Abstract

As a result of Russian aggression towards Ukraine, lowering European dependence on Russian energy has become a priority for the EU. Policy responses that address energy security have the potential to accelerate the EU’s path to carbon neutrality as well as to boost the funds available for energy efficiency improvements. However, due to the escalating cost of living, many fear energy policy changes may put even more pressure on those who are already struggling to pay their bills. This article argues that for geographic, historical and political reasons, the affordable and social housing sector in Central and Eastern European EU member states is the place to start with the implementation of new energy policy goals. These countries could use funds newly made available to address the needs of Ukrainian refugees while easing the housing problem that this region has been tussling with for decades.

Keywords

Introduction

Soon after the start of the war in Ukraine, energy security became a political priority for many European countries. Growing inflation, including increasing energy and food prices, has brought economic insecurity even to many middle-class households. While the speedy implementation of sustainable energy and energy efficiency measures could be a decisive part of the solution to the current European energy challenges, many fear that the financial weight of these changes will be put on those already struggling to pay their bills. Where to start then? This author believes that the affordable and social housing sector in Central and Eastern Europe (CEE) is the place to best maximise the impact of available funds and create a positive outcome while contributing to dealing with the dark reality of war in the EU’s neighbourhood.

Why CEE?

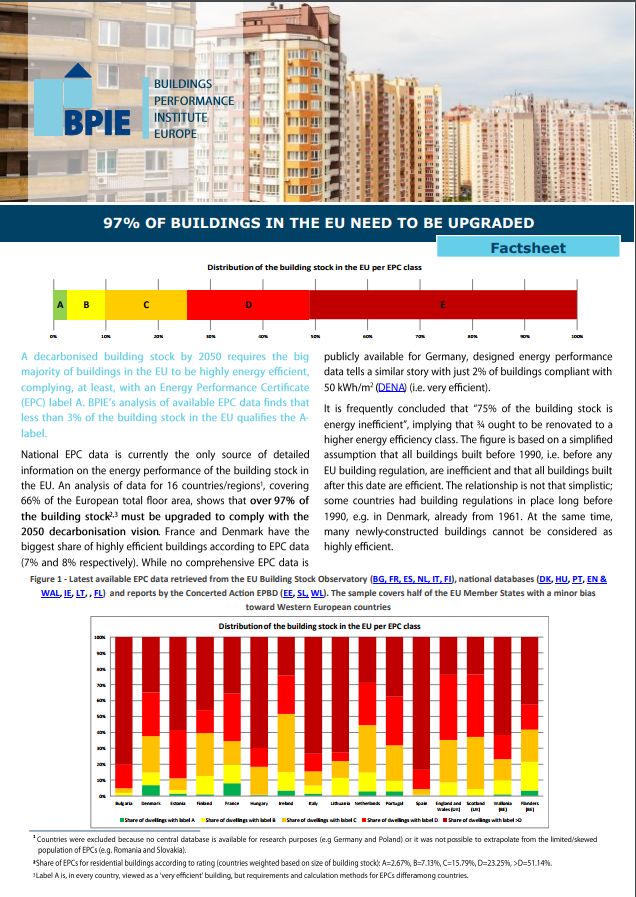

The war in Ukraine has brought many challenges. Why should housing be on our immediate agenda? First, increasing the quality of the housing stock could have a significant impact on energy savings and therefore on long-term energy security. In 2020, households represented 27% of final energy consumption (Eurostat 2020). More importantly, the residential sector accounts for 40% of EU gas demand (ACER 2022). Around 97% of housing stock across the EU does not meet a sufficient level of energy efficiency (BPIE 2017) and its improvement should be seen as an immediate priority, especially in Central Europe due to the above-average household energy consumption there (Enerdata 2021) and limited substitutes for Russian gas.

Second, CEE faces an influx of refugees from Ukraine. With 1.2 million registered Ukrainians in Poland, 380,000 in Czechia, 80,000 in Slovakia 1 and further significant numbers in Romania, Bulgaria, Lithuania and other CEE countries, the region is struggling to provide them with adequate accommodation. Quality emergency housing could later be easily turned into affordable social housing units to ease the housing problem that this region has faced for decades.

