The purpose of the paper is to provide an efficient pricing algorithm for American options with stochastic volatilities and jumps. This paper extends the double Heston model with double exponential jumps and derives the characteristic function of the model by Feynman–Kac theorem. With the obtained characteristic function, this paper also extends the Fourier-cosine expansion method for pricing Bermudan options to the model. Based on the COS method, this paper approximates American options by using Richardson extrapolation schemes on a series of Bermudan options and provides a pricing algorithm for American put options. Numerical results show that the proposed pricing algorithm is efficient, especially for short-term American put options.

It is important for efficiently pricing American options, because a majority of derivative contracts are American style. Single-factor stochastic volatility models, including Stein and Stein,1 Heston,2 and Schöbel and Zhu,3 can explain the volatility smile observed in the real market. Many literatures consider American options pricing under these models by developing some numerical methods, including the finite difference methods of Ikonen and Toivanen,4,5 Ito and Toivanen,6 Zhu and Chen,7 and some extensions, such as Kunoth et al.,8 Rambeerich et al.,9 Ballestra and Pacelli,10 and Burkovska et al.,11 the Monte Carlo simulation method of Abbas-Turki and Lapeyre12 and the tree methods of Beliaeva and Nawalkha13 and Ruckdeschel et al.14

However, single-factor stochastic volatility models are not able to fit the implied volatility smile very well. Evidence from Cont and Tankov,15 Fonseca et al.,16 Christoffersen et al.,17 and Fouque and Lorig18 indicate that single-factor models can do a poor job in capturing the term structures of implicit volatilities over time. By introducing another volatility process, Christoffersen et al.17 propose the double Heston model which can provide better empirical fit to the market price than the Heston model. However, Yu and Zhang,19 Zhou and Zhu,20 González-Urteaga,21 and Jang et al.22 provide strong evidence for stochastic volatility and jumps in prices. By adding the log-normal jump to the asset price, the stochastic volatility jump-diffusion models including the Bates model23 are proposed and applied in option pricing. Compare to log-normal jump, the double exponential jump-diffusion model proposed by Kou24 leads to tractable pricing formulas for path dependent options. Motivated by the superior features of the double Heston model and the double exponential jumps, this paper proposes a new model by combining double Heston model and double exponential jumps.

Additional two factors lead to a high-dimensional partial integro-differential equation which makes the aforementioned finite difference methods quite complex and difficult to be extended to double stochastic volatilities and jumps case. In contrast, the tree method and the Monte Carlo method are easier to be extended to this case. However, exponentially rising numbers of nodes and a large amount of simulation times will make these methods time-consuming. The COS method proposed by Fang and Oosterlee25 is a very efficient method for pricing European option and has been extended to Bermudan options.26,27 Based on the COS method, this paper takes American option as the combination of several Bermudan options and approximates the option price using a Richardson extrapolation technique.28

The rest of the paper is organized as follows. The following section develops the underlying pricing model. The subsequent section derives the characteristic function of the model. Then the method for pricing American options is detailed, followed by some numerical experiments. The last section concludes.

The model

Assume that , , and are all standard Brownian motions which satisfy and Suppose that the asset price process is governed by the following double Heston model with double exponential jumps (DHestonDJ)

where is the risk-neutral interest rate, is the rates of reversion, long-run mean volatility, and instantaneous volatility of variance process , respectively. remains strictly positive if the Feller conditions is satisfied. is a Poisson process with constant intensity . is a sequence of independent identically distribute nonnegative random variables, such that has an asymmetric double exponential distribution with the density.

where denotes the indicator function, so equals 1 if , but 0 otherwise. are the probability of the up-move jump and down-move jump, respectively. Suppose the processes , , , are all independent of and , . The density (2) implies . Suppose .

Remark The model contains the following known models as special cases.

the Heston model by setting and ;

the double Heston model by ;

the double exponential jump-diffusion model by setting .

