilience.

Building on this initiative, the European Commission published the first assessment of supply chain vulnerabilities for an initial set of 11 critical medicines 6 (HERA 2024). This pilot assessed factors such as the EU’s industrial capacity, supplier diversification, market concentration and demand predictability. However, it also revealed significant limitations such as the absence of a robust legal basis for data collection and information sharing.

To further improve the governance of pharmaceutical supply resilience, the Critical Medicines Alliance was launched in April 2024 7 to analyse the supply chains of medicines listed by the EMA as critical, identifying excessive dependencies, limited diversification and capacity constraints.

Alongside new governance measures aimed at strengthening the supply of critical medicines, in March 2025 the European Commission (2025) proposed a regulation—dubbed the Critical Medicines Act (CMA)—to enhance the availability of critical medicines within the EU. The CMA also seeks to improve access to certain medicines of common interest that are affected by market failures.

The following sections present the key characteristics of the specific objectives of the proposed CMA, accompanied by our comments.

Vulnerability: a (supply) chain is as strong as its weakest link

With the proposed CMA, the EU aims to reduce its exposure to shortages of medicinal products through the diversification of supply sources and investment in local production. Regardless of the strategy adopted, understanding the complexity of pharmaceutical supply chains is essential.

Behind every medicine lies a supply chain spanning multiple stages. Finished pharmaceutical products—such as tablets, injectables and creams—comprise APIs and excipients. APIs are synthesised from intermediates that undergo several chemical or fermentation steps. These intermediates, in turn, are derived from basic chemicals (e.g. solvents, reagents and acids), natural extracts (e.g. plant derivatives) or biological materials (e.g. enzymes, cultures and tissues used in biotech medicines). Every link in this chain can become a point of vulnerability if disrupted. The supply of many of these inputs is highly concentrated, often in specific countries or at specific sites, leading to potential vulnerabilities in the pharmaceutical supply chain.

For example, consider a strategy of diversifying imports of critical medicines—also shaped by geopolitical factors—by increasing reliance on India to reduce dependence on China. The CPA (2025, 30) explains that, although India is the second-largest exporter of many medicines and APIs after China, it remains heavily dependent on Chinese imports for raw materials and APIs. As a result, such diversification may be less effective than initially assumed. This is why the Critical Medicines Alliance (2025, 10) argues that, to strengthen supply chain resilience and flexibility, financial incentives should prioritise projects that integrate multiple tiers of the pharmaceutical supply chain. These efforts aim to ensure continuity of supply and support the creation of industrial consortia of manufacturing sites strategically distributed across the EU, involving diverse regions and member states.

Moreover, evidence in the pharmaceutical sector shows limited short-term capacity to change the geography of sourcing (OECD 2025, 33), due to constraints such as legacy investments in manufacturing facilities and supplier relationships, lengthy regulatory approvals, intellectual property complexities and a lack of alternative suppliers. Greater flexibility is expected in the longer term. Foreign direct investment trends show, in fact, that companies are adjusting their supply strategies. Since 2022 there has been a notable shift in production-focused investments towards destinations that are geographically and geopolitically closer, indicating that pharmaceutical firms have begun adopting strategies to minimise risk and to enhance supply chain resilience (OECD 2025, 34).

International trade agreements and other forms of cooperation, as envisaged under the CMA, can play a key role in supporting the redesign of the geographic structure of medicine supply chains.

Financial support for innovation and manufacturing

One of the main factors behind recent medicine shortages is the decline in the production of generic drugs within the EU, driven by low profitability, high capital investment requirements, rising energy costs and stringent environmental regulations. To address these challenges, the EU should adopt an industrial policy that supports both process and product innovation.

As far as process innovation is concerned, according to the CPA (2025, 110–116), several enabling technologies can support the efficiency of generics production: green chemistry, which emphasises the use of non-toxic solvents and renewable raw materials; flow chemistry, which employs microreactors to enhance scalability and process control compared to traditional batch production; photochemistry, which uses light to catalyse chemical reactions; and artificial intelligence, which can optimise processes from early stage R&D through to manufacturing control.

For product innovation, funding should be directed towards the development of medicines that rely on shorter, more resilient supply chains. A particularly promising area is biotechnological drugs, or biologics, which are derived from living cells such as bacteria, yeast or mammalian cultures. These advanced therapies play a vital role in high-impact therapeutic fields, including oncology, immunology and rare genetic diseases (CPA 2025, 109).

In addition to financial support, the proposed CMA emphasises the importance of streamlining national permitting procedures for new manufacturing facilities and the expansion of existing ones. Nonetheless, even though modern pharmaceutical manufacturing can be environmentally friendly and aligned with EU ‘green’ legislation, such projects often face local opposition—commonly referred to as the NIMBY (‘Not In My Back Yard’) phenomenon.

