Abstract

The rising cost of higher education has led to increased tuition costs for students and their families, forcing more students to secure larger amounts of debt to finance their educational pursuits. Although scholars have explored how student loan debt accumulation influences higher education persistence and graduation, an unexplored area of higher education finance and debt is the relationship between unpaid tuition balances on community college student graduation. This analysis attempts to illuminate this gap by utilizing a unique institutional dataset with data from the National Student Clearinghouse to analyze the relationship between unpaid tuition balances and postsecondary graduation for community college students. Results suggest that having an outstanding tuition balance dramatically decreases the likelihood of graduation 3 years out from the unpaid balance. Implications for future research and practice are discussed.

Keywords

Introduction

Educational researchers, institutional leaders, and government policymakers have noted that accumulating student loan debt is associated with higher levels of student attrition and with lower likelihoods of graduating from any higher education institution (DesJardins et al., 2002; Dowd & Coury, 2006; Gladieux & Perna, 2005; Herzog, 2018; McKinney & Burridge, 2015). A dramatic shift in public support for American higher education has led to a decrease in state subsidy support and increased tuition for students and their families (Ma et al., 2017). These trends have correlated to a rise in student loan accumulation and student loan default among undergraduate students (Hillman, 2014; Velez & Woo, 2017), with the national average of debt totaling $28,950 for students graduating from a 4-year public or nonpublic institution (The Institute for College Access & Success, 2020). The accumulation of postsecondary educational debt—both in the average amount and aggregate total—has had observable consequences for the overall health of the American economy (Brown et al., 2019) and critical implications for the equity agenda, complicating how lower socioeconomic individuals and individuals from traditionally underrepresented populations gain access to higher education altogether and persist through graduation (Tierney & Venegas, 2009).

Although scholars have analyzed the influence of student loan debt on postsecondary persistence and graduation, an underexplored area of research in higher education finance is the relationship between delinquent tuition debt and higher education graduation. Although accumulating loan debt totals may discourage students from progressing through subsequent terms (Dowd & Coury, 2006), higher education institutions often place registration holds on students’ accounts with delinquent tuition debts, preventing them from registering in future terms should they desire (Jackson, 2017). These holds often remain on the student's account until the balance is repaid, preventing students from reenrolling at the institution in the months or years after the initial stop-out. To recoup these delinquent balances public institutions often turn over delinquent accounts to state agencies for collection via state tax withholding, whereas private institutions might solicit third-party collection agencies. Community college students may be at an additional risk of unpaid tuition balances, given the socioeconomic and racial composition of the students who attend public 2-year institutions (Rios-Aguilar et al., 2018; Snyder et al., 2019). Community college students are less likely to borrow money relative to their 4-year peers (Gladieux & Perna, 2005), suggesting that community college students whose balances are left unmet through scholarships and grants will be forced to pay the remaining balance out of pocket.

Current research on the relationship between educational debt and graduation focuses on debt that is accumulated after students access the federal financial aid system (i.e., student loans). Delinquent tuition debt is unique in that it is educational debt that occurs because students have not accessed potential monies available via the federal financial aid system, either by failing to complete the financial aid process or by rejecting the awards that were offered. Research has demonstrated that completing the Free Application for Federal Student Aid (FAFSA) is a complicated and bureaucratic ordeal for students (Davidson, 2015; Taylor, 2019) and that community college students are at a greater risk of not accessing desperately needed monies through hurdles and barriers experienced throughout the financial aid process (Luna-Torres et al., 2019; McKinney & Novak, 2012). Because unpaid tuition balances are an underexplored phenomenon in higher education research, it is unclear how students’ experiences with the financial aid system influence delinquent tuition debt. However, research has shown that monies available through the federal financial aid system are enough to cover the average tuition and fees at a community college (Ma et al., 2017), suggesting that FAFSA completion has some relationship with delinquent tuition debt.

Given that institutions prevent students from persisting through subsequent terms if they have an unpaid tuition balance, it seems obvious that postsecondary credential completion percentages would be diminished for such students, and that studying such a phenomenon might not be necessary. However, because this phenomenon is understudied, institutional leaders and policymakers do not have a sense of the magnitude of the issue and its subsequent impact on institutional fiscal health or individual student success. It could be the case that most students with unpaid tuition balances find the needed economic resources to repay their previous tuition obligations and progress through their course of study with little to no delay. Because limited literature does not speak to this phenomenon institutional leaders and policymakers have no knowledge or resources to address potential gaps in service. This exploratory analysis addresses the gap in the literature by utilizing Chen’s (2008) heterogeneous framework on student departure and financial aid to analyze the relationship between delinquent tuition debt and postsecondary graduation for students at a large, urban, Midwest community college, and to illuminate any observable differences between the students who experience unpaid tuition balances and students who do not. Data from the National Student Clearinghouse was combined with the institutional data and binary logistic regression models constructed to understand the relationship between delinquent tuition and graduation, illuminating this gap in higher education finance research. Data on student demographics, pre-college characteristics, and FAFSA were controlled for in the analysis. Results suggest that students with unpaid tuition balances are at significantly diminished odds from graduating with any postsecondary credential, that the composition of students who endure delinquent tuition debt has implications for the equity agenda, and that the number of students who depart without a credential has crucial budgetary consequences for the college. Several implications for future research and practice are discussed.

Review of Literature

Theoretical Framework

Chen (2008) developed a heterogeneous model to understand how various financial aid awards and philosophies influence student dropout behavior from higher education. Chen (2008) explained that early models that attempted to understand how financial aid and economic considerations influence student departure were constructed with monolithic understandings of student populations and institutions. Little consideration was given to the variances in institutional and individual variables. Early studies of student departure and financial aid typically involved one institution where dropout rates were measured at one moment in time using descriptive statistics (Chen, 2008). Chen (2008) explained that larger, federal datasets with stratified samples across institutional and individual characteristics are ideal for these types of analyses and that logistic regression models can be utilized due to the dichotomous nature of student departure as the dependent variable.

