Abstract

This study aims at enhancing our understanding of criminogenic individual-level factors in white-collar crime, that is, fraudulent acts carried out in an occupational capacity or setting. We do so by examining consistency of rule-violating behaviour across different settings outside the occupational context in a sample of white-collar offenders (n = 637) and comparing it with a matched control group (n = 1809), controlling for socio-demographic, crime and organizational characteristics. Results show that white-collar offenders, including those holding high-trust organizational positions, engaged in regulatory income tax violations and regulatory traffic violations at significantly higher levels than did controls. This study concludes that individual characteristics are likely to underlie the identified cross-contextual consistency in rule-violating behaviour and debates the relevance of the findings for white-collar crime in organizations.

Introduction

A commonly held view in white-collar criminology is that individual involvement in white-collar crime results primarily from differential exposure to criminogenic corporate cultural values and occupational businesses practices (for example, Clinard and Yeager, 1980; Sutherland, 1983), organizational opportunity structures (for example, Benson and Simpson, 2009) or strains (for example, Agnew et al., 2009). The personal and social background of white-collar offenders (traits, states, cognitions) has traditionally been considered to be relatively unimportant or even irrelevant for understanding white-collar crime involvement (Braithwaite, 1984; Coleman, 2002; Sutherland, 1983). Although purely situational explanations are contested on several theoretical and empirical grounds (for example, the inability to account for between-individual differences leading up to differential outcomes in similar criminogenic conditions; Apel and Paternoster, 2009; Hirschi and Gottfredson, 1987, 1989) and a growing body of literature has brought ‘the offender back in’ (Benson, 2013: 324), research has struggled to disentangle the influence of criminogenic contextual forces and criminogenic individual-level factors (but see also, Jones and Kavanagh, 1996; Kish-Gephart et al., 2010).

One way of separating the two factors is by examining consistency in white-collar offenders’ rule-violating behaviour across different contexts outside the occupational and organizational context (Bem and Allen, 1974; Gottfredson and Hirschi, 1990; Junger et al., 2001) and comparing the level of rule-violating behaviour with a control group of individuals with similar socio-demographic backgrounds and organizational positions (Gottfredson and Hirschi, 1990; Herbert et al., 1998; Hirschi and Gottfredson, 1989). If white-collar offenders are overrepresented in rule-violating behaviour in different contexts outside their organizational setting, this would point towards a criminogenic propensity and contest a purely situational approach.

In the present study, we first examine to what extent white-collar offenders exhibit rule-violating behaviour compared with control individuals with matched socio-demographic backgrounds, selected from the general population. The analysis proceeded based on two independent types of rule-violating behaviour outside an organizational context: regulatory income tax violations and regulatory traffic violations. In a next step, we investigate rule-violating behaviour in those white-collar offenders from the sample who had only a single offence registered to their name, allowing us to explore whether these ‘one-shot’ offenders are truly law-abiding citizens and lacking a tendency for deviance altogether, as suggested in literature (for example, Benson and Kerley, 2001; Wheeler et al., 1988). Finally, we examine whether a tendency for rule-violating behaviour is also present in those offenders who occupy high-trust organizational positions, such as director, treasurer or company owner. Because of the assumed criminogenic nature, these positions play a central role in the study of white-collar crime (for example, Cressey, 1953; Sutherland, 1983). However, little attention has been given (a) to possible criminogenic characteristics, such as a tendency to bend or break rules, that select individuals into such high-trust positions, and (b) to interpersonal differences between individuals holding these positions, making some more willing or prone than others to take advantage of criminal opportunities (Apel and Paternoster, 2009; Gottfredson and Hirschi, 1990).

This study contributes to the literature in a number of ways. It is the first study to use a non-criminal outcome measure as a proxy for a criminogenic propensity in white-collar offenders, including those offenders who occupy potentially criminogenic high-trust positions. Also, by examining outcome measures in settings that are characterized by different and typically unrelated contextual influences, the present study helps to disentangle contextual and individual forces. Finally, this is the first study that compares white-collar offenders with a sample of matched controls, based on their socio-demographic characteristics and organizational positions (as suggested by Gottfredson and Hirschi, 1990; Herbert et al., 1998), rather than comparing white-collar offenders with street criminals, as has been done in previous studies (Benson and Kerley, 2001; Weisburd et al., 1991; Wheeler et al., 1988).

Consistency in criminal and deviant behaviour

In order to differentiate between contextual and individual factors, scholars have argued that consistency of criminal and deviant behaviour either over time or across contexts points towards the presence of criminogenic individual-level factors (for example, Bem and Allen, 1974; Caspi and Bem, 1990; Gottfredson and Hirschi, 1990). To date, only a few white-collar crime studies have been able to shed light on such behavioural consistency among white-collar offenders by following their criminal careers over an extensive period of time. These life-course studies reveal that only a minority shows consistency in criminal behaviour, and that most white-collar offenders are characterized by low-frequency offending (Benson and Kerley, 2001; Piquero and Weisburd, 2009; Van Onna et al., 2014; Weisburd and Waring, 2001). However, these studies also indicate that, once criminally active, white-collar offenders show less specialization than is typically thought (Benson and Moore, 1992; Van Onna et al., 2014).

A limitation of assessing criminal histories as a proxy for a criminogenic propensity is that, according to white-collar crime researchers, officially detected and registered offences portray only a part of true misconduct among white-collar offenders (Clinard and Yeager, 1980; Reed and Yeager, 1996; Sutherland, 1940). Self-report studies indicate that ‘true’ misconduct among white-collar offenders, both inside and outside the workplace, may be substantially higher than their criminal record indicates (Menard et al., 2011; Morris and El Sayed, 2013).

