Abstract

The current student debt burden is an unsustainable outcome of the government’s abdication of responsibility to secure access to higher education. Andrew Ross analyses the factors behind the funding crisis and suggests some ways to reestablish an affordable education system.

Corey Fields

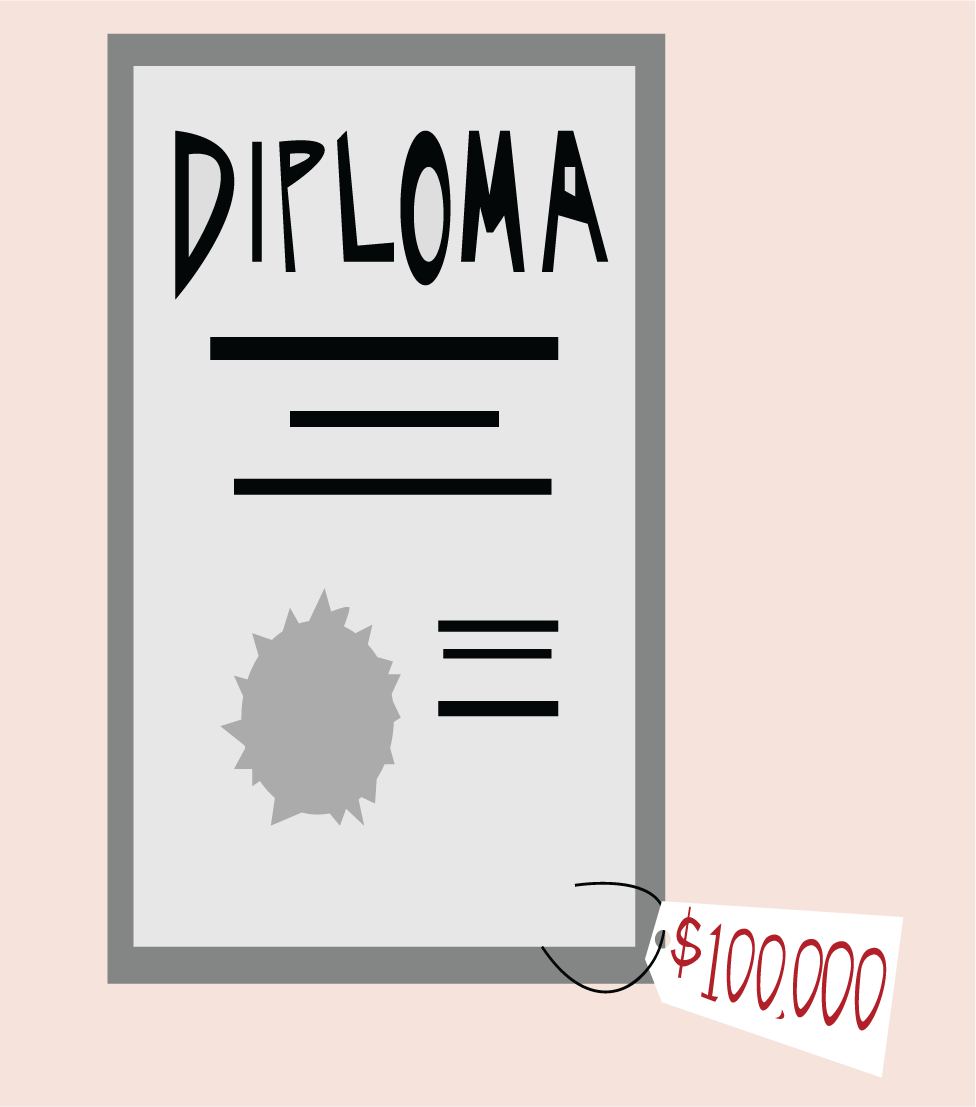

Government is fast exiting the business of funding higher education. At state universities, tuition costs have risen by 500 percent since 1985, and the price gap between leading public institutions and private colleges is narrowing sharply. Lawmakers in Washington and state capitols across the nation are compelling student users —the would-be beneficiaries—to finance their education privately. And the federal government is committed to lend monies, at unjustifiable rates of interest, to facilitate that end, leading to a student debt crisis that has become impossible to ignore.

