Abstract

We explore how firms navigate evolving moral markets’ fuzzy boundaries by employing sensegiving to address interpretive uncertainty following their strategic actions. We specifically consider how acquirers’ acquisition announcements and post-acquisition communications influence media positivity about the acquirer in the food processing industry’s natural, organic, and healthy moral market, contingent on the target’s category membership and acquirer/target category incongruence. We find that using more natural, organic, and healthy language enhances media positivity when the target straddles or is fully part of the natural, organic, and healthy category, announcing the target will retain its autonomy enhances media positivity regardless of the target’s category membership, and extreme misfits negatively influence media tenor, whereas misfits clarifying the acquirer’s commitment to the moral market moderate the sensegiving activities’ effects. We contribute to the moral markets literature by showing how firms sensegive to position themselves within evolving moral markets and to the categories literature by considering how firms navigate a moral market’s fuzzy and potentially shifting boundaries in ways that reduce interpretive uncertainty.

Keywords

The Niman Ranch brand continues our commitment to raising animals without antibiotics or artificial growth stimulants, and to responsible food and agriculture. With the long, family-owned heritage of our company, we understand and respect what Niman Ranch represents. All Niman Ranch livestock will continue to be raised by the same small family farmers and ranchers, following the same protocols, and with the same focus on sustainability.

Continued growth in the market for more sustainable products has seen the rise of “moral markets” formed by firms “whose raison d’être is to create social value by addressing the negative externalities associated with conventional practices, legacy technologies, and extant institutions” (Georgallis and Lee, 2020: 50–51). This movement has been especially prevalent in the food processing industry, where the rapid rise of organic and environmentally sustainable production practices—which avoid the use of drugs, synthetic pesticides, herbicides, and fertilizers, or genetically modified organisms, and employ humane treatment of animals and sustainable land management—and institutional certifications has created growing markets for these food products (hereafter, referred to as natural, organic and healthy, or NOH 1 food). For example, as regulations such as USDA Organic Certification became widely recognized and attracted large, established companies’ interest (Lee, 2009), the organic food category grew at a far faster rate—and with higher margins—than the overall food category (Organic Trade Association (OTA), 2024). This created a situation where the moral market not only gained legitimacy to stand on its own, but the new moral standards and values it represented (e.g. types of food, production and processing methods) started permeating the incumbent market as well.

For example, poultry giant Perdue Farms—a company known for employing “factory farm” practices—acquired Niman Ranch, which gained fame for treating its animals well and raising them without drugs or chemicals (Charles, 2015). Some initially received the acquisition negatively (Peterson, 2015) despite Perdue’s promise to guarantee Niman Ranch’s operational autonomy and maintain its values (Perdue Farms, 2015). Perdue continued consistently communicating that it was adopting sustainable practices and learning from Niman Ranch’s experiences. Eventually, Perdue was perceived positively for moving its practices in a more sustainable direction (Charles, 2015; Strom, 2016).

Perdue’s experience highlights the interesting dynamics that can occur in moral markets. Market categories become subject to diverse value-driven interpretations, as legitimating a new moral market category casts a negative light on firms in the conventional category (Georgallis and Lee, 2020). Market participants are aware that customers desire stronger commitments to the new category’s stricter moral standards. Yet, they vary widely in their positioning relative to the new moral standards—from firms “born” in the moral market and thus fully representing its values to those attempting to “straddle” into the moral market from the conventional category.

Durand and Paolella (2013: 1100) noted “Categories represent a meaningful consensus about some entities’ features” that are socially constructed by both audiences and category members. Straddling the boundary between the traditional category and the moral market category can blur shared understandings and expectations about firms’ features and behaviors, introducing both ambiguity and uncertainty when interpreting their actions (Weber and Mayer, 2014). More specifically, in an evolving moral market where firms from different sub-categories converge, successful category straddling becomes important for the individual firms and the growth of the market. However, their convergence makes audiences, such as the media, uncertain about what cognitive frame they should use when interpreting the firms’ actions.

Previous research has mainly considered how firms are penalized for category straddling (e.g. Zuckerman, 1999), and those studies exploring straddling’s benefits have focused primarily on how it creates value for firms (e.g. Paolella and Durand, 2016). Less attention has been paid to category straddling as a process that firms go through if new categories emerge from existing categories as they evolve (Durand and Khaire, 2017), and the boundaries between these categories become fuzzy. In particular, the microprocesses involved in sensegiving activities that accompany this transition have received limited attention (Vergne and Wry, 2014).

Scholars have noted sensegiving activities’ importance in constructing moral markets (Balsiger, 2021; Chaput and Paulsson, 2023; Hedberg and Lounsbury, 2021), particularly for markets such as NOH foods where products are visually indistinguishable from their less sustainable counterparts. Stakeholders rely heavily on firm communications and infomediaries such as the media to build their perceptions of participating firms and their products as the new market category is constructed (Chaput and Paulsson, 2023; Gilding and Glezos, 2021).

However, the importance of the media’s sentiment about moral market participants does not diminish after the initial category construction phase (Kennedy, 2008; Navis and Glynn, 2010). Media sentiment shapes how stakeholders perceive and make sense of firm actions, both affecting and reflecting public sentiment (Bowers, 2020; Brown et al., 2006; Carroll and McCombs, 2003; Pollock and Rindova, 2003; Rindova et al., 2007), and the media’s coverage is affected by market participants’ sensegiving activities (Hedberg and Lounsbury, 2021; Kennedy, 2008). Thus, the relationship between firms’ sensegiving activities and media sentiment will likely remain crucial. We therefore address the following question: How do the frequency and consistency of firms’ strategic sensegiving communications in evolving moral markets shape the media’s reactions to strategic actions?

We specifically consider the media’s positive language about a firm following its acquisition of another firm. We focus on acquisitions because they are visible strategic actions that show how firms interact and adjust within a moral market, and that have significant implications for the firm’s future value and market position (Haleblian et al., 2009). Acquisitions are also well-documented for frequently destroying acquired firms’ value (Haleblian et al., 2009), which can be a particular concern in moral markets when acquisitions cut across different sub-categories of firms with different levels of commitment to the moral market’s values. Such uncertainty can confuse key stakeholders about how the acquisition will provide value and increases the likelihood they view the acquirer negatively (Lee, 2009).

We explore how acquirers’ acquisition announcements and post-acquisition communications influence the media’s positivity about the acquirer, contingent on the target’s category membership and the type of category incongruence between the pair. We test our hypotheses using a unique dataset of 193 North American food processing industry acquisitions conducted by 91 firms between 2007 and 2012, focusing on two information properties of sensegiving activities (i.e. information richness and amount) that acquirers can use to manage interpretive uncertainty. We look at the extent to which acquirers use language that is desirable in the moral market (i.e. NOH language) in their acquisition announcement and post-acquisition press releases, and whether acquirers announce they will preserve the target firm’s operational autonomy, thus lowering the odds that its value will be destroyed. We also examine how categorical incongruencies existing between the acquirer and the target affect media sentiment.

Our findings indicate that using more NOH language enhances media positivity when the target straddles or is fully part of the NOH category, whereas announcing the target will retain its autonomy will enhance media positivity, regardless of the target’s category membership. We also find that extreme misfits negatively influence media tenor, whereas misfits that clarify the acquirer’s commitment to the moral market do not have a direct effect, but positively moderate the sensegiving activities’ effects.

Our study contributes to the growing research stream on moral markets (Balsiger, 2021; Georgallis and Lee, 2020; Lee et al., 2017) by focusing on a market’s evolving dynamics beyond the initial legitimation phase. We show how the richness and volume of firms’ sensegiving activities concurrent with and following acquisitions (Elsbach, 2012; Pollock et al., 2008; Pollock and Rindova, 2003; Sinha et al., 2015) affect the acquirers’ media coverage, thereby influencing the interpretive uncertainty about their moral market participation. Moral markets research has given limited attention to the dynamics of how individual firms attempt to position themselves within moral markets, how they are assessed, and how they influence the growth of individual firms within the larger frame of moral market’s evolution.

We also contribute to the categories literature, in which scholars tend to assume that categories can be neatly divided and have found that firms can be both penalized (e.g. Hsu et al., 2009; Zuckerman, 1999) and rewarded (Paolella and Durand, 2016) for straddling boundaries. We consider how firms navigate a moral market category with fuzzy and potentially shifting boundaries by using strategic communications to sensegive in ways that reduce interpretive uncertainty about their category membership and strategic actions. In particular, we show how category straddlers (i.e. which we call “mixed” firms) that are members of both the NOH and conventional categories can enhance media perceptions as effectively as firms fully in the NOH market category. These findings have implications for firms attempting category change—particularly through acquisitions—including how they can increase the likelihood that stakeholders accept their efforts.

Theory and hypothesis development

Moral markets, category straddling, and interpretive uncertainty

Moral markets emerge when entrepreneurs identify important social needs that conventional businesses are not satisfying. Firms driving moral markets’ development have distinct social and environmental missions, with clear stakeholder expectations that are often antithetical to the industry’s conventional operations (Georgallis and Lee, 2020; Wickert et al., 2017). Moral markets research has primarily focused on how movements pursuing social good can lead to the formation of new moral markets (Hedberg and Lounsbury, 2021) and, in particular, how interactions among firms and their key stakeholders form the market’s collective identity (Georgallis et al., 2019; Gilding and Glezos, 2021; Lee et al., 2017; McInerney, 2014). As such, these studies build heavily on the new market category construction literature, which emphasizes the need for producers to provide narratives and necessary framing to build a collective identity that stakeholders recognize as distinctive and accept as desirable (Kennedy, 2008; Lee et al., 2017; Navis and Glynn, 2010).

Forming a collective identity provides the basis for a category’s continued growth. However, once a category’s boundary is set, the focus shifts from gaining legitimacy by building the market’s collective identity to how individual actors within the market navigate the newly legitimated category (Kennedy, 2008; Navis and Glynn, 2010). Navis and Glynn (2010) demonstrated this dynamic in their study of the satellite radio industry. Once the new market category gained legitimacy, entrepreneurs and audiences both shifted their emphasis to the distinctiveness of individual organizations within the category’s legitimized boundaries. Implicit in this differentiation argument is that the category’s boundary, once set, is clear and unmoving, so that market participants can focus on differentiating themselves (David and Lee, 2022; Navis and Glynn, 2010).