To get a fuller understanding of white-collar offenders’ level of misconduct, scholars have urged for the inclusion of non-criminal rule-breaking measures, such as regulatory violations, in the analysis of white-collar offenders’ behaviour (for example, Weisburd and Waring, 2001). Importantly, relatively minor forms of misconduct are hypothesized to provide a better proxy for individuals’ criminogenic propensity than criminal behaviour that is typically more rare (Gottfredson and Hirschi, 1990; Hirschi, 1969; Hirschi and Gottfredson, 1994).

Rule-violating behaviour across contexts

The key assumption in the present paper is that heightened rule-violating behaviour across different contexts – outside an occupational capacity or setting – may signal an underlying criminogenic individual-level factor (Bem and Allen, 1974; Gottfredson and Hirschi, 1990; Junger et al., 2001). Conversely, a lack of such a consistency would support the commonly held view in white-collar criminology that: ‘It would be erroneous to assert that people who engaged in “reckless” activities at work and in certain conditions will do so always and at every phase of their daily life’ (Passas, 1990: 160; see also Braithwaite, 1984; Coleman, 2002).

In order to examine this assumption, we delineated two types of regulatory rule violation: regulatory income tax violations and regulatory traffic violations. We chose these two outcome measures for the following reasons. First, personal income tax violations represent acts of financial-economic misconduct, but these acts are not carried out in an occupational capacity or setting. As such, personal income tax violations fall outside the more narrow definition of white-collar crime that confines it to criminal or regulatory violations that are ‘committed in the course of the occupation’ (Sutherland, 1983: 7; see also, for example, Simpson, 2013). 1 Moreover, the filing of personal income tax is typically not directly influenced by criminogenic cultural values, opportunity structures or strains within organizations, factors that according to the commonly held view in white-collar criminology underlie individuals’ involvement in white-collar crime (see, for example, Braithwaite, 1984; Sutherland, 1983).

Second, in order to investigate whether a tendency for rule-violating behaviour extends outside the realm of financial-economic behaviour, we also examine acts of rule-violating behaviour in traffic. We chose traffic violations because they entail a completely different type of rule-violating behaviour. This approach follows earlier research that suggests that rule-violating behaviour in traffic and crime may both be outcomes of an underlying individual-level factor, such as low self-control or a tendency for risk-taking (Gottfredson and Hirschi, 1990: 92; Junger et al., 2001; Keane et al., 1993).

Lastly, an important, more practical, advantage of including these two types of regulatory violations is that individuals, independent of their occupation, have similar opportunities to violate such rules. Almost all individuals are liable to pay income tax and almost all individuals (can) own and drive cars (for example, 84 percent of Dutch adults have a driving licence; Kennisinsituut voor Mobiliteitsbeleid, 2012).

White-collar offenders: Distinct approaches

Since Sutherland coined the term white-collar crime almost 80 years ago, the question of how to characterize white-collar offenders has been at the centre of much debate. The controversy centres on whether the term should be used based on the nature of the fraudulent offence (for example, Benson and Moore, 1992; Edelhertz, 1970; Weisburd and Waring, 2001), or based on the occupational and organizational characteristics of the person who commits the offence (Sutherland, 1983: 7).

Studies that have taken the fraudulent offence as a starting point typically identify a heterogeneous sample of offenders in terms of types of fraudulent offences and social and criminal background characteristics (Benson and Kerley, 2001; Benson and Moore, 1992; Piquero and Weisburd, 2009; Van Onna et al., 2014; Weisburd and Waring, 2001). In contrast, studies using the so-called offender-based approach take a narrower focus, concentrating on offenders who occupy high-end positions in organizations, such as business owners, directors or treasurers, that bring with them power, responsibility and, above all, trust (Coleman, 2005; Sutherland, 1983). Given the narrower focus, scholars have argued that the two approaches to white-collar crime reflect not only that offenders differ in socio-demographic terms or offence types, but also that the respective white-collar offenders may differ considerably in individual characteristics (Braithwaite, 1985; Croall, 1989; Geis, 2000; Steffensmeier, 1989; but see Ben-David, 1991).

In the present study, both approaches can be identified. The overall sample is based on a selection of individuals who were involved in serious white-collar crime cases, meaning cases in which large amounts of money were defrauded, where offences were complex or organized in nature, or where the offences were committed over an extensive period. However, offenders were selected without taking into account their occupational or organizational position. The overall sample can thus be considered an offence-based sample. In addition, we selected a subsample of white-collar offenders (from the overall sample) who occupy high-trust positions, such as director or business owner, allowing us to investigate whether a tendency to violate rules is present in individuals who occupy potentially criminogenic positions in organizations.

White-collar offenders in high-trust positions

A substantial body of research contends that people may be attracted to and selected into high-trust organizational positions that are compatible with their personal traits (see Apel and Paternoster, 2009). An intriguing possibility proposed by white-collar scholars is that personal characteristics that promote occupational success may also stimulate rule-violating behaviour and even criminal involvement. For example, individuals with a tendency for risk-taking, a characteristic associated with both legitimate and illegitimate success, may be more motivated to occupy high-trust positions and may also be preferred by organizations (Coleman, 2005; Friedrichs, 2010; Wheeler, 1992). Similarly, Gross (1978: 67) argued that those who make it to the top of (large-scale) organizations have ‘distinctive personal characteristics such as ambitiousness, shrewdness and moral flexibility’. From this perspective, individuals in high-trust positions may be expected to have a heightened tendency for rule-violating behaviour. However, a heightened tendency for rule-violating at the top of organizations may also be the result of occupying a high-trust position. Holding a high-trust position that provides power and influence may, for example, make (some) individuals feel they are less dependent on others, increasing the likelihood of rule-violating behaviour, both inside and outside the work environment (Box, 1983: 38). In contrast, Hirschi and Gottfredson (1987) suggest that selection mechanisms hold back individuals with a propensity to violate rules because such individuals do not have the level of self-control necessary to advance upward through the organizational hierarchy and reach high-trust organizational positions, making a tendency for rule-violating behaviour among those in these positions less likely (Hirschi and Gottfredson, 1987; Gottfredson and Hirschi, 1990; Herbert et al., 1998).

