Abstract

Through stories, interviews, pictures, and financial records, the author narrates the inner workings of a rent-to-own company where he worked. Spending over two years on the job, he developed extensive field notes, performed qualitative interviews with management, analyzed a year’s worth of financial data, shedding new details on the intimate process of “rent-to-own,” which make the poor poorer.

In the summer of 2018, my boss sent me to collect a late payment for a rented bedroom set from “Jane.” When I arrived at the modest mobile home, I knocked on the door, but no one answered. When I got back in my truck, I saw someone looking at me through the front window. They quickly closed the drapes when they saw me looking back. I called my boss and let him know there was no answer, but admitted I did see someone looking at me through the window. He advised me to leave a door hanger, saying I had been there and to come back later.

Jane is one of 4.8 million customers in North America who is served every year by rent-to-own (RTO) businesses like the one I worked for, according to the Association of Progressive Rental Organizations (APRO), an RTO industry trade group.

My boss’s casual attitude toward this customer who was delinquent on their furniture payment was not surprising. For every trip I made to Jane’s home, $10 was added to her bill, along with a $1 a day fee for each day that the payment was late. Jane is one of 4.8 million customers in North America who is served every year by rent-to-own (RTO) businesses like the one I worked for, according to the Association of Progressive Rental Organizations (APRO), an RTO industry trade group. The trip to collect a late payment from Jane was one of the 582 “service calls” (a common RTO industry term) I made to customers over the nearly three years I worked for an Idaho-based RTO company. My primary job, however, was presumably to deliver and set up furniture, appliances, and electronics. Strikingly, an investigation of 7,517 RTO transactions by Michael H. Anderson, a Finance Professor at the University of Massachusetts-Dartmouth, found that nearly 40 percent, or about two out of every five, payments are made late.

I was offered the job at $12 an hour by a temporary staffing agency (for which this store heavily relies on for employees) because of my experience driving large trucks. I took the job because, as a single father of two children, if I worked full-time for 52 weeks a year, not missing one day for being sick or injured or going to any school or family events, this job would allow me to earn $24,960 annually before taxes. This amount is $3,630 above the federal poverty line for a family of three. To further complicate my situation, I was attending a local public university attempting to be the first person in my family to graduate from college. My educational goals forced me to limit my work to less than forty hours a week and, unfortunately, put my family below the poverty line. Nonetheless, it was the best-paying job offered to me by the temp agency in five years, and it allowed me to get an insider view of how the RTO industry operates.

At the urging of a sociology professor at the university, during the 35 months I worked for this RTO business, I took extensive daily field notes, performed lengthy interviews with management, and obtained comprehensive financial records. The data I gathered gave me unique sociological insights into how the RTO industry operates, often by targeting the most vulnerable, piling on fees, and creating a rent-confiscation cycle.

Targeting the Poor

Every May the 4th, the store where I worked offered a “May the 4th be with you” promotion. During the sales event, they offered almost anything in the store for only four dollars down, with free delivery and setup. Not surprisingly, this was an effective promotion that attracted many customers and garnered an increase in sales for the store. The high volume of deliveries during one of these sales promotions was viewed unenthusiastically by delivery drivers like me who had the strenuous physical work of delivering and installing washers, dryers, refrigerators, TVs, gaming systems, stereo systems and various kinds of household furniture.

The way RTO works is that customers who cannot afford a consumer good at retail price, such as a bed, couch, appliance, or a television, pay a small down payment and then pay weekly, biweekly, or monthly payments on the good until it is paid for with interest. How much interest is paid on such a good is subject to debate. According to research done by Michael H.

Anderson and his colleague, Sanjiv Jaggia, the average RTO sells goods for about 200 to 400 percent above the retail price. Where I worked, and in the other RTO stores I investigated, the interest rate was often much higher and depended greatly on the goods purchased.

