Abstract

In this article, we depart from prior research, which has typically focused on the acquiring firm CEO, and adopt a behavioral agency perspective to examine how self-interested target CEOs’ equity wealth shapes acquisition premium decisions. We argue that deal-specific windfall gains upon the acquisition announcement trigger immediate upward shifts in CEOs’ reference points, heightening risk aversion and motivating value-preserving behavior. Using a sample of 435 acquisitions from 1994 to 2020, we find that larger windfall gains are associated with smaller increases in final acquisition premiums. The type of prospective wealth available to the CEO moderates this effect: organizational prospects, such as strong revenue growth, weaken the pull of loss aversion and encourage more aggressive bargaining, whereas personal prospects, such as post-acquisition retention, amplify loss aversion. Our findings highlight the behavioral consequences of sudden wealth shocks and reveal how different forms of prospective value shape target CEOs’ influence over acquisition outcomes.

Introduction

Corporate governance research has long focused on how equity-based compensation can be used to reduce managerial agency costs (Eisenhardt, 1989; Jensen and Meckling, 1976). Agency costs partly stem from the risk differential between diversified, risk-neutral shareholders and risk-averse CEOs, whose personal wealth is often tied to firm performance. To align the interests of CEOs with those of shareholders, boards often use equity incentives such as stock options (Sanders and Hambrick, 2007), as they provide upside potential with limited downside risk. Subsequent work, adopting a behavioral perspective, challenges the view that stock options unconditionally increase CEO risk-taking (Wiseman and Gomez-Mejia, 1998). This view suggests that CEOs anchor on accumulated stock option wealth as a reference point, weighing the risk of losing current gains against the potential for future rewards (Kahneman and Tversky, 1979; Martin et al., 2013). Inherent to this logic is the assumption that CEOs’ reference points shift gradually in tandem with performance-based accumulation of stock option wealth.

While this model has advanced our understanding of CEO risk-taking, it overlooks a distinct and underexplored psychological mechanism: sudden windfall gains. Defined as unexpected, substantial increases in personal wealth due to external events, windfall gains may trigger an immediate, rather than incremental, shift in a CEO’s reference point. Unlike the gradual wealth accumulation examined in much of the behavioral agency literature (e.g. Benischke et al., 2019), which allows for measured recalibration of CEO risk-taking preferences over time, windfall gains provoke a sharp re-anchoring. Rather than adjusting incrementally, CEOs psychologically anchor to a new, much higher baseline of personal stock option wealth, even if it has not yet been realized. This sharp re-anchoring likely triggers heightened risk aversion, as the CEO becomes motivated to protect the gain already in hand rather than pursue further, uncertain returns. This suggests that reference points are not only shaped by historical performance, but are also highly sensitive to the timing, magnitude, and origin of gains, highlighting the need for a more dynamic, event-contingent view of risk behavior in CEO strategic decision-making.

A particularly salient context in which CEOs experience such windfall gains is M&As. Target firm CEOs especially often experience sudden gains in their stock option wealth when they become the target of an acquisition attempt (Hartzell et al., 2004). The extent to which target firm CEOs experience such deal-specific windfall gains, which we define as the gains in their personal equity wealth associated with increases in their firm’s underlying share price following the public announcement of the bid, depends on (1) the premium initially offered by the bidder and (2) the degree to which their compensation is tied to movements in the firm’s share price through equity grants such as shares and stock options (Hartzell et al., 2004; Jenter and Lewellen, 2015). Based on the logic above, we propose that target firm CEOs who experience larger gains in their equity wealth at the time of acquisition announcement prefer to forfeit the risky but potentially lucrative option of attempting to maximize the acquisition premium to prevent a loss in equity wealth. This should be reflected in a smaller difference between the initial premium offered and the final premium paid by the bidder. 1 By doing so, target firm CEOs protect any personal deal-specific gains due to increases in their firm’s share price following the bid.

We further explore the boundary conditions of our theory by examining how different forms of prospective value shape CEO responses to windfall gains. Behavioral agency theory often assumes a stable trade-off between current wealth and future upside (Martin et al., 2013), but in acquisition settings, CEOs must navigate distinct types of future value. We distinguish between organizational prospects (e.g. strong revenue growth) and personal prospects (e.g. anticipated retention), which may have opposing effects based on our theory. We hypothesize that organizational prospects elevate the CEO’s aspirations and reduce the relative importance of securing immediate gains, encouraging more aggressive bargaining. Although strong performance also benefits shareholders, it raises the CEO’s performance-based aspirations and increases the perceived opportunity cost of accepting a suboptimal premium. In contrast, we hypothesize that personal prospects make future rewards contingent on deal completion (Bilgili et al., 2017; Hambrick and Cannella, 1993), heightening risk aversion and promoting deal-preserving behavior. This divergence emphasizes the importance of what kind of value is at stake in shaping how CEOs manage windfall shocks. We test our framework using 435 domestic U.S. acquisitions completed between 1994 and 2020 and find support for our predictions.

This study contributes to a broader understanding of incentive alignment by showing that equity-based incentives, often viewed as tools to align CEO and shareholder interests, can, under certain conditions, generate unintended behavioral consequences when they generate sudden, deal-specific windfall gains. While traditional agency theory assumes that equity ownership promotes risk-taking aligned with shareholder interests (e.g. Eisenhardt, 1989; Jensen and Meckling, 1976), and behavioral agency theory highlights gradual shifts in risk preferences based on accumulated wealth (Wiseman and Gomez-Mejia, 1998), we introduce windfall gains as a distinct, event-driven anchoring mechanism. These externally triggered and unanticipated increases in CEO personal wealth, such as those resulting from acquisition bids, abruptly reset reference points and heighten risk aversion, leading to a preference for value preservation over further value maximization. Importantly, departing from prior work (Martin et al., 2013), we demonstrate that this effect is not uniform but depends on the type of prospective value CEOs face. Organizational prospects, such as strong revenue growth, shift attention toward future firm-based upside and mitigate risk aversion, encouraging assertive bargaining. In contrast, personal prospects, such as anticipated post-merger retention, compound the stakes and reinforce loss-averse CEOs’ preference for certainty and deal completion. In the M&A context, our theory, thus, suggests that the behavioral impact of windfall gains depends not only on their magnitude but also on how CEOs weigh current versus prospective wealth. This offers more nuance to understanding the interplay between prospective and current wealth.

Finally, we contribute to M&A research by foregrounding the behavioral dynamics of the public pre-deal phase; a critical, but understudied period in which deal terms are actively negotiated (Graebner and Eisenhardt, 2004; Pavicevic et al., 2023; Welch et al., 2020). Focusing on changes in the acquisition premium between the initial offer and the final agreement, we reveal that target CEO-driven variance in this phase is systematic, not random. Our findings suggest that target CEO preferences meaningfully influence acquisition outcomes, and that accounting for windfall-induced behavioral shifts is essential for understanding how and why final premiums deviate from initial offers. Indeed, our findings suggest that this distinction is important since premia, on average, increased by 14% during the public takeover phase in our sample, and these changes are not distributed randomly.

Theoretical background and hypotheses

Corporate governance research has long emphasized the use of equity-based compensation to mitigate agency costs by aligning CEO risk-taking preferences with those of shareholders (Eisenhardt, 1989; Jensen and Meckling, 1976). The central problem arises from the structural mismatch between risk-neutral shareholders—who diversify their investments—and CEOs, whose human and financial capital is concentrated in a single firm (Holmstrom, 1979). This results in CEOs being naturally risk averse, meaning that they tend to avoid risky strategic choices that could benefit shareholders but may threaten their personal wealth. To address this, boards commonly use stock options, assuming that such instruments incentivize CEOs to pursue value-enhancing, higher-risk strategies (Sanders and Hambrick, 2007). Positive agency theorists would argue that because stock options involve no upfront investment and do not need to be exercised, they expose CEOs to minimal downside risk while offering unlimited upside potential and, thus, encourage greater CEO risk-taking (Hall and Murphy, 2002).

Behavioral agency theorists, however, argue that including stock options may increase agency costs. Specifically, behavioral agency theory departs from agency theory by replacing the assumption that managerial agents are risk averse—always preferring less risk to more—with the empirically grounded assumption of loss aversion (Kahneman and Tversky, 1979). The concept of loss aversion is derived from prospect theory and suggests that CEOs will take less risk in gain contexts but are willing to take additional risk in situations wherein they are confronted with certain losses, that is, loss contexts (Kahneman and Tversky, 1979). Loss aversion has been integrated into the BAM through the concept of risk-bearing—or personal wealth at risk of loss. In addition to the CEO’s human capital that is tied to the success of the focal firm, risk-bearing also results from the accumulation of personal wealth, for example, in the form of assured future income. Equity risk-bearing refers specifically to the equity portion of the CEO’s personal wealth, including the CEO’s stock holdings (Beatty and Zajac, 1994; Benischke et al., 2019; Martin et al., 2013). This wealth equates to prospective losses in the event of failed risk-taking due to declines in the firm’s share price, given the correlation between the CEO’s equity wealth and the firm’s share price. This situation has been described as the agency problem of risk sharing, meaning that the CEO and shareholders share the risk of firm performance declines (Hall and Murphy, 2002; Holmstrom, 1979).

