Abstract

Acquisition decision-making often entails significant information asymmetries, which acquirers seek to mitigate through comprehensive due diligence analyses. While due diligence can help reduce the risk of acquisition failure, conducting thorough due diligence also slows down the decision-making process, consumes resources, and delays the realization of synergies. Drawing on decision comprehensiveness theory, we argue that the relationship between due diligence speed and acquirer stock market returns follows an inverted U-shaped curve, in which the optimal point is contingent on the decision-making context. Based on an analysis of a sample of 501 acquisitions of S&P 1500 firms, we find support for the existence of a curvilinear relationship and the moderating effects of industry complexity and dynamism, but not industry munificence. Our findings contribute to an enhanced understanding of the due diligence process and extend the existing research on the influence of external contingency factors in optimizing comprehensiveness and speed in strategic decision-making.

Keywords

Introduction

That was one of the questions I got, why we didn’t do more due diligence . . .. It’s interesting. We’ve made plenty of mistakes in acquisitions. Plenty. And we made mistakes in not making acquisitions, but the mistakes are always about making an improper assessment of the economic conditions in the future of the industry of the company

Poor acquisition outcomes are often attributed to adverse selection problems stemming from the information asymmetry between the acquirer and the target firm (Akerlof, 1970; Reuer and Ragozzino, 2008). To mitigate information asymmetries, acquirers commonly conduct thorough due diligence to assess the opportunities and risks of the proposed transaction (Wangerin, 2019). Through due diligence, detailed information on the target firm can be gathered and processed, thereby reducing the propensity for poor acquisition outcomes (Puranam et al., 2006).

On the contrary, conducting comprehensive due diligence requires extensive data collection and analysis, which slows down the decision-making process (Pavićević and Keil, 2021), consumes substantial resources (Reuer and Sakhartov, 2021), and delays the realization of acquisition synergies (Daley et al., 2024). Consequently, scholars have started to question the generally positive portrayal of prolonged due diligence processes (Reuer and Sakhartov, 2021) and have even contended that “in equilibrium, the acquirer engages in ‘too much’ due diligence” (Daley et al., 2024: 2115), calling for a more nuanced assessment of the ramifications of the due diligence process conducted in the pre-deal phase (Welch et al., 2020).

Given these competing pressures, there is likely to be an optimal level of due diligence beyond which further due diligence does not anymore contribute to improved decision-making that would justify the additional investment. However, determining this optimal balance between comprehensiveness and speed is challenging given the different types of acquisition targets and the different external industry contexts in which they operate.

We address this puzzle by drawing on decision comprehensiveness theory (Forbes, 2007; Fredrickson and Mitchell, 1984), which provides a theoretical foundation for us to examine the tension between information comprehensiveness and speed in strategic decision-making. Proponents of rational strategic decision-making argue that information comprehensiveness embodies rationality, as more exhaustive information gathering and processing enhance the effectiveness of decision outcomes (e.g. Fredrickson, 1984; Fredrickson and Mitchell, 1984). Other scholars, however, question the efficiency of information comprehensiveness, arguing that slower decision-making might prevent the optimal capitalization of opportunities (e.g. Wally and Baum, 1994). Regardless of one’s viewpoint, scholars have argued that external contingencies affect the relevance of comprehensiveness and speed in strategic decision-making (e.g. Dean and Sharfman, 1996; Eisenhardt, 1989). As contingencies for reaching a strategic decision, industry conditions shape the decision process design and the quality of the decision outcomes (Forbes, 2007; Siggelkow and Rivkin, 2005).

To deepen the understanding of the optimal balance between comprehensiveness and speed, as well as the external industry contingencies influencing this relationship, we pose the research question: “Whether and when due diligence length is beneficial in the acquisition decision-making process?” We expect to find an inverted U-shaped baseline relationship between due diligence speed and stock market returns and argue that industry conditions influence when this optimal point is reached. Specifically, we investigate how three external industry contingencies—munificence, complexity, and dynamism (Dess and Beard, 1984; Malhotra and Harrison, 2022)—influence acquisition outcomes. We argue that in munificent industries, characterized by abundant resources and growth prospects, there is a higher pressure for speed and a lower need for comprehensive analysis before conducting acquisitions, rendering a shorter due diligence process more beneficial. Conversely, in complex industries marked by greater stakeholder heterogeneity and opaque input-output relationships, the difficulty of assessing the target is higher, which should lead to longer due diligence processes being more advantageous. Finally, in dynamic industries, defined by market instability and the need for speed, longer due diligence processes may be less beneficial.

We test our predictions using a sample of 501 acquisitions from Standard & Poor’s (S&P) 1500 firms between 2003 and 2018. Following prior literature, we measure due diligence length in the pre-deal phase as the time between signing a non-disclosure agreement (NDA) and the public deal announcement (Marquardt and Zur, 2015; Pavićević and Keil, 2021). We extracted information on the NDA signing dates manually using S-4 and DEFM14A filings from the SEC database. As our dependent variable, we used the short-term stock market returns to the acquiring firm following acquisition announcements. While short-term stock market returns represent an imperfect proxy for longer-term acquisition performance, they allow us to avoid confounding events and link the independent and dependent variables more precisely than accounting measures or longer-term market returns. We also follow prior literature on the operationalization of industry conditions in terms of munificence, complexity, and dynamism (Connelly et al., 2016).

Our empirical analysis supports the existence of an inverted U-shaped baseline relationship between due diligence length and acquisition outcomes, as well as the moderating effects of industry complexity and dynamism, but not industry munificence. To assess the reliability of our results, we conducted a series of endogeneity and robustness checks. First, we applied a Heckman correction to address potential sample selection bias stemming from the endogenous availability of information on NDA signing dates, which requires sufficient SEC filings (Certo et al., 2016). Second, we used instrumental variable approaches, such as two-stage least squares (2SLS) regressions and a control function approach to address the endogenous nature of due diligence length (Clougherty et al., 2016). Third, we assessed the Robustness of Inference to Replacement (RIR) to alleviate concerns that omitted variables might drive our results (Busenbark et al., 2021).

With our study, we contribute to the literature in several ways. First, our findings yield new insights into pre-deal acquisition research (Pavićević and Keil, 2021; Reuer and Sakhartov, 2021; Welch et al., 2020) by documenting an inverted U-shaped relationship between due diligence length and stock market returns and by showing how industry conditions influence the relationship. While Pavićević and Keil (2021) found that a longer pre-deal process reduces managerial biases in acquisition decision-making, we extend this line of research by showing that, in certain settings, faster pre-deal due diligence may also be beneficial. Thereby, our paper also answers the call of Welch et al. (2020) to provide an added focus on the pre-deal phase.

Second, our study contributes to the research on the tension between information comprehensiveness and decision speed in strategic decision-making (Fredrickson and Mitchell, 1984; Miller and McKee, 2021). While this research stream originated already in the 1980s, there is a continuing debate about whether comprehensiveness and speed are mutually exclusive (Fredrickson and Mitchell, 1984; Samba et al., 2021) or whether they can coexist (Bartkus et al., 2022; Eisenhardt, 1989). By applying decision comprehensiveness theory to individual acquisition decisions, we also respond to Forbes’ (2007) call for an analysis of specific decision outcomes rather than aggregated firm-level measures.

Third, we extend existing research on the relevance of contingency factors on the optimal balance between comprehensiveness and speed in strategic decision-making (e.g. Boyd et al., 2012; Hough and White, 2003). While it is well-established that contingency factors affect strategic decision-making (e.g., Bourgeois and Eisenhardt, 1988; Wally and Baum, 1994) and decision outcomes (Malhotra and Harrison, 2022; Siggelkow and Rivkin, 2005), the theoretical mechanisms underlying these effects are poorly understood. We deepen the understanding of these mechanisms by examining the interplay of decision comprehensiveness theory and industry context.

Theory and hypotheses

Decision comprehensiveness theory

Decision comprehensiveness theory examines the extent to which decision-makers gather and process information from the external environment before making strategic decisions (Fredrickson and Mitchell, 1984). In an extensive synthesis of the existing literature, Forbes (2007) clustered prior research into two dominant perspectives. The first perspective highlights the benefits of comprehensiveness, suggesting that decision-makers can enhance their strategic understanding of a certain situation by gathering more information (i.e. the effectiveness perspective). The second perspective addresses the costs associated with gaining such comprehensiveness, especially regarding the time and resources consumed by the decision-making process relative to those benefits (i.e. the efficiency perspective).

The effectiveness perspective argues that greater information comprehensiveness leads to better decisions, making the overall decision process more rational (Fredrickson, 1984). This line of thought was conceptualized by Fredrickson and Mitchell (1984), who defined comprehensiveness to refer to the “extent to which organizations attempt to be exhaustive or exclusive in making and integrating strategic decisions” (p. 402). Firms that aim to achieve more rational decision-making have to put greater effort into gathering and processing information, for instance, by employing quantitative analytic techniques more extensively (Dean and Sharfman, 1993). In this vein, prior studies have shown that firms devote considerable effort to gathering and processing information during their decision-making activities to obtain the specific resources required for competitive advantages (e.g. Makadok and Barney, 2001).

The efficiency perspective also incorporates the costs associated with achieving the benefits of comprehensiveness (Hough and White, 2003). While a slower decision speed allows for a more thorough information search, speed itself is also argued to be a relevant prerequisite for decision quality (Judge and Miller, 1991). In this sense, Bower and Hout (1988) found that organizations that have the capability to make fast decisions have a competitive advantage because of “their ability to preempt new sources of value and force other companies to respond to their initiatives” (p. 144). Decision-makers may adopt new products, business models, or efficiency-gaining processes early on and may create faster preemptive organizational combinations that enable economies of scale and knowledge synergies (Baum and Wally, 2003). Longer decision-making processes also consume more resources from organizations and the actors involved in the process. Hence, shorter decision-making processes enable firms to capitalize faster on competitive advantages and reduce the resources consumed by the decision-making process.

