Abstract

This research utilizes Coronary Artery Risk Development in Young Adults (CARDIA) cohort study data to examine whether financial strain is associated with subsequent lower urinary tract symptoms among men and whether healthcare barriers, health risk behaviors, and comorbid conditions explain this association. CARDIA recruited Black and White participants aged 18 to 30 years at baseline (1985–1986) from four United States cities. The analytic sample was comprised of men with complete data for analyses involving financial strain trajectories across 7 assessments (n = 602) and mediation tests of data collected at 4 assessments (n = 634). The outcome variable, assessed when the mean age of men was 50 years, was the American Urologic Association Symptom Index score, recoded into four symptom categories: none (6.3%); mild (62.6%), moderate (28.5%), and severe (2.6%). Symptom category was regressed on financial strain variables, adjusting for age, race, education, and self-reported benign prostatic hyperplasia. Regression analyses and structural equation modeling tested potential mediators. Compared to not being financially strained across early and midlife adulthood, experiencing more than one shift in financial strain was associated with 84% greater odds (95% confidence interval [1.24, 2.75]) of being categorized into a worse symptom category. Structural equation modeling showed that both difficulty receiving healthcare and depressive symptoms explained an association between difficulty paying for medical care and worse symptoms. Additional research is needed to confirm findings and examine other mechanisms that may further explain associations between financial strain and symptoms, such as stress responses. Accumulated evidence may inform future prevention interventions, including integrated healthcare approaches.

Introduction

Lower urinary tract symptoms (LUTS) encompass frequent and/or urgent urination, difficulty urinating, bladder or urethral pain before, during, or after urination, and urinary incontinence (UI) (Cardozo et al., 2023). Symptoms of frequency, urgency, and difficulty urinating are particularly common among men, while symptoms of bladder or urethral pain and incontinence are less common. In one population-based study of adults aged 40 and older in the United States, United Kingdom, and Sweden, 20% and 22% of men reported frequent and urgent urination, respectively; 28% reported waking 2 or more times at night to urinate; and 20%, 19%, and 27% reported hesitancy, intermittency, or a weak stream while urinating, respectively (Coyne et al., 2009). In contrast, 5% and 3% of men reported bladder or urethral pain, respectively, and 9% reported urgency UI, at least sometimes (Coyne et al., 2009). In another population-based study of Columbian adults aged 18 and above, 6% and 24% of men reported overactive bladder (i.e. frequent and/or urgent urination) with and without UI, respectively (Plata et al., 2019).

Different indicators of financial strain, including poverty, financial insecurity, food insecurity, housing insecurity, unreliable transportation, and difficulty finding and keeping employment, are associated with overactive bladder (Sebesta et al., 2022; Tellechea et al., 2021; Xiao et al., 2024; Zwaschka et al., 2022), stress UI (urine loss with physical activity or increases in abdominal pressure such as a cough or sneeze) (Cao et al., 2022; Zwaschka et al., 2022), urgency UI (Cao et al., 2022; Lee et al., 2020; Okada et al., 2023; Zwaschka et al., 2022), and LUTS more broadly (Brady, Arguedas, et al., 2024; Brady, Cunningham, et al., 2024; Zwaschka et al., 2022). Most research has been conducted with samples of women (Brady, Arguedas, et al., 2024; Brady, Cunningham, et al., 2024; Tellechea et al., 2021) or women and men combined (Lee et al., 2020; Okada et al., 2023; Sebesta et al., 2022; Xiao et al., 2024; Zwaschka et al., 2022), with less research focused on men (Cao et al., 2022).

A better understanding of mechanisms linking financial strain with LUTS can inform social policies, public health programs, and healthcare approaches to prevent LUTS. Psychological stress (Lee et al., 2020; Sebesta et al., 2022; Tellechea et al., 2021; Zwaschka et al., 2022), physiological stress (Bishehsari et al., 2023; Cohen et al., 2016; O’Connor et al., 2021), constraints on health behaviors and resulting comorbid conditions (Brady, Arguedas, et al., 2024; Cohen et al., 2016), and less access to and ability to utilize healthcare (e.g. self-management of emergent LUTS vs. seeking treatment) (Brady, Arguedas, et al., 2024) have been discussed as potential mechanisms by which financial strain may become associated with LUTS over time. To date, however, almost no research has examined potential mechanisms linking financial strain with LUTS. Among women in the Coronary Artery Risk Development in Young Adults (CARDIA) cohort, higher levels of financial strain across early and midlife adulthood were associated with a greater likelihood of experiencing more severe LUTS with a greater impact on well-being at midlife (Brady, Arguedas, et al., 2024). Women’s financial strain led to underutilization of healthcare (i.e. not seeking healthcare because it was not covered by insurance or was too expensive) and health risk behaviors and comorbid conditions, which in turn led to more burdensome LUTS and impact.