While positive agency scholars tend to focus on the upside potential of risk sharing (Eisenhardt, 1989), risk sharing may be problematic because it leads to an even greater concentration of personal wealth in the focal firm (Holmstrom, 1979). In other words, behavioral agency scholars argue that CEOs subjectively interpret gains and losses relative to personal wealth at risk over time (Martin et al., 2013). Accordingly, because CEOs with higher equity risk-bearing will experience a greater loss of wealth in the event of failed firm risk-taking, BAM posits that managerial agents are expected to avoid additional risk-taking as their equity risk-bearing—or wealth at risk of loss—increases (e.g. Benischke et al., 2019, 2020; Devers et al., 2008; Martin et al., 2013). For example, Larraza-Kintana et al. (2007) find that stock option wealth is negatively related to managerial risk-taking, as reflected, among others, in lower R&D spending, fewer entries into new product markets, or less acquisition activity.

Recent extensions of the BAM incorporate the logic of mixed gambles, which further nuance how CEOs evaluate risk under conditions of wealth accumulation. This line of work argues that CEOs do not assess prospective gains and losses in isolation but consider them jointly—as a mixed gamble—when evaluating risky choices (Martin et al., 2013). Building on BAM’s core assumption that CEOs psychologically endow their existing equity wealth, treating it as a reference point against which the potential outcomes of strategic decisions are assessed, the mixed gambles perspective argues that the prospect of additional gains is often weighed against the potential loss of already accrued wealth, reinforcing a preference for risk avoidance. However, implicit in this literature is the assumption that reference points shift gradually through performance-linked equity accumulation. In most strategic decisions examined in the behavioral agency literature, both the magnitude and timing of potential gains and losses remain uncertain. Such decisions unfold over time and depend on the evolution of market conditions, competitive responses, and broader environmental developments. For example, investments in R&D may yield significant long-term gains or may fail entirely, and CEOs cannot know in advance how those outcomes will evolve (Benischke et al., 2019; Devers et al., 2008; Larraza-Kintana et al., 2007). As a result, CEOs do not know ex ante how much they stand to gain or lose, and their wealth adjusts gradually as performance information becomes available (Andrei et al., 2024). This gradual pattern reflects the nature of the settings typically studied in BAM research, rather than a theoretical requirement that reference points must always evolve slowly.

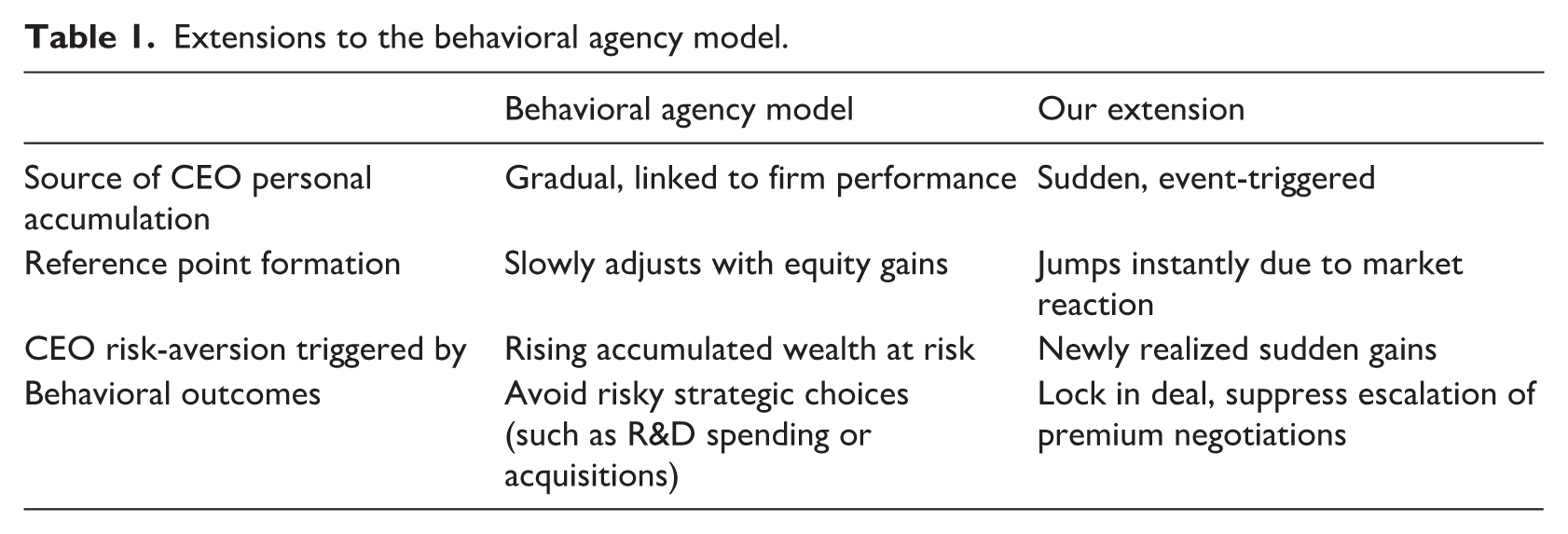

We challenge this assumption by theorizing that sudden, exogenous windfall gains—such as those associated with sudden gains in the target CEO’s stock option wealth when targeted for an M&A—provoke an immediate and discrete upward shift in CEOs’ reference points. These sharp gains can trigger a heightened risk aversion response that is not simply an extension of past performance, but a reactive behavioral shift toward preserving the newly acquired wealth. This dynamic remains underexplored and presents a critical gap in understanding CEO behavior under event-driven conditions (see Table 1) (see Note 1).

Extensions to the behavioral agency model.

By contrast, acquisition announcements create a situation in which the CEO can identify very clearly the specific amount of endowed wealth that would be lost if the deal were to collapse. This known downside exposure creates a sharper and more immediate adjustment of the CEO’s reference point than the uncertain and incremental adjustments associated with performance-based wealth accumulation in prior studies. Furthermore, unlike most strategic decisions where CEOs remain in their role regardless of outcomes, acquisition settings introduce a credible possibility of job loss, diminished future income, and reduced career opportunities if negotiations deteriorate or the bid fails (Hambrick and Cannella, 1993; Harford and Schonlau, 2013). This potential discontinuity in employment amplifies the personal salience of the endowed gain and further distinguishes this context from routine strategic risk-taking.

Taken together, these characteristics suggest that M&As provide a particularly compelling context to examine how equity-based incentives influence CEO behavior, not only because of the high financial stakes involved, but also because of the personal consequences target CEOs face during these transactions. The idea that self-interested CEOs use acquisitions to maximize personal gain is well established (Gamache et al., 2019), particularly in research on acquiring firms (Devers et al., 2013; Trautwein, 1990). This literature documents how CEOs may pursue acquisitions to increase compensation (Schmidt and Fowler, 1990), reduce employment risk (Gomez-Mejia and Wiseman, 1997), or expand firm size (Wowak et al., 2017). These behaviors have been mainly explained through a private interest perspective, which builds on agency logic to highlight how CEOs’ personal incentives, often structured through equity-based compensation, can distort value-maximizing acquisition decisions (Benischke et al., 2020).

While insightful, this perspective has focused almost exclusively on acquiring firm CEOs, often portraying target firm CEOs as passive participants or neutral facilitators of the transaction. For example, Spraggon and Bodolica (2011) acknowledge that a common limitation of this literature is that these studies tend to assume away the “bargaining power of target CEOs who may engage in despicable trade-offs between their personal benefits and target shareholders’ gains obtained from the transaction” (p. 215). Nonetheless, much of this work neglects growing evidence that target firm CEOs can, and do, shape acquisition outcomes in meaningful ways (e.g. Boone and Mulherin, 2007; Graebner and Eisenhardt, 2004). Unlike their acquiring counterparts, target CEOs often face the loss of their position and status after deal completion (Hambrick and Cannella, 1993), which may increase their motivation to act opportunistically. They may also have more latitude to do so, as they are less constrained by the need to manage a post-merger integration process or secure a long-term managerial mandate (Lehn and Zhao, 2006). Critically, it is target firm CEOs who typically experience windfall gains, as acquisition announcements frequently result in substantial increases in the target firm’s stock price, dramatically boosting the value of the CEO’s equity wealth. These gains are sudden, externally triggered, and often unrelated to the CEO’s prior performance, making them especially likely to re-anchor the CEOs’ reference point and activate loss-averse behavior.

However, even the few empirical studies that have examined how target firm CEOs benefit personally from M&As and the implications for shareholder outcomes have primarily been treated as incidental or background conditions. Most notably, Hartzell et al. (2004) show that target CEOs receiving special benefits, such as augmented golden parachutes, merger bonuses, or post-merger employment, tend to accept lower takeover premiums, suggesting a trade-off between personal gain and shareholder value. Building on this, Fich et al. (2011) find that over 13% of target firms grant their CEOs unscheduled stock options during confidential merger negotiations, and that such grants are associated with higher deal completion likelihoods but significantly lower acquisition premiums, effectively transferring value from target to bidder shareholders. Similarly, Fich et al. (2013) demonstrate that larger and more important golden parachutes increase the likelihood of deal completion but are also associated with lower takeover premiums, reinforcing concerns about the moral hazard posed by target CEO incentives. While these studies emphasize the role of special acquisition-related benefits in shaping merger outcomes, particularly through mechanisms that substitute for or amplify standard contractual incentives, they do not theorize the role of the above-mentioned windfall gains and target CEO’s behavioral response that such gains may prompt.

