Abstract

This article first expounds the concept of supply chain finance and its credit risk, describes the hierarchical structure of the Internet of Things and its key technologies, and combines the unique functions of the Internet of Things technology and the business process of the inventory pledge financing model to design the supply chain financial model based on the Internet of Things. Then it studies the credit risk assessment under the supply chain financial model based on the Internet of Things, and uses the support vector machine algorithm and Logistic regression method to establish a credit risk measurement model considering the subject rating and debt rating. Finally, an example analysis shows that the credit risk measurement model has a high accuracy rate for determining whether small and medium-sized enterprises in the supply chain financial model based on the Internet of Things are trustworthy. This will facilitate the revision and improvement of the existing credit evaluation system and improve the accuracy of measuring the current financial risk of supply chain. This research adopts the Internet of Things to measure financial credit risk in supply chain and provides a reference for the following researches.

Introduction

With the financing difficulties of small and medium-sized enterprises (SMEs) in traditional financial institutions such as banks, supply chain finance is becoming more and more urgent. Michael refined the definition of supply chain finance and described it as the process of reconfiguring and optimizing costs in a core enterprise-led industry chain. 1 With the development of society, more banks and enterprises will invest in the supply chain financial services. Domestic and foreign scholars have analyzed this financial business from different angles. Berger and Udell 2 first proposed some new ideas and frameworks for SMEs financing, and initially proposed the idea of supply chain finance; Leora Klapper 3 analyzed the mechanism and function of the inventory financial mode adopted by SMEs in the supply chain; Gonzalo Guillén et al. 4 studied short-term supply chain management integrating production and corporate financing plans, and proposed a reasonable supply chain management model that can affect the operation of enterprises and financial financing, thereby increasing overall revenue; Yan and Xu 5 systematically analyzed the financial problems of SMEs from the perspective of supply chain, and conducted evaluation and management research on its credit risk. By analyzing the risk model of accounts receivable financial mode, Wan 6 pointed out that the risk avoidance mechanism of supply chain finance dependence had the possibility of failure, which required banks to establish a new cooperative relationship with core enterprises. Besides, Bao 7 analyzed the causes of financial dilemma of Chinese SMEs and proposed a more operational coping strategy for the problems of supply chain finance in China.

However, how to strengthen the corresponding risk management in combination with the risk source to effectively control the risk is the key to the success of the supply chain financial business. 8 Most of the existing researches have started from the pattern design and analysis of supply chain financial business and failed to propose a systematic evaluation method for risk management. Therefore, combining the functions of the Internet of Things technology theoretically proposes credit risk assessment indicators based on the supply chain financial model of the Internet of Things and establishes a model for risk assessment, which will further deepen existing research and will guide the healthy and orderly development of supply chain financial services in practice. 9 From the actual situation, at present, in the credit evaluation of supply chain financial services, the bank’s choice of indicators and the setting of weights are completely given by experts based on past business experience. This kind of reliance on the expert’s judgment on the business makes the decision too subjective and affects the scientific evaluation of the enterprise.

Based on the above analysis and the credit risk assessment of the traditional financial mode, this article proposes an index system based on the Internet of Things’s supply chain financial credit risk assessment. The support vector machine (SVM) algorithm and Logistic regression method are used to establish a credit risk assessment model, which reduces the current limitations of most of the supply chain financial business metrics relying on expert evaluation. The Logistic regression model, the SVM model, and the integrated analysis method are used to classify whether the customers are trustworthy. By comparing the differences between the supply chain financial model based on the Internet of Things and the SMEs’ compliance probability under the traditional bank credit model, it is revealed that the supply chain finance based on the Internet of Things has alleviated the financing dilemma of SMEs to a certain extent. It also proposes that the construction of the customer’s basic database, which could improve the accuracy of measuring the current financial risk of supply chain, should be strengthened. After that, we will continue to deepen the research on supply chain financial credit risk measurement based on the Internet of Things and improve the accuracy of credit risk prediction model.

