Abstract

Inflation began to increase rapidly all around the world towards the end of 2021, and it remained elevated throughout 2022. Higher energy prices contributed significantly to the increase in inflation. However, core inflation, excluding the direct contribution of energy prices, was also significantly above the European Central Bank’s inflation target, which was partially due to the highly expansionary monetary policy implemented during the pandemic. Drawing on historical evidence, this article discusses how the European Central Bank should respond to the increase in inflation. Higher interest rates are necessary to counteract the Bank’s previous expansionary policy. However, when the economy faces significant headwinds, a monetary policy that is too tight may cause a severe recession. Lessons from earlier periods of inflation suggest that, from a long-term perspective, contractionary monetary policy is preferable despite the short-term pain. To limit the negative consequences, this contractionary policy should be coupled with supply-side reforms aimed at stimulating economic growth and increasing the resilience of the European economy.

Introduction

Consumer prices began to increase rapidly towards the end of 2021 and remained elevated throughout 2022. This outbreak of inflation is a global problem, but Europe has been more affected than, for example, the US. In the euro area, inflation reached 10% in November 2022, which was well above the European Central Bank’s (ECB) inflation target of 2%. Higher energy prices due to the war in Ukraine contributed to the rapid increase in prices. However, at 7%, core inflation, excluding the direct contribution of energy prices, was also well above the target. The real economy in the euro area performed relatively well despite the increase in inflation, with unemployment falling to its lowest level on record (Eurostat 2022). Nevertheless, forecasts by the ECB (2022a) and the OECD (2022a) suggest a significant weakening of economic activity in 2023, while inflation is expected to decline slowly but remain above the target. The European economy is likely to face a year of stagflation, that is, high inflation combined with weak economic growth.

From a monetary policy perspective, stagflation poses a significant challenge. Raising interest rates to combat inflation weakens the real economy, while expansionary policies aimed at supporting growth and employment will further aggravate the inflation problem. The challenge faced by the ECB is made worse by the highly expansionary monetary and fiscal policies that were pursued during the pandemic. The rapid increase in the money supply since 2020 also poses a threat to price stability.

The purpose of this article is to discuss the policy challenge faced by the ECB in fighting inflation. In the analysis the article draws on policy lessons from the historical inflationary periods of the Korean War in the early 1950s and the two oil price shocks of the 1970s. These historical lessons suggest that the expansionary policy implemented during the pandemic will force the ECB to pursue a contractionary policy in 2023 to prevent inflation from becoming entrenched.

The causes of consumer-price inflation

The increase in consumer-price inflation that began in the autumn of 2021 has several causes (see e.g. Stiglitz and Regmi 2022; Shapiro 2022). Lockdowns during the pandemic disrupted supply chains and created global shortages of certain goods and raw materials. The war in Ukraine has led to an energy crisis and rising energy costs, not least in Europe. The expansionary fiscal and monetary policy implemented during the pandemic provided households and businesses with money to spend once the pandemic restrictions on social mobility were eased. It is this combination of supply-side restrictions and pumped-up demand that has put upwards pressure on prices.

Much of the public debate on the causes of inflation has focused on the impact of higher energy prices. However, the effect of the expansionary monetary policy during the pandemic should not be underestimated. A major increase in energy prices may have a severe and negative short-term impact on the economy as inflation increases and the economy goes through a period of adjustment. However, once energy prices have stabilised and households and businesses have adjusted to the new energy situation, the negative impact on the economy should fade away—at least as long as second-round effects in terms of excessive wage demands are avoided. The inflationary impact may last longer if higher energy prices ignite a wage–inflation spiral. A slightly contractionary monetary policy that illustrates the central bank’s commitment to the inflation target is likely to anchor inflation expectations and prevent such a spiral from emerging.