However, moral markets present a fuzzier and more transient case due to their value-driven nature and interplay with the conventional market. First, moral markets emerge as the antithesis of conventional markets, often driven by social movements that are explicitly value-driven. However, moral markets’ antithetical natures also tie them to their roots in conventional markets. By emphasizing the new practices’ authenticity and normative superiority, moral market participants cast conventional market participants as inauthentic and inferior (Georgallis and Lee, 2020). Moral markets’ legitimacy and desirability attract other firms into the market despite these antithetical standards, making membership in the moral or conventional category less clear and more transient. Rather than differentiating themselves from other firms, these firms focus on how they position themselves in relation to the market’s moral standards as they straddle different categories (Balsiger, 2021; Georgallis and Lee, 2020).

Second, the certifications or state support schemes needed to establish a moral market and distinguish its participants also paradoxically allow companies that are less committed to the moral standards to enter the market category (Lee et al., 2017). This leads to a situation where companies with varying degrees of commitment to the moral market’s standards co-exist (Balsiger, 2021). As such, a moral market’s evolution is characterized by a broadening and co-mingling of firms from different categories—ranging from “purists” who strictly adhere to the new moral standards, to firms straddling (Durand and Paolella, 2013) the conventional and moral market categories, to conventional firms demonstrating only symbolic adherence (Balsiger, 2021).

This diversity and category straddling creates interpretive uncertainty (Weber and Mayer, 2014) for audiences. As firms belonging to categories with opposing values assimilate into the moral market, audiences that are trying to interpret various firms’ actions often have to deal with more than one cognitive frame. Multiple cognitive frames that stem from relational characteristics (i.e. attributes of the firms in relation to each other) (Weber and Mayer, 2014) make it more difficult for audiences to interpret firms’ actions and assess their value (Hsu, 2006; Negro et al., 2010; Zuckerman, 1999) because they are unable “to extrapolate current actions and to foresee their consequences” (Weick, 1995: 98–99). For instance, if a clearly conventional firm acquires a firm that is strongly identified with a moral market’s values, how should the audience interpret the move? Thus, the need for sensegiving activities—defined as deliberate attempts to “influence the sensemaking and meaning construction of others toward a preferred redefinition of organizational reality” (Gioia and Chittipeddi, 1991: 442)—becomes increasingly important.

Sensegiving activities and the media

Organizations use their external communications to provide narratives that enable key audiences to resolve uncertainty surrounding the firm’s viability and future prospects (e.g. Kennedy, 2008; Lounsbury and Glynn, 2001; Petkova et al., 2013; Porac et al., 2002). Extensive research has been conducted on effective meaning management through the media to influence broad stakeholder audiences during new category legitimation (e.g. Aldrich and Fiol, 1994; Kennedy, 2008; Navis and Glynn, 2010; Petkova et al., 2013). These studies emphasized the media’s role as a crucial intermediary that filters information about new developments, selecting issues, events, and organizations to highlight (Hoffman and Ocasio, 2001; Kennedy, 2008; Pollock et al., 2008), and thus shaping cognitive patterns and beliefs (Jonsson and Buhr, 2011).

As key evaluators of an organization’s feasibility, credibility, and appropriateness, the media also influences how the category progresses (Kennedy, 2008; Navis and Glynn, 2010). Kennedy (2008) and Navis and Glynn (2010) both found that while the media initially focused on presenting the new category members’ collective identity, its attention shifted to differentiating the narratives of individual organizations within the category once it was established. This suggests that as a market category matures, the media will remain influential, but its role may change. Hence, understanding how the media receives firms’ sensegiving activities will improve our understanding of how firms navigate the complex terrain of moral markets once they are established.

The food processing industry’s moral market

The food processing industry is a good example of an industry with an evolving moral market. The NOH sub-segment was motivated by the organic food movement in the 1970s. During this time, producing foods without any chemicals, antibiotics, or genetic modifications, and in ways that value biodiversity (Kowitt, 2015; Lee, 2009; Weber et al., 2008), gave rise to the demand for organic food. In the United States, organic food sales tripled over the past decade, making organic food a $63.8 billion (USD) business (OTA, 2024). Profit margins in this market are also significantly higher than for conventionally produced food (OTA, 2020). USDA Organic Certifications, created in 2002, spurred other labeling to materialize (i.e. natural, fair-trade, sustainable) and started to represent the new NOH moral standard in the food processing industry. It also opened the market to more industry participants who tried capturing a greater share of this lucrative and growing market by embracing more NOH values.

Some food producers—both newly founded and legacy—launched their own NOH products by developing and adapting their operations internally and getting certified by accrediting bodies. The NOH market initially relied heavily on organic certifications for its legitimacy and distinctiveness (Gilding and Glezos, 2021; Lee et al., 2017). But certifications alone were no longer sufficient to drive perceptions of firms as the market expanded and large, conventional firms used organic certifications to straddle categories, calling their authenticity and market commitment into question (Howard, 2009). Furthermore, rather than developing new product lines themselves, other firms actively merged with or acquired NOH firms that represented the new moral standard. By the end of 2002, the top 30 processors in the United States had acquired at least one or more NOH pioneer, and new NOH firms continued to emerge, attracting generous acquisition offers (Cornucopia Institute, 2015; Howard, 2009).

The media’s reaction to these acquisitions has often been negative. For example, journalists have warned their readers to not be fooled by conventional firms offering products under the “organic” label (e.g. Whoriskey, 2015). They have also focused on how NOH firms were forced to change their production methods after being acquired (Peters, 2015; USA Today, 2013). Such negative reactions are reasonable, as prior research has shown that acquirers do sometimes destroy targets’ value (Devers et al., 2020; Haleblian et al., 2009). Moreover, as NOH values are generally antithetical to conventional firms’ practices (Lee, 2009; Weber et al., 2008), whether NOH and conventional firms can successfully combine generates uncertainty. Combining multiple and incongruent cognitive frames from respective categories also confuses audiences about how to make sense of firms’ actions (Weber and Mayer, 2014). Even when an acquisition does not involve a conventional firm, it may still be unclear to external audiences whether the acquisition will destroy or interfere with pursuing the moral market’s values.

Thus, the food processing industry context presents high interpretive uncertainty, with firms from different categories providing audiences with multiple cognitive frames for interpreting their actions. This makes it useful for studying our theoretical arguments. We explore how firms’ sensegiving efforts at the time of and following acquisitions influence the media, and the extent to which their efforts’ success are influenced by their degree of category membership.

Resolving interpretive uncertainty through sensegiving activities

Acquisitions are inherently ambiguous events (Daft and Macintosh, 1981; Graffin et al., 2016; Weber and Mayer, 2014) whose outcome variability (Haleblian et al., 2009; King et al., 2004) often make stakeholders unsure of how to interpret their implications. As such, acquisitions provide firms with a great opportunity to strategically resolve stakeholders’ interpretive uncertainty through carefully formed communications. Firms’ communication efforts surrounding ambiguous events have been actively researched. For example, Graffin and colleagues (2011) examined how releasing unrelated company news around CEO succession (i.e. strategic noise) could influence analysts’ performance outlook for a firm. Similarly, scholars have identified that issuing unrelated positive firm information surrounding acquisitions can offset negative market reactions (i.e. impression offsetting) (Graffin et al., 2016). In addition, hinting at future acquisitions (i.e. foreshadowing) to security analysts can allow firms to receive fewer negative analyst evaluations than those who do not (e.g. Busenbark et al., 2017).

While past research has used acquisition events as a context to demonstrate how firms use their communications to influence key stakeholder evaluations, they have mostly focused on using information unrelated to the focal acquisition to influence short-term investor responses in the days following the announcement. We instead focus on communicating acquisition-related information and how it influences the media’s positive language in its ongoing coverage. Furthermore, we also consider the effect of category membership to support these communications. We look at the extent to which the target is fully within a moral market category, straddles the category and another category, or lies outside the moral market category influences how the communications are received. We argue their sensegiving’s effectiveness will be contingent on the perceived authenticity of the acquirer’s claim that it will make lasting and substantial organizational changes (Grimes et al., 2019; Kovács and Horwitz, 2021). Therefore, positive media coverage will occur when the acquirer communicates information aligned with the moral market’s standards and their substantive actions support these claims.

Information properties of sensegiving activities

Two information properties help firms reduce interpretive uncertainty: amount and richness (Daft and Lengel, 1986; Daft and Macintosh, 1981). The amount of information refers to the “volume or quantity of data about organizational activities” (Daft and Macintosh, 1981: 210) and affects receivers’ perceived familiarity with the subject and the information’s truthfulness (Hawkins and Hoch, 1992; Zajonc, 1968). Information richness is defined as “the ability of information to change understanding” (Daft and Lengel, 1986: 560). Communication is deemed rich if it can bridge different perspectives or resolve ambiguous issues to shift understanding (Daft and Lengel, 1986); thus, providing rich information can play a crucial role in resolving uncertainty. Interpretive uncertainty is resolved when the elements of a single interpretive frame are agreed upon and become shared (Weber and Mayer, 2014). In this regard, the acquirer’s acquisition-related announcements can be potent for resolving stakeholders’ uncertainty (Busenbark et al., 2017; Graffin et al., 2016) by giving information that can potentially align the interpretive frames. Thus, the greater and richer the information that acquirers provide during and after the acquisition, the more it can help stakeholders make sense of what the deal signifies for the target and the acquirer’s operations (e.g. Paruchuri et al., 2006).

In moral markets, one important aspect of information richness is using language consistent with the market’s moral standards. In our research context, the extent to which acquirers employ NOH-consistent language in their acquisition announcements can reduce interpretive uncertainty by linking the acquirer to the NOH market’s interpretive frame (Weber and Mayer, 2014), illustrating their future path together. Furthermore, given that the acquisition announcement is the most widely circulated document describing the acquisition, and that media accounts cite them frequently (Davies, 2008), using more NOH-consistent words in press releases increases the likelihood these words will influence the acquirer’s subsequent media coverage. Providing information that aligns with NOH values helps reduce interpretive uncertainty by aligning the audience’s cognitive frames with the desired category.

For example, when General Mills acquired NOH firm Food Should Taste Good, its announcement included a statement from General Mills’s president that used many NOH words (in bold below) to explain the acquisition’s potential:

“This acquisition further positions us for continued growth with a great new brand in an entirely new category in our

In contrast, some firms have simply highlighted operational synergies between the two companies without using much NOH language, as in TreeHouse Foods’s acquisition announcement for NOH firm San Antonio Farms:

We are very excited to add Mexican sauces to our family of products, [. . .] Salsa, picante and other Mexican sauces are experiencing great growth and private label Mexican sauces are growing even faster than the total category. San Antonio Farms is a well-managed company with premium products, a history of profitable growth with talented and dedicated employees. The transaction will be neutral to TreeHouse earnings over the balance of the year, but is expected to add approximately $0.05 per share to earnings in 2008.

