Abstract

Amanda M. Czerniawski charts two centuries of height and weight’s actuarial ideals.

The death knell of the Body Mass Index (BMI) is sounding as evidence of its ineffectiveness as a reliable measure of health builds. In an opinion article for the journal Obesity, two researchers from the University of Alberta in Canada argue that we cannot rely on anthropometric measures alone in diagnosing obesity; there is too much potential to misdiagnose patients who are “fat but fit” as having obesity or those who are “thin-but-metabolically-obese” as healthy. And many other studies confirm that BMI, our standard measure of body fat and general health, may be faulty.

A 2016 study in the International Journal of Obesity authored by researchers from the University of California–Los Angeles found BMI an unreliable indicator of general health. In their study, nearly half of the overweight and 15% of the obese subjects were deemed healthy while 30% in the “normal” BMI range were discovered to be metabolically unhealthy when additional measures of health (e.g., blood pressure, glucose, and cholesterol and triglyceride levels) were included in the evaluation. By their estimation, some 54 million Americans may be misclassified as “unhealthy” using BMI standards alone.

Another study presented at the American College of Cardiology’s Annual Scientific Session in April 2016 found that waist circumference better predicts future heart disease than simple weight or BMI calculations. Part of the reason is that BMI is based on the relationship between height and weight. BMI does not distinguish between the weight of muscle and that of fat. As a consequence, many Olympic athletes and professional football players fall into the “obese” range according to BMI.

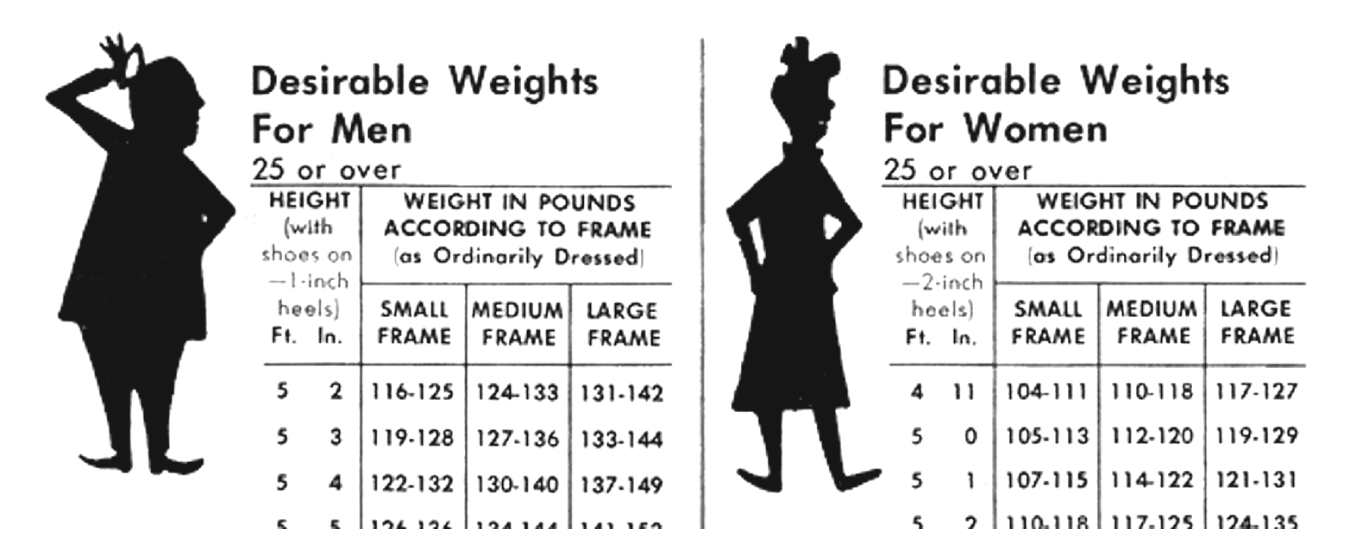

An illustration from a 1965 Kaiser Permanente member newsletter.

None of this should be too surprising. Scientists have debated the utility of BMI for years. A group of statisticians and epidemiologists from the National Cancer Institute and the Centers of Disease Control and Prevention, for example, reported in 2005 that individuals who are classified as overweight (but not obese) have a lower risk of death than those of normal weight, while the very thin have a slight increased risk of death. Studies such as these, investigating and calculating mortality risks based on body weight measures, are part of a larger trend in American society that was begun in earnest by life insurance companies in the early 20th century.