Third, EU policymakers cannot afford not to consider the housing issue of the utmost importance. Despite the high support for Russian sanctions (Globsec 2022, 35), the volume of narratives about CEE governments prioritising sanctions and humanitarian support over the well-being of their citizens is significant (International Republican Institute 2022, 7). The rising cost of living as a result of NATO members’ involvement in the war is a narrative that is becoming increasingly present in Central European alternative media. The political stability of countries affected by migration, especially front-line states such as Slovakia, where the Covid-19 pandemic led to the rise of right-wing populism, is linked to the ability of their political representation to provide support in times of crisis. Without addressing this issue, it may become increasingly difficult to maintain public support for Ukraine, including for new energy security policies.

Finally, despite the fact that the economic challenges of the war and the related refugee crisis are affecting the whole EU, the situation in the CEE region is worsened by the underdeveloped affordable housing sector. Since the massive state withdrawal from housing provision and subsidisation in 1989–90, there has been little public policy interest in housing.

Specifics of the CEE housing sector

Due to restitution and privatisation policies, a significant portion of the housing stock in CEE has come into private ownership. Several countries, including Czechia, Romania and Croatia (Hegedüs et al. 2017, 23) also introduced tenant-protection laws for restituted properties to cap rent increases. For a period of time, these policies provided affordable housing conditions for mostly middle-class urban citizens, who were able to privatise their rental housing. However, those who fell through the cracks found themselves with minimal support.

Despite many citizens managing to acquire private housing through this process, the quality of the buildings was often very low due to long-term under-investment in maintenance. Moreover, the rent price cap, which in some cases had been in place for more than a decade, further prevented private landlords of restituted properties from investing in their properties. Furthermore, ‘typically the housing stock in the worst condition remained in public (municipal) ownership, and the most vulnerable households became the typical social tenants’ (Hegedüs et al. 2017, 26). In the past 20 years, renovation subsidy schemes have helped to significantly improve housing in Central Europe, albeit mainly apartment buildings. However, many private owners still find themselves locked into inefficient and costly heating systems. Alongside other reasons, the lack of development of both the affordable and the social housing sectors means that the numbers of those threatened by energy poverty in the EU member states is highest in the CEE region (ENACT 2019).

Additional burden

In the past decade, housing prices in Europe have increased by 30% (Housing Europe 2021b, 19). Although the Covid-19 pandemic, inflation and rising energy prices have affected the whole of Europe, the consequences for CEE countries have been harder to deal with than in those countries with developed affordable housing networks such as Germany or the UK. CEE middle-income groups, which cannot access the narrowly targeted and limited social housing schemes, have started to face affordability problems. Moreover, in the first quarter of 2022, house prices in the EU rose on average by 10.5% year on year. However, this increase was much higher in Central Europe (24.7% in Czechia) and the Baltics (20.1% in Estonia and 19.1% in Lithuania) (Eurostat 2022). The influx of refugees has also led to increased rental costs in affected CEE cities. For instance, in April 2022 rental prices in Poland’s largest cities were estimated to be about 20% higher than at the beginning of the year (Szymanska 2022).

Accessibility of funding

Despite a lack of data about the extent of this issue and gaps in terminology, the growing risk of energy poverty has been increasingly addressed by the European Parliament. From the Clean Energy for All Europeans package to the Report on Access to Decent and Affordable Housing for All (Van Sparrentak 2020), the urgency of this issue as well as its interconnectedness with the need for investment in the energy efficiency of European housing stock are recognised across the political spectrum. The bigger problem is the issue of financing support for property owners and developers.

Among the most commonly mentioned potential financial sources are the Recovery and Resilience Facility and the Coronavirus Response Investment Initiative, created in response to the impact of Covid-19; the Social Climate Fund, promised by the Fit for 55 legislation; and more established funds, such as the European Regional Development Fund. However, access to these funds by private and municipal owners and developers—two key groups of owners in the CEE—remains limited. In other words, the money is there, but flexibility is needed. The ability to blend private and public money, the increased eligibility of private entities and public–private development projects to access this money, and improved communication and administrative support from the state level are just some of the areas where a flexible approach to the processing of these funds could untap opportunities for more bankable affordable housing projects accessible to different income groups.