The purpose of the present study is to examine whether trajectories of financial strain across 25 years are associated with subsequent LUTS among men in the CARDIA cohort study, as well as mechanisms that could explain this association. Individuals of male versus female biological sex are at risk for different LUTS due to differences in anatomy and physiology of the urogenital system, as well as women’s experience of pregnancy and childbirth (Altman et al., 2023). This study adds to research examining the association between financial strain and LUTS among men, specifically (Cao et al., 2022). It also examines whether mechanisms linking financial strain to men’s LUTS are similar to those linking financial strain to women’s LUTS.

Methods

Procedure

CARDIA is a prospective cohort study that recruited 5,115 Black and White women and men aged 18 to 30 years at baseline (1985–86; Year 0) from the populations of four U.S. cities (Birmingham, AL; Minneapolis, MN; Chicago, IL; Oakland, CA) (Friedman et al., 1988). In-person follow-up examinations were conducted 2, 5, 7, 10, 15, 20, and 25 years after baseline with response rates of 91%, 86%, 81%, 79%, 74%, 72%, and 72% of the surviving cohort, respectively. Written informed consent was obtained at each exam, and the IRB at each center approved study protocols.

Following the Year 25 (2010–2011) examination, an IRB-approved ancillary study collected data on LUTS among CARDIA participants via questionnaire mailings between March 2012 and February 2013. Out of the 1,517 surviving CARDIA men available at the Year 25 examination, LUTS questions were completed by 996 men, 939 of whom had complete data (61.9%).

Measures

Lower Urinary Tract Symptoms

The presence and severity of Lower Urinary Tract Symptoms (LUTS) were measured with the American Urologic Association Symptom Index score, which includes storage symptoms (urgency, frequency, nocturia), emptying symptoms (hesitancy, intermittency, and weak stream), and a post-micturition symptom (incomplete emptying) assessed across the past month with response options related to frequency: “not at all, less than 1 in 5 times, less than half the time, about half the time, more than half the time, and almost always” (Barry et al., 2008). Summed scores could range from 0 to 35. Scores from men with complete LUTS data were recoded into four symptom categories: none (score of 0; n = 59, 6.3%), mild (score of 1 to 7; n = 588, 62.6%), moderate (score of 8 to 19; n = 268, 28.5%), severe (score of 20–35; n = 24, 2.6%).