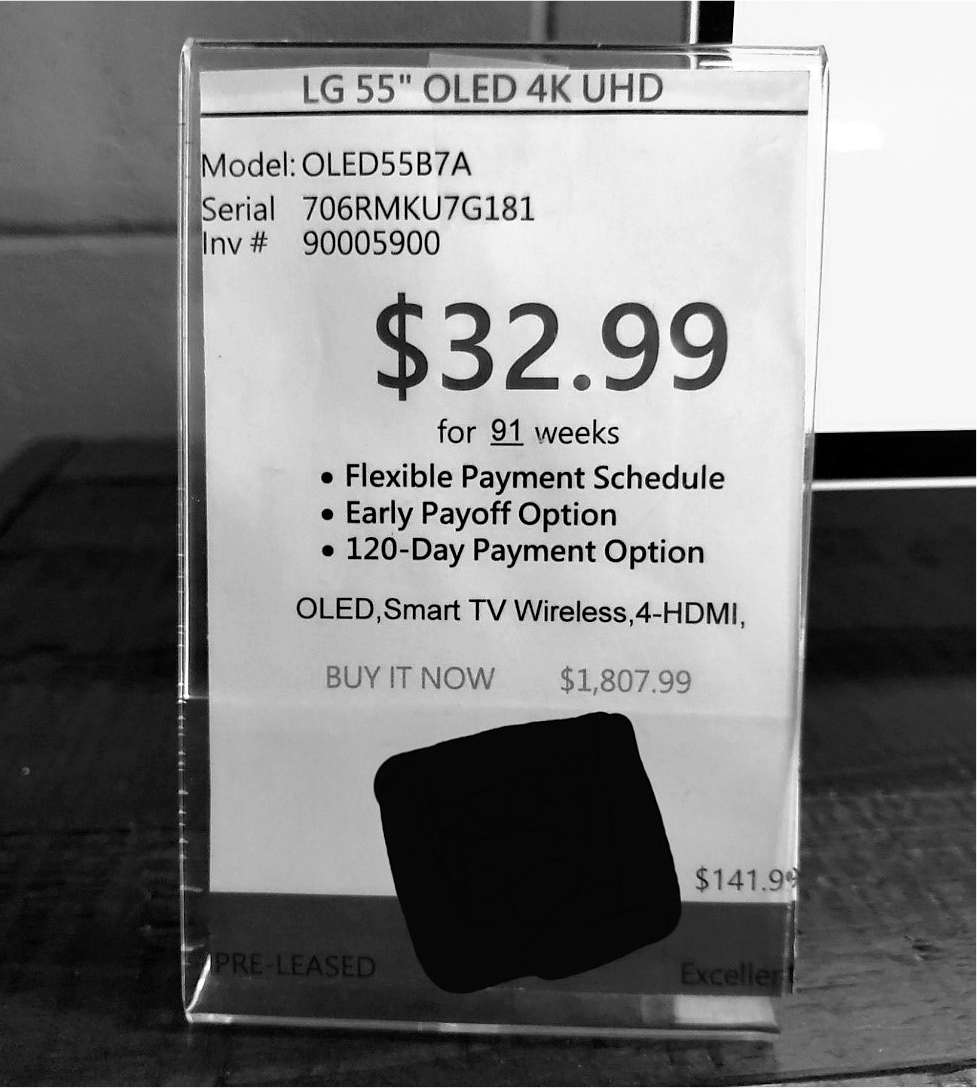

For example, the LG 55-inch 4K is a popular mid-level television. The store where I worked offered the television (used) for $32.99 a week for 91 weeks, plus a 6 percent sales tax. A customer who fulfilled this contract by making only the minimum weekly payments would pay $3,182.22 for the television. However, an internet search at the time of this writing found the same television listed for $329.99 at the online site of a big-box retailer. Thus, the cost of the TV where I worked was more than 900 percent above retail. The store also offers a “buy it now” option at $1,807.99, a price that no one pays for obvious reasons. From a purely financial perspective, it would be irrational for anyone to buy a television from this store. However, if you don’t have the money or credit to buy the TV, but do have the first weekly rental payment (or come in during a sales promotion), this television could be in your home and installed the same day for a small (and negotiable) upfront cost.