It seems that the current energy crisis has increased the willingness of European politicians to tackle these issues more quickly. A great example of taking a flexible approach to the allocation of grants is the Cohesion’s Action for Refugees in Europe initiative, for which the European People’s Party Group pushed through an urgent procedure in March 2022. The initiative gives flexibility to member states to retroactively allocate unused EU funds to refugee crisis measures including emergency housing (European Commission 2022). The need for flexibility to transfer resources between the priorities and programmes of the Cohesion Fund was highlighted in a joint statement made by 10 CEE member states to the European Commission in April 2022. The flexibility issue was also recently discussed at the Employment and Social Committee public hearing on ‘The escalating energy poverty and housing affordability crisis’ on 11 July 2022, where it was raised by expert guest Ludovic Voet of the European Trade Union Confederation (European Parliament 2022, 17:07). A willingness to think outside of the box can also be seen in the Czech Presidency’s call for the expansion of local energy communities (European Economic and Social Committee 2022).

In the long term, however, the ability to allocate funds for the renovation of private housing is the key flexibility component needed and unfortunately this issue remains largely unresolved. As housing falls under national and local competences, it is mainly up to CEE member states to address this issue in their financial schemes.

Another group of EU funds which may have a positive impact on the development of affordable housing in Europe is that proposed for the Ukraine crisis response and to boost the energy security of the EU. In particular, the new REPowerEU chapters of the Recovery and Resilience Fund are focused on ending the EU’s dependence on Russian fossil fuels through several measures including installing efficient heating systems and replacing fossil fuels in homes, the redirecting of funds to help Ukrainian refugees (European Council 2022) and the long-discussed ‘Marshall Plan for Ukraine’ (Ukrainian Think Tanks Liaison Office in Brussels 2017). Unlike the funds named above, these have a much clearer geographic focus and expect cooperation at the local level. In particular, the funds intended to assist with emergency housing in the regions affected by the migration wave provide a great opportunity to pilot new social housing projects in close cooperation with municipalities. The basic principles for emergency and social housing are similar: ‘The main question is, how refugee housing can be realized to meet the needs of inhabitants of existing cities, of the newly arriving population of refugees and of future generations, and how to develop new districts that are socially balanced and economically viable’ (Eichner and Ivanova 2018, 2). As the need for such accommodation may last for years, healthy building design, in compliance with budget limits, is a must in order to provide sustainable non-stigmatising housing stock in a way that allows social integration. Obviously, such housing is also easily convertible into social housing units. This approach has been successfully tested in the past and there are stakeholders ready to implement it in the front-line states. An excellent example of such a project is the Empty Spaces to Homes approach piloted by Habitat for Humanity, which currently partners with local authorities and socially minded land and property owners in Poland and Hungary to convert empty and vacant spaces into quality accommodation for vulnerable communities (Habitat for Humanity 2022). Another example of modern emergency housing is the module house approach implemented in 2017 by Aktivhaus in the German municipality of Winnenden (Wang 2017).

Finally, investments in the recovery of Ukraine also represent an opportunity for the CEE housing sector. The Ukrainian social housing sector was severely underfunded even before the war. With only 1% of people living in state-owned homes (2018 data) and only 72 social housing apartments in a capital of 2.8 million inhabitants (2021 data, Bobrova 2022), renovating the housing stock will be one of EU’s priorities. Post-war recovery funds will likely boost the house renovation sector in the entire CEE region, which may help new innovative solutions to enter the market. This is especially true when it comes to piloting of affordable housing solutions that can be transferred within the CEE countries. Due to similarities in housing stock, there are many stakeholders, such as members of Housing Europe (Housing Europe 2022), that are to share replicable renovations know-how in Ukraine. Such cooperation can hopefully bring more visibility to the affordable housing sector domestically and increase its cooperation with the state.

Conclusion

The war in Ukraine is creating escalating financial pressure on European households and exposes the extent of Europe’s vulnerability to energy poverty. The housing crisis is particularly severe in those CEE countries with an underdeveloped safety net for people struggling to access housing or maintain their property. The allocation of available funds to creating quality housing stock is not only a vital part of measures to increase independence from Russian gas, but an opportunity to address a problem whose potential to undermine the resilience of CEE democracies has been underestimated for years. A redesign of housing policy is a massive task for any country, and it would be unreasonable to expect the refugee crises to trigger large-scale changes. However, the solutions that are currently being piloted by local governments and the international development sector in the affected countries could trigger the policy changes needed for the development of bankable and sustainable solutions accessible to both the most vulnerable and those on middle incomes.

Footnotes

Notes

Author biography

{kind=link}