Financial Strain

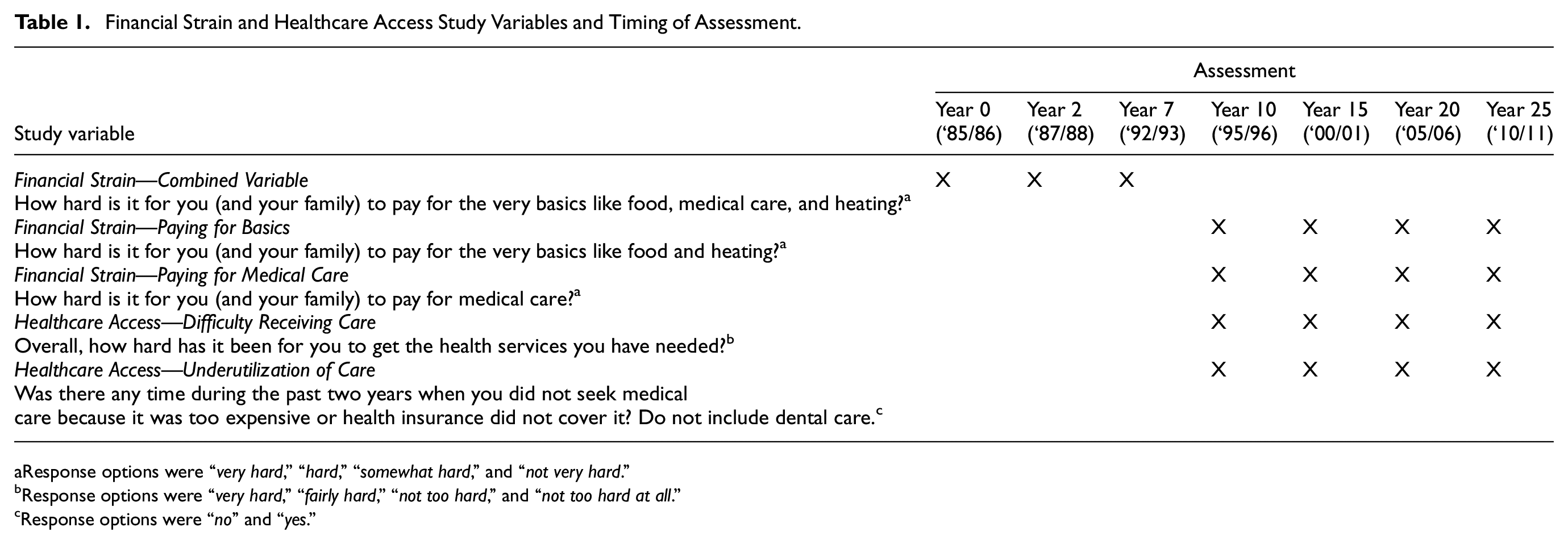

Financial strain was assessed through 1 to 2 questions at different assessments (Table 1). Responses were coded to create dichotomous variables, with “not very hard” coded as 0 (reference group) and other responses coded as 1. To facilitate the creation of a financial strain trajectory group variable, a combined financial strain indicator was created for Years 10, 15, 20, and 25 (Table 2). If participants indicated any response other than “not very hard” for either paying for the very basics or medical care, they received a value of 1; otherwise, they received a value of 0. Five financial strain trajectory groups were created to characterize dichotomized responses to questions at Years 0, 2, 7, 10, 15, 20, and 25: consistently not strained (values of 0 across all seven assessments), consistently strained (values of 1 across all seven assessments), a single shift into being financially strained (values of 0 followed by one or more values of 1), a single shift into not being financially strained (values of 1 following by one or more values of 0); and more than one shift in strain (all remaining patterns). In addition to being classified into a financial strain trajectory group, respondents were assigned a value for another variable indicating the number of seven assessments at which they reported financial strain. For planned mediation analyses, two financial strain variables (difficulty paying for the very basics, and difficulty paying for medical care) were additionally created by summing across Year 10 and Year 15 values.

Financial Strain and Healthcare Access Study Variables and Timing of Assessment.

Response options were “very hard,” “hard,” “somewhat hard,” and “not very hard.”

Response options were “very hard,” “fairly hard,” “not too hard,” and “not too hard at all.”

Response options were “no” and “yes.”

Financial Strain, Healthcare Access, Comorbidity Index, and Depressive Symptom Variables by Year of Assessment, within the Total Sample and by 2012–13 LUTS Category.

At Years 0, 2, and 7, participants were asked, “How hard is it for you (and your family) to pay for the very basics like food, medical care, and heating?” At Years 10, 15, 20, and 25, separate questions were asked about difficulty paying for the “very basics like food and heating” and difficulty paying for “medical care.” To facilitate the creation of the financial strain trajectory group variable, a combined financial strain indicator was created for Years 10, 15, 20, and 25. If participants indicated any response other than “not very hard” for either paying for the very basics or medical care, they received a value of 1; otherwise, they received a value of 0.

Healthcare Access (Proposed Mediator)

For difficulty receiving care (Table 1), responses were coded to create a dichotomous variable, with “not too hard” and “not too hard at all” coded as 0 (reference group) and other responses coded as 1. For underutilization of care (Table 1), response options were “no” (coded 0) and “yes” (coded 1). For planned mediation analyses, two healthcare access variables (difficulty receiving care and underutilization of care) were created by summing Year 20 and Year 25 values.

