Abstract

Does the gender pay gap affect women’s ability to repay their student debt? This study investigates the extent to which an income contingent scheme benefits women because of their individual earnings. Using the Australian Household, Income, and Labour Dynamics in Australia Survey, gender differences in debt repayment behaviour over the past two decades was examined. The regression model comprised interaction terms including risk-averse, low socio-economic status, low wealth and low income. The industries where the majority of women are employed – education and health – were also examined. It was found that over 2002–2014, women generally had less student debt than men, but those who were low income carried more debt. This is the first study to include an analysis of student debt by industry through a gender lens. Given the increasing amount of student debt Australians are carrying, it is important for policymakers to pay attention to its effects to ensure fairness and equity.

Introduction

The benefits of higher education are well established for individuals in terms of relatively higher incomes and rates of employment (Barr, 1998, 2004). The private rate of return has been quantified to be as high as 21.1% in Australia (Borland et al., 2000). Such benefits are seen to justify shifting the higher education costs from taxpayers to students, particularly in the neoliberal environment (Chang and McLaren, 2018; Nygreen, 2018; Tesar, 2019).

Australian students are advantaged by access to a student loan scheme that defers repayments until an income threshold is met. Australia introduced the first income contingent loan (ICL) scheme to broaden higher education access and reduce the financial burden of higher education provision on government over 30 years ago. Other countries with well-established full or partial ICL schemes include England, New Zealand, the Netherlands, South Korea and Hungary (Britton et al., 2018). The ICL scheme has progressive income thresholds for repayment. For example, the Australian ICL has nil repayment for those with gross incomes under AUD$51,957 and 2% of income is paid for those with incomes in the AUD$51,957–57,729 income bracket in 2018–2019. Progressive increases in income brackets and repayment rates follow, with the top tier being 8% repayment on incomes over AUD$107,214.

Another major distinction of the Australian ICL scheme from student loans in other countries such as the United States, where many loans are privatised, is the treatment of interest. The Australian ICL scheme does not charge debtors interest, but balances are adjusted in June each year for inflation, established by the Consumer Price Index (CPI) that has averaged 2.4% over the last decade. In comparison, in 2018 interest rates for Federal loans in the United States ranged between 5.0 and 7.6%, and private loans ranged from 3.9–14.3% (Kirkham, 2019). The rate of interest for Federal Loans in the United States is linked to the 10-year Treasury bond rate plus a fixed percentage. Changing the indexation from the CPI to the Treasury bond rate, capped at 6%, was similarly proposed in Australia in 2014 through legislation that did not pass Parliament (Dow, 2014).

The purpose of the inflation adjustment is to maintain the real value of student debt on the government’s balance sheet and reflect opportunity cost for the lender, functioning in a similar manner as an interest charge. If the recipient pays off the ICL debt, they have paid the principal borrowing amount plus an additional sum (the ‘adjustment’), which is added to the principal and thus compounds the debt. As compulsory repayments depend on income earned, some recipients take longer than others to pay off the loan, thus incurring more adjustments and compounding effects than others. If a recipient never pays off the loan, then they receive a larger subsidy from the government than those that do. Indeed, 21.8% of Australian ICL debts are unlikely to be repaid, which equates to a significant amount of the total ICL debt, forecasted to reach AUD$11 billion in 2025 (Parliamentary Budget Office, 2016). Hence, governments will continue to be motivated to review the current settings in the neoliberal environment.

It is from this perspective that the impact of Australia’s ICL system on women is examined. In light of the increasing attention on the gender pay gap, it is timely to inspect whether a scheme designed to increase the rate of repayment as incomes increase has unintentional consequences. Given that women earn lower incomes than men and tend to have time out of the workforce, it is likely that women take longer to pay down their ICL loan, thus incurring more adjustments over time. This being the case, they also have their repayment deducted from their incomes for longer periods of time. The Australian Household, Income, and Labour Dynamics in Australia (HILDA) Survey data is used from 2002–2018 to test this hypothesis through inspection of descriptive statistics, transition tables, and a regression model including demographic and socio-economic characteristics for student debt levels.

The Australian ICL scheme henceforth referred to as the HELP system. The Higher Education Loan Program (HELP), formerly the Higher Education Contribution Scheme (HECS), is the principal scheme in Australia. See Parliament of Australia (2018) for an explanation of these and other loan schemes.

The remainder of this paper has the following structure. The next section sets the context of the gender wage gap in Australia and the intention of the HELP scheme. Section 3 briefly reviews the literature on the impact of student debt on financial decision-making. The subsequent section explains the empirical methodology and the data employed in the analysis. Section 5 presents the results and Section 6 discusses the findings.

Background of gender and the Australian HELP scheme

The field of feminist economics despairs at assumptions underpinning ‘rational’ decision-making and policies made from a traditional masculinist model of reasoning that favour the rights and needs of men (Gonzalez-Arnal and Kilkev, 2009). Globally, the constraints of student debt schemes and gender shape decisions for university study and the labour market (Dwyer et al., 2013). Dwyer et al. (2013) express the view that consideration of tertiary finance as a gendered issue is important for a number of reasons: (a) graduate incomes for female-dominated occupations may not pass the cost–benefit threshold for tertiary study; (b) the gender pay gap for women is particularly large for jobs that do not require a tertiary qualification and the gender pay gap reduces student debt repayment capacity; (c) women may have fewer options for jobs that do not require tertiary qualifications, and therefore feel pressured to attend university; and (d) women may want more support during study than men, including for academic preparation, family support and engaging with peer networks, and therefore drop out or fail to attend university at all. Thus, returns on higher education are likely to be differentiated, and indeed for some, not guaranteed (Gonzalez-Arnal and Kilkev, 2009).