Deriving the characteristic function

Let denote the strike price. For the asset price satisfying the DHestonDJ model (1), we define the characteristic function of the asset price at time as follows

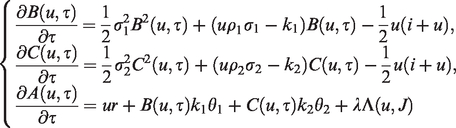

where is imaginary unit. By Feynman–Kac theorem, satisfies the following partial integro-differential equation

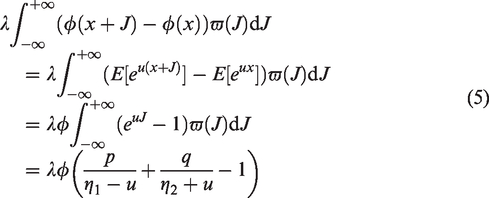

By direct calculation, we rewrite the integral term in equation (4) as follows

According to Duffie et al.29 and Heston,2 has the following form

The above equation produces the following system of three ordinary differential equations

where . By solving the above equations, we obtain the characteristic function as below

where

For the forthcoming computation, we also provide the first two cumulants , as follows

where

Pricing method and algorithm for American options

Let be the current time, be the maturity, and be the collection of all exercise dates with . Let denote the price of an American option and denote the price of a Bermudan option with the exercise times equally spaced, where and then

Assume that can be expanded to with respect to as

with parameters To approximate , we compute a number of times with successively smaller steps, . In such a way, we obtain the increasing exercise opportunities and a sequence of approximation . Based on polynomial interpolation and an asymptotic -expansion, we can construct repeated Richardson extrapolation scheme28 as follows

where and . Figure 1 indicates the four-point Richardson extrapolation scheme.

The four-point Richardson extrapolation scheme.

Bermudan options pricing based on the COS method

Assume that , is the continuation value and is the value of the payoff. The value of a Bermudan option with exercise dates can be expressed by a backward recursion as

By Fourier-cosine series expansion, can be approximated by

where denotes taking the real part of the argument. Putting the above equation into equation (13) and interchanging integration and summation gives the COS formula for approximating by as

where

To obtain Bermudan option price, we need to recover from . We split into two parts by the early exercise point

Equation (20) can be written in the following matrix-vector-product form

where denotes taking the imaginary part of the argument

It is obvious that is a Hankel matrix and is a Toeplitz matrix. With the help of fast Fourier transform algorithm, and can be computed efficiently.

The accuracy of the COS method is related to the size of the integrating range . According to Fang and Oosterlee,25 we define the truncation range as follows

where , L is a proportion constant. For the DHestonDJ model (1), and is provided by equations (8) and (9), respectively.

The hybrid pricing algorithm based on COS and Richardson extrapolation technology

By combining the COS and Richardson extrapolation technology, we provide the following hybrid algorithm for pricing American put options.

Algorithm 1: The algorithm for pricing an American put option

Numerical experiments

We use the four-point Richardson extrapolation schemes and the COS method (Re-COS) to price American put options. The exercise opportunities of each Bermuda option are , respectively. For comparison, we also use four-point Richardson extrapolation schemes and the convolution method proposed by Lord et al.30 (Re-CONV) to evaluate American options. For COS method, we use grid points in equation (14) and in equation (29). For CONV method, we use dampening factor 0.5, grid points and . The model parameter values used in the computation are: We specify three maturities , , and . Under each maturity, we specify , , and . Table 1 reports the results.

Comparison of the accuracy between the Re-COS method and the Re-CONV method for pricing American put options with different strike, maturity and under the DHestonDJ model.

