Abstract

Foreign direct investment (FDI) is widely welcomed as it can improve the standard of living in the recipient country. However, depending on the target sector and/or the nationality of the investor, FDI may pose a risk to national security; this is why some countries have adopted screening procedures. Since 2020 the European Commission has coordinated its member states in screening FDI, but not all EU members have national screening mechanisms in place. Moreover, those mechanisms that do exist are not homogenous, for example, in their identification of protected sectors. This incompleteness and heterogeneity are weaknesses that undermine the security of the EU due to the high level of integration within the single market.

Introduction

Foreign direct investment (FDI) is a cross-border capital movement that widens business opportunities and may increase the capital stock, the productivity and, ultimately, the standard of living in the recipient country. For this reason, many countries have reduced the legal obstacles to FDI and promoted it via bilateral treaties and the establishment of specific national agencies. However, to safeguard national security, countries may set conditions or prohibit some FDI, thus deviating from the obligations that arise under the treaties and agreements that promote international economic integration. In the context of capital mobility and increasing geopolitical tension, FDI screening has become a crucial policy in government agendas, especially in developed economies.

This article argues that, notwithstanding the benefits of coordination among member states delivered by the recent EU regulation on FDI screening (European Parliament and Council 2019), both differences in identifying risky FDI and the absence of certain states from this coordination may undermine the security of the EU due to the effectiveness of the European single market. The first section explains when FDI may pose a risk for national security. The second section describes the origins of the EU regulation and the third summarises the Commission’s first two reports on the regulation’s implementation. The fourth section indicates the main ‘between-the-lines’ explanation for the need for an EU-level screening regulation. The fifth section offers some concluding remarks on critical aspects of the current EU regulation.

The risks posed by FDI

Theodore H. Moran (2009) identified three potential threats to national security that might emerge from FDI. These are related to the ability of the foreign investor to (1) restrict or deny the provision of output from the newly acquired producer; (2) deploy or sell sensitive technology so as to be harmful to the national interest of the targeted country; and (3) penetrate the targeted country’s systems so as to monitor, conduct surveillance or place destructive malware within those systems.

When it comes to ‘national security’, countries enjoy substantial discretion in invoking this as a reason to deviate from international commitments. This is why some authors have dubbed the national security exception within the WTO a Pandora’s box (Boklan and Bahri 2020) and a black hole (Bacchus 2022).

In general, the protective shield against risky FDI is shaped to guarantee satisfaction of the physical and safety needs of the population, to preserve internal stability and to assure the sustainability of the national economy. Hence, the screening of FDI usually takes place when investors target infrastructure and goods that are relevant for defence, energy, transport, healthcare and other sectors that national governments may include in their industrial policy. Along with the sector, the authorities may consider the identity of the foreign investor relevant to gauge the potential risk of FDI: many developed economies, for example, include the country of origin of the investor among the relevant factors.

Without ex ante control of the FDI and an acknowledgement of the incompleteness of ex ante sectoral regulations, any ex post intervention—such as monetary sanctions—would be insufficient to restore the status quo ante or compensate for the damage already caused.

The rationale for an EU regulation

In the EU, FDI screening likely to affect national security or public order is a competence of the member states (see art. 4(2) of the Treaty on European Union; arts. 52(1) and 65(1b) of the Treaty on the Functioning of the European Union). However, in an integrated market such as the European one, the negative effects of unscreened or unapproved FDI in one country could extend to other countries. This is clearly the case when considering transnational networks such as railway lines, pipelines and power grids; for example, more than 15% of Europe’s power is traded between countries through cables called interconnectors, making it the world’s most interdependent region in terms of electricity (Hook and Thomas 2022). However, this may also be the case where there are strongly integrated regional value chains, and European value chains are more integrated at the regional level than those in Asia or on the American continent (Huidrom et al. 2019, 10). Hence, after its speedy approval, 1 in October 2020 a regulation establishing a framework for the control of FDI in the EU became fully applicable (European Parliament and Council 2019).