Information asymmetry in acquisition decision-making

In his seminal article, Akerlof (1970) put forward the idea of a “market for lemons,” in which information asymmetries between market participants may lead to adverse selection problems. This framework is particularly appropriate when considering acquisition decisions. Information asymmetries between the acquirer and the target increase the difficulty of assessing the true value potential of the target (Wu and Reuer, 2021). Moreover, the seller might even be inclined to misrepresent the target’s quality (Reuer and Ragozzino, 2008). Consequently, information asymmetries can result in critical details about a deal being missed, which may subsequently lead to unfavorable acquisition outcomes (Coff, 1999).

Acquirers invest significant effort in conducting due diligence to reduce information asymmetry (Reuer and Ragozzino, 2008; Wangerin, 2019). After the initial screening of public information, acquirers obtain access to private information that is not available to the public, denoting the formal beginning of the due diligence process (Marquardt and Zur, 2015; Pavićević and Keil, 2021). During this process, both parties engage in a mutual learning (Martin and Shalev, 2017), allowing previously unknown information to unravel (Chakrabarti and Mitchell, 2016).

In the due diligence process, acquirers undergo a belief-updating process regarding the value potential of the deal (Puranam et al., 2006), which ultimately affects the acquirer’s decision to continue with the commitment to buy or to walk away (Kirtley and O’Mahony, 2023). This updating process requires iterative deliberation, making the length of due diligence an important contributor to its effectiveness (Pavićević and Keil, 2021). Due to time compression diseconomies, shortening the due diligence process too much can lead to diminishing returns (Dierickx and Cool, 1989). Through a longer due diligence process, firms can assess, gather, and analyze more information, thereby reducing information asymmetry (Samuelson, 1984).

The more informed the acquirer is, the less likely it is that the acquirer will make a mistake in the acquisition process by, for example, overpaying for the target (Coff, 1999). Consistent with this, Pavićević and Keil (2021) found in a recent study that a longer due diligence process lowers the risk of cognitive biases, leading to higher-quality acquisition decision-making processes. Similarly, Cuypers et al. (2017) found that acquirers’ ability to secure value depends on the magnitude of the information asymmetries and how acquirers cope with the uncertainty. Thus, longer due diligence processes may be beneficial, as firms can better mitigate information asymmetries, potentially increasing value creation in deals.

However, as the due diligence process lengthens, the use of scarce resources increases significantly, along with costs for external services from audit, legal, and consulting firms, as well as investment banks (Cole et al., 2016). For example, Lajoux (2010) notes that buyers spend millions of dollars uncovering private information, attempting to identify every possible risk before making a decision, even though “firms typically have substantial stores of private information that is not visible through arms-length due diligence” (Chakrabarti and Mitchell, 2016: 37). Hence, the length of due diligence processes has a diminishing marginal utility, which raises the issue of efficiency (Angwin et al., 2015; Reuer and Sakhartov, 2021).

In addition to the increasing costs associated with longer due diligence processes, a longer due diligence process will also delay the realization of the anticipated synergies (Daley et al., 2024). Hence, new growth areas or technological advances are achieved later, creating opportunity costs arising from longer decision-making processes (Cording et al., 2008) and potentially allowing competitors to tap into new opportunities earlier (Carow et al., 2004; McNamara et al., 2008). A longer pre-deal due diligence process may also decrease the potential first-mover advantages and the competitive advantages gained through an acquisition (Bower and Hout, 1988). Hence, a longer due diligence process can ultimately diminish the overall net present value of the deal.

These competing forces lead to an intricate balance between insufficient and excessive due diligence efforts. On one hand, firms may conduct insufficient pre-deal due diligence, missing critical information that diminishes the deal’s value potential. On the other hand, firms may overcommit to due diligence efforts, diminishing the deal’s value potential due to the excessive effort. Due to the interplay of these competing forces, the decision comprehensiveness theory leads us to our baseline hypothesis, according to which the length of the due diligence process on the stock market returns to the acquiring company follows an inverted U-shaped curve:

Contingencies of industry conditions in acquisition decisions

Extensive research has documented the importance of companies to align with relevant aspects of their external environments, and how external contingencies influence strategic decisions (e.g. Donaldson, 1987). In strategic decision-making, industry conditions can simultaneously offer opportunities and impose constraints (Hrebiniak and Snow, 1980). In the context of acquisitions, these conditions shape how acquirers assess potential targets and structure deals.

We examine three industry conditions that could influence an acquirer’s decision-making context using the dimensions introduced by Dess and Beard (1984): munificence, complexity, and dynamism. These dimensions have been frequently used in management research (Connelly et al., 2016; Malhotra and Harrison, 2022) and have different implications for the level of uncertainty experienced by the acquiring firm (Boyd, 1995). Furthermore, prior research suggests that these industry conditions can exert a particularly strong influence on firms’ strategic decision-making processes (Brauer and Wiersema, 2012; Judge and Miller, 1991).

Industry munificence and due diligence length

Industry munificence is associated with abundant resources and sustained growth (Dess and Beard, 1984). This abundance of resources not only ensures firms’ basic survival but also empowers them to pursue various strategic objectives (Castrogiovanni, 1991). Moreover, the growth prospects of firms operating in munificent industries are bolstered by the diverse range of strategic options available (Tushman and Anderson, 1986). In essence, industry munificence encapsulates the overall attractiveness and potential profitability within a specific industry, enabling firms to simultaneously engage in multiple strategies to maintain or enhance their competitive edge.

Drawing from Luciano et al. (2020), who argue that munificent environments have lower information processing requirements, the need to base acquisition decisions on extensive information collection may be relaxed. As information gathering during the due diligence process generally has a marginally diminishing utility beyond the inflection point (Angwin et al., 2015; Reuer and Sakhartov, 2021), firms in industries with high growth potential may not need as exhaustive information to be able to make profitable acquisition decisions. To the contrary, firms might find it more beneficial to streamline their information-gathering processes (Kelly and Amburgey, 1991). Prior research has also argued that munificent industries carry a lower downside risk, as adverse decisions are less likely to be severely penalized (Speed, 1994).

Moreover, the speed of decision-making can play a pivotal role in securing access to critical resources. Munificent industries attract new entrants into the market, making the market increasingly competitive (Randolph and Dess, 1984). Given that acquisitions are frequently used to capture growth opportunities, favorable market conditions also heighten the competition for attractive targets. Consequently, the importance of faster due diligence processes increases in order for firms to secure first-mover advantages.

While a potential counterargument would be that in munificent industries, there are more targets available for potential acquisition, making the speed of acquisition decision-making less relevant, we argue that in munificent industries, acquirers face both a “race” to secure the optimal targets (justifying faster decisions) and the luxury of multiple good options (limiting the benefits of extensive due diligence). Therefore, based on decision comprehensiveness theory, we hypothesize that in munificent industries, the optimal balance between due diligence comprehensiveness and speed is achieved earlier than in less munificent industries:

Industry complexity and due diligence length

Industry complexity is associated with greater stakeholder heterogeneity in terms of the number and size of stakeholders (Dess and Beard, 1984). A larger and more diverse set of stakeholders leads to greater intra-industry inequality (Miles et al., 1993). Thus, in complex industries, there is a wider array of factors that determine success (Heeley et al., 2007), and within these industries, the connections among resources, competition, and performance are less clear-cut (Ndofor et al., 2015). Under these circumstances, understanding the relevant causal relationships may be more difficult, thereby requiring greater effort in strategic decision-making.

As industry complexity increases, the importance of comprehensive information gathering and processing becomes more pronounced (Snowden and Boone, 2007). This heightened need is driven by the multilayered dynamics inherent in complex industries (Ndofor et al., 2015). Such industries present a greater risk of misjudgment, highlighting the necessity for a robust and sound information base attained through rigorous due diligence. Under these conditions, extensive analysis is paramount to discerning and comprehending the different interconnections and variables relevant to the success of an acquisition transaction. Supporting this assertion, Siggelkow and Rivkin (2005) argued that companies within complex environments need a broader information-gathering approach to develop a sound understanding than companies operating in simpler environments. Moreover, in complex environments, more comprehensive information collection and analysis can serve not only to mitigate risks but also to uncover latent synergy potentials, nuanced interdependencies, and emerging market trends that might otherwise remain obscured without sufficient informational depth.

Comprehensive due diligence is more important, as it can be challenging to fully understand key aspects of deal potential, such as the product-market space occupied by various competitors, the presence of niche opportunities, the bargaining power of suppliers, and the potential for collaboration with competitors (Malhotra and Harrison, 2022). Structured procedures and protocols may prevent overlooking obscure deal aspects that should be incorporated accordingly, especially in complex environments (Judge and Miller, 1991). Prior research has also more generally argued that the breadth and depth of industry knowledge and more elaborate information processing contribute to competitive advantage in more complex industries (Ferrier, 2001; Luciano et al., 2020). In this vein, including experts, such as the board of directors, and their expertise in the due diligence process should be beneficial under these conditions, which, however, comes at the cost of slower decision-making (Kim et al., 2011).

