Abstract

This paper revisits the exchange rate–stock return nexus by examining how macro-financial fundamentals—specifically interest rate and inflation differentials relative to the United States—shape the impact of currency fluctuations on equity markets in 14 developed and 16 emerging economies. Motivated by gaps in the literature that overlook threshold behaviour, cross-sectional dependence, and distributional heterogeneity, the paper develops a novel two-stage CCE-augmented Panel Smooth Transition Regression (PSTR) model combined with Quantile Treatment Effects (QTE). This methodological innovation enables the identification of nonlinear regime shifts driven by macroeconomic differentials while addressing endogeneity and global spillovers. The results reveal sharp regime transitions associated with interest rate and inflation thresholds, particularly in developed markets. In emerging markets, exchange rate depreciation significantly lowers stock returns only when inflation differentials exceed a critical threshold, underscoring the role of macroeconomic instability. For developed markets, high-interest rate differentials magnify the negative effect of exchange rate fluctuations on equity performance, consistent with carry-trade dynamics. QTE analysis shows that emerging markets underperform during bearish conditions due to higher exchange rate volatility but outperform during bullish phases, reflecting a conditional “high-risk, high-return” pattern. These findings offer new insights for monetary authorities, investors, and portfolio risk managers.

Keywords

Introduction

Global financial integration has amplified the interaction between exchange rate movements and stock market performance, making currency fluctuations an essential component of asset pricing, corporate valuations, and investment strategies (Gong et al., 2025; Hussain et al., 2024; Sokhanvar et al., 2024). The effect of currency fluctuation on stock market performance is particularly pronounced for firms with multinational exposure, where shifts in exchange rates influence export competitiveness, production costs, and ultimately their stock returns (Aftab et al., 2024; Bosupeng et al., 2024).

Theoretical underpinnings of this relationship are well established in the flow-oriented model and the portfolio balance approach (Bonga-Bonga, 2018; Dornbusch & Fischer, 1980; Singh et al., 2024). The former posits that currency depreciation boosts exports and raises stock prices, while the latter suggests that attractive stock market valuations stimulate foreign capital inflows, leading to currency appreciation.

Based on this theoretical foundation, a substantial empirical literature has explored the exchange rate–stock return relationship across a variety of economies. Early studies documented linear or directional linkages, with several reporting causality from exchange rates to stock prices (Alashi, 2022; Dash & Sahu, 2018; He et al., 2023). However, research has increasingly shown that these effects are not constant across time or economic conditions. A growing body of work demonstrates asymmetric or nonlinear interactions, often driven by crises, policy shifts, or market stress (Bahmani-Oskooee & Saha, 2016; Bhutto & Chang, 2019; Dang et al., 2020). Other studies identify the importance of external shocks—such as oil prices, macroeconomic policy changes, or volatility regimes—in shaping this relationship (Ajala et al., 2021; Awadzie, 2021; Odionye et al., 2024).

Despite these significant insights, three important gaps remain in the literature. First, although interest rate and inflation differentials are central to international finance—affecting capital flows, currency valuation, and economic competitiveness—existing studies have not examined whether threshold levels in these differentials produce nonlinear shifts in the exchange rate–stock return relationship. This omission is particularly relevant during periods such as the COVID-19 pandemic, when unprecedented monetary divergence caused sharp fluctuations in these differentials. Second, while interest rate differentials underpin the mechanics of currency carry trade strategies and stock market valuation (Bonga-Bonga & Rangoanana, 2022; Chen et al., 2021; Fung et al., 2013), no study has explored whether interest rate differential translate into a transition mechanism through which exchange rate changes influence stock returns. Third, and most critically, prior research has not analysed distributional differences in the impact of exchange rate movements on stock returns between emerging and developed markets in the context of quantile treatment effect (QTE). This is a substantial limitation because emerging markets typically face higher volatility, weaker institutions, and greater exposure to external shocks (Bonga-Bonga & Mpoha, 2025; Chancharat & Chancharat, 2025) compared to developed economies. To date, no study has evaluated these differences using a treatment-effect approach based on exchange rate volatility.

To address these gaps, this paper offers three key contributions. First, it examines how interest rate and inflation differentials shape the relationship between exchange rate changes and stock returns in major emerging and developed markets. Second, it analyses the distributional differences in the impact of exchange rate movements on stock returns across these market groups using a QTE framework. Third, it introduces a methodological advancement by developing a two-stage Common Correlated Effects (CCE) PSTR model that simultaneously addresses endogeneity and cross-sectional dependence (CSD), thereby improving the identification of nonlinear macro-financial dynamics.

The remainder of the paper is structured as follows: Section 2 reviews the literature on exchange rate and stock market nexus, Section 3 describes the methodological framework, Section 4 presents the results and discussion, and Section 5 concludes with policy implications and avenues for future research.

Literature Review

Studies on the relationship between exchange rate movements and stock market performance has expanded significantly, reflecting growing recognition that this nexus is non-linear, asymmetric, and highly sensitive to macro-financial conditions. Although the empirical evidence is wide-ranging, it remains fragmented across modelling approaches, country contexts, and crisis periods. To provide conceptual clarity, the existing studies can be organised into four major thematic strands, each contributing distinct insights yet leaving important gaps that this study seeks to address.

The first and most prominent strand consists of studies employing asymmetric non-linear modelling using NARDL frameworks. This body of work argues that currency appreciations and depreciations may exert different effects on stock returns, and that these effects can vary across short- and long-run horizons. Bahmani-Oskooee and Saha (2016) documented short-term asymmetries in the United States, while Moussa and Delhoumi (2022) identified similar short-run dynamics in MENA markets. Dang et al. (2020) found both short- and long-run asymmetries in Vietnam, and Ahmed (2020) showed that the nature of the exchange rate regime influences the degree of asymmetry in Egypt. Extending the focus beyond exchange rates alone, Ghumro et al. (2024) integrated investor sentiment into a NARDL model for the U.S. stock market, revealing that sentiment had a stronger influence than exchange rates, particularly after the 2008 financial crisis. Although these contributions reinforce the importance of non-linear dynamics, they mostly analyse single economies or narrow regions, often restrict attention to short-run asymmetries, and rarely examine whether broader macroeconomic variables induce threshold effects that could shift the underlying relationship.

A second body of literature applies threshold cointegration and threshold error-correction models to capture state-dependent relationships between exchange rates and stock prices. Yau and Nieh (2009) found evidence of asymmetry in Taiwan but not Japan, illustrating the importance of country-specific financial and structural characteristics. Kollias et al. (2016) observed that stock and currency markets in Norway and the United Kingdom exhibit stronger bidirectional causality during financial crises, suggesting that market stress amplifies cross-market linkages. Saman (2015) further highlighted that economic news contributes to short-run non-linearities, though again within a limited geographical context. While these models successfully detect structural breaks and asymmetric error-correction behaviour, they typically rely on statistical thresholds rather than macro-financial transition variables such as interest rate or inflation differentials, limiting their ability to explain why regime shifts occur.

A third stream of research adopts regime-switching and volatility-state models. These approaches emphasise that the link between stock returns and exchange rate movements differs across high- and low-volatility regimes. Chkili and Nguyen (2014) showed that BRICS markets display regime-dependent interactions, with stock market developments exerting heterogeneous effects on exchange rates depending on volatility conditions. Wasiaturrahma et al. (2020) used a Markov-switching EGARCH model to uncover asymmetric return volatility in Indonesia, while Frömmel et al. (2022) demonstrated that the USD/Euro exchange rate alternates between regimes shaped by purchasing power parity and interest rate parity. da Silva (2023) found that in Brazil and Mexico, stock returns influence exchange rates differently across volatility regimes. Although these studies capture important shifts in volatility, their regimes are generally treated as exogenous statistical states rather than outcomes that evolve endogenously with macroeconomic fundamentals.