In the public mind, the “privatization of education” encompasses university-industry partnerships, intellectual property licensing agreements, corporate sponsorship of research, or “contract education”—whereby a firm will pay a community college to up-skill its trainees. But the quintessential act of education privatization is to shift responsibility for funding onto individuals.

This transfer of fiscal responsibility from the state has been proceeding for more than three decades. Even in the immediate pre-recessionary years, when debt was still considered a worthy asset and employment a plausible prospect, it was easy to predict that mounting levels of student debt were unsustainable over time. Today, in the face of chronic underemployment, we can safely conclude that a large portion of the 1 trillion dollars currently owed by debtors is unpayable in their lifetimes. Two-thirds of U.S. students graduate with loan debt, averaging $27,000, and then rapidly fall behind in their payments—41 percent of the class of 2005 is either delinquent or in default.

Increasingly, student debt is a topic of discussion at family dinner tables and even in the halls of Congress. Thanks in large part to the great public amplifier of the Occupy movement, this year’s presidential contenders have been forced to embrace student loan reform as a talking point in their respective campaigns. But as student debt becomes the primary source of funding for American colleges and universities, it threatens the democratic ideal of a freethinking citizenry.

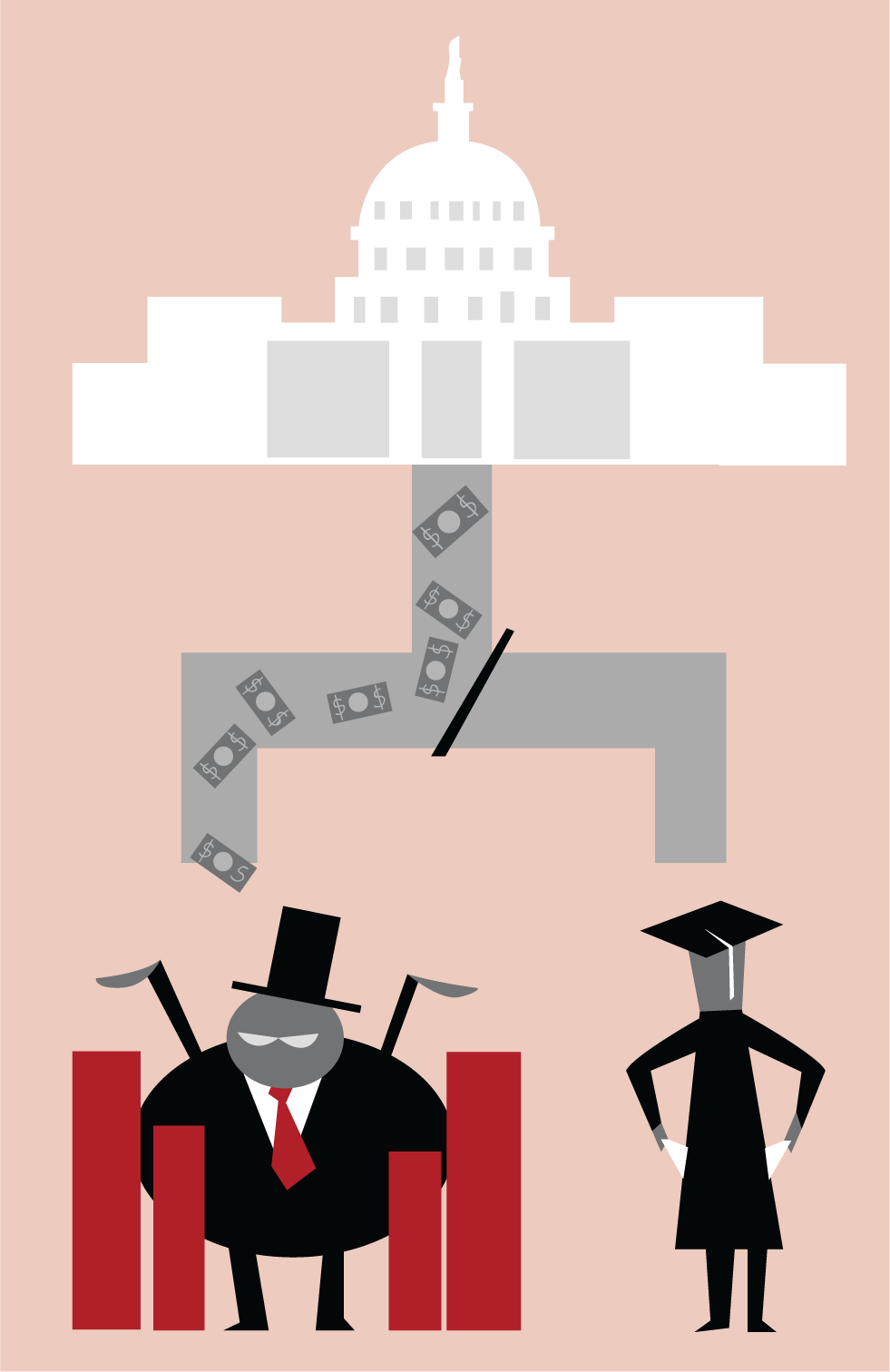

How the Profits Flow

Universities are one of the few places where neoliberalism—the economic program of deregulation, financialization, and free enterprise that used to be known as the Washington Consensus—has not missed a beat since its death was prematurely declared. In 2010, the federal government disbanded the old Federal Family Education Loan Program (FFELP) lending system. FFELP had been an extremely lucrative program for private banks, which were subsidized for issuing government-guaranteed loans. As part of this reorganization, all federal loans now originate with the government, though service fees for administering the loans are still designated to Sallie Mae, Nelnet, and other industry giants. In taking this step, the federal government put its official stamp on the neoliberal funding formula that is now normative in U.S. higher education.