An expansionary monetary policy, on the other hand, that pumps up demand well above the economy’s ability to produce may cause a prolonged inflation problem. High demand reduces unemployment, and increases inflation and inflation expectations, which in turn leads to higher wage demands and further inflation. A wage–inflation spiral is triggered. History suggests that once this has occurred, it will take years of monetary policy restraint to break the spiral. Seen from a long-term perspective, the main factor threatening price stability presently is not higher energy prices but the expansionary monetary policy during the pandemic.

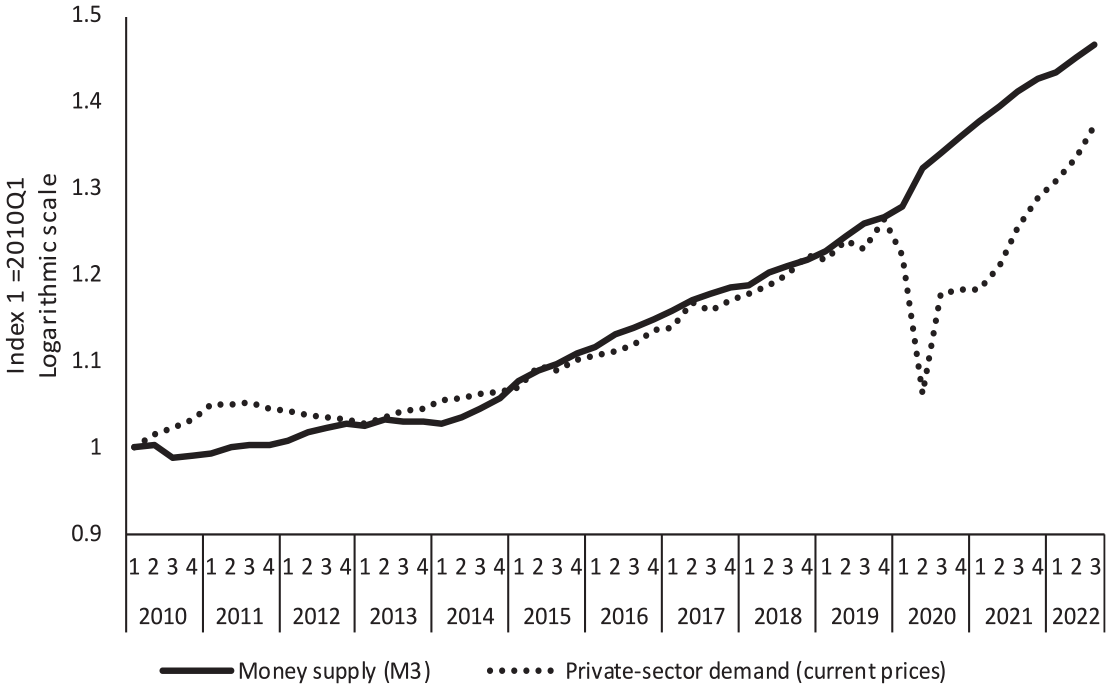

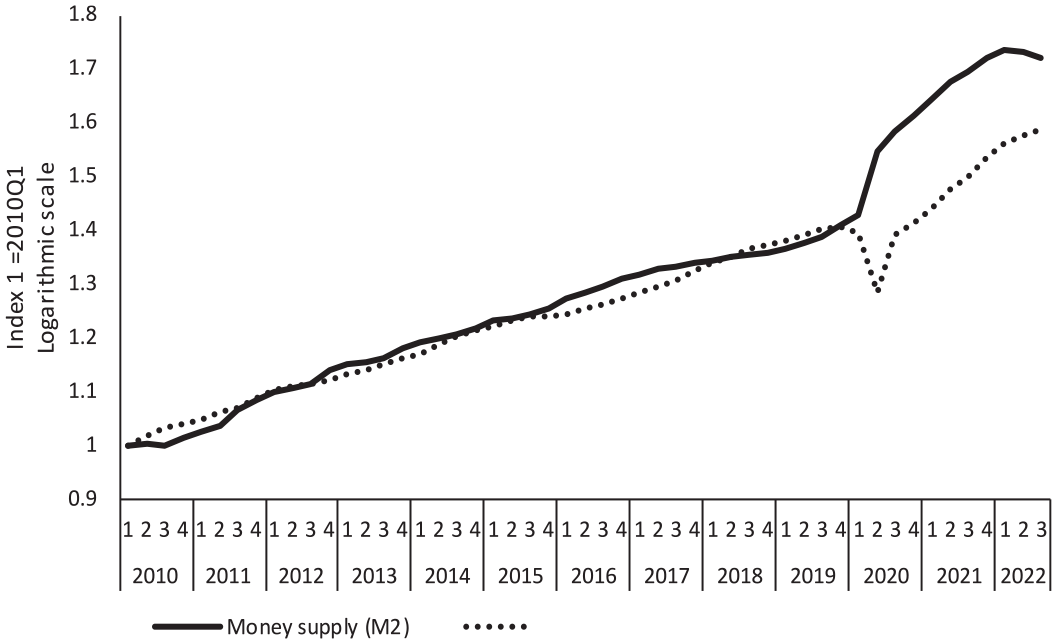

As an illustration of the impact of the expansionary monetary policy during the pandemic, consider Figures 1 and 2. The first figure illustrates private-sector demand, that is, household consumption and business investments, in nominal prices, as well as the broad money supply (M3) 1 for the euro area between 2010 and 2022. The latter figure contains the corresponding statistics for the US. 2 Each series is an index that takes the value of 1 in Quarter 1 of 2010. The scale is logarithmic; thus the slope of the curve represents the percentage-growth rate. Over the long-term, the supply of money and private-sector demand should follow each other closely. A faster increase in the money supply than demand implies that there is a potential for demand to increase in the future and vice versa. When demand increases, there are two main effects on the economy. Businesses might either increase supply to meet the higher demand or raise their prices—or a combination of these two. A rapid increase in demand is likely to mostly spill over into higher prices as the supply side struggles to scale up production to meet the higher demand.

Nominal money supply and private-sector demand in the euro area, Quarter 1 2010–Quarter 3 2022.

Nominal money supply and private-sector demand in the US, Quarter 1 2010–Quarter 3 2022.

Prior to the outbreak of the pandemic in 2020, the two curves moved in parallel, with only small and temporary deviations from each other. During the pandemic, the two curves became decoupled; the quantitative-easing programmes of the ECB and the US Federal Reserve Bank pumped up the money supply, while the pandemic caused a decline in private-sector demand.

Since the pandemic, demand has increased rapidly, faster than the pre-pandemic trend, as it tries to catch up with the increase in the money supply. Due to supply disruptions, a significant part of the increase in demand has been met through higher prices. Inflation reached 6% in the euro area and 8% in the US prior to the war in Ukraine and the major increase in energy prices that took place thereafter. As can be seen in Figures 1 and 2, there was still a significant gap between the money supply and demand towards the end of 2022, suggesting that inflationary pressure will remain going into 2023.