Given these factors, one could argue that women are advantaged by the HELP scheme. The high-income thresholds and income contingency mean that women may not earn enough to pay off the debt over their working lives and thus their education has been heavily subsided by the government. It is an intended outcome that the design supports equity of access and places the burden of repayment on those that can afford to pay (Barr, 1998).

However, a report by Grattan Institute in 2016, entitled ‘HELP for the Future: Fairer Repayment of Student Debt’, put the spotlight on women. The author of the report stated that ‘the major cause of HELP’s problems is that debtors who earn less than its initial threshold … do not repay’ and that ‘women’s repayment rates are critical to HELP’s finances’ (Norton, 2016: 18). Additionally, Norton (2016) argues that half of HELP debtors should not feel financial strain from the extra repayment as many women live in a couple household with incomes that exceed AUD$80,000 per year. The crux of the report was that if the initial repayment threshold was lowered, more women would be captured in the compulsory repayment and thus, in aggregate, more of the outstanding HELP debt would be paid down.

Off the back of this report, Parliament passed a reform in 2018 to reduce the initial repayment threshold from AUD$51,957–45,000 (with a reduction in the initial threshold repayment rate from 2 to 1%). For those with incomes of AUD$45,000 per year, the HELP repayment would be AUD$9 a week. The legislation (Higher Education Support Legislation Amendment (Student Loan Sustainability) Bill [Parliament of Australia, 2018]) stated that the purpose of the change was to improve the sustainability of the HELP scheme by bringing more individuals into the repayment scope over time, while acknowledging the higher and sooner repayment of HELP for some students may reduce access to higher education. In particular, it was noted that there were disproportionate impacts on women and other low-income groups: The Government currently carries a higher deferral subsidy from demographic groups that tend to have lower incomes. This includes women, individuals in part-time work, or individuals in low paid professions. As a result, some of these individuals, including women, may be making repayments for the first time as a result of the introduction of a lower minimum repayment threshold. Addressing this income inequality, however, is not the role of the higher education loans system (Higher Education Support Legislation Amendment (Student Loan Sustainability) Bill 2018: 6–7).

The gender pay gap in Australia ranges between 17.3 and 26.7%, depending on seniority of position and industry. An analysis of 4 million employees and 11,000 employers by the Workplace Gender Equality Agency (WGEA) in 2018 found significant gender pay gaps remain once compositional differences between men and women are accounted for and comparing like-for-like remuneration (controlling for level of occupational seniority, industry and employment status). Thus, inequalities in pay between men and women are not explained by the different ways that men and women work, or the different roles that women and men play at equivalent occupational levels within an organisation. However, the report found that more organisations than ever before are taking specific actions on pay equity, such as pay gap audits and analyses (WGEA, 2018).

Given that organisations are reassessing policies through a gender lens, government should be motivated to do the same. There are consequences for government at the aggregate level. For example, women under financial strain because they are on low incomes or because they make repayments over longer periods have less financial capacity to save for unforeseen life events and retirement, thus putting pressure on the public purse. In addition, this money is withheld from spending, reducing economic activity.

Review of the literature

The literature on student debt is concentrated in the United States, where student debt was recently labelled a USD$1.5 trillion crisis (Friedman, 2018). High student debt levels are found to have a negative impact on some individuals’ financial decisions and circumstances (Williams and Oumlil, 2015), which of itself can be a barrier to participating in tertiary education (Burdman, 2005; Linsenmeier et al., 2006). Higher instances of late bill payment, credit denials, increased applications for hardship funds, as well as other social and economic disadvantages are examples of the effects of high student debt (Bricker and Thompson, 2016; Despard et al., 2016). Further, having large student debts can make unforeseen events especially hard to navigate, like job loss, divorce and illness (Dwyer et al., 2013). Student debt has been linked with financial stress, anxiety and depression. Financial stress also has a negative impact on academic performance (Archuleta et al., 2013). In aggregate, high student debt can have negative consequences on productivity and economic growth (Barros et al., 2011; Ferretti et al., 2016).

American and Canadian research supports the contention that the cost of study affects student diversity (Despard et al., 2016; Jackson and Reynolds, 2013; Javine, 2013; Woloschuck et al., 2010). In Australia and England, students from low socio-economic backgrounds, as well as women, older students, single parents, and students with family responsibilities, have all been found to be debt-averse and less likely to study if they will accumulate debt (Gonzalez-Arnal and Kilkev, 2009; Marks, 2009). An Australian survey of 7000 high school students who were questioned regarding their intention to participate in higher education found that 39% of students from low socio-economic backgrounds believed that costs might stop them from attending (James, 2002). This finding compared with 23% of students from high socio-economic backgrounds. Wright (2005) also found that student fees were the primary factor in study decisions of students from low socio-economic backgrounds, leading to reduced participation in the Sydney region (Wright, 2005). Students expressed unease about the level of debt they incurred as a direct consequence of attending university and commented on their lack of foresight in relation to the repayment of this money.

