Abstract

The teaching of financial literacy through game-based approaches is legitimized by the ability of game-based learning (GBL) to simulate financial decisions that young people have not yet encountered in their lives due to limited legal capacity and economic dependence on the parental home. Although results on the general effectiveness of games are already available, the question about for which students GBL is effective in teaching financial literacy has not yet been researched in depth. Based on pedagogical interest theory, a pre–post design (n = 50; 30 female students) was conducted to investigate the effects of high school students’ individual prerequisites on their game experience and their development of situational interest by playing an analog game and debriefing. The main findings indicate that a higher level of prior motivation for this topic has a positive effect on game experience and situational interest. A high level of prior knowledge and leisure activities concerning finance may have a somewhat negative effect. Such games are particularly suitable for students who are aware of the subjective significance of finance but have not previously had the opportunity to engage with this topic for different reasons.

Introduction

Teaching economic content and processes through games has a long history. One of the best-known games with this intention is Monopoly, which was originally developed to illustrate the negative effects of capitalism and is now considered one of the most popular board games (Donovan, 2017). The market for games to teach economics education is still growing. Especially regarding the promotion of financial literacy, according to our own count in 2020, there were more than 75 (serious) games. The goal of these games is to promote particular areas of financial literacy, including personal finance management, as in Celebrity Calamity; consumer education, as in Night of the Living Debt; and economic citizenship education, as in Chair the Fed. The implementation of games to promote financial literacy provides the opportunity to simulate economic decisions that young people have not yet encountered in their lives due to limited legal capacity and economic dependence on the parental home. These games allow students of lower socioeconomic status to simulate decisions they would not otherwise be confronted with (e.g., regarding financial investments).

Promoting financial literacy at a young age is important (Koh, 2016) for multiple reasons, including the growing personal responsibility for retirement planning and the increasing complexity of financial products (Aprea et al., 2016), a statistical correlation between socioeconomic background and financial literacy (Kaiser and Lutter, 2015) and a decrease in interest in economic topics (Kantar, 2019). Although financial literacy promotion has become an important policy in 59 countries of the Organization for Economic Co-operation and Development (OECD) (OECD, 2015), confusion remains regarding how to do so effectively (Kaiser and Menkhoff, 2020).

The introduction of economics classes is generally recommended in upper secondary education because all students can still be reached at this time. In addition, students are able to understand more complex heuristics and processes and begin to become increasingly economically independent (Pfändler, 2021; Walstad, 2001). One promising approach for students in secondary education is the use of game-based learning (GBL) as an experiential learning method (Amagir et al., 2017; Drever et al., 2015; Totenhagen et al., 2015).

The expectations for this learning method are high, justified by the ability of such games to simulate current and future financial decisions that students may have to make in various roles (e.g., consumer, employee, entrepreneur). Additionally, digital games continue to increase in popularity as students play for hours in their leisure time. For example, in the 16–29 age group, 75% of individuals regularly play computer games, regardless of gender (Tenzer, 2021). Researchers suggest that this motivation for playing games should also be adapted for learning (MacGee, 2007).

Research on this method is also increasing, especially in domains such as STEM (Mayer, 2019). However, the growth of published studies on the effectiveness of GBL is slower in the domain of financial literacy (Huizenga et al., 2019; Wilson et al., 2020).

There is evidence across domains that although GBL may offer advantages over other methods (Freitas, 2018; Wouters et al., 2013; Zhonggen, 2019), such advantages need to be interpreted with caution (Young et al., 2012). In regard to the promotion of financial literacy in general, students and their individual prerequisites influence the learning process (Fernandes et al., 2014); therefore, these prerequisites need to be considered when implementing any learning method. Consequently, a well-thought-out game and instructional design that are based on relevant prerequisites of the target group are needed. However, it is still unclear what this means, particularly for the use of GBL (Renninger and Hidi, 2016).

Against this background, this paper aims to investigate the influence of individual prerequisites on game experience and the development of situational interest as important learning goals of GBL (Krapp, 2005; Ryan and Deci, 2018). First, the theoretical background explains the interrelation of GBL and financial education (section ‘Game-Based Financial Education’). The role and function of financial interest as a driver of the long-term development of financial literacy is explained. In this regard, the main focus lies on the individual prerequisites that need to be considered when deciding upon a GBL approach. Three research questions are derived based on this background (section ‘Research Questions’). Based on a pre–post test design with three points of measurement (see section ‘Method’), these three questions are systematically analyzed (see section ‘Results’). Finally, the influences of individual prerequisites on financial interest within a GBL approach are discussed (section ‘Discussion’).

Game-Based Financial Education

Financial education, that is, the promotion of financial literacy, encompasses both informal socialization and formal learning opportunities. Family socialization currently exerts the greatest influence (Rudeloff, 2019; Shim et al., 2015). Formal learning opportunities may provide a way to compensate for the resulting inequalities. Financial literacy is a competency that requires lifelong learning as different demands are placed on individuals depending on their life stage and available resources (Drever et al., 2015). Early definitions described financial literacy as a combination of knowledge, attitudes, and behaviors that serve personal financial management (Moore, 2003). Beyond personal financial management, the definition has since been expanded to include consumer and economic literacy (Aprea, 2014). This broader approach is also reflected in a current OECD definition, which, following a definition of competence, also includes a society-wide perspective. According to this, financial literacy can be defined as knowledge and understanding of financial concepts and risks, as well as the skills and attitudes to apply such knowledge and understanding in order to make effective decisions across a range of financial contexts, to improve the financial well-being of individuals and society, and to enable participation in economic life (OECD, 2019: 13).

This definition includes not only knowledge but also a set of skills – including cognitive and affective aspects such as interest – that are necessary to empower young people in the financial domain (ibid.; Koh, 2016). Interest, as a predictor for learning and a learning goal itself, is considered important in knowledge acquisition and behavior change (Harackiewicz et al., 2016). In this respect, fostering an interest in the topic of finance can support engagement with the topic beyond institutional learning.

Reviews of the effectiveness of promoting financial literacy for students in secondary school point to the potential of experiential learning (Amagir et al., 2017; Drever et al. 2015; Totenhagen et al., 2015), which includes GBL (Ke, 2016). The rationale for this assumption is that adolescents are at an age of increasing freedom of choice with regard to dealing with finances. These decisions can be simulated by GBL in a risk-free environment (Drever et al., 2015).

Game-based learning in promoting financial literacy

GBL is an instructionally supported use of an educational (serious) or entertainment game and is considered to be a problem-based learning method. While entertainment games are designed with the goal of achieving engagement with the medium, the goal of serious games is to promote defined learning goals. These goals determine all design decisions (Mayer, 2014). Instructional support includes the selection and processing of information before, during, and after playing a game (Moreno and Mayer, 2005). It can be directly implemented in the game or by an instructor.

The game medium has a wide variety of forms (Salen and Zimmerman, 2010) and should be distinguished from gamification and plain simulation methods (Loh et al., 2015; Prensky, 2004). These are important elements but are not sufficient criteria to define a game. Accordingly, Mayer (2014) suggests that games must combine the following five elements to be considered a game: games are (1) rule-based, simulative systems that (2) react responsively to game decisions and (3) increase in complexity; they are also (4) challenging and (5) inviting to game players (Mayer, 2014). A subsequent reflection on affective and cognitive levels is also important because of the game's simulative and therefore limited representation of reality; moreover, such reflection is needed to promote learning transfer (Crookall, 2015; Taub et al., 2019).

The range of games for promoting financial literacy is highly diverse. There are games for almost all age groups: games that can be used for children as young as five and that teach the basics of money and saving in a playful way (e.g., Peter Pig's Money Counter; The Budget Game) and games that are intended to promote the avoidance of student loans and are aimed at prospective college students (e.g., inTuition). Furthermore, games differ according to their medium, with most being digital games. Occasionally, games are offered in digital (e.g., Chair the Fed) as well as analog form (e.g., Cashflow 101). Most of these games have not yet been empirically tested for their effectiveness. Exceptions include Chair the Fed (Wilson et al., 2020), No Credit. Game Over! (Huizenga et al., 2019) and Money Hero (Nadolny et al., 2019). An assessment of dependent variables has been performed by using postgame subject tests (Nadolny et al., 2019; Wilson et al., 2020) and by analyzing game data (Huizenga et al., 2019; Nadolny et al., 2019). However, studies have not yet investigated for which target group these games are particularly suitable.

Evidence for GBL in financial education

For a learning medium to be developed and implemented in a way that promotes learning, it is important to consider learners’ individual prerequisites for the content and learning methods (MacGee, 2007; Qian and Clark, 2016). These prerequisites should be considered in design decisions and the subsequent verification of their effectiveness. For example, attitudes toward entertainment games are assumed not to apply automatically to serious games (Boyle et al., 2016; Riemer and Schrader, 2015).