Supply chain finance and its credit risk

The concept of supply chain finance

The supply chain describes the process of material flow from the purchase of raw materials, the manufacture, and sale of products to the final consumers. 10 Supply chain finance refers to the practice of core enterprises and financing enterprises with core enterprises as the fulcrum and supply chain trade relations as the link, and provides financing services for other nodal enterprises in the supply chain with the influence of core enterprises. 11

Supply chain finance financing model

According to the specific business process, industrial chain finance can be divided into three modes: accounts receivable mode, inventory pledge mode, and prepayment mode. 12

Supply chain financial credit risk

This article defines the supply chain financial credit risk 13 as follows: based on the supply chain financial business, in the process of financing credits for SMEs in the supply chain by commercial banks, the possibility of default due to SMEs’ own factors or environmental impacts will bring losses to commercial banks. 14 Its characteristics are summarized as follows:

Credit risk is non-normally distributed; credit risk has complexity; credit risk has information asymmetry; credit risk is disseminative; credit risk is difficult to monitor; credit risk is sudden.

Supply chain financial model based on Internet of Things

Overview of the Internet of Things

The Internet of Things is a network technology that uses intelligent sensing technology to connect items to the Internet for information exchange and communication to achieve intelligent identification, tracking, and supervision under a contractual agreement. 15

The hierarchical structure of the Internet of Things

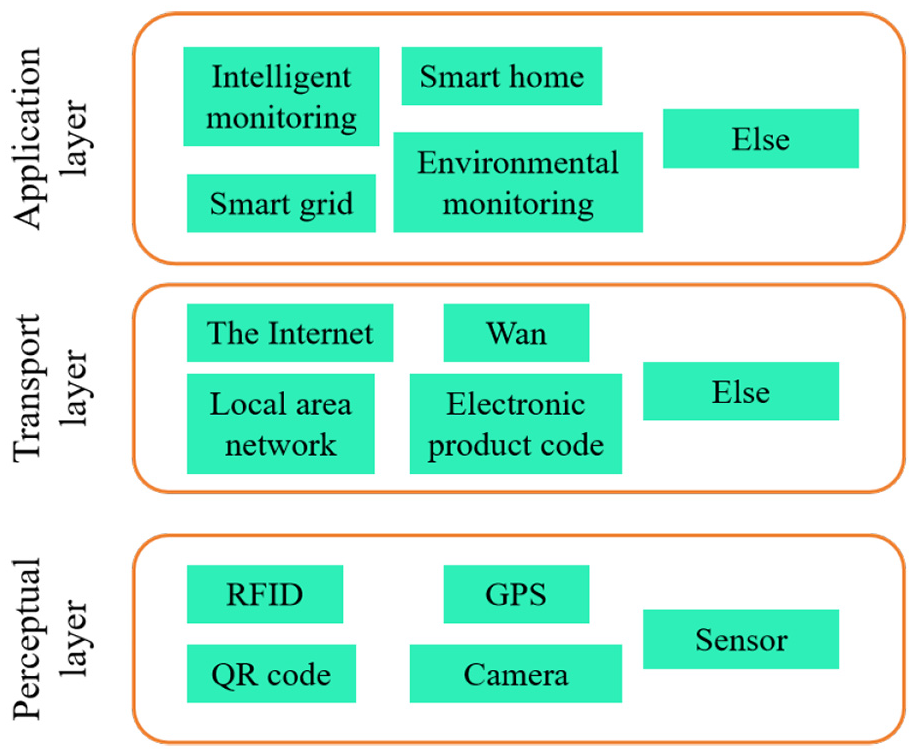

The Internet of Things is composed of three layers, as shown in Figure 1. The first layer is the perception layer, the second layer is the network transmission layer, and the third layer is the application layer. On the basis of the first two layers, the acquired data and related information can be intelligently processed and applied. The Internet of Things has a wide range of applications, as shown in the application layer in Figure 1. The Internet of Things is widely used in intelligent monitoring, smart grid, smart home, environmental monitoring, and other aspects.

The architecture diagram of Internet of Things.

The key technology of Internet of Things

1. Radio Frequency Identification (RFID):

This technology is a non-contact automatic identification system that automatically recognizes a target object through radio frequency wireless signals and realizes acquiring relevant data. The system mainly includes electronic tags, readers, and computer networks. The electronic tag is composed of a chip and an antenna, and mainly identifies the target object by attaching to the object. The electronic tag has a unique electronic code for storing relevant information of the target object. For example, an electronic tag is embedded in the pledge in the inventory pledge financial mode, and information related to the pledge is stored. The reader reads the information in the electronic tag through the radio frequency wireless signal. It first needs to send a specific inquiry signal. When the electronic tag reaches this signal range, it will sense the signal and give a response signal with the information stored in the electronic tag. After receiving the response information signal, the reader will transmit it to the host in the computer network after the corresponding processing, and the host completes the functions of data processing, transmission and communication.

