Abstract

The EU does not suffer from a lack of ambition on digital policy. From ‘strategic autonomy’ to ‘technological sovereignty’, European leaders like to portray the EU as a geopolitical heavyweight on digital. In practice, however, the European digital single market continues to be exposed to many of the fundamental challenges that have plagued it since its inception. The ongoing European effort to draft the global rulebook on tech regulation remains a laudable endeavour, but this has contributed little to boosting the competitiveness of the European digital sector. Many European tech companies still struggle to offer their services outside of national borders and expand their reach to a genuinely European customer base. The EU must tackle inconsistent regulations, close infrastructure gaps, promote investment, and facilitate secure, yet speedy data flows. These issues are integral to helping to turn the digital single market into a tech hub for global business. This article puts forward a number of policy proposals for upgrading the European digital agenda as one of the main conduits for ensuring European economic growth and improved global standing.

Keywords

Introduction

Digital laggard. Slow to innovate. Analogue. In recent years, the EU has received its fair share of unappealing descriptions. From the low number of digital unicorns to the limited availability of venture capital, the EU always seems to be ‘catching up’. While this cynical view has at times been over-exaggerated by the media and the lobbying networks of third-country competitors, the old continent is indeed punching below its weight in the digital sector. This has not always been the case. For decades European companies were at the forefront of innovation and vital to the supply chains of the global market. State-of-the-art research initiatives and a highly specialised workforce pushed scientific frontiers and gave the EU the confidence of one of the technological leaders of the twenty-first century. However, since the global financial crunch and ensuing eurozone crisis, the EU’s digital clout has started to dwindle. Ruthless (and at times even unfair) competition from North America and South-East Asia has become an additional challenge for European competitiveness.

The European digital tale is a mixed bag of notable success stories, complex challenges and missed opportunities. If one is looking for the main flaw of the Union, the problematic Gordian knot, the answer lies in the lack of scale. The digital single market of more than 400 million Europeans continues to be fragmented, split along state borders, and handicapped by both the conflicting interests of national champions and regulatory protectionism. Even though it has all of the necessary basic ingredients, the EU’s digital ambition cannot flourish enough to become one of the main vehicles for increased economic growth and prosperity across the continent.

To its credit, the EU has tried to solve some of the most pressing issues in the digital realm when it comes to protecting user privacy, safeguarding fair competition and setting out a comprehensive approach to digital governance. Europe has become the international trend-setter and pioneer of innovative legislation for the online realm. However, European policymakers cannot rest only on these laurels. If the EU has managed to construct a digital backbone for online governance through the likes of the General Data Protection Regulation (GDPR), the Digital Markets Act and the AI Act, a new impetus is needed for the upcoming European Commission mandate. The EU needs to put flesh and bulk on its digital skeleton; more meat on the bone is needed if the Union is serious about keeping its position among the international heavyweights in the age of great-power competition.

This article takes stock of certain key indicators when it comes to relevant legislation for the online domain and the overall tech track record of the EU. The text proceeds with a number of suggestions for the collective upgrade of the European digital single market to improve its competitiveness and resilience. The article is part of the Wilfried Martens Centre’s ‘7 Ds for Sustainability’ initiative which provides strategic policy proposals for the European centre–right (Hefele, Welle et al. 2023).

The state of (digital) affairs

The contemporary debate on European digital clout gets easily boxed in by narrow assumptions about the lack of European big tech giants (e.g. ‘Why is there no European Google?’) or the increasing supranational legislation for the online domain (‘Too much tech regulation will kill the future European digital industry’). In order to get the proper pulse of the European digital market, such premises need to be put in the proper perspective. Additionally, we should assess several other key indicators of the EU’s technological competitiveness.

Tech legislation

From a macro perspective, the institutional logic of the EU’s digital agenda follows an inherent policy purpose. Europe has tried to integrate the values and regulatory levers of the continental social market economy into the online space. In essence, this innovative legislation has tried to insert the state within the digital realm, setting up the regulatory arbiters that are essential for fair competition. Most importantly, it aims to instil individual rights and responsibilities—providing a sense of order and predictability within the chaotic online domain.