Life insurance companies used height and weight tables, first developed by Belgian mathematician Lambert Adolphe Jacques Quetelet in 1836, as an actuarial guide in evaluating policy applicants. During the late 19th century, American physicians believed that plumpness was a positive indicator of health and necessary to combat contagious diseases, such as tuberculosis, that were ravaging the population. Therefore, thinness was discouraged, especially in youth (who were considered particularly vulnerable). Life insurance companies used this conventional wisdom in considering prospective policyholders, and their medical examiners often denied policies to young, underweight individuals while assuming a more liberal approach toward accepting applicants of heavier builds, especially when they were under the age of 30.

Unfortunately, there was no industry standard that explicitly specified what constituted a medical risk and reliable data on the mortality rates of various risk groups were deficient or nonexistent. Even with regard to weight, the companies’ medical examiners were inconsistent in their selection criteria and each company relied on its own data to produce an individualized standard for evaluating life insurance applicants. The height and weight tables of the late 19th century reflected the limitations of scarce data and inconsistent medical opinions. A more uniform approach was not possible until 1889, when both the Actuarial Society of America (ASA) and the Association of Life Insurance Medical Directors of America (ALIMDA) were founded, helping medical directors and actuaries throughout the industry to share data and ideas.

This lead to a pivotal moment in 1895, when ALIMDA tasked George R. Shepherd, medical director of the Connecticut Mutual Life Insurance Company, with creating a standard, industry-wide height and weight table.

Shepherd analyzed data from over 70,000 policyholders in the United States and Canada over two years to devise a height and weight table that was soon adopted as a standard throughout the life insurance industry. It did not come without reservations: While Shepherd concluded that a variation of 20% above or below the average weights listed in the table should be considered an insurance risk, others disagreed. Brandreth Symonds, chief medical director of the Mutual Life Insurance Company of New York, argued, for instance, that the lowest incidence of death coincided not with those of average weights but with those who were 5% below the average (and, for those under the age of 30, 5–10% above the average).

As debate over risk continued and burgeoning business provided additional data for analysis, more tables emerged. The delineation between average and risky weights fluctuated accordingly.

But why was the life insurance industry responsible for these tables? First, as a business, it was highly incentivized to maximize its profits by perfecting the medical selection process of prospective policyholders. Second, the rocky start of institutionalized medicine in American allowed the insurance industry to become the authoritative voice in documenting the relation between weight and mortality.

The medical community at the time faced internal problems of consensus and external problems of legitimacy. As a professional field, physicians suffered from a lack of cohesion and public authority. For example, the American Medical Association (AMA), originally established in 1846 and reorganized in 1901, struggled to survive internal brawls. It was not unheard of for conflicts between physicians over possible treatments to become physically violent. Consequently, the medical field was ill-equipped to collect the necessarily large quantities of data that could substantiate medical claims and, thus, bolster its credibility. Life insurance companies fueled the investigation of the relation between weight and mortality.

Fewer than 200 years ago, weight was not regarded as an important health issue. In fact, at the turn of the 20th century, low body weight was medical practitioners’ leading concern of medical practitioners.

At the turn of the 20th century, sanitary conditions improved, halting the spread of infectious diseases. Infant mortality decreased while life expectancy increased. As individuals began to live longer, a new breed of diseases began to affect the population, including cancer and diseases of the heart. This shift from contagious to degenerative diseases prompted physicians to reconsider the benefits of a solid body weight, since extra weight in young individuals, in particular, seemed to be losing its advantage. Insurance companies, spurred by a number of industry-wide investigations into mortality risk assessment, revised their weight standards to accommodate the shift in mortal afflictions.

Over the next few decades, the life insurance industry (Metropolitan Life Insurance Company, in particular) combined both medical experience and actuarial data to continually update these tables and create separate ones for women. By the 1940s, these height and weight tables has been transformed from internal tools to facilitate the standardization of the medical selection process to guides recommending “ideal” body weights to the general public.

Life insurance companies were instrumental in categorizing bodies and raising public awareness of the dangers of obesity. They established welfare divisions to implement programs and publish pamphlets to promote longevity and arouse public support for disease prevention and treatment. Through these public health campaigns, the height and weight tables established a system of classification, differentiating those who fit the ideal from those deemed unfit, and became part of the medical literature for years to come.

Like the 20th century tables, BMI is a tool that is not immune to revision. In 1998, the federal government shifted the boundaries between normal and overweight, and an estimated 29 million Americans were redefined as overweight, overnight.

Today, as the medical community debates the evaluative power of BMI, we must recall the history of its predecessor—the height and weight table. Fewer than 200 years ago, weight was not regarded as an important health issue. In fact, at the turn of the 20th century, low body weight, not overweight, was the leading concern of medical practitioners. As conditions changed, modifications were made to the tables; our tools today are in need of recalibration. Instead of a one-size fits all measure, we need to diversify healthcare’s toolkit.