However, not all studies agree. Andrews (1999) and Aungles et al. (2002) did not find that the proportion of people studying from low socio-economic backgrounds had changed much over time. These findings support work from New Zealand (Tumen and Shulruf, 2008) and the United States (Waddell and Singell, 2011) suggesting that increased student debt is not a discouraging factor and is, indeed, an effective vehicle for access among higher need students (Yezdani, 2015). An experiment conducted recently by Bartholomae et al. (2019) that explicitly tested the gender effect in student debt borrowing decisions also found no significant gender differences.

Student debt has been linked to a delay in childbearing for women in the United States and Australia (Bozick and Estacion, 2014; Jackson, 2002). However, other authors attributed the fact that women were having children at older ages to wider societal trends (Armstrong, 2004). Nonetheless, this line of questioning triggered some evidence-based responses to investigating the issue of the impact of student debt on financial decision-making. In a survey of student nurses in New Zealand, for example, 69% of respondents indicated that having student debt was an impediment to further study, buying a home, and starting a family (O’Connor, 2003). Student debt can also create problems in obtaining finance. A random sample of bank managers in New Zealand revealed that 51% had declined applications for finance and mortgages because of student debt (Pearse, 2003). Other Australian research found no association between student debt and lower fertility rates, but that the magnitude of the student debt did affect parenthood decisions (Yu et al., 2007).

Finally, there is limited literature relating to gender and repayment of student debt. A study by Saleh et al. (2017) found that it takes women an average of 0.168 years’ more salary than men to pay back student loans in the United States. The authors state that ‘it clearly takes longer for females on average to repay their college loans than it does for males, and this serves as a major impediment to the financial success and equal progress of females in modern society’ (Saleh et al., 2017: 236). The American Association of University Women reported that, 4 years after graduation, men had paid off 44% of their student loan debt, while women had only been able to pay off 33% due to the gender pay gap (American Association of University Women, 2016). Particularly disadvantaged were African-American and Hispanic women, paying off 9% and 3% of student loans respectively over the same period.

Examination of 10 years of the Australian HILDA Survey (2001–2011) shows substantial repayment capacity differences between male and female debtors (Higgins and Sinning, 2013). Average debt levels of male graduates drop relatively quickly over time, whereas female graduates’ levels of debt remain constant, leading to projections that outstanding debt levels for female university graduates remain high while male balances are close to zero or very low. Data analysis of Australian Tax Office statistics raises further concern, as they reveal that the average time to make the first compulsory ICL payment (for both men and women) increased from 4.9 years in 2007 to 5.1 years in 2011, and the average time to repay the debt grew from 7.5 years in 2007 to 8.1 years in 2011 (Highfield and Warren, 2015). Highfield and Warren (2015) however, did not provide an analysis of repayment by gender.

Data and methodology

The literature suggests that accumulating student debt can be a barrier to accessing higher education and can cause financial stress and other financial consequences post study. In Australia, there has been some focus on the study decisions of people with low-socio-economic status (SES) in this respect, with debt-aversion seen as one of the deterring factors. However, no study investigating the repayment behaviour of people with these characteristics once holding student debt was identified. It would be reasonable to assume that people who are of low income, low wealth and low SES maintain higher levels of student debt because of the income contingent nature of the HELP scheme and their reduced capacity to make voluntary repayments. It would also be reasonable to assume that risk-averse people behave similarly to debt-averse people, in that once they have accumulated student debt, they pay it down at a faster rate than risk-seeking people, if economically possible.

Furthermore, the context of the gender pay gap and the HELP scheme highlights the need to understand the effects of women’s repayment capacity in more detail; accordingly, the current research questions focused on the repayment behaviour of women. As the gender pay gap can vary by industry, this study makes a novel contribution to the literature by investigating the HELP repayment behaviour of females in industries where females are most frequently employed. An assumption was made that the gender pay gap in these industries means that women hold higher HELP balances than men.

Accordingly, the research hypotheses are: H1: Females that are of low income, low wealth, and low socio-economic status maintain higher levels of HELP H2: Females that are risk-averse maintain lower levels of HELP H3: Females in industries with the highest female participation rates maintain higher levels of HELP

The HILDA sample information on HELP does not perfectly correspond with the information provided by the Department of Education and Training (DET, 2018). The HILDA student debtors comprised 8% of the sample in 2002, 8% in 2006, 9% in 2010 and 12% in 2014. By comparison, DET (2018) reports that the proportion of the Australian population that had outstanding student debt (HELP debt) was 2% in 2002, 6% in 2006, 7% in 2010 and 9% in 2014. Thus, the HILDA sample is marginally overstated.

The results must be interpreted within the limitations of the data. HILDA does offer advantages over other datasets, such as that provided by the Australian Tax Office, in terms of generalisability and access to individual demographic and socio-economic factors.

The gender analysis of student debt is considered in four parts. First, descriptive statistics using the HILDA survey provide an overview of gender differences and trends over time. The descriptive statistics present participation rates and average balances of student debt for males and females, as well as by attitude to risk-taking, age, SES, household type, year, education, wealth, personal income and industry classification.