2. Global Positioning System (GPS):

GPS is a combination of satellite and communication technology applications. GPS can quickly and accurately acquire the three-dimensional position, velocity, and time information of the target object without weather and time constraints, and has the characteristics of high precision, high efficiency, and automation. GPS is an indispensable part of the Internet of Things system. In the inventory pledge financing model, effective control of the pledge liquidity is one of the urgent problems to be solved. RFID can effectively solve the real-time tracking of pledges in a small area, and once the pledge is transported over long distance, RFID alone cannot solve the problem. Combining RFID with GPS can solve the problem well. A transport vehicle equipped with a GPS receiver can be accurately located after satellite positioning.

3. Data analysis and processing technology:

In the architecture hierarchy of the Internet of Things, the types and quantities of information transmitted from the sensing layer to the application layer are gradually increased, and the amount of data that needs to be processed and analyzed is multiplied. 16 Data analysis and processing functions are a key to the effective application of the Internet of Things, and the emergence of cloud computing has realized this possibility.

Supply chain finance model based on Internet of Things

The original intention of this article is to optimize the existing financial mode of supply chain finance by using the Internet of Things technology. Combining the working principle of Internet of Things and the characteristics of inventory pledge financing business, the system architecture based on inventory pledge financing business is designed, including four levels: perception layer, network transmission layer, data processing layer, and application layer, 17 as shown in Figure 2.

IoT system architecture diagram based on inventory pledge financing model.

The perception layer is mainly responsible for collecting various types of information in the inventory pledge financing business. The first is the review of the information of the participating entities in the supply chain finance, such as the background of the supply chain, the credit strength of the core enterprise, the debt situation of the financing SMEs, the operational status, and the ownership of the pledge. These are entered by third-party logistics companies based on business application forms and market research. Then, the collection information of the pledge is collected, and the information (quantity, real-time picture, and in-transit information) of the pledge is identified by the video probe, the electronic tag, and the sensor node. Finally, it is necessary to collect external environmental information such as the market competition of the pledge. The information collected by the sensing layer will be transmitted to the database of the network transport layer through a network such as the Internet or a wide area network. The sensor layer and the network transport layer are connected by means of sensor intermediate technology, self-organizing network technology, and codec collaborative information processing. In the IoT system architecture based on inventory pledge financing, the data in the network transport layer mainly contains the main information related to the pledge during the business development process. For example, the information of the participating entities, the ownership of the pledge, the information of the pledge, and the market price of the pledge. The collection of such information enhances the ability to monitor pledges and prevent fraud, while providing a database for dealing with the risk of price volatility of pledges.

The data processing layer is the key part of the system architecture of the Internet of Things. The cloud computing platform in this layer carries out business evaluation analysis, value analysis of pledges, and inventory analysis of pledges through relevant information obtained from the database of the network transmission layer. The data processing layer mainly processes the acquired information through the application of the cloud computing platform, comprehensively evaluates the application for the inventory pledge financing of the financing SMEs, and determines the appropriate pledge rate according to the evaluation. According to the real-time market price of the pledge obtained from the network transmission layer and the pledge rate, the pledge market price is tracked, and the future trend is predicted. Based on this, the mark-to-market management of pledges is realized to avoid the risk of price volatility caused by similar competition in the market.

In the organization of the application layer, the third-party logistics enterprise connects to the system through a local interface to operate the system. The employees of the logistics enterprise carry out relevant operations according to the information obtained in the business process and the system, and evaluate the pledge of the financing SMEs through the application of the sensing layer and the data processing layer. According to the results of the business process, the logistics enterprise conducts intelligent monitoring, punctuality management, pledge outbound transportation, information transmission, and other instruction operations on the pledge. Banks, core enterprises, and financing SMEs connect to the system architecture through remote interfaces. Through the system, real-time sharing of information is realized, information transparency is improved, and fraudulent behaviors are effectively prevented, thereby reducing the risk of bank external loans.