Strike

Re-COS

Re-CONV

Re-COS

Re-CONV

Re-COS

Re-CONV

80

0.2717

0.2718

0.2819

0.2819

0.2922

0.2921

90

1.6115

1.6108

1.6407

1.6398

1.6698

1.6689

100

5.2923

5.2908

5.3346

5.3330

5.3767

5.3750

110

11.7460

11.7444

11.7820

11.7804

11.8180

11.8163

120

20.2933

20.2921

20.3110

20.3098

20.3289

20.3277

80

1.0166

1.0166

1.0433

1.0433

1.0701

1.0701

90

3.1906

3.1903

3.2386

3.2382

3.2863

3.2860

100

7.2976

7.2968

7.3578

7.3570

7.4176

7.4169

110

13.4182

13.4171

13.4754

13.4743

13.5323

13.5312

120

21.2164

21.2152

21.2582

21.2570

21.3000

21.2989

80

2.5532

2.5542

2.6046

2.6057

2.6560

2.6571

90

5.4997

5.5008

5.5722

5.5733

5.6444

5.6454

100

9.9384

9.9391

10.0229

10.0236

10.1069

10.1076

110

15.8335

15.8338

15.9183

15.9185

16.0025

16.0028

120

23.0097

23.0095

23.0839

23.0837

23.1578

23.1576

DHestonDJ: double Heston model with double exponential jumps; Re-CONV: Richardson extrapolation schemes and the CONV method; Re-COS: Richardson extrapolation schemes and the COS method.

Our numerical experiments show that the two methods have almost the same accuracy. If we take the Re-CONV method as the benchmark, the relative error of Re-COS does not exceed 0.0549%, while the absolute error of Re-COS does not exceed 0.0017. We observe that the effect of on the error is negligible, while the effect of on the error is significant. Both the absolute error and relative error of Re-COS increases with the decrease of .