Responding to inflation: lessons from the past

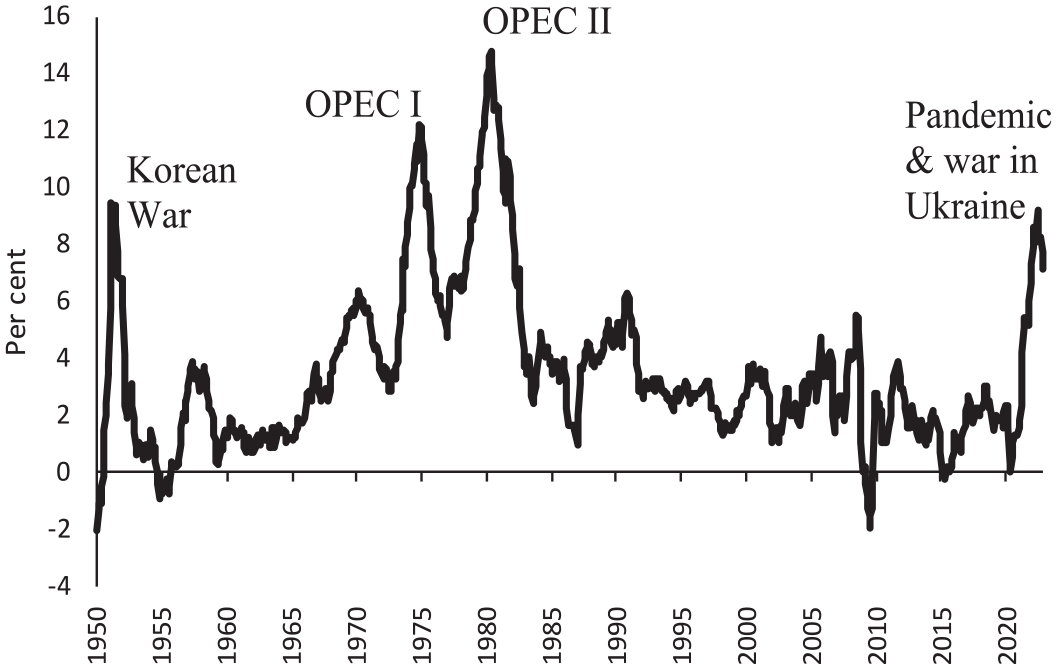

High inflation due to the combination of supply disruptions and rapidly growing demand is not new. Similar outbreaks of inflation took place in the early 1950s during the Korean War and during the two oil price shocks of the 1970s (OPEC I in 1973 and OPEC II in 1979). These two events are illustrated in Figure 3, which shows the consumer-price inflation rate in the US in the period 1950–2022.

Consumer price inflation in the US 1950–2022.