Over and above a possible selection or contextual effect, criminologists who focus on individual-level explanations of crime, expect individual differences in rule-violating behaviour among individuals in high-trust positions. For example, Gottfredson and Hirschi (1990; see also Hirschi and Gottfredson, 1987, 1989) expect that the level of self-control is relatively high among individuals who reach high-trust positions, but also that white-collar offenders have relatively low self-control compared with their business peers. Alternatively, white-collar offenders may have a relatively high tendency for risk-taking or possess above average ‘moral flexibility’ (Gross, 1978: 67) or ‘moral insensibility’ (Ross, 1977: 31) compared with other businesspeople in high-trust positions. The few studies that have directly contrasted white-collar offenders with businesspeople in similar organizational positions have identified several personal differences that may be associated with a heightened tendency for rule-violating behaviour, such as low self-control and a greater tendency to disregard rules and social norms (Blickle et al., 2006; Collins and Schmidt, 1993).

Current study and hypotheses

Rule-violating behaviour in white-collar offenders and controls

To date, no study has compared rule-violating behaviour across different contexts among white-collar offenders with control individuals with comparable socio-demographic backgrounds and who occupy similar organizational positions. Previous comparative studies have contrasted white-collar offenders with (non-violent) street-crime offenders. These studies showed that white-collar offenders are less criminally active and exhibit less problematic and deviant behaviour compared with street-crime offenders (for example, Benson and Kerley, 2001; Weisburd et al., 1991; Wheeler et al., 1988). However, these studies shed little light on the matter of whether white-collar offenders have a heightened tendency to violate rules or not. A comparison between white-collar offenders and their peers is called for to establish this (Gottfredson and Hirschi, 1990; Herbert et al., 1998). Because white-collar offenders are often described as conventional or ordinary members of the general population (see Coleman, 2002; Friedrichs and Schwartz, 2008; Wheeler et al., 1988), individuals from the general population are arguably a qualified comparison group for white-collar offenders.

We therefore compare a sample of white-collar offenders with a control group of individuals from the general population. In order to rule out the influence of confounding background characteristics, we matched offenders and controls on socio-demographic background (age, sex, region of residence, business ownership and income). Taking these factors into account, we hypothesize that white-collar offenders show greater involvement in both types of rule-violating behaviour compared with their peers, but we also expect that they are relatively more frequently involved in income tax violations than in traffic violations (Hypothesis 1).

Rule-violating behaviour in one-shot offenders

In order to control for differences in criminal history and to understand whether even ‘one-shot’ white-collar offenders, who are described as lacking a propensity for deviance altogether (Benson and Kerley, 2001; Wheeler et al., 1988), in fact have a tendency for rule violation, we contrast offenders who had only a single white-collar offence registered to their name with their matched peers and with white-collar offenders who had multiple criminal justice contacts. We expect that the ‘one-shot’ offenders commit fewer rule violations across contexts than the offenders with multiple criminal justice contacts, but that they commit more rule violations than matched controls (Hypothesis 2).

Rule-violating behaviour and high-trust positions

We also examine whether individuals in high-trust positions, such as company owner or director, demonstrate a heightened or attenuated level of rule-violating behaviour compared with individuals who do not hold such positions. Given the contradictory theoretical expectations and empirical evidence regarding the (direction of) a potential selection and contextual effect, we do not formulate a specific hypothesis (Hypothesis 3).

In a final analysis, we compare white-collar offenders in high-trust positions with business peers in similar positions, allowing us to control for individual characteristics that may be confounded with holding a high-trust position and for contextual forces prompting or limiting rule-violating behaviour. We hypothesize that white-collar offenders in high-trust positions show higher levels of rule violation across contexts, compared with controls in similar high-trust positions (Hypothesis 4).