However, NOH language’s effectiveness will be contingent on how well it aligns with the target’s perceived category. The more clearly the target is a member of the moral market, the greater the authenticity of the acquirer’s claims, and the more likely the media will be to perceive that the acquirer is making a fundamental commitment to the moral market (Alcañiz et al., 2010; Grimes et al., 2019). In our context, we expect acquirers using more NOH language in their acquisition announcements to receive more positive media coverage after acquiring firms from the NOH category. This will provide better alignment between the target’s characteristics and the acquiring firm’s future behavior, thus providing an interpretive frame that can help enhance how positively the media discusses the firm. Furthermore, we expect this relationship will hold even when the target firm’s product lines straddle conventional and NOH categories (which we refer to as a “mixed” category membership), as the acquirer’s use of NOH language should allow it to emphasize the target’s NOH attributes. Thus, we hypothesize that:

Hypothesis 1. Using more NOH language in the acquisition announcement will have a positive relationship with the acquirer’s post-acquisition media tenor when the target has mixed or NOH category membership.

Another piece of rich information that can clarify interpretive uncertainty is the acquirer’s post-acquisition integration plan—specifically, whether the acquirer will allow the target to maintain its operational autonomy (Zaheer et al., 2013). Acquirers often claim that they can create synergies and operational efficiencies by reducing unit costs in production, inventory holding, marketing, advertising, and distribution if they integrate an acquisition target’s operations with their existing operations (Larsson and Finkelstein, 1999; Pablo, 1994). However, a high degree of post-acquisition integration can be problematic when the target firm’s value lies in practices and a culture the acquirer does not share (Paruchuri et al., 2006). Pushing for greater integration in these situations can lead to disruptions, such as higher executive turnover, loss of key employees, loss of resources through cost-cutting measures, and undermining an organizational culture that provides key intangible resources (Paruchuri et al., 2006). In such cases, giving target firms more operational autonomy and discretion helps avoid such damage (Zaheer et al., 2013). Thus, stipulating that the target will maintain its operational autonomy reduces expectations that the acquirer will destroy the target’s value.

In the context of food processing industry acquisitions, firms may be tempted to integrate targets to achieve cost savings and maximize efficiency, given strategic relatedness. However, because players in this category arose as part of a movement promoting specific values and practices (Austin and Leonard, 2008) that are antithetical to what conventional firms represent (Wickert et al., 2017), when the target is part of or straddles the NOH market category, integrating it might increase concerns that the acquirer will destroy the target’s value. We therefore expect that announcing the target is going to maintain its autonomy will reduce this source of interpretive uncertainty and increase the positive tenor of a firm’s post-acquisition media coverage when the target is either in a mixed or NOH category. Thus, we hypothesize that

Hypothesis 2. Announcing that the target will maintain its autonomy will have a greater positive relationship with the acquirer’s post-acquisition media tenor when the target has mixed or NOH category membership.

Whereas the acquisition announcement plays an important role in shaping media assessments, continuing to provide abundant and rich information consistent with the moral market’s values over time can reinforce and add validity to the announcement’s claims (Gioia and Thomas, 1996). While previous studies have considered the volume of information provided (e.g. Kennedy, 2008; Petkova et al., 2008; Pollock et al., 2008), communication continuity has received less attention. Category membership reinforcement and change are iterative processes that unfold over time, as information communicated is received and interpreted by stakeholders, and the modified version is then fed back to the organization (Gioia et al., 2000, 2014). Thus, a firm’s ongoing efforts are required to actively promote and solidify its desired organizational reality (Grimes et al., 2019; Hamilton and Gioia, 2009).

We therefore argue that continuously using more language consistent with the moral market in post-acquisition press releases is another sensegiving activity that acquirers can employ to influence their media coverage tenor by increasing their associations with the moral market and the perceived truthfulness of their claims (Hawkins and Hoch, 1992; Zajonc, 1968). Continuous communication also reinforces that the acquirer was not just taking advantage of the acquisition announcement and is making sincere efforts to change its identity and values (Gioia and Thomas, 1996). In our context, just as using more NOH language in the acquisition announcement can clarify the acquirer’s intention to engage in more NOH practices, consistently using more NOH language to describe the acquirer’s own activities in their subsequent press releases reinforces the perception that the acquirer is embracing more NOH standards. We therefore hypothesize:

Hypothesis 3. Using more NOH language in the acquirer’s post-acquisition press releases will have a positive relationship with the acquirer’s post-acquisition media tenor when the target has mixed or NOH category membership.

The effects of acquirer and target categorical differences

Thus far, we have focused on the effects of the target’s category membership. However, the acquirer can also vary in the extent to which it is a member of the moral market category, lies outside the category, or is a category straddler. We argue that different acquirer and target category misfits can also have different effects on the media’s tenor. Given that we expect interpretive uncertainty to decrease positive tenor (Weber and Mayer, 2014), we expect that more extreme misfits, where either the acquirer or the target is fully within the moral market category and the other firm lies fully outside the category, will increase interpretive uncertainty and thus have a negative relationship with positive media tenor. In our context, a conventional firm acquiring a NOH firm raises the most significant concerns about the acquirer’s authentic commitment to NOH values. Conversely, an NOH firm acquiring a conventional target also raises the concern that the acquirer may be moving away from its NOH values in a quest to get bigger. Both scenarios increase interpretive uncertainty. We therefore hypothesize:

Hypothesis 4a. The more extreme the categorical difference between the acquirer and the target, the less positive the acquirer’s post-acquisition media tenor.

However, the acquisition could also clarify the acquirer’s strategic direction, thereby reducing interpretive uncertainty. If the acquirer is a boundary straddler and acquires a moral market firm, this can signify the firm’s commitment to the moral market, reducing interpretive uncertainty about the firm’s intentions and increasing the positivity of the firm’s media tenor. 2 Also, an NOH firm’s acquisition of a mixed target can signal that the target’s NOH aspects will be preserved or enhanced (due to assumptions that the acquirer’s values will dominate when there is little interpretive uncertainty about what those values are), reducing interpretive uncertainty in ways that lead to more positive media tenor. Thus, we expect that NOH firms acquiring a mixed target or vice versa will have more positive media tenor than other misfits. We therefore hypothesize:

Hypothesis 4b. Acquisitions that clarify the acquirer is becoming more NOH will be positively associated with the acquirer’s post-acquisition media tenor.

Data and methods

Sample and data collection

We tested our hypotheses using a sample of North American (Canadian and US) firms in the food processing industry that acquired other food processing firms 3 between 2007 and 2012. We chose to examine the North American organic food processing industry during this study period because it follows the USDA’s establishment of national organic standards in 2002. We chose 2007 as the first observation year because this is when the USDA started archiving its centralized certified organic operations list, which we used to determine acquirer and target category membership. By 2007, the industry had had enough time to adapt to the unified national standards, thus providing the ability to observe their and other trends’ effects on the industry’s structure. NOH firms continued to receive generous acquisition offers (Cornucopia Institute, 2015), and consumer demand for NOH products was growing (Howard, 2009), making this a useful period for observing the microprocesses shaping the market’s dynamics following the initial market creation phase.

We used the Food Industry M&A Reports and Thompson One databases to identify all food processing industry acquisitions. We ended our data collection in 2012 because this was the last year for which we had access to the Food Industry M&A Reports. We only included completed deals where more than 51% of shares were purchased by the acquirer. We also excluded acquisition deals that were simple acquisitions of physical facilities rather than acquisitions of a brand or an entire company. For acquisition deals that were done by subsidiaries, we searched for their parent firms in their acquisition announcement press releases and in Hoover’s database (www.hoovers.com), and replaced the subsidiary’s name with the parent firm’s name. After we triangulated the two databases and excluded firms that did not have any media coverage either before or after the acquisition, our final sample included 193 acquisitions conducted by 91 firms.

Dependent variable

Post-acquisition media tenor

Our dependent variable is the positive proportion of affective language used in the acquirer’s media coverage during the 12 months following the acquisition event. The media can frame and influence stakeholders’ perceptions of firms by using positive and negative language in articles (Deephouse, 2000; Pollock and Rindova, 2003); the positive tenor of media coverage reflects how favorably the acquisition affected the media’s perceptions of the acquirer. We collected 19,732 articles about the acquirers from LexisNexis using the following criteria: (1) the articles were more than 200 words long, and (2) they mentioned the acquirer’s name at least five times in the main body of the article to ensure the article is about the focal firm. We collected all media articles in North America included in LexisNexis, excluding newswire articles. 4 To measure an acquirer’s post-acquisition media tenor, we collected media coverage for 1 year following the acquisition, beginning the day after the acquisition date. We also calculated the same measure for the year prior to the acquisition date as a control.

We used the text analysis program Linguistic Inquiry and Word Count (LIWC) (Pennebaker et al., 2015) to content analyze each article and determine the proportion of positive affective language. LIWC includes validated dictionaries for positive and negative affect (http://liwc.wpengine.com). We calculated the tenor of each article as the number of positive words divided by total affective (positive plus negative) words. We then calculated the overall tenor of a firm’s media coverage for the 12 months following the acquisition by calculating the average positive tenor of a firm’s coverage across all articles. 5

Independent variables

NOH words in the acquisition announcement

We built a custom NOH dictionary that included words connoting relevant products or processes in media and firm-issued texts to assess the acquirers’ NOH terminology use. We followed the guidelines for establishing construct validity using computer-aided text analysis (Short et al., 2010): (1) we employed multiple techniques to identify words that represented the NOH construct; (2) we validated the dictionary using experts to assess its face validity; and (3) we assessed the dictionary’s predictive validity by comparing human and machine coding of the same text (Wade et al., 1997) to assess its inter-rater reliability and how well the dictionary captured the NOH construct.

To construct the dictionary, we began by using the term “organic,” as defined by the USDA (USDA, 2011):

Organic is a labelling term that indicates that the food or other agricultural product has been produced through approved methods. These methods integrate cultural, biological, and mechanical practices that foster cycling of resources, promote ecological balance, and conserve biodiversity. Synthetic fertilizers, sewage sludge, irradiation, and genetic engineering may not be used.