Rather than relying on one singular theoretical orientation to interpret financial aid packages’ influence on student enrollment and dropout behaviors, Chen’s heterogeneous model integrates perspectives from various disciplines and theoretical orientations, including psychology, sociology, organizational, and interactionist theories (Chen & DesJardins, 2010). In addition to these four categories, Chen (2008) advocated that several economic theories be considered when modeling how financial aid influences student departure: (1) liquidity constraints, (2) price elasticity or sensitivity, and (3) debt aversion (Chen & DesJardins, 2010). Chen (2008) explained that the introduction of economic theories into the theoretical models designed to understand student departure began in the 1960s and were grounded in the understanding of Human Capital Theory. Human Capital Theory assumes that actors within markets (higher education in this case) make rational decisions regarding the time and energy required by pursuing education and weigh those costs against the potential earnings and utility of obtaining a higher education degree (Chen, 2008). However, Chen (2008) noted that these market assumptions about rational actors failed to consider how different racial, ethnic, and socioeconomic populations hold different attitudes towards money and debt and that these different attitudes and cultural assumptions might explain why specific student populations fail to matriculate or persist through higher education at certain thresholds of financial aid and real cost.

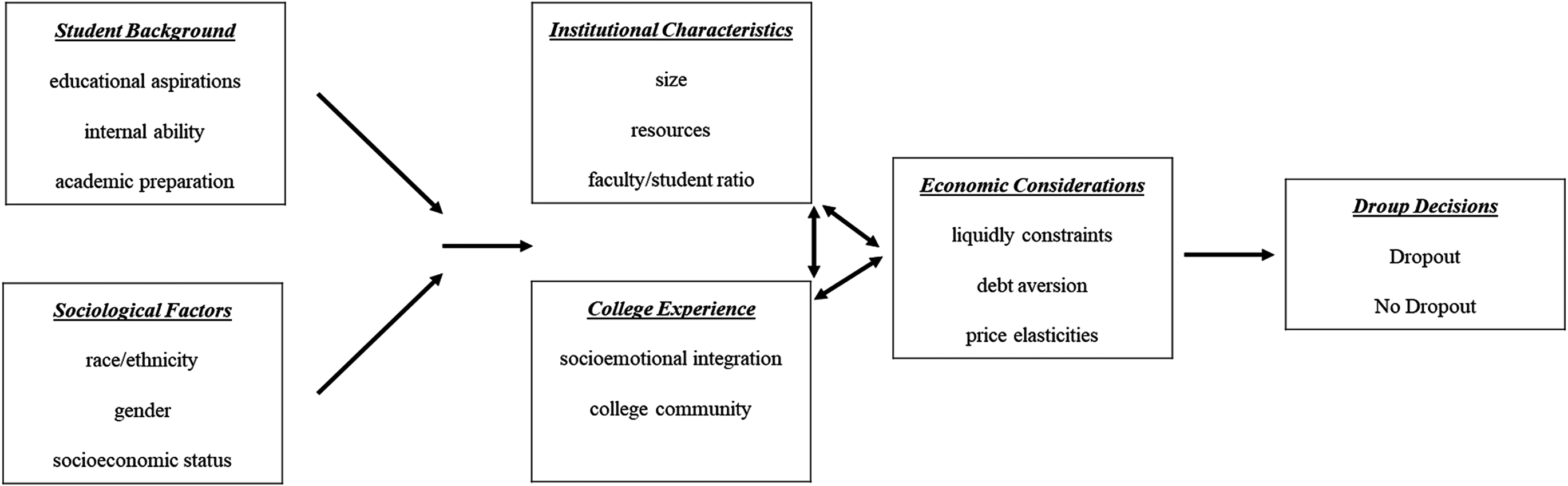

Chen and DesJardins (2010) noted that an essential assumption in Chen’s (2008) model is that individuals from lower socioeconomic backgrounds will be more price sensitive to their education’s overall cost when grants and scholarships are reduced, increasing their cost-share burden and influencing their dropout. Coupled with this assumption, individuals from racial, cultural, or socioeconomic backgrounds that have an aversion to debt may experience higher dropout rates with financial aid packages that heavily rely on loans (Chen, 2008). Chen and DesJardins (2010) also noted that work-study programs and aid packages featuring a higher ratio of loans to overall cost would not influence students’ behavior relative to gift-aid packages. A second assumption that can be tested with Chen’s model is that similar aid packages will affect students of color in different, observable ways compared to their White peers (Chen, 2008) (Figure 1).

Visual Representation of Chen’s Heterogenous Model of Student Departure (Adapted from Chen and Desjardins (2010) and from Chen (2007)).

Several studies have found validity in Chen’s (2008) model and the assumption that different types of aid influence persistence and dropout behavior differently for students of color (Chen & DesJardins, 2010; Luna-Torres et al., 2019; Yang & Venezia, 2020). Chen and DesJardins (2010) utilized data from the Beginning Post-Secondary (BPS:96/01) and the National Postsecondary Student Aid Study (NPSAS:96) federal data cohorts to analyze the interaction between student dropout and financial aid. Chen and Desjardins employed a discrete-time event history model to track and interpret student dropout over 6 years. When compared to White students, the authors found that students of color were less likely to drop out when awarded a Pell Grant; the results revealed an increased effect among Hispanic and Asian students in particular. When evaluating the likelihood of dropout without the Pell Grant, these same students were more likely to drop out than their White peers, suggesting that students who receive the Pell Grant have increased odds of persisting through college. Luna-Torres et al. (2019) utilized data from a large, urban community college in Texas that serves more than 70,000 students in an academic year. Controlling for race, gender, and socioeconomic status, the researchers found that financial aid packages with higher ratios of gift-aid to loans positively influenced persistence rates for students of color and lower socioeconomic students. Yang and Venezia (2020) utilized data from the 2004/2009 Beginning Postsecondary Students Longitudinal Study (BPS: 04/09) to study the impact of financial aid on rural community college students’ graduation. The authors used the Integrated Postsecondary Education Data System (IPEDS) to determine whether students were rural, urban, or suburban students. Although the authors did not find statistically significant results on the effect of Pell Grants and graduation 3 and 6 years after starting at a community college, they did find that higher amounts of Federal Unsubsidized Loans had a negative effect on graduation, suggesting that rural community college students have an aversion to particular types of debt.

FAFSA Completion

The combination of both grant and loan awards can often cover a community college's entire published costs (Ma et al., 2017). Thus, most community college students could pay their tuition obligations each term through some combination of Title IV awards by completing the FAFSA. However, research has shown that community college students fail to complete the FAFSA and secure Title IV awards relative to their peers in other sectors of higher education (Grinder et al., 2018; Holzman et al., 2020; Klasik, 2012; McKinney & Novak, 2012; Romano & Millard, 2006; Snyder et al., 2019). Utilizing federal data, Romano and Millard (2006) found that nearly two-thirds of all community college students did not file a FAFSA in 1999–2000. Only 1.2 million of the 8.9 million community college students in 2015–2016 received any Title IV award (Grinder et al., 2018). Both Klasik (2012) and Holzman et al. (2020) noted that lower socioeconomic students and students of color were less likely to complete the FAFSA than students from higher socioeconomic backgrounds and White students, respectively. Lower socioeconomic students are overrepresented at community colleges relative to American higher education sectors (Snyder et al., 2019). Several studies have noted that part-time community college students are less likely to complete the FAFSA and receive a Title IV award relative to their full-time peers, even when controlling for socioeconomic status (McKinney & Novak, 2012; Romano & Millard, 2006; Snyder et al., 2019).