Measurement of supply chain finance credit risk based on Internet of Things

The credit evaluation methods of the supply chain finance are mostly based on experts’ opinions and precious experiences, which are too subjective and short of scientific foundations. Based on the above analysis, this article proposes the credit risk assessment under the supply chain finance mode based on the Internet of Things on the basis of the credit risk assessment of the traditional financial mode and uses the SVM algorithm and Logistic regression method to establish the credit risk assessment model, which overcomes the subjective shortcomings of expert assessment and improves the objectivity of the assessment.18,19

Supply chain financial credit risk evaluation index system based on Internet of Things

Under the framework of the bank’s traditional credit policy, it mainly examines the scale and strength of enterprises, balance sheets, collateral, and guarantees. To the enterprise, credit risk evaluation is mainly done by examining the financial indicators. 20 However, due to the imperfect financial system of SMEs, the poor transparency of corporate management, and the inability to provide guarantees or other mortgage assets in accordance with bank regulations, bank evaluations have found that the probability of compliance is very low, it is difficult to obtain bank credit, and it is unable to solve the problem of shortage of funds.

This article draws on the basic framework of traditional business credit evaluation and follows the principles of comprehensiveness, science, pertinence, impartiality, legitimacy, and operability. According to the characteristics of the IoT-based supply chain finance business, it combines the credit level of the borrower, focuses on the characteristics of self-liquidation of the single financing business and the ability of the lender to organize the transaction, and conducts credit evaluation on the business. The evaluation index system mainly examines the following four aspects:

Applicant qualifications, including corporate quality, operational capability, profitability, solvency, and development potential. Focus on selecting the main indicators in the traditional business rating.

Counterparty qualifications, including counterparty credit rating, counterparty industry characteristics, operating ability, and solvency.

The assets under the financing, including the characteristics of the assets and the characteristics of the accounts receivable.

Supply chain operations, including industry status, close cooperation, and past transaction performance. The supply chain operation status is the overall evaluation of the bank’s transaction quality of trusted companies. The whole evaluation system is divided into four categories, a total of 27 indicators are shown in Table 1. The evaluation index system of supply chain financial credit based on the Internet of Things is shown in Figure 3. The dotted line in the figure is an indicator specific to the supply chain financial model based on the Internet of Things.

Twenty-seven 3-level indicators.

OL, operating leverage.

Supply chain financial credit evaluation index system based on Internet of Things.

Credit risk assessment model of supply chain financial model based on Internet of Things

The algorithms used in this article are Logistic regression algorithm and SVM algorithm. The Logistic regression model is a probability-based model. The output of the model is the probability estimate that the model belongs to a positive or negative class for a certain data point that needs to be predicted. This feature is suitable for the probability of compliance of the enterprise in this article. SVM is a non-linear mapping method that converts low-dimensional non-linear separability into high-dimensional space to make it linearly separable. SVM is not a probabilistic model, but it can use the model to estimate the positive class negative class. Logistic regression algorithm and SVM algorithm have many advantages, such as, Logistic regression calculation is not costly, easy to understand and implement; SVM generalization error rate is low, computational cost is not large, and the result is easy to explain. However, there are also shortcomings. For example, Logistic regression is easy to under-fitting, and classification accuracy may not be high; SVM is sensitive to parameter adjustment and kernel function selection. The original classifier is only applicable to the processing of the second type of problems without modification. When applied to a data set with multiple indicators and large data samples, the classification result will be inaccurate. In this article, the method is to combine the two, use the advantages of the two models, discard their disadvantages, and then use the new integrated discriminant analysis to evaluate the credit risk of supply chain finance model. Factors affecting the quality of the model include the authenticity and regularity of the data, the appropriateness of the training parameters, and so on. In addition, since the SVM is not suitable for data sets with large data samples, in order to improve the accuracy of the prediction, the size of the data set should be appropriately selected. The parameter adjustment of the model should also be careful.

Evaluation model based on Logistic regression

Logistic regression is an important supervised classification model,

21

which is widely used. Its output is the probability value between

The general classification rule of Logistic regression algorithm is that the output value of sigmoid function is the threshold value, with 0.5 as the threshold value, and its corresponding decision function representation is

After obtaining the expression of the logistic regression model, the next step is to solve the coefficients of the model. In mathematics, a method of maximum likelihood estimation is usually used. This method first obtains a list of parameters, so that the probability value of the model for a given data is maximized under this column of parameters. In the logistic regression model, the log-likelihood function values are expressed as follows

Using the sigmoid function

where

Evaluation model based on SVM algorithm

In the traditional Logistic regression algorithm, the model uses 0.5 as the fixed demarcation point as the threshold of classification. Although the classification result is easy to understand, it may cause misjudgment to the sample. Therefore, in order to improve the accuracy of discriminating whether the customer is trustworthy, the model needs to be optimized. The optimization method used in this article is to introduce the SVM algorithm based on the logistic regression model. 23 The algorithm studied in this article belongs to the category of classification algorithm, so this article only introduces the SVM classifier. Maximizing classification interval is the basic idea of SVM, which is based on the basic principle of minimizing structural risk and statistical theory. This model is to find the balance between the learning effect and the complexity of the model among sample information, so that the model can obtain better learning ability.