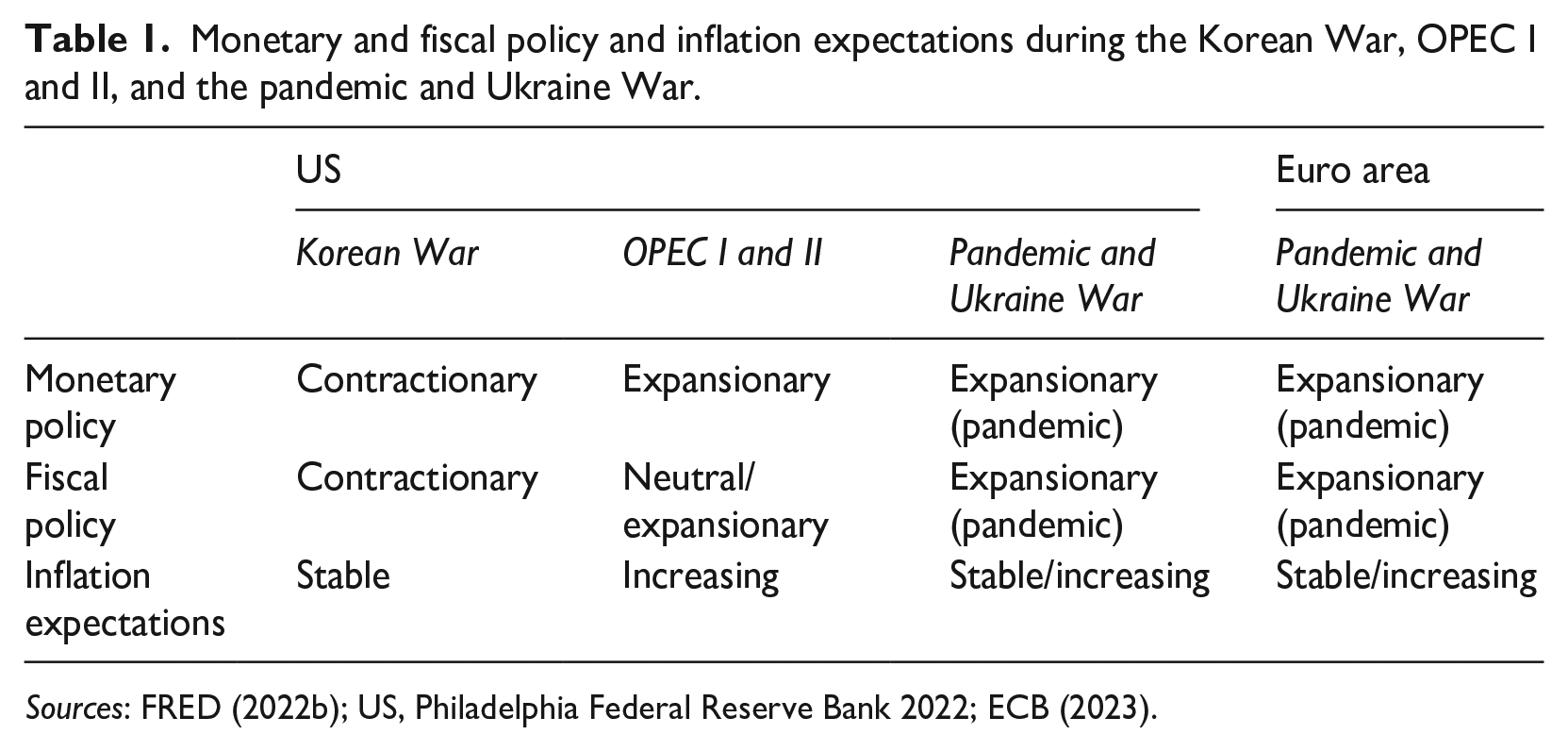

Here the focus will be on the US as the euro area did not exist prior to 1999. In addition, most European economies were still reeling from the effects of the Second World War in the early 1950s. As indicated by Figure 3, an interesting difference between the situations in the 1950s and the 1970s is the duration of the increase in inflation. During the Korean War, inflation was transitory and lasted two years. During the 1970s inflation became entrenched and lasted for more than a decade. The differing inflation outcomes raise two questions: what were the main differences between the two inflationary episodes and what can central banks learn from them today? Each situation is unique and comparisons across historical events will always entail some speculative elements. However, there are some interesting differences between the two periods that offer some guidance to present-day policymakers. As illustrated by Table 1, there are essentially three differences between the 1950s and the 1970s.

Monetary and fiscal policy and inflation expectations during the Korean War, OPEC I and II, and the pandemic and Ukraine War.

First, during the Korean War, monetary policy became contractionary. The Federal Reserve ended the bond-buying programme (quantitative easing) it had launched during the Second World War and interest rates were allowed to rise (Walsh 1993). The policy response in the 1970s was different. The federal government partially financed the war in Vietnam by expanding the money supply. Monetary policy became even more expansionary following the oil price shock (Nelson 2022).

Second, while defence spending increased during the Korean War, the public debt-to-GDP ratio fell from 93% in 1949 to 68% in 1953 (FRED 2022b). The declining debt ratio indicates a contractionary fiscal policy overall. During the 1970s, the debt ratio increased for three years in a row between 1975 and 1977. The increase was small by modern standards, but signalled the end of the long decline in the debt ratio that had taken place since the Second World War.

Third, inflation expectations according to the Livingstone survey (US, Philadelphia Federal Reserve Bank 2022) were relatively stable during the Korean War. They increased from 0% to 5% in 1951 but fell back to 2% the year after. No wage–inflation spiral was triggered. In the 1970s, the partial financing of the Vietnam War through loose monetary policies caused an upward pressure on inflation expectations. This increased further following the two oil price shocks. The expansionary monetary policy contributed to a wage–inflation spiral that was not broken until the early 1980s through the highly contractionary policies of Paul Volcker, who replaced Arthur Burs as chairman of the Federal Reserve. However, this contractionary policy came at a high short-term cost with regard to losses in output and higher unemployment. The unemployment rate doubled between May 1979 and November 1982 before it began to decline.