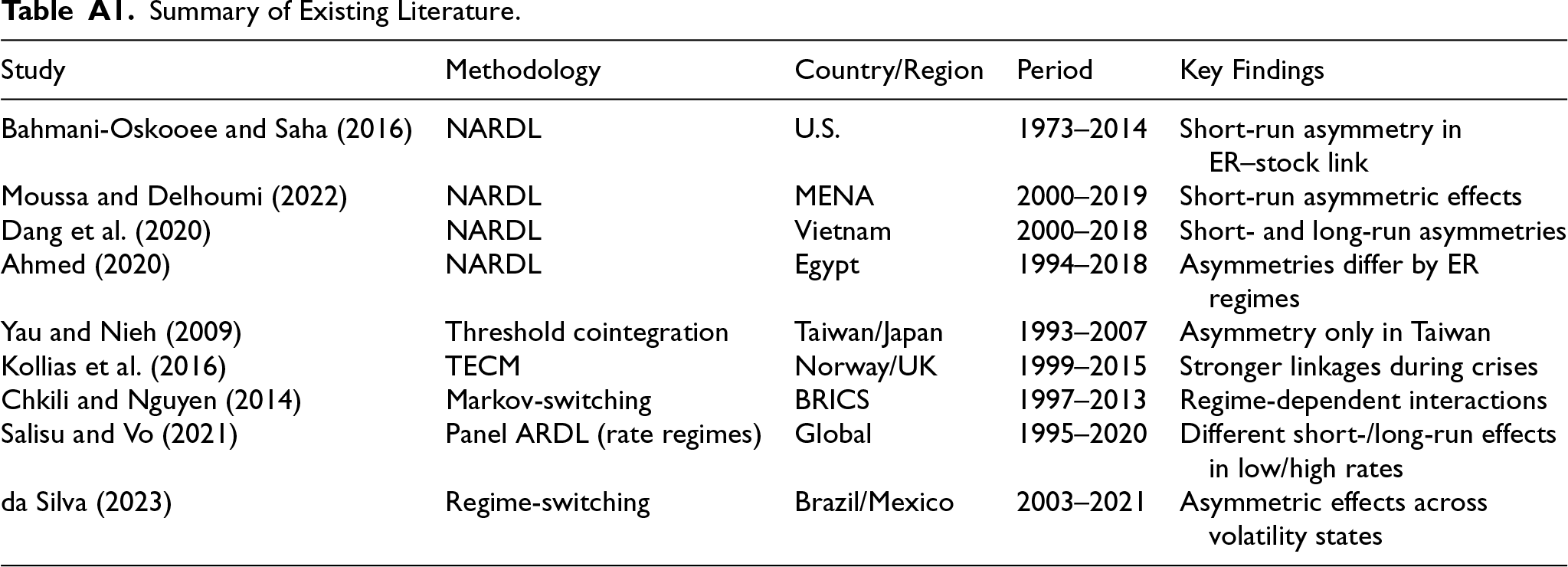

A fourth and more limited strand of the literature directly incorporates macroeconomic conditionality, particularly through interest rate environments and policy regimes. Salisu and Vo (2021) examined stock–exchange rate dynamics under low and high interest rate regimes and showed that the direction and persistence of exchange rate effects differ across these regimes. Their analysis, however, did not identify significant appreciation-depreciation asymmetries and did not incorporate inflation differentials, which are theoretically central to exchange rate determination. Moreover, despite the profound macro-financial disruptions caused by the COVID-19 pandemic, research examining how the crisis altered the exchange rate–stock return relationship remains scarce. COVID-19 produced unprecedented divergence in interest and inflation differentials as central banks implemented aggressive monetary interventions, yet few studies have investigated whether these shifts generated new threshold effects or altered the distributional sensitivity of stock returns to exchange rate volatility. Very little work differentiates between developed and emerging markets in this context, even though emerging markets experienced sharper currency fluctuations and greater capital flow volatility during the pandemic. Table A1 in the appendix provides a summary of the key existing studies on this topic.

When viewed collectively, the literature reveals several persistent limitations. Empirical studies are often restricted to individual countries or regional groupings, which constrains generalisability. Many contributions selectively include macroeconomic variables while overlooking critical fundamentals such as inflation differentials. Regime-switching models frequently rely on exogenous, statistically determined regimes rather than allowing macro-financial variables to drive smooth transitions between states. Crisis periods, especially the COVID-19 pandemic, are insufficiently examined, despite offering a natural stress-test environment for evaluating macro-financial thresholds. Finally, the distributional effects of exchange rate changes remain understudied, as most empirical models estimate mean effects and do not assess how the impact varies across the full distribution of stock returns, particularly when comparing structurally distinct markets such as high-volatility emerging economies and low-volatility developed economies.

This study directly addresses these limitations by using a Panel Smooth Transition Regression (PSTR) model to examine non-linearities in the exchange rate–stock return relationship across 14 developed and 16 emerging economies. Interest rate differentials and inflation differentials are incorporated as transition variables, allowing the relationship to evolve endogenously with macroeconomic conditions. By focusing on the 2019–2021 period, which encompasses the COVID-19 pandemic, the analysis offers novel insights into how macro-financial thresholds interacted with crisis-driven volatility. The study further contributes to the literature by applying QTE analysis to capture the distributional effects of exchange rate volatility, distinguishing emerging markets as the treatment group and developed markets as the control group. This integrated approach yields a deeper understanding of both non-linear macro-financial linkages and heterogeneous stock market responses across the return distribution, thereby providing new theoretical and empirical insights with implications for policy, investment strategy, and risk management.

Methodology

Baseline Model Specification

This study examines the impact of exchange rate movements on stock returns, moderated by interest rate and inflation differentials relative to the US. Following Bahmani-Oskooee and Saha (2016), the baseline model is:

Given the potential asymmetries and threshold effects in stock returns, a non-linear PSTR model is employed (Gonzalez et al., 2005). The basic PSTR model with two regimes is:

The transition function

Given the potential endogeneity between stock returns and changes in exchange rates—stemming from reverse causality documented in the literature (Alagidede et al., 2011; Inci & Lee, 2014)—and the likelihood of CSD arising from shared exposure to global shocks such as commodity price fluctuations and monetary policy spillovers, this study incorporates both issues directly into the PSTR estimation. To do so, it proposes a Two-Stage CCE-Augmented PSTR model. In the first stage, a proxy for exchange rate changes is estimated using the following specification:

The fitted values

The second stage addresses the issue of cross sectional dependence by augmenting the model with the cross sectional average of the key variables while using the proxy of the change in exchange rate to address the issue of endogeneity. It is important to note that the PSTR model is augmented with cross-sectional averages following the CCE approach of Pesaran (2006) and later extensions for nonlinear panels (Chudik & Pesaran, 2015; Kapetanios et al., 2011). Specifically, the second-stage model includes the following cross-sectional means:

The expression of the proposed two-stage CCE augmented PSTR model is presented in Equation 6 as:

In this specification,

Before estimating Equation 6, it is necessary to test for linearity against the PSTR model and to determine the number of transition functions in the model. To test for linearity in the PSTR model, the transition function is approximated by its first-order Taylor expansion around zero. The null hypothesis of linearity is then tested through an auxiliary regression:

Two other tests that can be used are the Wald

To examine how changes in the exchange rate affect stock returns across different points of the return distribution—using emerging economies as the treatment group and developed economies as the control group based on the magnitude of their exchange rate volatility—this study applies a QTE approach. Let

In the context of this study, the unconditional and conditional QTE will be differentiated. The conditional QTE (CQTE) extends the analysis by incorporating control variables which may also influence stock returns. By adding control variables, the CQTE captures the effect of exchange rate volatility after accounting for these additional factors, allowing for a more precise estimation of the treatment effect. The conditional version adjusts the quantile function for these covariates X, and the CQTE at quantile

In this context,

The QTEs are estimated using a cluster-bootstrapped procedure (by country) to generate robust 95% confidence intervals. This approach follows Firpo (2007) and Athey and Imbens (2006), allowing for heterogeneous treatment effects across the entire distribution rather than only the mean.

Data Description

In this study, a balanced panel dataset consisting of quarterly observations from 14 developed market countries and 16 emerging market countries 2 is used, covering the period from 2019Q1 to 2021Q4. The sample period is selected to include the COVID-19 crisis, which is critical for assessing the threshold effects of interest rate and inflation differentials on the stock return–exchange rate relationship.