Several structural barriers have been identified as possible explanations for the lack of community college student FAFSA completions (Davidson, 2015; Rios-Aguilar et al., 2018; Taylor, 2019). Davidson (2015) noted that the financial aid verification process, a quality control measure established by the U.S. Department of Education to ensure the FAFSA’s information is accurate, is a costly program that often requires the most high-risk students to complete additional steps to secure Title IV awards. Rios-Aguilar et al. (2018) found that almost half of the students at a large, Urban community college were selected for some sort of financial aid verification. The verification process often requires students to supply additional paperwork to the institution’s financial aid office. Scholars have noted that the verification process differs significantly between institutions and higher education sectors (MacCallum, 2008; Romano & Millard, 2006). MacCallum (2008) found that institutions that spent less resources on their financial aid offices had lower FAFSA completions. Rios-Aguilar et al. (2018) found that 75% of students flagged for verification never finished the process and that 20% of those students would have been eligible to receive a Pell Grant. Taylor’s (2019) analysis of financial aid information and directions found that the average higher education institution's directions are written at a reading level that 50% of the United States population has not achieved. Although Taylor did find that community college financial aid information was the most accessible when compared to other sectors of American higher education, the average community colleges’ financial aid directions were written at a 12.7-grade level, suggesting that students who graduate high school with a 12th-grade reading level will lack the necessary comprehension to understand the financial aid process at their local community college. Structured interventions can help minoritized populations complete their FAFSAs and secure their needed Title IV awards. With H&R Block, Bettinger et al. (2012) designed an empirical study where a treatment group of tax filers were assisted in completing the FAFSA. Compared to students who received no additional assistance in completing the FAFSA, dependent students who received the assistance increased their FAFSA completions by 15%, increased their enrollment in public colleges and universities by 6.5%, and increased their persistence through year 2 by 8%.

Student Loans, Loan Default, and Consumer Debt

Over the past 30 years, a shift in federal financial aid policy has prioritized student loans over gift aid (Baum et al., 2019; Hillman, 2014). This policy shift has been coupled with increased tuition costs and decreased purchasing power of what gift-aid is awarded to students (Baum et al., 2019; Ma et al., 2017). Increased costs have forced students and their families to secure higher student loans to access higher education (Canché González, 2020; Velez & Woo, 2017). Using data from two national samples, Canché González (2020) found a 15% increase in the number of students who borrowed loans from 1991 to 2013 and found that the average amount of student debt increased by $5,800 during the same timeframe. Velez and Woo (2017) found that 68% of college seniors in 2011–2012 had borrowed money to help finance their education, a percentage up from 51% in 1999–2000. Further, Velez and Woo (2017) also found that the average student debt increased by more than $10,000 when adjusted for inflation. In an analysis of borrowing patterns from 2000 to 2016, Chan et al. (2019) found increased odds of borrowing for Black students than their White peers and decreased odds for borrowing for Hispanic students during the same timeframe.

Two trends are associated with the increase in student loan accumulation. First, student debt has become a larger percentage of the aggregate consumer debt composition (Brown et al., 2019; Federal Reserve Bank of New York, 2020). A recent Quarterly Report on Consumer Debt revealed that student loan debt has grown from 3% of all household debt in 2003 to 11% in 2020 (Federal Reserve Bank of New York, 2020). Brown et al. (2019) found that the average amount of consumer debt held by Americans aged 65 and older increased between 2003 and 2007, whereas the average amount of consumer debt decreased for Americans aged 18–34 during the same timeframe. However, the composition of that debt changed; mortgage and auto loans remained the largest portion of consumer debt for older Americans, whereas educational debt, typically in student loans, became the leading portion of debt for younger Americans. It must be noted that these studies reflect debt accumulated through student loans and not debt accumulated through delinquent tuition balances. Because unpaid tuition debt is an understudied phenomenon, it is unclear how including delinquent tuition debt within the larger understanding of consumer debt would alter the average American's debt composition or how much unpaid tuition debt would comprise overall educational debt relative to student loans.

Second, many borrowers with higher average debts have led to an increase in student loan default (Gladieux & Perna, 2005; Hillman, 2014). Hillman (2014) explained that the number of undergraduate students who entered default within 2 years of college graduation rose by more than 250,000 between 2003 and 2010 and that 1 of 10 borrowers of federal student loans will default on their payments at some point in time. Gladieux and Perna (2005) found that undergraduate students who dropped out and borrowed money had similar economic prospects to those students who dropped out and did not borrow money but were saddled with a mean loan amount of $7,000 that required repayment. Almost 25% of these non-graduates defaulted on their loans at least once between 1996 and 2001. Again, these default means only include those students who defaulted on loan payments and not those students who defaulted on delinquent tuition payments. Delinquent tuition accounts turned over to the state, or third-party collection agencies could seize money through state tax returns. At the same time, students in loan default may negotiate more favorable terms for repayment or secure extended loan forbearance. It is unclear how unpaid tuition balances map against the growing phenomenon of educational debt default and how students meet their various debt obligations.

Although no specific empirical research exists on the debt collection of students with unpaid tuition bills, trends in student loan default, and broader American consumer debt collection, can help higher education researchers and practitioners determine what students may be at risk for not paying their tuition balances (Braga et al., 2019; Gross et al., 2009; Hillman, 2014). In a review of the literature surrounding student loan default rates over 30 years, Gross et al. (2009) found that students who attended community colleges and proprietary institutions were more likely to default on their loans when compared to students who attended 4-year institutions, but that the differences virtually disappear when controlled for student characteristics. However, Hillman’s (2014) analysis did find an increased probability of default among students who attended 2- and 4-year proprietary institutions, despite controlling for student demographics. Gross et al. (2009) also noted that students who attended institutions with greater wealth and financial resources were less likely to default on their loans when compared to students who attended institutions with fewer resources. Both Gross et al. (2009) and Hillman (2014) noted several student demographics and socioeconomic characteristics associated with higher default rates. Students of color, mainly Black and African American students, are more likely to default on their loans than their White peers. Students from lower income households and households that claim more dependents are also associated with higher default rates. In addition to institutional and student characteristics, Gross et al. (2009) also noted several academic correlations to the default rate. These characteristics include enrollment intensity and area of study.