However, the extent to which GBL can be used effectively to promote financial literacy has not been empirically tested. The few studies conducted to date in this domain confirm an advantage of GBL over traditional learning methods in terms of an increase in financial knowledge (Duzhak et al., 2021; Huang and Hsu, 2011; Wilson et al., 2020). This is also evident across domains, especially in mathematics and language learning (Wouters et al., 2013). Regarding the motivational advantage that is primarily associated with this method (Riemer and Schrader, 2015), no consistent results have been found for economics education in general (Khan and Pearce, 2015; Nadolny et al., 2019; Rogmans and Abaza, 2019) or financial education in particular (Nadolny et al., 2019).

Although previous studies of GBL in financial education have not examined which individual prerequisites influence financial literacy, studies of economics education in general have offered preliminary evidence, based on which two main results can be derived according to gender and prior achievement concerning knowledge acquisition. First, the influence of gender is controversial. For example, there is evidence that gender exerts no influence on play behavior in economics education (Dobrescu et al., 2015; Lin, 2018) but that gender can partially explain the variance in learning outcomes through GBL (Duzhak et al., 2021). Second, prior achievement, such as grade point average (GPA) (ibid.; Lin, 2018) and subject motivation, are positive influencing factors on knowledge acquisition (Lin, 2018) and engagement (Rogmans and Abaza, 2019) during play. Finally, lower-performing students seem to benefit from GBL approaches in regard to learning (Yin, 2020).

Currently, few results are available for the influence of individual prerequisites on GBL. This influence relates not only to knowledge development but also to the promotion of motivation. Therefore, a theory-driven examination of for whom GBL is suitable should be conducted. Interest is considered to be a motivational disposition that is content-specific as well as a predictor and important goal of learning (Hidi and Harackiewicz, 2000). Interest consists of cognitive as well as noncognitive aspects, which are also related to financial knowledge (Förster and Happ, 2019).

Interest development via GBL

Following the person-object theory of interest (POI) by Krapp (2005), interest consists of the two components of affective activation and value-related valence, which is defined as subjective meaningfulness. Interest can be a psychological state that can be triggered or an individual trait called individual interest (Renninger and Hidi, 2019). Based on different theoretical conceptions of interest, four phases can be assumed, in each of which affective activation and value-related valence are relevant to different degrees (Hidi and Renninger, 2006).

Situational interest as a state is differentiated into triggered and maintained situational interest (ibid.). In triggered situational interest, affective activation – either positive or negative – is central and can be deepened by appropriate tasks (ibid.). Thus, games, exposure to technologies, or group work may prove beneficial (Mitchell, 1993; Swarat et al., 2012). For example, a funny picture is sufficient to trigger situational interest, but maintaining interest throughout a whole lesson requires an additional subjectively meaningful component: value-related valence (Prenzel et al., 2001). Situational interest as a state can be followed by a trait, namely, emerging and well-developed individual interest (Hidi and Renninger, 2006), with the last stage being primarily achieved through individual drive and predominantly characterized by positive emotions, high value, and in-depth expertise (Renninger and Hidi, 2019).

If interest develops, then people deal with a topic (1) frequently, (2) voluntarily, (3) in greater depth, (4) with increasing knowledge, and (5) independently (Renninger and Hidi, 2016). If one or more of these behaviors can be measured, then increasing interest development can be assumed. In this context, developed individual interest as a trait is considered to be changeable only in the long term. For shorter periods of time, change might be possible through repeated engagement – one-time interventions thus lead to changes mainly in the area of situational interest (ibid.). Promoting such changes is important because situational interest can lead to deeper learning and higher engagement (Renninger and Hidi, 2019), and it is a prerequisite for the development of individual interest (Hidi and Renninger, 2006). Moreover, interest can predict inter- and intrapersonal domain-specific performance (Harackiewicz et al., 2016).

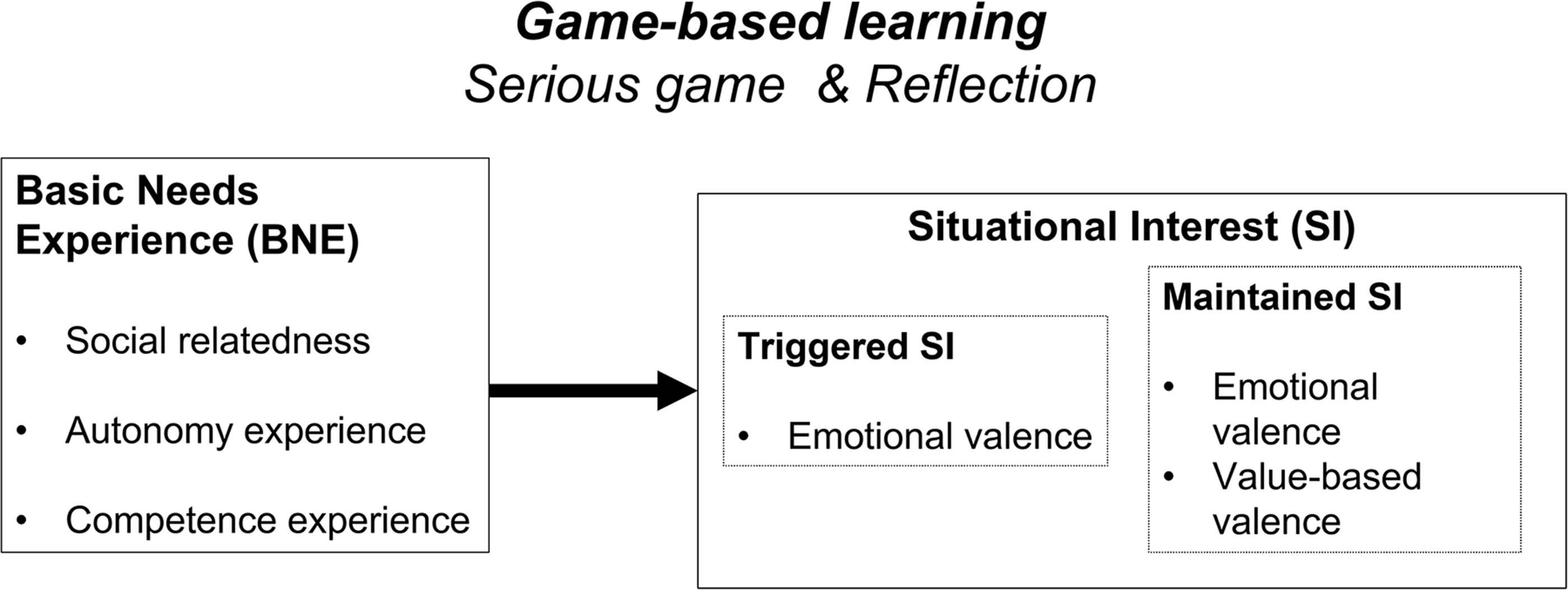

The extent to which interest develops, in turn, depends on predictors and facilitation by the learning environment (Renninger and Hidi, 2016). According to Krapp (2005), an increase in situational interest can be achieved by a targeted promotion of the basic needs experience (BNE) (see also Krapp and Ryan, 2002). Krapp (2005) links Deci and Ryan's self-determination theory (SDT) (Deci and Ryan, 1990) with the POI (Prenzel, 1986). SDT, according to Deci and Ryan (1990), assumes that intrinsic motivation can develop when three so-called basic psychological needs are met in a (learning) situation. Supporting the psychological needs of competence, autonomy and social relatedness during learning will, in turn, promote interest in the subject being taught (Krapp, 2005).

Several studies have empirically confirmed the link between BNE and interest development (Großmann and Wilde, 2018; Minnaert et al., 2011; Tsai et al., 2008). In addition, an implicit link between basic psychological needs and interest development can be asserted. In this case, interest development can be measured when freedom of choice, social inclusion or social support is emphasized (Flowerday et al., 2004; Renninger and Hidi, 2019). BNE can be provided while playing a game for learning or entertainment purposes and might explain the appeal of such play (Przybylski et al., 2010). The responsiveness of GBL offers many opportunities for competence feedback, and freedom of choice – for example, through personalizations – can support autonomy experience, while relatedness is supported by players perceiving themselves as a relevant part of a game world (Ryan and Rigby, 2019). BNE can also be supported by the frequent use of a BNE-based questionnaire for the evaluation of game design (ibid.). Thus, it is assumed that a well-designed game can promote BNE. The existing framework should, in turn, promote the development of situational interest through game-based content (see Figure 1).

Development of SI through BNE via GBL (according to Krapp and Ryan, 2002).