Method

Sample

White-collar offender sample

Overall white-collar offender sample

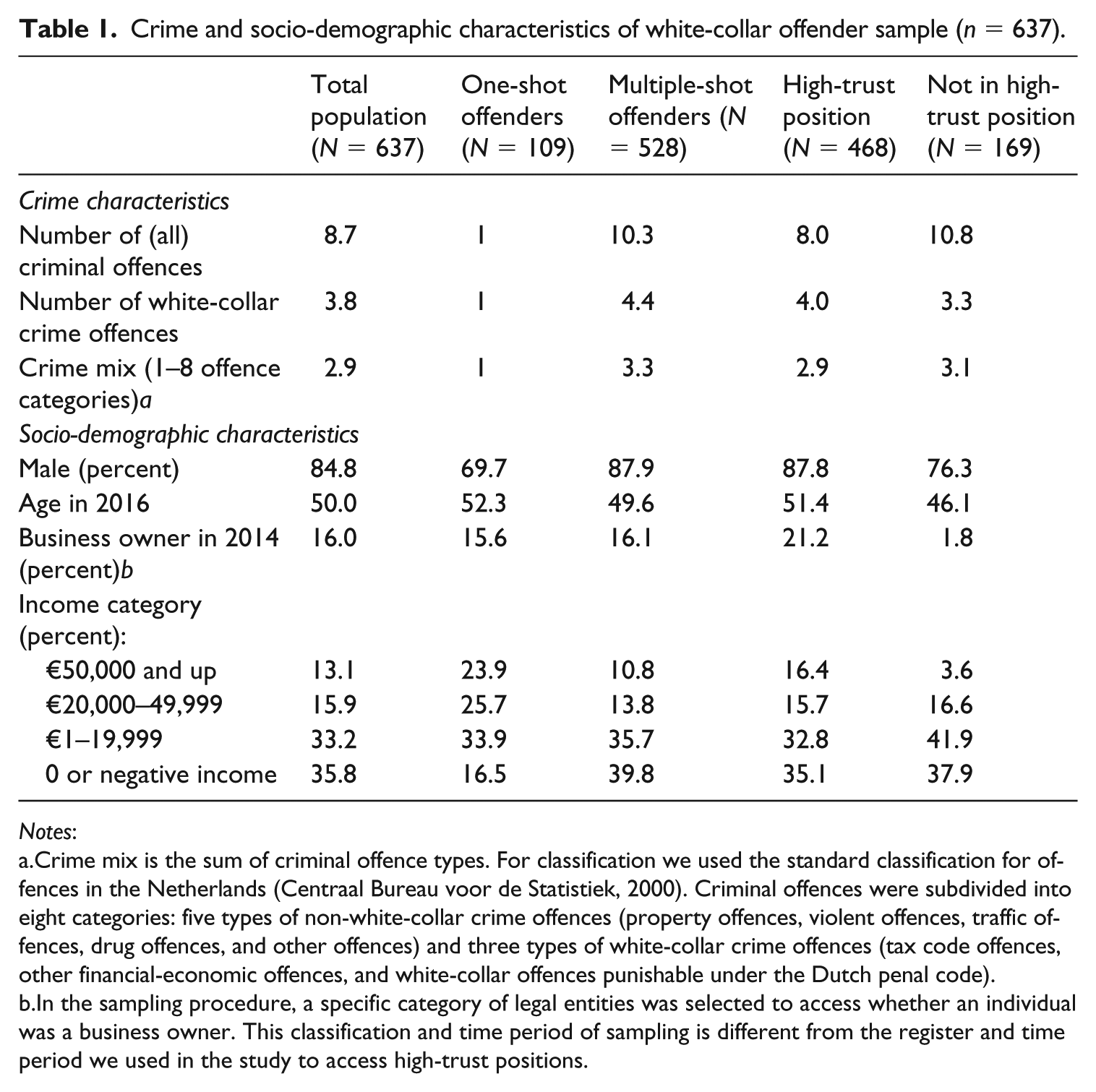

The sample consists of 637 individuals who were prosecuted by the Netherlands Public Prosecution Service for white-collar crime cases between 2008 and 2012 (Van Onna et al., 2014). The sample was not stratified on offence categories but the selection offences broadly fit the offence-based definition of white-collar crime used in prior white-collar crime research (Benson and Kerley, 2001; Benson and Moore, 1992; Weisburd et al., 1991; Weisburd and Waring, 2001; Wheeler et al., 1988). Although the selection offences include a wide range of offences such as ‘contrepreneural’ crimes (for example, swindles against companies; see also Friedrichs, 2010) and intra-organizational ‘occupational’ crimes (for example, large-scale embezzlement; see also Clinard and Quinney, 1973), almost half of all selection offences (44.9 percent) are violations of the criminal tax code (Functioneel Parket, 2012; Van Onna et al., 2014). Closer examination showed that these tax offences are predominantly corporate crimes and turnover tax crimes (Functioneel Parket, 2012). It is important to note that, in contrast to regulatory income tax violations, these violations of the criminal tax code are carried out in an occupational capacity by owners or directors of a company. The selection offences were selected by the Public Prosecution Service for the seriousness of the crime, meaning cases in which large amounts of money were defrauded, where offences were complex or organized in nature, or where the offences were committed over an extensive period (for a more detailed description of the selection offences, see Van Onna et al., 2014; Functioneel Parket, 2012). Table 1 shows the crime and socio-demographic characteristics of the sample. 2

Crime and socio-demographic characteristics of white-collar offender sample (n = 637).

Notes:

. Crime mix is the sum of criminal offence types. For classification we used the standard classification for offences in the Netherlands (Centraal Bureau voor de Statistiek, 2000). Criminal offences were subdivided into eight categories: five types of non-white-collar crime offences (property offences, violent offences, traffic offences, drug offences, and other offences) and three types of white-collar crime offences (tax code offences, other financial-economic offences, and white-collar offences punishable under the Dutch penal code).

. In the sampling procedure, a specific category of legal entities was selected to access whether an individual was a business owner. This classification and time period of sampling is different from the register and time period we used in the study to access high-trust positions.

Sample of one-shot white-collar offenders

To identify offenders who had only one offence registered to their name, we used historical offending information registered in the Judicial Documentation System (JDS) of the Netherlands Ministry of Security and Justice (comparable to ‘rap sheets’). 3 The subsample of offenders with one offence registered to their name (n = 109; 17.1 percent) is considerably smaller than that of offenders with multiple offences registered to their name (n = 528; 82.9 percent). Because the white-collar crime cases for which the offenders were prosecuted (the selection criterion for the present study) typically consist of serious crimes, many offenders were prosecuted for more than one offence. A white-collar offender who had not had a justice contact before the white-collar crime case (the selection criterion for the present study) but was prosecuted for several offences in that case is categorized as an offender with multiple offences. 4

Sample of white-collar offenders in high-trust positions

We selected those offenders from the overall sample who were registered as holding a high-trust white-collar position (between 2010 and 2012) according to the Netherlands Tax and Customs Administration (Chamber of Commerce Register). The most prevalent positions in this register are: (company) director, company owner, sole shareholder, partner, and authorized representative. These positions are held in a private liability company, public company, foundation or other legal entity that is obligated by Dutch law to be registered. The sample consists of 468 white-collar offenders in high-trust positions (73.5 percent of the overall offender sample).