Educational policy that continues to rely on student loans to finance higher education may take away from the larger economic benefits to society by shackling their college graduates with this type of debt, making it more likely that a college graduate will fail to meet their other debt obligations. Further, students of color and lower economic students are less likely to have outstanding debt obligations, suggesting that minoritized populations have less access to the credit and debt service sector relative to their more privileged peers. However, when these populations secure educational debt, they are more likely to default, highlighting the liquidity constraints and unstable employment opportunities that disproportionally affect high-risk communities. Like the previous studies and reports on educational debt default and broader consumer debt composition, delinquent tuition balances are not considered, so it is unknown how unpaid debt turned over to state collection agencies increases these students’ debt obligations.

Several studies and reports have noted how borrowing student loans and secure educational debt can deter students from enrolling in higher education altogether or encourage students to dropout of higher education before earning a credential (DesJardins et al., 2002; Dowd & Coury, 2006; Gladieux & Perna, 2005; Herzog, 2018; McKinney & Burridge, 2015). Gladieux and Perna (2005) found that half of the students borrowed money to finance their postsecondary pursuits. In contrast, students at public and private 4-year institutions were more likely to borrow money relative to community college students. More than one-fifth of these students had departed postsecondary institutions by 2001 without a credential. Using federal data, both Gladieux and Perna (2005) and McKinney and Burridge (2015) found that community college students who did secure a student loan were more likely to persist relative to their peers without loans. However, McKinney and Burridge (2015) found that gains in persistence rates were only observed through year 2 of college, and that persistence rates declined between years 3 and 6. Dowd and Coury (2006), also using federal data, found that student loans had a negative effect on persistence through year 2 of college but little impact on credential attainment. However, the authors theorize that students who are discouraged from persisting due to accumulating debt totals would be more likely to stop-out before graduation.

It must be noted that the above studies and reports only focus on loan debt and do not consider how delinquent tuition balances might also influence persistence and graduation. Studies on the effect of loan accumulation on persistence and graduation reveal a psychological impact; students may be discouraged from enrolling in higher education or persisting through subsequent terms as debt accumulates. In many cases, delinquent tuition accounts physically prevent students from persisting to subsequent terms. Thus, it is likely that delinquent tuition debts are, on average, lower than student loan debt totals, but must be repaid quickly for the student to progress through their education. To date, no empirical studies exist on the relationship between delinquent tuition balances and graduation, intensifying the need to illuminate this gap in educational finance and debt accumulation research.

Methods and Data

Data

For this analysis, data were collected from Alpha Community College (pseudonym), a large, urban community college in the Midwest United States. Information on all students enrolled in the fall of 2016 was received from the institution’s research office via an Excel document. The fall of 2016 was selected as the year of study because it provides for 3 years of persistence and graduation data after the initial enrollment date. Although this analysis includes students beyond the first-time, full-time cohort, tracking graduation and persistence rates for community college students 3 years after enrollment is consistent with the National Center for Education Statistics’ IPEDS reporting timeframe of 150% of the normal time for graduation (National Center for Education Statistics, n.d.). For 2-year institutions, this timeframe is 3 years.

In the fall of 2016, Alpha Community College had 17,755 unique students enrolled for credit. From these initial records of students, 2,286 students were high school students participating in the state’s dual enrollment program. These students were excluded from the analysis, as they were not eligible for federal financial aid and are not required to pay tuition for their coursework under most circumstances. In addition to the high school students, 664 international students were also excluded from the analysis. Most foreign-born students are not eligible for Title IV awards (U.S. Department of Education, n.d.), and international students must demonstrate their financial capabilities before being granted their student visas (U.S. Department of Homeland Security, n.d.). As a result, less than 2% of the international students in the fall of 2016 had an unpaid tuition balance. Once these two student groups were excluded, a sample of 14,805 students were included in the analysis. Data from the bursar’s Alpha Community College office were combined with the larger enrollment data to identify those students from the fall of 2016 who had unpaid tuition balances on their accounts. Of the 14,805 students included in the sample, 652 students had unpaid tuition balances in the fall of 2016, which was 4.4% of the sample. Alpha Community College’s policy requires students to pay all tuition and fees before registering for a subsequent term, so students with unpaid tuition balances are prohibited from progressing through future terms with a delinquent balance. Finally, data from the National Student Clearing House was combined with the institutional data to determine graduation rates at both Alpha Community College and any Title IV institution.

Research Questions and Methods

Two research questions guided this analysis:

What is the relationship between an unpaid tuition balance and postsecondary credential obtainment for community college students? Are there any observable differences in the students who have unpaid tuition balances at a community college?

To answer each of these questions, descriptive statistics were gathered, comparing the entire sample of students to the students who had unpaid tuition balances. Most of the control variables gathered for this analysis were categorical, so the percentages of both the entire sample and students with unpaid tuition balances were calculated. For continuous variables, means and standard deviations were included.

A binary logistic regression model was conducted to calculate the odds of postsecondary graduation for students with an unpaid tuition balance. Binary regression was chosen because this model’s dependent variable was credential completion and had a dichotomous outcome of “Yes” or “No.” These outcomes were coded as “1” and ‘0,” respectively, within the dataset. Institutional data and data from the National Student Clearing House were combined to create a dichotomous credential obtainment outcome 3 years after the term in question. The model explained 22.5% (Nagelkerke R2) of the variance of credential completion in 68.6% of the cases. The Hosmer and Lemeshow Test revealed a p = .612, suggesting a good fit for the model.

A binary logistic regression model was also conducted to determine if any of the first analysis’s control variables might influence the odds that a student would leave the term with an unpaid tuition balance. The binary regression model was also appropriate for this model, as the outcome for finishing the term with an unpaid tuition balance was “Yes” or “No.” Within the dataset, this outcome was coded as “1” and “2,” respectively. Given the dichotomous nature of the dependent variable, binary logistic regression was appropriate for this analysis. This model explained 27.4% (Nagelkerke R2) of the variance in 90.8% of the cases. The Hosmer and Lemeshow Test revealed a p = .823, suggesting a good fit for the model.

The inclusion of several control variables was guided by Chen’s (2008) model and previous literature on the connection between financial aid and student outcomes (Luna-Torres et al., 2019; MacCallum, 2008; McKinney & Novak, 2012). Student demographic information was captured on ethnicity, gender, and age. Several pre-college and enrollment variables were collected, including students’ placement test scores in math and writing. Information was also collected on the type of credential students were pursuing to determine how the study’s intended length might influence unpaid tuition. Finally, several financial aid variables were captured to determine how the verification process and specific financial awards might influence credential obtainment and unpaid tuition balances.