Non-linear support vector machine: The data sample set in this article is either linearly separable or non-linear SVM. Processing with high-dimensional feature space can make the sample linearly separable and then solve the optimal hyperplane. Kernel function will be used in the solution process.

Define the mapping

The corresponding classification function is as follows

Research on integration of Logistic regression and SVM algorithm

The traditional Logistic regression algorithm uses a fixed demarcation point as the classification threshold, which is easy to misjudge the sample. The SVM model inherits the method of statistical learning. It has a good theoretical foundation and good generalization ability, but there are still some shortcomings when used alone. For example, when applied to a data set with multiple indicators and large data samples, the classification results will be inaccurate. Therefore, many researchers have combined SVM with other machine learning algorithms to improve the algorithm to improve the accuracy of model classification. In this article, by consulting related materials, the optimization method is used to introduce the SVM algorithm into the traditional logistic regression model and use the output of SVM to provide belief support for the output of the logistic regression model.

Integrated thinking

Logistic regression model of this article is based on the sigmoid function model, the result is a value between

Integrated discriminant analysis

The discriminant analysis criterion of the integrated algorithm is that based on the logistic regression model, the output values of each training data set are divided into five sub-intervals from small to large, namely

Steps to integrate Logistic regression and SVM algorithms:

Run the processed training sample set into the algorithm and collect the output result of the logistic regression model and corresponding output value to the five consecutive intervals of the division.

In the five interval segments, divide the training data set into five parts, run the algorithm, calculate the correct rate of the logistic regression model as

On the test data set, the test data set is also divided into five parts, and the logistic regression model is used to calculate with the SVM model. Assume that in the test data set, the output result values are

According to the classification accuracy rate

It can be simply understood that the logistic regression algorithm is used for calculation, and then divided into five intervals, and then the two algorithms are used to classify and calculate on the corresponding interval data, thereby realizing the function of integrated discrimination.

The rule established in this article breaks the fixed criterion of the logistic regression model with 0.5 as the demarcation point. The classification correctness rate on the five consecutive sub-intervals divided by the output probability is compared with the classification accuracy of the SVM. It uses the output of SVM to provide support beliefs for the output of Logistic regression model, and reduces the risk of misjudgment during the operation of the algorithm, thus improving the classification accuracy of the data sample set.

Model evaluation

After the model is derived, the model is evaluated. The quality of the model is usually judged by the accuracy of the predicted result. The receiver operating characteristic curve (ROC) curve is a commonly used parameter of the test model, and its corresponding value is the AUC (Area Under ROC Curve). The ROC curve is obtained, and the larger the AUC value, the better the classifier effect (Figure 4).

Overall flow chart.

The false positive rate (FPR) and the true positive rate (TPR) are calculated according to the output of the algorithm. Based on these two quantities, the abscissa and ordinate of the ROC curve can be determined, which are FPR and TPR, respectively. The definitions of the two are: TPR = TP / (TP + FN), which represents the proportion of the actual examples in the positive examples of the model prediction results. FPR = FP / (FP + TN), which represents the ratio of the actual false positives in the positive examples of the model prediction results to all counterexamples.

Model verification

As the banks have insufficient data reserves for SME customers in the supply chain finance business, they have not established a complete data storage and management system. Therefore, in view of the current status of supply chain financial business and the lack of data, the supply chain financial business is mainly applicable to the background of SMEs. The sample data selected in this article is the financial data of 102 listed companies before the 31 December 2006 issue of the SMEs in Guotai An Number Library. (There are 67 good customers and 35 bad customers.) Because the evaluation indicators are all financial indicators, the relative evaluation criteria are blurred. According to the psychological factors proposed by Lu Yuejin, the evaluation level and the quantitative rating theory are determined. 24 For the four-level evaluation of the data with low precision requirements, the sample data are divided into four grades of 10, 7, 4 and 0 according to each index, and the score results are standardized, and the data are analyzed.