Moreover, the dominant assumption across these studies is that the key CEO-influenced decisions occur during private, pre-announcement deal structuring. As such, they implicitly assume away the possibility that the acquisition premium itself may be subject to strategic negotiation after the bid is made public, during the critical public pre-acquisition phase. Hence, while prior work has considered the distributional implications of privately negotiated benefits, it has paid little attention to how large, exogenously triggered equity gains may recalibrate target CEOs’ risk preferences and influence their behavior during the public pre-acquisition phase, when key deal terms, including the final acquisition premium, are still subject to negotiation.

The M&A setting, therefore, offers an ideal context to explore how sudden windfall gains, triggered by an acquisition offer, can rapidly shift target CEOs’ reference points and trigger behavioral responses that deviate from shareholder value maximization. In what follows, we develop a theoretical framework that builds on the BAM to explain how and why such windfall-induced shifts affect acquisition outcomes.

CEO equity risk-bearing and acquisition premiums

Prior research has shown that when a firm receives an acquisition bid, its share price increases, and this increase is mainly determined by the size of the acquisition premium offered by the bidder (Huang and Walkling, 1987; Jensen and Ruback, 1983). After receiving a bid, target firm CEOs may choose to respond in one of two ways: they can try to push for a higher premium by engaging in aggressive negotiations with the bidder, or they may seek instead to swiftly complete the deal by accepting the offered premium as is or with limited negotiations. Pushing for a higher acquisition premium may seem initially appealing because any subsequent share price gains may translate into additional gains in personal wealth for the CEO. Yet, insisting on a higher premium can potentially discourage the acquiring party from completing the deal if it believes it overpays for the target (Jacobsen, 2014). Specifically, because a given deal will only create value for the acquirer as long as the synergistic potential of the deal exceeds the premium paid for it (Schijven and Hitt, 2012), there is a limit to how much an acquirer would be willing to pay before it considers the deal economically unviable and walks away from the deal (Cotter and Zenner, 1994). To date, however, existing theory offers limited insights into how self-interested target firm CEOs will typically respond to an acquisition bid.

Although the initial offer price is publicly announced at the start of the takeover process, this figure is not simply an opening bid. By the time a deal is announced, the parties have typically already negotiated extensively, exchanged confidential information, and conducted initial due diligence, which means that the announced price reflects substantial pre-announcement agreement. At the same time, the period between announcement and completion is not purely procedural. Prior research shows that the final terms can still be revised in response to additional information discovery, the outcomes of further due diligence, the satisfaction of pre-determined clauses in the definitive agreement, or shifts in the parties’ bargaining positions (Boone and Mulherin, 2007; Jacobsen, 2014). As a result, even though the agreement announced publicly is already the product of meaningful negotiation, there remains scope for adjustments to the acquisition premium during the public phase. Incorporating this structure of the acquisition process helps clarify why target CEOs’ preferences and actions during this period can continue to influence the evolution of the final deal terms.

In this study, drawing on theoretical guidance from BAM, we argue that target CEOs’ responses to an acquisition bid are determined by their deal-specific windfall gains. As noted above, these deal-specific windfall gains refer to target CEOs’ gains in their personal equity wealth associated with increases in their firm’s underlying share price following the public announcement of the bid. Since target CEOs’ wealth gains are shaped by both the structure of the CEO’s equity-based compensation and the size of the initial premium offered by the acquirer, target CEOs holding a greater number of shares and options in their firms will experience greater instant deal-specific gains in their equity wealth following an acquisition bid, and these gains will be even larger if the bidder offers a higher initial premium. Consistent with the instant endowment hypothesis by Thaler and Johnson (1990), which suggests that the CEO’s current assessment of their wealth at risk of loss includes wealth that has just been received (see also Devers et al., 2008; Larraza-Kintana et al., 2007; Martin et al., 2013; Wiseman and Gomez-Mejia, 1998), we argue that these deal-specific gains are immediately endowed and thus become part of CEOs’ assessment of their current wealth at risk of loss. Although both CEOs and shareholders may benefit from increases in the acquisition premium, the nature of their exposure to the negotiation differs. Shareholders evaluate the offer from a diversified portfolio perspective, while the CEO’s assessment is tied to a concentrated firm-specific wealth position.

Given that target firm CEOs have most likely fully endowed their deal-specific gains in personal equity wealth following the public announcement of the acquisition, a deal that fails after a bid is made implies an immediate loss in target firm CEOs’ equity wealth because they lose out on what were essentially guaranteed gains had the bid been accepted as is. Specifically, when a bid fails to materialize, and an acquisition is withdrawn, the market downwardly corrects the target firm’s share price in response to the revised expectation of no acquisition premium being paid at all (Bradley et al., 1988; Jacobsen, 2014; Ruback, 1988). Because such downward revisions lead to the full or partial elimination of share price gains made by the acquisition announcement, and because the CEO’s equity wealth—specifically the value of the shares they own in the firm—is tied to movements in the firm’s share price, a failed deal essentially translates into an immediate loss of the CEO’s endowed deal-specific wealth. Given that prior research drawing on the BAM shows that CEOs take action to avoid such losses instead of seeking to maximize their existing wealth (e.g. Benischke et al., 2019; Martin et al., 2013; Wiseman and Gomez-Mejia, 1998), it is likely that target firm CEOs will seek to protect their gains to settle for a lower premium in return for the greater certainty that the deal is completed. In fact, the potential downside (loss of all deal-specific equity wealth should the deal not materialize) is significantly larger than any potential upside (marginal gains in their deal-specific equity wealth due to a higher premium and the associated increase in share price).

Although shareholders also benefit when acquisition premiums increase, their evaluation of the deal differs fundamentally from that of the CEO. Shareholders typically assess the transaction from a diversified portfolio perspective, and their exposure to deal failure is limited to the financial component of their investment (Holmstrom, 1979). As such, shareholders can rationally tolerate the risk that extended negotiations may lead to a withdrawn offer if the expected value of securing a higher premium outweighs this downside. In contrast, deal-specific gains become incorporated into the CEO’s current wealth position and thus elevate the personal stakes of preserving these gains (Wiseman and Gomez-Mejia, 1998). Because the CEO bears concentrated firm-specific wealth exposure (Hall and Murphy, 2002) and faces potential employment-related and career-related consequences if the deal collapses (Hambrick and Cannella, 1993), the CEO’s preferences may diverge from those of shareholders even when both parties benefit from higher premiums. This divergence is central to the BAM and clarifies how deal-specific gains capture CEO self-interest in the public pre-acquisition phase.

In short, despite the upside potential of pursuing higher premiums, we expect target firm CEOs with higher levels of deal-specific windfall gains to minimize the risk that the bidder will walk away from the proposed deal by accepting a lower premium. Said differently, we propose that target firm CEOs with higher levels of deal-specific windfall gains will prioritize the protection of their wealth at risk of loss and thus have a lower incentive to bargain for higher acquisition premiums during the public pre-acquisition phase, that is, the phase following the public announcement of the deal (Boone and Mulherin, 2007). Among completed deals, this should be reflected in a negative relationship between target CEOs’ equity risk-bearing and the difference in initial (i.e. premium offered at the time of public announcement) and final acquisition premium (i.e. premium eventually paid at completion of the deal):

Trade-offs between deal-specific windfall gains and prospective wealth

We have argued that when a firm becomes the target of an acquisition bid, the target CEO experiences deal-specific windfall gains due to the immediate increase in the firm’s share price. These gains are particularly large for CEOs with high equity-based compensation (e.g. shares and options), as their personal wealth is tightly coupled with movements in their firm’s share price. Drawing on behavioral agency theory (Wiseman and Gomez-Mejia, 1998) and the instant endowment effect (Thaler and Johnson, 1990), we argue that these windfall gains are immediately endowed and incorporated into the CEOs’ reference point for wealth at risk of loss.

During the public pre-acquisition phase, CEOs face a central behavioral trade-off: they can secure their endowed wealth by accepting the current offer, or push for a higher premium, risking deal failure and the associated loss of their gains. Because the downside risk (i.e. complete loss of deal-specific wealth if the acquirer walks away) typically outweighs the marginal upside of a higher premium, CEOs with substantial equity gains are expected to behave in loss-averse ways, opting for bargaining conservatism rather than premium maximization. This results in smaller changes in acquisition premiums between the initial offer and the final deal terms. However, the strength and direction of this trade-off likely vary depending on the type and salience of prospective value available to the CEO (Martin et al., 2013). Accordingly, factors that alter the CEO’s assessment of prospective value can shift how salient the endowed gain appears and thereby influence the extent to which loss aversion governs the CEO’s bargaining stance.