The historical lesson from the 1950s and the 1970s is that it is important for monetary policy to respond strongly to rising inflation even if it is caused by supply-side disruptions. This is especially true when monetary policy was highly expansionary prior to the supply shock. Once inflation has become entrenched, disinflation policies are far more costly compared to a rapid policy response during the early stages of the inflation process. The comparison between the present situation and the two historical episodes in Table 1 suggests clear similarities between the present and the two oil price shocks. However, there is still time to prevent inflation from becoming entrenched as expectations have remained relatively anchored so far.

Conclusions

The increase in energy prices following the outbreak of the Ukraine War has contributed significantly to higher consumer prices. However, the expansionary monetary policy pursued during the pandemic has also put an upwards pressure on prices. A key policy failure of the 1970s that allowed inflation to become entrenched was the reluctance of the Federal Reserve to recognise the contribution of its own monetary policy to the inflation problem (Nelson 2022). Like today, inflation was not simply the outcome of higher energy prices but also of previous policy decisions. Steering inflation back to the ECB’s target level will require monetary policy constraint for some time to come. The key questions are how contractionary should the policy be and how quickly should inflation be brought back to the target?

The gap between the money supply and demand illustrated in Figures 1 and 2 can be closed in three ways. The first is by reducing the money supply. Reversing quantitative easing, so-called quantitative tightening, can contribute to this process. However, over the short term such a policy risks causing a reduction in demand as well, which will prolong the adjustment process. Second, the supply-side restrictions may come to an end, ensuring that high demand can be met through an increase in the supply of goods and services rather than through increasing prices. Although the economy will eventually adjust to the new energy situation, it may take some time before all supply-side problems have been solved. This is unlikely to happen during 2023. Third, the gap between the money supply and demand can be closed through continued high inflation. However, persistent inflation risks spilling over into higher inflation expectations and generating a wage–inflation spiral, making it much harder for the ECB to bring inflation back to the target in the future.

The Federal Reserve has begun to reduce the money supply through quantitative tightening. The ECB is expected to follow suit in early 2023 (ECB 2022c). This policy response illustrates a commitment to the inflation target but risks a difficult disinflationary period in the short term. Policies that are too contractionary can cause long-term harm to the real economy through, for example, a permanent increase in unemployment, as was the case in some countries during the 1970s and 1980s (Blanchard and Summers 1986). Furthermore, higher interest rates may cause financial difficulties for indebted households, businesses and governments. In a worst-case scenario, higher borrowing costs may trigger a costly financial correction. Nevertheless, for the long term, rapid disinflation is likely the best policy. This would solve the inflation problem quickly, reduce the risk of rising inflation expectations and thus reduce the possibility of a wage–inflation spiral. The real economy would then be given an opportunity to recover towards the mid-2020s, once the inflation rate has been pushed down to the target. Failing to respond to the inflation threat due to high government debt levels would imply that the central bank is inclined to implement fiscal policies under which savers are taxed to reduce the public debt burden. The historical evidence suggests that such a policy would reduce economic growth over the long term and therefore should be avoided.

Contractionary monetary policy will cause both a short-term slowdown in real economic activity and higher unemployment. To avoid a permanent increase in unemployment, the contractionary policies should be coupled with structural reforms that strengthen the real economy (Andersson and Jonung 2023). Economic flexibility is essential to allow the economy to adjust to major shocks quickly and with as few costs as possible (Björnskov 2016). The more flexible the economy is, the lower the negative impact of economic crises. The euro area has lagged behind the US in terms of economic growth for two decades, partially due to the lack of economic flexibility. Since the introduction of the euro, real growth in the euro area has on average been close to one percentage point lower per year than in the US. Economic reforms at both the national and the EU level are essential to close this growth gap (Andersson and Jonung 2023). The rapid increase in the money supply during the pandemic was caused by an overreliance on monetary policy. The time has come to end this policy and focus economic policies on addressing the core issues causing the growth problems in the euro area.

Footnotes

Notes

Author biography