The EU regulation does not replace national FDI screening mechanisms but establishes a mechanism for cooperation between the Commission and the member states. With the regulation, the Commission assumes a coordination role but has no power to block non-EU FDI from coming into the EU. According to the procedure, the member state that is screening an FDI is obliged to notify the other member states and the Commission of this; they can then respectively provide a comment and an opinion on the operation. The final decision on whether to approve or prohibit the FDI is always up to the targeted member state. Only if the FDI is capable of affecting EU-funded projects (for example, the Horizon 2020 research programme or the EU4Health programme) or critical EU infrastructure (e.g. the Galileo satellite system or the continental Trans-European Networks; see European Commission and Parliament 2021) does the targeted country have to provide an explanation if its actions deviate from the recommendations in the Commission’s opinion (European Parliament and Council 2019, art. 8(1c)).

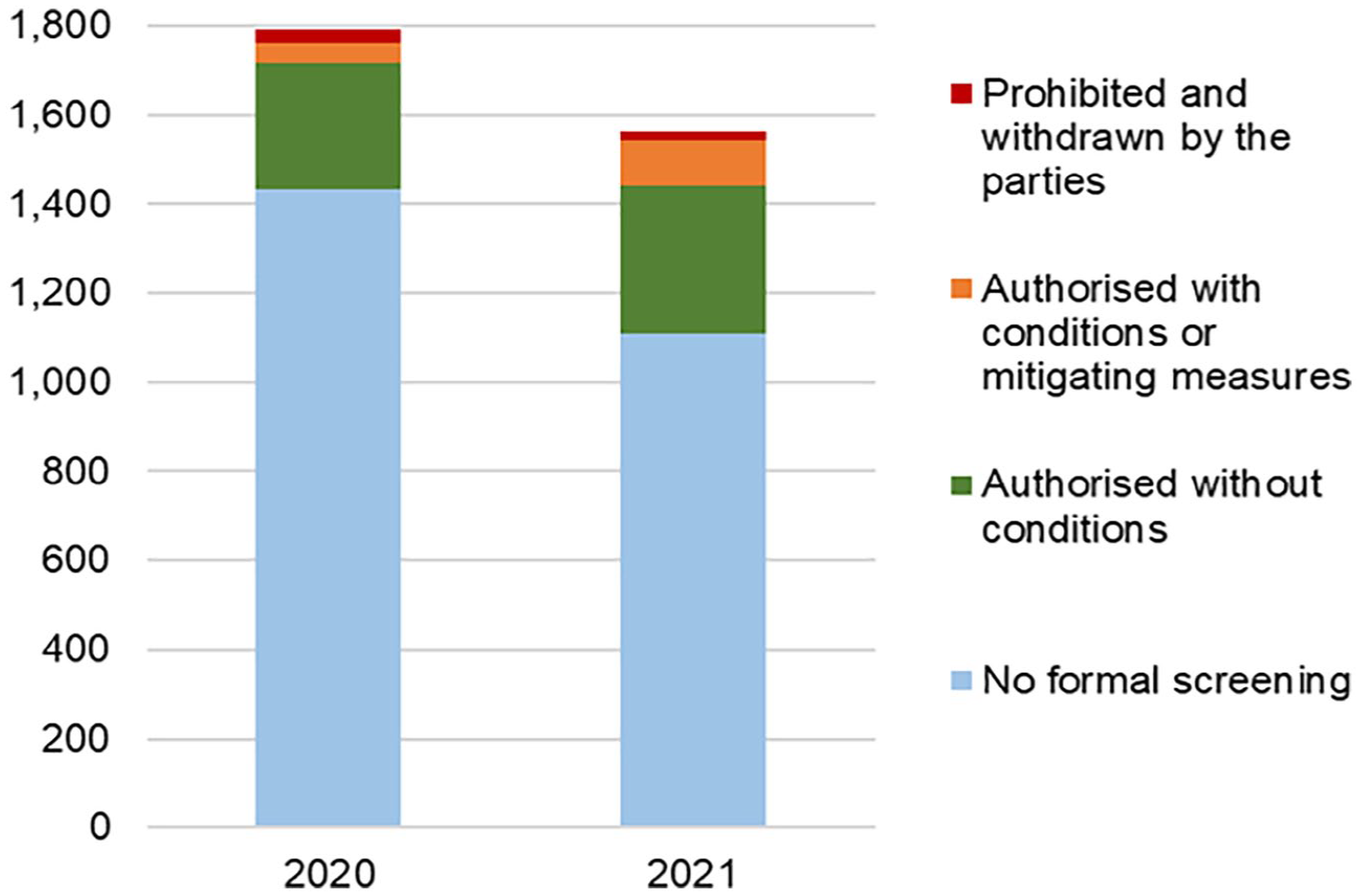

EU regulation: over 3,000 notifications in two years but few prohibitions

In 2020 and 2021 member states examined a total of 3,356 FDI dossiers under the procedure. In most cases, these dossiers were not subject to a formal check as they were not capable of affecting security or public order: this was the case for 79% of dossiers in 2020 and 71% in 2021 (Figure 1). Most of the dossiers subject to formal control were approved without conditions: 79% in 2020 and 73% in 2021. In 2021 23% of the cases subject to examination were approved with conditions. This was the case, for example, regarding the acquisition of a majority share in Engie EPS by Taiwan Cement Corporation. Engie