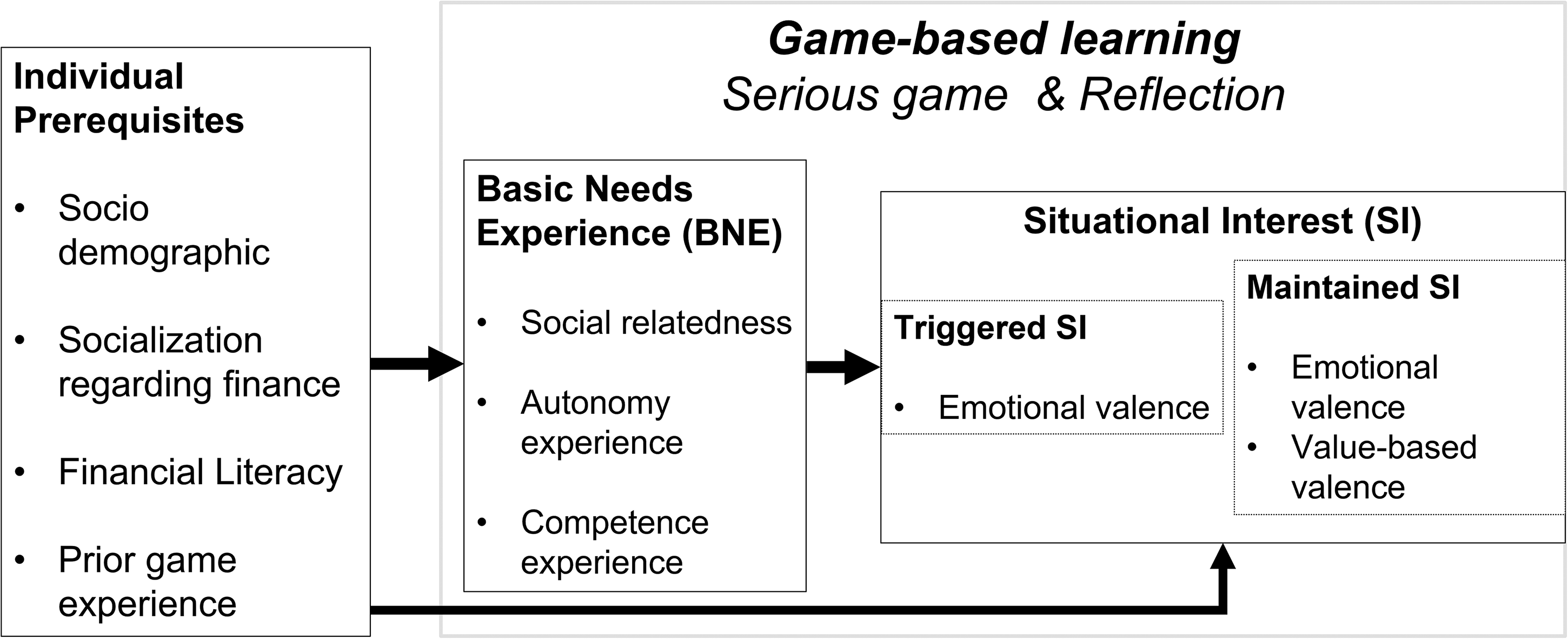

In addition to an adequately structured learning environment that supports BNE, individual prerequisites of interest development in general need to be considered. These include age, gender, prior interest, family background on a topic, motivational variables such as self-efficacy, and the opportunity that a person has to engage with a topic (Ainley, 2017; Renninger and Hidi, 2019).

Interest in financial topics

According to the current state of research, these general findings on the determinants of interest development and its influence can also be applied to the area of financial literacy. Regarding interest in financial matters, the findings suggest that male students have a greater interest in the topic of finance than female students (Förster and Happ, 2019). Additionally, interest is positively correlated with content-specific knowledge (Förster et al., 2017); therefore, when it is controlled for, interest might be a better predictor of knowledge development in the area of finance than gender (Förster and Happ, 2019). Moreover, for females, interest and knowledge also seem to be particularly relevant for dealing with economic issues in their education (Jüttler and Schumann, 2019). New findings support this result: In one case, active engagement with the topic of finance – as an indicator of individual interest (Renninger and Hidi, 2016) – was found to lead to an improvement in knowledge (Förster et al., 2019). The individual's ability to interact with the issue (Ainley, 2017), such as by having a bank account, was also found to be conducive to further engagement (Förster et al., 2019). Unlike engagement, for example, by watching videos, early ownership of a bank account depends less on voluntary effort than on financial socialization (Shim et al. 2015).

In her study, Rudeloff (2019) showed that economic interest was positively correlated with the cognitive aspect of financial literacy, which was also true for parental influence. It has also been repeatedly confirmed that socioeconomic background is correlated with the cognitive facet of financial literacy (Förster et al., 2018).

These studies provide evidence that in addition to contextual factors (e.g., type of school), family background, prior knowledge, individual interest, and gender, both across domains and in the case of finance, are important individual prerequisites for the development of domain-specific interest

Against this outlined background, Figure 2 integrates the mentioned predictors, which represent crucial individual variables. These variables are differentiated into categories concerning financial literacy and the GBL method. BNE, in this case, is considered a goal of GBL. Moreover, it can be assumed that the development of situational interest is influenced by BNE.

Working model of the influence of individual prerequisites of game experience and situational interest in GBL.

Research Questions

There is evidence that experiential learning can be effective in promoting financial literacy for students in secondary education (Amagir et al., 2017; Drever et al. 2015) and that interest can be fostered through problem-based methods (Harackiewicz et al., 2016). However, there is little research related to ways that interest can be promoted through GBL in any domain (Renninger and Hidi, 2016). Furthermore, there are few studies on the use of GBL to promote interest in economic topics (Ellahi et al., 2017) or in financial matters (Huizenga et al., 2019).

Therefore, we investigate which prerequisites are important in the context of GBL to foster the development of interest in financial matters. This study should clarify for whom GBL is more effective and which individual prerequisites need to be considered in instructional design (see Figure 2). To reach this aim, the effects of students’ prerequisites are analyzed at two separate stages of GBL: (1) during the game and (2) during reflection after the game as an important part of instructional support. This approach helps illuminate which prerequisites are important at which stage of GBL.

This goal raises the following research questions:

How do individual student prerequisites influence students’ game experience (BNE) in a serious financial game? How do individual student prerequisites influence students’ situational interest while playing under the control of their game experience (BNE)? How do individual student prerequisites influence students’ situational interest during reflection under the control of their game experience (BNE)?

Method

To answer these questions, the analog board game “Moonshot” has been developed and used in upper secondary classes (see section ‘Sample’). The development included a two-year iterative piloting process involving experts from various disciplines (including game development, science, and teachers). One game can be played by 4–5 students.To achieve an individual chosen game goal called “life dream” (e.g., a successful influencer or sports career, the implementation of an environmental protection project), players must make financial decisions under changing economic conditions. These decisions include purchasing insurance, taking out loans, investments and budgeting (for further details, see Platz et al., 2021). When making financial decisions, players must also prioritize them in consideration of other resources to reach their game goal, such as time, education, and family. Through changing economic conditions such as adjusted interest rate targets and economic policy decisions during the course of the game, the game also integrates the economic citizenship dimension of financial literacy. Subsequent to the game, players are given reflection prompts to identify successful game strategies. These strategies and the simulation are then compared to the real (financial) world. The teacher then leads a discussion on the consequences corresponding to financial decisions on different levels of society. Finally, students are given the opportunity to break down their own life goal into phases and create a budget to achieve it.