Today, at a time when lending rates are at a historic low, federal loans are offered at rates (3.4 percent for subsidized, and 6.8 percent for unsubsidized Stafford loans, and 7.9 percent for PLUS loans for parents) that far exceed those at which the government borrows money. The profits are extravagant: 120 percent of every defaulted loan is recovered. In the private sector, they are even higher. While banks now only issue 20 percent of all student loans, the rate of increase in loan issuance is greater than for federal loans, and so private lending is expected to surpass the government sector in 10 to 15 years.

Unlike almost every other kind of debt, student loans are non-dischargeable through bankruptcy, and, over time, collection agencies have been granted extraordinary powers to extract payments, including the right to garnish wages, tax returns, and social security. It’s no wonder that student loans are among the most lucrative sectors of the financial industry. Nor is it any surprise to find a thriving market in securitized loans (almost a quarter—$234.2 billion—of the aggregate $1 trillion debt) known as SLABS (Student Loans Asset-Backed Securities).

Given the predatory nature of student lending, many commentators have compared SLABS to the subprime mortgage securitization racket that inflated the housing bubble and triggered the financial crash. Since SLABS are often bundled with other kinds of loans and traded on secondary debt markets, investors are not only speculating on the risk status of student loans, but also profiting from resale of the loans though collateralized derivatives. In the meantime, creditors stand to profit most from defaults, when additional fees and penalties kick in, and so they often seek out high-risk borrowers just as subprime lenders did during the housing bubble.

Over 40 percent of the class of 2005 is either delinquent or in default of their student loans.