Stock market indices (

The interest rate differential (

CPI data for all countries and the US are reported quarterly, using end-of-quarter values. The inflation differential (

Descriptive Statistics

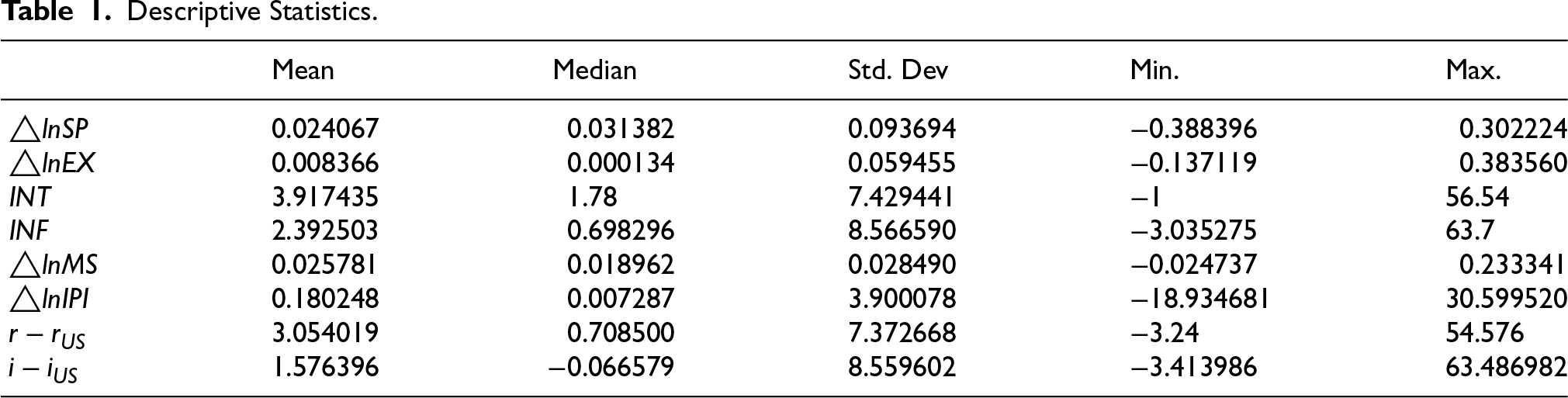

Table 1 summarises key statistics. The dependent variable,

Descriptive Statistics.

Descriptive Statistics.

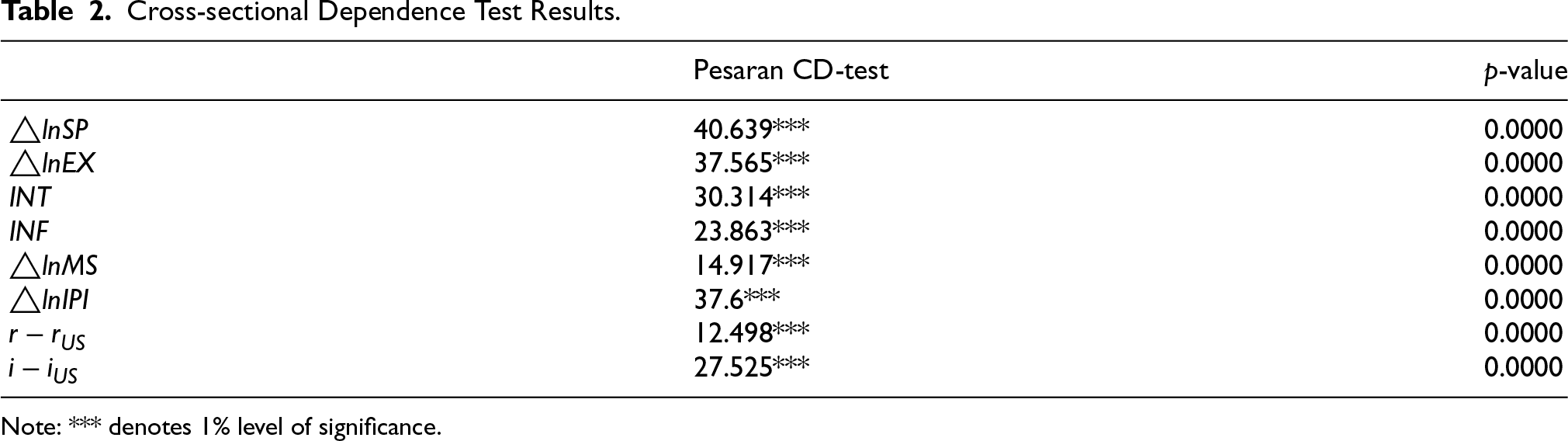

Before estimating any panel model, it is essential to determine whether the data exhibit CSD, which arises when units (countries) are jointly influenced by common shocks. CSD is a well-documented feature of international financial panels and can bias estimates and unit root tests if ignored (Chudik & Pesaran, 2015; Pesaran, 2004).

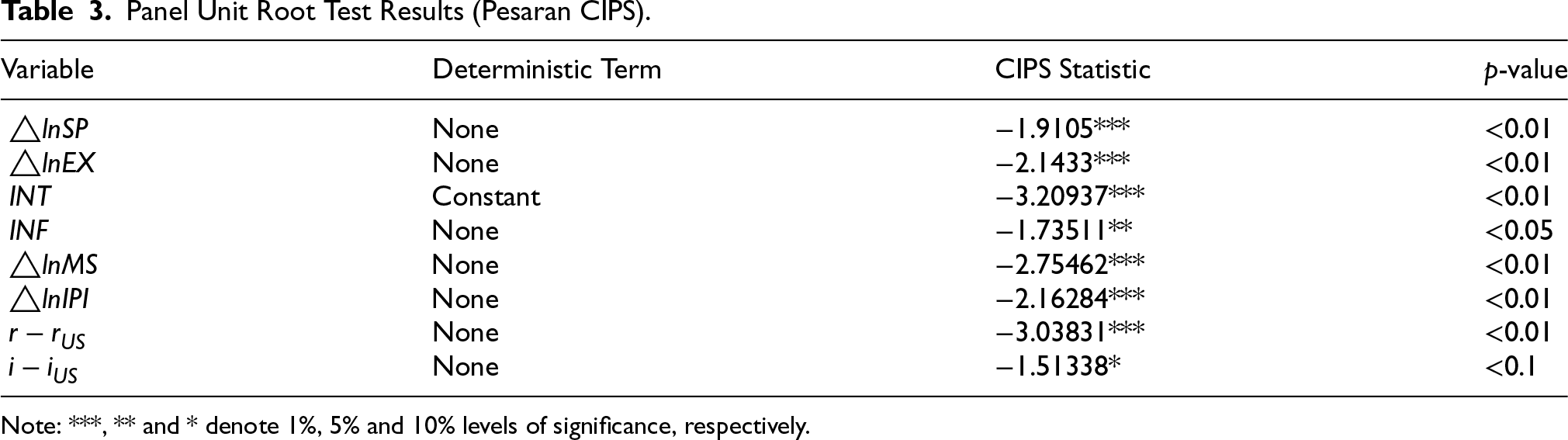

Table 2 shows that all variables exhibit strong CSD as the null hypothesis of cross sectional independence is rejected (all Pesaran CD-statistics significant at 1%). This pattern is consistent with global spillover channels documented in the literature (e.g., Dedola et al., 2017; Rey, 2015). Because of this, the analysis employs the second-generation cross-sectionally augmented Im-Pesaran-Shin (CIPS) panel unit root test is conducted. Table 3 reports CIPS results. All key variables are stationary at conventional significance levels, confirming their suitability for the PSTR model.

Cross-sectional Dependence Test Results.

Cross-sectional Dependence Test Results.

Note: *** denotes 1% level of significance.

Panel Unit Root Test Results (Pesaran CIPS).

Note: ***, ** and * denote 1%, 5% and 10% levels of significance, respectively.