EPS is an Italian subsidiary of the French company Engie. In light of this takeover bid, in 2021 the parties notified the Italian authorities, which then, in line with the EU regulation, informed the Commission and the other EU member states. The Commission, Belgium and France showed an interest in the transaction by requesting further information, but they refrained from passing comment or expressing an opinion. The Italian government approved the transaction but imposed specific requirements on the acquiring firm. The member states prohibited FDI in just 1% of notified operations in 2021 and 2% in 2020.

EU FDI screening: total notifications and type of decision.

These figures confirm, as the European Commission (2021a, 11) writes in its first report, that ‘Member States screening foreign investments, and the European Union at large, remain very open to FDI, intervening only in a very small proportion of cases to address deals likely to affect security or public order.’

The origin of the EU regulation

During the last three decades, the move towards globalisation has been punctuated by two waves of FDI protectionism. The first occurred in 2007 and 2008 2 when sovereign wealth funds increased their international purchases, mainly fuelled by high commodity prices and a record oil price. The second wave began in February 2017, 3 when the German, French and Italian governments sent a joint letter to the Commission proposing EU-level protection against FDI that threatens ‘public security and public order’, especially when it is ‘part of other countries’ strategic industrial policies’ and when ‘such investment is subsidised by state bodies’ (Germany, Federal Ministry for Economic Affairs and Climate Protection 2017). This triggered the legislative procedure leading to the EU regulation.