In 2016 European member states agreed on the first comprehensive framework to protect European citizens’ personal privacy and sensitive data online (the GDPR). This was followed by a twin effort to make sure that offline rules apply to the online domain (the Digital Services Act) and that digital giants do not monopolise online competition at the expense of European businesses and citizens (the Digital Markets Act). In parallel, new rules are kicking in for trusted data management, while the EU institutions are also closing on the long-awaited framework for AI. In short, Europe has tried to put in place foundational guardrails for the digital economy which reflect its own tenets of humanism, open competition and the rule of law.

There are two main shortcomings to this otherwise laudable and truly European approach. First, the implementation of these rules may remain elusive. The GDPR has been a case study of good intentions and comprehensive norm-setting, but with restricted options for pan-European implementation. From the limited staffing or administrative resources given to national authorities, to the fact that certain data protection authorities are handling a disproportionate number of cases (Ryan and Toner 2020), much is left to be desired on enforcement. This is a cautionary tale for all of the new tech regulations currently in the making.

Second, setting up global tech standards requires not only ambition and legal wit, but also a position of strength. Promoting the global rulebook does not guarantee the EU a place around the winners’ table. The widely discussed ‘Brussels effect’ of Europe influencing the international tech and business environment through regulation (Bradford 2020) holds true only as long as the European market can leverage its global share and economic clout. Brussels likes to see itself as the global referee on tech, but this will count for little if the EU does not also ensure its global competitiveness.