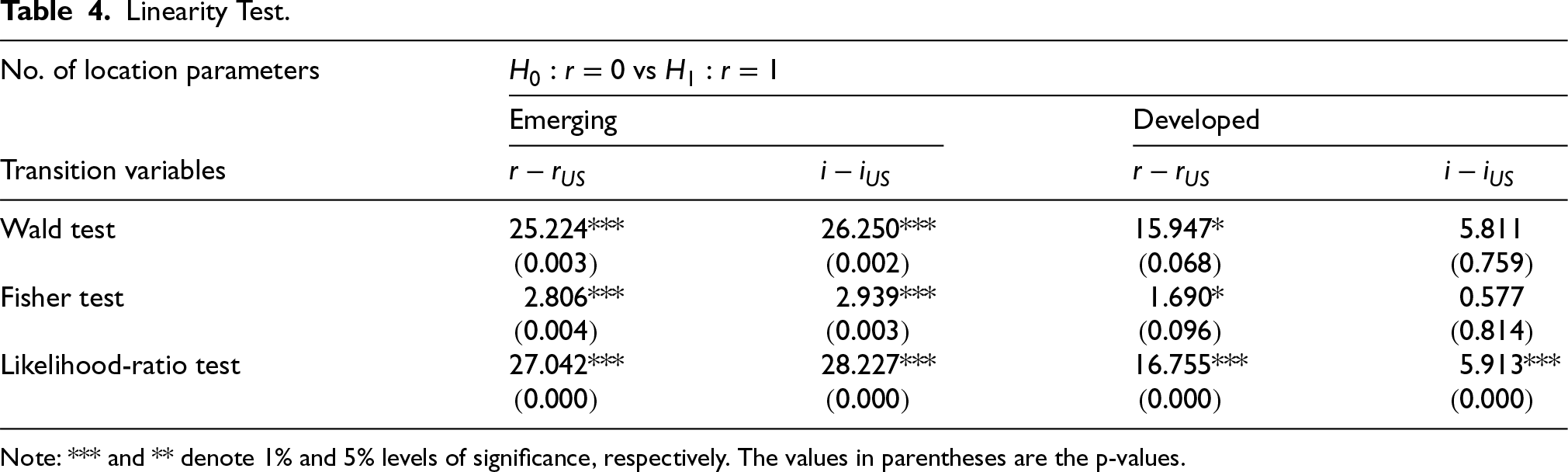

Table 4 presents the linearity test results. For emerging markets, all tests (Wald, Fisher, and Likelihood-ratio) strongly reject linearity for both transition variables (interest rate and inflation differentials), confirming non-linear effects. In developed markets, the linearity tests provide partial evidence of non-linearity for the interest rate differential, but the inflation differential the LR test reject the null hypothesis of linearity, confirming that a nonlinear model should be considered for model estimation.

Linearity Test.

Linearity Test.

Note: *** and ** denote 1% and 5% levels of significance, respectively. The values in parentheses are the p-values.

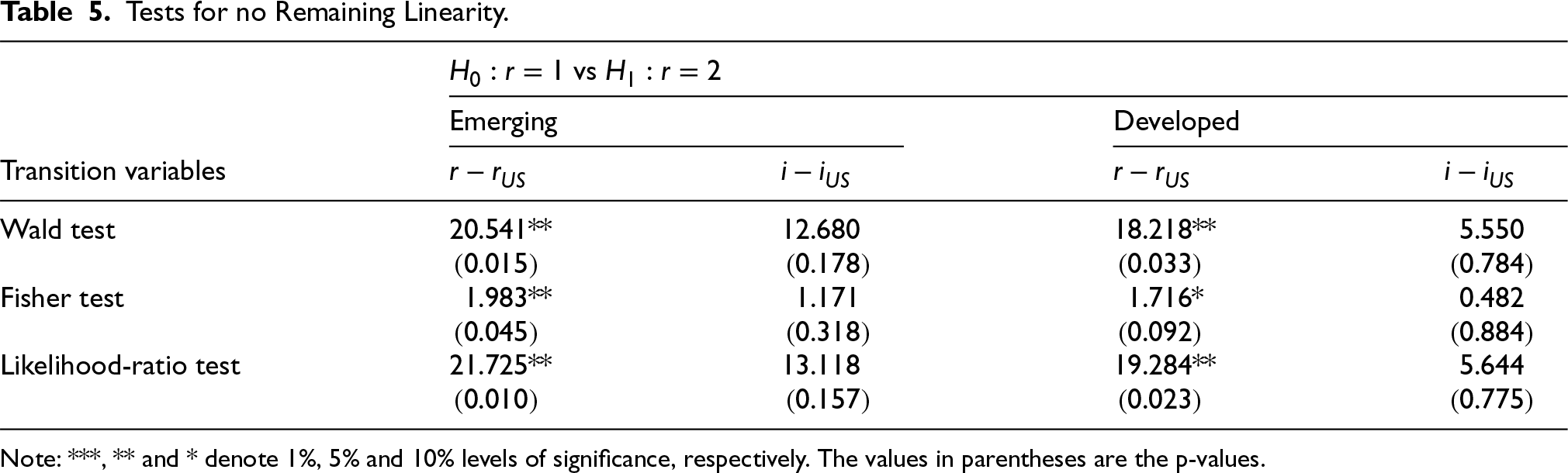

Tests for additional thresholds (Table 5) suggest no further threshold for inflation differentials in both markets but potential second thresholds for interest rate differentials. Given sample size limitations, a single threshold is used for both the interest and inflation differentials in both groups for the sake of comparability.

Tests for no Remaining Linearity.

Note: ***, ** and * denote 1%, 5% and 10% levels of significance, respectively. The values in parentheses are the p-values.

To address the presence of CSD on the data, this study employs a PSTR framework augmented with cross-sectional averages. Moreover, given the potential endogeneity between exchange rate movements and stock returns—particularly the possibility of reverse causality—the analysis adopts a two-stage PSTR approach that incorporates these averages in both stages. In the first stage, a proxy for exchange rate changes is estimated to isolate the exogenous component of currency movements. This proxy is then included in the second-stage PSTR model to mitigate endogeneity. The inclusion of cross-sectional averages of the main variable's averages (

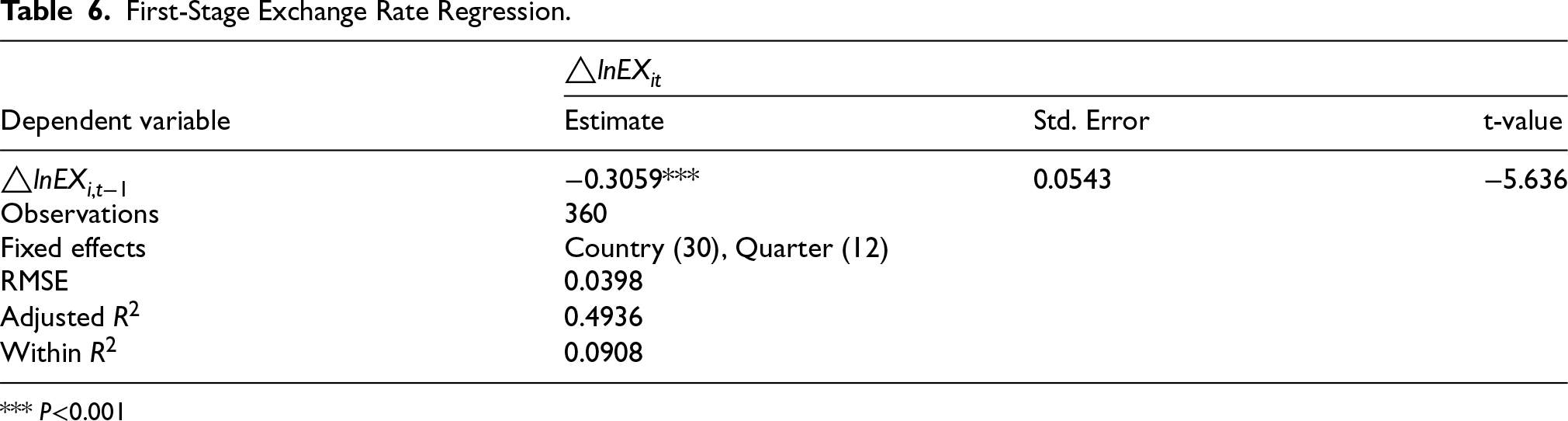

As part of the two-stage estimation strategy, the first step models the dynamics of exchange-rate based on random walk model. 3 Table 6 presents the results of the estimation of the model.