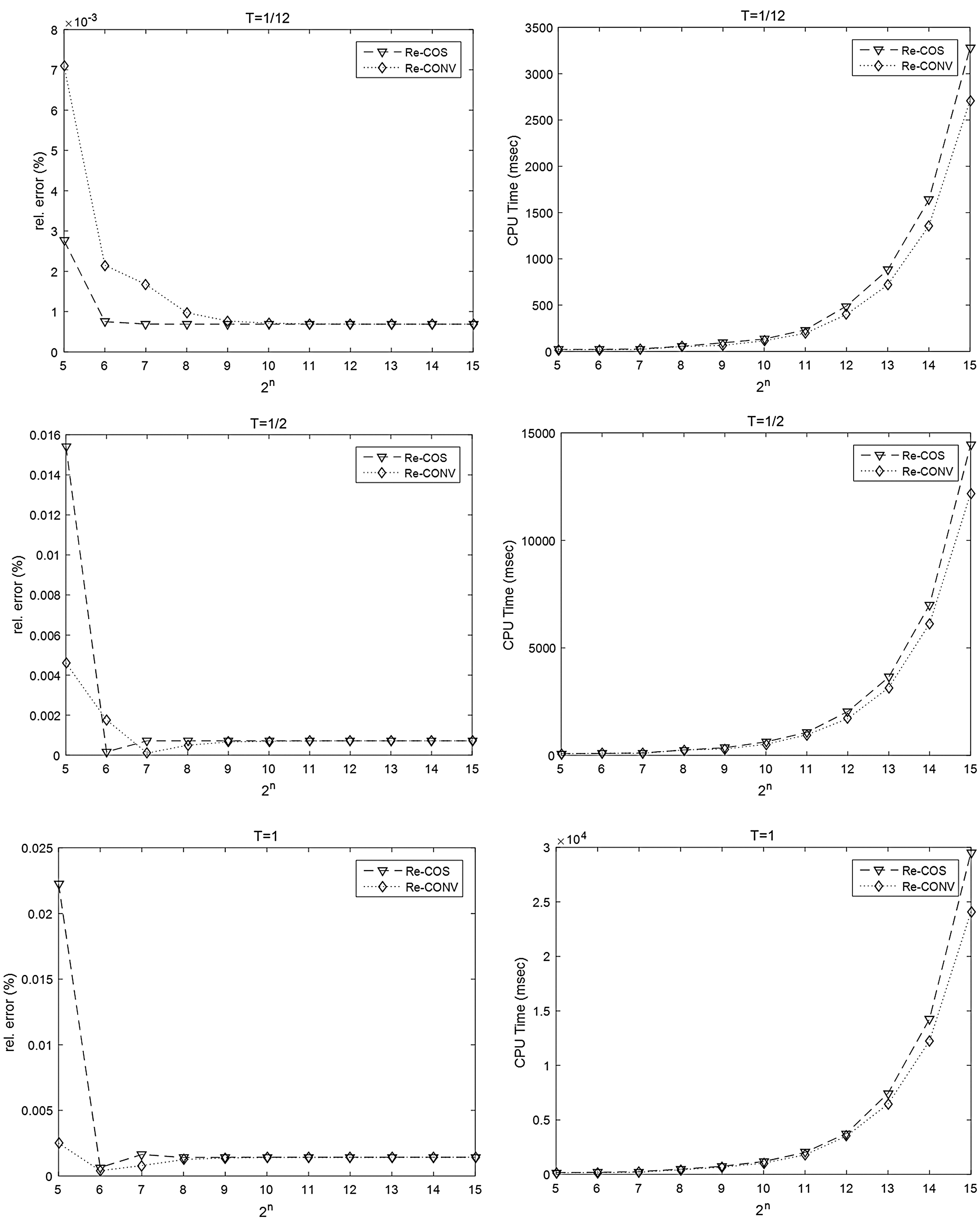

Furthermore, we measure the convergence of the above two methods by the relative error. We approximate an American put option by the Bermudan put options with daily exercise (direct approximation) and take the obtained price as the benchmark. We compute the relative error of the Re-COS and Re-CONV method under (short term), 1/2 (middle term), and 1 (long term), respectively, and compare the convergence of the two methods with grid points. We specify , . Other parameters are the same with the ones used in Table 1. For the direct approximation method, we use exercise opportunities 30, 128, and 256 under , 1/2, and 1, respectively and grid points under each maturity. For Re-COS, we use . For Re-CONV, we use and dampening factor 0.5. For four-point Richardson extrapolation schemes, we use exercise opportunities: , , and under , 1/2, and 1, respectively. Figure 2 summarizes the main results. The CPU time wasted by the two methods with grid points is also presented in Figure 2.

The comparison of convergence and CPU time between the Re-COS method and the Re-CONV method with grid points for pricing American put options. We use (25, 24, 23, 22), (27, 26, 25, 24), (28, 27, 26, 25) in four-point Richardson extrapolation schemes under T = 1/12, 1/2, 1, respectively. The benchmark prices are computed by the Bermudan put options with daily exercise, that is, 30, 128, 256 exercise opportunities under T = 1/12, 1/2, 1, respectively. Re-CONV: Richardson extrapolation schemes and the CONV method; Re-COS: Richardson extrapolation schemes and the COS method.

From Figure 2, we see that both the two methods present smooth and stable convergence under each maturity. The Re-COS method converges with fewer grid options compared to the Re-CONV method. It only needs and grid points to obtain stable convergence for the Re-COS method under and , respectively, while it needs grid points to obtain the same convergence for the Re-CONV method. The CPU time wasted by the Re-COS method is little longer than the Re-CONV method for more than grid options. Since the Re-COS method has converged with grid points, the disadvantage of the Re-COS method in time can be negligible. Table 1 and Figure 2 verify that the Re-COS method is efficient for pricing American put options, especially for short-term American options.

Conclusion

The double Heston model with double exponential jumps incorporates several important features of stock return. We derive the characteristic function of the model. Under the model, we approximate American options by combining Richardson extrapolation technique and the COS method and provide a pricing algorithm for American put options. Numerical results show that the presented algorithm is efficient for pricing American put options, especially for short-term American put options. Although the values of American call options can be obtained by the put-call symmetry, our numerical results (not reported in the paper) show the performance of our algorithm for call options is not as good as for put options.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Natural Science Foundation of China (grant no. 11601420), the Natural Science Foundation of Shaanxi Province, China (grant no. 2017JM1021) and the Scientific Research Fundation of the Education Department of Shaanxi Province, China (grant no. 17JK0714).

References

1.

SteinJCSteinEM.Stock price distributions with stochastic volatility: an analytic approach. Rev Financ Stud1991;

4: 727–752.

2.

HestonSL.A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev Financ Stud1993;

6: 327–343.

3.

SchöbelRZhuJ.Stochastic volatility with an Ornstein-Uhlenbeck process: an extension. Eur Financ Rev1998;

3: 23–46.

4.