Competitiveness, skills and infrastructure

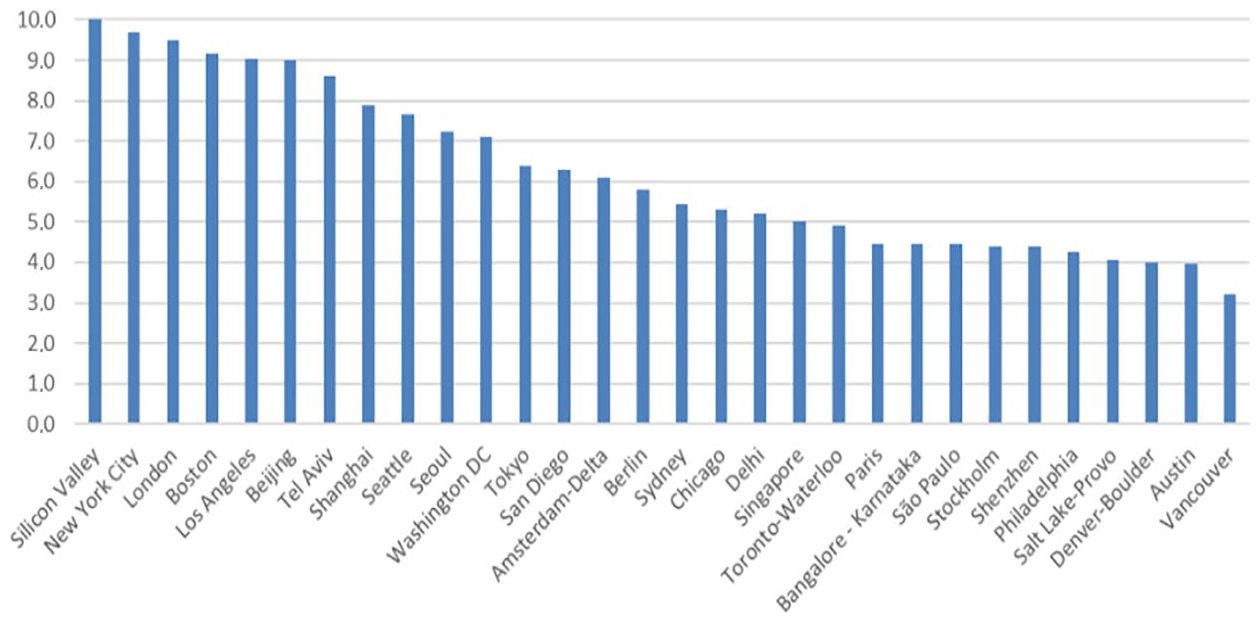

Looking more closely at a number of key indicators of the EU’s digital competitiveness brings about a sense of concern, rather than optimism. Only 2 of the top 20 largest tech companies in 2022 were European (Ponciano 2022). This negative trend does not only hold true in terms of digital giants with billions of euros of revenue, but is also replicated when we zoom in and explore the European start-up scene. Among the top 30 global cities with the best start-up ecosystems (Figure 1), there are only four European capitals (Berlin, Amsterdam, Paris and Stockholm).

Global start-up ecosystem ranking 2021.

Out of the dozen most valuable unicorns globally, the top five are based in the US, with another four in China, and none in the EU (European Commission 2020, 58). Тhe comprehensive Digital Economy and Society Index report for 2022 concludes that one of the most important factors for boosting Europe’s start-up track record is ‘exploiting the full potential of the EU single market and overcoming the persisting legal and economic barriers between EU Member States’ (European Commission 2020, 61). This recommendation could improve the potential success rate not only of early stage companies, but also of traditional small and medium-sized enterprises and the European financial technology sector (Kuzmanova 2020).