Comorbidity Index and Depressive Symptoms (Proposed Mediators)

Separately for Years 10, 15, 20, and 25, a comorbidity index was created by combining the following behaviors and health conditions: smoking, physical inactivity, body mass index, hypertension, and diabetes. Smoking categories were based on American Heart Association (AHA) criteria (Lloyd-Jones et al., 2010). Physical activity was self−reported as the frequency of participation over the prior 12 months in vigorous and moderate-intensity activities and reported as a score in exercise units using the validated CARDIA Physical Activity History (Jacobs et al., 1989). Participants were categorized as inactive (<100 exercise units, poor), active but not meeting guidelines (100−299 exercise units, intermediate), and meeting guidelines (≥300 exercise units, ideal) to approximate AHA criteria for physical activity (Lloyd-Jones et al., 2010). Body mass index was calculated as body weight (in kilograms) divided by the square of a participant’s height (in meters). Hypertension was defined as present (score of 1 vs. 0) when systolic blood pressure was measured at 140 mmHg or greater, diastolic blood pressure was measured at 90 mmHg or greater, or the participant reported taking hypertensive medications. Diabetes was defined as present (score of 1 vs. 0) when fasting glucose was greater than or equal to 126 mg/DL, a 2-hr glucose tolerance test yielded a finding greater than or equal to 200 mg/DL, or the participant’s hemoglobin HbA1c was greater than or equal to 6.5%. Variables for behaviors and health conditions were converted to standardized z-scores and averaged within the assessment; the result was then standardized (Little et al., 2013).

Depressive symptoms were examined separately from other health conditions because previous analyses showed that depressive symptoms, but not other cardiovascular disease risk factors, were associated with CARDIA men’s LUTS (Markland et al., 2024). Depressive symptoms were assessed with the 20-item Center for Epidemiologic Studies-Depression Scale (CES-D) (Radloff, 1977).

For planned mediation analyses, Year 20 and Year 25 standardized comorbidity indices were averaged; the result was then standardized. Year 20 and 25 depressive symptoms were also averaged and standardized.

Analytic Approach

The analytic sample was comprised of men with complete data for exposure and outcome variables. Preliminary analyses examined distributions of study variables within the total analytic sample and by LUTS category, and whether variable distributions differed by race. To test research questions, proportional odds logistic regression analyses were first conducted. One set of analyses adjusted for Year 25 age, race (Black vs. White), and Year 25 education (high school or less, some college, college graduate); a separate set of analyses additionally adjusted for self-reported benign prostatic hyperplasia (BPH), assessed at the same time as LUTS. The proportional odds assumption was tested and not violated for logistic regression analyses. Structural equation modeling was then conducted to simultaneously estimate the direct and indirect effects of financial strain variables on LUTS for those mediation pathways supported through regression analyses. Regression analyses were conducted using R version 4.3. SEM models were fit using the lavaan package in R.

Financial Strain Analyses Utilizing Years 0 to 25

LUTS was regressed on the financial strain trajectory group variable, with “consistently not strained” as the reference group. Separately, LUTS was regressed on the number of assessments at which participants reported financial strain.

Mediation Analyses Utilizing Years 10 to 25

Eight mediation models were fit to analyze the potential association between a single financial strain variable (difficulty paying for the very basics, difficulty paying for medical care) and LUTS, adjusting for a single healthcare access variable (difficulty receiving care or underutilization of care), the comorbidity index, or depressive symptoms. Formal tests of mediation were conducted when the magnitude of the effect of the financial strain variable was reduced with further adjustment for a given proposed mediator. A bootstrap was conducted, using 1,000 resamples, to calculate the difference in financial strain coefficients when adjusting versus not adjusting for the healthcare access, comorbidity index, or depressive symptoms variable. A 95% confidence interval for this difference was obtained from the bootstrap using the percentile method (Efron & Tibshirani, 1993).

Mediation Analyses Utilizing Structural Equation Modeling

A two-stage limited information approach was applied. In the first stage, the polychoric correlation matrix was estimated (Olsson, 1979); in the second stage, model parameters were estimated from the correlation matrix (Jöreskog, 1994). The model was saturated to avoid potential bias in parameter estimates due to model misspecification. Results for indirect effects were verified using a non-parametric bootstrap, as indirect effects have asymmetrical distributions of the standard error (MacKinnon et al., 2004).