At its core, the relationship between CEO equity risk-bearing and acquisition premium change is shaped by a trade-off between protecting immediate, deal-specific gains and pursuing additional, prospective value (Martin et al., 2013; Martin et al., 2016). Contextual factors influence how CEOs navigate this trade-off (Benischke et al., 2019). When the target firm is experiencing strong revenue growth, CEOs are more likely to perceive future firm-based rewards, such as strategic opportunities or alternative bids, which can elevate their reference point and reduce the perceived magnitude of the endowed gain. In this setting, CEOs may show a weaker behavioral response, meaning they may negotiate more assertively. Conversely, when CEO retention by the acquiring firm is anticipated, prospective value is more personal in nature, tied to their future, career-related value. These non-financial stakes compound the CEO’s financial exposure, increase the CEO’s perceived wealth at risk, and amplify the motivation to avoid deal failure at all costs. In short, while both conditions introduce prospective value, we argue that they diverge in their effects: revenue growth mitigates, while anticipated retention intensifies, the CEO’s risk-averse response to deal-specific equity gains.

Target revenue growth, deal-specific windfall gains, and acquisition premium

When a target firm is experiencing strong revenue growth, it signals financial health and future opportunities, which can be seized through continued independent operations, strategic investments, or alternative acquisition bids. CEOs of such firms are likely to see the current bid as undervaluing the firm’s potential. Revenue growth elevates the CEO’s reference point: they likely perceive their firm and, by extension, their own equity holdings, which are tied to the firm’s share price, as worth more than the current offer implies (Martin et al., 2016). By increasing the CEO’s perceived prospective upside, strong organizational prospects reduce the relative weight placed on the endowed gain and move the CEO closer to risk neutrality, making continued bargaining appear less threatening. This elevated reference point introduces a trade-off between immediate, deal-specific windfall gains and the pursuit of prospective wealth tied to the firm’s future trajectory. Even when holding substantial equity-based gains, CEOs of high-growth firms may view the deal-specific windfall as less critical compared to what they expect to earn from future opportunities (Wiseman and Gomez-Mejia, 1998; Zolotoy et al., 2021), whether by securing a higher acquisition premium or through continued strategic success as an independent firm.

Thus, strong revenue growth weakens the behavioral pull of immediate gains by shifting attention toward prospective wealth. CEOs in high-growth firms may thus be more willing to engage in aggressive bargaining, despite the risk of losing their current gains, because they perceive the potential upside of future wealth to be even greater. This dynamic attenuates the negative relationship between equity-based gains and premium change. Formally:

Target CEO retention, deal-specific windfall gains, and acquisition premium

Much like strong revenue growth creates expectations of future financial value through firm performance, the anticipated retention of the target CEO by the acquiring firm creates prospective personal value tied to career continuity, status, and non-financial rewards. During the negotiation phase, retention is often promised or implied, and this expectation begins to shape the CEO’s calculus well before the deal is finalized (Bilgili et al., 2017; Hartzell et al., 2004). The prospect of retention introduces a trade-off between securing immediate, deal-specific windfall gains and protecting future, career-related gains. Because these future benefits are contingent on successful deal completion, anticipated retention heightens the CEO’s perceived wealth at risk and increases the subjective magnitude of potential losses, thereby reinforcing the loss-averse response to endowed gains (Bilgili et al., 2017). CEOs anticipating a role in the post-merger entity are motivated to maintain goodwill with the acquirer and avoid actions, such as aggressive bargaining, that could put their prospective role at risk (Harford and Schonlau, 2013). Consistent with this view, Walsh already argued that M&A negotiations that involve intense bargaining “are likely to strain and shatter the relationships between the top management teams, resulting in high top management turnover in the target company” (1989: 310).

Unlike organizational prospects, personal prospective value does not weaken attention to the endowed gain but instead compounds it. This trade-off is particularly salient when the CEO has already experienced a substantial equity-based wealth increase. With both financial and career-based gains at stake, risk aversion is amplified. Rather than extracting additional premium value, the CEO becomes motivated to protect their wealth and future position in the merged organization. This dynamic makes them more conservative in negotiations, increasing their preference for deal completion over premium maximization. Formally:

Taken together, these moderators clarify how different forms of prospective value either weaken or intensify the CEO’s perception of the endowed gain, thereby shaping the degree to which loss aversion influences negotiation behavior in the public pre-acquisition phase.

Data and methodology

Data and sample

Our sample consists of U.S. domestic acquisitions between two S&P 1500 firms completed between 1994 and 2020. We focus on acquisitions between two S&P 1500 firms, given that we need to collect data on CEO compensation, for which we rely on Execucomp. Considering that the objective of the study is to examine whether the target CEO’s private interests, as determined by their deal-specific windfall gains, influence the premium decision above and beyond the well-documented influence of the acquiring firm CEO, it is critical to be able to obtain data on CEO compensation for both the acquiring CEO as well as the target CEO. Data on acquisitions are obtained from SDC Platinum, firm-level data from Compustat, and stock price data from CRSP. Our dependent variable requires information on the final distribution to shareholders; therefore, we can only include completed deals. We also excluded deals in which either the acquirer or the target is a financial services firm (SIC category 6). After applying these filters, the final sample consists of 435 acquisitions.

Variables

Dependent variable

To capture how the acquisition premium changes during the public takeover period, we measure the change in acquisition premium, defined as the difference between the announcement premium and the premium paid to shareholders upon deal completion. Changes in deal premium after the deal announcement are common since the initial premium reflects merely a preliminary consensus based on limited information among both parties. With more information gradually coming to light, the parties may seek to re-negotiate specific aspects of the initial agreement (Haspeslagh and Jemison, 1991; Welch et al., 2020). The change in acquisition premium has rarely been examined empirically, but it is closely captured in our theoretical arguments, which predict a higher or lower willingness to push for a greater premium, depending on the equity gains associated with the acquisition announcement. This variable has larger positive values when the target shareholders get a higher final premium than the initial offer, smaller values when the final premium is close to the initial offer, or even negative values when the final premium is below the initial offer. We measure change in acquisition premium as the difference between the announcement premium and the premium paid to shareholders upon deal completion. The announcement premium, in turn, is calculated as the difference between the target stock price on the day of the announcement and the target stock price 30 days before the announcement, divided by the target stock price 30 days before the announcement (Laamanen, 2007). 2 The premium paid to shareholders upon deal completion is calculated as the difference between the price per share paid to target shareholders in the final distribution and the target stock price 30 days before the announcement, divided by the target stock price 30 days before the announcement (Beckman and Haunschild, 2002; Hayward and Hambrick, 1997). In robustness tests, we winsorize this variable at the first percentile to account for potential outliers and obtain similar results.

To illustrate this measure, consider the following examples taken from the acquisitions in our sample. 3 In the acquisition of Gentiva Health Services Inc., announced on 2014-05-15, the closing price of Gentiva Health Services Inc. shares 30 days before the announcement was $7.62, and the closing price on the day of the announcement was $13.83. The offer premium was thus $81.50%. The final distribution to shareholders on the day the deal became effective (2015-02-02) was $19.36 per share. Thus, the final premium paid was 154.13%. This implies a change in acquisition premium of 72.63%. On the other hand, in the acquisition of Rosetta Resources Inc., announced on 2015-05-11, the closing price of Rosetta Resources Inc. shares 30 days before the announcement was $21.55, and the closing price on the day of the announcement was $24.58. The offer premium was thus $14.03%. The final distribution to shareholders on the day the deal became effective (2015-07-20) was $19.97 per share. Thus, the final premium paid was -7.34%. This implies a change in acquisition premium of -21.37%. The measure thus captures the acquisition premium changes between the announcement premium and the premium paid to shareholders upon deal completion.

Our dependent variable measure relies on firms publicly disclosing a proposed price at acquisition announcement, and this raises the question of which firms typically engage in such disclosure. To address this question empirically, we examined deal price disclosure across multiple subsamples. In our main analysis sample, only 3 of 435 transactions lack an announcement price in SDC. In the set of completed deals used in our selection model (489 transactions), 32 deals (about 6%) do not have a recorded announcement price; this rises to 138 out of 697 (about 20%) when including non-completed deals. Looking across all completed U.S. deals during our study period, 511 out of 2860 transactions (about 18%) lack an announcement price in SDC, or 884 out of 3698 (about 24%) when non-completed deals are included. These figures indicate that public deals with price disclosure in announcements are more common than those with nondisclosure announcements.

Independent variable

Target CEO equity gain is measured as the sum of the number of all options and shares owned by the target CEO in the year before the announcement, multiplied by the value of the initial acquisition announcement premium offered at the time of announcement (Hartzell et al., 2004). To illustrate, consider the following examples taken from the acquisitions in our sample. 4 In the acquisition of Centigram Communications Corp, announced on 2000-06-09, the CEO, Robert L. Puette, held 513.30 thousand shares and options. The closing price of the Centigram Communications Corp shares 30 days before the announcement was $16.50, and the closing price on the announcement day was $24.57. The offer premium was thus $8.25. Multiplying this by the equity at risk, the equity gain for the CEO was $4.23 million. On the other hand, in the acquisition of NUI Corp, announced on 2004-07-15, the CEO John Kean Jr., held 371.88 thousand shares and options. The closing price of the NUI Corp 30 days before the announcement was $13.90, and the closing price on the announcement day was $13.30. The offer premium was thus -$0.60. Multiplying this by the equity at risk, the equity gain for the CEO was -$0.22 million (a loss in this case). The measure thus captures how the value of the target CEO’s equity changes due to the premium offered at the time of the acquisition announcement. Thus, the measure reflects the value of the deal-specific equity at risk and windfall gains.