Further descriptive statistics are provided by graphing cohort differences in HELP levels. Cohort differences are modelled by identifying when participants first responded positively to having student debt and grouping participants into cohorts based on the years 2002 or before, 2003–2006, 2007–2010 and 2011–2014. Students in the first cohort may have accumulated student debt any time before 2002, thus pushing down average student debts. Categories of average student debt owing were also generated to show the gender difference in the distribution across the sample.

Transition tables are used to illustrate the proportion of individuals moving between categories. Using a binary student debt variable, equal to 1 if HELP is greater than AUD$0, the category of interest in terms of understanding gender differences in HELP repayment is the proportion of individuals moving from 1 to 0 in the HELP binary variable. That is, those who held no student debt (0) in time t but held student debt (1) in t-1.

Finally, a pooled regression model tested for the significance of gender and other demographic and socio-economic factors on HELP levels. Demographic and socio-economic factors included gender, age, education, personal income, household type, SES, wealth and attitudes to taking financial risk. The panel data regression model is as follows:

Year is a dummy variable for each wave of the Wealth module.

Gender is a binary variable where female is (1) and male (0).

Age is represented by a series of age category dummy variables, recoded from the HILDA continuous age variable. The categories include ages 16–24, 25–34, 35–44, 45–54, 55–64 and over 65 years.

Household type is a series of dummy variables, recoded from 28 HILDA household structure categories to 4 categories. These categories include couples with children, couple, lone parent and lone person households.

Education represents a series of qualification dummy variables, where respondents nominate their highest qualification attained. The 10 categories in HILDA have been recoded to 3 groupings, where degree indicates a degree or higher educational qualification, a vocational qualification indicates further study after school that is not a university program, and Year11/12 represents completion of school-level education and unknown or undetermined education.

SES is a series of categories, recoded from the 10 Socio-Economic Indexes for Areas (SEIFA) classifications in HILDA to 5. These categories include low SES (SEIFA 1–2), low–mid SES (SEIFA 3–4), mid SES (SEIFA 5–6), mid–high SES (SEIFA 7–8) and high SES (SEIFA 9–10).

Wealth is a series of household net wealth categories, recoded from a continuous variable in HILDA. The categories include less than AUD$499,000, AUD$500,000–999,999, AUD$1,000,000–1,499,999 and greater than AUD$1,500,000.

Personal income is a series of personal income dummy variables comprising four categories. The categories have been recoded from the continuous variable in HILDA. The categories include personal income less than AUD$19,999, AUD$20,000–49,999, AUD$50,000–99,999 and AUD$100,000 and over. Low-income earners were assumed to be those earning less than AUD$19,999 per annum, approximately a quarter of Australian average earnings.

Attitude to risk-taking is derived from an attitudinal question in the Wealth module, where respondents are asked to rate their level of willingness to take financial risks. Responses to positive risk-taking (‘substantial’, ‘above-average’ and ‘average’ risk) were recoded into a dummy variable ‘risk-taking’. Individuals indicating no appetite for risk taking were recoded as ‘no risk’. Responses to the fifth option, ‘I never have any cash’ were excluded from the variables for the purposes of this analysis.

Industry is a series of 19 industry dummies from the Australian and New Zealand Standard Industrial Classification 2006 division, available in HILDA.