Results

The analytic sample size was 602 for analyses involving trajectories of financial strain and the number of assessments at which participants experienced financial strain, and 634 for analyses involving mediation tests. Compared to the 305 men with outcome data who were not in either analytic sample, men in the analytic samples were slightly older by the Year 25 assessment (mean age 50.3 vs. 49.3 years); in addition, a greater percentage were White (64.4% vs. 44.6%) and college graduates (56.6% vs. 36.1%), and a smaller percentage reported difficulty paying for the very basics (21.8% vs. 29.4%), difficulty paying for medical care (28.7% vs. 38.9%), and difficulty receiving healthcare (7.9% vs. 14.0%) at the Year 25 assessment (all p-values < .05). There was no statistically significant difference in underutilization of healthcare at Year 25 between men who were in (12.1%) versus not in (15.3%) the analytic samples.

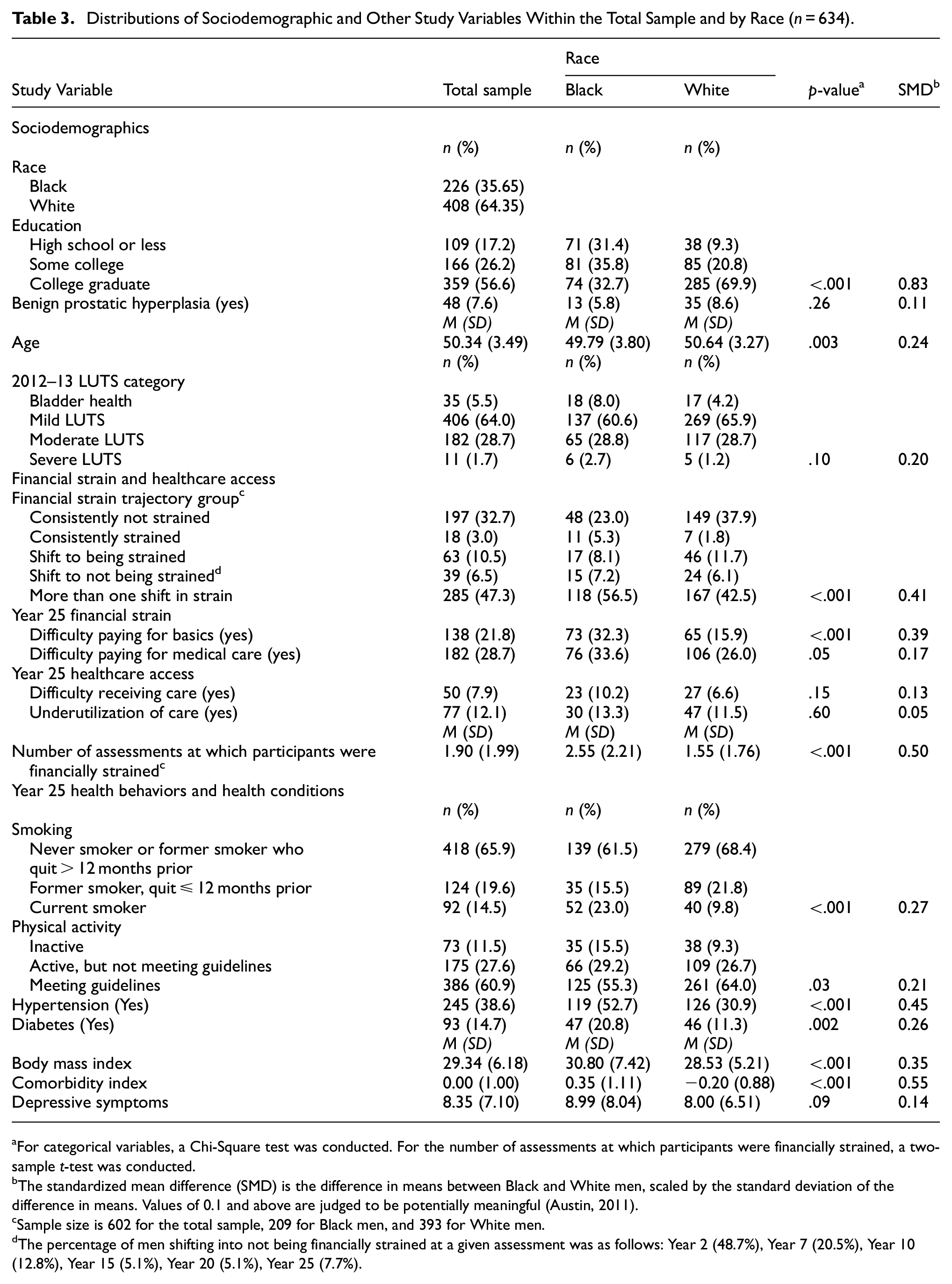

Table 2 shows financial strain, healthcare access, comorbidity index, and depressive symptom variables by year of assessment, within the total sample and by 2012–13 LUTS category. Table 3 shows that Black and White men did not differ with respect to LUTS category. Significant differences showed that a smaller percentage of Black men than White men reported lack of financial strain across all 7 assessments, and a greater percentage reported more than one shift in strain. Black men (M = 2.5, SD = 2.2) also reported financial strain at a greater number of assessments in comparison to White men (M = 1.5, SD = 1.8; see bottom of the table). At Year 25, a greater percentage of Black men than White men reported difficulty paying for basics and paying for medical care. Black and White men did not differ statistically with respect to reports of difficulty receiving healthcare and underutilization of healthcare. A greater percentage of Black men than White men reported poorer health behaviors and health conditions; depressive symptoms did not differ statistically by racial identity.

Distributions of Sociodemographic and Other Study Variables Within the Total Sample and by Race (n = 634).

For categorical variables, a Chi-Square test was conducted. For the number of assessments at which participants were financially strained, a two-sample t-test was conducted.

The standardized mean difference (SMD) is the difference in means between Black and White men, scaled by the standard deviation of the difference in means. Values of 0.1 and above are judged to be potentially meaningful (Austin, 2011).