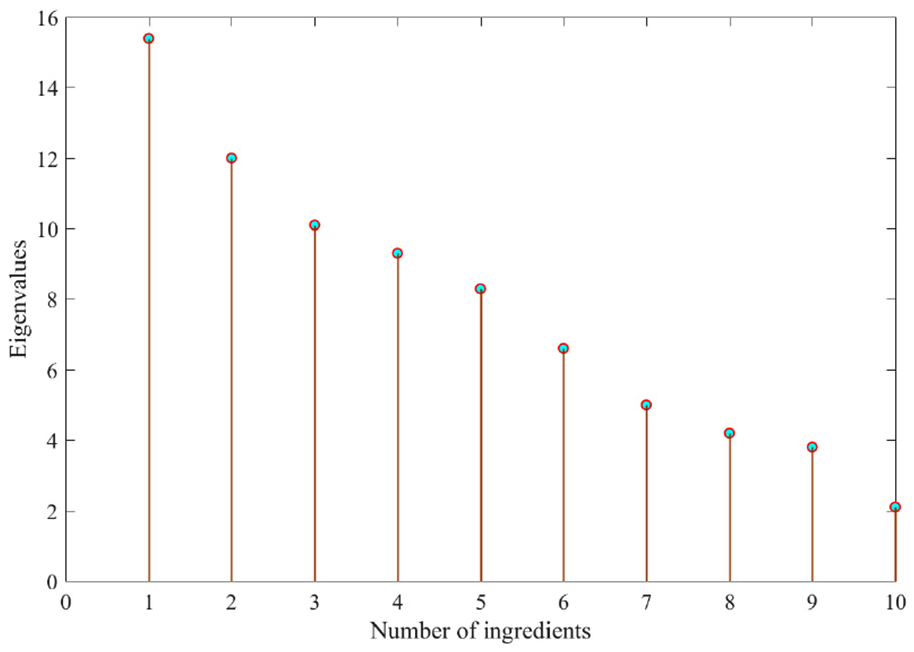

In order to reduce the workload of data analysis, the principal components analysis of the data is first performed. The cumulative contribution rate of the eigenvalues of the first 10 principal components has reached 74.687%, and the gravel map is shown in Figure 5.

Perform regression model analysis. The regression method is a stepwise selection and introduction method, that is, the probability of the likelihood ratio obtained by the maximum likelihood estimation is taken as the criterion for introducing the variable, and the iterative method is used to calculate step by step until the log-likelihood ratio no longer changes.

Principal components analysis.

Factor score coefficient matrix.

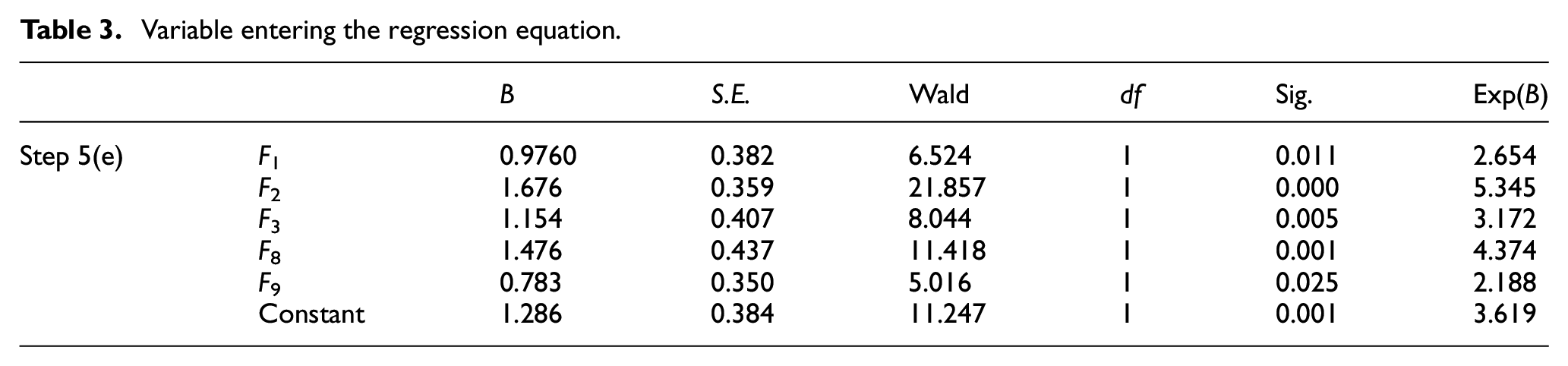

As can be seen from Table 3, F1, F2, F3, F8, and F9 are retained in the model, indicating that F1, F2, F3, F8, and F9 have a significant influence on the predictor’s compliance rate. The parameter estimation and its statistical test are shown in Table 3. The effect of each coefficient statistic test is significant.