Results

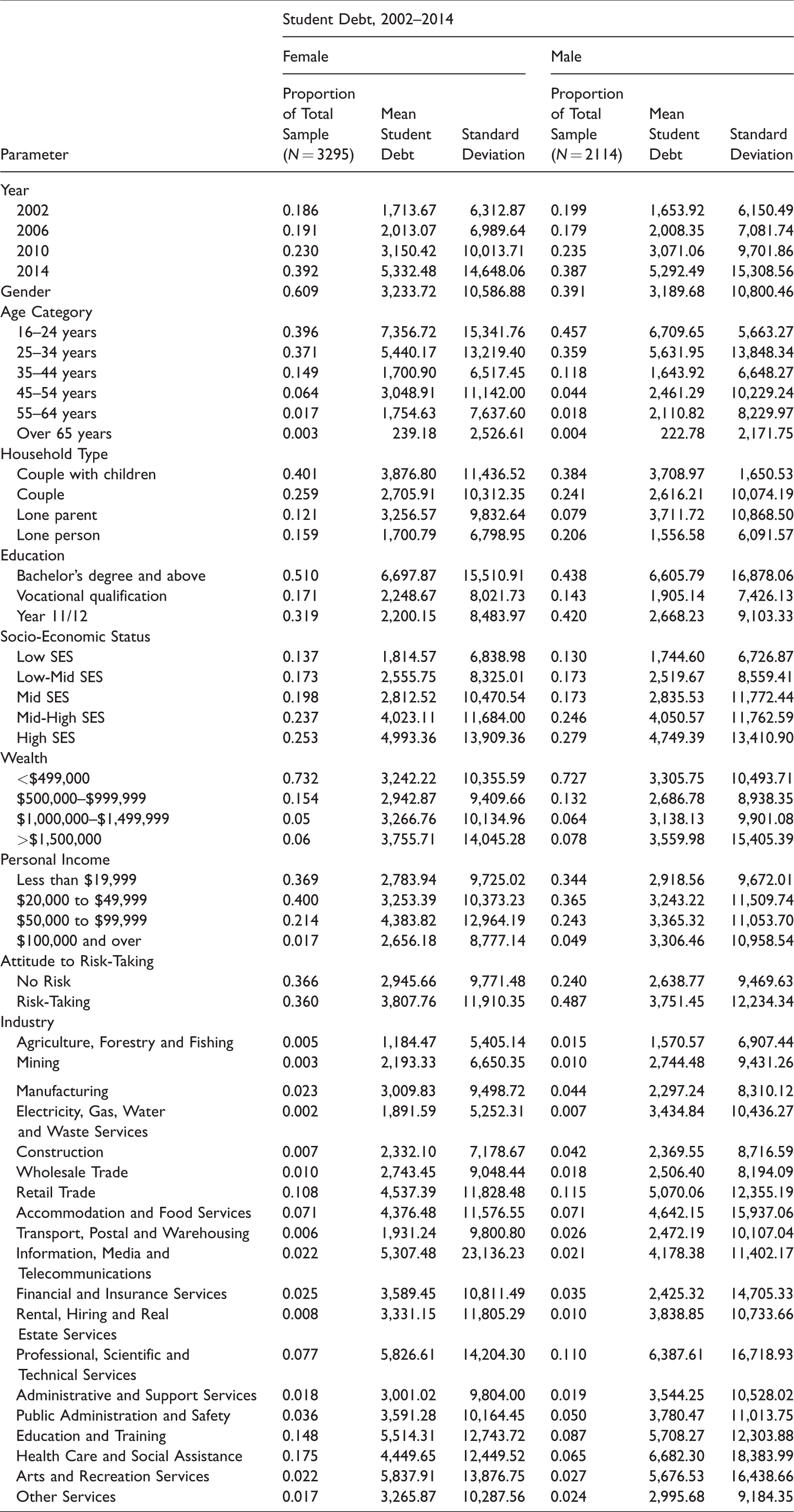

Table 1 provides an overview of HELP balances for women and men of selected demographic and socio-economic characteristics, averaged over the 2002–2014 sample period. The table shows that female HELP debtors amounted to 60.9% (or 3295 respondents) over the 2002–2014 sample, with an average student debt of AUD$3,233.72. Males comprised 39.1% of HELP debtors, with an average student debt of $3,189.68. In 2002, female HELP debtors’ average balances were AUD$1,713.67, which increased to AUD$5,332.48 in 2014. Males experienced similar increases, averaging AUD$1,653.92 in 2002 and AUD$5,292.49 in 2014. In general, female student debtors were slightly older, had higher levels of education, lower levels of participation in the labour force, and lower rates of personal income than their male counterparts. Importantly, a very large portion of the student debtor population was under 34 years old.

Descriptive Statistics, Student Debt Holders.