Design

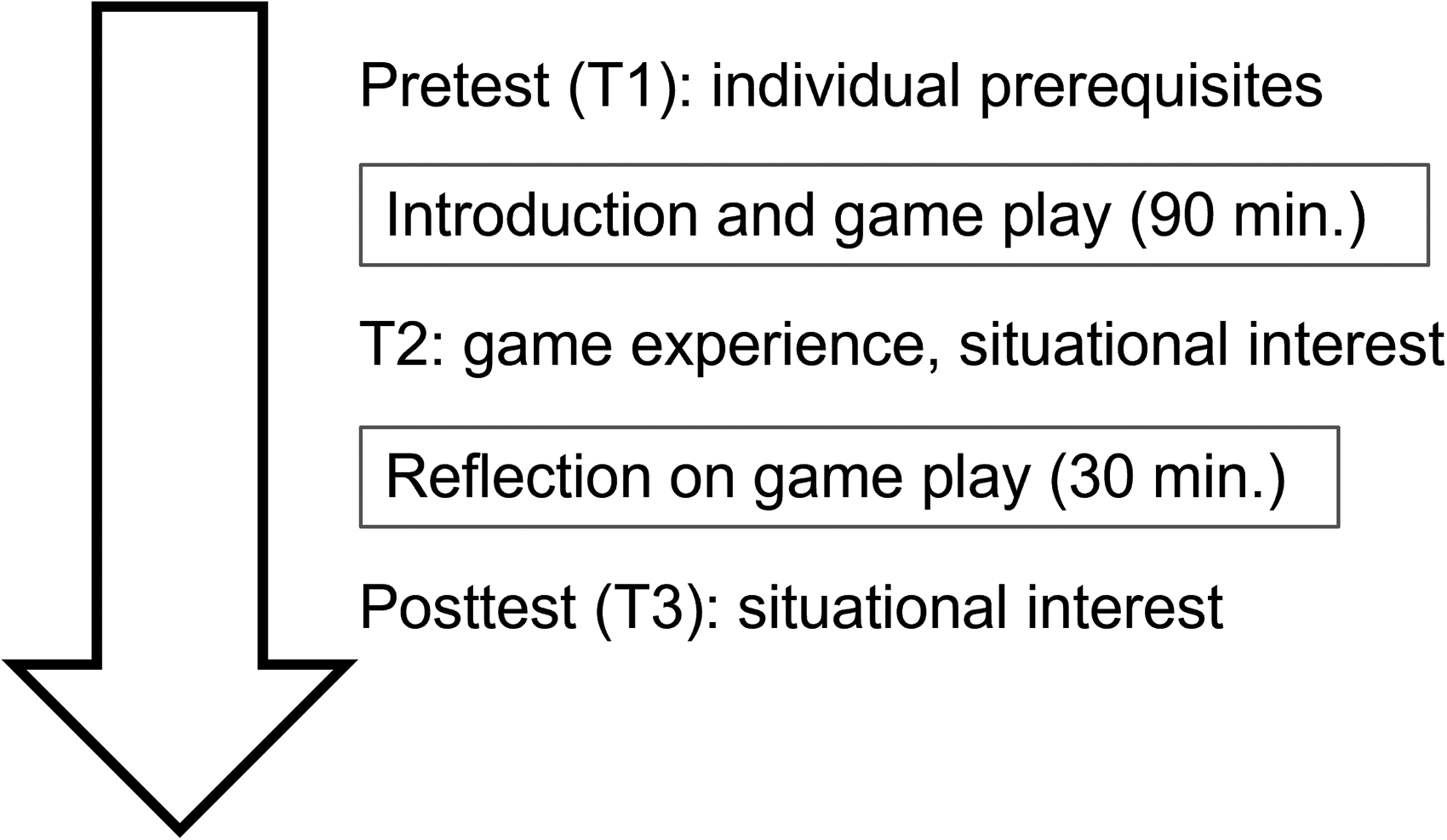

The present study followed a pre–posttest design with three measurement time points (T1, T2, and T3) at two high schools in Germany (Baden-Wuerttemberg). The study was conducted in the summer of 2019 at the end of the school year and lasted 180 min in total (Figure 3). All students were recruited after official approval by the school administration. The students were given written consent forms, which were completed by students of legal age themselves or, in the case of minors, by their parents and were then collected. The subjects were students in the upper grades of two high schools (grades 12 and 13). At T1, a preliminary survey was conducted in which financial knowledge, financial motivation, previous gaming experiences, financial socialization at home, engagement with money, finance in everyday life, and sociobiographical data (age, gender, etc.) were assessed. The questionnaire lasted 45 min in total.

Study process.

Sample

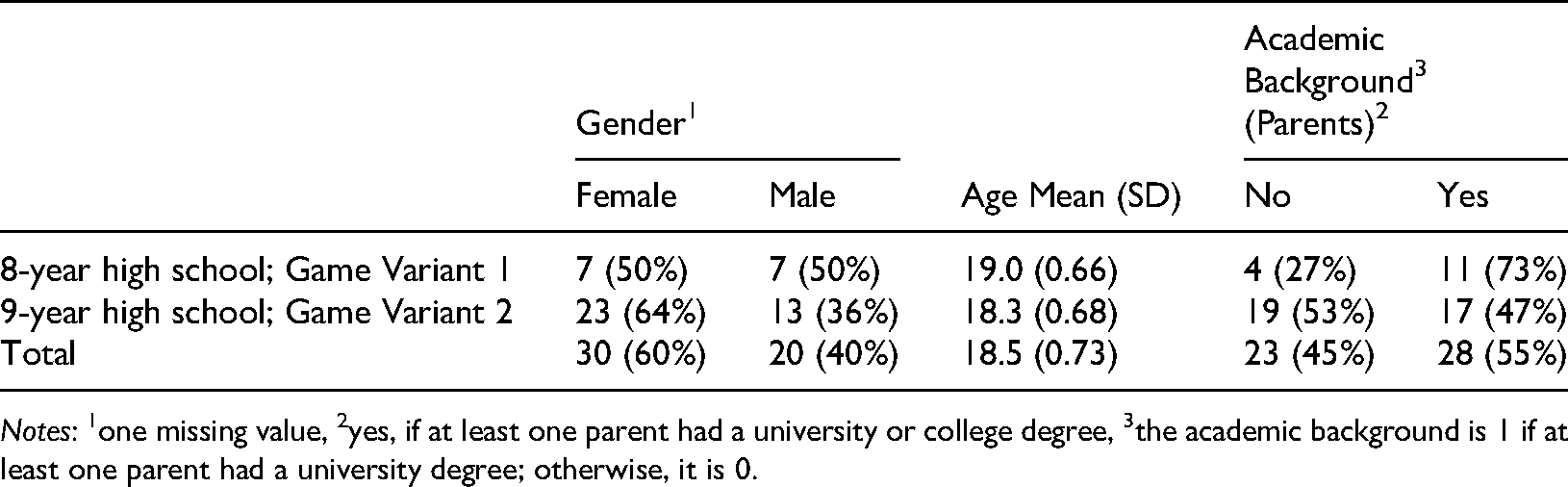

Table 1 represents the study sample. The students were enrolled in two high schools in Germany. The only relevant difference between the two schools was in the number of years (8 vs. 9) that students had to complete before graduation. Since all students were in the same grade, the students from the 8-year high school were younger than the students from the 9-year high school.

Sample.

Notes: 1one missing value, 2yes, if at least one parent had a university or college degree, 3the academic background is 1 if at least one parent had a university degree; otherwise, it is 0.

Instrument

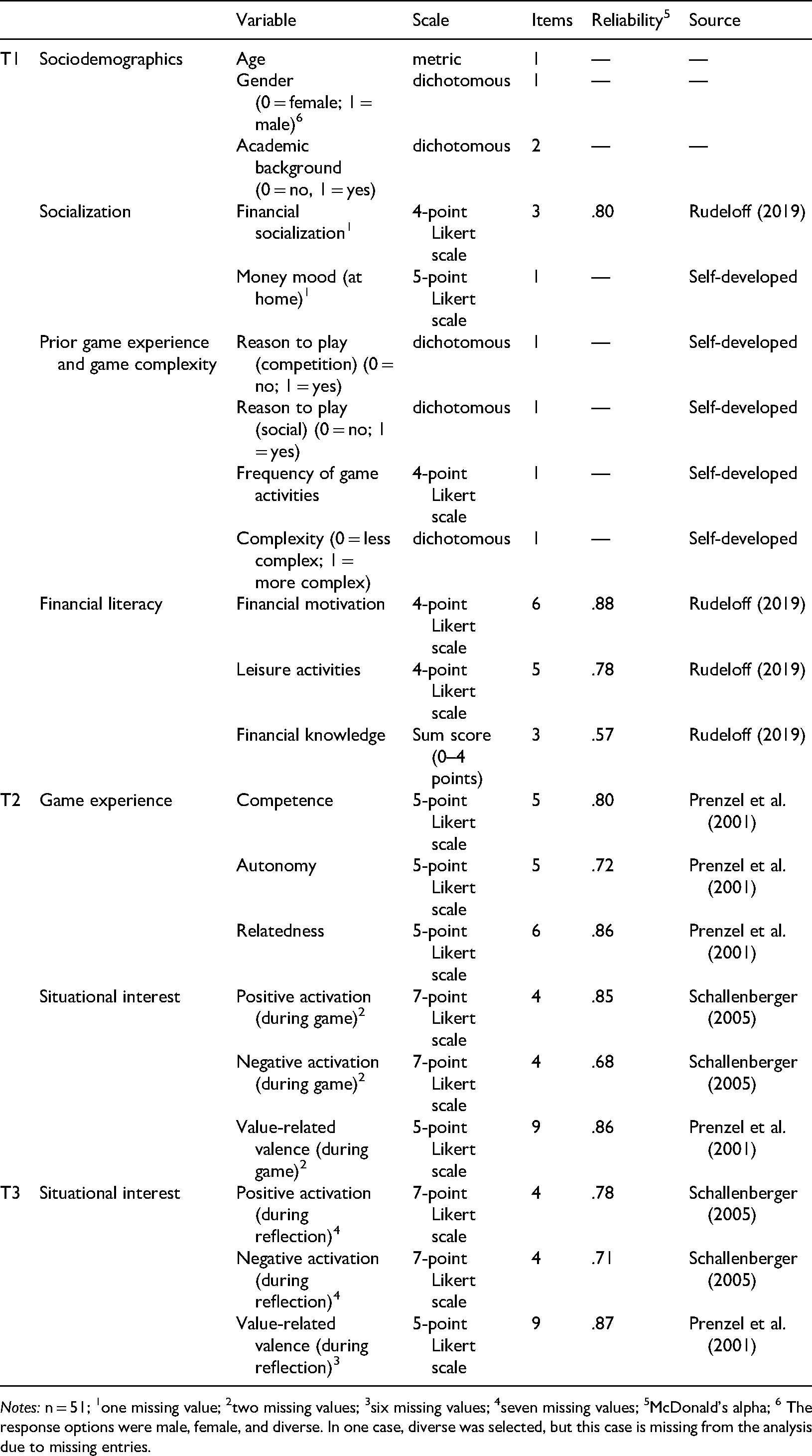

Online questionnaires were used to measure students’ individual prerequisites (T1), gaming experience (T2) and situational interest (T2, T3) during the games and reflection (using SoSciSurvey 1 ). In addition to gender, age, parental academic background and students’ financial socialization, prerequisites comprise experience with and motivational dispositions toward both the game medium and the finance content. To examine the influence of the students’ own gaming experience and motivation, in addition to gaming frequency, self-developed scales were used to determine whether students tended to play for cooperative or competitive reasons in their free time. Individual financial interest in conjunction with key indicators, such as voluntary engagement with the subject, was also considered (Renninger and Hidi, 2016).