Hence, we argue that in complex industries, comprehensive information collection and analysis are relatively more important than speed to make an optimal decision. Therefore, we hypothesize that in more complex industries, the optimal balance between due diligence comprehensiveness and speed is reached later than in less complex industries:

Industry dynamism and due diligence length

Industry dynamism is associated with market instability and a lack of predictability (Dess and Beard, 1984). Hence, industry dynamism describes the extent to which a particular industry is in flux and the speed at which change takes place. New product introductions, novel technologies, breakthroughs in substitute inputs, and regulatory changes occur more often in dynamic industries, increasing overall market volatility (Chen et al., 2017). In essence, industry dynamism influences strategic decision-making by necessitating rapid adjustments, proactive market monitoring, and flexibility, prompting companies to adopt agile and adaptive approaches to remain competitive (Schilke, 2014).

Acquisition opportunities arise at short notice but also disappear just as quickly, resulting in the relevant information becoming obsolete (Bourgeois and Eisenhardt, 1988). As information loses its value, acquirers have to capitalize on it before the underlying assumptions are no longer valid (Eisenhardt, 1989). Due to the short-lived nature of information under dynamic conditions, collecting comprehensive information becomes a burden compared to when there are more stable industry conditions. Thus, in dynamic conditions, faster utilization of easy-to-grasp information is needed. Consistent with this, Davis et al. (2009) argued that highly structured procedures for strategic decision-making are of limited value in dynamic environments and proposed the use of “simple rules” to speed up decision-making.

Creating competitive advantage through acquisitions in dynamic environments requires the ability to adapt to changing conditions. An extensive due diligence process may result in a realized deal failing to meet its initially defined objectives, as changes may have already occurred in the meantime (Karim et al., 2016). For example, Alphabet’s (Google) founder and former CEO Larry Page has often been quoted for using a “toothbrush test” to quickly assess potential acquisition targets for Alphabet asking whether the company offers a service that “you will use once or twice a day.” Hence, being able to adapt to changes quickly by carrying out acquisitions with a shorter due diligence time may enhance firms’ ability to capitalize on these competitive actions under these conditions (McNamara et al., 2008). Therefore, faster due diligence processes are likely to be better suited to meeting the demanding requirements of a rapidly changing environment and to reducing the risk of “missing the window” (Judge and Miller, 1991). The marginally decreasing benefits of comprehensive due diligence are outweighed earlier by the benefits of speed than in less dynamic industries. Accordingly, we hypothesize that in dynamic industries, the optimal balance between due diligence comprehensiveness and speed is reached earlier than in less dynamic industries:

Methods

Sample and data

We test our hypotheses using a sample of acquisitions of US firms listed in the S&P 1500 Index at least once between 2003 and 2018. We extracted acquisition-related information from the Refinitiv SDC Platinum database. We followed prior acquisition literature (Moeller et al., 2004) and excluded firms from the financial sector (SIC codes 6000–6999) due to different regulatory requirements. While data on pre-deal due diligence length is not readily available in any research database, acquirers and targets are required to file statements with the SEC related to an acquisition when the acquisition needs shareholder approval or includes the issuance of new stock. We thus followed prior literature (e.g. Marquardt and Zur, 2015; Pavićević and Keil, 2021) and manually extracted these acquisition-related SEC filings from SEC EDGAR platform. We used the merger background sections of DEFM14A and S-4 statements (Boone and Mulherin, 2007). We removed acquisitions for which the filings are not available from our sample. This is essentially the case for cash-only deals and deals being structured as a tender offer or where the acquirer already owns a large stake in the target, and thus no DEFM14A or S-4 needs to be filed. 1 We retrieved firm-level financial data for the acquiring and target firms from Refinitiv Datastream. After excluding observations with missing data our final sample included 501 acquisitions. The detailed sample composition is shown in Appendix A.

Main variables

Due diligence length

We measured the length of the pre-deal due diligence process as the period between signing an NDA and the date of announcement, following prior literature (Marquardt and Zur, 2015; Pavićević and Keil, 2021). We manually scanned the background sections of S-4 and DEFM14A filings. In the background sections of these filings, all communication between the target and the acquiring firm is described in great detail, including the signing date of the NDA. If we could not identify the date of the NDA in this section, we searched the remaining corpus of the filing. We then calculated the difference in days between the NDA date and the deal announcement date (as reported in the SDC database) to measure Due Diligence Length. Larger values indicate a slower pace and a longer due diligence, potentially allowing for more information processing, while smaller values represent a faster pace and a shorter due diligence.

Cumulative abnormal return

We measured the short-term stock market returns to the acquiring firm based on the 3-day cumulative abnormal return (CAR) to the acquisition announcement. Although CARs have been used extensively in prior acquisition research as a measure of acquisition performance (Devers et al., 2020; Haleblian et al., 2009; King et al., 2021), they have also been criticized as an imperfect measure that does not correlate with other measures of acquisition performance and the longer-term acquisition performance (e.g. Oler et al., 2008; Zollo and Meier, 2008). We nevertheless chose to use this short-term measure of investor reaction because it allowed us to match the due diligence length directly to an individual acquisition, rather than examining average due diligence lengths over multiple acquisitions, and to avoid potential confounding events (McWilliams and Siegel, 1997). Moreover, we found it informative to examine whether and when different due diligence process lengths cause observable investor reactions.

While we do not expect investors to go through the SEC filings of the acquiring companies to find out how long the due diligence process was, the investors and media often enquire about the speed of decision-making in the investor events in which an acquisition is being announced. For example, when Dow Chemicals acquired Rohm et Haas with an exceptionally high acquisition premium at record speed, Dow Chemical’s CEO Andrew Liveris was quite explicit that they had to “move fast in just a few weeks” to do the deal. Similarly, when Salesforce bought Slack, Marc Benioff, the CEO and founder of Salesforce, said that he had not expected the company to be able to do any deals during the COVID-19 pandemic before the opportunity to buy Slack “suddenly emerged.” In addition to explicit public references to the speed at which a given deal was made, investors are also able to observe multiple different deal characteristics and make their own assessments of whether they believe in the deal or not, and how well-justified the deal is. Depending on the speed with which the due diligence process was conducted, the deal might entail different cues that are likely to signal the quality of the deal for the investor community.

Industry conditions

We determine the acquirer’s industry conditions of munificence, complexity, and dynamism using the entire Datastream database to calculate the industry condition variables. 2 Industry complexity represents the heterogeneity in the number and size of different market participants (Dess and Beard, 1984). We measure Industry Complexity as one minus the Herfindahl Index, which displays the sum of the squared market shares of all firms in a given Fama-French 17 industry category per year (Malhotra and Harrison, 2022). Industry munificence represents an industry’s ability to support growth and an abundance of resources. We measure Industry Munificence as the predicted value of a regression of industry sales from the last 5 years to the current year divided by the average industry sales for each Fama-French 17 categories. Industry dynamism refers to the transience of the industry and its underlying pace of change (Connelly et al., 2016). Thus, we measure Industry Dynamism as the standard error of the above-described regression divided by the average industry sales for each Fama-French 17 categories.

Control variables

We account for a variety of factors at the acquirer, target, and deal levels that might also influence acquisition performance. First, we control for Acquirer Size using the natural logarithm of employees (Kim et al., 2011). We assess firm performance through market-based Acquirer Tobin’s Q and accounting-based Acquirer RoA. Recognizing that financial slack may influence acquisition decisions (Hayward and Hambrick, 1997), we control for Acquirer Slack, defined by the asset-to-liability ratio. Potential penalties for deal termination, which may affect market perceptions (Officer, 2003; Pavićević and Keil, 2021), are captured using a binary variable, Acquirer Termination Fee. As acquisition advisors might potentially influence the quality of acquisition outcomes, we include a control variable Acquirer Advisors, which is the number of financial advisors provided in the SDC database (Pavićević and Keil, 2021). Finally, to account for the acquirer’s experience in acquisition decisions, we include Acquisition Experience, quantifying the log-transformed number of deals during the three preceding years (Laamanen and Keil, 2008).

With regard to target-related controls, we control for a series of variables analogous to those for acquirers, including Target Size, Target Tobin’s Q, and Target Termination Fee. In addition, we account for Target Growth Opportunities as the target market capitalization divided by total liabilities (Pavićević and Keil, 2021) and Target Analyst Coverage as the number of analysts following the target firm. Finally, at the deal level, we include Diversifying Deal as a binary variable for deals outside the same Fama-French 17 industry category (Martin and Shalev, 2017). The nature of a deal’s financing is displayed as Cash Payment, indicating the proportion of cash used in the transaction (King et al., 2021). In addition, we account for Relative Deal Size, which juxtaposes the transaction value against the acquirer’s market capitalization from the previous year (Goranova et al., 2017). Finally, we determine if a transaction occurred during periods of heightened acquisition activity. While our approach for the measurement of Acquisition Wave aligns with the methodology set out by Carow et al. (2004), we adopt the time limit for acquisition waves as 3 years before and after peaks, as suggested by McNamara et al. (2008).