We then expanded to similar terms or labels that are often used to describe healthy products. Examples include “free-range,” “cage-free,” “natural,” “grass-fed,” “pasture-raised,” and “humane” (USDA, 2011). Although these labels do not qualify a product as organic or allow a firm to claim it is producing certified organic food, firms and the media use them widely as labels to describe healthy food. In particular, the term “natural” is commonly used by food marketers to describe how healthy and environmentally conscious products are (Dunckel et al., 2020; Kuchler et al., 2023). Although “natural” is not the same as organic and does not have a standard definition from regulating agencies like the USDA or the US Food & Drug Administration (USFDA), both agencies nevertheless loosely define the term. For meat, poultry, and eggs, USDA defines natural as “minimally processed and contains no artificial ingredients” (Dunckel et al., 2020; USDA, 2024). For all other food products, the USFDA defines natural as “nothing artificial or synthetic (including all color additives regardless of source) has been included in, or has been added to, a food that would not normally be expected to be in that food” (Dunckel et al., 2020; USFDA, 2018). Given that firms can identify as NOH using these terms, we have included them in our dictionary.

To further develop our NOH word list, we searched common words found in the sample corpus of media coverage on NOH firms and organic issues. We searched news articles in LexisNexis from 2007 to 2008 to retrieve articles about organic food, 6 yielding a total of 355 articles and 10 press releases by NOH firms that we read to identify common NOH words.

We established the face validity of these words by consulting experts, including four journalists covering the food industry, two academics in relevant disciplines, and three organic farmers. The expert panel selected words that they thought represented the NOH values from the words we provided. We then used Thesaurus.com to find synonyms for the key words organic, natural, and healthy, as well as possible variations of these words. The final list included 181 words, such as organic*, green, sustainable, non-GMO, and biodiversity (see the Online Supplement for the full dictionary). Finally, we randomly selected 1 article for 28 firms (30%) and manually coded these articles and placed them into 3 groups (low, moderate, and high NOH). We then used the computer-coded results to put firms into the same three groups and compared the results with manually coded articles. Comparing the results showed 89% agreement between our manual and computer-coded NOH groupings, suggesting good reliability (Wade et al., 1997).

We collected acquisition announcements from press release outlets on LexisNexis. 7 We measured the NOH words in the acquisition announcements as the proportion of NOH dictionary words in the press releases multiplied by 100. We analyzed the press releases’ NOH content using LIWC. We gave firms that did not issue press releases announcing the acquisition a value of zero.

NOH words in post-acquisition press releases

To create this measure, we collected 3369 press releases 8 from LexisNexis issued by the acquiring firms for the 1-year period starting from the day after the acquisition announcement. We employed the aforementioned method to capture the NOH words used in their press releases and then calculated the average value across all of the acquirers’ post-acquisition press releases.

Announced autonomy plan

Using the acquisition announcements collected, announced autonomy plan was coded one if the acquirer clearly stated in the acquisition announcement that it intended to give the target autonomy, and zero otherwise. Following previous research (Paruchuri et al., 2006), we categorized the plan as giving the target autonomy when the press release included statements such as “continue as it always had,” “not to reduce jobs,” “will be run separately/independently,” “continue to be run by (the target’s current CEO),” and “not change the production of the product.” A trained coder and the first and second authors compared the coding on 30% of the acquisition announcements and achieved 96.5% agreement. We coded as zero ambiguous statements that left intentions unclear or failed to mention whether they intended to integrate the target firm. We also coded as zero firms that did not issue press releases announcing the acquisition. Thus, this measure is a conservative count of when acquirers intended to give targets autonomy.

Target category

We determined a target’s category by using qualitative and quantitative indicators to assess the extent to which their products and practices aligned with the organic food industry. One quantitative indicator, derived from the USDA certified organic operation list, was the number of organic certifications a firm and/or its subsidiaries had at the time of the acquisition. USDA organic certifications serve as both symbolic and substantive representations of a firm’s NOH category membership, as they are the official standard in the United States that guarantees organic production integrity. Businesses that earn more than $5000 in annual organic sales must be certified to label their products organic.

However, not all firms that embrace organic values and practices seek USDA certification, due to administrative costs and other reasons. 9 Moreover, as some conventional food processing firms can easily afford multiple USDA organic certifications without emphasizing the values associated with organic production organization-wide, we also considered qualitative indicators to distinguish companies with an NOH orientation from conventional food companies that simply have an organic product line.

To code qualitative evidence of a target’s category membership, we primarily used its official pre-acquisition website. We accessed these earlier versions of the websites using the Wayback Machine (www.archive.org/web), a digital archive that stores the history of information available on the Internet, as reflected in past versions of websites. We accessed equivalent pages on each website that discussed each firm’s primary businesses and values at the time of the acquisition. Since firms are likely to display the values they emphasize on their websites, we only read information provided on websites that could be accessed in two clicks or less (Gehman and Grimes, 2017). If we could not find a website for our study’s time period, we consulted other sources, such as firms’ annual reports and the databases Bloomberg and PrivCo (for private companies) to obtain company information. We devised an eight-item checklist that captured NOH values based on multiple factsheets provided by the USDA about organic food, farming, and labeling. These values included emphasizing the use of non-GMO or organic ingredients in products, promoting animal welfare, and environmental sustainability directly related to food production 10 (see the Online Supplement for the complete item list).

After gathering both quantitative and qualitative indicators, we coded target firms into one of three categories: conventional, mixed, or NOH. We initially coded each target firm based on its number of organic certifications at the time of the acquisition. The number of USDA organic certifications ranged from zero to four, and the scores based on qualitative indicators ranged from 0 to 5 for target firms. We used the data’s distribution to determine the cut-off points for placing firms in each category. We coded target firms conventional when they had zero USDA organic certifications, mixed when they had one certification, and NOH when they had two or more certifications.

After this initial grouping, we re-categorized firms, when necessary, based on our qualitative indicators. We shifted a target firm one category closer to conventional if it had none of the qualitative indicators (i.e. from NOH to mixed, or from mixed to conventional). If a firm had one of the qualitative indictors, we shifted it one category closer to NOH (i.e. from conventional to mixed, or from mixed to NOH). If the firm had two or more qualitative indicators, we categorized the firm as NOH. Two trained coders coded 40 firms in 20 acquisition events (10% of the sample) using the same sources, and their inter-rater agreement was 92.5%. We included separate dummy variables coded 1 if the target firm was mixed or NOH, respectively, and 0 otherwise. We used conventional as the excluded category.

Category misfits. 11

To identify category misfits, we first coded the acquirer’s category using the same process employed for coding the target’s category. Because the acquirers were generally much larger, the number of USDA organic certifications ranged from 0 to 30 for acquirers. We coded acquirer firms conventional when they had zero or one USDA organic certification, mixed when they had two to four certifications, and NOH when they had five or more certifications. We then reassessed the categories for their robustness using qualitative indicator scores, which ranged from 0 to 5, and adjusted the categories using the same criteria discussed above. We created separate dummy variables coded 1 if the acquirer firm was mixed or NOH, respectively, and 0 otherwise. If an acquirer engaged in multiple acquisitions, its categorization was updated to reflect changes due to prior acquisitions and/or divestitures. Based on the target and acquirer categories, we created three dummy variables that captured the type of category misfit. We coded extreme misfit one when the acquirer was conventional and the target was NOH, or vice versa. We coded clarifying NOH misfit one when a mixed acquirer bought an NOH target or vice versa. We coded clarifying conventional misfit one when a conventional acquirer bought a mixed target or vice versa. Preliminary analyses showed that clarifying conventional misfit was not significant; thus, its effects were the same as for acquisitions where the acquirer and target were from the same category (the excluded category in our analyses), so we included these firms as part of the excluded category.

Control variables

Pre-acquisition media tenor

As noted above, we calculated the positivity of the acquirer’s media tenor from 1 year prior to the day before (t − 1) the acquisition date.

Total media coverage and total press releases

We controlled for the acquirer’s general media visibility by including separate measures for each acquirer’s total number of articles and press releases during the year before and the year after the acquisition (i.e. the sum over a 2-year period). Since some firms had 0 values, we added a 1 to all values and then log-transformed the measures to reduce the influence of extreme values.

Previous acquisitions

We measured this variable as the number of previous horizontal (i.e. within-industry) acquisitions conducted by an acquirer in the year prior to the current acquisition. We counted previous acquisitions within the last year rather than all prior acquisitions because the most recent acquisitions were more likely to be covered in the media. The number of previous acquisitions ranged from 0 to 5 acquisitions.

Ownership type

Because public firms might receive more media coverage than private firms, and thus experience a greater change in media coverage, we controlled for the acquiring firms’ ownership type by including a dummy variable coded 1 if the acquirer was publicly traded and 0 otherwise.

Acquirer category

The media may be more positively predisposed toward mixed or NOH acquirers. As such, we included separate dummy variables coded 1 if the acquirer firm was mixed or NOH, respectively, and 0 otherwise in our models testing Hypotheses 1–3.

CEO change

CEO succession events could also influence the acquirer’s media coverage; thus, we also controlled for CEO successions. For public firms, we used the EXECUCOMP database. For private firms, we searched their press releases for terms like “CEO,” “CEO change,” and “resign*.” We coded this variable 1 if there was a CEO change event during our study’s observation period and 0 otherwise.

Total recalls

Firms that have product recalls might have received more negative media coverage, so we controlled for acquiring firms’ number of recalls during the observation period. We used the USFDA’s recall database and counted the total number of recalls up to and including each observation year.

Discrediting words in acquisition announcements and post-acquisition press releases

It is also possible that some articles include language that can discredit or contradict NOH language. For example, a press release about an organic mislabeling accusation would include many moral category words but would also include words that are discrediting (e.g. “accusations that our products are not organic”). To take this into account, we also developed a dictionary of terms that journalists used to portray firms in a negative light (available in the Online Supplement), and we included the proportion of discrediting words in the acquisition announcement and press releases multiplied by 100 as separate control variables. 12

Year dummies

We included dummy variables for the years 2008 to 2012 to control for any year specific effects, with 2007 as the excluded category.

We were unable to control for measures such as firm size and performance 13 because 32% of our acquirers were privately held, and these data were not reliably available for all firms in all years. Over three-quarters of the target firms (78%) were also privately held, which limited the data we could collect on them. However, our pre-acquisition media tenor control at least partially captures the effects that size and performance may have on our dependent variable, since they would have a similar relationship with pre-acquisition coverage. Furthermore, as we will discuss, our robustness tests suggest that omitted variable bias is unlikely to be an issue.

Data analysis

Because our dependent variable is continuous, and preliminary analyses showed it was normally distributed, we analyzed the data using OLS regressions in STATA 17. Since there were multiple observations for some firms in the sample, we calculated robust standard errors to correct for serial correlation (White, 1980).