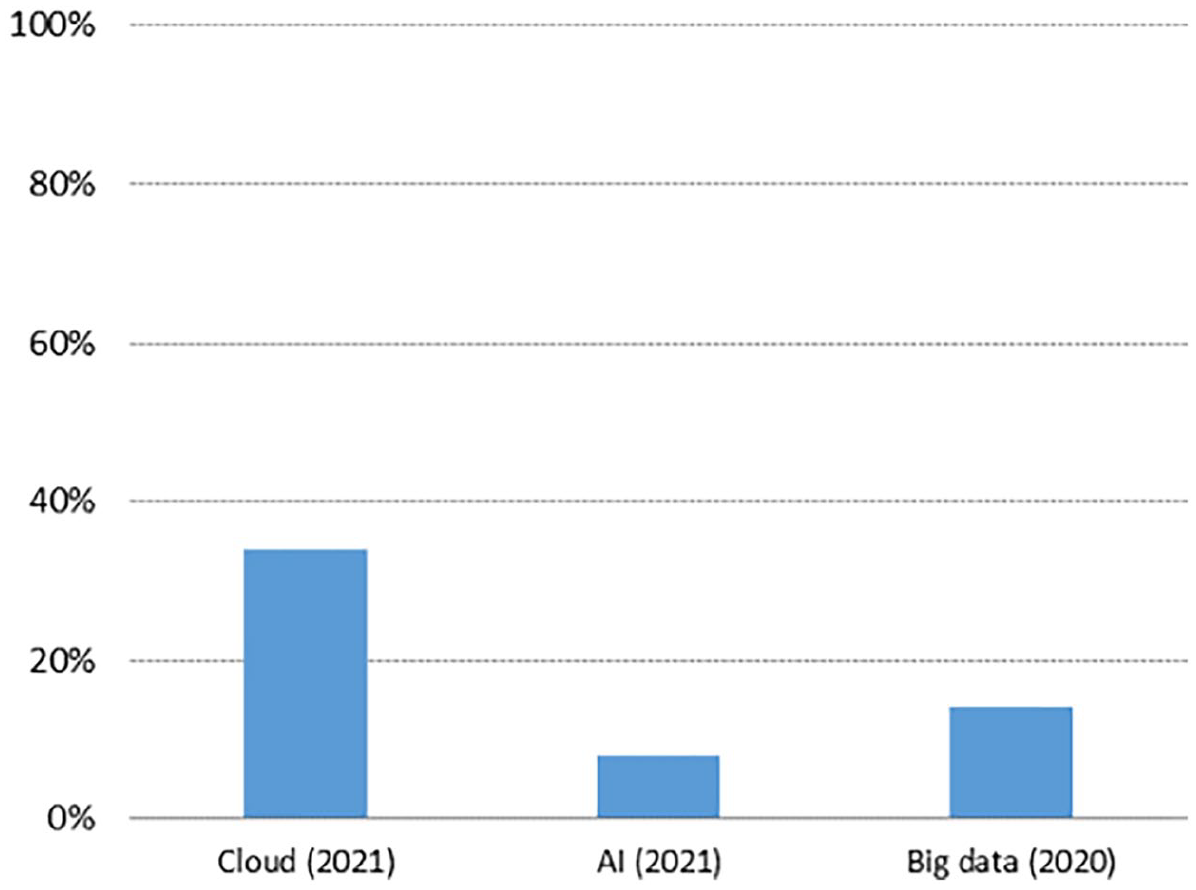

Looking beyond digital unicorns or start-up ventures, the digital credentials of existing European companies at large is far from impressive. The latest available pan-EU official data on the adoption of advanced technologies such as AI or big data as part of the operations of European enterprises show a dismal performance (Figure 2). In numerous instances companies lack the finances, labour force or operational resolve to implement innovative digital technologies in their workflows.

Adoption of advanced technologies (% of enterprises) in the EU, 2020/21.

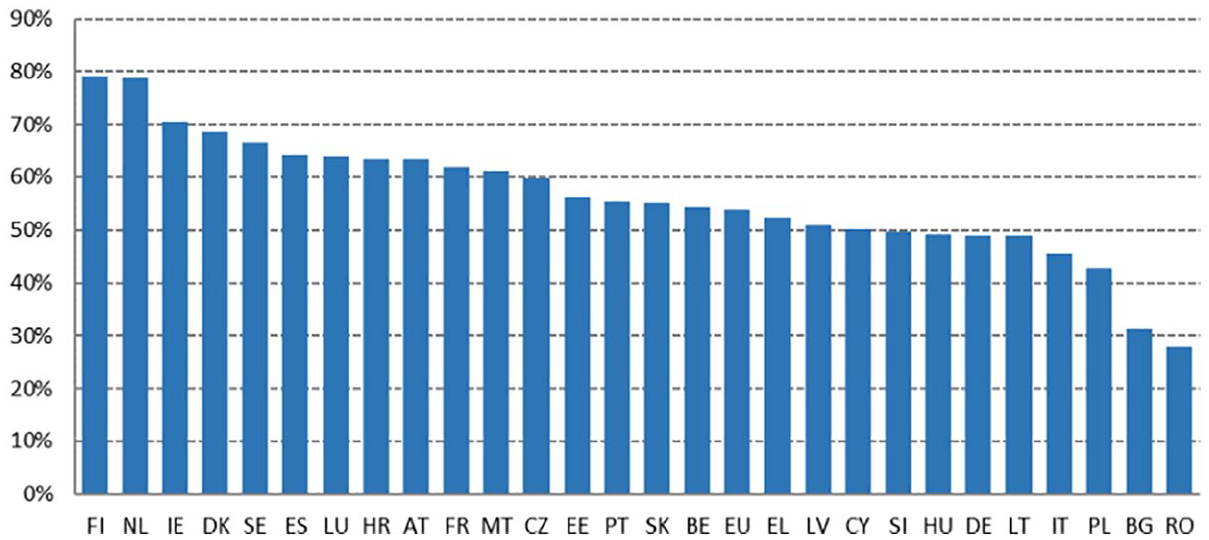

This trend is exacerbated by the fact that there is still a shortage of properly qualified information and communications technology (ICT) specialists across the EU. More than 60% of European companies reported that they had difficulties filling ICT vacancies (Eurostat 2023). Unfortunately, this might become an embedded problem as the basic digital literacy of European citizens is rather average. This is not only about geographical inequalities or illustrative of an East–West divide, though. Countries such as Germany and Italy register some of the most unsatisfactory results overall (Figure 3).

Percentage of individuals having at least basic digital skills, 2021.