Game experience (T2) was assessed by a scale that captured BNE and situational interest (positive activation, negative activation and value-related valence). Situational interest was also measured during reflection (T3). Established scales were used and adapted to the game. The questionnaire was reviewed by a school class before use and checked for possible inconsistencies and misinterpretations through the thinking-out-loud approach. In this process, corresponding terms were adapted from older scales. Table 2 provides an overview of the test instrument separated by the three points of measurement.

Overview of the test instrument.

Notes: n = 51; 1one missing value; 2two missing values; 3six missing values; 4seven missing values; 5McDonald's alpha; 6 The response options were male, female, and diverse. In one case, diverse was selected, but this case is missing from the analysis due to missing entries.

Game complexity: The game is available in two versions that differ in their degree of complexity. In version 1, only financial decisions between different alternatives must be made, whereas in version 2, the students must also consider limited time resources. In version 2, the students are therefore much more limited, and decisions must be weighed more carefully. These differences serve to test the extent to which different game mechanics affect the game experience, especially the experience of competence and autonomy.

Socialization: Socialization was measured by two variables in this study. Money mood described the atmosphere at home when financial topics were discussed (item (translated): “When the subject of money is raised at home, the mood is usually…” (tense vs. relaxed, with higher values indicating a more relaxed atmosphere). Financial socialization was measured based on three items concerning the extent to which parents talked to their children about finances and involved them in financial topics at home (example item (translated): “My parents tell me how the family is doing financially”). In addition, the ownership of a bank account was recorded. However, since all students stated that they already had their own bank account, this data was not included in the analysis.

Prior game experience: This part concerned previous game experience. The students were asked about the main reasons why they played games (competitive vs. social). In addition, gaming frequency (ranging from 4 = several times a week to 1 = yearly) represented another important variable to measure engagement with games, which can be compared to this type of game.

Financial literacy: To measure financial literacy, a short knowledge test was used consisting of four single-choice items (example item (translated): “When do we speak of inflation?”) that were selected, based on their difficulty, from a validated financial literacy test by Rudeloff (2019). In addition to students’ financial knowledge, financial motivation (trait) was measured before playing. Again, a questionnaire from Rudeloff (2019) was used (example item (translated): “When I’m dealing with issues around finances, I try to avoid them”). Leisure activities regarding finance were measured by five items that assessed how engaged students were with money and financial information in their leisure time (example item (translated): “In my leisure time, I voluntarily listen to radio programs/podcasts on the subject of finance”).

Basic needs and situational interest: BNE was measured after the game (T2) based on the three dimensions of competence and autonomy experience as well as relatedness. To measure these dimensions, a questionnaire by Prenzel et al. (2001) was adapted and the language was updated by discussing the items with students. All items were also adapted to the learning medium game (example items: competence experience (translated): “While playing, I had sufficient opportunity to try out my own game strategies”; autonomy experience (translated): “While playing, I was encouraged to do things on my own”; relatedness (translated): “I received support in case of difficulties”). Students’ situational interest was measured both after the game and after reflection. The positive activation (example item (translated): “How did you feel while playing the game?” (bored vs. excited) and negative activation (example item (translated): “How did you feel while playing?” (relaxed vs. stressed)) items were based on Schallenberger (2005), and the item on value-related valence (example item (translated): “While playing, I was put in situations where I could realize for myself how important the issues were”) was adapted from Prenzel et al. (2001).

Analysis

In addition to descriptive and bivariate comparisons, linear regression models were calculated with the software program Mplus (Muthén and Muthén, 2018). Based on this software, a maximum likelihood (ML) estimation was used for standardized regression estimates. For financial knowledge, the sum score of the knowledge test was used. All variables represented manifest estimators following classic test theory with satisfactory to good reliability, with the exception of financial knowledge (see Table 2). Game experience during the game (basic needs and situational interest; T2) and during the reflection phase (situational interest; T3) were modeled as dependent variables. Financial socialization, financial literacy (interest and knowledge), sociodemographic variables (gender, age and academic background) and prior game experience were independent variables. Due to the small sample size and the somewhat short interval between T2 and T3, instead of one mediation model, two separate models were calculated that considered BNE as a control variable. This approach has the advantage of interpreting the effects of students’ prerequisites on situational interest independent of their game experience. The limitations of this analytical strategy (including the relatively low reliability of the knowledge test) are discussed in section ‘Limitations’.

There were only a few missing values, ranging from 2% to 13% in total. However, these values were missing completely at random (MCAR). Therefore, cases with missing values on the observed variables were deleted from the corresponding analyses (listwise deletion).