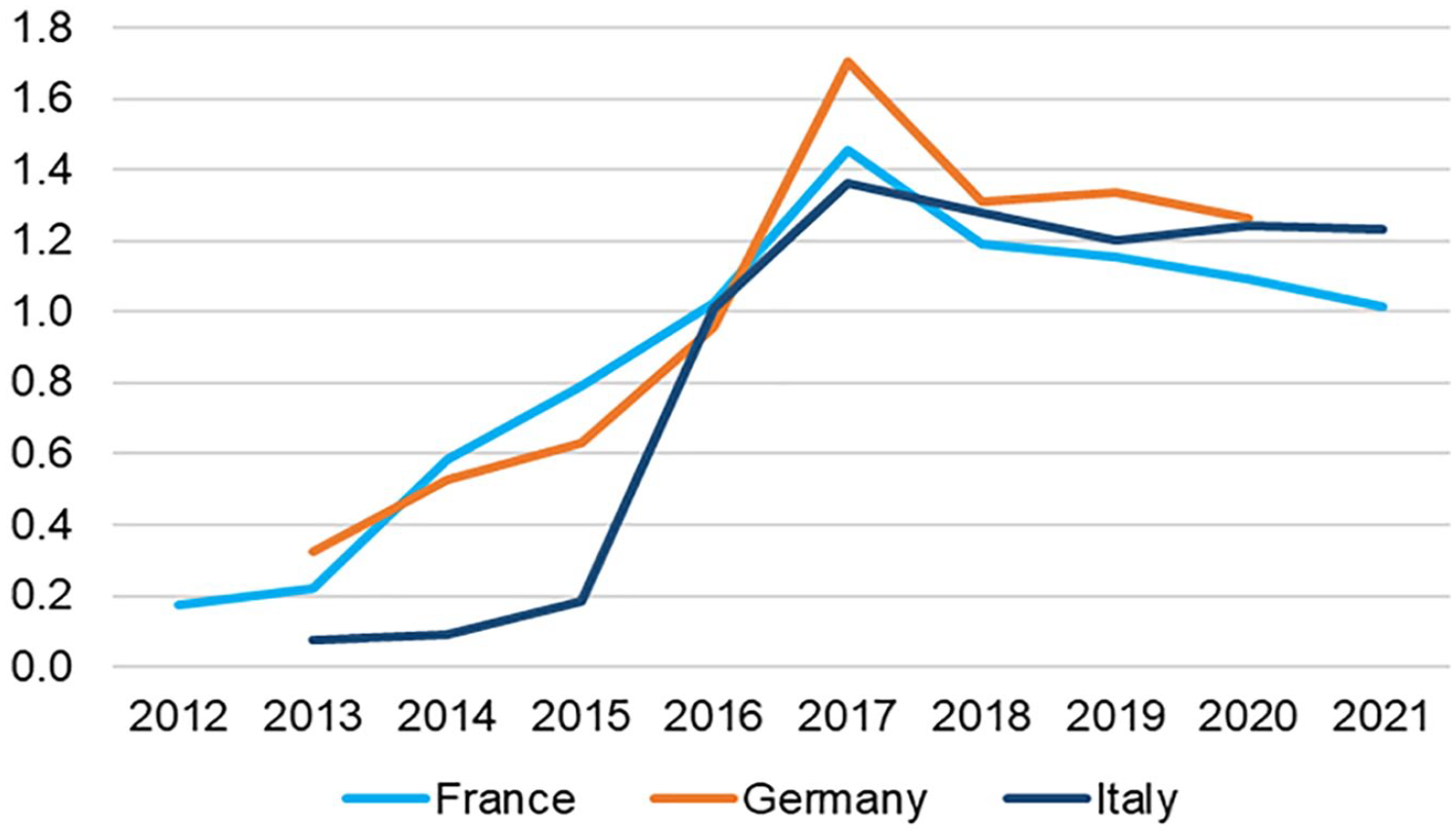

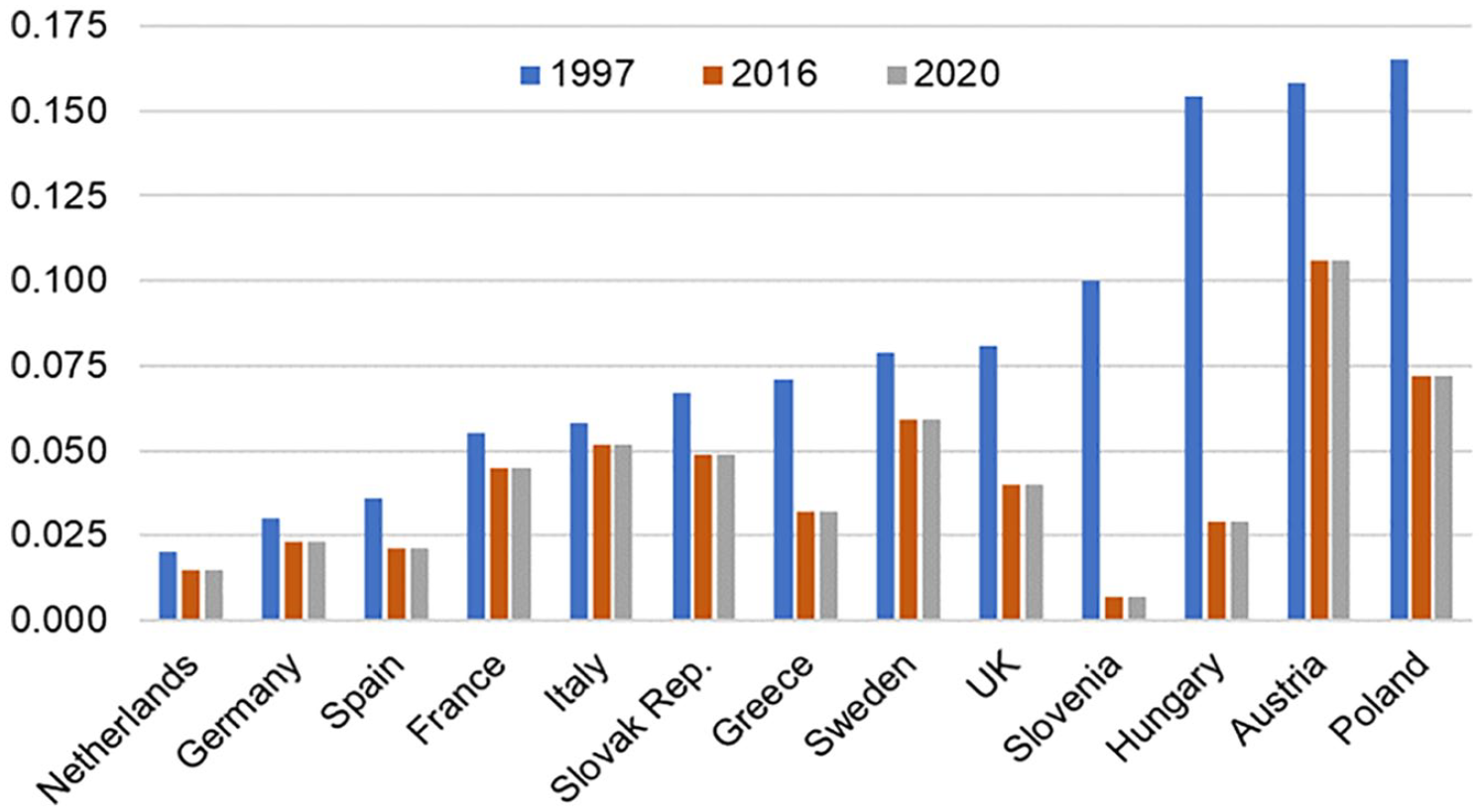

In 2017 China was the third largest economic power globally after the US and the EU27, and was scoring a series of impressive current account surpluses, building up a war chest for outward FDI (see Figure 2). It was making purchases in a context in which many European countries were becoming more open to FDI, as demonstrated by the reduction in their scores in the FDI Regulatory Restrictiveness Index 4 (see Figure 3).

FDI stock from China (% of total inward FDI).

FDI Regulatory Restrictiveness Index.

China’s upsurge in outward FDI has been instrumental to its ‘Made in China 2025’ industrial policy, announced in 2015, which includes investing in foreign firms with superior technology and know-how in order to transfer this back home with the aim of boosting Chinese competitiveness. This policy’s effectiveness is strengthened by China’s disputable market economy status (European Commission 2017, 16–17; USTR 2022, 14). The Chinese authorities have the power to drive state-controlled enterprises and to subsidise domestic firms in order to invest abroad. Moreover, the one-party system allows the Chinese authorities to undertake policies that have long-term expected rewards while sacrificing the short-term profitability of the controlled asset in a foreign country, even, for example, through a voluntary act of sabotage (Riela and Zamborsky 2020, 60–6).

Conclusion: towards a first assessment of the EU regulation

The initial review of the EU regulation will take place by 12 October 2023, when the Commission will evaluate its functioning and effectiveness and, if necessary, recommend amendments (European Parliament and Council 2019, art. 15). The OECD, entrusted with this job by the Commission, has already analysed the EU regulation over its first two years of implementation and has highlighted its strengths and shortcomings (OECD 2022). In the view of the Organisation, the EU regulation has ‘improved co-operation and co-ordination among Member States’ and ‘has allowed for better informed screening decisions’ (OECD 2022, 7). However, it also found that the EU’s procedures ‘result in delays, inefficient procedures, duplication of work, or tight timelines that strain resources and lead to unsatisfactory national screening decisions’ (OECD 2022, 7).