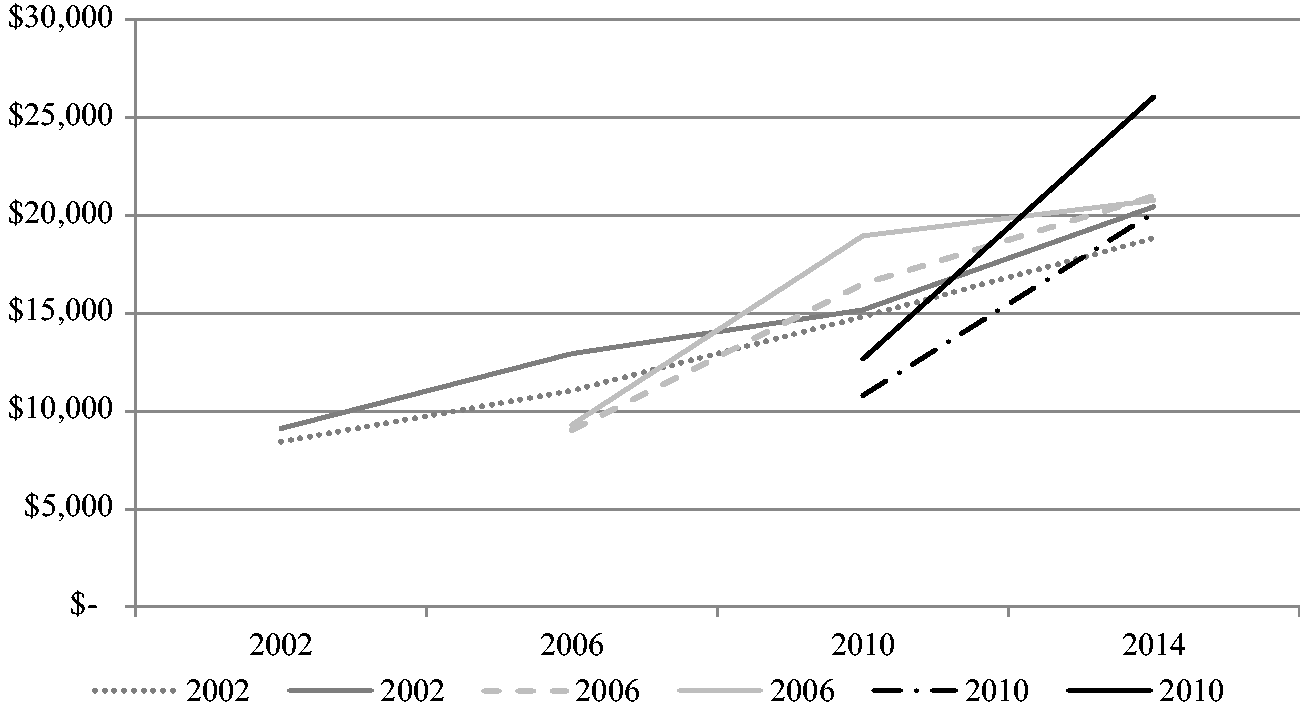

Figure 1 shows the trajectories of males and females for the level of student debt across cohorts. The trajectory of the 2002 cohort, the longest time span, shows a constant upward trajectory for females over the 12-year period, whereas the overall debt for males reduced in 2010, and then increased in 2014. Reasons for this pattern of debt for men are unknown, but labour market challenges related to the Global Financial Crisis may have increased return to study. The 2006 trajectory shows a hump shape for men, converging with the female trajectory in 2014. The 2010 trajectory shows more divergence between the female and male trajectories, with males showing a much steeper gradient.

Cohort trajectories.

These data highlight worrying trends in HELP balances for both males and females. The cohort holding student debt since (at least) 2002 does not seem to be reducing its balance over time as much as would be expected. In fact, no downward trend was discernible. This finding is consistent with estimates of increasing average times to repay debt (Highfield and Warren, 2015). The steeper gradients, or quicker escalation, of debts for more recent cohorts, combined with the very long pay-down times observed, means student debt stays with the holder for quite a long time, which is not ideal for either the government budget or the debt holder, especially if holding student debt has negative consequences for other financial decisions.

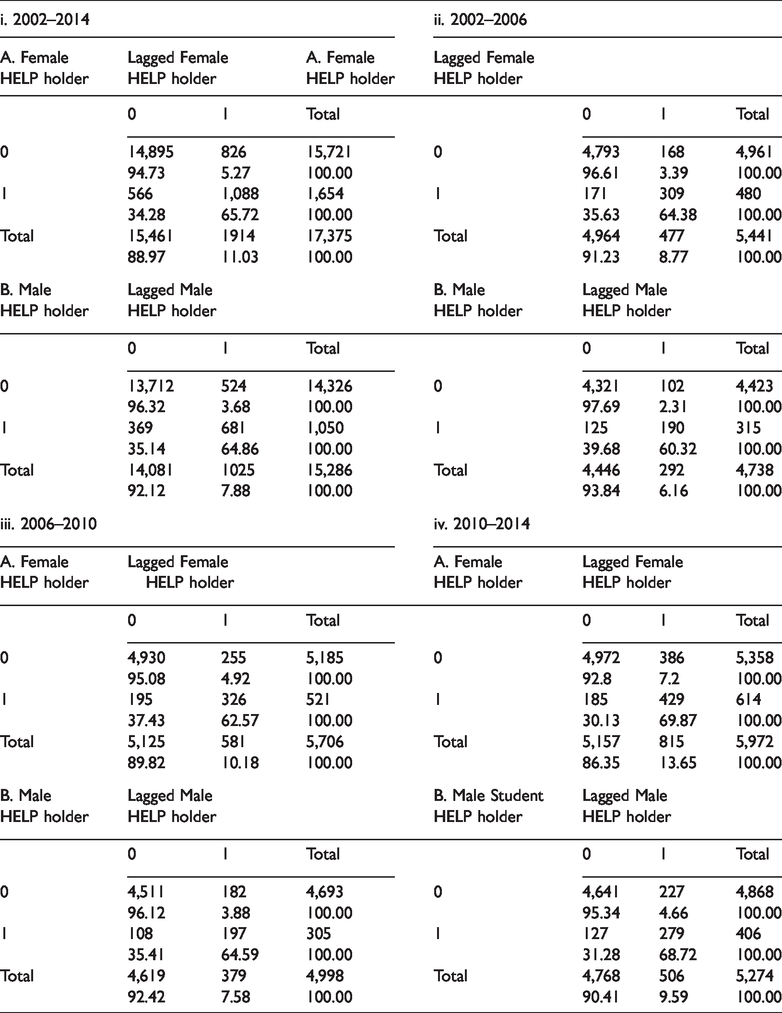

Further insight into repayment behaviours is provided by inspecting the transition tables on the binary HELP variable. Table 2, panel (i) shows that for females, 94.73% of respondents have never held student debt, while 65.72% continue to hold student debt. Over the sample period, 34.28% of respondents transitioned into having student debt, while 5.27% of females paid off the debt (transitioned out of holding student debt). A comparison of panels A and B shows that the proportion of women that paid off student debt over the sample period was slightly more than that of their male counterparts (5.27% vs. 3.68%). This trend is upheld in panels (ii), (iii) and (iv) that show the change in states between each of the Wealth modules. Interestingly, the number of HELP holders who remain in the same state (1,1) have increased over time (64.38/60.32% in 2002–2006, 62.57/64.59% in 2006–2010, and 69.87/68.72% in 2010–2014). This is a concerning trend for policymakers looking to reduce the HELP burden on the balance sheet.