Sample size is 602 for the total sample, 209 for Black men, and 393 for White men.

The percentage of men shifting into not being financially strained at a given assessment was as follows: Year 2 (48.7%), Year 7 (20.5%), Year 10 (12.8%), Year 15 (5.1%), Year 20 (5.1%), Year 25 (7.7%).

Table 4 shows the association of the financial strain trajectory variable, representing strain between Year 0 (1985–86) and Year 25 (2010–11), with 2012–13 LUTS. In comparison to men who were consistently not strained, men who experienced more than one shift in strain had 84% greater odds (95% CI [1.25,2.74]) of belonging to a worse LUTS category (i.e. experiencing a higher number of and more frequent LUTS). For each additional assessment at which men reported financial strain, they had 13% greater odds (95% CI [1.04,1.24]) of membership to a worse LUTS category (see bottom row). The same pattern of associations was observed with adjustment for BPH.

Associations of financial strain trajectory variables with 2012–13 LUTS category membership among CARDIA men with complete data, with and without adjustment for benign prostatic hyperplasia (BPH) (n = 602).

Table 5 shows the association of financial strain, healthcare access barriers, poor health behaviors and health conditions (comorbidity index), and depressive symptoms, assessed between Year 10 (1995–96) and Year 25 (2010–11), with 2012–13 LUTS. When examined separately, difficulty paying for medical care, both healthcare access barriers (difficulty receiving healthcare, underutilization of healthcare due to cost and lack of coverage), the comorbidity index, and depressive symptoms were each associated with greater odds of belonging to a worse LUTS category. The odds ratios for difficulty paying for the very basics (OR = 1.32; 95%CI [1.00, 1.75]) and medical care (OR = 1.34; 95% CI [1.03, 1.74]) were similar, although the former’s confidence interval was bounded by 1 and statistically non-significant. The same pattern of associations was observed with adjustment for BPH.

Associations of Year 10-Year 25 Financial Strain and Healthcare Access Variables With 2012–13 LUTS Category Membership Among CARDIA Men With Complete Data, With and Without Adjustment for Benign Prostatic Hyperplasia (BPH) (n = 634).

The effect of this financial strain variable was significantly attenuated by the addition of the healthcare access variable.

The effect of this financial strain variable was significantly attenuated by the addition of the depressive symptoms variable.