First-Stage Exchange Rate Regression.

First-Stage Exchange Rate Regression.

*** P<0.001

The coefficient on lagged exchange-rate growth is negative and highly significant. This indicates a strong mean-reverting pattern in quarterly exchange-rate changes: when a currency appreciates (or depreciates) in one quarter, it tends to partially reverse in the following quarter.

This pattern is consistent with established findings in international finance, where short-term exchange-rate movements often overshoot and subsequently correct (Dornbusch, 1976; Engel & West, 2005). The predicted value of this regression is used as a proxy of the change in exchange rate in the second stage of the PSTR estimation.

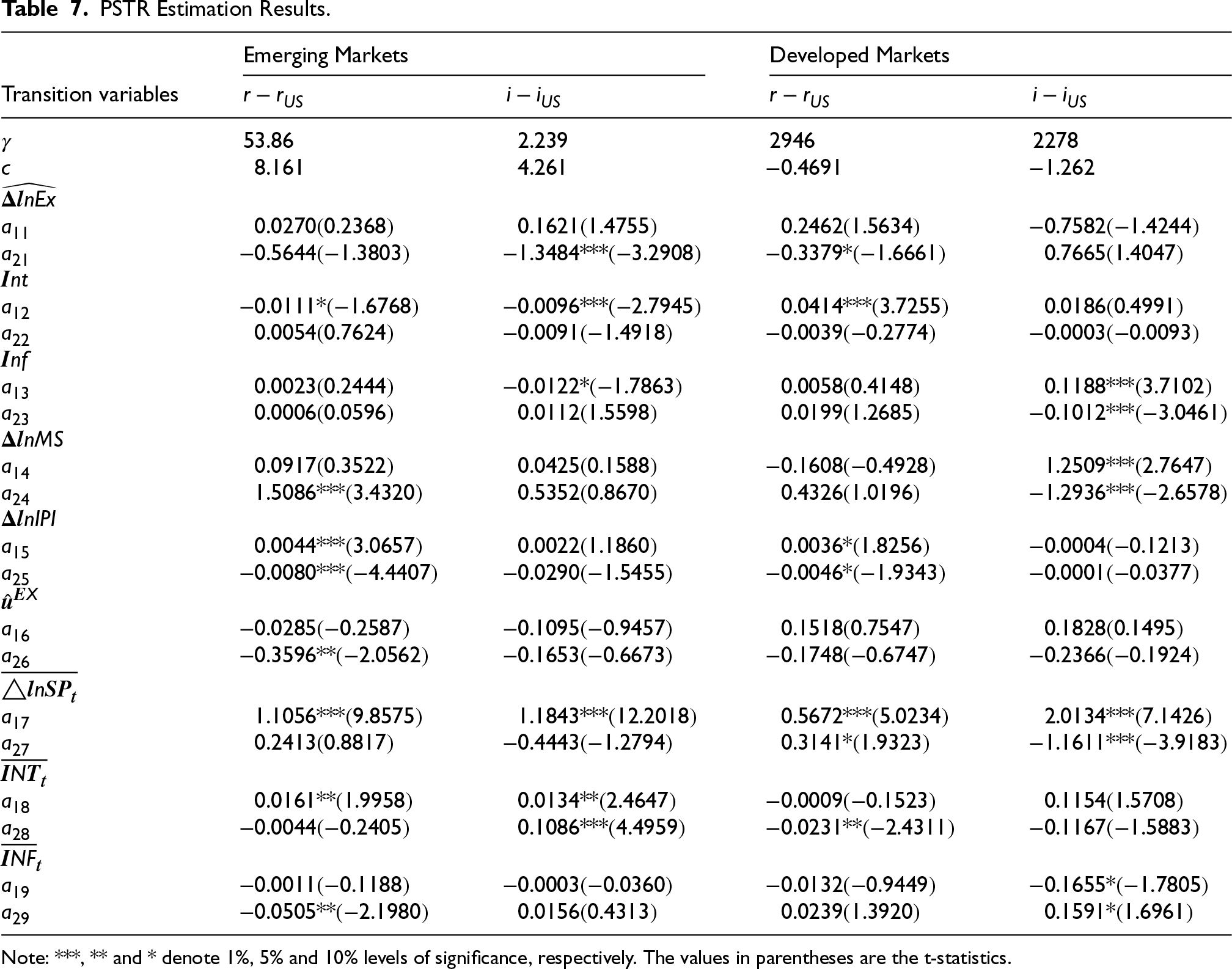

The estimation of the results of the second -stage PSTR augmented with cross sectional average, as in Equation 6, is presented in Table 7. The results highlight significant differences between emerging and developed markets. For emerging markets, the transition speed parameter

PSTR Estimation Results.

Note: ***, ** and * denote 1%, 5% and 10% levels of significance, respectively. The values in parentheses are the t-statistics.

In developed markets, the

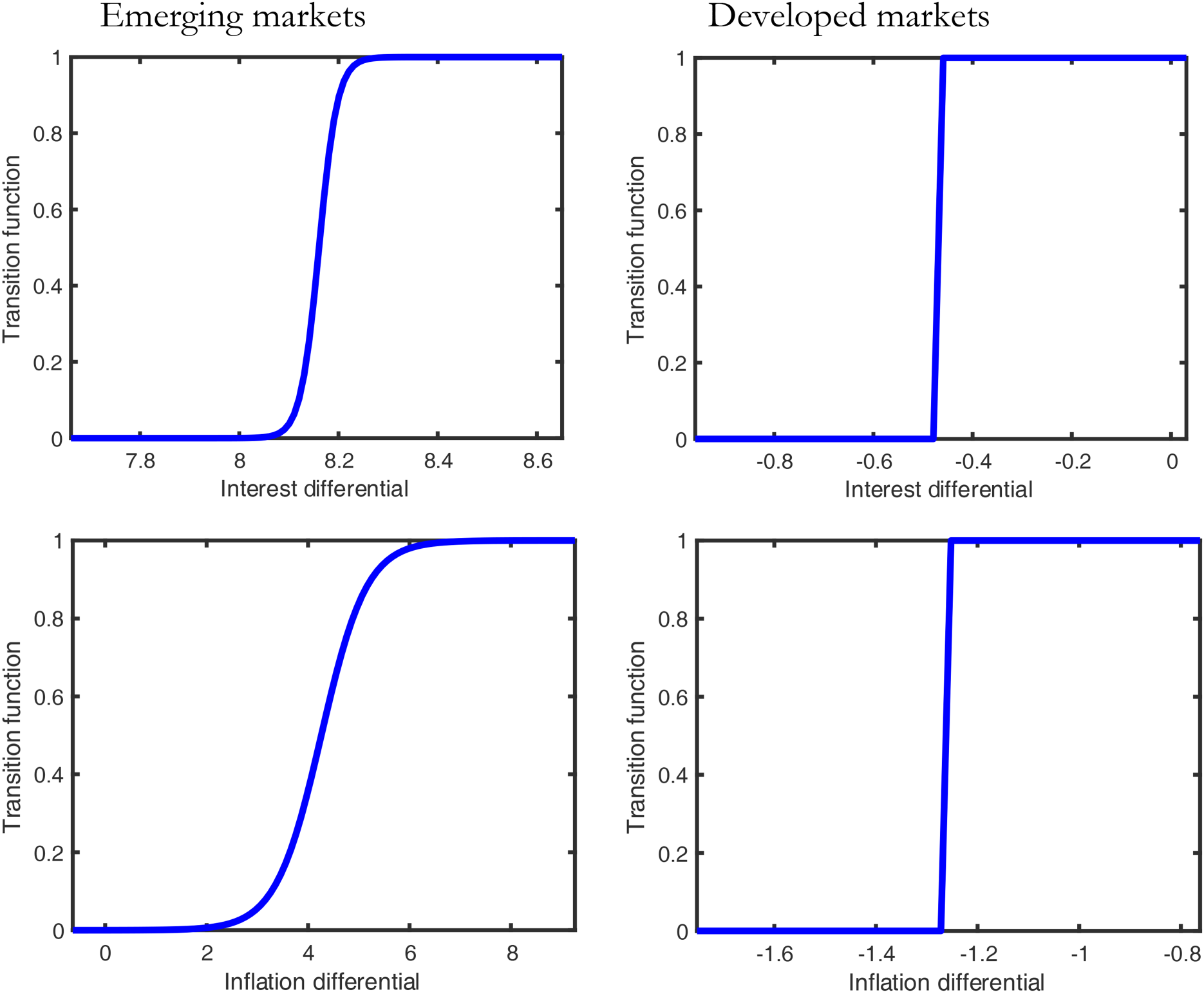

Figure 1 shows that the regime change is abrupt for the two transition variables in developed economies, while it is less abrupt only for interest and inflation differentials in emerging economies, showing high sensitivity of developed markets to specific external shocks.