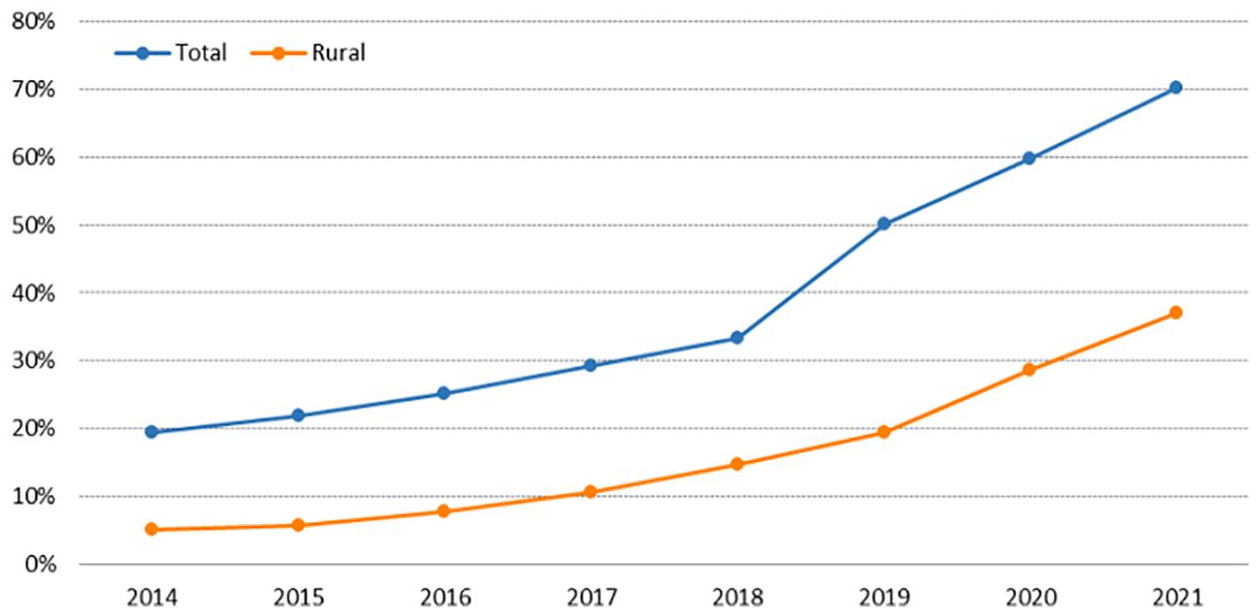

Digital infrastructure is another key indicator which must be considered. While the whole continent has full broadband coverage, only about 70% of households have the necessary connectivity to receive gigabit speeds (Figure 4). More worryingly, there is a clear divide between urban and rural areas, where these numbers drop precipitously. In parallel, the EU is proceeding only slowly with the rollout of 5G as the national spectrum-assignment procedures are sluggish (Myers 2023).

Fixed very high capacity network coverage (% of households) in the EU 2014–21.

It is important to note that the EU is aware of these trends and shortcomings. The current European Commission has launched a highly ambitious digital agenda for 2030, alongside a number of financial vehicles devoted to digitisation. The Digital Decade policy programme puts forward a number of targets for digital skills, connectivity, infrastructure, semiconductors and key public services. The success of this programme could unlock at least €1.3 trillion in economic value by the end of the decade (Randery 2022). The EU has also not shied away from designating considerable resources for this endeavour. At least 20% of the European Recovery and Resilience Facility mechanism funds have been earmarked for digital investments. More than €120 billion has been dedicated to reforms and investment through grants and loans in the next several years. European leaders have also dedicated €43 billion to bolstering semiconductor capacities and critical supply through the EU Chips Act.

Upgrading the digital single market (2024–9)

Completing the European digital single market is becoming an essential prerequisite for maintaining the EU’s global competitiveness in the years to come. What is more, the European digital agenda is directly tied to the EU’s growth prospects and opening up new employment opportunities across the continent. If the EU does not revive its drive for technological leadership and digital strength by effectively pooling and expanding its resources, it will find itself dwarfed by North America and Asia. This would threaten the geopolitical relevance of the EU and be a heavy blow to the economic prosperity of its citizens. A comprehensive push in several vital directions is needed for the upcoming European Commission mandate.