Results

Descriptive and bivariate interrelations

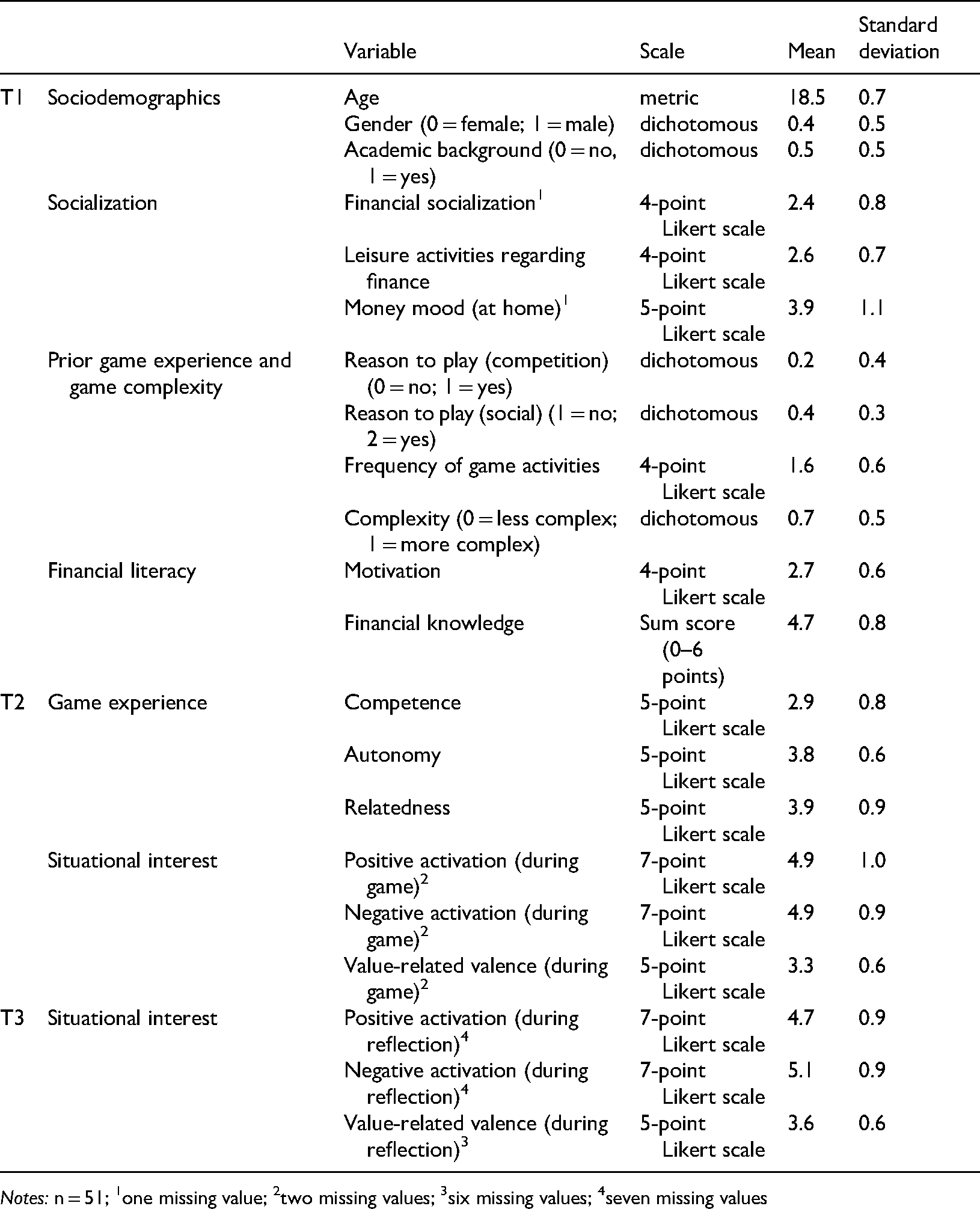

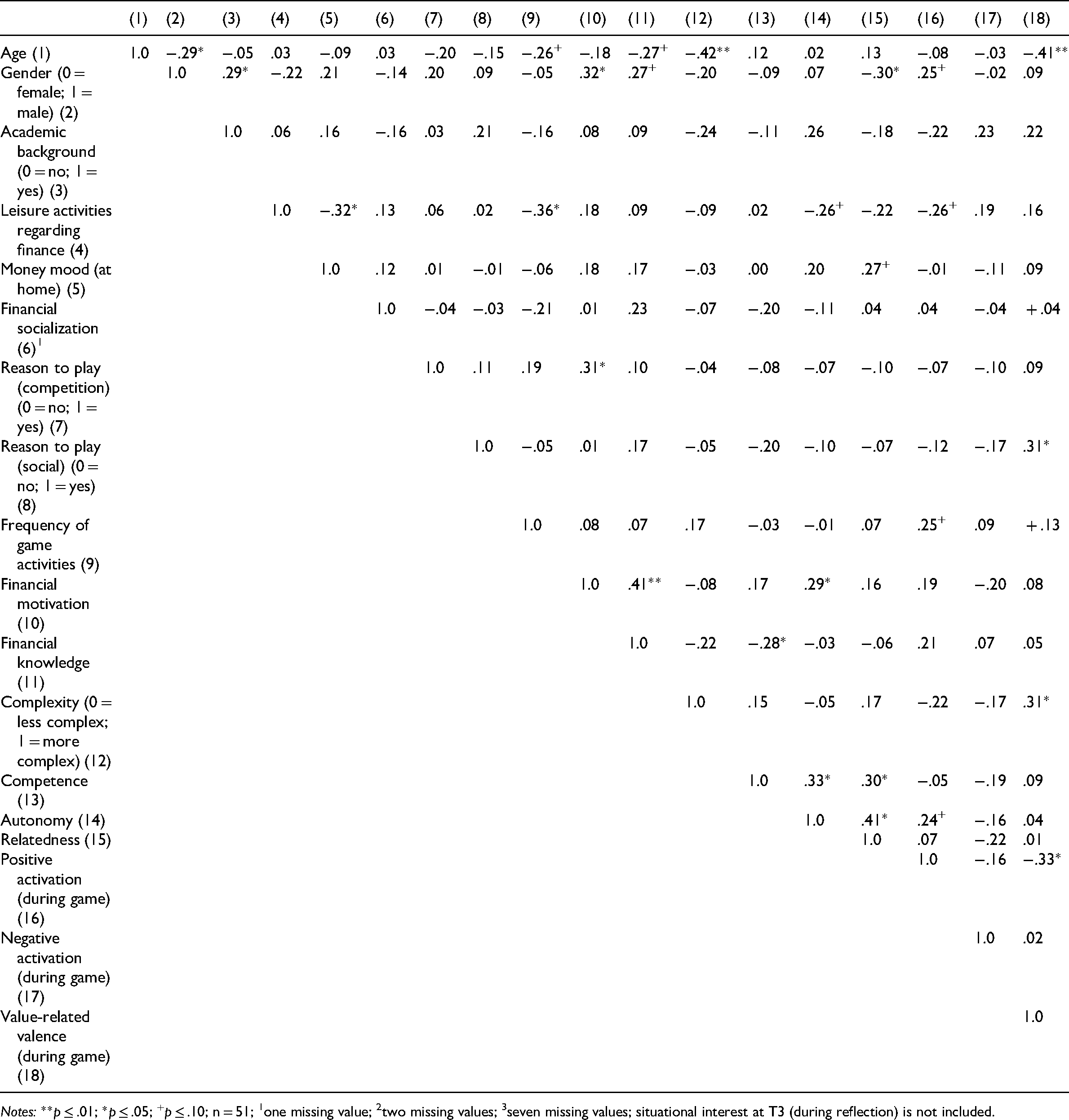

Table 3 provides an overview of the means and standard deviations of the students’ variables considered in the empirical analyses, including their interest and knowledge before playing. In this regard, notably, students tend to have high expressions in the various variables with relatively low variances. However, the values can be considered moderate (no obvious ceiling effects). Table 4 shows the bivariate correlations between the different variables. No noticeable interdependencies were found between the independent variables. One exception is basic needs, which are in line with moderate correlations in SDT (Deci et al., 2013).

Descriptive statistics.

Notes: n = 51; 1one missing value; 2two missing values; 3six missing values; 4seven missing values

Overview of bivariate correlations.

Notes: **p ≤ .01; *p ≤ .05; +p ≤ .10; n = 51; 1one missing value; 2two missing values; 3seven missing values; situational interest at T3 (during reflection) is not included.

Prediction of game experience and situational interest

Tables 5–7 show the results regarding the three research questions. To consider possible multicollinearity issues based on bivariate correlations of independent variables (see Table 4), variance inflation factors (VIFs) were calculated. These were between 1.13 and 1.83, indicating no multicollinearity.

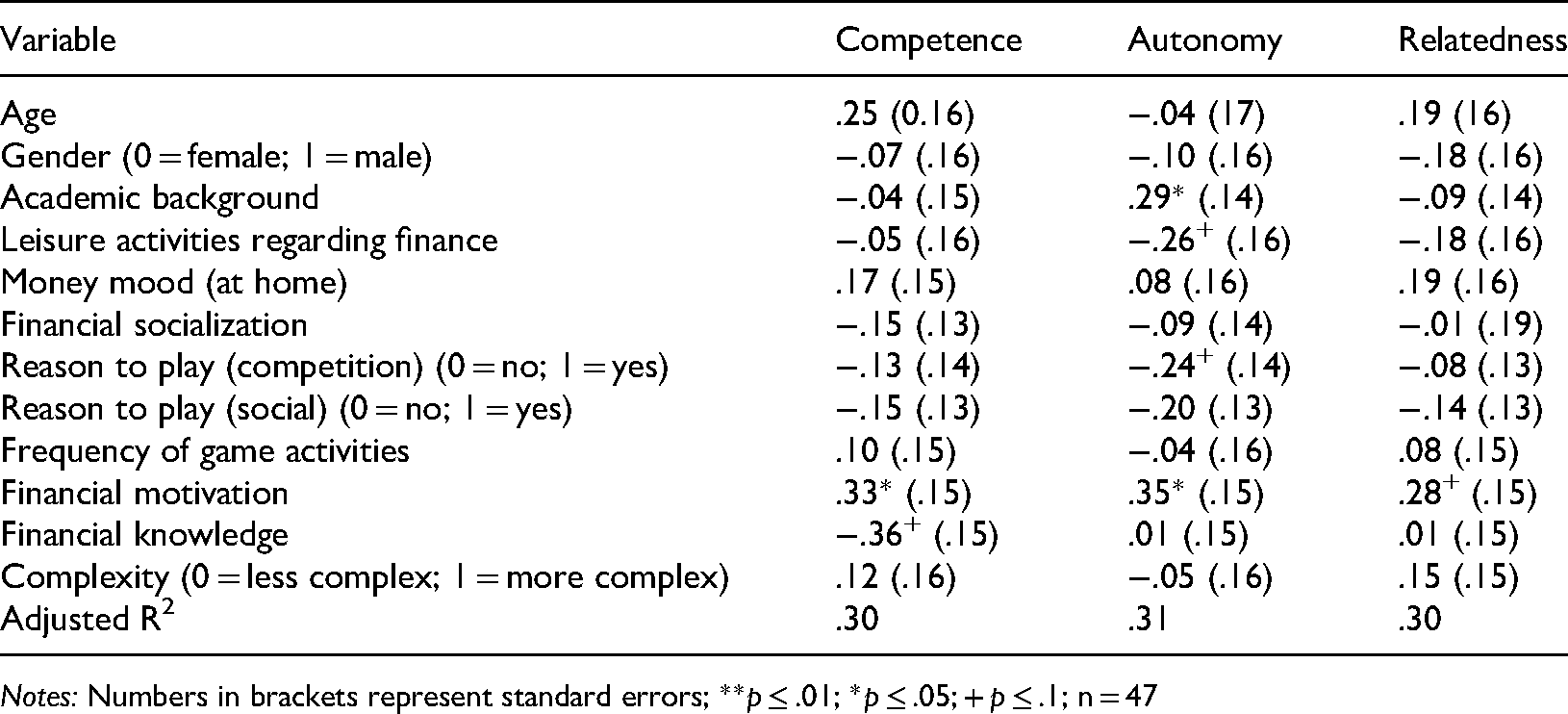

Explanation of students’ BNE during the game.