Results

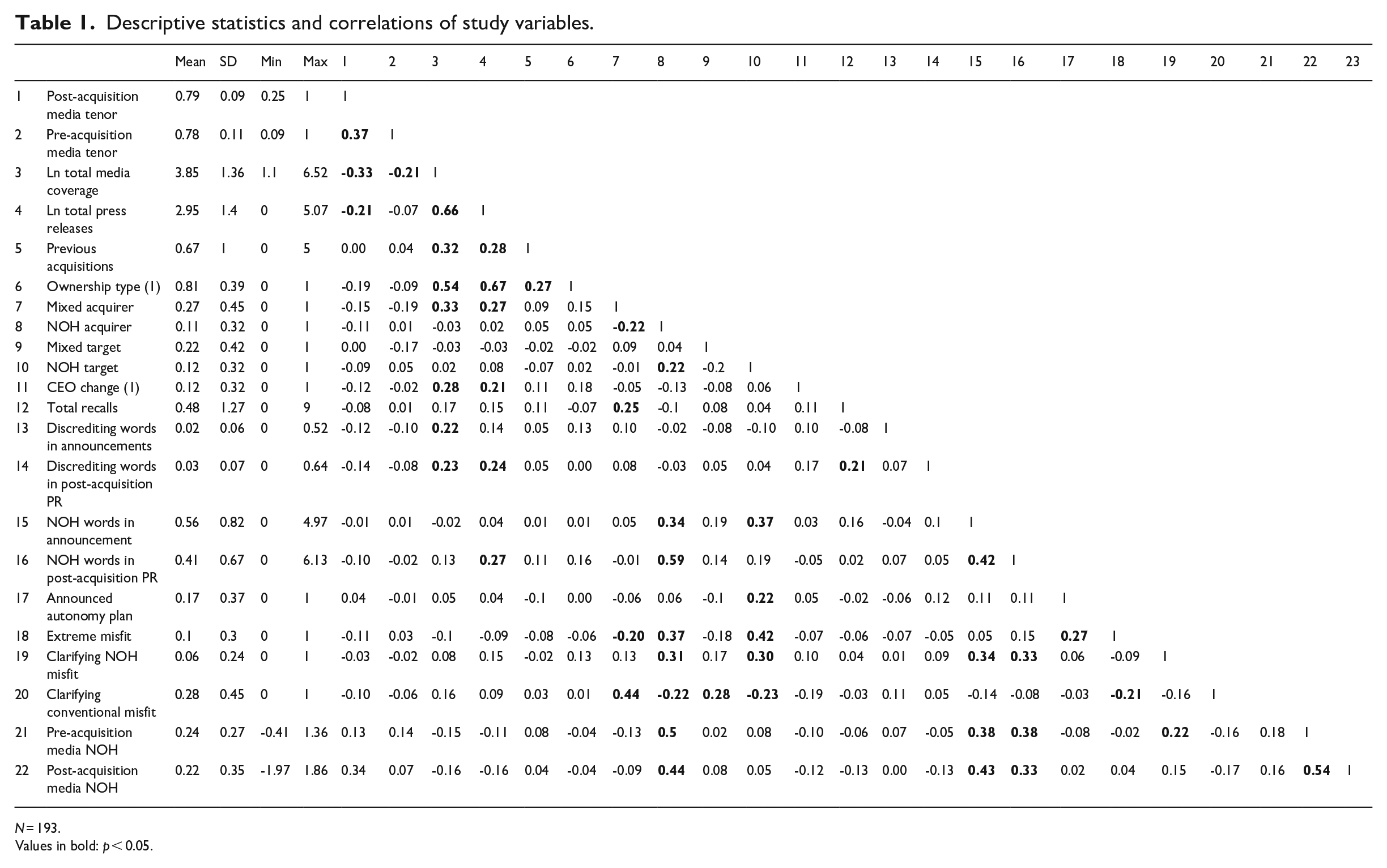

Table 1 provides descriptive statistics and correlations for the measures used in the analysis. We tested for multicollinearity using variance inflation factors (VIFs) and multicollinearity condition numbers (MCNs) for each model. The VIFs ranged from 1.07 to 2.75, all below the recommended cut-off point of 10 (Chatterjee and Price, 1991). The MCNs were 12.64 for the models testing H1-H3 and 11.90 for the models testing H4a and H4b, which were below the cut-off of 30 (Belsley et al., 2005). Thus, collinearity does not appear to be an issue.

Descriptive statistics and correlations of study variables.

N = 193.

Values in bold: p < 0.05.

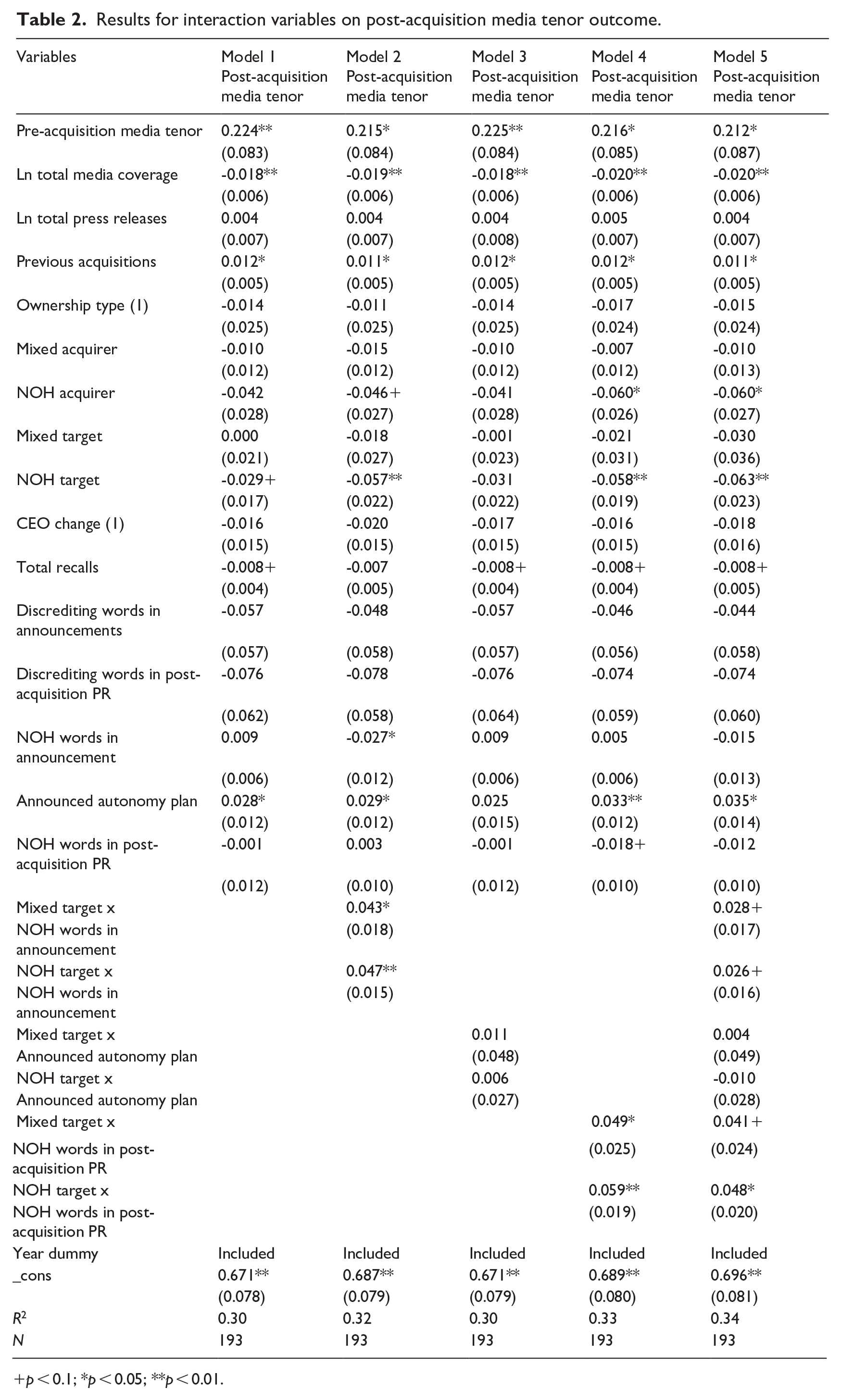

Table 2 presents the models testing Hypotheses 1–3. Model 1 presents the control and independent variables’ main effects. Models 2–4 test Hypotheses 1–3. Model 2 adds the interactions between target firm category and the level of NOH language used in the acquisition announcement, Model 3 tests the interactions between target firm category and announced autonomy plan, and Model 4 adds the interactions between target firm category and the level of NOH language used in the post-acquisition press releases. Model 5 is the fully saturated model that includes all the interactions. Hypothesis 1 predicted that using more NOH words in the acquisition announcement would be positively associated with post-acquisition media tenor when the target has mixed or NOH category membership. Model 2 in Table 2 shows that the interactions between NOH words in the acquisition announcement and both the mixed (p = 0.021) and NOH (p = 0.002) target dummies are positive and significant when predicting media tenor, supporting Hypothesis 1. It is also worth noting that the main effect of NOH language in the announcement is negative and significant (p = 0.031), indicating that when the target is conventional, using more NOH language in the announcement reduces the acquirer’s positive media tenor. The interactions are marginally significant in the fully saturated model with p-values of 0.098 and 0.10.

Results for interaction variables on post-acquisition media tenor outcome.

p < 0.1; *p < 0.05; **p < 0.01.