The transition functions and threshold variables.

For emerging markets, the interest-differential PSTR model reveals notable nonlinear dynamics, as reflected in the relatively large transition parameter (γ=53.86), which indicates a sharp and abrupt shift between regimes once the interest rate differential surpasses the estimated threshold (c = 8.161). The estimated coefficients for the lower and upper regimes, a11 = 0.0270 and a21 = - 0.5644, respectively, suggest that the marginal effect of exchange rate changes on stock returns would shift substantially across regimes. However, both coefficients are statistically insignificant, implying that the influence of exchange rate movements on stock returns does not meaningfully depend on the level of interest rate differentials in emerging markets.

This result suggests that interest rate spreads relative to the United States may not be the main driver of exchange rate–stock return linkages in these economies. Instead, exchange rate fluctuations in emerging markets may respond more strongly to alternative macroeconomic fundamentals. Consistent with this interpretation, Bonga-Bonga (2019) demonstrates that exchange rate movements in many emerging economies are highly sensitive to shifts in the current account, particularly changes in imports and exports. This evidence supports the view that trade-related fundamentals, rather than interest rate differentials, may be the dominant channel through which exchange rate variations influence stock returns in emerging economies.

Emerging Markets – Inflation Differential

For emerging markets, the PSTR model uses the inflation differential as the transition variable indicates pronounced nonlinear behaviour. The transition parameter

This result indicates that when the inflation differential between emerging markets and the United States exceeds approximately 4.26%, exchange rate depreciation reduces stock market returns. Below this threshold, the effect of currency depreciation is effectively zero. The findings therefore suggest that depreciation becomes harmful only when it is associated with heightened inflationary pressures. In such conditions, rising inflation erodes real returns, increases uncertainty, and discourages investment—leading to a crowding-out effect in emerging market stock markets, including those in Africa.

While earlier studies argue that exchange rate depreciation can stimulate stock market activity by improving export competitiveness and attracting foreign investment (van Pham & Delpachitra, 2014; Zarei et al., 2019), the present results highlight an important nuance: depreciation accompanied by high inflation has the opposite effect. Under these circumstances, investors may withdraw from equity markets and reallocate their portfolios to safer or more stable equity markets.

Developed Markets – Interest Rate Differential

The findings for developed economies reveal that the relationship between exchange rate fluctuations and stock market returns varies meaningfully across the two regimes defined by the interest rate differential with the United States. When the differential is low, exchange rate movements do not significantly affect stock returns. This result may reflect a degree of return equalisation across developed markets, where interest rate convergence contributes to similar real returns and reduces the sensitivity of equity markets to currency fluctuations.

In contrast, when the interest rate differential is high, exchange rate fluctuations exert a negative long-run effect on stock market performance. This outcome is consistent with the dynamics of carry trade activity. Although carry trade strategies—where investors borrow in low-interest-rate currencies and invest in high-interest-rate markets—can initially generate capital inflows that support stock prices, the eventual unwinding of these positions tends to reverse these gains. As investors close their profit positions, capital outflows may occur, placing downward pressure on equity markets. This mechanism aligns with the evidence presented by Bonga-Bonga and Rangoanana (2022), who show that high-interest-rate environments may attract short-term speculative inflows but do not necessarily support sustained stock market performance.

Developed Markets – Inflation Differential

The results reported in Table 7 show that, in general, exchange rate fluctuations do not impact on stock return in developed economies through inflation differential between developed economies and the United States. Below or above the threshold determined by this differential, exchange rate fluctuations do not impact on stock market returns in developed economies. This result suggests that in developed economies, inflation differentials relative to the United States do not constitute an important channel through which exchange rate fluctuations influence stock market returns. The absence of significant effects below or above the estimated threshold reflects the structural stability of advanced economies, where inflation is typically low, well anchored, and subject to strong monetary policy credibility. Because exchange rate pass-through to domestic prices is limited and inflation expectations remain stable, currency movements do not generate the type of inflationary pressures that would materially affect equity valuations. As a result, stock markets in developed economies remain largely insulated from exchange rate shocks operating through inflation differentials.

Although the central contribution of this paper lies in assessing how exchange rate fluctuations affect stock returns across thresholds defined by interest rate and inflation differentials, several additional findings merit attention. For instance, the results in Table 7 indicate that increases in money supply in developed economies are associated with higher stock returns when the inflation differential with the United States is low. This outcome reflects the classic liquidity effect: an expansion in money supply lowers financing costs, boosts market liquidity, and encourages greater participation in equity markets (Naik & Reddy, 2021). However, this positive effect diminishes when the increase in money supply becomes inflationary. As inflation differentials rise, the stimulatory impact of liquidity is offset by higher uncertainty, reduced real returns, and the potential for monetary tightening, which together weaken the beneficial influence of money supply growth on stock performance.