Notes: Numbers in brackets represent standard errors; **p ≤ .01; *p ≤ .05; + p ≤ .1; n = 47

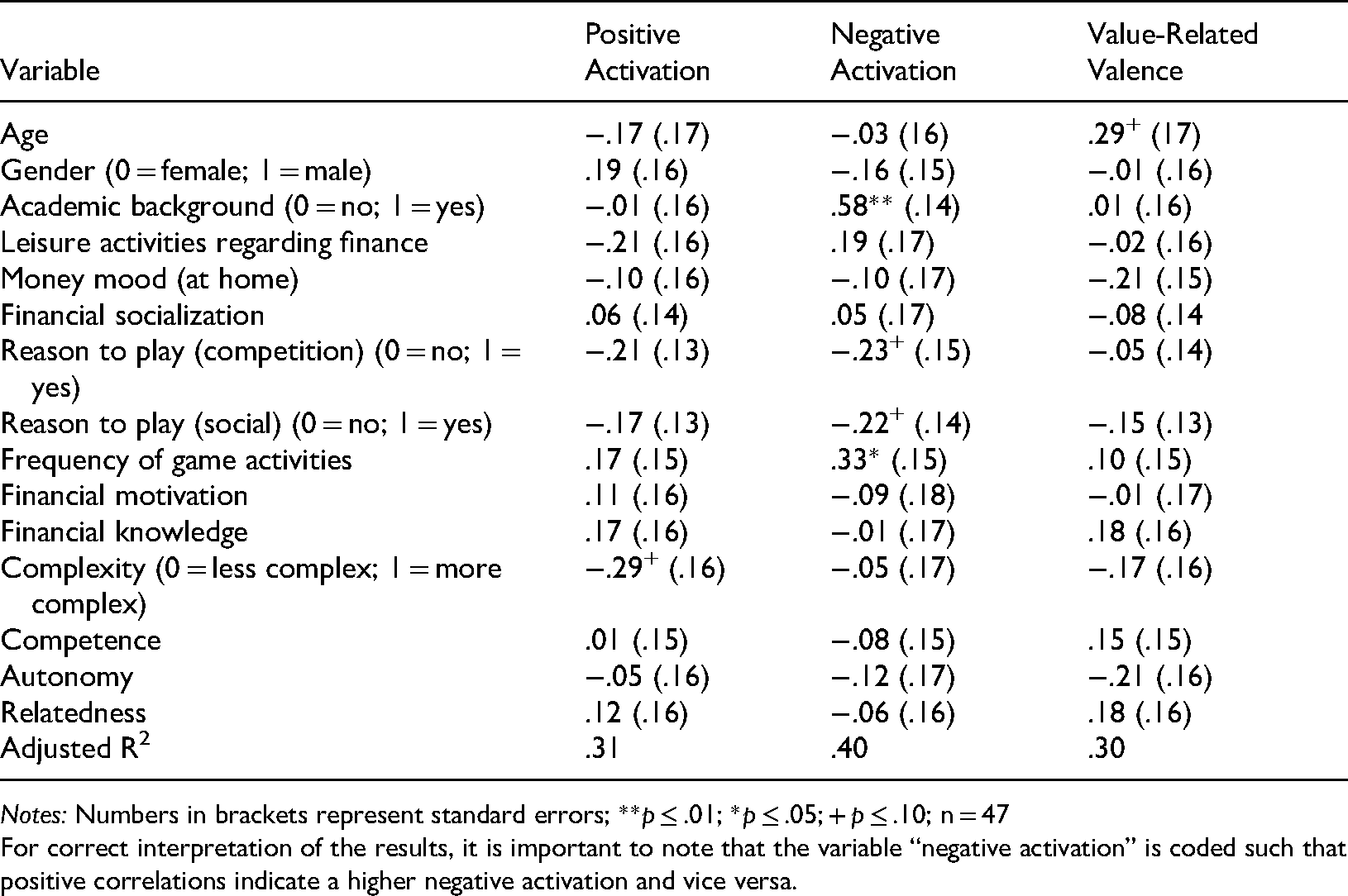

Explanation of situational interest during the game.

Notes: Numbers in brackets represent standard errors; **p ≤ .01; *p ≤ .05; + p ≤ .10; n = 47

For correct interpretation of the results, it is important to note that the variable “negative activation” is coded such that positive correlations indicate a higher negative activation and vice versa.

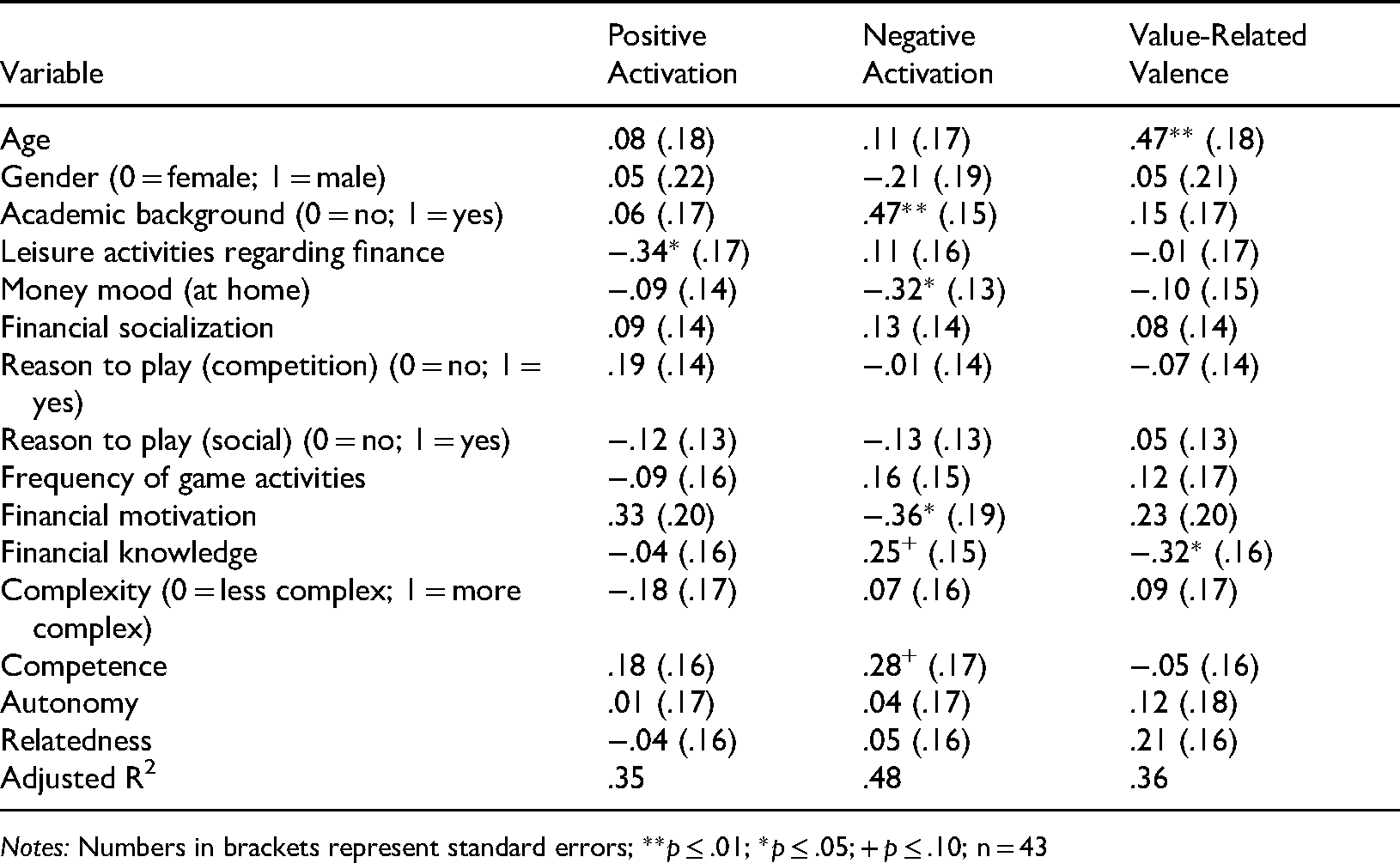

Explanation of situational interest during reflection.

Notes: Numbers in brackets represent standard errors; **p ≤ .01; *p ≤ .05; + p ≤ .10; n = 43

When considering the explanation of students’ BNE during the game (first research question), it becomes obvious that both financial motivation and financial knowledge play the most significant role – in addition to financial socialization. Regarding this finding, it is remarkable that financial motivation and financial knowledge show contrary effects: Although motivation has a positive effect on all basic needs, financial knowledge only has a negative effect on competence. In addition, there is a negative effect of leisure activities and academic background on autonomy. This result means that students who are more concerned with finances and money in their free time feel less autonomous and involved in the game. Finally, there is a small effect of students’ prior game experience, suggesting that students who are more likely to play for competitive reasons perceive themselves as less autonomous when playing. Furthermore, a positive correlation exists between academic background and the experience of autonomy. The explained variance of all three dependent variables lies between 30 and 50 percent.