IkonenSToivanenJ.Efficient numerical methods for pricing American options under stochastic volatility. Numer Method Part Diff Eq2008;

24: 104–126.

5.

IkonenSToivanenJ.Operator splitting methods for pricing American options under stochastic volatility. Numer Math2009;

113: 299–324.

6.

ItoKToivanenJ.Lagrange multiplier approach with optimized finite difference stencils for pricing American options under stochastic volatility. Siam J Sci Comput2009;

31: 2646–2664.

7.

ZhuSPChenWT.A predictor-corrector scheme based on ADI method for pricing American puts with stochastic volatility. Comput Math Appl2011;

62: 1–26.

8.

KunothASchneiderCWiechersK.Multiscale methods for the valuation of American options with stochastic volatility. Int J Comput Math2012;

89: 1145–116300.

9.

RambeerichNTangmanDYLollchundMRet al.

High-order computational methods for option valuation under multifactor models. Eur J Oper Res2013;

224: 219–226.

10.

BallestraLVPacelliG.Pricing European and American options with two stochastic factors: a highly efficient radial basis function approach. J Econ Dyn Control2013;

37: 1142–1167.

11.

BurkovskaOHaasdonkBSalomonJet al.

Reduced basis methods for pricing options with the Black-Scholes and Heston model. Siam J Finan Math2015;

6: 685–712.

12.

Abbas-TurkiLALapeyreB.American options by Malliavin calculus and nonparametric variance and bias reduction methods. Siam J Finan Math2012;

3: 479–510.

13.

BeliaevaNANawalkhaSK.A simple approach to pricing American options under the Heston stochastic volatility model. J Deriv2010;

17: 25–43.

14.

RuckdeschelPSayerTSzimayerA.Pricing American options in the Heston model: a close look at incorporating correlation. J Deriv2013;

20: 9–29.

15.

ContRTankovP.Financial modelling with jump processes.

London:

Chapman & Hall/CRC, 2004.

ChristoffersenPHestonSJacobsK.The shape and term structure of the index option smirk: why multifactor stochastic volatility models work so well. Manage Sci2009;

55: 1914–1932.

18.

FouqueJPLorigMJ.A fast mean-reverting correction to Heston’s stochastic volatility model. Siam J Finan Math2011;

2: 221–254.

19.

YuCZhangJ.Bayesian approach to Markov switching stochastic volatility model with jumps. Commun Stat-Simul C2011;

40: 1613–1626.

20.

ZhouHGZhuJ.An empirical examination of jump risk in asset pricing and volatility forecasting in China’s equity and bond markets. Pacific-Basin Fin J2012;

20: 857–880.

21.

González-UrteagaA.Further empirical evidence on stochastic volatility models with jumps in returns. Span Rev Financial Econ2012;

10: 11–17.

22.

JangWWEomYHKimDH.Empirical performance of alternative option pricing models with stochastic volatility and leverage effects. Asia Pac J Financ Stud2014;

43: 432–464.

23.

BatesD.Jumps and stochastic volatility: the exchange rate processes implicit in Deutschemark options. Rev Financ Stud1996;

9: 69–107.

24.

KouSG.A jump diffusion model for option pricing. Manage Sci2002;

48: 1086–1101.

25.

FangFOosterleeCW.A novel pricing method for European options based on Fourier-cosine series expansions. Siam J Sci Comput200831: 826–848.

26.

FangFOosterleeCW.Pricing early-exercise and discrete barrier options by Fourier-cosine series expansions. Numer Math2009;

114: 27–62.

27.

FangFOosterleeCW.A Fourier-based valuation method for Bermudan and barrier options under Heston’s model. Siam J Finan Math2011;

2: 439–463.

28.

ChangC-CChungS-LStapletonRC.Richardson extrapolation technique for pricing American-style options. J Fut Mark2007;

27: 791–817.

29.

DuffieDPanJSingletonK.Transform analysis and asset pricing for affine jump-diffusions. Econometrica2000;

68: 1343–1376.

30.

LordRFangFBervoetsFet al.

A fast and accurate FFT-based method for pricing early-exercise options under Lévy processes. Siam J Sci Comput2008;

30: 1678–1705.