Moderating variables

The two variables we use to test the boundary conditions of our main prediction are target revenue growth and target CEO retained. We measure target revenue growth over the preceding 3 years. Our theoretical arguments for the effect of target growth are based on the target CEO having more confidence in their future earnings potential if the acquisition does not eventuate. Short-term growth, such as year-on-year growth, cannot capture these theoretical ideas well. Hence, we calculate target revenue growth as target total revenue at t minus target total revenue at t-3 divided by target total revenue at t-3. In sensitivity tests, we obtain very similar results using growth over the preceding 2 years.

We captured whether the target CEO is retained after the acquisition. This variable is coded as a dummy variable that takes the value of 1 if the target remained either on the executive or the board of the target or acquirer firm in any of the 3 years following the acquisition.

Control variables

We control for multiple potential confounders. At the transaction level, we control whether the acquisition attempt is friendly or hostile. Friendly acquisition is measured using an indicator variable that takes the value of 1 if the acquisition is classified as friendly and 0 if otherwise. We also control for acquisitions by tender offer using a variable that takes the value of 1 if the acquisition is classified as a tender offer and 0 if otherwise. Given that target CEOs may be in a better negotiating position when there are multiple potential buyers, we include a variable, competing bidder, that takes the value of 1 if there is more than 1 buyer interested in the target and 0 otherwise. The use of takeover defense has also been shown to influence acquisition premia (Zhu, 2013); we, thus, include a binary variable—defense tactics used—that takes the value of 1 if the target was classified as having used defensive tactics and 0 if otherwise. In order to account for information asymmetries and competitive considerations, we control whether the transaction is horizontal, given that unrelated acquisitions are associated with greater information asymmetries (Capron and Shen, 2007). Horizontal acquisition is measured using an indicator variable that takes the value of 1 if the target and the acquirer are active in the same primary 4-digit SIC industry and 0 if otherwise.

We control for acquirer experience, given that more experienced acquirers may be less prone to overpaying in acquisition deals (Kim et al., 2011), measured as the number of acquisitions the acquirer announced in the 3 years before the focal deal. The market reaction to the acquisition announcement may influence the willingness of the target CEO to negotiate. To account for this effect, we use the target cumulative abnormal return (CAR) to capture the target stock market reaction. In estimating the benchmark model, we use an equally weighted market model with an estimation period of 150 days that ends at least 30 days before the acquisition announcement. The CAR is then estimated as the daily difference between the return as predicted by the benchmark model and the actual return in the event window. In our case, we define the event window as the announcement day to 3 days after the announcement. Finally, we controlled for the duration of the public period, measured as the number of days between the announcement date and the date the acquisition became effective, to account for the possibility that longer durations allow for changes in performance that influence the difference between announcement completion premiums (Coff, 1999; Li et al., 2017).

At the firm level, to capture the size and power differential between the acquirer and target, we control for relative size measured as the target’s total assets divided by the acquirer’s total assets. We also control target ROS measured as EBITDA divided by total sales for the target. To account for the monetary incentives of target firm directors, we include a variable, director pay, that is measured at the logarithm of the sum of the total pay that target firm directors received. Finally, we controlled for target CEO entrenchment using the Bebchuk et al. (2009) index.

Since our study suggests that target CEO self-interest explains variance in the acquisition premium decisions beyond acquiring firm CEO characteristics, we also control for a number of variables at the acquirer CEO level. Here, we control for acquirer CEO duality, which we measure as a dummy variable that takes the value of 1 if the acquirer CEO is also the chairperson and 0 if otherwise. We further control for acquirer CEO age, measured as age in years. In order to control for the acquiring CEO’s managerial self-interest, we also control for acquirer CEO total compensation, measured as the logarithm of the dollar value of the acquirer CEO’s total compensation. Finally, we measure acquirer CEO gender using an indicator variable that takes the value of 1 if the CEO is male and 0 if the CEO is female.

At the target CEO level, we also control for target CEO duality to control for the target CEO’s power over the board. We measure target CEO duality using a dummy variable coded as 1 if the target CEO is also the chairperson and 0 if otherwise. We further control for target CEO age, measured in years. It is also important to control for compensation to isolate the effect of deal-specific windfall gains (Devers et al., 2008). Target CEO total compensation is measured as the logarithm of the dollar value of the target CEO’s total compensation. We measure target CEO gender using an indicator variable that takes the value of 1 if the CEO is male and 0 if the CEO is female. We also controlled for golden parachute payouts measured by multiplying the total of the target CEO’s salary and bonus by three if the CEO has a golden parachute clause in the contract (Fich et al., 2013). Another important consideration for the target CEO is lost compensation (Fich et al., 2013). To account for this effect, we follow the Fich et al. (2013) method to estimate a variable target CEO lost compensation that captures the compensation the target CEO forgoes by accepting the deal rather than remaining with the firm in the CEO role until retirement age.

Finally, we controlled for industry-level effects. Specifically, we account for competitive considerations at the industry level using industry concentration measured as the Herfindahl-Hirschman index (at the 2-digit SIC code level). To account for how attractive an industry is, we measure industry growth as the year-on-year growth in the primary industry (at the 2-digit SIC code level) in which the target firm operated the year before the announcement. To capture uncertainty in the industry environment, we measure industry volatility as the errors of a regression in which we regress years on industry sales (at the 2-digit SIC code level; like most measures of industry volatility, we use 5-year periods in constructing this measure; Dess and Beard, 1984). We also include year and industry (at the 2-digit SIC level) fixed effects to account for temporal and time-invariant industry effects.

Results

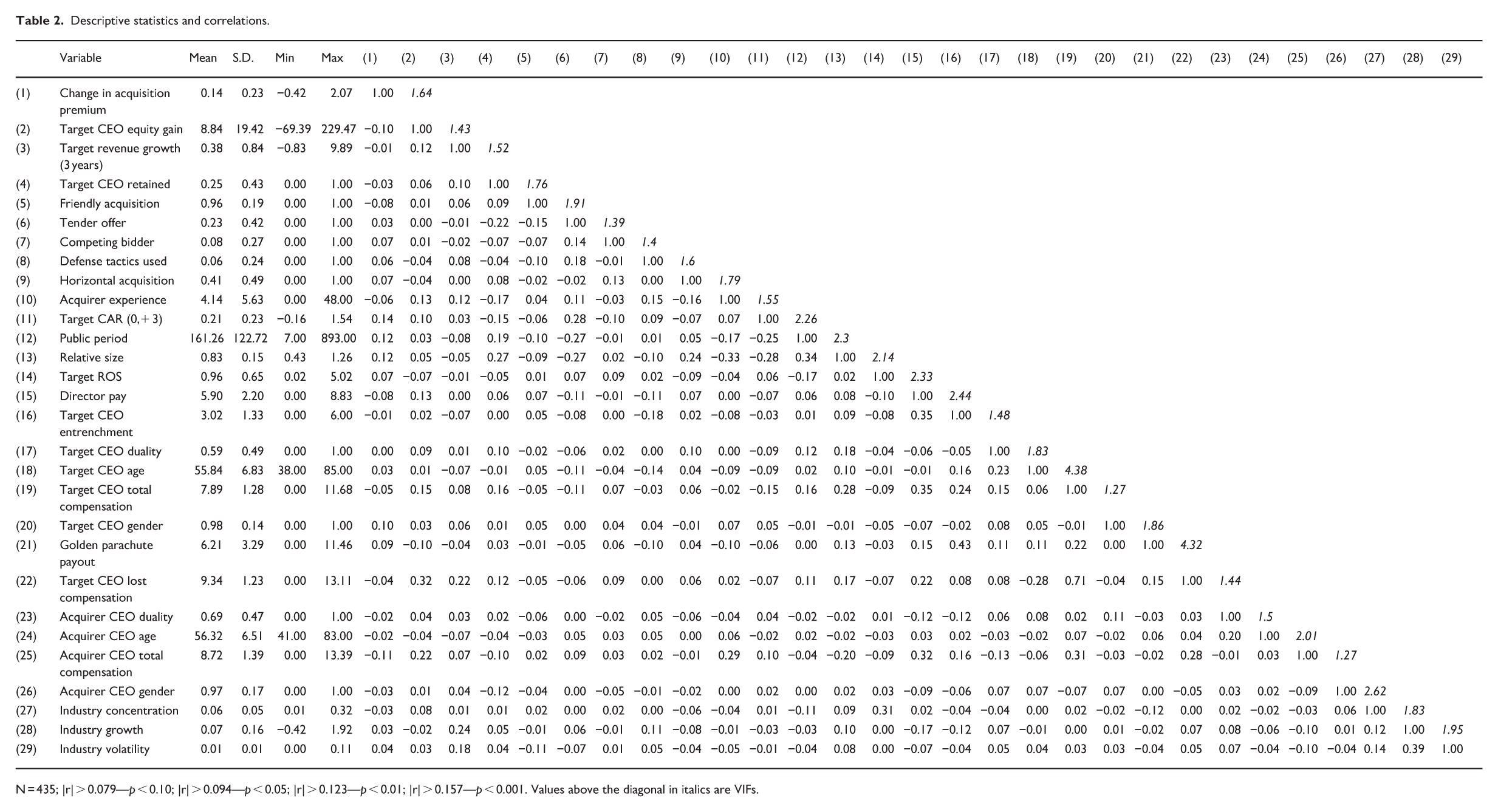

Table 2 shows the descriptive statistics and correlations for all variables included in the analysis. As seen from Table 2, we do not observe any correlations between first-order variables, which would point toward multicollinearity issues. Nonetheless, we further assessed the presence of potential collinearity concerns using variance inflation factor analysis (VIF). The mean VIF for the full model is 1.97, and no individual VIF is higher than the critical value of 10 (see values in italics above the diagonal in Table 2). We, therefore, conclude that multicollinearity is unlikely to influence our results.