Transition Tables.

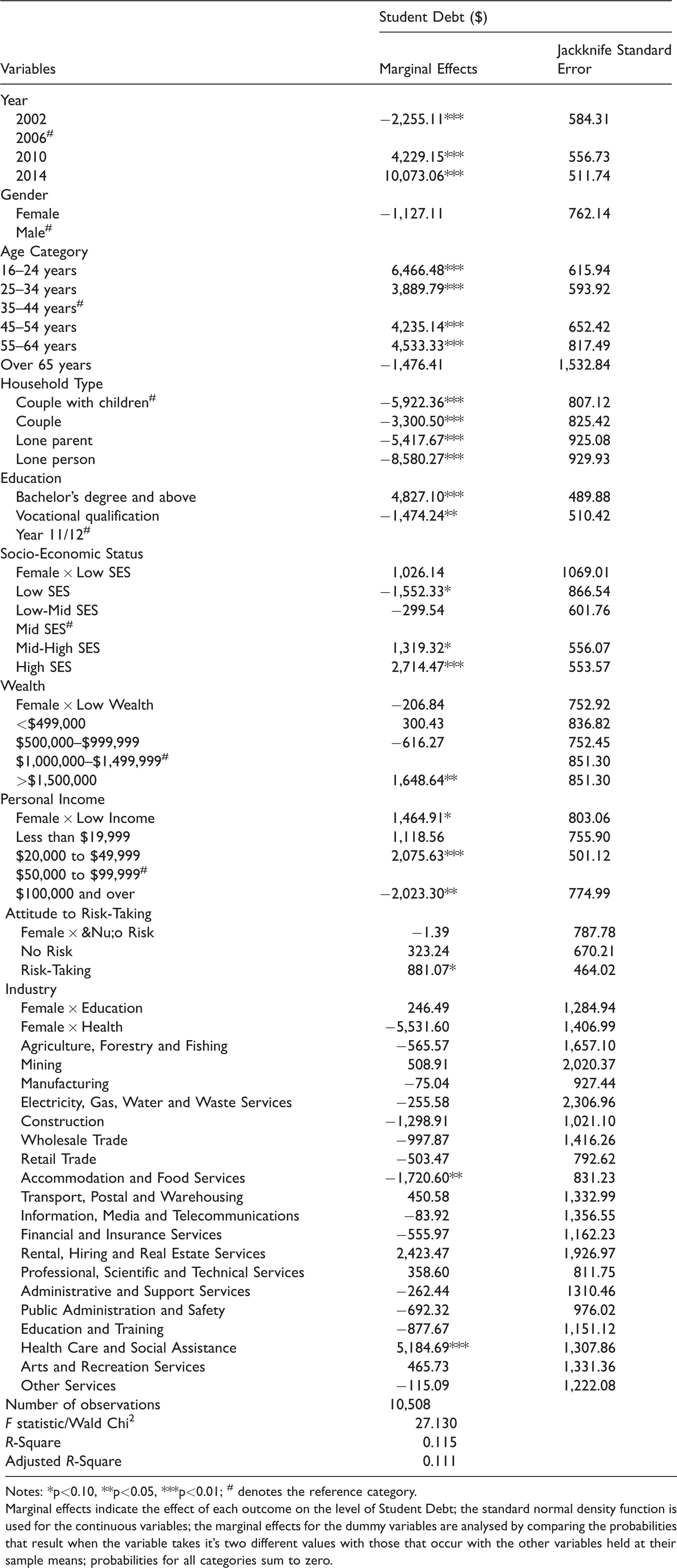

Regression results provided in Table 3 provide marginal effects, Jackknife standard errors and levels of significance for 10,508 observations. The adjusted R2 reports a goodness of fit of 11.06%, meaning there is significant variance not explained by the model. Generally, and reporting only on the statistical coefficients, HELP balances have increased over the years: they are larger in younger age groups, they are larger for university qualifications, and larger if you are in categories of high SES, high wealth, and mid-range personal income. Those who are willing to take financial risks also have slightly higher levels of HELP than the average. Those on high incomes, of low SES, and holding a vocational qualification are likely to have lower HELP balances than the average. Interestingly, all household types are significant and negative, meaning that people in these household types have HELP balances substantially under the average. For household structures where having children as dependents can strain household resources and result in gendered work/care decisions, such as couples with children and lone parents, the results are similar. The marginal effects coefficient are 5,922.36 and −5,417.67, respectively. In comparison, lone person households is −8,580.27 and couples are −3,300.50. In response to the Grattan Institute report, it seems there is some merit to the assertion that those in coupled households have the capacity to repay HELP debt.

Pooled Regression.

Notes: *p<0.10, **p<0.05, ***p<0.01; # denotes the reference category.

Marginal effects indicate the effect of each outcome on the level of Student Debt; the standard normal density function is used for the continuous variables; the marginal effects for the dummy variables are analysed by comparing the probabilities that result when the variable takes it's two different values with those that occur with the other variables held at their sample means; probabilities for all categories sum to zero.