Software

If the previous decade was devoted to pioneering innovative legislation for the digital domain, now comes the time for implementation and the filling of important gaps. The next five years should be about deepening rather than widening. The EU will need to implement extremely ambitious pieces of legislation, such as the Digital Markets Act, the Digital Services Act and the AI Act, which will require an innovative approach to supranational enforcement and put an additional strain on the Commission’s staff and internal operations. This will be the ultimate test of whether the EU is indeed serious about operating a successful quasi-federal framework for the digital realm and therefore moving beyond being an aspirational paper tiger.

Additionally, the Commission should deliver on the fundamentals of the digital single market—creating the best conditions for facilitating public/private investment, overcoming fragmentation and reducing the bureaucratic burden for European business. Less is more, and the European Commission should follow up on its Better Regulation agenda in order to simplify and streamline the bulky red tape which is especially stifling for small and medium-sized enterprises and innovative companies. Legislative complexity and legal uncertainty need to be reduced. The completion of the European Capital Markets Union (CMU) is long overdue and a new impetus is needed to finally create a single market for capital and easier cross-continental investment. Accelerating and facilitating access to funding, streamlining existing EU funding, and targeting both at mature technologies, clean tech and cutting-edge innovation should become pressing priorities (Chivot 2023).

Additionally, the EU needs to expand its efforts to deliver a series of digital products which could be beneficial for the everyday lives of European citizens. Initiatives such as the European Health Data Space or an EU e-identity service should be developed in close cooperation with national authorities, alongside a long-term comprehensive effort to improve basic digital skills.

Hardware

Improved digital connectivity, together with secure infrastructure, is an additional priority area. The EU should follow up on its commitment to ensure high-speed digital connectivity across the continent, with a special focus on rural areas. There are visible digital divides which need to be overcome. The financial vehicles that are part of the EU’s cohesion policy, the Recovery and Resilience Fund, and the Connecting Europe Facility provide vital opportunities for boosting overall connectivity. Additionally, expansion of 5G infrastructure coverage to all populated areas should be accelerated, while the hardware and maintenance service should be provided by trusted vendors. Given the strategic importance and national security implications of such infrastructure, the EU should double down on its efforts to implement the 5G Toolkit and continue to prevent high-risk vendors 1 from becoming embedded in such services.

Even though the EU continues to have a stake in the design and manufacturing of semiconductors, the continent still faces setbacks when it comes to fabrication technologies and next-generation chip design (European Commission 2021, 6). European member states should improve their cooperation on semiconductors in order to both increase the EU’s overall share in the global market and guarantee the sufficient supply of advanced chips, which will be vital for consumer electronics, next-generation vehicles and AI-powered technology. Ensuring the secure supply of vital rare-earth elements and components through boosted domestic production and expanded imports from trusted partners also needs to be high on the agenda.

The Commission should additionally encourage further spillovers and sharing of resources to boost the EU’s cloud ecosystem and expand joint efforts in quantum technologies. What is more, the EU should elevate its digital ambition and explore ways of pooling joint resources, technical capacity and human resources in an advanced European research unit dedicated to supporting the EU’s long-term competitiveness in the fields of innovation, industry and defence. A European DARPA 2 should not remain an aspiration, but become a practical reality in the late 2020s. The geopolitical relevance of the EU will be directly linked to its technological leadership and industrial strength in the years to come.

Cyber resilience, deterrence and opposing digital authoritarianism

Cyber resilience is an extremely important, but still under-developed branch of Europe’s collective digital agenda. Going beyond the basic notion of ‘cybersecurity’, the Union needs to ensure that it has the necessary digital defensive capabilities within its borders and is also able to deter the offensive operations of hostile third-country actors and their proxies. EU member states and supranational institutions need to strengthen the necessary legal framework and response mechanisms to protect Europeans from cyber-attacks, compromised online privacy and vulnerable personal devices, as well as illicit tracking and surveillance. The mass-market penetration of affordable foreign (often Chinese) interconnected Internet of Things (IoT) devices may be beneficial for European users but also carries potential vulnerabilities.