Overwhelmingly, the people taking advantage of these and similar sales events are low-income (often working mothers with children), according to statistics released by the Association of Progressive Rental Organizations. And states with a large population of working poor people provide an ideal setting for RTO businesses. According to a collaborative study done by United Way called the ALICE project, working families in Idaho who are asset limited and income constrained have increased since the end of The Great Recession. Roughly one out of every three households in Idaho are either in poverty or struggle daily to pay their bills. The most financially desperate people in this expanded population are the people this business is targeting. The process of targeting the working poor begins when this business regularly advertises “no upfront cost,” “low weekly rates,” and “no credit needed” on a giant billboard outside. The sign glowingly announces that if you are low on cash and have bad credit, this is the store for you.

The management at the store where I worked actively filtered out customers with the purchasing power to get these items at retail. If a potential customer questioned the inflated price, the sales staff would agree with their complaints and tell them to go somewhere else. My manager, “Dan,” who has been the sales manager for this store for over sixteen years, candidly explained to me in an interview:

Sometimes they’ll say “I can go to Wal-Mart and get that for less.” Then I tell them, “If you’re going retail you should!”

“Absolutely, we’re an alternative to that,” I tell people. If you got the money to buy it, I very much encourage you to. That way I don’t get into an argument and I’m really telling them, “Well yeah, we’re here if you can’t do it.”

Often, this is enough to make a potential customer with the ability to buy retail promptly leave the store. The process of filtering out and targeting only those who have very little money and bad credit is the bedrock for how this business operates.

This RTO store places a display in front of its products, prominently highlighting the weekly price while making the number of weeks needed to own the product less visible.

Jeff Cates

The Confiscation Cycle of RTO

This kind of interest-infused price inflation is not unique to televisions. Although the markup on electronics like televisions and gaming systems was the highest, sofas, bed sets, dining room sets, and major appliances were also sold at about eight times the original price, a price that many poor people are ultimately unable to pay. Often the price charged to the poorest customers who end up unable to pay off their contract also included additional charges such as “service calls” for collection on past due payments and late fees. Eventually, the goods were repossessed.

A study in 2000 by the Federal Trade Commission claims about 70 percent of RTO customers paid off their goods. More recent, but still outdated, proprietary data from four stores studied by California Polytechnic University and University of Massachusetts professors revealed conversely that 73 percent of weekly payment contracts and 52 percent of monthly payment contracts resulted in return or repossession of goods. These latter numbers fall in line with the best guess by “Nick,” an eleven-year store employee who estimated that only 30-40 percent of customers fulfilled their contract. I asked him why so many customers defaulted on their agreement. He opined:

Catchy slogans are often promoted next to a major road to draw in potential customers.

Jeff Cates

The reality of it comes up. You know, the reality of, wow, $700 sofa and I’m going to end up paying $3,000 for it. Or, they overextend themselves, and we don’t, we never look at a customer and say, “ Hey, you’ve already got too much. You’ve listed an income of $2,000, and you’re putting out $800 in monthly rent. What about your other bills?” Reality catches up with people.

These inflated prices would be overwhelming for anyone, let alone for the working poor. All customers are encouraged to “overextend themselves” if they have a job or consistent income. This sales tactic at RTO is unlike other lending institutions who have more of an incentive to not overextend someone or to openly admit it. For instance, banks don’t have a neatly worked out system of dealing with repossessed homes or cars like rent-to-own stores do for furniture items, appliances, and electronics. Deliberately overextending customers with high-interest debt is standard practice, rather than an outlier. As Nick clearly states, “We never tell a customer they have too much.”

Predatory Inclusion

It is easy to assume that the RTO industry preys on poorly educated or less intelligent people who cannot understand the inflated prices, but the situation is more complicated. The RTO industry makes money through what sociologists Louise Seam-ster and Raphael Charron-Chenier call “predatory inclusion.” Primarily associated with loans for education and homes, predatory inclusion is when marginalized people are allowed access to goods, services, and opportunities generally associated with the middle-class. However, the benefits of that access are significantly undermined by the unequal conditions of repayment.