Findings

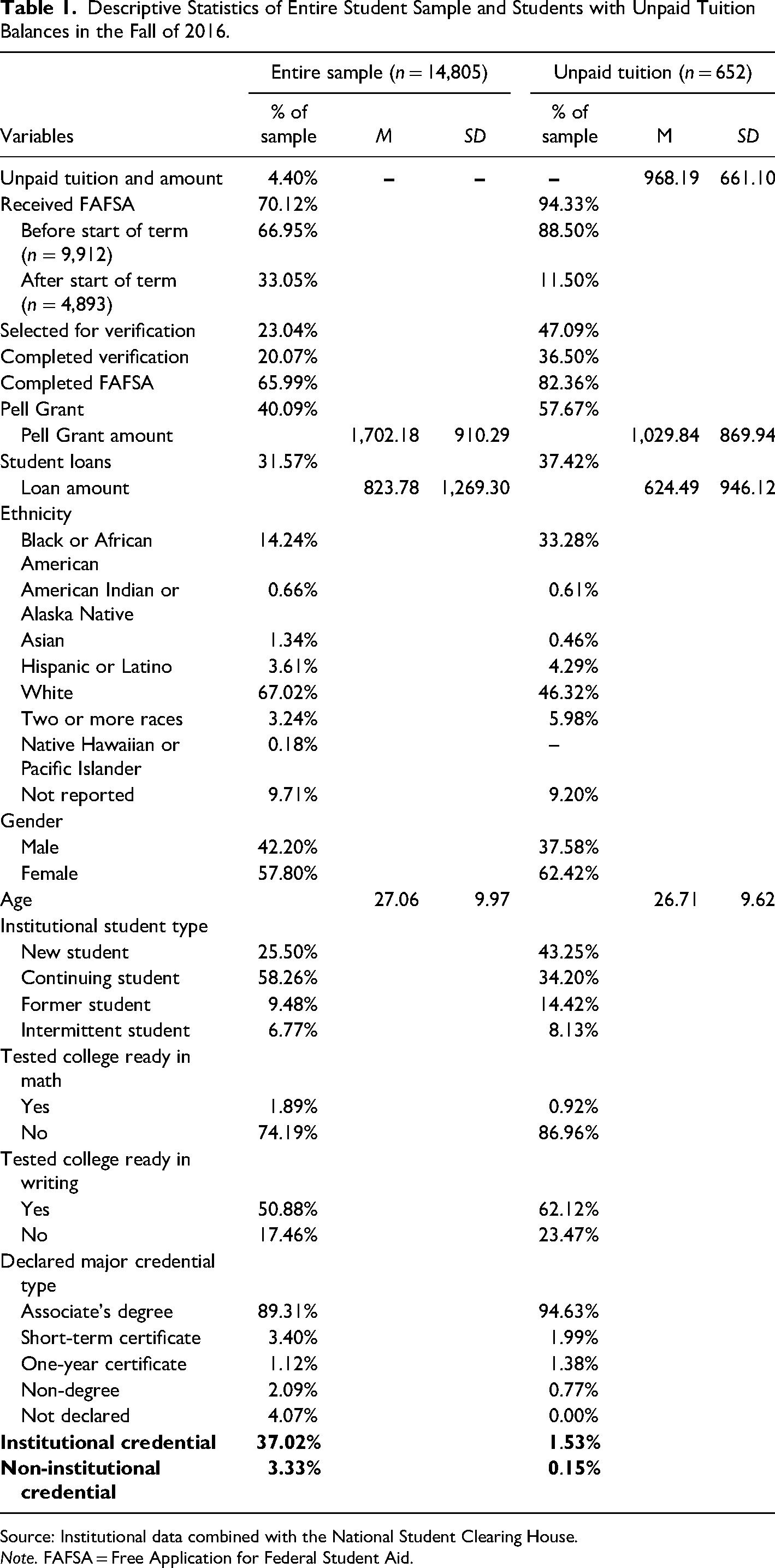

Table 1 includes the descriptive statistics comparing the entire sample of students to those who had unpaid tuition balances. Six hundred and fifty-two students at Alpha Community College had unpaid tuition balances in the fall of 2016, with a M = $969.19, SD = $661.10. As was reported above, 4.4% of the students included in this analysis had an unpaid tuition balance in the fall of 2016. Graduation rates were reported for both credentials obtained at Alpha Community College and credentials obtained at institutions that report to the National Student Clearinghouse. Students without delinquent tuition accounts in the fall of 2016 graduated at a rate of 37.02% at Alpha Community College, compared to a graduation rate of 1.53% for students who had delinquent tuition accounts. Beyond Alpha Community College, the graduation rates during the same timeframe were 3.33% and 0.15%, respectively.

Descriptive Statistics of Entire Student Sample and Students with Unpaid Tuition Balances in the Fall of 2016.

Source: Institutional data combined with the National Student Clearing House.

Note. FAFSA = Free Application for Federal Student Aid.

The descriptive statistics revealed essential differences between the entire sample and the students with delinquent tuition accounts. African American students represented 14.24% of the entire sample of students in the fall of 2016 but comprised 33.28% of the students with unpaid tuition balances. Eighty-two percent of the students with unpaid tuition balances completed the FAFSA, compared to only 65.99% of the entire sample. However, 47.09% of students with unpaid tuition balances were selected for FAFSA verification, compared to only 23% of students in the entire sample. The type of financial awards also differed between the two groups. Students with unpaid tuition balances had Pell Grants awards with a M = $1,029.84, SD = $869.94, compared to M = $1,702.18, SD = $910.29 of the entire sample. Loan amounts were also different, as students with unpaid tuition balances had M = $624.49, SD = $946.12 compared to M = $823.78, SD = $1,269.30 for students in the entire sample.