Variable entering the regression equation.

The estimated logistic regression model is as follows

The

Train and test Logistic regression and SVM algorithm models

In all, 102 sets of sample data were randomly divided into training data samples and test data samples. Take 80 sets of training data samples and 22 sets of test data samples as an example.

After model training, get the parameter of Logistic regression model, input reorganize into the model, and verify with test set data. The result of model judgment, 0 indicates normal, that is, trustworthy; 1 indiccates not keeping your word. In order to conveniently find the AUC value evaluation model, according to the obtained running results, the ROC curve of the Logistic model is plotted by two variables, TPR and FPR, as shown in Figure 6. The AUC is calculated by the ROC curve to be 0.8371.

ROC curve of Logistic model.

In the same training SVM algorithm model, the parameter

ROC curve of SVM model.

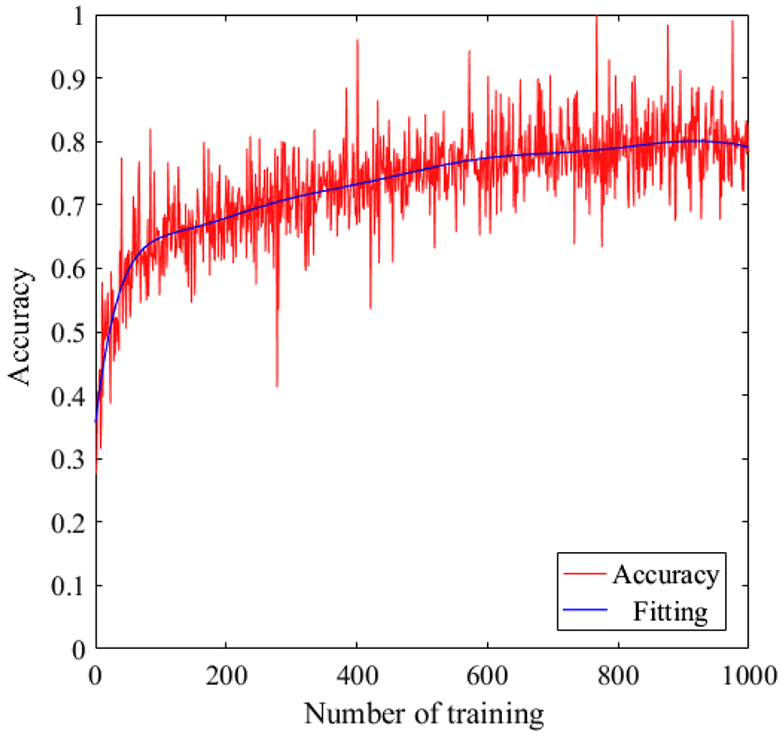

Model accuracy varies with training times.

Comparison before and after algorithm fusion

According to the integrated analysis method constructed in this article, the ROC curve of the integrated analysis method model is shown in Figure 9. The AUC is calculated by the ROC curve to be 0.8919. This article conducts several experiments and trains at different data levels of 50%, 60%, 70%, and so on to verify that the integrated analysis method has better classification effect than the simple logistic regression model and SVM model, and improves the accuracy of model classification. The AUC value is calculated by the model ROC curve. The larger the AUC value is, the better the model effect is. Figure 10 shows the AUC value obtained from the ROC curve before and after the algorithm fusion under different training data quantities. It can be seen that as the amount of data increases, the accuracy of classification before and after algorithm fusion is increasing. Under different data volumes, the model accuracy rate changes with the number of trainings as shown in Figure 11.

ROC curve of integrated analytical method.

Comparison before and after algorithm fusion.

11 model accuracy rate varies with data volume.

According to the integrated model, under the condition that the probability limit is 0.5, the total accuracy of the model is 85.4%, with the average accuracy of 93.2% for customers with good credit and 77.6% for customers with poor credit.