The OECD has extensively analysed the procedural aspects of the regulation, and this will inform the Commission’s forthcoming report. However, in these concluding remarks we focus on two aspects relevant to the EU’s economy and political model: the incompleteness and the heterogeneity of EU-level FDI screening.

Incompleteness: one-third of EU member states still have no operational framework for FDI screening

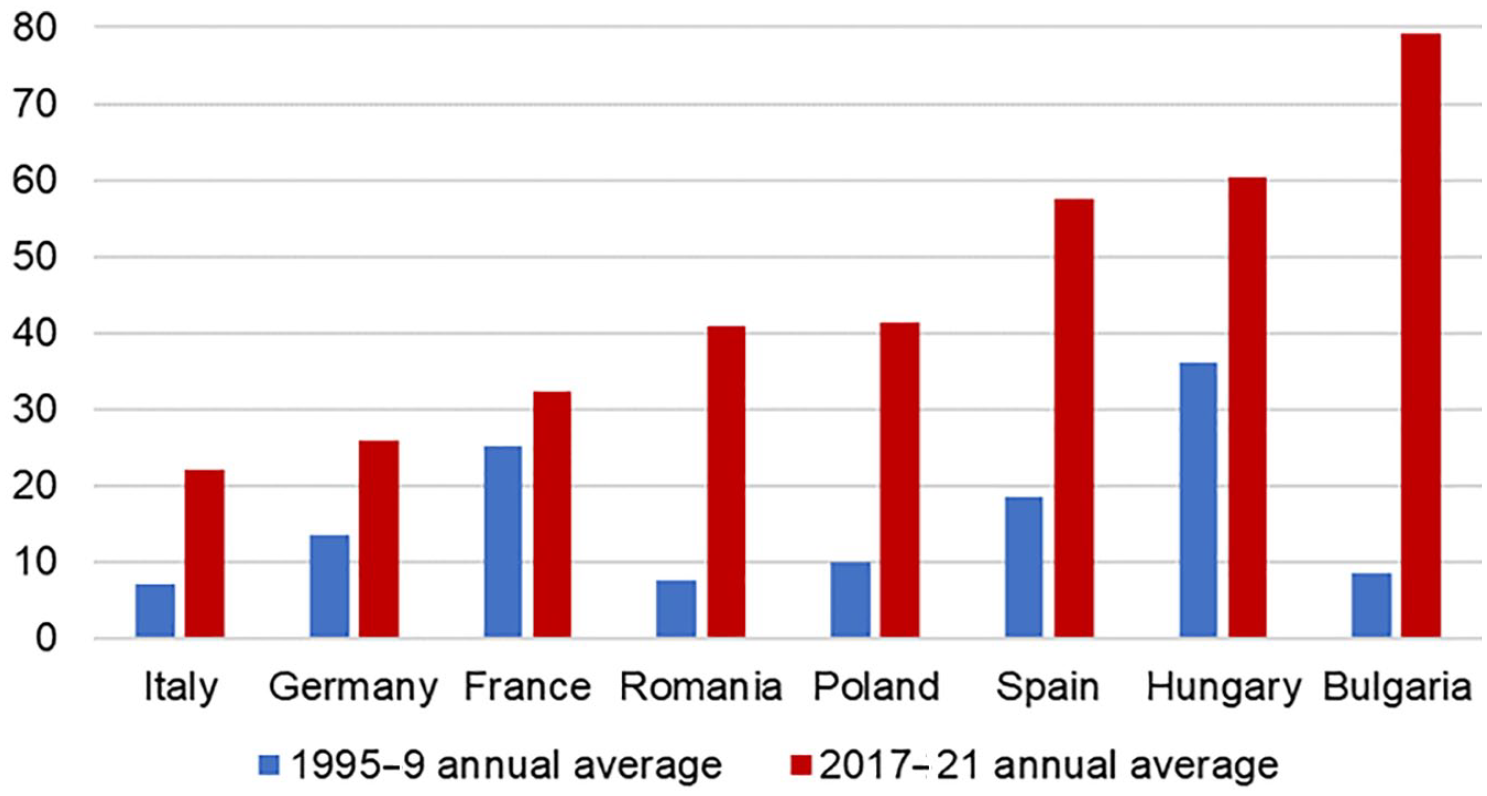

According to the Commission’s Second Annual Report (European Commission 2022b), 18 member states have a national FDI screening mechanism in force, 7 have a consultative or legislative process underway that is expected to result in the adoption of a new mechanism (Belgium, Croatia, Estonia, Greece, Ireland, Luxembourg and Sweden), and 2 have no publicly reported initiative underway (Bulgaria and Cyprus). The member states are free to decide whether they want to set up an FDI screening mechanism or to screen a particular FDI, but those with no screening mechanism in place are not obliged to notify the Commission of FDI within their territory. According to the OECD (2022, 18), reservations about screening inward FDI can be explained by the need some countries have to attract foreign capital. Figure 4 shows the variation in levels of FDI stock compared to GDP in some EU countries, which might explain the varying positions regarding FDI screening (UNCTAD 2023).

Inward FDI stock as a percentage of GDP.

Notwithstanding the sovereign competence in this policy area and the invitation to member states with a screening mechanism in place to prevent any form of circumvention (European Parliament and Council 2019, art. 3(6)), the Commission has repeatedly invited all member states to put a national screening mechanism in place. This has been in guidance published at the onset of the Covid-19 pandemic (European Commission 2020, 2), in the Trade Policy Review (European Commission 2021b, 21) and again in guidance published after Russia’s invasion of Ukraine (European Commission 2022a, 3). The latter stressed that setting up and enforcing a fully fledged FDI screening mechanism ‘is all the more urgent in the current context’ (European Commission 2022a, 3).

Heterogeneity: EU members with a national FDI screening mechanism do not necessarily protect the same sectors