Corey Fields

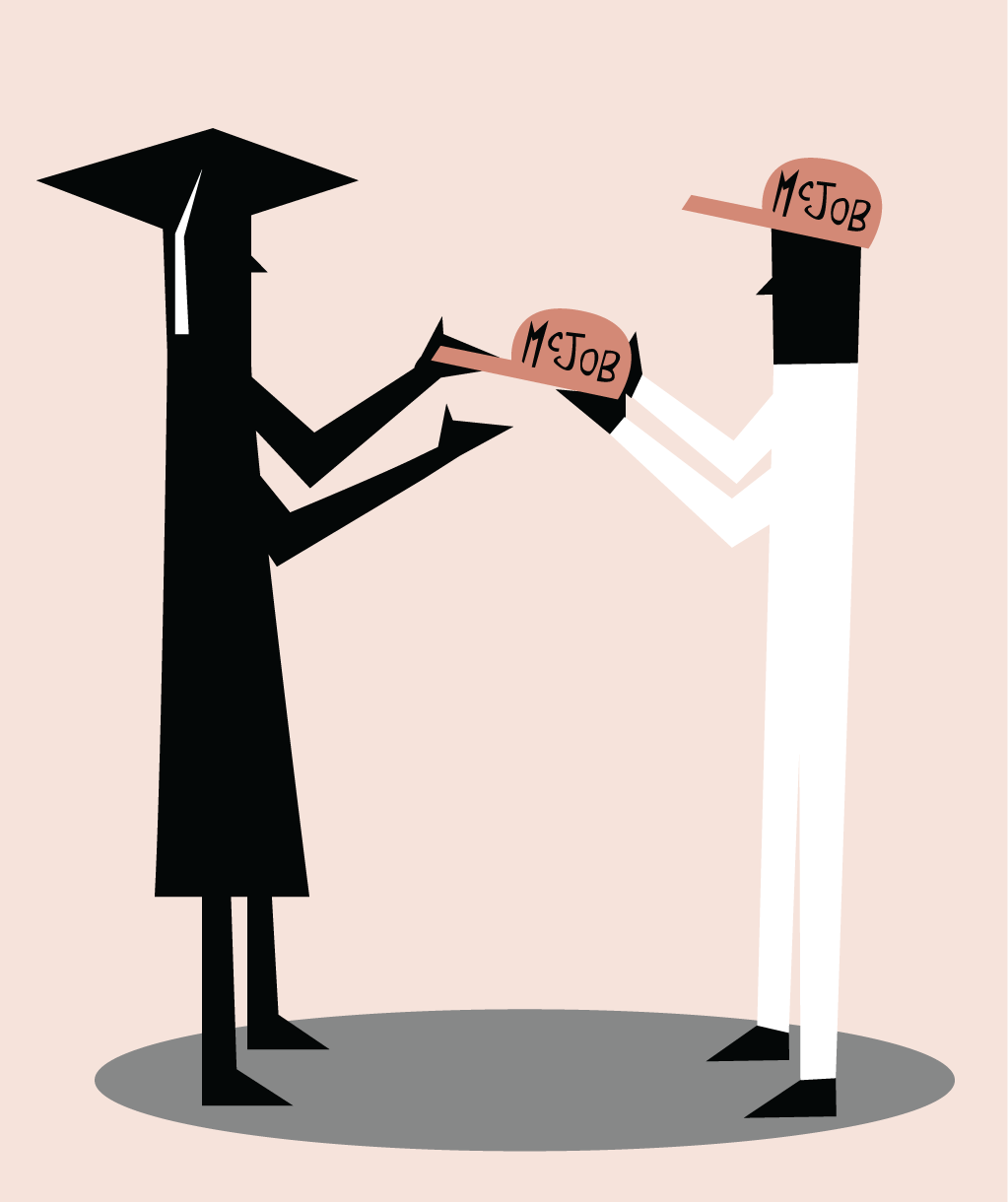

This is not the only way debt-based profit is mined from the daily business of higher education. As low-income families get priced out of public colleges, they are pushed into the for-profit system, whose mercurial rise has been fueled by the ready availability of federal loans. For families with a multigenerational experience of college, the staggering array of higher education choices can be confusing. But first-generation students, with limited access to information about their choices, are especially easy prey for the “admissions counselors” of for-profit colleges that act as a conduit for the lending industry.

Corey Fields

In the for-profit sector, 95 percent of students graduate with debt (versus 58 percent of students at all institutions), and graduation rates, already low, are falling. While the largest proportion of student debt is racked up by students from middle-income families seeking a private university degree, the overall impact of debt is magnified among low-income families. African Americans, among all racialized groups, graduate with the highest debt on average, and those in Deep South states, where community colleges do not participate in the federal loan system, are most disadvantaged of all.

Unlike almost every other kind of debt, student loans are non-dischargeable through bankruptcy.

Indenture or Investment?