Regarding the second and third research questions, Tables 6 and 7 present the effects of prior experiences, socialization and financial literacy on students’ situational interest during the game and reflection, controlling for BNE. In general, the situational effects of BNE are somewhat small or nonexistent, with the only exception being negative activation during reflection, where there is a negative effect of autonomy. In addition to BNE, leisure activities regarding finance show a tendency to have negative effects, especially on positive activation during reflection. Again, for situational interest, financial motivation and financial knowledge show contradictory effects in the same way as seen for BNE. In addition, students who played version 1 of the game show higher positive activation during the game and during reflection. Finally, there is a relatively strong effect of age on value-related valence during reflection, which shows that older students score higher on value-related valence than younger students. Players’ academic background also correlates negatively with negative activation during play and reflection. This result means that the GBL method tends to promote negative emotional activation in students with an educational background. As before, both models show high explained variances considering the small number of included variables.

Discussion

Summary

This paper addresses the question, for which students GBL is effective in teaching financial literacy. Based on three multiple regression models, the results provide indications of how students’ individual prerequisites affect the gaming experience (see Table 5). The results suggest that financial literacy, that is, professional competence, can best explain BNE during play. That is, if students are already more involved in financial topics at home, such involvement tends to have a negative effect on their game experience in a serious financial game – especially on autonomy experience. Similar results exist for financial knowledge, which has a negative effect on competence experience. In contrast, higher financial motivation has a positive effect on the gaming experience, and students with an academic background feel more autonomous. Motivation is the most important predictor of BNE, which is consistent with previous results (Ryan and Rigby, 2019). Thus, GBL is particularly effective for those who are motivated (or interested) but have little experience and prior knowledge in this domain. In contrast, students with more prior knowledge may feel underchallenged.

Considering the effects on situational interest during games and especially during reflection, prior financial motivation and knowledge again show strong but contrary effects. This result supports the conclusion that GBL is suitable for students who already have a basic motivation to deal with financial topics but for unknown reasons have not yet addressed them in depth. Against this background, the game seems to have an effect on students who are most in need of this kind of education and not those who are already very interested and skilled. Since we do not measure improvement in financial literacy, this does not necessarily mean that students with high prior knowledge do not benefit from the game. However, it must be noted that there are no negative effects of financial knowledge on situational interest or on perceived autonomy and relatedness during game play. This inconsistency and the contrary effects of financial motivation and financial knowledge are discussed in more detail with regard to possible limitations of this study.

The interrelation of individual prerequisites and game experience on postgame situational interest shows generally higher effects on the non-cognitive facet of situational interest Previous gaming experiences and gaming frequency, which have a significant effect on negative activation, seem to be particularly important. In contrast, lower game complexity has a positive effect on positive activation, which might be because of cognitive overload when playing the more complex version of the game. Older age is a predictor of value-related valence. Thus, a game about personal financial management seems to be more meaningful for older students, which is also in line with previous research (e.g., Lusardi, 2019). In addition, it should be emphasized that the effect of a game depends on its design. For example, there is evidence that games in economics education are more motivating if they are challenging and embedded in the curriculum (Platz, 2022). This is further underlined through our analysis by modelling the two versions of the game as a control variable. Players who played version 1 with higher complexity showed higher affective activation. However, generalizing statements cannot be made about the effect of games in this context since game designs may not differ only with regard to their complexity (Pawar et al., 2019).

For the reflection phase, the positive influence of prior motivation on affective activation can again be confirmed, while leisure activities and prior knowledge exert a negative influence on situational interest The influence of academic background on negative activation is relatively high. One explanation of this high effect is that students with a higher academic background probably have more difficulty with an unconventional learning method that enables an easy introduction to financial topics. This finding is similar to empirical evidence demonstrating that tasks that are too easy are demotivating for high-performing students (Atkinson, 1998). Against this background, this result confirms evidence for the significance of parental influence on the learning experience at school (Campbell and Verna, 2007). Furthermore, it highlights that GBL approaches in finances are not appropriate for all students, who differ in their financial interest and prior financial knowledge as well as their socioeconomic background.

Accordingly, during game play, situational interest is influenced primarily by previous game experience. In connection with reflection tasks, the influence of financial literacy on situational interest becomes more important. Therefore, this kind of game is most suitable for students with higher motivation but little previous experience and knowledge in finance.

Although the effect sizes are generally small or moderate, they should not be underestimated due to the design approach with its three points of measurement. Additionally, it must be positively highlighted that approximately 30 to 50 percent of the variance of the dependent variables are explained by the empirical models. However, due to the small sample size and the high number of predictors for each regression model, robustness checks are necessary. Bootstrapping with 2000 random samples revealed that the adjusted R2 lies between 10 and 45 percent with a 95 percent confidence interval. Following Ellis (2010), an adjusted R2 equal or higher than 25 percent must be considered high. Therefore, the adjusted R2 of the nine regression models could be considered at least moderate. Despite these positive aspects, there are several important limitations.

Limitations

From a methodological point of view, the small sample size must be mentioned, due to which the lack of significance of some results can be explained. As a result of the small sample, it was also not possible to perform a mediation model, which could likely underline the importance of BNE in more detail. Additionally, the conclusions about the influence of prior knowledge can only be evaluated to a limited extent since this topic was surveyed with very few items. Regarding this variable, the low reliability of financial knowledge must be mentioned. Such low reliability is likely due to the small number of items, which differ greatly in their financial content. For this reason, a replication study to test financial knowledge with a larger item battery is strongly recommended. In addition, GPA should be obtained as well as the subject grade for economics because these could act as potential confounding variables. For replication studies, we therefore recommend considering a valid survey of GPA by collecting school records (see, e.g., Duzhak et al., 2021; Lin, 2018).

Considering these limitations, the inconsistency of the effects of financial knowledge mentioned above and the contrary effects of financial motivation, we further analyzed the robustness of the estimated model by using bootstrapping with 2000 random samples. Based on this, we analyzed the confidence intervals of the calculated estimators, finding that zero in the case of financial knowledge was also a plausible value for the prediction of perceived competence (see Table 5). Considering financial motivation, in most cases, zero was a plausible value only with a 90 percent confidence interval. This strongly underlines the importance of replication studies since the estimated values only provide a tendency. However, the contrary effects of financial knowledge and financial motivation still must be seen as likely and cannot be lead back on multicollinearity issues.

Another point of criticism is the retrospective measurement of affective activation instead of continuous-state sampling (Schallenberger, 2005). Here, we had to strike a balance between a precise measurement and the associated interruption of the flow of the game. Accordingly, the affective experience was solicited directly after the game. In addition, all courses had an economic focus and were at the highest level of full-time education in Germany, which limits the external validity of this study. The external validity is further limited by the fact that the game was only played once. Therefore, the results can only be transferred to possible effects of repeated game play to a limited extent. Regarding the actual playing time, the effects were only surveyed for a comparatively short playing time of 45 min. Similar games are mostly played longer and repeatedly. At this point, it is still unclear how game experience and interest develop over repeated rounds of play. Addressing this open question is one possible implication among other key implications for research and instructional practice.

Implications

Based on the results and their limitations, numerous important questions arise for future research in this area. Central to these is how repeated play affects situational interest (state). What is its impact on individual interest (trait) and related behaviors? In pursuing these questions, the replicability of the results obtained here should also be tested with a more representative group of students and a larger sample. This question also applies to a comparison with students in vocational education, who already have more experience in dealing with finances due to their paid training (Förster et al., 2017). Another question concerns which games are particularly suitable for promoting financial literacy and how they can be adequately integrated into the learning process. Games such as "Moonshot", which deal with the topic of personal financial management, can be recommended for students who are at the beginning of the upper secondary level in general education and who have little prior knowledge and experience but growing motivation in this area (Walstad, 2001). Another possible field could be vocational preparation courses for migrants to promote integration in this respect. In addition, it became clear that reflection on the game exerts an impact on the value-related valence of the promoted topic. Thus, reflection can serve to support students in their further game strategies and to guide them in transferring the lessons learned from the game to their own lives.

Footnotes

Availability of Data and Materials Statement

The datasets used and/or analyzed during the current study are available from the corresponding author on reasonable request.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Ethics Statement

All relevant national standards concerning the recruitment and information of the participating students, schools, and organizations were respected (with written informed consent). Participation in this study was voluntary. At the first point of measurement, the school administrations approved all surveys consistent with the German standards for school surveys at the time. In addition, all participants were older than 16, and most of them were already of legal age. Since our research project is not associated with any risks or burdens, no additional consent was required from legal representatives (Az.: 6499.10/417). All participants were of legal age, or consent was given by legal representatives, and participants were fully informed and agreed to participate.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article