Robustness Check

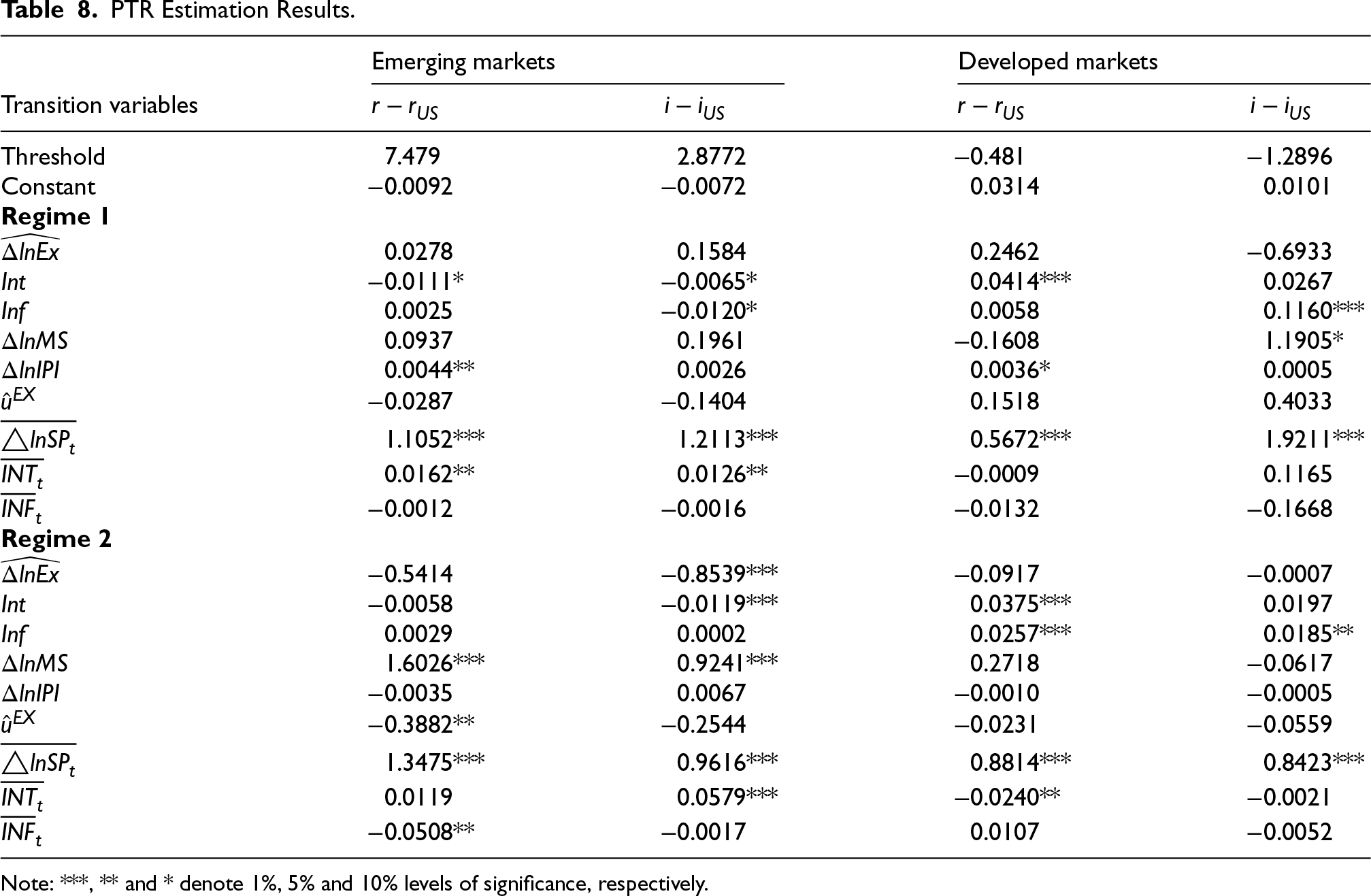

This robustness check compares the PSTR model with the PTR model, both capturing non-linear relationships differently—PSTR allows smooth transitions, while PTR enforces sharp regime shifts. The high transition parameter γ in the PSTR model suggests a steep shift, making PTR a natural alternative.

The goal is to verify if the non-linear patterns in PSTR hold under PTR. As shown in Table 8, both models yield similar estimates, confirming that the findings are not heavily model-dependent. More importantly, the robustness check reveals that the policy implications drawn from the PSTR model remain qualitatively and quantitatively consistent when using the PTR model.

PTR Estimation Results.

PTR Estimation Results.

Note: ***, ** and * denote 1%, 5% and 10% levels of significance, respectively.

The QTE in the context of this study evaluates how the impact of exchange rate fluctuations on stock returns differs across the distribution of stock market returns. Specifically, it measures the difference at a given quantile of the stock return distribution between the treatment group—countries characterised by high exchange rate volatility—and the control group—countries with relatively low exchange rate volatility. The underlying hypothesis is that the effect of exchange rate changes on stock returns is not uniform but conditional on both the level of exchange rate volatility and the position of the stock market in its return distribution. For instance, the effect may be more pronounced during extreme market conditions, such as bear markets (lower quantiles) or bull markets (upper quantiles), compared to median states.

In this framework, emerging markets are designated as the treatment group due to their typically higher exchange rate volatility, while developed economies serve as the control group given their comparatively more stable exchange rate dynamics. By applying the QTE methodology, the analysis captures heterogeneous effects across market conditions, providing deeper insights into whether exchange rate shocks exert asymmetric influences on stock returns depending on both the volatility environment and the prevailing phase of the market cycle.