Not only are the poor promised “middle-class goods” at low upfront costs, but the free options embedded in the RTO contract also make doing business with RTOs even more alluring, especially for those who live on tight budgets. RTO offers free and often same-day delivery, setup, installation, and repair of products. For instance, if something goes wrong with the merchandise before the contract is up, it will be repaired or replaced for free. This free service includes additional delivery, setup, and pickup of a replacement item (if needed) at no extra charge. These options make getting the merchandise quick, easy, and seemingly worry-free, at least until the day comes when they can no longer afford the overpriced item, and it is removed as swiftly as it was delivered and installed.

We live in an aspirational society where we are told that a set of consumer goods and access to the institutions required to get them are the well-earned spoils of hardworking people. This image often does not align with a reality where real wages have not increased for many Americans in decades, a great deal of whom work full-time jobs for 40 or more hours a week. Consequently, for numerous Americans, high-end consumer goods such as furniture, appliances, and big-screen televisions are purchased on credit. In April 2019, the Federal Reserve noted that Americans’ revolving debt (mostly credit card balances) reached more than $1 trillion.

For those who do not have credit and are frustrated by so many goods being just out of reach, RTOs and other sub-prime lenders who offer “easy” access to the items that everyone is assumed to need can seem like salvation. RTO customers are told that if they have a job, their credit does not matter. In the store where I worked—and standard across the industry— almost anyone employed is given credit even if the financial information provided reveals they cannot afford what they are getting. As Nick admits, “You could come in, and if you listed an average income of $1,000, and if you want to rent $1,000 from us, we’ll let you.” This business tactic allows the poor to gain (often temporary) access to luxury electronic devices and high-end first-world necessities by making it easy for nearly anyone to get “credit.”

Moreover, customers are reassured that if they ultimately cannot pay, there are no negative consequences (except their inability to continue to use the item). This assurance is only partially true. Until 2019, a loophole in a Texas law allowed RTO businesses to have customers who fell behind on their payments charged in criminal court, even if they returned the merchandise. In some cases, I delivered legal notices to customers for debts owed, even after repossession had occurred. In Idaho, as in many states, debt from previous unpaid weeks with the merchandise can be collected through the civil courts and could result in customers having their wages garnished or jail time if they could not pay.

The case of rent-to-own shows that predatory inclusion extends beyond the loans that promise inclusion through upward mobility. With its small ticket items and easy credit, rent-to-own shows that even the most modest of daily life exclusions provide opportunities for predatory inclusion. Moreover, since these items are easily repossessed, it enables predation to reach new heights as the lender aggressively overextends.

RTO as Lender of Last Resort

According to economic researchers Sanjiv Jaggia, Herve Jacques Marc Roche, and Michael H. Anderson, there are over 9,000 RTO stores in the United States that generate over $8.5 billion in annual revenue. Their recent study in the Journal of Public Affairs argues that the kind of subprime lending that RTOs offer should not be looked at the same as other usurious models like payday loans, check cashing firms, and pawn shops. Their analysis asserts that even though there is a high rate of returned merchandise nationally, RTOs “may be the only feasible way of acquisition” for common household goods that financially distressed people need and want to consume.

The way RTO works is that customers who cannot afford a consumer good at retail price, such as a bed, couch, appliance, or a television, pay a small down payment and then pay weekly, biweekly, or monthly payments on the good until it is paid for with interest

This store often paints clever slogans and enticing deals on the storefront windows to attract potential customers.

Jeff Cates

However, the positioning of RTOs as lenders of last resort that provide needed (or at least wanted) goods to the working poor ignores alternative means of acquiring such goods that are less well advertised. Second-hand stores and layaway programs provide similar consumer products at retail cost or much less. According to the US Economic Census, there are over 25,000 second-hand stores, consignment businesses, and Not-For-Profit resale stores in the United States that generate over $17 billion annually selling furniture, appliances, and electronics at a fraction of the RTO cost. For instance, within just a few miles of the RTO store where I worked, there are at least three used goods stores that have similar household items, including furniture, televisions, and appliances, at much more affordable prices with delivery options for those who need it. One of these stores even sells used cars.