Since the integrated analysis method model is based on the logistic regression model, the output values of each training data set are divided into five sub-intervals from small to large. Then, in two sub-intervals, the two methods are used to train separately, and the correct rate of each training is obtained. The logistic regression classification accuracy rate is compared with the SVM classification correctness rate, so as to select the result of the model classification obtained by inputting the test data set. This model breaks the fixed criterion of the previous logistic regression model with a demarcation point of 0.5. Compared with a single classification method like SVM, it reduces the risk of misjudgment during the operation of the algorithm, thus improving the classification accuracy of the data sample set.

Empirical research

A petrochemical company A is local refiner in A province. Its upstream supplier is China petrochemical corporation B branch. Sinopec B Branch provides A petrochemical company with stable crude oil supply every month according to the crude oil index, and A petrochemical company carries out refining and production. A petrochemical company and upstream supplier Sinopec B branch adopt the prepayment method. As A petrochemical company has the capital demand for prepaid payment, it applies to the bank for supply chain financial financing based on prepayments, which is used to prepay the upstream Sinopec B branch. 25

Company A is initially rated by its corporate status, financial status, and trading status.

1. Calculate the probability of compliance of enterprises based on the supply chain financial model of the Internet of Things.

According to the situation of company A, it is scored as shown in Table 4. First, standardize

Company A rating (supply chain financial model).

OL, operating leverage.

The probability p value is 87.079%, indicating that A petrochemical company’s compliance probability is 87.079%, and the credit risk is small. The integrated analysis method model is used to determine the probability of 0, and the result is trustworthy. The ROC curve and the AUC value are shown in Figure 12, and the AUC value is 0.995.

2. Calculate the probability of compliance of enterprises in traditional mode

ROC curve and AUC value.

The traditional model only considers the company’s own situation (such as enterprise quality, operational capability, profitability, solvency, development potential, etc.) as the top 16 indicators.

Taking 102 data as samples, the probabilistic probability is calculated by principal components analysis and logistic method.

The results of the principal components analysis method are as follows:

Thirteen gravel map.

Using the logistic regression method, the expression of the promise probability is

First, normalize

The probability P value is 38.919%, indicating that A petrochemical company’s compliance probability is 38.919%, and its credit status is poor, making it difficult for the bank to grant credit.

Summary

As the credit level of A company is not high, that probability of compliance of A company would be only 38.919% in traditional ways. However, the supply chain financial credit evaluation system based on the Internet of Things has more comprehensively evaluated SMEs. From focusing on the assessment of the credit risk of SMEs themselves to the assessment of the entire supply chain, from the assessment of static financial data of SMEs to the dynamic evaluation of the entire transaction process, it pays more attention to the self-compensation of its single transaction. Due to the stable business contacts between A and its core enterprise (namely upstream supplier Sinopec B branch), under the supply chain finance mode, the integrated analysis method model is used to determine that the result is 0 and the probability of non-compliance is 87.079%, and the bank can grant credit to it. Therefore, the supply chain financial mode based on the Internet of Things not only correctly evaluates the real risks of business but also enables more SMEs to enter the service scope of banks. Banks can effectively solve the financing difficulties of SMEs by effectively controlling the assets under financing and avoiding most risks.

Conclusion

This article analyzes the characteristics of the Internet of Things and combines it with the supply chain finance mode. A credit risk assessment index system of the supply chain finance based on the Internet of Things has been proposed, and a credit risk assessment model has been established using SVM and Logistic regression methods. The credit risk assessment index system and model could provide a more scientific way to measure the credit risk of supply chain finance than expert assessment. The customers are classified into trustworthy and untrustworthy by using Logistic regression and SVM models. And a conclusion could be drawn that credit risk assessment model provides a high degree of accuracy for the SMEs under the supply chain financial model based on the Internet of Things, which provides a strong guarantee for the rapid development of supply chain financial security. By further comparing the model based on the Internet of Things with the traditional bank credit model, it is revealed that the supply chain finance based on the Internet of Things has alleviated the financial dilemma of SMEs. This article provides a more scientific way to evaluate the financial credit and finds a more accurate way to measure the current financial risk of supply chain.

Footnotes

Handling Editor: Jinsong Wu

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work is supported by the National Natural Science Foundation of China (no. 71631008 and no. 71371194).