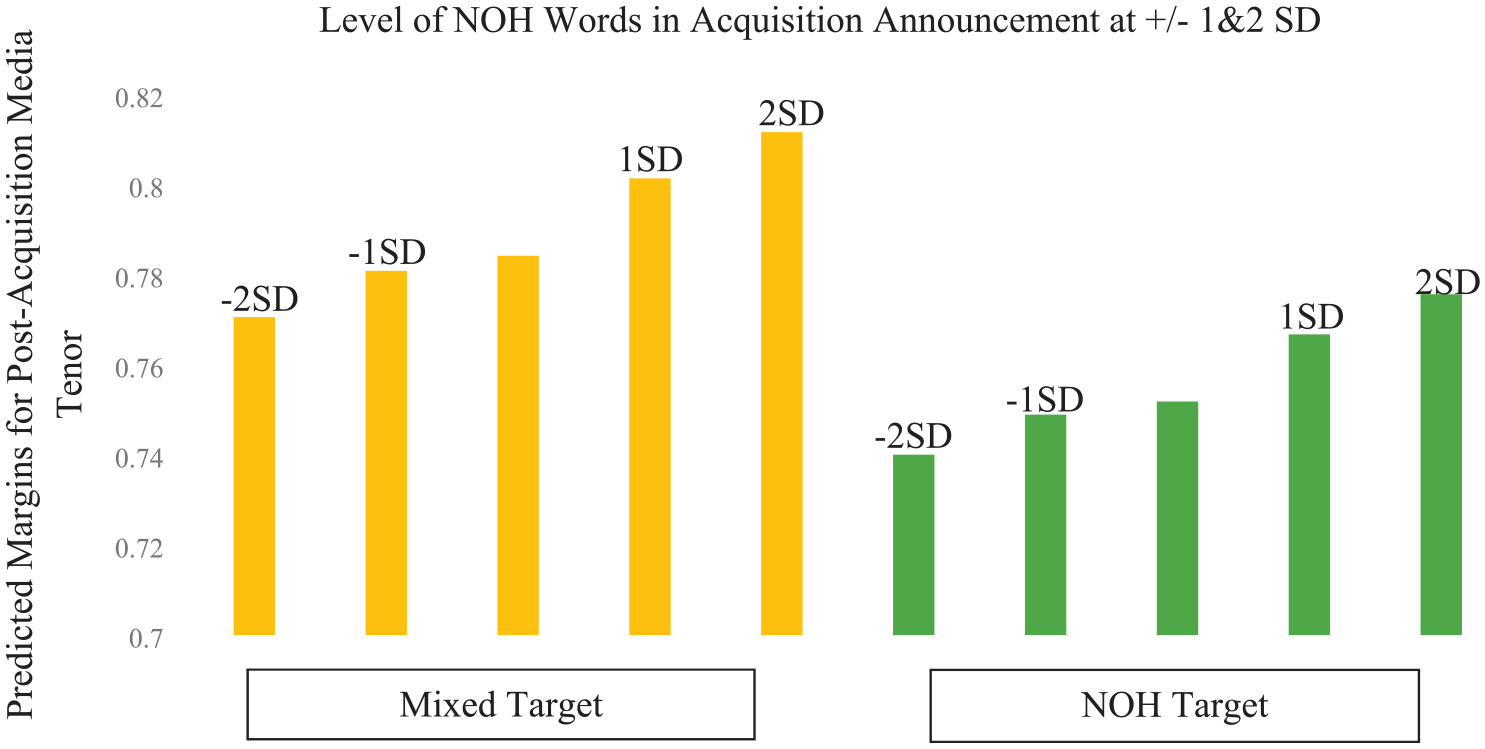

To accurately assess whether the results support our hypothesis across the range of NOH language used, we use the coefficients from Model 5 to graph the interactions using margins analysis (Busenbark et al., 2022a). Figure 1 depicts how media tenor shifts with changes in NOH language usage in the acquisition announcement from two standard deviations below to two standard deviations above the mean usage of 0.5. When the target’s category is mixed, the positive tenor in media coverage is 0.77 when the NOH language in the acquisition announcement is two standard deviations below the mean, increasing to 0.81 at two standard deviations above the mean, a relative increase of 5.3%. For a NOH target, the positive media tenor is 0.74 when the announcement NOH is two standard deviations below the mean, and increases to 0.78 as the announcement NOH increases to two standard deviations above the mean, a relative increase of 4.8%. Thus, Hypothesis 1 is supported. We also tested if the coefficients for mixed and NOH targets were significantly different from each other, but they were not.

Moderation effect of target category on the relationship between NOH words in acquisition announcement and media tenor.

Hypothesis 2 predicted that the positive relationship between announced autonomy and positive media tenor would be stronger when acquiring NOH targets. Both the main effect of announced autonomy and its interaction term are not significant in Model 3, failing to support Hypothesis 2. However, the main effect of announced autonomy is positive and significant in the main effects only model and in the fully saturated Model 5, where the interactions again are not significant. Thus, announced autonomy appears to have a significant positive relationship with positive media tenor regardless of the target’s category.

Hypothesis 3 predicted that using NOH language in post-acquisition press releases would have a positive relationship with positive media tenor for mixed and NOH targets. The results in Model 4 of Table 2 show that the interactions between both mixed (p = 0.046) and NOH targets (p = 0.002) and NOH language in post-acquisition press releases are positive and significant, supporting Hypothesis 3. The interactions remain positive and significant in the fully saturated model with p-values of 0.093 and 0.021.

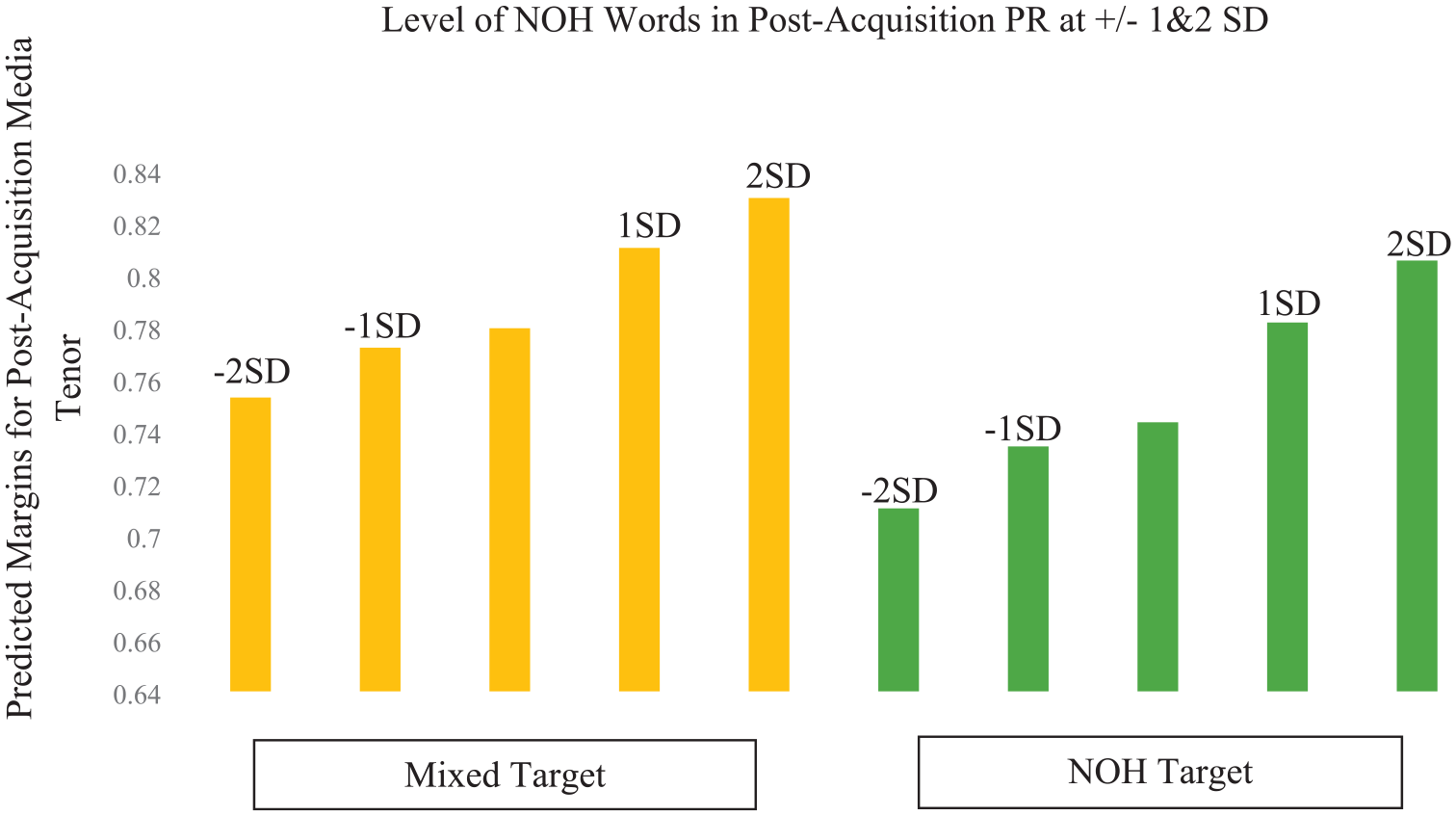

Figure 2 depicts how media tenor shifts with changes in NOH language usage in the post-acquisition press releases from two standard deviations below to two standard deviations above the mean usage of 0.41. Figure 2 shows that for a target from a mixed category, the positive tenor in media coverage is 0.75 when the post-acquisition press release NOH was two standard deviations below the mean, but increased to 0.83 as press release NOH increased to two standard deviations above the mean, a relative increase of 10.2%. For a target from the NOH category, the positive tenor in media coverage is 0.71 when post-acquisition press release NOH was two standard deviations below the mean, but increased to 0.81 as press release NOH increases to two standard deviations above the mean, a relative increase of 13.4%. Hypothesis 3 is therefore supported. Again, tests showed that the interaction coefficients were not significantly different for mixed and NOH targets.

Moderation effect of target category on the relationship between NOH words in post-acquisition PR and media tenor.