Control group sample

Overall control group sample

The control group (n = 1809) was drawn from the central database of the Netherlands Tax and Customs Administration, which holds all registered individuals and legal entities in the Netherlands (Beheer van Relatie data base). For each white-collar offender, we pair-wise drew three control individuals who matched each offender on five socio-demographic characteristics: age, sex, region of residence in the Netherlands (13 geographical regions), income group (12 groups) and whether they had a company registered to his/her name. 5 The income of offenders was established using the mean reported income to the Netherlands Tax and Customs Administration over the years 2008–10. Subsequently, 12 income groups were established, each consisting of at least 20 individuals (n = 20). 6 These five characteristics were then used to form a key for each offender. For example: a male, born in 1961, living in the north of the Netherlands, income group €40,000–49,999, with a company registered to his name. This key was then used to randomly select individuals who matched these five characteristics from the central database. 7

Control group for one-shot white-collar offenders

The pair-wise sampling also allowed us to establish a matched control group (with the same five socio-demographic characteristics) for the ‘one-shot’ white-collar offender subgroup (n = 321; 17.7 percent) and the multiple-shot offender subgroup (n = 1488; 82.3 percent).

Control group for offenders in high-trust positions

We selected from the overall control group those individuals who were registered as holding a high-trust white-collar position (between 2010 and 2012) according to the Netherlands Tax and Customs Administration Chamber of Commerce Register). The number of control individuals occupying high-trust positions is 744 (41.1 percent of the overall control group sample).

Dependent variables

Regulatory income tax violations

Data on regulatory income tax violations were gathered from the Netherlands Tax and Customs Administration for a seven-year period (2006–12). We used the aggregated data of two types of regulatory violations for income tax that are registered by the Netherlands Tax and Customs Administration: omission violations for less serious tax violations where the Netherlands Tax and Customs Administration does not assume intent, and transgression violations for serious, deliberate tax violations. 8

Regulatory traffic violations

Data on traffic violations were obtained from the Netherlands Central Fine Collection Agency (CJIB), which registers all traffic violations in the Netherlands. 9 For this study, we used the regulatory traffic violations for an 11-year period (2003–13) that were registered in the central register in 2013. The most common traffic violations are: driving with an expired test certificate, speeding, using a cell phone while driving, and driving through a red light.

Analytic plan

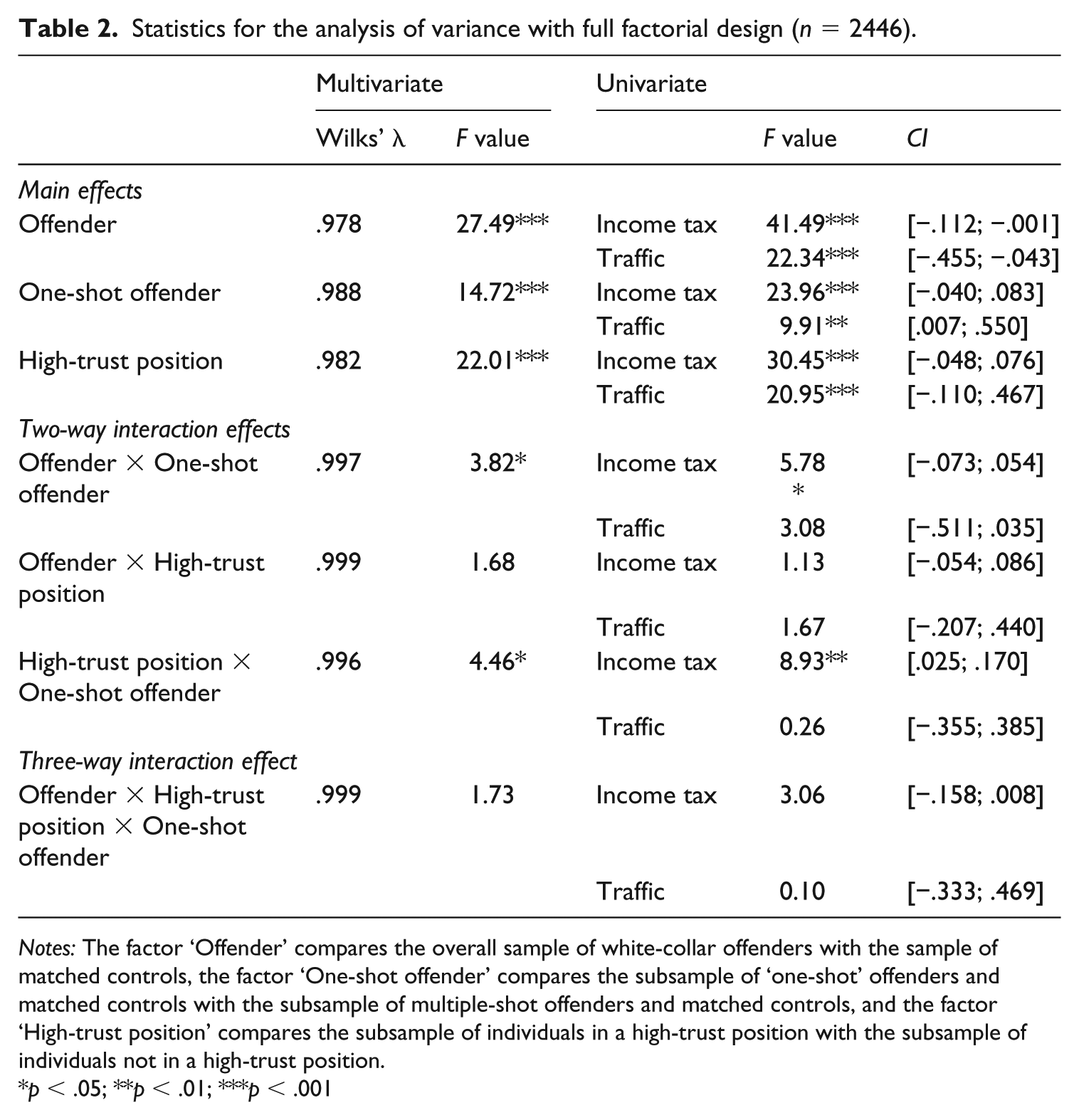

The analytic plan consisted of two steps. In the first step, we conducted an analysis of variance (MANOVA) on income tax violation and traffic violation, with a 2 (offender – control group) by 2 (one-shot offenders [and controls] – multiple-shot offenders [and controls]) by 2 (high-trust positions – no position) with a full factorial design. The results give an overview of the effects of the three independent variables and their interactions on rule-violating behaviour.