Mediation tests suggested that difficulty receiving healthcare, underutilization of healthcare, and depressive symptoms each explained the associations of both difficulty paying for basics and difficulty paying for medical care with LUTS (see Table 5, superscripts a and b). For example, after adjusting for difficulty receiving care, a healthcare access barrier, the odds of belonging to a worse LUTS category for each assessment at which participants reported difficulty paying for medical care was reduced by roughly 75% (odds ratios of 1.34 and 1.36, without and with BPH adjustment, were reduced to 1.09 and 1.08; see Table 5, mediation test 5). The comorbidity index did not act as a mediator. Across mediation tests, the same pattern of associations was observed with and without adjustment for BPH.

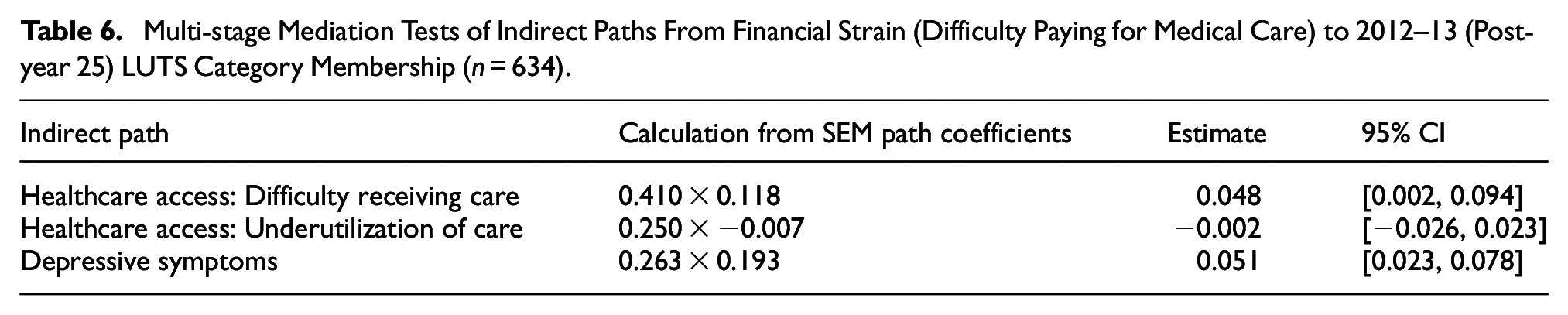

In an initial structural equation model (SEM), difficulty paying for basics and difficulty paying for medical care covaried to a high degree (ρ = .97, p < .01). For this reason, only difficulty paying for medical care was included in the SEM (see Figure 1). Difficulty paying for medical care (Years 10 and 15) and difficulty receiving care (Years 20 and 25) were associated (β = .41, 95% CI [0.32, 0.50]), as was difficulty receiving care and worse LUTS after Year 25 (β = .12, 95% CI [0.01, 0.23]). Difficulty paying for medical care (Years 10 and 15) and depressive symptoms (Years 20 and 25) also were associated (β = .26, 95% CI [0.18, 0.34]), as were depressive symptoms and worse LUTS after Year 25 (β = .19, 95% CI [0.10, 0.28]). These mediation pathways eliminated a direct association between difficulty paying for medical care and LUTS. Multi-stage mediation tests of indirect paths involving difficulty receiving care and depressive symptoms were significant (see Table 6), indicating that these mediators explained the association between financial strain and LUTS category. Although difficulty paying for medical care was associated with underutilization of care, underutilization of care was not associated with LUTS category in the SEM.

Direct and indirect effects of difficulty paying for medical care on 2012–13 LUTS category membership among CARDIA men with complete data (n = 634).

Multi-stage Mediation Tests of Indirect Paths From Financial Strain (Difficulty Paying for Medical Care) to 2012–13 (Post-year 25) LUTS Category Membership (n = 634).

Discussion

Trajectories of financial strain, assessed 7 times across a 25-year period among men, were associated with LUTS, a composite measure assessed in 2012–13, two years after the last assessment of financial strain when the mean age of men was 50 years. Specifically, experiencing more than one shift in financial strain across early and midlife adulthood was associated with over 80% greater odds of being categorized into a worse LUTS category, in comparison to consistently not being financially strained. Separate analyses showed that each assessment at which men reported being financially strained was associated with over 10% greater odds of being categorized into a worse LUTS category. Findings are consistent with previous literature (Brady, Arguedas, et al., 2024; Brady, Cunningham, et al., 2024; Lee et al., 2020; Okada et al., 2023; Sebesta et al., 2022; Tellechea et al., 2021; Xiao et al., 2024; Zwaschka et al., 2022) and extend literature focused specifically on men’s LUTS (Cao et al., 2022).