Several variables of interest relating to females were not significant. The marginal effect for gender was not significant, but the direction of the relationship between HELP balances and being female was negative (−1,127.11). Likewise, the interaction term for Female × Low Wealth was negative but not significant (−206.84) and Female × No Risk was very small and negative (−1.39). While not significant, the direction of the change indicates that women in these categories maintain lower HELP balances than males. There could be several explanations for these results, but the most likely one is that women are studying in fields that do not accrue as much HELP as males, and/or have shorter programmes of study. The descriptive statistics in Table 3 (transition tables in particular) show that there are just as many women as men with HELP over the sample period, so these results are unlikely to be due to women avoiding entering tertiary education. An alternative explanation could be that women in these categories make enough income to meet the repayment thresholds and/or make voluntary contributions in order to pay down HELP balance. More detailed information is needed to support these contentions, but it certainly appears that women maintain lower HELP balances than men, thus repaying their fair share.

However, two of the interaction terms had positive coefficients. Female × Low SES was not significant but had a positive marginal effect (1,026.14). In comparison to the Low SES variable being significant at the 10% level and negative (−1,552.33), this is worth noting. Females in this category may be finding it more difficult than their male counterparts to reduce their HELP balances. The other positive interaction term was Female × Low Income (1,464.91), which was significant at the 10% level. Similarly, women in this category had higher HELP levels than men. The magnitudes of the two positive effects were not great compared with some of the other marginal effects reported (e.g. in 2014 it was 10,073.06), but it does indicate that women are finding it harder than their male counterparts to reduce the balance over time.

Finally, industries were examined: only two industries were significant. Generally, people in Health Care and Social Assistance held AUD$5,184.69 more HELP. This is likely to be associated with medicine, dentistry and other related professions where lengthy degrees and training are required. Those in Accommodation and Food Services had AUD$1,720.60 less HELP; degree-level qualifications are not necessarily required. The descriptive statistics showed that women are primarily employed in the Health Care and Social Assistance and Education and Training industries. Interaction terms were created for these two industries to ascertain the HELP repayment behaviour of women. Regression analysis showed no significance for the two marginal effects. Women working in the health sector though, were likely to have AUD$5,531.60 less HELP than their male counterparts. This result can most likely be attributed to the difference in the HELP debt associated with more female-dominated professions within the health discipline, such as nursing.

This analysis makes important contributions to the discourse on student debt. Overall, the HELP repayment behaviour of women was found to be marginally better than men, which refutes the assertion by Grattan Institute that there is a problem with women failing to pay their way. The results need to be interpreted within the limitations of the data . Nonetheless, the HILDA data do provide evidence that females in particular categories, such as low income and low SES, hold higher HELP balances than similar males. Notwithstanding the lack of significance, we provided partial support for H1: that females who are of low income, low wealth, and low socio-economic status maintain higher levels of HELP. Regarding H2, the Female × No Risk interaction term was not significant and the magnitude very small, so the hypothesis that females that are risk-averse maintain lower levels of HELP was not supported; they are on a par with average HELP balances. Finally, females in the health industry maintain lower HELP balances than their male counterparts, while females in education and training hold slightly higher balances. Thus, overall, H3: women in industries with the highest female participation rates maintain higher levels of HELP, was not supported.

Discussion

This study makes several contributions to the literature. First, the results add to the current literature on student debt trajectories. By including an additional observation point (2014) the study extends the earlier work of Higgins and Sinning (2013) and provides new insights into cohort differences, observing the increasing debt trends. Transition tables further report gender differences in HELP repayment behaviour over the whole sample period as well as in between Wealth modules, and highlight concerning trends regarding the increasing proportion of HELP holders who do not pay off their balance.

We did not find gender to be a significant factor in the level of HELP balance, and for many of the female interaction terms, the direction of the relationship was negative. This means that there was no evidence that women are holding significantly higher balances of HELP than men, which could happen were they affected by the gender wage gap or not paying down their fair share of HELP, as asserted by the Grattan Institute. However, we did find that women in low SES and low-income categories were carrying more HELP than males in the same category. In the HILDA data averaged over the 12-year period, the magnitude of these differences was relatively small (1,026.14 and 1,464.91 respectively). Future research should revisit these statistics, given the policy change to lower the initial income threshold for compulsory repayment in 2019.

This study makes a further contribution to the literature by examining the relationship between industry classifications and HELP balances. Further research could examine Return on Investment in education in specific industries. For example, the descriptive statistics showed higher HELP balances for industries such as Arts and Recreation Services, and Health Care and Social Assistance in relation to women.

While the data were specific to Australia, the findings are important for higher education policymakers internationally. In aggregate, high student debt can have negative consequences on productivity and economic growth and widen the gender wealth gap (Barros et al., 2011; Ferretti et al., 2016). Researchers and public policymakers are encouraged to monitor the disquieting trends of increasing student-debt balances that may produce different financial outcomes for men and women. Future research on understanding whether prolonged holding of student debt changes the financial decision-making of women, including changing jobs, starting their own businesses, applying for loans or other activities is encouraged.

Supplemental Material

PFE895182 Supplemental Material - Supplemental material for Women pay their way on income contingent student debt

Supplemental material, PFE895182 Supplemental Material for Women pay their way on income contingent student debt by Tracey West in Policy Futures in Education

Footnotes

Acknowledgements

The authors would like to acknowledge the reviewers for their highly constructive comments that made this paper more valuable.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.