Analysis

Given the continuous nature of the dependent variable in our analyses, we employed linear regression models. Following recommendations made by previous literature (Certo et al., 2016), we ran standard ordinary least squares (OLS) regressions and addressed the interdependence of observations by clustering standard errors at the individual firm to account for potential heteroscedasticity (Petersen, 2009). We also included year and industry effects using Fama-French 17 industry categories. For regression models containing interaction terms, we mean-centered all predictor variables, which allowed the main effects to be interpreted at the average level of the moderator. We also winsorized continuous variables at the 1st and 99th percentiles to reduce the effect of potential outliers. We used the 1-year lagged values to alleviate reverse causality concerns for the control variables. To test Hypothesis 1, predicting an inverted U-shaped relationship between due diligence length and short-term market returns to the acquiring firm, we estimated the following regression model:

where indices i and t stand for firm and time, Controls is a vector of control variables, Year and Industry are fixed effects, and ε is an error term. y is CAR and x is Due Diligence Length. To test Hypotheses 2-4 according to which industry conditions moderate the inverted U-shaped relationship, we included an interaction term between due diligence length and the industry conditions. Following prior studies (Aiken and West, 1991; Veltrop et al., 2018), we included only a linear-by-linear interaction term consistent with the arguments developed in our hypotheses. This reflects our assumption that the curvilinear relationship holds across all levels of the industry conditions, while the overall form of the curvilinear relationship appears largely stable and that the inflection point shifts depending on the industry condition (Haans et al., 2016). Thus, we estimated the following model:

where z represents the industry conditions. The hypothesized moderating effects of the industry conditions are captured by β4 and the interaction terms of x and z. A negative sign for Hypothesis 2 on industry munificence, a positive sign for Hypothesis 3 on industry complexity, and a negative sign for Hypothesis 4 on industry dynamism, respectively, would be in line with our expectations.

To mitigate a potential selection bias, we also conducted a Heckman correction to account for the potential endogeneity arising from the composition of our sample (Certo et al., 2016). Specifically, as we point out in our sample selection description, due diligence data might not always be available. Thus, we sought a suitable exclusion criterion that would affect the availability of due diligence data in the form of the necessary S-4 and DEFM14A filings, but that would not impact investor reactions. Institutional investors are associated with increased professionalization of firms’ corporate governance, making it more likely that firms’ charters or bylaws require firms to more closely interact with their shareholders, ultimately resulting in increased transparency (Connelly et al., 2010). In turn, higher shareholdings of institutional investors on the sides of the acquirer and the target should result in a higher likelihood of available disclosure regarding the acquisition and, thus, the signing date of the NDA. We calculated the average shareholdings of institutional investors across the acquiring and target firms (Institutional Investors) and used this as our exclusion criterion. We ran a first-stage probit regression on the likelihood of due diligence data availability, including our control variables and Institutional Investors (displayed in Model 1 of Appendix C), and derived the inverse Mills ratio (InvMills), which we then included in all our second-stage regressions.

Results

Descriptive statistics

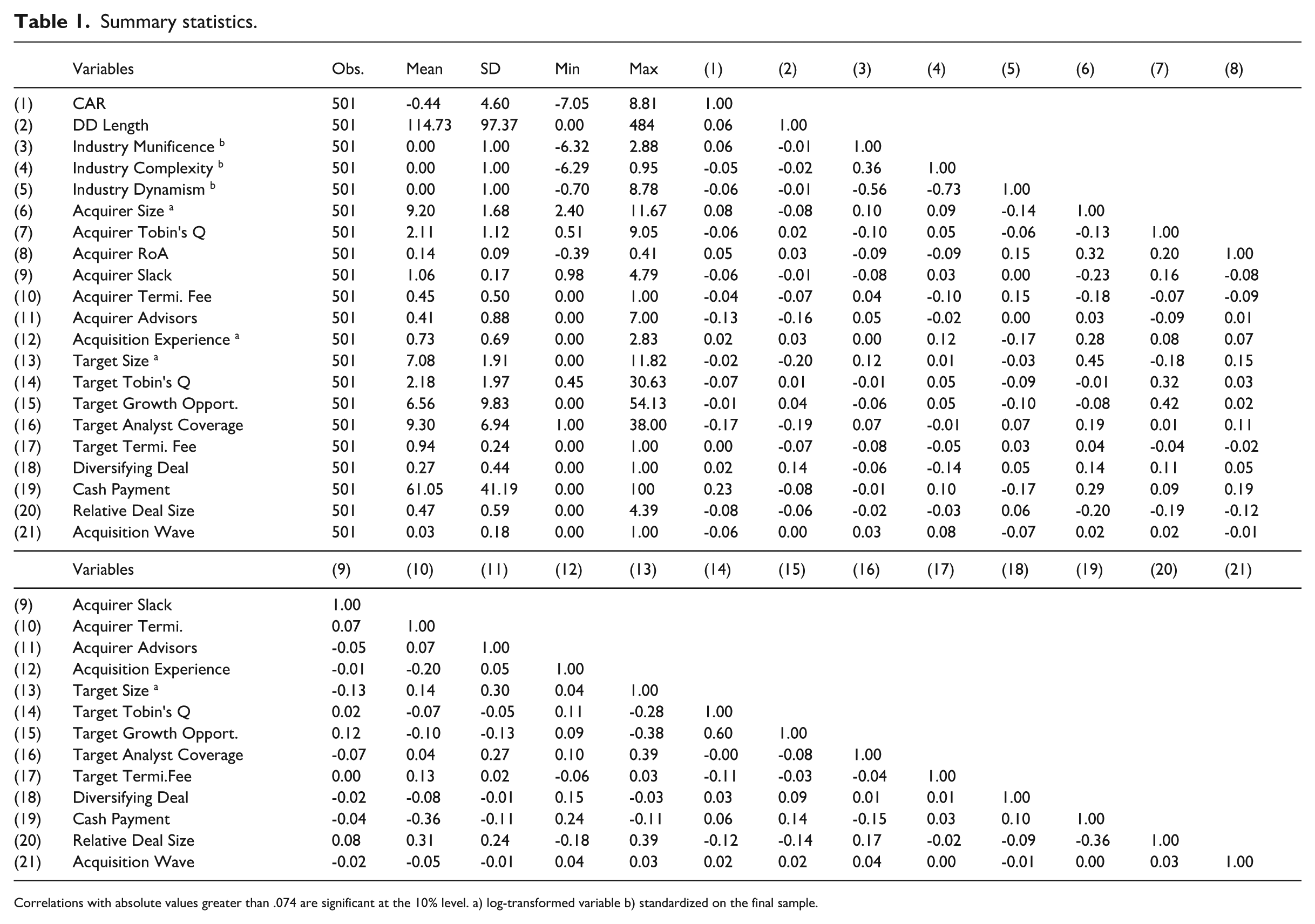

Table 1 displays the summary statistics and correlation coefficients of all the variables used in the regression models. The means and standard deviations are in line with the findings of prior acquisition research (Cuypers et al., 2017; Goranova et al., 2017). The average CAR to the acquiring companies is slightly negative. The mean value of Due Diligence Length is 114.73 days, which aligns with the study by Pavićević and Keil (2021). The industry condition variables are standardized values and, therefore, have means of zero and standard deviations of one. To compare the validity of our calculations with those of previous studies, we calculated the variables on a firm-year sample for the entire S&P 1500 Index, obtaining variables with summary statistics similar to those of Malhotra and Harrison (2022).

Summary statistics.

Correlations with absolute values greater than .074 are significant at the 10% level. a) log-transformed variable b) standardized on the final sample.

Regarding correlations, we find that Due Diligence Length is slightly positively but insignificantly associated with CAR. In terms of direct associations, Industry Dynamism and Industry Complexity are negatively correlated with CAR, while Industry Munificence is positively correlated. The correlation analysis across all control variables further indicates that multicollinearity should not be a major concern. The few higher correlations (e.g. Acquirer Size and Target Size) are economically justified. To further assess this issue, we calculate variance inflation factors and observe that all values are below 5.