The EU needs to finalise progress on the Cyber Resilience Act and expand its efforts on the bolstered cybersecurity requirements for software and hardware products. In 2020, the EU invoked its cyber diplomacy tools for the first time and imposed sanctions against Russian and Chinese individuals for conducting malicious cyber-attacks. The EU must stand ready to counter such malicious behaviour in cyberspace and have the necessary mechanisms to prevent, deter and respond to external threats in the digital domain. Closer transatlantic cooperation to meet these challenges is needed, together with an extension of NATO’s capabilities in defending Allies in cyberspace.

The EU is facing growing challenges in the field of technology and digital policies from the People’s Republic of China. The country is developing a unique model of neo-mercantilist techno-nationalism, which goes against the principles of free trade, open competition, and respect for international law and intellectual property (IP) rights (Lilkov 2020). European businesses have continuously suffered from intellectual property theft, cyber-attacks and being deterred from accessing the Chinese markets. If the EU is dedicated to the concept of strategic autonomy it should find ways to strengthen its export-control mechanisms and limit the export of sensitive technologies, which could undermine European technological leadership or be used for authoritarian purposes and directly against fundamental human rights.

The EU and its sovereign member states should boost national and collective efforts on investment screening in the field of key technologies. European member states should enforce the provisions for conflicts of interest and the transparency of funding sources when it comes to joint research or partnerships with Chinese individuals, researchers or academic institutions. Finally, the Union needs to bolster its arsenal by having the necessary supranational tools to sanction or fully ban malicious third-country applications that are acting as tools for foreign surveillance or political propaganda that go against the interests of European citizens.

Transatlantic partnership and international cooperation

When it comes to the international dimension, the transatlantic alliance remains a key pillar for Europe’s digital agenda. Some of the most pressing international issues, such as developing international technological standards, securing supply chains for advanced technology, curbing devastating cyber-attacks and implementing export controls on dual-use technological items with military applications, can only be tackled if Brussels and Washington maintain and enhance their ambitious partnership. In this regard the expanded EU–US Trade and Technology Council (TTC) could be a vital tool for pursuing an ambitious joint agenda and expanding bilateral trade, which currently surpasses €100 billion annually in digital goods and services. The TTC has already made progress on items such as trustworthy AI, supply-chain monitoring and joint standards for electric vehicles. An additional effort is needed to grow this joint agenda and turn the TTC into an expanded supranational mechanism for transatlantic deliberation and decision-making.

It is important to note that even though there are huge overlaps in EU–US interests in the digital sector, Europe pursues a different philosophy when it comes to privacy protection and digital market set-up. The TTC should not be used as a pressure point to water down European tech regulation. Additionally, EU–US tech relations have been hampered by a lack of trust when it comes to data sharing since the European Court of Justice stated in 2020 that the US does not provide sufficient guarantees for the protection of personal data coming from the EU (Lee 2020). The US needs to provide a viable and trusted mechanism that ensures that Europe’s provisions are being met.

On the international front, the EU needs to continue its landmark efforts to shape the golden standards on tech regulation and to partner with like-minded countries globally. There is a myriad of potential spillovers or joint interests which could be pursued in the fields of digital trade, infrastructure rollout and cybersecurity. Brussels should additionally boost its Global Gateway Strategy and deliver on its commitment to expand smart, clean and digital infrastructure in a number of partner countries. Efforts such as the EU–Asia Connectivity platform and the enhanced partnership with Japan in the field of digital services, transportation and energy should be strengthened and fully expanded to other countries. Similar ambitious and transparent initiatives should urgently be developed and implemented in Africa with partner countries.

Footnotes

Notes

Author biography