In the second step, we conducted analyses of variance to separately test the four hypotheses: offenders are over-involved in rule-violating behaviour compared with controls (Hypothesis 1); one-shot offenders commit fewer rule violations than offenders with multiple criminal justice contacts, but commit more rule violations than matched controls (Hypothesis 2); rule violations among individuals in high-trust positions differ from individuals who do not hold such positions (Hypothesis 3); offenders in high-trust positions show higher levels of rule violation compared with controls in similar high-trust positions (Hypothesis 4).

Because the assumption of homogeneity of the covariances for the analyses of variance was not met (BOX M-tests, p’s < .001), we report the bootstrapped confidence intervals for all analyses to provide a more robust estimate of the effect (n = 1000; 95 percent).

Results

The results from the full factorial analysis of variance are presented in the first section and the results for Hypotheses 1 to 4 are detailed in the second section.

Full factorial analysis

The effects of the analysis of variance with a full factorial design are reported in Table 2. The results show strong multivariate and univariate main effects and some multivariate and univariate interaction effects. However, not all effects met the bootstrap criteria in the full factorial model, suggesting that the distribution of rule-violating behaviour may have caused some of the effects. The main effect regarding the first and central hypothesis of this study, that offenders differ from matched controls in rule-violating behaviour, met the criteria. 10

Statistics for the analysis of variance with full factorial design (n = 2446).

Notes: The factor ‘Offender’ compares the overall sample of white-collar offenders with the sample of matched controls, the factor ‘One-shot offender’ compares the subsample of ‘one-shot’ offenders and matched controls with the subsample of multiple-shot offenders and matched controls, and the factor ‘High-trust position’ compares the subsample of individuals in a high-trust position with the subsample of individuals not in a high-trust position.

