Abstract

Raphael Charron-Chenier and Louise Seamster on debt and social inequality.

In the 2003 documentary “Born Rich,” Ivanka Trump recalls a homeless man sitting outside Trump Tower: “I remember my father pointing to him and saying, ‘You know, that guy has $8 billion more than me,’ because he was in such extreme debt at that point. It makes me all the more proud of my parents, that they got through that.” On the one hand, this anecdote highlights the widely shared assumption that debt is bad, a personal failure that people have to “go through” and can be proud to overcome. On the other hand, it also hints that something in that understanding of debt is not quite right.

Like most people, sociologists of wealth inequality typically assume that having more debt means being worse off. Intuitively, this seems correct. Yet thinking of debt only as “negative” wealth can lead to serious conceptual problems. To avoid the absurdity of declaring a homeless man richer than Donald Trump, we must employ a more robust sociological approach to debt. If we don’t, we risk using misleading measures of inequality.

Having more wealth is obviously a good thing, but having more debt is not always bad. Conceptualizing debt as the negative image of assets—as something to be subtracted from assets to determine net worth—can distort our picture of inequality because debt is not always a burden. It can also provide significant advantages—if it is the right kind of debt, deployed by the right person.

The term “debt” describes two related but different concepts. Debt also refers to negative net worth—having more liabilities than assets. But debt can also refer to a specific legal instrument that ties debtors to lenders. For debtors, debt is an obligation to pay a certain amount of money to a specific lender under narrowly defined conditions, in exchange of which debtors receive money or goods. For lenders, debt is a property right to the income stream that flows from the debtor. In many cases, financial institutions can buy and sell these property rights (and the income stream bundled to them) on secondary financial markets.

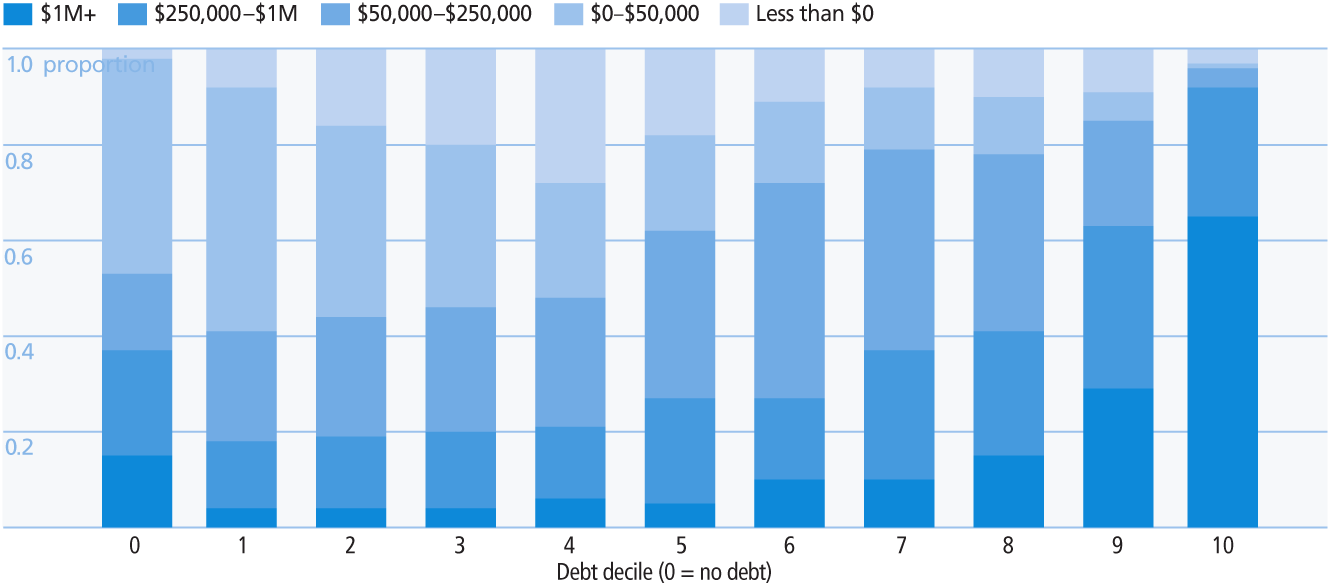

When thinking about debt, the standard assumption is that negative net worth and owing money to a financial institution are closely correlated. People who owe the most money probably have the lowest net worth, and people with the lowest net worth probably owe the most money. It turns out, however, that net worth and debt are positively correlated: the more debt a household has, the more likely they are to have substantial financial assets. The first figure shows how American households’ net worth varies as a function of their debt. Each bar represents a decile of debt, defined here as owing money to another party (10 = highest debt, 0 = no debt). Thus we see that American households who owed the most money in 2016 were also the most likely to have a total net worth of more than $1 million. Nearly 65% of the most indebted households in the U.S. are millionaires. This is almost five times more millionaires than can be found in households with no debt, and more than fifteen times more than in households in the bottom third of the debt distribution.