Empirical results

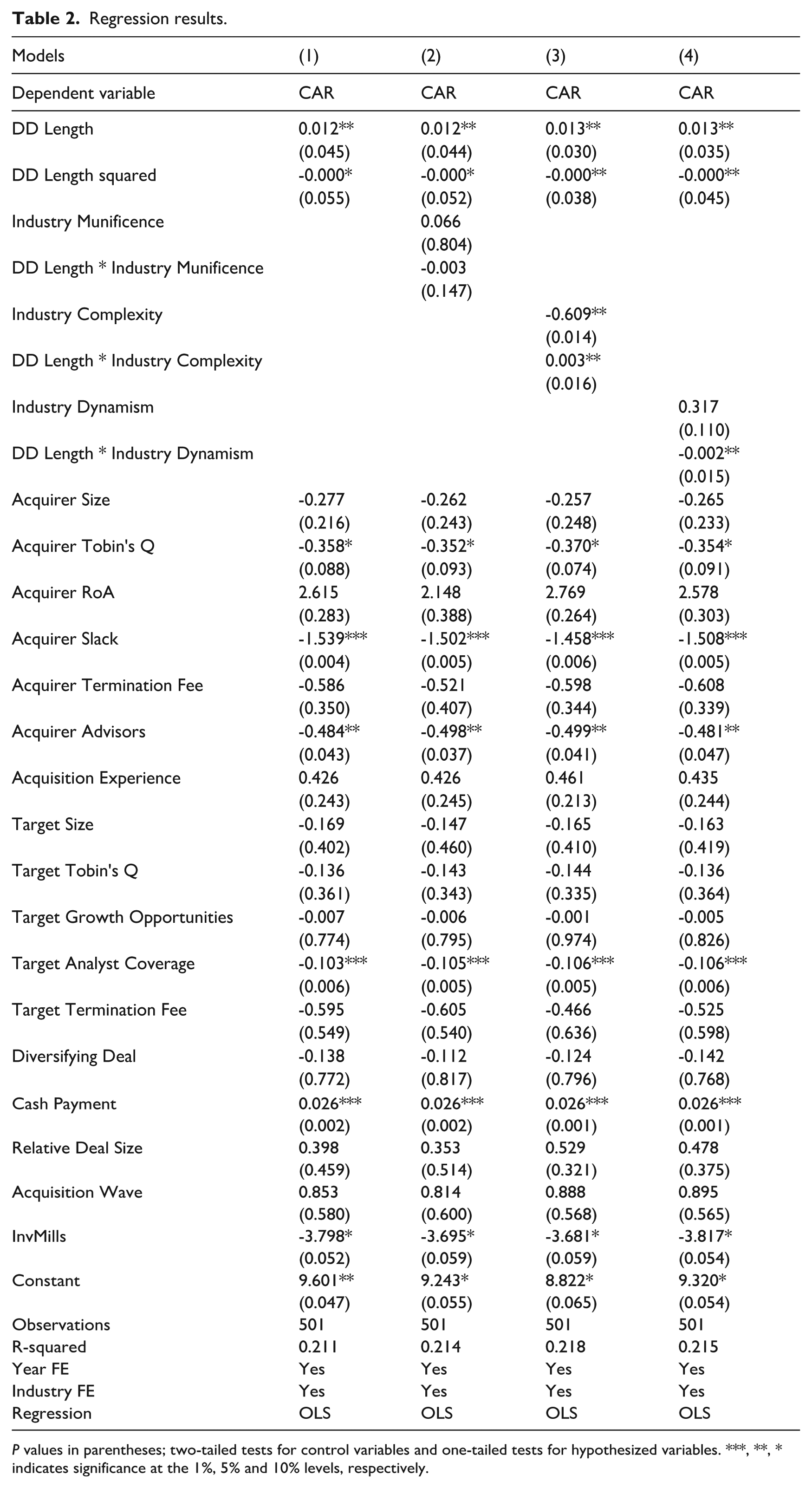

Table 2 provides the results of our main regression models. In Model 1, we test Hypothesis 1 in which we predicted an inverted U-shaped relationship between due diligence length and acquirer stock market returns. We find a positive coefficient for the linear term (β = 0.012; p = 0.045) and a negative coefficient for the squared term (β = −0.000; p = 0.055) of Due Diligence Length predicting CAR. This means that due diligence length is, on average, positively related to investor reactions, but that this relationship becomes less positive or even negative for longer due diligence processes. To further verify the existence of the inverted U-shaped relationship, we utilize the Stata command utest developed by Lind and Mehlum (2010). The test reported in Appendix B confirms that (1) the inflection point at 235.43 days is well within the data range, (2) the slope of due diligence length left of the inflection point is positive and statistically significant, while its slope right of the inflection point is negative and statistically significant, and (3) the test statistic for the overall presence of an inverted U-shaped relationship is also statistically significant. Collectively, the results strongly support our assumption of an inverted U-shaped relationship.

Regression results.

P values in parentheses; two-tailed tests for control variables and one-tailed tests for hypothesized variables. ***, **, * indicates significance at the 1%, 5% and 10% levels, respectively.

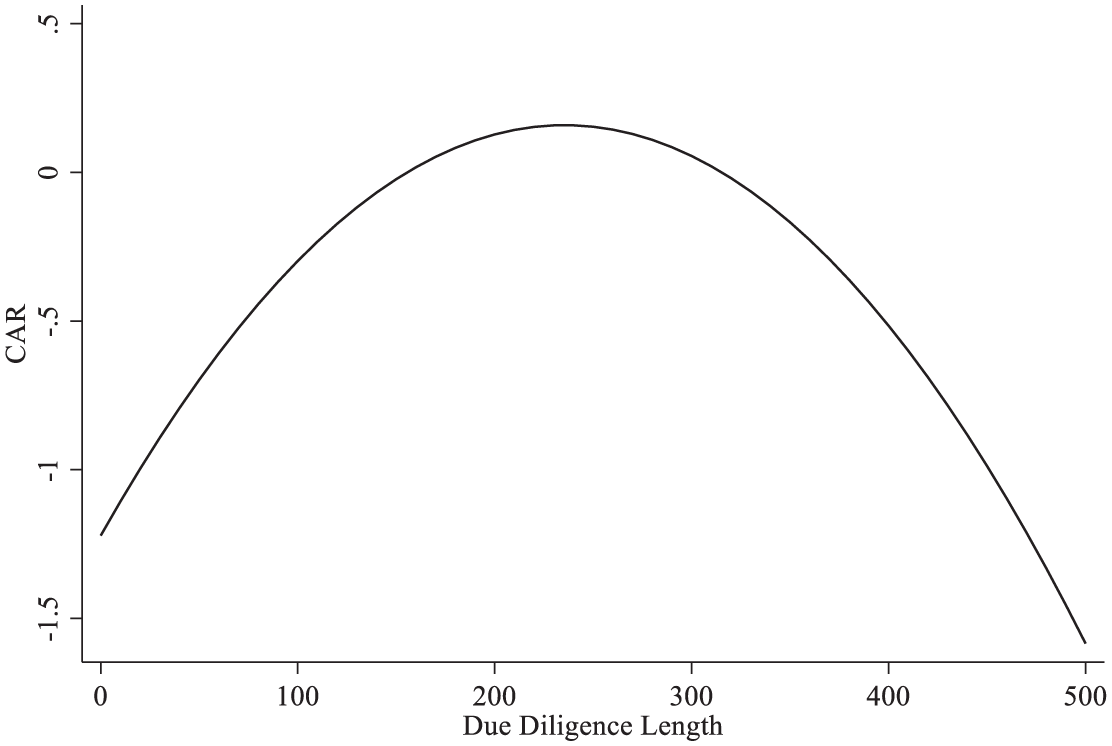

In addition to the statistical testing, we plotted the results in Figure 1 to provide a graphical illustration. The figure shows a fully inverted U-shape whose inflection point reaches positive values of CAR, while moving away from the inflection point results in lower values of CAR transitioning to values below zero. To assess the economic significance, we calculate the predicted CAR at the inflection point, the inflection point minus one SD, and the inflection point plus one SD. We find a CAR of 0.159% at the inflection point of 235.43 days of due diligence, which decreases to -0.058% when moving to 142.06 days (235.43 – 97.37) or 328.80 days (235.43 + 97.37) of due diligence. These deviations from the inflection point reflect losses in the firms’ average market capitalization of $55,202,630.3,4 Collectively, the results provide support for Hypothesis 1.

Margins plot—Due Diligence Length and CAR.

In Model 2, we investigate Hypothesis 2, in which we predicted that industry munificence negatively moderates the curvilinear relationship between due diligence length and acquirer stock market returns. The results show a negative but insignificant coefficient for the interaction term between Due Diligence Length and Industry Munificence (β = −0.003; p = 0.147). This means that the inflection point does not significantly shift, while we continue to find evidence for the curvilinear relationship. Thus, our results do not provide support for Hypothesis 2.