Of course, some would argue that buying cast-off goods at second-hand stores is quite different from buying new products. True, but while the market for used and new goods should be clearly delineated, RTO blurs the line between new and used.In the store where I worked, much of the goods acquired under RTO agreements were used goods that had been repossessed and cleaned. Because the store had other retail outlets across the region, they perpetuated the appearance of providing new goods by allowing customers to look at a vibrant 50-inch touch screen to see digital images of (new) select items in a range of colors or styles. When a customer selected a blue sofa that wasn’t in stock at the local store, we picked one up and delivered it from another store. Sometimes customers were surprised when the delivered item wasn’t new like the image on the screen, but most ultimately took possession anyway since it was already at their door. Certainly, RTOs offer some consumer advantage by offering free delivery and repair, but such services do not offset the difference in price by buying directly from the used furniture market.

In the market for new consumer goods, layaway is less common than in the past, but it is not unheard of. Struggling retailers like Kmart and Sears continue to offer free or low-cost layaway. Additionally, many big-box stores offer layaway programs that are less usurious, including Big Lots, TJ Maxx, and Best Buy. Walmart, the largest retailer in the United States, offers layaway only at Christmas time. Still, even with its shorter timeframe Walmart allows people to purchase many of the same goods acquired at RTO businesses for the same weekly payment at zero interest.

However the RTO industry redirects attention from other means by which poor Americans can obtain retail goods. As Nick illuminates, “We tout it as a way to get the product. A way to make your life better when you don’t have credit, when you don’t have money. But do we stop? No. When the numbers say we rented $70,000 [monthly] and it’s going up, great! We don’t care how it goes up.” In other words, enabling access to these products via easy credit is not merely about helping poor people buy commodities they would typically not be able to afford. This business is also about targeting and extracting profit from those desperate enough to sign these high-interest contracts while fully aware that many of the deals will end in return or repossession.

Debt Delivered

Not every one of the 388 deliveries during my employment ended in repossession or with unhappy customers. However, many did. I took part in 157 repossessions over 233 days. While some, like Jane, didn’t answer the door, others, like “Jack,” answered the door before I could knock. A heavy-set man sitting in a wheelchair with no legs from the knee down, Jack wore a Vietnam veteran’s hat and an American flag tank top. From the moment the door opened, he immediately began to apologize for being late. He explained that he was waiting on his next social security check and that he’d make a payment in a few days. I said, “No problem, sir. I’ll let Dan know,” and went back to my truck.

I called Dan and attempted to explain the situation, but he quickly interrupted me and ordered me to get some money or repossess the bedroom set immediately. Reluctantly, I went back and told the customer what Dan had said. In agitation, he expressed that the only reason he got the bedroom set was that he had accidentally soiled his other one and had no family in town to help him clean it up.

His voice took an edge of frustration as he explained how he got an advertising flyer in the mail claiming he could have a luxury bedroom set delivered for free, with free installation, for $40 a week. Dan even threw in the first two weeks free, since Jack was a veteran. Disheartened, Jack explained that he stayed on top of his payments for four months, but he got impossibly behind after spending two weeks in the hospital. After missing two weekly payments, along with the additional late fees and “service” fees, costs snowballed out of control, and he couldn’t afford to have a bed anymore.

Not only are the poor promised “middle-class goods” at low upfront costs, but the free options embedded in the RTO contract also make doing business with RTOs even more alluring, especially for those who live on tight budgets.

It was at that moment I decided I was not going to repossess Jack’s bedroom set, regardless of Dan’s orders. I went back to my truck, called Dan, told him that I could not do the repossession, and announced that I was coming back to the store. Dan answered, “Okay, see you soon.” When I got back to the store, Dan said nothing about that situation and quickly sent me on another delivery. When I returned, I asked him what he was going to do about Jack. He told me that after we spoke, he sent a different driver to Jack’s house. They repossessed the bedroom set.