Descriptive statistics and correlations.

N = 435; |r| > 0.079—p < 0.10; |r| > 0.094—p < 0.05; |r| > 0.123—p < 0.01; |r| > 0.157—p < 0.001. Values above the diagonal in italics are VIFs.

A key challenge in identifying the relationship between changes in acquisition premium and target CEO equity gain arises from potentially omitted variables. In our context, there may be unobserved target and acquirer CEOs, target and acquirer firms, and deal characteristics that can potentially influence this relationship. For instance, a target CEO who is a skilful negotiator may have negotiated more equity-based compensation and a better acquisition premium for the target. One approach for dealing with this type of endogeneity is using instrumental variable techniques. However, finding valid, theoretically derived instruments is challenging in our context since the role of the target CEO in the acquisition premium decision is not well understood. To deal with this issue, we rely on synthetically derived instruments. These allow us to construct empirically valid instruments without making strong theoretical assumptions about which instruments to use. Using two-stage least squares instrumental variable regression with year and industry fixed effects, we believe we can alleviate endogeneity concerns arising from potentially omitted variables.

To construct empirically valid instruments, we rely on two separate approaches to constructing synthetic instrumental variables. First, we create eigenvector-based synthetic instruments that exploit the map patterns in the spatial dimension of the target headquarters (e.g. Busenbark et al., 2022). These eigenvector-based synthetic instruments are exogenous and correlated with the variable of interest by construction (Le Gallo and Páez, 2013; see also Juhl, 2021, for methodological details). Second, we use the method Dzhumashev and Tursunalieva (2025) developed to create a second set of instrumental variables. This approach relies on the direction of the relationship between the endogenous variable and the dependent variable and the relationship between the endogenous variable and the error term in the structural equation to construct an instrument orthogonal to the error term. 5

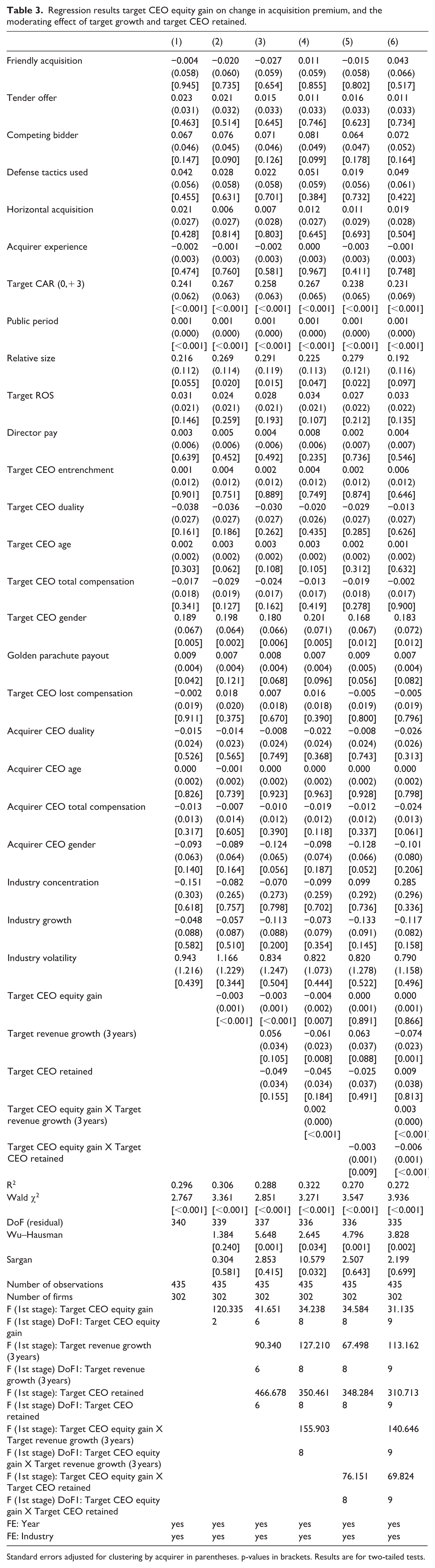

Table 3 presents the results of the hypothesis tests. Model 1 shows the baseline model, including all control variables, year, and industry effects. In Model 2, the target CEO equity gain variable is instrumented using two synthetic instrumental variables. The first stage F statistic (F = 120.335; p ⩽ 0.001, df = 2) indicates that the instruments are relevant (Semadeni et al., 2014). The Wu–Hausman test (χ2 = 1.384; p = 0.240) indicates that endogeneity may not be present in this model, while the Sargan test (χ2 = 0.304; p = 0.581) indicates no association between the instruments and the structural error. In addition, the robustness of inference to replacement test (Frank et al., 2013) suggests that 50.26% of the estimate would have to be due to bias to invalidate an inference.

Regression results target CEO equity gain on change in acquisition premium, and the moderating effect of target growth and target CEO retained.

Standard errors adjusted for clustering by acquirer in parentheses. p-values in brackets. Results are for two-tailed tests.

Hypothesis 1 predicts that target CEO deal-specific equity gains should be negatively related to changes in the acquisition premium. The target CEO equity gain variable has a negative and significant effect (b = -0.003; p ⩽ 0.001) on the change in acquisition premium. Regarding effect size, this coefficient implies that as the target CEO’s deal-specific windfall gains increases by one standard deviation ($19.42 million) from its mean ($8.84 million), the change in acquisition premium reduces from 13.8% to 8.5%. Given an average target market value of approximately 4802.3 million (based on the target’s stock price 30 days before the announcement), such a reduction implies an average loss of 256.5 million in target market value. In combination, these results support our Hypothesis 1 that the deal-specific risk-bearing of target CEO equity wealth negatively influences the change in acquisition premium in our data.

Model 3 introduces the main effects of the moderator variables. Model 4 introduces the interaction of target CEO equity gain and target revenue growth. In this model, target CEO equity gain, target revenue growth, and the interaction of target CEO equity gain and target revenue growth are instrumented using four synthetic instrumental variables and their interactions. The first stage F for target CEO equity gain (F = 34.238; p ⩽ 0.001, df = 8), target revenue growth (F = 127.210; p ⩽ 0.001, df = 8), and the interaction of target CEO equity gain and target revenue growth (F = 155.903; p ⩽ 0.001, df = 8) indicate that the instruments are relevant (Semadeni et al., 2014). In addition, the Wu–Hausman (χ2 = 2.645; p = 0.034) indicates that this model may suffer from endogeneity, while the Sargan test (χ2 = 10.579; p = 0.032) indicates that there may be an association between the instruments and the structural error. Hypothesis 2 predicts that the effect of CEO deal-specific windfall gains is weaker (less negative) when target revenue growth is higher. Consistent with our predictions, the interaction term is positive and significant (b = 0.002; p ⩽ 0.001). Hence, although the overidentification test suggests potential instrument correlation in this specification, results are consistent across alternative estimators, and we, thus, conclude that our data support Hypothesis 2.

Model 5 introduces the interaction of target CEO equity gain and target CEO retained. In this model, target CEO equity gain, target CEO retained, and the interaction of target CEO equity gain and target CEO retained are instrumented using four synthetic instrumental variables and their interactions. The first stage F for target CEO equity gain (F = 34.584; p ⩽ 0.001, df = 8), target CEO retained (F = 348.284; p ⩽ 0.001, df = 8), and the interaction of target CEO equity gain and target CEO retained (F = 76.151; p ⩽ 0.001, df = 8) indicate that the instruments are relevant (Semadeni et al., 2014). The Wu–Hausman (χ2 = 4.796; p = 0.001) indicates that this model may suffer from endogeneity, while the Sargan test (χ2 = 2.507; p = 0.643) indicates no association between the instruments and the structural error. The interaction term is negative and significant (b = -0.003; p = 0.009). Hence, Hypothesis 3 is supported in our sample.