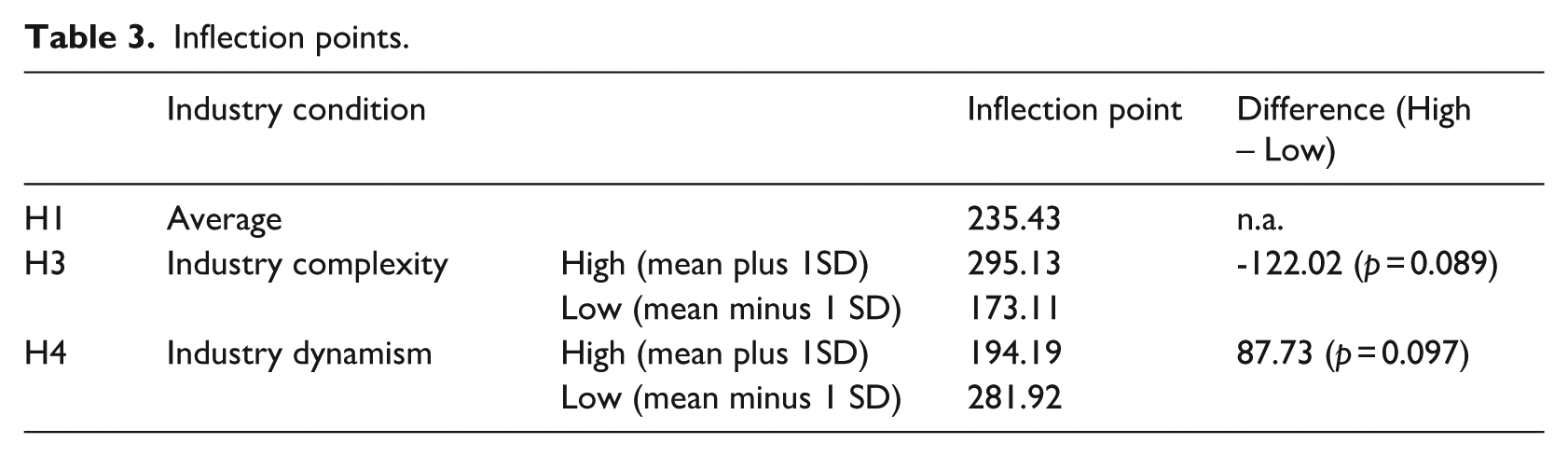

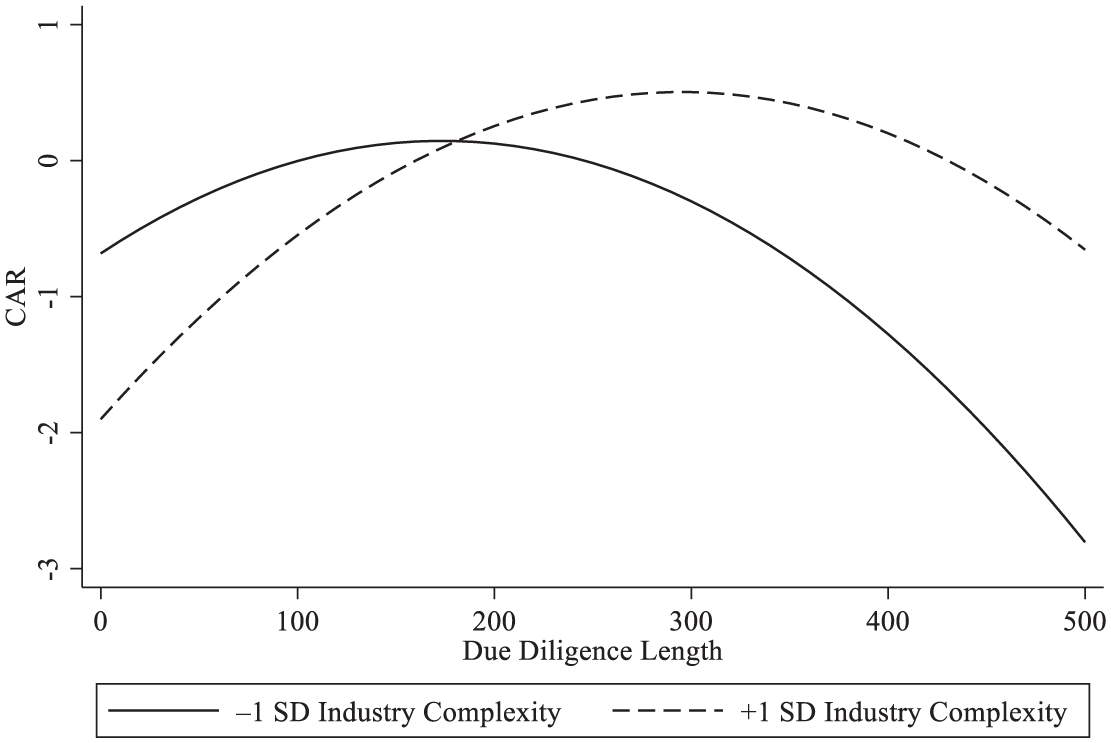

In Model 3, we examine Hypothesis 3, in which we predicted a positively moderating effect of industry complexity on the main relationship. We find a positive and significant coefficient for the interaction term between Due Diligence Length and Industry Complexity (β = 0.003; p = 0.016) predicting investor reactions. This suggests that under higher industry complexity, the inflection point shifts to the right, making the negative (positive) effects of shorter (longer) due diligence more pronounced. Specifically, the results displayed in Table 3 show that the inflection point in high industry complexity (mean plus one SD) shifts to 295.13 days and to 173.11 days in low industry complexity (mean minus one SD). We find that the difference between the inflection points in high and low industry complexity of 122.02 days is statistically significant (p = 0.089).

Inflection points.

To gain further insights into the nature of this interaction effect, we plotted the curvilinear relationship of due diligence length and investor reactions at high (mean plus 1 SD) and low levels (mean minus 1 SD) of industry complexity. The plot in Figure 2 is consistent with H2 in that the inflection point (i.e. the maximum value of investor reactions) occurs for higher values of due diligence length in industries with higher complexity. In terms of economic significance, we calculate the predicted CAR under high industry complexity at the inflection point (295.13 days) and at the inflection point plus one SD (392.50 days). We find a CAR of 0.504% for 295.13 days and of 0.242% for 392.50 days, resulting in a difference of the firms’ average market capitalization of $66,650,180. This difference is about 20% larger than for the average industry conditions. Thus, these results provide support for Hypothesis 3.

Margins plot—Due Diligence Length and CAR: Industry Complexity.

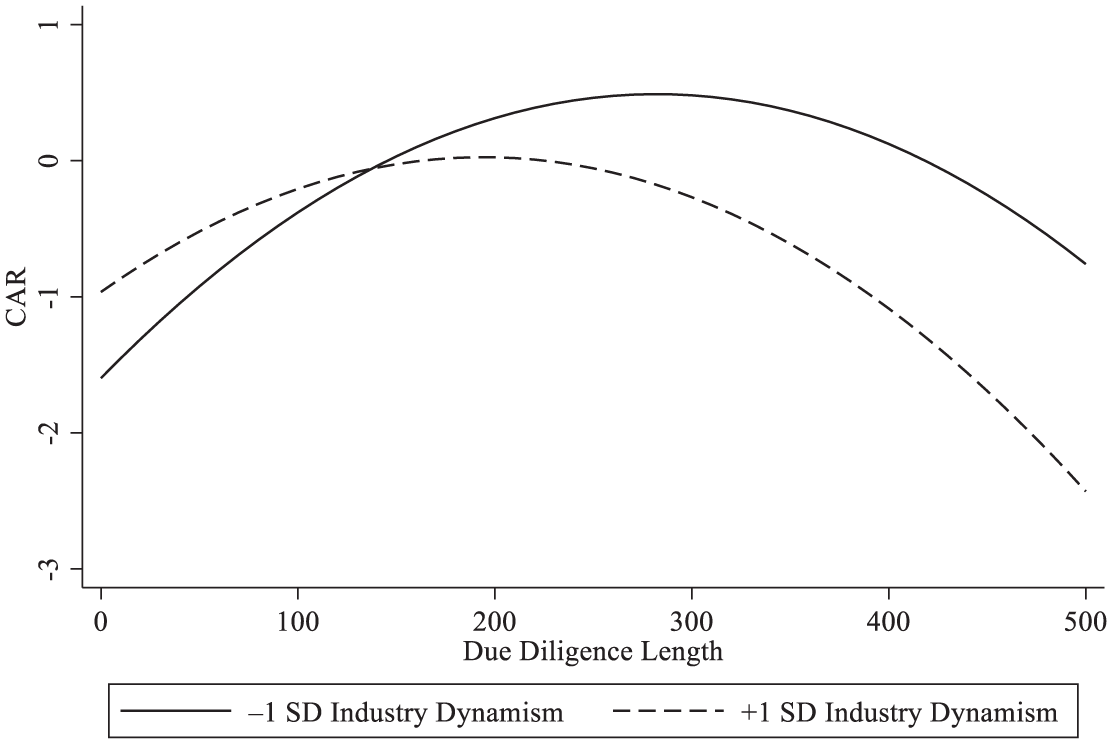

In Model 4 of Table 2, we test Hypothesis 4 regarding the negative moderation effect of industry dynamism. The results document a negative and significant coefficient for the interaction term between Due Diligence Length and Industry Dynamism (β = −0.002; p = 0.015). This finding translates into a shift of the inflection point to the left under high industry dynamism, highlighting a tendency for shorter due diligence. To be more precise, the results displayed in Table 3 indicate that the inflection point in high industry dynamism (mean plus one SD) moves to 194.19 days and to 281.92 days in low industry dynamism (mean minus one SD). The resulting difference between the inflection points in high and low industry dynamism of 87.73 days is also statistically significant (p = 0.097). The margins plot displayed in Figure 3 confirms this pattern. For the economic significance, we calculate the CAR under high industry dynamism at the inflection point (194.19 days) and at the inflection point plus one SD (291.56 days). We find a predicted CAR of 0.026% for 194.19 days and of -0.223% for 291.56 days. This deviation from the inflection point results in a difference of the firms’ average market capitalization of $63,343,110, which is about 15% larger than for the average industry conditions (as calculated for H1). Therefore, we find evidence that also supports Hypothesis 4.

Margins plot—Due Diligence Length and CAR: Industry Dynamism.

Endogeneity checks and robustness tests

Endogeneity checks

Due diligence length is not randomly assigned, but rather a strategic choice, and thus, unobserved factors could drive due diligence length and investor reactions at the same time. We used several methodological approaches to tackle this concern.

First, we ran 2SLS regressions, which required us to find instruments that satisfy the relevance condition of being correlated with the endogenous variable and the exogeneity condition of being uncorrelated with the error term in the second stage (Semadeni et al., 2014). The instruments are included in a first-stage regression predicting the potentially endogenous variable (Due Diligence Length). The predicted values from this first-stage regression were then used in the second-stage regressions to estimate the outcome variable (CAR). We followed (Semadeni, Withers, and Certo, 2014)bib84 in applying two instrumental variables. First, we created a dummy variable indicating the presence of a Top-tier Advisor (Goldman Sachs, Merrill Lynch, Bank of America, Morgan Stanley, Citigroup, and JP Morgan). Top-tier advisors have better capabilities that could lead to shorter due diligence. At the same time, previous research has provided no conclusive results regarding their relationship with market returns (e.g. Hunter and Jagtiani, 2003; Ismail, 2010; Servaes and Zenner, 1996). Second, we calculated Performance Asymmetry, the difference between the return on assets of the acquirer and the target. According to Sakhartov and Reuer (2023), acquirer-target performance asymmetry enhances the pre-deal valuation challenge for the acquirer. 5 We then included both Top-tier Advisor and Performance Asymmetry variables and all our control variables in the first-stage regression predicting Due Diligence Length, as displayed in Model 2 of Appendix C. We then used the estimated values for Due Diligence Length in the second-stage regression. Given the complexity of instrumentalizing the polynomial and interaction terms, as well as the increased likelihood of misspecification, we confined ourselves to running 2SLS regressions for Hypothesis 1. The results reported in Model 1 of Appendix D support our predictions.

Second, we employed a two-stage control function procedure, which is well suited for addressing endogeneity concerns in regression models where a potentially endogenous variable interacts with other variables (Pavićević and Keil, 2021; Wooldridge, 2015). Similar to the 2SLS approach, this method has the same first-stage regression (see Model 2 of Appendix C), but then uses the residuals instead of the predicted values. The exogenous variation in the residuals then acts as a control function in the second-stage regressions, addressing endogeneity concerns within the due diligence length (Wooldridge, 2015). The biggest advantage over the 2SLS approach is that the control function does not require us to instrumentalize the polynomial and interaction terms, providing us with a more suitable way to tackle endogeneity. When including the Residuals in all our second-stage regression models, substituting potential confounders that might influence the endogenous regressor (Wooldridge, 2015), our results remain consistent (Appendix D).