With wealth now diverted more exclusively to the 1 percent (bypassing the top quintile to which most college graduates aspire), the belief that education debt is a smart investment in a high-income future has eroded. Should we, instead, compare student debt to a form of indenture? The analogy has served as a useful provocation. In a knowledge economy, where a college degree is considered a passport to a decent livelihood, workforce entrants must go into debt in return for the right to labor. This kind of contract is the essence of indenture. Moreover, for the traditionally indentured, employment has usually been guaranteed or is readily available, and the bonds are paid off in a relatively timely manner. By contrast, student debt can endure for decades, and employment prospects are more and more precarious. A damaged credit score—triggered by two delayed payments—will generate additional obstacles to finding employment, since many employers consult the student debt payment schedules of applicants to gauge their reliability.

The emerging pattern for those who want to preserve their credit record is to put their preferred career paths on hold for several years, and therefore risk abandoning them, until they have paid off their loans through employment options that are much less desirable. Ironically, the quickest pathway toward discharging debts is to find work in the finance industry, issuing loans, or speculating on derivatives. For those caught in the limbo of more precarious labor, the burden of finding the means to pay off student debt may drastically reduce the choices traditionally available to the college-educated workforce. The outcome is a nightmare to national economic managers struggling to keep the standard elements of the American Dream in place—homeownership, family formation, upwardly mobile consumer behavior.

Practically speaking, no reform program of any substance is on the legislative horizon, least of all one that would regulate the predatory lending practices of Wall Street banks. Congressional members have proposed the Student Loan Forgiveness Act (H.R. 4170)—which allows for loan forgiveness after 10 years of appropriate debt service—and the Private Student Bankruptcy Fairness Act (H.R. 2028)—which seeks to restore the ability to discharge private student loans through bankruptcy. But these bills have no chance of passing in their current form.

The debt relief being pushed by the Obama administration this year is a token gesture, aimed at getting some traction on the youth vote—especially the more disillusioned or alienated student constituencies. GOP interest in blocking any Obama competitive advantage ensured that, in June, the House approved a bill extending the temporary lower rate (3.4 percent) on subsidized Stafford loans for another year. Hailed as a major victory in the Obama camp, the relief amounted to a mere $9 in savings per month for a handful of borrowers. At the same time, and with much less public attention, graduate students lost the federal subsidy by which the government paid the interest accrued on subsidized loans while in school and for six months after graduation.

Nor should we expect enlightened responses from university leaders, for whom debt-financed education has lavishly serviced their own bank accounts. The salaries of senior administrators have risen in tandem with tuition costs and student debt. Faculty have established their own wall of denial around the issue, which may take some time to breach. Since their salaries have been stagnant or rising at rates below the cost of living increases, they (quite rightly) don’t feel responsible for skyrocketing college costs. Nor are they keen to inflame public sentiment that may further destabilize the fragile state of their profession.

Student debtors have begun to break the silence. At Occupy locations around the country, those confronting chronic underemployment while being saddled with crushing debt burdens offered eloquent testimony. Tumblr and other websites swelled with the stories of students who felt too constrained by guilt to stand up in the face-to-face agora of Occupy. The act of casting aside the shame and humiliation that accompanies debt, especially for those aspiring to join the middle class, was an important kind of “coming out” for student debtors. It seemed to herald a decisive political moment, and may now be blossoming into a movement all of its own (see www.strikedebt.org). The alternative—suffering the consequences of debt and default in private—is a thinly documented trail of tears, leading to depression, divorce, and suicide in ever increasing numbers.

Analysts who have investigated Occupy’s claims about the 1 percent have concluded that, of all the factors responsible for the upward redistribution of wealth, financial manipulation of debt ranks very high. But the imposition of debt is not just a mode of wealth accumulation, it is also a form of social control, with acute political consequences.

This was most notable in the case of the International Monetary Fund (IMF) “debt trap” visited upon so many postcolonial countries as part of Cold War client diplomacy. In the global North, debt has been institutionalized for so long as a “good” consumer asset that we forget how homeownership was promoted as an explicitly anti-socialist policy in the United States in the 1920s. Subsequently, the long-term mortgage loan became the basis of anti-communist citizenship; William Levitt, the master merchant builder, pronounced that “no man can be a homeowner and a Communist.” In the postwar decades, the threat of a ruined credit score effectively limited the political agility of our “nation of homeowners.”