p < .05; **p < .01; ***p < .001

Hypotheses

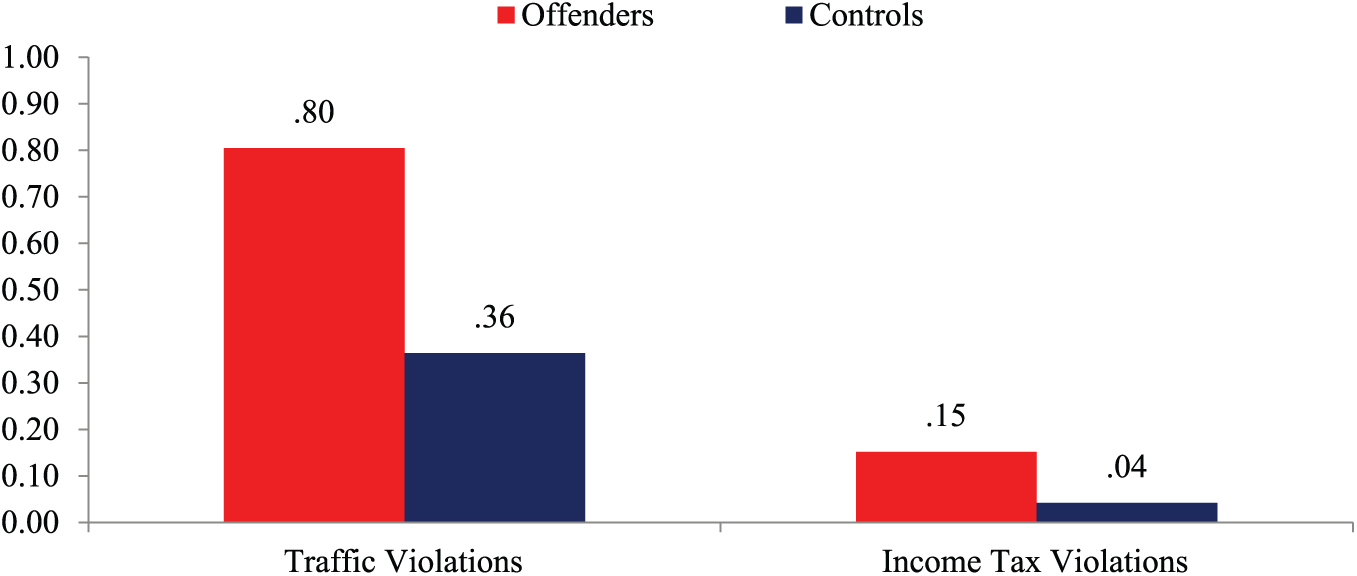

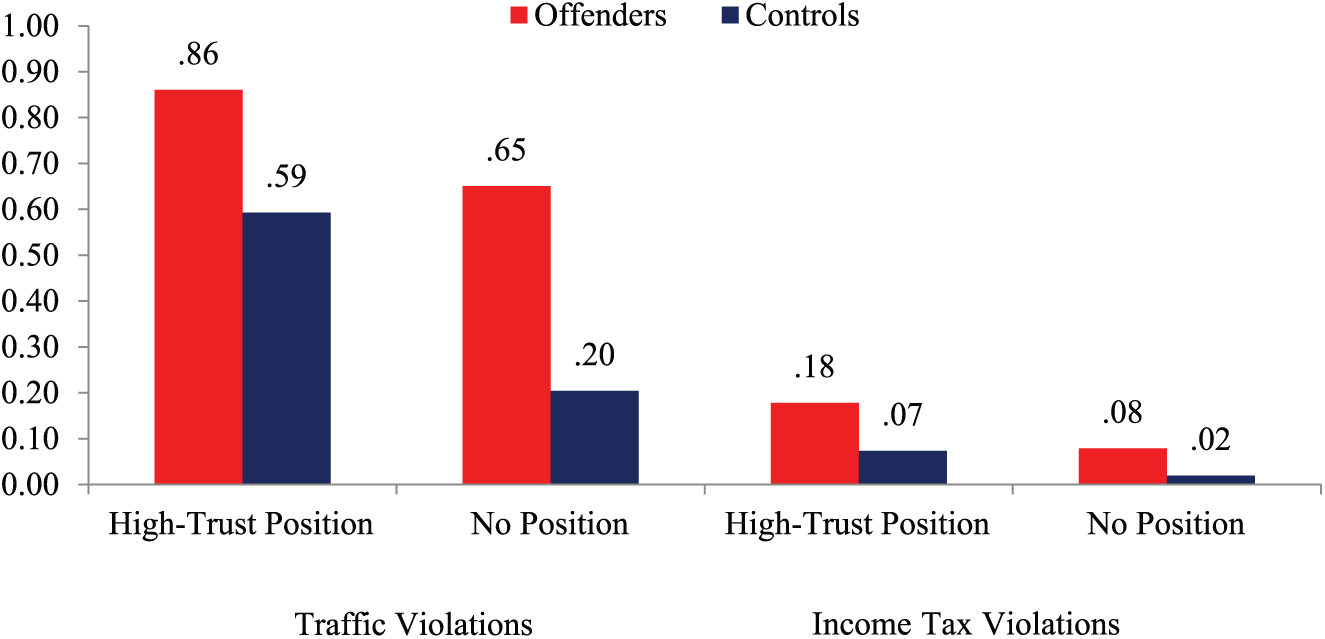

Below, we report the results of the separate analyses to test the four hypotheses. Figures 1 and 2 visually depict the main results regarding the hypotheses.

Average number of traffic violations and income tax violations per year for white-collar offenders and controls (n = 2446).

Average number of traffic violations and income tax violations per year for white-collar offenders and controls in high-trust positions and not in high-trust positions (n = 2446).

Rule-violating behaviour in white-collar offenders and controls

The full factorial analysis of variance shows that rule-violating behaviour differed between offenders and controls. A separate analysis of variance testing Hypothesis 1 confirms this result: Wilks’ λ = .896; F (2, 2443) = 142.49, p < .001. Figure 1 depicts the average number of traffic violations and income tax violations per year in white-collar offenders and control individuals with similar socio-demographic backgrounds. It shows (univariate results) that white-collar offenders were over-involved in traffic violations (M = 0.80, SD = 1.32), F (1, 2444) = 106.71, p < .001; CI = [−.550; −.335] and income tax violations (M = 0.15, SD = 0.21), F (1, 2444) = 230.77, p < .001; CI = [−.128; −.093] compared with controls (M = 0.36, SD = 0.74; M = 0.04, SD = 0.13, respectively). Results thus confirm Hypothesis 1: white-collar offenders were over-involved in both types of rule violation, but were relatively more frequently involved in income tax violations.

Rule-violating behaviour in one-shot offenders

In order to test the differences between (1) ‘one-shot’ offenders and multiple-shot offenders, and between (2) ‘one-shot’ offenders and matched controls, we performed two additional MANOVA’s. The first analysis shows that ‘one-shot’ offenders differed in rule-violating behaviour compared with offenders with multiple offences registered to their names: Wilks’ λ = .966; F (2, 634) = 11, 16, p < .001. 11 In support of the first part of the second hypothesis, univariate results show that ‘one-shot’ offenders were less involved in traffic violations (M = 0.55, SD = 0.88), F (1, 635) = 4.89, p < .05; CI = [.082; .517] and in income tax violations (M = 0.07; SD = 0.15), F (1, 635) = 19.85, p < .001; CI = [.063; .131] than were white-collar offenders with multiple offences registered to their name (M = 0.86, SD = 1.38; M = 0.17, SD = 0.21, respectively).

Regarding the second part of this hypothesis, the results show that ‘one-shot’ offenders differed in rule-violating behaviour from matched controls: Wilks’ λ = .945; F (2, 427) = 12.35, p < .001. In line with the hypothesis, univariate findings display that matched controls were under-involved in both traffic violations (M = 0.30, SD = 0.55), F (1, 428) = 12.28, p < .01; CI = [−.439; −.061] and income tax violations (M = 0.02, SD = 0.10), F (1, 428) = 14.48, p < .001; CI = [−.078; −.019] compared with ‘one-shot’ offenders.

Taken together, the results confirm Hypothesis 2: ‘one-shot’ offenders committed fewer rule violations than did white-collar offenders who had multiple criminal justice contacts, but they committed more rule violations than matched controls with a comparable socio-demographic background.

Rule-violating behaviour in high-trust positions

The full factorial analysis of variance (Table 2) shows inconclusive results regarding the relationship between high-trust position and rule-violating behaviour (Hypothesis 3). A separate analysis of variance shows that individuals in high-trust positions differed from individuals not occupying such positions in rule-violating behaviour: Wilks’ λ = .903; F (2, 2443) = 130.49, p < .001. 12 Univariate results show that individuals in high-trust positions showed higher levels of traffic violation (M = 0.69, SD = 1.18), F (1, 2444) = 133.99, p < .001; CI = [.358; .510] and income tax violation (M = 0.11, SD = 0.20), F (1, 2444) = 179.67, p < .001; CI = [.074; .100] compared with individuals who do not occupy a high-trust position (M = 0.27, SD = 0.57; M = 0.03, SD = 0.10, respectively).

To test Hypothesis 4 we performed a MANOVA. Results, as depicted in Figure 2, show that white-collar offenders in high-trust positions were over-involved in rule-violating behaviour compared with their business controls: Wilks’ λ = .931; F (2, 1209) = 44.64, p < .001. 13 Univariate results show that white-collar offenders in high-trust positions committed significantly more traffic violations, F (1, 1210) = 15.00, p < .001; CI = [−.414; −.128] and more income tax violations, F (1, 1210) = 84.03, p < .001; CI = [−.127; −.080].