Third, since we lack clear exogenous variation and, despite our additional tests, we cannot completely rule out that an omitted variable drives our results, we assessed the sensitivity of our results to bias. Specifically, we calculated the robustness of inference to replacement (RiR). The RiR indicates the percentage of observations that would need to be replaced with zero-effect-size observations to invalidate the results (Busenbark et al., 2021). Unlike the impact threshold of a confounding variable (ITCV), which indicates how strongly a hypothetical omitted variable must correlate with the independent and dependent variables to falsify the results, the RiR offers greater generalizability (Busenbark et al., 2021, 2022). This also makes it more appropriate for models that include interaction effects. For Hypothesis 1, we tested the linear as well as the squared term of Due Diligence Length and found that, respectively, 15.2% and 61.0% of the estimate would have to be due to bias to invalidate the inference. We repeated the test for the interaction terms consisting of the linear term of Due Diligence Length and industry complexity for Hypothesis 3, as well as industry dynamism for Hypothesis 4. For Hypothesis 3 (industry complexity), the corresponding figure was 23.7%, and for Hypothesis 4 (industry dynamism), it is 25.0%. Given these high percentages that would need to be replaced with those having a zero effect, the RiR highlights that it is quite unlikely that a bias could overturn our findings.

Robustness tests

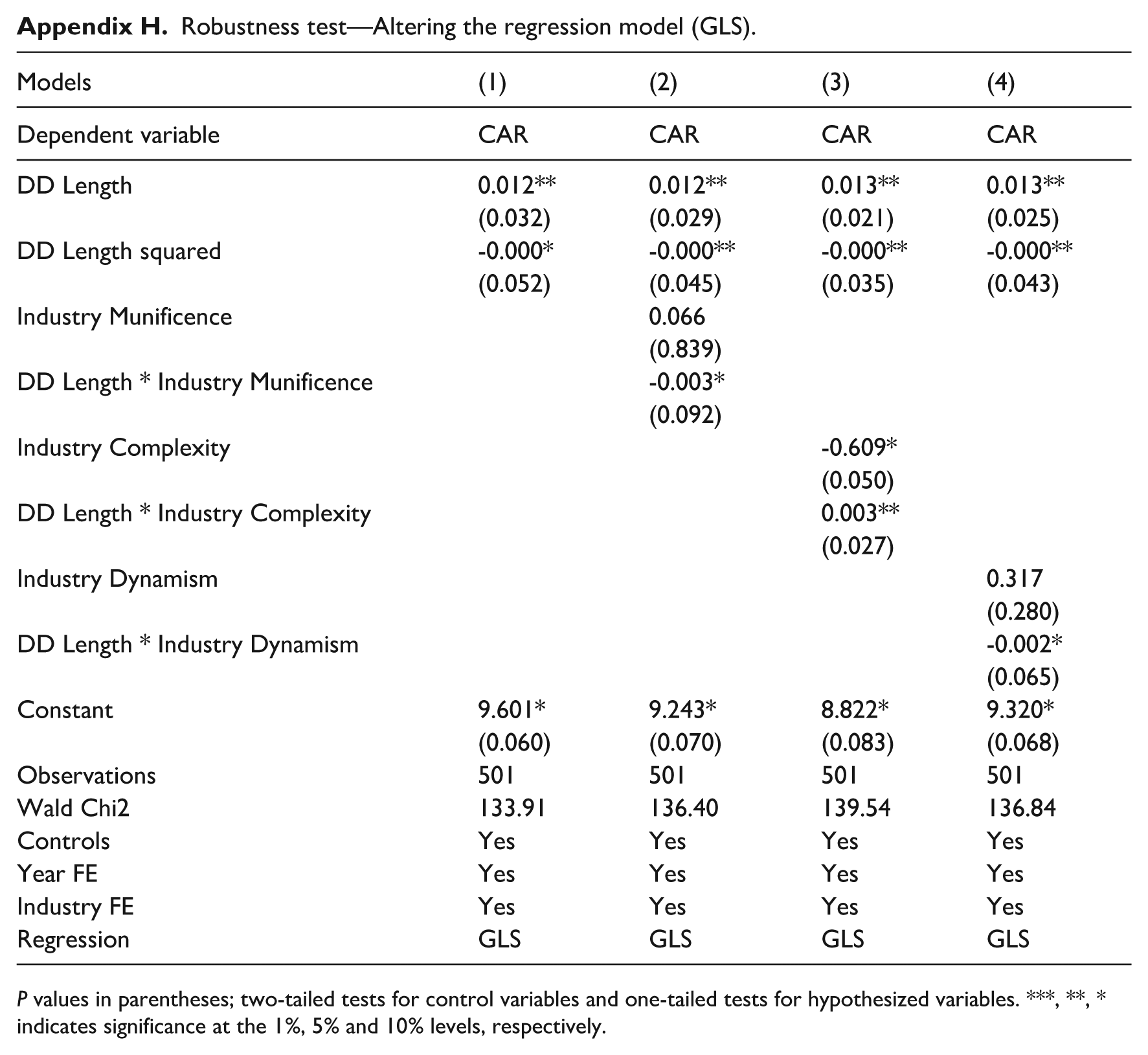

We also run a range of other robustness tests. First, we included acquisition premium and information leakage as additional controls to further attenuate the concerns of omitted factors driving our results. We calculated acquisition premiums using the market value and acquisition price when the SDC variable was missing. We captured information leakage as the change in the acquirer’s share price 30 days before the announcement. Appendix E provides the results, which confirm our primary findings. Second, we changed the calculation of our moderating variables from using the industry of the acquirer to the industry of the target. Appendix F shows the results, which provide further evidence for our main findings. Third, we employ alternative event windows surrounding the deal announcement to compute our dependent variable, CAR. Appendix G displays the results, which remain highly similar. Fourth, we applied an alternative analytical approach to account for multiple occurrences of certain acquirers in our sample. We followed Pavićević and Keil (2021) by implementing generalized least squares (GLS) regressions, accommodating potentially unequal error variance and intra-firm error term correlations. We address the interdependence of observations by clustering standard errors at the firm level and incorporating year and industry effects. The results displayed in Appendix H are also consistent with our main findings.

Discussion

Given adverse selection problems in acquisition decisions, scholars have long sought to understand the antecedents of poor acquisition outcomes (Haleblian et al., 2009; King et al., 2021). Along these lines, previous studies have examined the role of information asymmetries between the parties involved in the transaction (Ragozzino and Reuer, 2023; Reuer and Ragozzino, 2008). However, surprisingly little attention has been given to the tension between the comprehensiveness and speed of the due diligence process and the influence of different external contingencies on this relationship. Drawing on decision comprehensiveness theory (Forbes, 2007; Miller and McKee, 2021), we predict and find an inverted U-shaped baseline relationship between due diligence length and investor reaction to the acquisition announcement. Moreover, we argue and find that different external conditions influence this relationship and the optimal balance between comprehensiveness and speed. Specifically, we examine the effects of industry munificence, industry complexity, and industry dynamism. Based on our empirical analysis, we find that industry complexity moderates the relationship positively in favor of longer due diligence processes and that industry dynamism moderates the relationship negatively in favor of shorter due diligence processes.

Theoretical contributions

We make several contributions to the existing literature. First, we enrich research on the acquisition pre-deal processes by deepening the understanding of the pre-deal due diligence process (Marquardt and Zur, 2015; Pavićević and Keil, 2021; Welch et al., 2020). While previous studies have primarily addressed the question of optimal due diligence length from a theoretical point of view (Daley et al., 2024; Reuer and Sakhartov, 2021), we build on this prior work and provide novel empirical evidence supporting the existence of an inverted U-shaped relationship. In line with the proposition by Daley et al. (2024: 2115) that “in equilibrium, the acquirer engages in ‘too much’ due diligence,” we show that in certain settings, longer due diligence can indeed become detrimental. While Pavićević and Keil (2021) present insights into how the pace of the pre-deal process may reduce managerial biases in acquisitions, we show that in some settings, shorter due diligence processes may also be more beneficial. Our study also responds to the call of Welch et al. (2020) for more research on the due diligence process. Considering that the pre-deal phase is instrumental in determining the prospective value of a deal (Angwin et al., 2015), our study helps to bridge an important research gap on value creation in acquisitions.

Second, our study adds to decision comprehensiveness theory and the broader literature on strategic decision-making by enhancing the understanding of the optimal balance between information comprehensiveness and decision speed (Eisenhardt, 1989; Fredrickson, 1984; Fredrickson and Mitchell, 1984). We enrich this conversation by introducing novel empirical results to the recent debate (Bartkus et al., 2022; Miller and McKee, 2021; Samba et al., 2021). By empirically examining a specific strategic decision-making situation, for which the decision-making speed is accurately documented, we show that the balancing between decision comprehensiveness and speed is contingent on the specific contextual situation.

Moreover, contrary to much of the prior research, we focus on evaluating the quality of specific strategic decisions rather than assessing firm performance as a whole, as suggested by Forbes (2007). This is an important difference, as the mechanisms linking the comprehensiveness-speed continuum to decision quality might differ when observed at the aggregated firm level (Bourgeois and Eisenhardt, 1988; Dean and Sharfman, 1996). In this vein, our study also accounts for the opportunity costs—losses resulting from delayed synergy realization.