Human capital remains a critical driver of innovation in the pharmaceutical sector, even in an era increasingly shaped by artificial intelligence and robotics. 8 However, the European API industry faces significant challenges in attracting qualified professionals, such as chemists and biotechnologists. In contrast, India and China have made substantial investments in education and benefit from favourable demographics, providing a large pool of young, cost-effective talent for API R&D. To remain competitive, Europe must preserve and strengthen its solid scientific foundation by fostering deeper collaboration and integration between universities and industry.

Collaborative procurement, not just for the cheapest supplier

EU health systems have increasingly relied on generic medicines, prioritising procurement based on the lowest price to reduce pressure on national healthcare budgets (Critical Medicines Alliance 2025, 4). However, when supply depends on a single supplier, the pursuit of efficiency can expose vulnerabilities and undermine resilience. Therefore, the CMA advocates for procurement rules based on the Most Economically Advantageous Tender, which goes beyond simply selecting the lowest-cost option. The Most Economically Advantageous Tender incorporates additional factors that enhance supply chain resilience, such as stockholding obligations, a diversified supplier base, contract performance clauses ensuring timely delivery and contingency measures for potential delays. Where appropriate, national procurement procedures should also adopt multi-winner approaches and consider the extent to which a medicine’s supply chain is located within the EU. Furthermore, since fragmented national procurement practices often lead to less favourable contract terms, the proposed CMA supports the development of collaborative procurement mechanisms, building on the successful experience gained during the Covid-19 pandemic.

EU solidarity in the supply and demand of critical medicines

The CMA encourages action on both the supply side (manufacturing) and the demand side (procurement). To avoid inequalities between EU member states, the principle of solidarity should be made effective on both fronts, ensuring that countries with production capabilities and strategic stocks can support those without.

On the supply side, although the CMA regulation references the use of state aid, such measures must be applied judiciously. It is neither feasible nor desirable for every member state to scale up the production of vulnerable medicines independently. From an industrial perspective, the production of generics depends on economies of scale, which are viable only within a market larger than any single EU country; otherwise, the EU risks inefficient overcapacity. From an equity perspective, member states differ in their fiscal capacity to provide state aid, due to differences in debt-to-GDP ratios and borrowing costs, leaving some countries at a disadvantage when it comes to investment. For this reason, the Critical Medicines Alliance (2025, 12) recommends leveraging the Strategic Technologies for Europe Platform 9 to channel investment towards essential pharmaceutical capabilities across the EU.

On the demand side, some EU countries may be negatively affected by an unequal distribution of critical medicines across borders, often as a result of national procurement requirements. This issue is frequently linked to the widespread use of contingency stock obligations, which require suppliers to maintain reserves of critical medicines for national use. Because these reserves are typically restricted to domestic consumption, they can limit exports to other member states in need.

As a partial solution to the risk of inequitable access within the internal market, the CMA proposes collaborative procurement, such as arrangements through which the European Commission procures certain medicines on behalf of, or in the name of, the member states. However, participation in such joint procurement initiatives remains voluntary. As long as one or more member states do not participate in these joint initiatives, a structural vulnerability persists, undermining the resilience of the EU as a whole.

Environmental policy and generics pricing

In addition to the proposals outlined above, the EU must address inconsistencies between EU and national legislation that can unintentionally exacerbate medicine supply issues, as illustrated by a case reported by Müller (2025).

Metformin, a first-line generic treatment for type 2 diabetes, is at risk of reduced availability due to new environmental compliance costs. The Urban Waste Water Treatment Directive (European Parliament and Council 2024) mandates advanced treatment of wastewater to remove micropollutants, including pharmaceutical residues. Under the directive, pharmaceutical manufacturers are required to cover at least 80% of the cost for this additional treatment stage.

Because metformin is excreted largely unchanged in urine, its environmental footprint is significant. However, in EU member states where generic drug prices are strictly regulated and cannot be increased, manufacturers cannot recover the added environmental costs. As a result, metformin could become economically unviable and thus unavailable in certain markets, forcing patients to turn to more expensive alternatives. This risk extends to other critical medicines as well, such as amoxicillin, used for bacterial infections, and tamoxifen, used in the treatment and prevention of breast cancer.

Conclusion: it won’t be cheap

The regulation proposed by the European Commission in March 2025—the CMA—marks the latest step in the EU’s strategy to strengthen the availability of critical medicines. After decades of prioritising efficiency, the focus must now shift towards resilience, that is, developing supply chains that can better withstand future shocks.

Yet, enhancing resilience comes at a cost. Any policy aimed at reducing the risk of supply disruptions for critical medicines will inevitably lead to higher expenses. Abandoning the just-in-time model in favour of just-in-case stockpiling entails upfront procurement costs and greater spending on storage (Masters and Edgecliffe-Johnson 2021). Diversifying supply sources often means sacrificing economies of scale, which are particularly significant in the pharmaceutical sector. Rebuilding domestic production capacity will face challenges, especially due to the higher labour and energy costs within the EU compared to those in the traditional supplier countries. Ultimately, these measures will impose financial burdens on citizens, either as patients, through higher drug prices, or as taxpayers, through increased public spending. Nonetheless, these additional costs could be largely offset by improvements in public health outcomes.