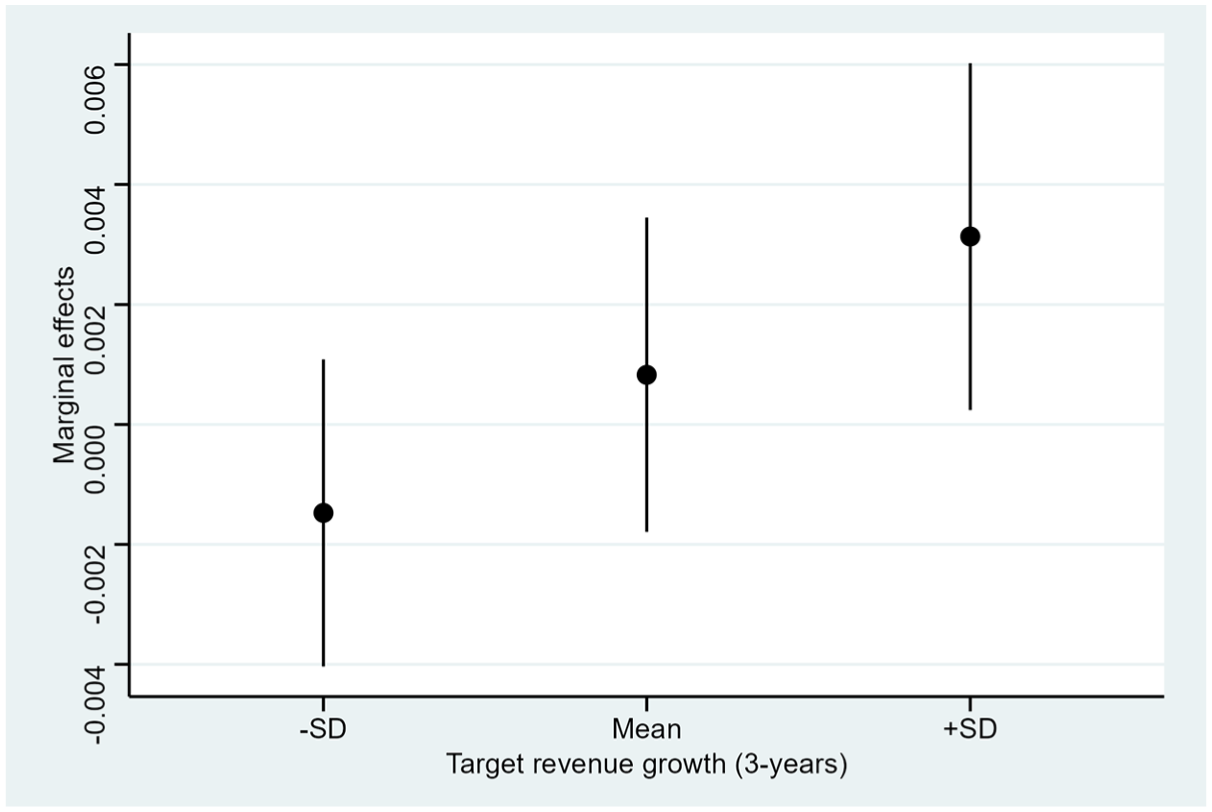

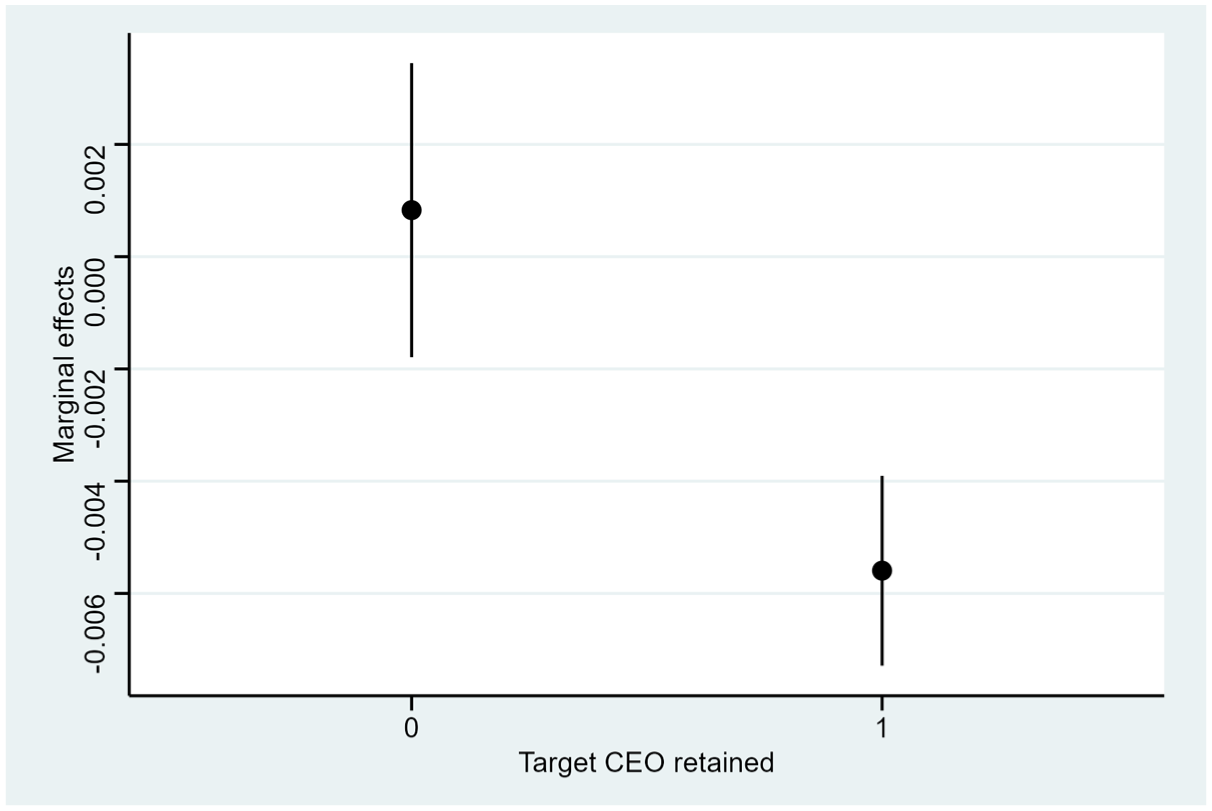

Model 6 shows the fully specified model, including all interactions that further corroborate the results presented in Models 1–5. We use this model to further assess the interaction effects by estimating the marginal effects of the target CEO equity gain variable as the target revenue growth variables move from low (mean − SD) through medium (mean) to high (mean + SD) and the target CEO retained variable from 0 to 1 (holding all other variables at their means). To illustrate how the marginal effects change as a function of target revenue growth and the target CEO retained variable, we plot these marginal effects along with 95% confidence intervals in Figures 1 and 2, respectively. As can be seen in Figure 1, the marginal effect of target CEO equity gain is -0.001 (CI [-0.004; 0.001]) when target growth is low (target growth = -0.456), 0.0008 (CI [-0.001; 0.003]) when target growth is medium (target growth = 0.381), and 0.003 (CI [0.0002; 0.006]) when target growth is high (target growth = 1.218). Figure 2 shows that the marginal effect of target CEO equity gain is 0.0008 (CI [−0.001; 0.003]) when the target CEO is not retained (target CEO retained = 0), and −0.005 (CI [−0.007; −0.004]) when the target CEO is retained (target CEO retained = 1).

Marginal effects of target CEO equity gain and target revenue growth on change in acquisition premium.

Marginal effects of target CEO equity gain and target CEO retained on change in acquisition premium.

Robustness tests

We use two-stage least squares instrumental variable regression with year and industry fixed effects to identify the effect of target CEO equity gains on the change in acquisition premium because we suspect that there may be endogeneity in our models. The Wu–Hausman tests support this suspicion for most models, but in Model 2, the test suggests that there may be no endogeneity. Hence, we also estimate our models with ordinary regression with year and industry fixed effects. These models’ results are similar to those presented in the main analysis above, but the interaction of target CEO equity gain and target CEO retained is no longer significant in either Model 5 or Model 6. We prefer the results that control for endogeneity because the Wu–Hausman test indicates that these models may suffer from endogeneity.

The robustness of inference to replacement test indicates that our results are unlikely to be invalidated by omitted variables; nevertheless, we have also tested how including a range of additional variables may influence our results. Specifically, the initial offer price may influence how the target CEO negotiates, such that when an initial offer is high, there may be fewer incentives to push for an even higher premium. When we include the initial premium as a control variable in our models, the effect is negative and significant in all models, and our results remain similar with slightly larger effect sizes. Second, when the acquirer’s stock experiences a positive reaction to the acquisition announcement, this may signal to the target CEO that there is more room for negotiation. When we include acquirer CAR (measured around the acquisition announcement (0, + 3)) as a control in our model, the effect is positive but insignificant in all models, while our main results remain very similar to those reported. Capturing industry-relatedness with SIC-based measures can be problematic (Hoberg and Phillips, 2010). Thus, we use the three-digit SIC equivalent text-based product market similarity measure developed by Hoberg and Phillips (2010) as an alternative and receive very similar results. Fourth, to control for the potential influence of board and ownership effects, we have also estimated models that include the proportion of independent board members, board size, the average age of directors, ownership concentration, and the proportion of shares held by institutional investors. In all these models, our results remain consistent with those presented here; however, the sample size is reduced by approximately 26%, and we therefore prefer the models presented here.

Finally, our models include a range of control variables at the transaction, firm, industry, and CEO levels. Including many control variables can lead to mis-specified models and invalid inferences (Cinelli et al., 2024). We thus also estimate models in which we only include the variables of interest, year, and industry fixed effects. In all these models, the results remain largely consistent. In an additional robustness test, we also include a control variable capturing whether the current target CEO was a founder, or not. The results are consistent with those reported in our main analysis. The results for all robustness tests are available upon request.