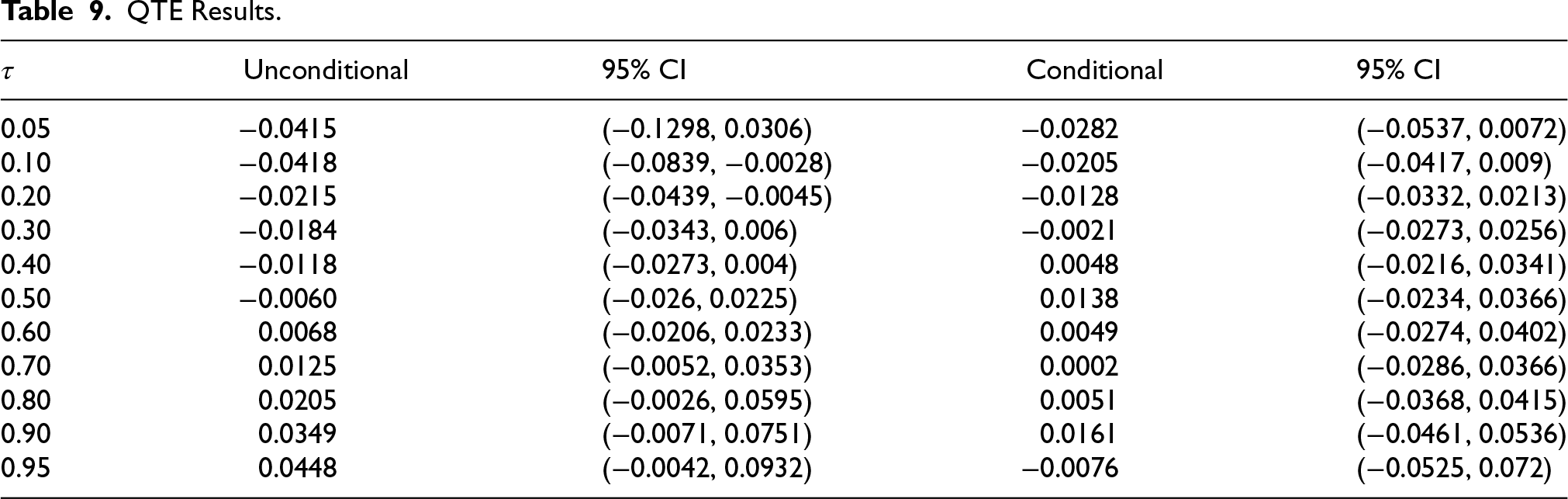

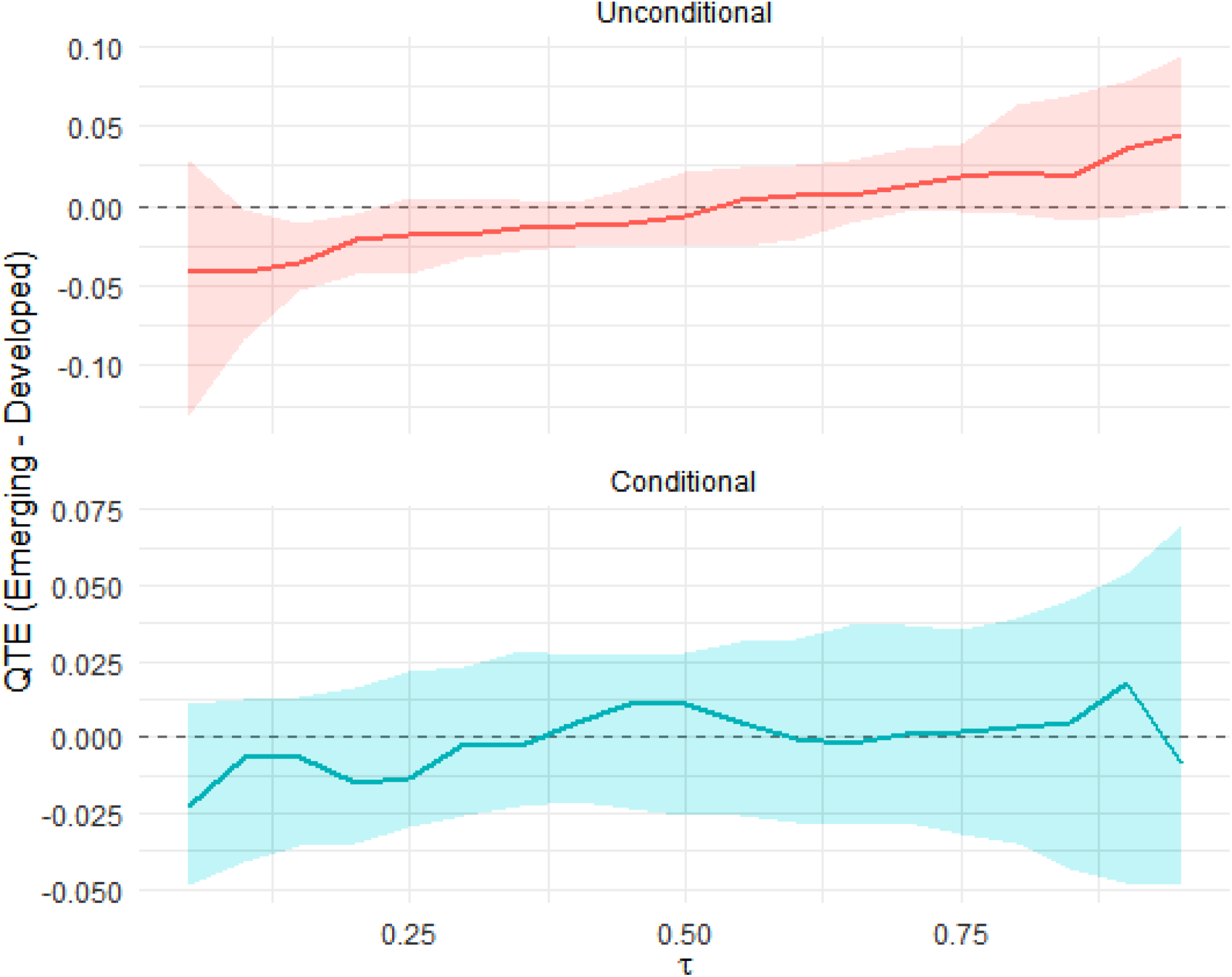

The results of the QTE based on the estimation of Equations 11 and 12 are reported in Figure 2 and Table 9, showing the results of the unconditional QTE and conditional QTE. It is worth noting that the estimation covers the period from 2019Q1 to 2021Q4 to include COVID-19 periods. Lower quantiles reflect bear markets, and higher quantiles indicate bull markets.

QTE Results.

QTE Results.

Plots of the unconditional and conditional quantile treatment effects of emerging markets on stock returns with 95% bootstrap confidence intervals (cluster bootstrap by country).

The results reported in Figure 2 show that, in the case of the unconditional QTE, exchange rate changes lead to lower stock returns for emerging markets (countries with higher exchange rate volatility) compared to developed economies during the bear market. This negative effect is statistically significant at the 10% and 20% quantiles, which correspond to bearish market conditions. However, at higher quantiles, the results indicate that exchange rate changes are associated with higher stock returns for emerging markets compared to developed economies. A similar pattern is observed in the case of the conditional QTE, but with some notable differences. In particular, the reduction in stock returns for emerging markets relative to developed economies is less pronounced under the conditional QTE, suggesting that macroeconomic variables reduce the adverse effects of exchange rate volatility during bear markets. Moreover, these macroeconomic variables substantially reduce the emerging-market premium during bull markets, as shown by the comparison between the magnitudes of unconditional and conditional QTE in the upper quantiles.

This finding highlights the asymmetric nature of the relationship between exchange rate fluctuations and stock market performance across different market states. Emerging markets are more vulnerable to exchange rate shocks because their financial systems tend to be less mature, with weaker hedging mechanisms, higher exposure to foreign capital flows, and greater dependence on imported goods and services. During bear markets, these structural vulnerabilities amplify the negative effects of exchange rate volatility, particularly when combined with unfavourable macroeconomic conditions such as inflationary pressures, current account imbalances, or policy uncertainty. The conditional QTE results underscore this point by showing that macroeconomic fundamentals not only intensify the adverse effects during downturns but also limit the potential gains during bullish phases. In contrast, developed economies benefit from stronger institutional frameworks, deeper financial markets, and more effective macroeconomic policies, which mitigate the negative consequences of exchange rate fluctuations and allow for more stable performance across the return distribution.

In addition, these results provide empirical support for the well-documented principle of “high risk, high returns” in the context of emerging markets. During bullish phases, emerging markets consistently outperform developed economies, underscoring their potential for superior returns when both global and domestic conditions are favourable. This performance can be interpreted as a compensation for the higher risk premium that investors demand when allocating capital to markets characterised by greater exchange rate volatility, institutional weaknesses, and macroeconomic instability. In other words, although emerging markets expose investors to heightened uncertainty and vulnerability to shocks, the higher risk premium ensures that, when risks do not materialise or when growth prospects are strong, investors are rewarded with returns that exceed those available in more stable developed markets. However, the findings of this paper reveal that, contrary to the common belief, the principle of “high risk, high return” in emerging markets does not hold uniformly across all market conditions. Instead, it applies primarily during bullish phases, where favourable global and domestic environments allow investors to be compensated for the higher risk premium associated with these markets. In bearish conditions, however, the elevated risks of exchange rate volatility and macroeconomic fragility are not offset by higher returns; rather, they translate into disproportionately larger losses compared to developed economies. This asymmetry underscores the conditional nature of the risk–return trade-off in emerging markets.

This study set out to examine how exchange rate fluctuations influence stock returns in developed and emerging economies by explicitly accounting for threshold effects generated by interest rate and inflation differentials relative to the United States. A second objective was to assess whether these effects differ across the return distribution, particularly during bearish and bullish market conditions. To achieve these goals, the study proposed a two-stage CCE-augmented PSTR model that simultaneously addresses endogeneity and strong CSD—features that characterise globally integrated financial markets. Complementing this approach, QTE analysis was employed to capture distributional heterogeneity between emerging and developed markets.

The empirical results reveal substantial nonlinearities. In emerging markets, inflation differentials play a decisive role: exchange rate depreciation reduces stock returns only when the inflation gap exceeds a critical threshold, highlighting the vulnerability of these markets to inflation-driven macroeconomic instability. Developed markets, by contrast, are more sensitive to interest rate differentials, with high differentials amplifying the negative effect of exchange rate fluctuations—consistent with the unwinding of carry-trade positions. QTE estimates further show that emerging markets underperform during bearish regimes due to heightened exchange rate volatility but outperform during bullish regimes, reflecting a conditional rather than uniform high-risk, high-return pattern.

These results yield several policy insights. Emerging economies should prioritise inflation stabilisation to prevent exchange-rate-induced erosion of equity market performance. Strengthening monetary policy credibility, improving inflation-targeting frameworks, and expanding market-based hedging instruments can mitigate downside risks. Developed economies, where interest rate differentials matter more, should monitor capital flow dynamics and carry-trade exposures, particularly during periods of monetary policy divergence with the United States. For investors and portfolio managers, the evidence underscores the need for regime-aware strategies that account for asymmetric responses across market states, especially when allocating assets across emerging and developed markets.

Overall, the study advances the understanding of macro-financial transmission mechanisms by showing that exchange rate effects on stock returns are not linear, uniform, or universal, but instead conditioned by structural characteristics, macroeconomic thresholds, and market regimes.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Notes

Appendix

Summary of Existing Literature.

| Study | Methodology | Country/Region | Period | Key Findings |

|---|---|---|---|---|

| Bahmani-Oskooee and Saha (2016) | NARDL | U.S. | 1973–2014 | Short-run asymmetry in ER–stock link |

| Moussa and Delhoumi (2022) | NARDL | MENA | 2000–2019 | Short-run asymmetric effects |

| Dang et al. (2020) | NARDL | Vietnam | 2000–2018 | Short- and long-run asymmetries |

| Ahmed (2020) | NARDL | Egypt | 1994–2018 | Asymmetries differ by ER regimes |

| Yau and Nieh (2009) | Threshold cointegration | Taiwan/Japan | 1993–2007 | Asymmetry only in Taiwan |

| Kollias et al. (2016) | TECM | Norway/UK | 1999–2015 | Stronger linkages during crises |

| Chkili and Nguyen (2014) | Markov-switching | BRICS | 1997–2013 | Regime-dependent interactions |

| Salisu and Vo (2021) | Panel ARDL (rate regimes) | Global | 1995–2020 | Different short-/long-run effects in low/high rates |

| da Silva (2023) | Regime-switching | Brazil/Mexico | 2003–2021 | Asymmetric effects across volatility states |