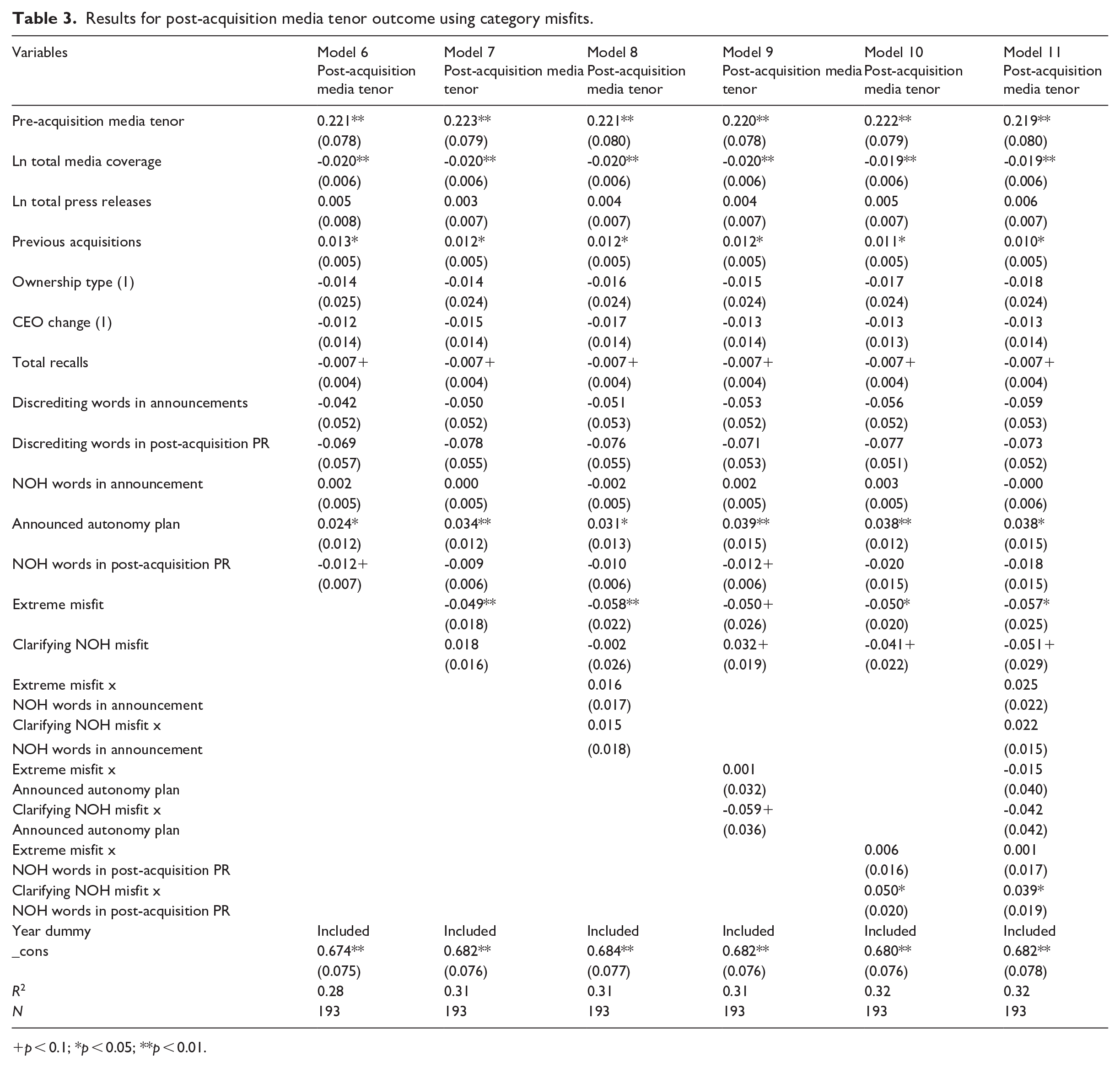

Table 3 presents the models testing Hypotheses 4a and 4b. Model 6 includes the control variables, and Model 7 adds the category misfit variables. Hypotheses 4a and 4b predicted differing impacts of category misfit on post-acquisition media tenor. We found that acquisitions characterized by extreme misfit between the acquirer and target had a negative relationship with positive media tenor (p = 0.007), thus supporting Hypothesis 4a. However, clarifying NOH misfit was not significantly related to media tenor, failing to support Hypothesis 4b.

Results for post-acquisition media tenor outcome using category misfits.

p < 0.1; *p < 0.05; **p < 0.01.

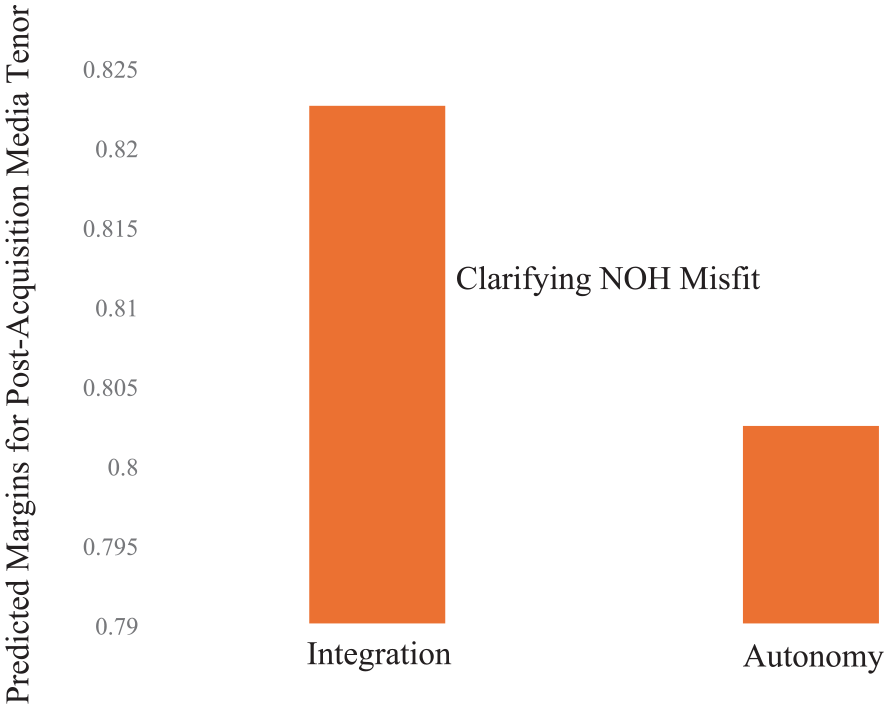

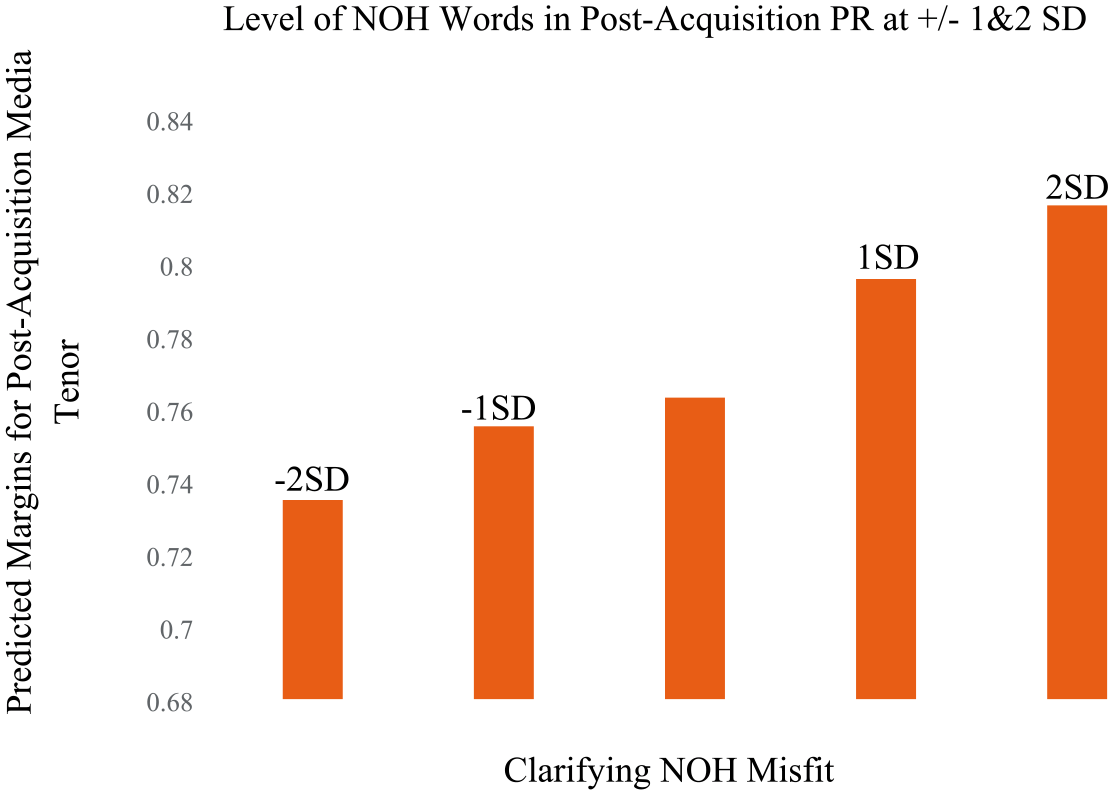

Although not hypothesized, we were curious about the potential influence that category misfits might have on the effectiveness of acquirers’ sensegiving. Models 8–10 include the interactions between the category misfit variables and announcement NOH, announced autonomy plans, and post-acquisition PR NOH. Extreme misfit did not have a significant interaction effect with any of the sensegiving mechanisms, although its main effect remained significant in all models. Clarifying NOH misfit did not have a significant interaction with announcement NOH, but Model 9 shows that, while only marginally significant, clarifying NOH weakened the relationship between acquirer announced autonomy and positive media tenor (p = 0.09), although this relationship was not significant in the fully saturated Model 11. Model 10 shows that clarifying NOH misfit enhanced the relationship between post-acquisition PR NOH words and media tenor (p = 0.012), and this relationship remained significant in the fully saturated model (p = 0.045).

Figure 3 illustrates the shift in media tenor using Model 9 for clarifying NOH misfit pairs when the acquirer announced their autonomy plan. Specifically, the figure indicates that the positive media tenor decreased by 0.02 when the autonomy plan was explicitly announced by the acquirer. Figure 4 demonstrates that for clarifying NOH misfits, the positive media tenor increased from 0.74—when the post-acquisition press release NOH was two standard deviations below the mean—to 0.79 as the press release NOH rose to two standard deviations above the mean, a 7.5% increase.

Moderation effect of clarifying NOH misfit on the relationship between announced autonomy plan and media tenor.

Moderation effect of clarifying NOH misfit on the relationship between NOH words in post-acquisition PR and media tenor.

Robustness tests

In addition to our primary analyses, we conducted several robustness tests. As a more general endogeneity check, we calculated the robustness of an inference to replacement (RIR) for the variables in our model (Frank, 2000). Scholars are increasingly using the impact threshold of a confound variable (ITCV) and/or the RIR to conduct sensitivity analyses to quantify the impact omitted variables must have to cause a potential endogeneity problem (e.g. Busenbark et al., 2017). Given that ITCV analyses have a limited ability to assess interaction terms (Busenbark et al., 2022b), we calculated RIRs for the variables used in our interaction terms using Models 5 and 7 in the main analysis. The RIR quantifies how many biased cases are required to invalidate the causal inference (Busenbark et al., 2022b). We have used both the konfound and pkonfound commands in STATA. We used pkonfound for the indicator variables that do not work with the konfound command (see Busenbark et al., 2022b, for a detailed explanation).