Can the same be said of student debt? Protest is no longer a rite of passage for students. The rising debt burden has played no small part in stifling the optional political imagination of students in the decades since the 1960s. Now typically saddled with debts on day one of college, they are obliged to seek out low-paying jobs to stave off further debt; they are compelled to think of their degree as a bargain for which their future wages have been traded. These are not conditions under which a free critical mind is likely to be cultivated. This is one of the reasons why student debt abolition might be more effectively approached as the target of a political movement than one aimed at limited economic reforms.

Corey Fields

Debt relief is sorely needed but this single corrective act by itself won’t alter the formula for debt-financed education.

Real Debt Relief

Most of the initiatives that have sprung up in response to the student debt crisis are aimed at limited economic reforms, such as restoring bankruptcy provisions and other protections that are enjoyed by consumer debtors. But paying for education is not like buying a flat-screen TV, and student loans should not be packaged in the same way.

Real change will alter the customary neoliberal practice of treating public goods, like education, as a profit center. The long list of developed and developing countries—none of them as affluent as the United States—which provide free public education demonstrate how different national priorities are elsewhere. The United States is an outlier in this regard, and efforts to export the pay-per model have met with strong student resistance, most recently, in Chile, England, and Quebec. In response to efforts by states to pay off their sovereign debt by slashing education budgets, the European student resistance crystallized around the slogan, “We Won’t Pay for Your Crisis.” In college towns across the United States, the red square, symbol of the Quebec movement (carrement dans le rouge), recently became the summer clothing accessory of choice.

Debt relief is sorely needed, and a write-off of all current student debt would be a noble, and appropriate, contribution to the jubilee tradition, whereby elites periodically forgive unsustainable debt burdens. But this single corrective act by itself won’t alter the formula for the debt financing of education. An affordable education system needs to be reestablished.

Corey Fields

As part of our Occupy Student Debt Campaign, we argued that for $70 billion a year, the federal government could, and should, cover the tuition of all students enrolled in two and four year public colleges. In the twentieth century, the decision to properly fund K-12 education was a prerequisite for a society that wanted a stable middle class. If the American middle class has any future in this century, then a decision will have to be made to extend the guarantee to tertiary education. Loans should be interest-free—no one should profit from them. So, too, private universities, which benefit from public largesse in all sorts of ways, but not least through the federal loan program, should adopt fiscal transparency. Students and their families surely have a right to know how colleges spend and allocate their tuition fees.

Top university administrators and trustees have had little to say about the rapid escalation of tuition costs over the last two decades. They seem content to weather the current storm. It is unlikely that costs will stabilize until demand falls off, and even if this were to happen nationally, the growth in overseas demand—fueled by the desire of the swelling middle class in the global South for brand-name degrees—would more than make up the deficit.

Analysts put the global growth rate at 80 percent over the next decade, and that figure may well dictate how college administrators, faced with weakening political will on the part of their state legislatures, react to budgetary dilemmas. The rush to establish online and offshore programs, and branch campuses is a telltale symptom of their response. There are many risks involved in such ventures, especially those hosted by authoritarian states. But the prospect of adding overseas revenue streams will continue to attract higher education’s fiscal managers, driven by desperation or ambition or simply by their training in neoliberal economics.

The struggle over wages was a defining feature of the industrial era. Will the struggle over debt play a similar role in the postindustrial economy? Given the centrality of higher education to the formation of knowledge capitalism, the growing conflict around student debt seems to fit the bill. Bargaining over the outcome will take many forms. Just as industrial elites once recognized that wages had to be raised to stimulate consumer purchasing, so too, they will entertain the reduction of debt burdens to facilitate the re-entry of middle-class debtors into the circuits of big-ticket consumption.

Some are already contemplating debt strikes and other methods of debt refusal. For these tactics to gain legitimacy in the public mind, the moral ideology of honoring debts, however unjustly incurred, will need to be challenged and eroded. The track record of the finance sector before and after 2008 shows that this morality does not apply to Wall Street. Loans are no more than electronic figures on a computer screen. They are new forms of money and credit that did not exist hitherto and they are created ex nihilo for the use of the borrower. Financiers know this, and so they treat debts accordingly, as matters to be renegotiated or written off at will. Only the little people are expected to actually pay off their debts.