The primary purpose of this study was to examine mechanisms that may explain an association between financial strain and men’s LUTS. Regression analyses, which examined mediators one by one, showed that associations of different types of financial strain (difficulty paying for basics, difficulty paying for medical care) with LUTS could be explained by three of four examined mediators: difficulty receiving care, underutilization of care, and depressive symptoms. Because difficulty paying for basics and difficulty paying for medical care were highly correlated, structural equation modeling (SEM) focused on difficulty paying for medical care. The SEM analysis examined which of the three mediators supported through regression analyses explained associations between difficulty paying for medical care and LUTS when all mediators were included in the model simultaneously. Two mediation pathways were supported: both difficulty receiving care and depressive symptoms explained the association between difficulty paying for medical care and worse LUTS. Findings among CARDIA men were similar to previously observed findings among CARDIA women (Brady, Arguedas, et al., 2024), in that healthcare barriers and health conditions both mediated the association between financial strain and LUTS for men and women. There were nuanced differences in findings, as well. Difficulty receiving healthcare, rather than underutilization of healthcare, mediated the association between financial strain and LUTS among men. Depressive symptoms, rather than a comorbidity index combining different unhealthy behaviors and health conditions, mediated the association between financial strain and LUTS among men.

Implications for Clinical Practice and Public Health Policies and Programs

Mechanisms linking financial strain to LUTS appear to be biopsychosocial (Engel, 1977) in nature. Corresponding prevention and treatment approaches must consider both the individual and the environment in which the individual is embedded. Men’s reported difficulty receiving healthcare may have been a function of the health policy and services landscape in the U.S. across the past several decades (e.g. concentration of practices and specialists in specific geographic regions; lack of universal healthcare; health insurance policies with inadequate coverage, high deductibles, and high copays) (National Academies of Sciences et al., 2018). Depressive symptoms may be conceptualized as a consequence of financial strain that can cause cumulative damage to biological systems—including brain-bladder communication and lower urinary tract function—through stress responses (Cohen et al., 2016; O’Connor et al., 2021; Smith et al., 2024). Integration of medical care with social care and behavioral health/mental healthcare (Goldman et al., 2022; Thiam et al., 2021) may prove essential to the prevention and treatment of LUTS impacted by financial strain.

Study Limitations and Strengths

A notable limitation of the present study is that LUTS were not assessed during the first 25 years of the CARDIA cohort study, which was designed to study the etiology of cardiovascular disease. This prevented the examination of incident LUTS. While findings are consistent with the idea that financial strain may lead to worse LUTS, it is also conceivable that LUTS may lead to depressive symptoms and financial strain. An additional limitation is that CARDIA men with financial strain were underrepresented in the analytic sample; despite this limitation, observed associations both confirm and extend existing literature. Findings did not take into account adaptive behaviors to accommodate LUTS (e.g. fluid restriction, voiding without urgency to avoid symptoms, and use of absorbent products to manage leakage), which may affect perceived symptoms. In addition, BPH was self-reported, and the present study did not account for prior or current LUTS treatment.

Study strengths include the assessment of LUTS among a community-based sample that was aged 18 to 30 years at the earliest assessment of financial strain. Whereas most studies have examined indicators of financial strain at one point in time, the present study examined financial strain 7 times across 25 years, with the last assessment in 2010–11, after the 2007–09 U.S. economic crisis (Wallace et al., 2022). The present study also examined different potential mediators of associations between financial strain and LUTS.

Conclusions

Difficulty receiving healthcare and depressive symptoms explained an association between financial strain and LUTS among men living in the United States. Research is needed to confirm findings and examine other mechanisms that may further explain the association between financial strain and LUTS, such as stress responses. Research across different countries may be conducted to examine similarities and differences in mechanisms, particularly given the varied healthcare models utilized by different countries. Accumulated evidence may inform future social policies, public health programs, and healthcare practices.