Third, we extend existing research on the influence of contingency factors on strategic decision-making (Boyd et al., 2012; Hough and White, 2003). While prior literature has acknowledged the role of contingency factors in shaping strategic decisions (Wally and Baum, 1994) and the ensuing firm outcomes (Malhotra and Harrison, 2022; Siggelkow and Rivkin, 2005), the mechanisms underlying these relationships remain somewhat elusive (Forbes, 2007). To address this, we focus on the characteristics of the information context and the nature of information needed for strategic decision-making (Bergh et al., 2019; Cuypers et al., 2017). Therefore, we put forward a more nuanced understanding of the mechanism between contingency factors and subsequent outcomes. Specifically, we find that industry dynamism renders faster decision-making beneficial, whereas, in complex industries, slower decision-making is more beneficial. Contrary to our expectation, the effect of industry munificence is non-significant. Given that industry munificence can represent a highly dynamic, but also complex decision-making context, it could also be that these different effects cancel each other out in munificent contexts.

Finally, our findings also contribute to the classical theories in economics by elucidating how due diligence length functions as a mechanism to mitigate asymmetric information risks in acquisitions. Consistent with Akerlof’s (1970) “lemons” problem, acquisitions inherently suffer from adverse selection risks due to the limited availability of information about target firms. Our results illustrate that while extended due diligence can reduce uncertainty by uncovering hidden information, excessive duration triggers diminishing returns as the marginal value of additional insights declines. Furthermore, our study highlights the critical role of external contingencies in shaping the effectiveness with which firms can address information asymmetries. This interplay provides a deeper understanding of how firms can optimize information gathering to navigate uncertainty without undermining the speed needed to seize time-sensitive opportunities, thereby enriching the application of information economics theories in high-stakes strategic decisions.

Practical implications

Our study also has important implications for practitioners. First, we challenge the conventional wisdom that dominates the corporate acquisition landscape, that “more due diligence is always better” (e.g. Eccles et al., 1999). Our findings suggest that there is an optimal amount of due diligence, beyond which the benefits of additional analyses are limited or even negative. Being aware of this enables managers to develop practices that help them better assess the costs and benefits of due diligence and, over time, improve their ability to optimize these processes in the presence of different external contingencies.

Second, professionals involved in acquisitions, including internal acquisition teams and, in particular, external advisors, may have an inherent bias to advocate for extended due diligence due to the way they are incentivized. This can occur even when longer due diligence processes may not be beneficial. Our study’s insights provide managers overseeing acquisition activities with empirical support to help them better utilize external advisors and internal acquisition teams. On the contrary, with a contingency framework on the determinants of the optimal amount and types of due diligence needed in different types of deals, acquisition professionals may more accurately customize their services to meet the needs of their clients, thereby fostering better-optimized analyses and more favorable acquisition outcomes.

Limitations and avenues for future research

Our study also has limitations, some of which provide potential avenues for future research. First, we examine the acquisition outcomes based on the 3-day stock market returns to the acquiring firm following the acquisition announcement. Although short-term stock market returns have been used extensively in prior acquisition research as a measure of acquisition performance (Devers et al., 2020; Haleblian et al., 2009; King et al., 2021), the measure has also been criticized for not being a good predictor of longer-term acquisition performance (e.g. Oler et al., 2008; Zollo and Meier, 2008). We chose to use the measure as our dependent variable because it allowed us to most precisely match our dependent and independent variables at the level of each individual acquisition and to avoid the influence of confounding events associated with longer-term measures (McWilliams and Siegel, 1997). Moreover, given that acquisition performance is driven by a large number of other factors, including potential challenges in the post-merger integration process that occur only later, we needed a measure that can be measured already in the pre-deal stage. Having said that, the use of short-term stock market returns as the dependent variable is nevertheless a limitation. Future studies could examine the effect of due diligence length on longer-term outcomes by leveraging company-internal data that matches the characteristics of the due diligence processes to internally known long-term acquisition outcomes.

Second, we do not expect investors to analyze the SEC filings of the acquiring companies to find out how long the due diligence process was and then base their reactions on that. However, investors and media often do enquire about the speed of decision-making in the investor events in which an acquisition is being announced. In addition to explicit public references, investors also observe multiple different deal characteristics and make their own assessments of whether they believe in the deal or not, and how well-justified the deal is. Depending on the speed with which the due diligence process was conducted, the deal might entail different cues that can signal the quality of the deal to the investor community.

Third, we measure due diligence by the length of the due diligence process. The ultimate output of the due diligence process, however, is the product of the due diligence’s length and intensity. As decision-process intensity is not externally observable, we can empirically only assess the duration of the due diligence process. Due to the existence of time compression diseconomies (Dierickx and Cool, 1989) in such interactively evolving analysis processes, we believe that this choice is justified. However, given this limitation, we encourage future research to complement our findings by delving into the details of due diligence processes with company-internal data to provide a joint analysis of both the length and intensity of due diligence.

Fourth, we focus on due diligence in the pre-deal phase between the NDA signing and the deal announcement. However, the post-announcement due diligence until the deal’s closure (Golubov et al., 2012) and the post-merger integration process (PMI) are also highly important for value creation in acquisitions. While pre-deal due diligence sets the basis for value creation through acquisitions (Welch et al., 2020), expectations associated with a deal can either be realized or missed during the later stages (Graebner et al., 2017). In line with Sakhartov and Reuer (2023), who distinguish between the pre-deal valuation challenge and the post-announcement integration challenge, an intriguing question arises: Does longer preparation in the form of due diligence favor faster and ultimately better integration?

Fifth, a potential limitation of our study arises from selection biases inherent in the acquisition process. Specifically, the choice to consider acquisitions, the selection of targets, and the decision to pursue deals could introduce selection effects that may influence the observed relationship between due diligence length and acquisition outcomes. Although we control for industry-fixed effects to account for unobserved heterogeneity and apply a control function approach, we cannot completely rule out all sources of bias. Future research could further address these concerns by exploring additional selection mechanisms through experimental or longitudinal designs, potentially identifying more precise determinants of deal selection and timing.

Sixth, another possible limitation of our study relates to the potential for strategic timing of acquisition announcements, which may influence the observed relationship between due diligence length and market reactions. Although we assume that the due diligence period concludes with the signing of the definitive agreement, this assumption may not fully account for variations in the actual duration of due diligence or potential delays in announcement timing. While our focus on public target firms mitigates some of these concerns—given the stricter regulatory requirements and disclosure norms that limit firms’ ability to strategically delay or accelerate announcements—information leakage or other timing-related factors could still affect investor responses. Future research could investigate this further by examining alternative measures, particularly in contexts where disclosure requirements differ.

Seventh, our study’s focus on acquisitions in the United States may limit the generalizability of our findings to other regulatory and institutional contexts. The U.S. regulatory environment, characterized by stringent disclosure requirements and premerger notifications under the Hart-Scott-Rodino Act, may shape the due diligence process differently compared to other countries. Future research could expand on this by studying acquisition activities in non-U.S. settings to explore how differences in regulatory frameworks impact the due diligence process and its performance implications.

Finally, in the absence of an exogenous shock, a potential endogeneity concern remains. Although we conducted multiple robustness checks to address this issue—such as 2SLS, a two-stage control function approach, and a RiR—we cannot fully rule out the possibility that some endogeneity may still affect our findings.

Conclusion

Prior research has viewed longer due diligence processes in acquisitions generally as beneficial. In this study, we are among the first to theoretically and empirically address the potential downside of prolonged due diligence, shedding light on the intricate balance between comprehensiveness and speed in acquisition decision-making. Drawing on decision comprehensiveness theory, we contribute to an enhanced understanding of how decision-making processes influence value creation in acquisitions. We hope to encourage future researchers to further explore the temporal dynamics of due diligence and factors determining its efficiency, including how the interplay between duration and intensity affects value creation, and how other contextual variables, such as the regulatory environments, influence due diligence practices. By doing so, future studies can help unravel the puzzle of how due diligence practices shape successful acquisition outcomes.

Footnotes

Appendix

Robustness test—Altering the regression model (GLS).

| Models | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| Dependent variable | CAR | CAR | CAR | CAR |

| DD Length | 0.012** | 0.012** | 0.013** | 0.013** |

| (0.032) | (0.029) | (0.021) | (0.025) | |

| DD Length squared | -0.000* | -0.000** | -0.000** | -0.000** |

| (0.052) | (0.045) | (0.035) | (0.043) | |

| Industry Munificence | 0.066 | |||

| (0.839) | ||||

| DD Length * Industry Munificence | -0.003* | |||

| (0.092) | ||||

| Industry Complexity | -0.609* | |||

| (0.050) | ||||

| DD Length * Industry Complexity | 0.003** | |||

| (0.027) | ||||

| Industry Dynamism | 0.317 | |||

| (0.280) | ||||

| DD Length * Industry Dynamism | -0.002* | |||

| (0.065) | ||||

| Constant | 9.601* | 9.243* | 8.822* | 9.320* |

| (0.060) | (0.070) | (0.083) | (0.068) | |

| Observations | 501 | 501 | 501 | 501 |

| Wald Chi2 | 133.91 | 136.40 | 139.54 | 136.84 |

| Controls | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes |

| Regression | GLS | GLS | GLS | GLS |

P values in parentheses; two-tailed tests for control variables and one-tailed tests for hypothesized variables. ***, **, * indicates significance at the 1%, 5% and 10% levels, respectively.

Acknowledgements

We thank Dennis Veltrop for his valuable comments and suggestions as well as for feedback from the Annual Meeting of the Academy of Management (2024). We also thank Julia Berginski and Leonie Brill for excellent research assistance.

Authors’ note

Data stem from commercial databases and hand collection of firms’ disclosure reports.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.