The RIR ranged from 26.85% to 57.48% (Table 4 in the Online Supplement provides specific values), where the lowest percentage was associated with the NOH target and the highest percentage with the mixed target. To put this into perspective, an omitted variable would need to overturn the relationship between mixed target and post-acquisition media tenor in 111 of 193 cases, which seems highly unlikely. In the case of post-acquisition press release NOH, which had an RIR of 40.48%, 78 of 193 cases need to be invalid. Considering the main effects’ RIR, we can assume that omitted variables would be less of an issue because interaction terms are rarely biased, as the unexplained variance would need to be correlated in the same direction with the dependent variable and both first- and second-order effects (Bun and Harrison, 2019).

As a more specific check, to assess whether media outlets largely reproducing firms’ press releases in their articles affected our findings, we considered whether the positive language used in firms’ press releases affected media tenor and was correlated with their use of NOH terms. Firms’ positive tenor was correlated with their NOH language at .10 in their acquisition announcements and at .19 in their post-acquisition press releases, suggesting a weak to moderate relationship (i.e. 1% to 4% of the variance in one measure was explained by the other). We also included firm post-acquisition press release tenor as a control in our models, and it was not significant in any model (see Tables 5 and 6 in the Online Supplement).

Post-acquisition media NOH

Although our focus was on media tenor, we were also interested in whether the media started using more NOH language in articles about the acquirers following the acquisition of mixed and NOH targets. We used the NOH dictionary we developed to derive the level of NOH language in firm’s post-acquisition media coverage using a process identical to the one we used to create the media tenor variable. The results showed a significant interaction between post-acquisition press release NOH and NOH targets (p = 0.008) (see Model 4 in Table 7 in the Online Supplement), but no significant interactions with acquisition announcement, NOH language, or announced autonomy plan. Thus, the media did not appear to pick up and use NOH language simply based on acquisition announcements, unless the target category was reinforced in the post-acquisition press releases.

Acquisition novelty

It is also possible that acquirers who were already NOH might not receive much additional media coverage for making a NOH acquisition. To assess whether this was the case, we conducted a t-test comparing the mean change in media coverage between NOH acquirers versus mixed and conventional acquirers. The difference in the means between the two groups was not significant, suggesting that NOH acquirers were not discounted.

Shorter windows for news articles

It is possible that the 1-year window we used to gauge media sentiment could include confounding events. Thus, we also tested shorter coverage windows of 1 week and 1 month, 3 months, and 6 months to calculate our dependent variable. Following the same article collection rules as above, we had 59 observations with non-zero values and 139 observations with zero values for the 1-week period, which provided insufficient power to run the analysis. When we used the 1-month window, 110 observations had non-zero values and 83 observations had zero values, which, although better, still had limited power. Thus, we were unsurprised when we only found one marginally significant relationship (see Tables 8 and 9 in the Online Supplement). Using 3-month and 6-month windows yielded 149 and 171 non-zero observations. We found weaker but similar significant results to our main analysis (see Tables 10–13 in the Online Supplement). Furthermore, events that affect the positivity of media coverage but are unrelated to the acquisition would only make it harder to find our observed relationships, making our tests more conservative. Given the frequency with which firms receive media coverage, that category membership is not a short-term construct, and that category change is not a short-term process, we believe our 1-year window is reasonable.

Controlling for firm performance

We conducted a sub-sample analysis using only public acquirers to test if post-acquisition performance affected the results. This was to account for the possibility that post-acquisition performance would have a significant impact on media tenor, overshadowing the impact of sensegiving activities and targets’ category membership. Sub-sample analysis shows that although better performance following the acquisition positively influenced the post-acquisition media tenor for the firm, the results of our main analysis did not change substantially, even when controlling for firm performance (see Tables 14 and 15 in the Online Supplement). Although we need to be careful when interpreting the sub-sample analysis, as excluding private firms reduces the sample size considerably (22%), this indicates the robustness of our original findings.

Discussion

In this study, we examined how the media, as an important information intermediary, reacts to firms’ sensegiving in moral markets. Our results show that sensegiving efforts by acquirers at the time of and after an acquisition can reduce interpretive uncertainty and influence media sentiment. The media is more positive when a target with partial or full NOH category membership is acquired and the acquirer uses more NOH language in its acquisition announcement and post-acquisition press releases. We also found that the media is more positive when the acquirer announces the target firm will maintain its autonomy, regardless of the target’s category membership, unless the acquisition clarifies the acquirer’s strategic intentions. And we found that the media is less positive when there is an extreme misfit between the acquirer and target’s categorical differences.

Our study builds on and extends the literature on moral markets by investigating how individual firms attempt to navigate the moral market past its initial legitimation stage using sensegiving activities. Moral markets differ from other market categories that have clearer boundaries once legitimated. Evolving moral markets exhibit fuzzier boundaries as moral principles permeate neighboring categories to varying degrees, creating interpretive uncertainty for key audiences.

Our aim was to better understand whether the sensegiving activities of firms participating in moral markets affected the media’s interpretive uncertainty and assessments of firms’ actions. We found that acquiring firms’ sensegiving efforts in their external communications to align the cognitive frames employed were effective in enhancing media sentiment. Acquirers using press releases to communicate their adherence to the new moral standards during and after the acquisition event were effective in influencing media sentiment about the firm, but only when the target straddled or was fully in the new moral category. If the target was conventional, then using more NOH language was negatively related to media sentiment, suggesting the media may be sensitive to “greenwashing” (Kim and Lyon, 2015) efforts, and that authenticity is important for the sensegiving to be effective. It also appears that acquiring a target that conforms to the moral market’s standards alone is insufficient; firms also need to use rhetoric that is aligned with the desired category association to help reduce the media’s uncertainty about what is likely to happen. This interpretation is consistent with prior theorizing on intangible asset accumulation (Dierickx and Cool, 1989). The target needs to have some characteristics consistent with the message the acquirer is providing, thereby helping the acquirer enhance its evaluation.

We also contribute to the categories literature by looking into conditions where category straddling is desirable and can help reduce, rather than increase, interpretive uncertainty. Whereas a significant amount of categories research has focused on the negative effects of category straddling (e.g. Hsu, 2006; Zuckerman, 1999), scholars have also begun exploring when straddling is valued (e.g. Paolella and Durand, 2016; Wry et al., 2014). Our findings add to this work by showing that category straddlers are as effective as non-straddlers in reducing interpretive uncertainty when sufficient sensegiving is also employed. Prior research has not considered how companies’ strategic communications can reduce the interpretive uncertainty that accompanies category straddling. The fuzziness straddling creates provides some freedom for acquirers to choose which categorical aspects to emphasize in their sensegiving activities.

Another interesting implication is that acquisitions in moral markets can indicate whether the firm is moving further into the category, but gradual transitions appear to be more informative than large moves. Extreme categorical differences between the acquirer and target (i.e. from fully conventional to fully NOH, or vice versa) appear more likely to increase interpretive uncertainty and are perceived more negatively by the media. Acquisitions of firms completely in the moral market by firms completely outside the moral market likely raise concerns that the acquirer will destroy the target’s value (Haleblian et al., 2009). Conversely, acquisitions by firms completely in the category of firms completely outside the category may raise questions about the acquirer’s continued commitment to the moral market’s values. However, when either the target or the acquirer straddles the moral market category, the acquisition can be more easily interpreted as enhancing the acquirer’s commitment to the moral market, thereby reducing interpretive uncertainty and prompting more positive media sentiment. For instance, if a firm with mixed NOH standing acquires a fully NOH firm, observers may interpret this as the acquiring firm trying to develop more NOH standards and know-how.

The negative moderation effect of the autonomy announcement by clarifying misfits seems to support this argument. We found in our primary analysis that the media responds positively to autonomy announcements regarding the target’s category membership, which makes sense, given general concerns about the target’s unique value-creating capabilities being destroyed post-integration (Haleblian et al., 2009). However, when there are “clarifying” misfits between the acquirer and target that suggest the acquirer is becoming more committed to the moral market, the media may interpret the acquisition as an attempt to enhance the acquirer’s commitment to the moral market—thus expecting a greater level of integration. Announcing the target will maintain its autonomy violates this expectation. These findings suggest a more nuanced understanding of how firms can approach autonomy announcements. If the acquisition does not clarify the acquirer is moving further into the moral market category, rather than trying to promote the “synergies” an acquisition will allegedly create, then acquirers can assure stakeholders that they will not break what they have just paid dearly for—which is often stakeholders’ more pressing concern. However, if it is a clarifying acquisition, they may want to indicate that greater integration is likely. This also suggests that firms need to be careful about making large changes to their category membership and may be better off easing their way into category straddling or shifting by taking a stepwise approach.

In sum, our findings provide interesting implications for an acquirer’s target choices. Given that acquiring a target with a mixed category membership can positively influence media evaluations as much as a NOH target with appropriate communication, opting for a mixed target rather than a firm fully in the NOH category can be a safer choice, especially if the acquirer is trying to move into the NOH category. Choosing an ambiguous target gives the acquirer more flexibility and can reduce negative concerns associated with the acquisition. Moreover, it may also be possible that acquiring a firm in a moral market category simply costs more, due to its desirability, than firms with mixed or conventional bearings. Lower costs, along with more flexibility and less negativity, can significantly reduce the risk to the acquiring firm. Then, once the acquirer has adjusted into the mixed category, it can start moving fully into the NOH category with less risk. Ambiguous targets like the mixed target firms in our sample serve as positive examples of the category straddling that scholars have begun to explore (e.g. David and Lee, 2022; Paolella and Durand, 2016; Wry et al., 2014).

More broadly, our findings also highlight a unique situation where boundaries between market categories are not very clear-cut, even after legitimation. An underlying assumption of the categories literature is that the boundaries between categories are clear once a category is legitimated (David and Lee, 2022; Navis and Glynn, 2010). Moreover, the new market category construction literature focuses on how new market categories distinguish themselves from existing categories (Durand and Khaire, 2017). However, evolving moral markets present a more complex situation; once the category has emerged, more conventional firms start straddling into the market to capture its benefits, creating fuzzier category membership boundaries, since many firms are neither fully in nor out of the moral market. Thus, understanding the strategic actions that moral market participants can take, and how they shape perceived category boundaries, can shed greater light on their evolution.

Finally, our post hoc analyses also showed that whereas using more NOH language in the acquisition announcement did not increase the media’s use of NOH language in its subsequent coverage, consistently using NOH language in post-acquisition press releases was positively associated with the media’s use of more NOH language in the acquirer’s coverage when the target was in the NOH category. This finding suggests that if a firm seeks to ensure that the media reflects the desired message (Price et al., 2008; Rindova et al., 2007), it needs to consistently employ the language it desires in its messaging over time.

Limitations and future research directions