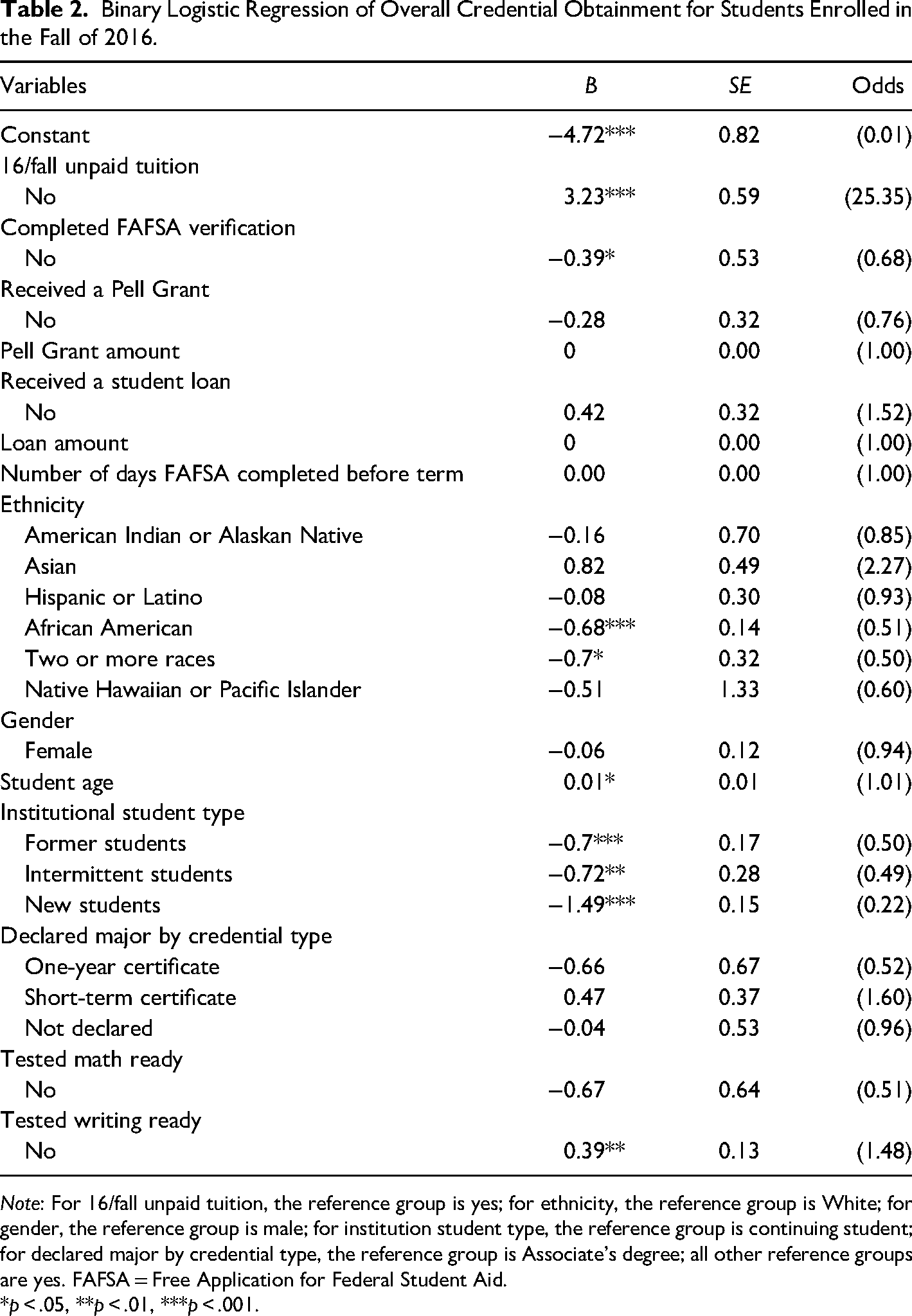

Table 2 contains the binary logistic regression model results calculating the odds of postsecondary graduation with an unpaid tuition balance. When controlling for student demographic information, pre-college enrollment characteristics, and FAFSA information, students who did not have unpaid tuition balances were 25 times more likely to graduate from any postsecondary institution compared to students who had delinquent tuition accounts. Compared to White students, African American students were half as likely to graduate when controlling for a host of covariates, including unpaid tuition balances. Only Asian students had a higher likelihood of graduating when controlling for unpaid tuition balances. Students who did not complete the financial aid verification process were 30% less likely to graduate within 3 years than students who completed the verification process. Receiving a Pell Grant increased the odds of graduation, but the amount of the Pell Grant did not change these odds. Receiving a student loan lowered the odds of graduation, but like the Pell Grant, the student loan amount did not change these odds.

Binary Logistic Regression of Overall Credential Obtainment for Students Enrolled in the Fall of 2016.

Note: For 16/fall unpaid tuition, the reference group is yes; for ethnicity, the reference group is White; for gender, the reference group is male; for institution student type, the reference group is continuing student; for declared major by credential type, the reference group is Associate's degree; all other reference groups are yes. FAFSA = Free Application for Federal Student Aid.

*p < .05, **p < .01, ***p < .001.