With each wave of protectionism, governments have widened the number of sectors protected from FDI. However, by overstretching this protective shield, governments might obstruct efficiency improvements, trigger retaliatory protectionism by other countries or structurally reduce the value of protected firms (Matucci 2020, 21–2). Notwithstanding this widespread trend, it is not guaranteed that EU members are converging on a homogenous model, as member states do not necessarily protect the same sectors. The EU cannot interfere with member states’ competences and the regulation merely suggests a list of sectors in which countries ‘may consider’ evaluating the effects of FDI (European Parliament and Council 2019, art. 4(1)). These include energy, transport, water, health, safety (from food to cybersecurity), defence, aerospace, data, media pluralism, electoral and financial infrastructure, and technologies such as artificial intelligence, robotics, semiconductors, nanotechnologies and biotechnologies (European Parliament and Council 2019, art. 4(1)). Moreover, a country-based approach is also preferable because national economies have experienced specialisations due to the effectiveness of the four fundamental freedoms of the European single market (Mongelli et al. 2016, 29–34).

The alarm that triggered the adoption of the EU regulation for FDI screening seems to have stopped ringing, as FDI from China has stabilised in value (Figure 2). However, the incompleteness and heterogeneity of EU-level FDI screening may yet become a problem, especially in the context of geopolitical tensions that have led US Treasury Secretary Janet Yellen to call for a reshaping of trade relationships around ‘trusted partners’ (Yellen 2022). As in trade, where the EU member states decided from the very beginning to speak with one voice and act together in a customs union, the EU’s economy has reached a level of integration such that it cannot tolerate soft underbellies that could be used as gateways into the single market. This is especially true if the foreign investor is linked to an authoritarian regime. The immediate capital surplus that comes with FDI could turn into medium-term economic damage and a long-term political risk.

Footnotes

Funding

The author received no financial support for the research, authorship and/or publication of this article.

Notes

Author biography