Discussion and conclusion

This study highlights how sudden, deal-specific windfall gains shape the strategic behavior of target firm CEOs during the public pre-acquisition process. Drawing on and extending behavioral agency theory, we theorized and showed that such gains trigger an immediate re-anchoring of loss-averse CEOs’ reference point, heightening risk aversion and motivating value-preserving behavior. Our analysis shows that CEOs with larger windfall gains, stemming from equity-based compensation and substantial initial acquisition premiums, are less likely to push for higher premiums after the public deal announcement and instead prioritize securing their gains. This effect is weakened when the firm has strong revenue growth, reflecting organizational prospects, and strengthened when the CEO is likely to be retained post-acquisition, reflecting personal prospects. These findings contribute to multiple research streams.

First, we introduce windfall gains as a novel psychological anchoring mechanism within the behavioral agency theory. While prior behavioral agency research has emphasized gradual changes in CEO risk preferences as equity wealth accumulates over time (e.g. Benischke et al., 2019; Devers et al., 2008; Martin et al.,2013, 2016) we argue that sudden, exogenously triggered gains, such as those generated by acquisition announcements, provoke a sharper, more reactive form of risk aversion. This dynamic complements existing theories by demonstrating that not all wealth accumulation is behaviorally equivalent. Windfall gains shift the CEO’s reference point abruptly, leading to a heightened preference for value preservation over value maximization. In doing so, we respond to calls for a more dynamic, event-contingent understanding of risk behavior in strategic decision-making and extend behavioral agency theory to account for timing, magnitude, and source of wealth gains as key behavioral variables.

One important implication of our focus on windfall gains is that our theory highlights the importance of distinguishing between organizational and personal sources of prospective value when analyzing CEO decision-making under conditions of windfall gains, especially in the M&A context. Although revenue growth and anticipated retention introduce forward-looking incentives that interact with the CEO’s existing equity-based wealth, consistent with the framework advanced by Martin et al. (2013), they do so in psychologically distinct ways. Organizational prospects, such as strong revenue growth, signal firm-level opportunity and elevate the CEO’s aspirational reference point, potentially making the current acquisition offer seem undervalued. This can reduce the behavioral pull of loss aversion by reframing the initial equity gain as a baseline for further upside, thereby encouraging more aggressive bargaining. In contrast, personal prospects, such as post-acquisition CEO retention, heighten the salience of career continuity, status, and future influence; outcomes that are contingent on deal completion. When combined with substantial deal-specific wealth, these personal stakes intensify the CEO’s motivation to preserve financial and non-financial benefits, leading to greater risk aversion. In this way, organizational and personal prospects shape the CEO’s calculus, but in opposing directions: one promotes strategic assertiveness, the other strategic caution. This distinction highlights the need for a more nuanced view of CEO incentive structures, which considers not only the magnitude of wealth at stake but also the source and framing of prospective gains.

Our moderating results reveal that contextual conditions do not simply weaken or strengthen the baseline relationship but meaningfully alter the CEO’s risk posture. In high-growth contexts, the conditional effect becomes positive, indicating that strong organizational prospects elevate the CEO’s aspirational reference point (Martin et al., 2016) and increase perceived future upside. This reduces the salience of the endowed gain and shifts the CEO from a loss-averse stance toward greater risk neutrality or even modest risk seeking. By contrast, at low and moderate growth levels, prospective value is insufficient to reframe the endowed gain, and the relationship centers around zero, consistent with a more neutral mixed-gamble evaluation (Martin et al., 2013; Wiseman and Gomez-Mejia, 1998).

The retention results display the opposite logic. When retention is anticipated, deal-specific gains continue to exert a negative influence on premium revisions, reflecting heightened loss aversion due to deal-contingent personal value tied to employment continuity and future influence (Bilgili et al., 2017; Hambrick and Cannella, 1993). Without retention, however, the relationship flattens, suggesting that the endowed gain exerts less motivational pull when personal future benefits are absent. These patterns indicate that CEOs move between loss-averse, neutral, and more opportunity-seeking stances depending on the structure of prospective value. They also highlight a promising direction for future research, namely examining how other forms of forward-looking incentives, such as alternative career opportunities or reputational considerations, shape CEO responses to event-driven wealth shocks in acquisition settings.

Our study also contributes to the M&A literature by further highlighting target firm CEOs’ active and strategic role in shaping acquisition outcomes. Much prior work has focused on acquiring CEOs and attributed acquisition premiums to their motivations and compensation structures (e.g. Sanders and Hambrick, 2007). We show that this view is incomplete. Target CEOs, particularly when endowed with large, sudden equity gains, exert meaningful influence over deal outcomes, especially during the public pre-acquisition phase, where final deal terms remain in flux. Attributing acquisition premiums solely to acquirer-side dynamics risks misrepresenting the underlying power and incentive dynamics of M&A negotiations.

Another contribution of our study lies in our novel approach to capturing the outcome of the public pre-acquisition phase by examining the difference between the initial premium offered by the bidder and the final premium paid upon completion. Few prior studies in the finance (e.g. Aktas et al., 2010; Officer, 2003) and strategy literature (e.g. Coff, 1999; Pavicevic et al., 2023; Walsh, 1989) explicitly focus on changes in acquisition outcomes during the public pre-acquisition phase, making it the least understood phase in the acquisition literature (Welch et al., 2020). Despite the central role of the acquisition premium in M&A, prior work tends to assume away these negotiations and often focuses on the initial premium only. Our results suggest that this approach can introduce bias, given that premia on average change by 14% during the public takeover period, an amount which, across the transactions in our sample, corresponds to an average of 700 million dollars. Examining the changes in acquisition premium during the public takeover phase, thus, presents a meaningful way to capture the behavioral dynamics playing out in the pre-deal phase and may also offer a valuable complement to research on pre-deal duration and completion likelihood (e.g. Chakrabarti and Mitchell, 2016; Chakraborty and Fuad, 2024; Hawn, 2021; Hennig et al., 2025; Li et al., 2017; Muehlfeld et al., 2012; Pavicevic and Keil, 2021).

Our study also adds to the governance literature, in particular to the stream of research that has pointed toward the agency cost implications of equity compensation. That is, while some studies have already shown that equity compensation may generally result in CEO behavior that is detrimental to shareholder value (e.g. Wowak et al., 2015), in the acquisition context, these studies have suggested that these incentive alignment problems tend to result in a transfer of shareholder wealth from the acquirer to the target firm’s shareholders (Bradley et al., 1988; Datta et al., 1992; Loughran and Vijh, 1997). This view is shared by other behavioral decision-making studies showing that cognitive biases often result in suboptimal decisions at the expense of acquiring firm shareholders (Hayward and Hambrick, 1997). Advancing this discourse in the literature, we offer a more nuanced view of distributional outcomes in acquisitions. Whereas prior research has argued that acquirers overpay and target shareholders benefit (Bradley et al., 1988; Loughran and Vijh, 1997), our findings suggest that target shareholders may also incur opportunity costs. When target CEOs are motivated to protect personal gains, they may accept lower premiums, effectively trading potential shareholder value for personal certainty. However, it is unclear if shareholders would indeed prefer target CEOs to negotiate for a higher premium or have similar interests as target CEOs, that is, to protect their windfall gains (Hartzell et al., 2004). Future research, especially qualitative work, should further explore this question.

Limitations and future research

Our study’s results must be interpreted in light of several limitations. First, we have identified a lack of research on the effect of the target CEO’s private interests on acquisition outcomes. As a first step, we have addressed this lacuna by studying the independent main effect of target CEO deal-specific windfall gains on the likelihood of pushing for a higher premium following the public announcement of the deal. While we have controlled for target CEO power using proxies such as CEO duality and entrenchment, future research is encouraged to further develop this research stream by considering the interaction between target CEO and board characteristics. Further, there is promise in examining the interaction between acquiring and target firm CEOs and their combined effect on acquisition outcomes, a question beyond the scope of the present study. Second, we encourage research that examines the degree to which target CEO attributes may influence their behavioral responses to losses in endowed wealth. Such attributes potentially establish important boundary conditions for our framework (Benischke et al., 2019). Finally, our sample focuses on acquisitions where both the acquirer and target are S&P 1500 firms, representing a subset of all M&A transactions and may differ from the broader population regarding deal size, complexity, and frequency. While this focus may limit the generalizability of our findings, it also provides advantages for our study. Specifically, these transactions are subject to stringent disclosure requirements and involve publicly available, high-quality data for both parties, which reduces information asymmetries and enhances measurement precision.

Conclusion

Overall, our study highlights how sudden, deal-specific windfall gains reshape loss-averse CEOs’ behavior by triggering acute risk aversion during acquisition negotiations. We further show that the effect of these sudden gains depends on the type of prospective value available: organizational prospects (e.g. revenue growth) encourage assertive bargaining by shifting the CEO’s focus to future upside, while personal prospects (e.g. anticipated retention) amplify risk aversion and promote deal closure. These findings extend behavioral agency theory by emphasizing the role of context in shaping how CEOs respond to unexpected wealth shocks.

Footnotes

Acknowledgements

The authors thank Ryan Krause, Geoffrey Martin, and participants of the Academy of Management Annual Meeting in Boston, SMS Special Conference in Las Vegas and a workshop presentation at the Rotterdam School of Management for feedback on earlier versions of the article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.