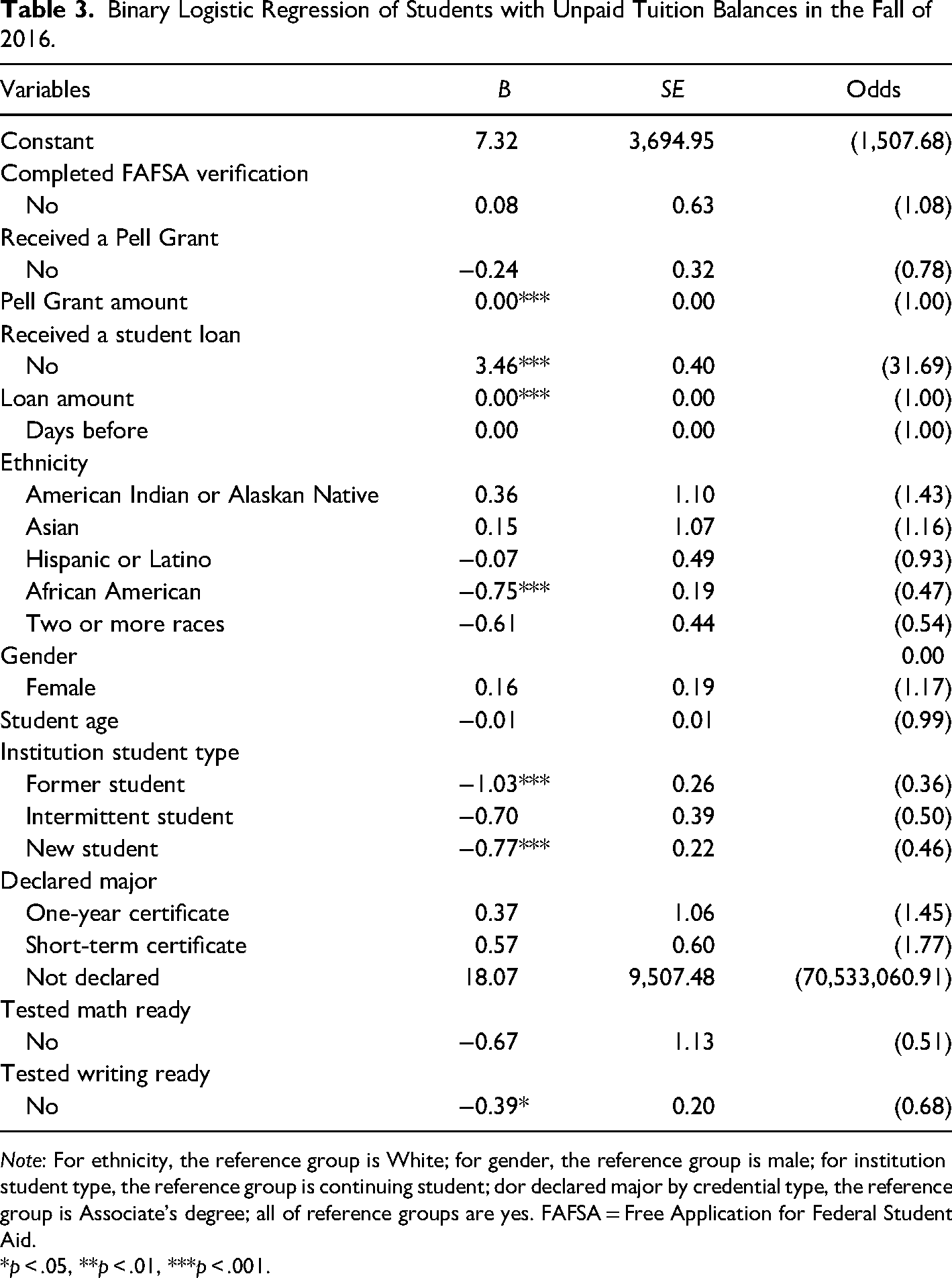

Table 3 contains the binary logistic regression model results examining the relationship between student, pre-college, and financial aid characteristics and unpaid tuition balances. From the first model, African American students were twice as likely not to graduate if they incurred unpaid tuition. However, White students were twice as likely to have an unpaid tuition balance when controlling for student demographic information, precollege enrollment characteristics, and FAFSA information. Students who did not complete the FAFSA verification process were 10% more likely to have delinquent tuition balances than those who did complete the verification process. Students who did not receive a Pell Grant were 20% less likely to have unpaid tuition balances than students who did receive a Pell Grant. Similar to the first model, the amount of Pell Grant did not change these odds. Students that did not receive a student loan were 31 times more likely to have unpaid tuition balances than students who received a student loan. Similar to the Pell Grant, the amount of student loans did not change these odds.

Binary Logistic Regression of Students with Unpaid Tuition Balances in the Fall of 2016.

Note: For ethnicity, the reference group is White; for gender, the reference group is male; for institution student type, the reference group is continuing student; dor declared major by credential type, the reference group is Associate’s degree; all of reference groups are yes. FAFSA = Free Application for Federal Student Aid.

*p < .05, **p < .01, ***p < .001.

Discussion

Although a more significant percentage of students with unpaid tuition balances initially completed the FASFA in higher numbers than expected, not completing the financial aid verification process was associated with decreased odds of graduating within 3 years and increased odds of ending the term with an unpaid balance. This finding is consistent with other research that suggests community college students are less likely to borrow student loans (Gladieux & Perna, 2005) and are less likely to complete the financial aid verification process relative to students in other higher education sectors, likely due to the racial, ethnic, and economic composition of the students who typically enroll at a community college (Davidson, 2015; Rios-Aguilar et al., 2018). Given Chen and DesJardins’s (2010) notion that lower socioeconomic students will be more price-sensitive based upon their overall reduction in costs due to financial aid, those students with the most significant economic need who are selected for financial aid verification are at higher risk for incurring an unpaid balance at the end of a term and are subsequently less likely to graduate with a postsecondary credential 3 years after their initial enrollment. Students who did not receive a Pell Grant were at higher odds of not graduating compared to their peers, suggesting that timely delivery of needed finances could help lower socioeconomic students meet their tuition obligations.

Consistent with Chen’s (2008) assertion that the type of financial awards will influence dropout behaviors differently among students from different economic and social backgrounds, students who did not receive a Pell Grant were less likely to graduate than their peers who did receive a Pell Grant, whereas those students who did not receive a student loan were more likely to graduate. This would suggest that students who receive gift-aid that reduces their education costs are more likely to persist and subsequently graduate. Several studies have noted the positive effect that gift-aid has on enrollment, persistence, and graduation through postsecondary education (Brock, 2010; Ison, 2020; Umbricht, 2016). However, those students who did not receive a Pell Grant were less likely to have an unpaid balance at the end of the term when compared to their peers who did receive a Pell Grant. This should not be interpreted to mean that increasing the number of Pell Grant recipients at a given community college will increase the number of students with unpaid tuition balances at the end of a given term. Rather, this would suggest that lower socioeconomic students are more prone to unpaid tuition balances, mainly when their needed financial aid is not applied to their accounts. More detailed research is needed to understand how lower socioeconomic status influences the ability to meet tuition obligations.

Implications for Research, Policy, and Practice

From a research perspective, more quantitative analysis is needed from different types of public, 2-year institutions to determine the prevalence of unpaid tuition for community college students. Additional research evaluating other years of initial enrollment is also needed to determine if the percentage of students with unpaid tuition balances in this analysis is consistent over multiple years. It could be the case that the 4.4% of students found with this analysis was an outlier and that the number of students with unpaid tuition balances at community colleges does not represent a significant threat to the fiscal health of the institution. However, given the magnitude of the diminished odds of graduation with an unpaid tuition balance found in this analysis, the need for community college administrators and policymakers to address unpaid tuition balances appears pressing, particularly in light of the continued growth of performance-based funding, which awards state appropriations based on student outcome measures and not mere enrollment. Students who incur an unpaid tuition early in their higher education career would yield little, if any, revenue to the institution through tuition payments. Those students with low academic performance yield little to any revenue to the institution through performance-based appropriations, suggesting that community colleges may expend a significant number of resources on students who yield no revenue back to the college. More research is needed to determine the academic performance of students with unpaid tuition balances. Besides additional quantitative analysis, qualitative research on students’ experience with unpaid tuition balances would provide critical information to policymakers and community college administrators who could influence both policy and practice around this issue.