Distribution of net worth across debt levels

Source: 2016 Survey of Consumer Finances

Distribution of net worth by assets

Source: 2016 Survey of Consumer Finances

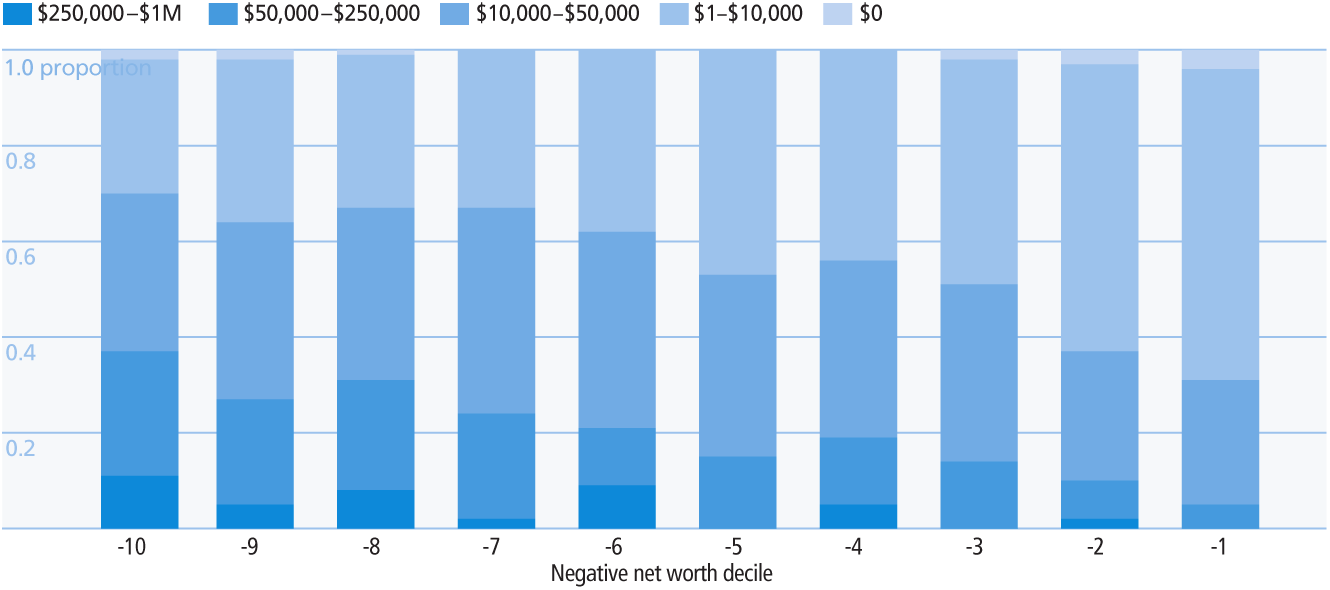

Likewise, what it means to have no wealth or even a negative net worth is not straightforward. Households with a negative net worth do tend to have fewer assets than households with a positive net worth. But most do have at least some assets, even if not a large amount. Among households with negative wealth, lower total net worth is in fact associated with higher asset levels. As the second figure shows, about a third of the households with the lowest net worth actually have more than $50,000 in assets.

These counterintuitive correlations between debts and assets affect our estimates of inequality. For example, one common way to describe global wealth inequality is to compare the wealth of a few top wealth holders to the poorest portion of the planet. Surprisingly, the poorest tenth of the world population includes a fair amount of American households. Put more bluntly, these measures are misleading. They make mortgaged suburban homeowners in the United States look poor, while property-less renters in much poorer countries look middle-class.

Debt is big business. It influences most American families, from the poorest to the richest. In the increasingly financialized United States, that influence will likely expand. The role of debt, however, varies across households. For better-off families, debt is often “good,” and financialization often lowers the cost of borrowing. Having debt does not mean living in an upside-down world of negative physical assets. It just means that families have deferred payments for the things they are currently enjoying: a home, a college education, or a new business. Debt allows households to pay for expensive things that will be worth even more in the future. It means improved credit scores and tax-deductible interest payments.

Poorer and marginalized households by contrast are more likely to hold “bad” debt. For the portion of the population living paycheck to paycheck, debt is often tied to small sums needed to make ends meet. The assets that come with this debt are not durable investments in a house, a business, or a college degree; they are consumed right away to put food on the table, keep the heat on, or pay for healthcare. Poorer households often borrow only a few hundred to a few thousand dollars at a time, but these small amounts can create larger catastrophes than the massive debt owed by better-off households. Traditional financial institutions, like banks, do not provide products for precarious borrowers as part of their core business, so poor households often rely instead on payday lenders, rent-to-own stores, car title lenders, pawnshops, and other fringe banking institutions that impose astronomical interest rates and other exploitive conditions. These services are an example of what we call “predatory inclusion”: they include in the debtor economy vulnerable households that have trouble getting desperately needed loans, but they leverage this desperation to extract as much profit as possible from these borrowers.

Sociologists should examine debt on its own rather than bundle debt into measures of total net worth. In this way, our research might better reflect the different experiences of debt and our changing relationship to it over the last few decades. Beyond simply determining who accumulates the most debt, we should assess how the consequences of debt vary across social position, how people manage debt, and the consequences of debt repayment or forgiveness.

Moreover, asking what has changed about the way lenders package, collect, and securitize debt, who decides the terms for issuing and collecting debt, and what information is employed in lending decisions can all go a good distance in explaining the changing landscape of debt and its consequences for social inequality. This includes putting the lie to the Trump family’s equation of negative net worth with homelessness outside their golden tower.