Taken together, although the results of the full factorial model are inconclusive about the relationship between high-trust position and rule violation, the findings of the separate analysis show that high-trust positions were associated with increased levels of rule-violating behaviour (Hypothesis 3). Moreover, results show that white-collar offenders in high-trust positions were over-involved in rule-violating behaviour compared with matched controls, confirming Hypothesis 4.

Discussion

This paper started out with the notion that white-collar crime is typically understood to be a result of criminogenic work-related environments in which individual differences have little importance or relevance. The present study examines this convention by exploring whether white-collar offenders exhibit rule-violating behaviour in different contexts (outside the organizational context), as a proxy for a criminogenic propensity, and compares these outcomes with a matched control sample selected from the general population, while taking into account socio-demographic, crime and organizational characteristics. Several key findings emerge from this study.

Results clearly show that white-collar offenders exhibited a heightened tendency for rule-violating behaviour. Controlling for differences in socio-demographic background, our results show that white-collar offenders were over-involved in income tax violations and traffic violations compared with controls selected from the general population. Contrary to what is suggested by prior theorizing, even ‘one-shot’ offenders showed an elevated tendency for rule-violating behaviour (Benson and Kerley, 2001; Weisburd and Waring, 2001; Wheeler et al., 1988). These results suggest that the traditional stereotype of white-collar offenders as law-abiding members of society may need adjustment.

We also found that white-collar offenders in high-trust positions, such as director, commissioner or treasurer, exhibited significantly higher levels of cross-contextual rule-violating behaviour than controls in these positions. This finding is consistent with theory and research that suggests that meaningful personal and psychological differences exist between white-collar offenders and business peers in similar positions (Blickle et al., 2006; Collins and Schmidt, 1993; Herbert et al., 1998; Hirschi and Gottfredson, 1987, 1989).

Importantly, the analyses pertained to two different and unrelated types of rule-violating behaviour. The analyses for income tax violations showed that white-collar offenders were more likely to engage in rule-violating behaviour that is related to the financial-economic realm but is not carried out in an occupational capacity or setting. The analyses for traffic violations showed that white-collar offenders were also more likely to display rule-violating behaviour that reflects a completely different type of misconduct. This behavioural consistency indicates that factors that remain stable across different contexts, such as offender characteristics, are important in explaining the identified rule-violating behaviour (Bem and Allen, 1974; Gottfredson and Hirschi, 1990).

In sum, our findings clearly support the idea that personal characteristics underlie the identified rule-violating behaviour in white-collar offenders, including ‘one-shot’ offenders and those holding high-trust positions in organizations. This finding is in line with the growing body of research that suggests that individual-level factors are highly relevant in unravelling the aetiology of white-collar crime (for example, Alalehto, 2003; Benson and Manchak, 2014; Eaton and Korach, 2016; Elliot, 2010; Perri, 2011; Ragatz and Fremouw, 2010; Walters and Geyer, 2004). Although rule-violating behaviour in this study is restricted to regulatory violations outside the occupational and organizational context, a tendency of individuals to break rules is likely to be important in deviant and criminal behaviour in a work-related context as well. For example, offenders who have a tendency to break rules may be more willing to take advantage of opportunity structures (Benson and Simpson, 2009), be more receptive to unethical business cultures (Kish-Gephart et al., 2010) or align their personal goals more easily with criminogenic corporate goals (Gross, 1978). Also, individuals at the top of organizations with such a tendency may not only directly affect the executive and managerial decision-making process but also contribute to an unethical business climate in the organization (Apel and Paternoster, 2009; Schwartz et al., 2005). Empirical support for the association between transgressions outside the business environment and work-related deviance and crime comes from recent studies that found a positive relationship between executives’ rule violation outside the business environment (for example driving under the influence, speeding, domestic violence) and the propensity to exploit and trade on insider information (Davidson et al., 2015), and between CEOs’ and CFOs’ ‘off-the-job’ misconduct and the propensity to misreport financial statements (Davidson et al., 2016).

In closing, we address a number of limitations of the present study and outline our future research plans. First, even though the matched control group design allowed us to rule out several confounding variables, we cannot fully exclude the possibility that unobserved contextual factors may have contributed to the identified elevated rule-violating behaviour in white-collar offenders. One such factor is the probability of being audited or sanctioned by the Netherlands Tax and Customs Administration, which may differ between offenders and controls (or, for that matter, between individuals in high-trust positions and individuals who do not occupy these positions). However, this potential bias cannot account for the identified consistency with elevated traffic violations, a consistency that is in line with individual-level explanations of deviance and crime. Second, some of the measurements we used, such as officially registered reported income, may be incomplete. We also were not able to access certain possibly important conditions, such as the size of the organizations the high-trust positions were held in. Third, white-collar offenders in our sample may not be representative of the population of white-collar offenders in the Netherlands for two reasons: the sample consisted of detected and prosecuted offenders (who may not be representative of undetected offenders), and these offenders were involved in serious white-collar crime cases. 14 The sample may not be representative of offenders who are involved in minor white-collar offences. Lastly, because the control samples are linked through socio-demographic profiles to the offender sample, the controls are not necessarily representative of the general population in the Netherlands, or of the population of individuals who occupy high-trust positions. However, despite these potential weaknesses, we believe that the study, with its rarely used comparative research design and unique data, has several desirable characteristics not often encountered in white-collar crime studies, and we have no grounds to assume that the limitations influenced our conclusions in a meaningful way.

Despite these limitations, findings in this study warrant further research into the nature and role of individual-level factors in white-collar offenders. In future research we plan to focus on an individual-level factor that has largely been neglected in the study of white-collar crime: weakened or broken bonds to conventional society (Hirschi, 1969; Sampson and Laub, 1993). We feel this research can critically advance our understanding of the complex role of individual-level factors in white-collar crime involvement.

Footnotes

Acknowledgements

We would like to thank Wim Huisman at VU University Amsterdam and the anonymous reviewers for their helpful comments.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.