From a policy perspective, community college administrators and congressional legislators need to ensure that the FAFSA and the verification process’s specific requirements are clear and consistent for students. Davidson (2015) noted that the U.S. Department of Education has simplified the initial FASFA process for students and their families but has not addressed the verification process. Further, Taylor’s (2019) analysis showed that institutional directions for completing the financial aid process are written at a level beyond most community college students. If institutions cannot simplify the directions for the verification process to a level that most students can understand, the U.S. Department of Education and congressional legislators should reduce the administrative burden of the verification process for institutions, possibly eliminating the process altogether. As Davidson (2015) noted, more than 50% of the information collected from financial aid verifications is not accurate and does not include the initial information that triggered the verification process in the first place. Instead of establishing a level of quality control as it was intended to do, the financial aid verification process has become another systematic barrier preventing lower socioeconomic students and students of color from achieving a postsecondary credential, as well as a catalyst for incurring a delinquent tuition balance that could harm their overall economic stability.

From an institutional perspective, community college administrators need to be mindful of how their in-term tuition reimbursement policies may be creating barriers to future enrollment, particularly for students of color and lower socioeconomic students. Community colleges are commonly understood to enroll a higher number of students whose economic and social circumstances are in greater flux than their peers at 4-year institutions. Students that are forced to withdraw in the middle of a semester are often required to pay back their Title IV awards, leaving an unpaid balance in their wake. Chen’s (2008) integration of liquidity constraints into understanding financial aid and student departure helps conceptualize why a student, even a student who succeeds academically, might feel compelled to make an economical choice that does not prioritize their outstanding tuition obligation. Students with limited financial means may be forced into higher work hours in the middle of a term. Institutions cannot survive financially if the tuition obligations of their students cannot be met. However, the decision to pursue higher education is not a commodity purchased at a single moment in time. Rather, it is a long series of decisions over time, with subsequent commitments to multiple terms of enrollment, which incur multiple tuition balances over multiple years. Emergency funds and scholarship dollars that can be strategically utilized to help students in crisis times could go a long way toward facilitating future enrollments, which is beneficial to both the student and the institution.

Although emergency funds and scholarship dollars can certainly improve persistence rates in the short term, situations will arise that will require students to step away from their institution in the middle of a semester or term. Community college administrators should be mindful of the tension between short-term financial losses that allow students to withdraw without outstanding tuition costs versus the potential long-term gain associated with future enrollments. Although the notion of allowing a student to leave the institution without a financial obligation seems counterintuitive to the culture of responsibility and autonomy that an institution of higher education hopes to instill in their students, institutions themselves should consider how their enrollment policies and procedures might be encouraging enrollment from students who have not completed the necessary financial aid processes that will secure their appropriate financial aid awards. Although every individual student is ultimately responsible for their enrollment into postsecondary education, students often assume that higher education institutions would not allow them to engage in an enrollment pattern that is detrimental to their success. Establishing stricter guidelines that require students to submit FAFSA information earlier in the enrollment cycle might lower overall enrollment in the short-term but could provide students with the necessary time to complete the needed enrollment steps that will make them successful in the long-run, allowing them to meet their tuition obligations.

Limitations

Several limitations with this study should be noted. First, Chen’s (2008) model recommends that studies of financial aid on student outcomes are better conducted with robust sample sets by including multiple institutions across various higher education sectors. Due to the exploratory nature of this analysis, including data from various institutions was not possible. Institutions report unpaid tuition balances to their respective state agencies at different points throughout the academic year and provide students with varying types of payment options for delinquent balances. To include a larger sample size of multiple institutions, more time would have been needed to ensure that students included in the sample experienced tuition holds at similar points throughout their academic trajectories and that institution’s reporting processes to state collection agencies were consistent. Thus, caution should be used when interpreting these results against other institutional considerations and practices. Second, several studies have noted that socioeconomic status significantly affects a student’s ability to matriculate to college (Klasik, 2012) and graduate with a credential (Snyder et al., 2019). Data were collected on those students who were eligible for a Pell Grant and were included in the analysis, but this information was only available for those students who submitted a FAFSA. Thus, socioeconomic data on the sample were limited. Access to additional databases, such as state tax records, might provide better insight into the students’ economic situation. However, these data were not available at the time of the analysis. A third limitation to this analysis is that students who enroll at a community college might do so without the intent to finishing a credential. Although students are required to select a major or program of study when they submit a FAFSA, institutional practice would suggest that many students choose a major to secure Title IV awards even when they do not intent to complete. To control for this, a variable on student status that Alpha Community College uses to capture those students who do not intend to complete a postsecondary credential was included in the analysis. However, it is likely that some students who never intended to complete a credential did so to capture Title IV awards and were included in the analysis with no means of control. Finally, this study utilized a cohort of students enrolled in the Fall of 2016 and evaluated graduation rates 3 years out. Research has noted that community college students often take over 3 years to graduate with a credential (Juszkiewics, 2017). Tracking the graduation rate of students beyond 3 years might yield different results.

Conclusion

This research attempts to illuminate a gap in the literature by analyzing the relationship between unpaid tuition balances and postsecondary credential obtainment for community college students and mapping the findings against the broader scholarship on student loan debt accumulation, student loan default, and overall consumer debt collection. Although larger economic considerations influence students’ ability to meet their tuition obligations, this analysis suggests that unpaid tuition balances at community colleges have an observable connection to a student’s ability to persist through graduation within 3 years. If it were the case that students had access to greater financial resources, and whose liquidity constraints were assuaged as Chen’s (2008) model suggests, students could repay these tuition balances with little or no concern. Thus, although tuition holds are mainly a secondary or mediating concern to the larger economic stratification at play, both institutional leaders and policymakers are required to administer higher education institutions within this larger economic context, developing policies and practices that support equitable access to and success within higher education. Given the stark, inequitable consequences of unpaid tuition balances on lower socioeconomic students and students of color, policymakers and institutional leaders must take heed of their enrollment and financial aid practices to ensure that students who enroll at a community college can persist from term to term and achieve their academic goals.

Although this initial analysis has yielded significant findings for community college leaders and student affairs practitioners, many questions remain regarding unpaid tuition balances of community college students and their consequences on students’ educational aspirations. How long does it take a student to repay a delinquent tuition balance? Are these balances collected through state agencies via a state tax withholding, or are these balances collected via a third-party vendor? Do students who incur these balances ever return to higher education once these delinquent balances are satisfied? Each of these questions requires more research and careful consideration of institutional practice surrounding financial aid and student success. Only by addressing gaps in service can institutions forge a more equitable future for the students they serve. Unpaid tuition balances should be included in future conversations surrounding financial aid, student success, and who ultimately gains access to American higher education.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.