Abstract

We examine the role of ownership in organizational responses to performance shortfalls. State owners prize performance stability over being competitive, and their firms thus frame performance shortfalls differently than private firms do. In particular, state firms’ performance-stability orientation makes them respond to small performance shortfalls more readily than private firms do. They largely disregard performance comparisons with industry competitors, which more readily trigger divestitures at private firms. Comparisons among state firms matter relatively more. We find empirical support for these propositions in the population of Chinese state and private firms publicly traded in Shanghai and Shenzhen Stock Exchanges from 2003 to 2019. The frame-contingent responsiveness we document extends theory of organizational behavior and adds important nuance to our understanding of state-firm inertia.

Introduction

Performance feedback is central to the behavioral theory of the firm (BToF). Boundedly rational firm actors compare performance results to aspiration levels (Cyert and March, 1963) and may respond to performance shortfalls with changes such as leadership turnover (Moliterno et al., 2014), alliance formation (Kavusan and Frankort, 2019), network dissolution (Clough and Piezunka, 2020), R&D investments (Xu et al., 2019), acquisitions (Kuusela et al., 2017) and divestitures (Vidal and Mitchell, 2015).

Firm responsiveness, however, varies strongly (Klingebiel, 2018; Kotiloglu et al., 2019). This motivates a research stream seeking to understand why firms with similar performance feedback vary in their propensities to change (Audia and Greve, 2021; Gavetti et al., 2012; Posen et al., 2018). Contingencies include managerial characteristics (Schumacher et al., 2020; Zhang and Greve, 2019), firm size (Audia and Greve, 2006; Smulowitz et al., 2020), organizational structure (Gaba and Joseph, 2013; Joseph et al., 2016), firm experience (Desai, 2008; Eggers and Suh, 2019), and network position (Hu et al., 2022; Shijaku et al., 2020).

Such studies usefully delineate organizational conditions under which one might expect some firms to react to shortfalls more nimbly than others. However, beyond organizations’ structural ability to change, such as their information processing capabilities (Baumann et al., 2019), for example, a more behavioral understanding of feedback responsiveness seems in order. Firm characteristics may create heterogeneity in the decision frames used for feedback interpretation. Such decision frames can generate response heterogeneity among firms even when they are structurally just as able to change.

We examine the impact of ownership (Cyert and March, 1963), particularly state versus private. Owner objectives (Boyd and Solarino, 2016) provide guiderails for how performance is assessed and how feedback is interpreted (Audia and Greve, 2021; Greve and Zhang, 2017). Managers may be influenced by their upbringing, social circles, or political environments, among others, but they arguably experience no stronger direct influence on the decision frames than by those who own the firm they work for and whose aims they are employed to further (La Porta et al., 1999).

The recent resurgence of state ownership (Cuervo-Cazurra et al., 2014) provides an opportunity to contrast two well-delineated types of owners, government and private entities. Among the 100 largest multinational firms in the world, state owners control 19 (Cuervo-Cazurra et al., 2014). In 2019, roughly 31% of all listed Chinese firms had a state owner. While private firms mostly strive to return money to investors, 1 state firms additionally fulfill political goals such as ensuring societal stability (Megginson and Netter, 2001). State firms duly aim to steady their financial performance, providing reliable employment and guarding against social unrest (Wen, 2020). State firms are to absorb fluctuations such as those caused by the recent pandemic (The Wall Street Journal, 2020).

State firms, therefore, have a stability mandate. Their state owners seek steady performance over time and worry less about how this compares to other firms. We argue that this focus on stability and historical context makes state firms perceive a negative deviation from past performance levels as a more significant problem than their privately held peers do, responding more promptly to such shortfalls. By the same token, state firms pay relatively less attention to how they stack up against competitors. We expect to detect these diverging emphases by examining firms’ organizational responses to historical and social performance-feedback metrics.

Organizational responses to feedback often involve resource reconfigurations. Divestitures in particular are an intuitive reaction to perceiving a problem (Bergh and Lim, 2008; Moliterno and Wiersema, 2007) 2 and are readily identifiable (e.g. Kuusela et al., 2017; Shimizu, 2007; Vidal and Mitchell, 2015). The announcements of divestitures worldwide totaled over $200 billion in 2016 (Deloitte, 2017). Both state and private firms take this resource-reconfiguration route to problem-solving (Doh et al., 2004). 3 Divestitures thus are an ideal indicator for a test of our hypotheses.

We study the population of firms traded on Chinese stock exchanges between 2003 and 2019. We find that performance (return on assets) shortfalls relative to historical aspirations more strongly influence divestiture behavior in state firms than private firms, and that performance shortfalls relative to social aspirations more strongly influence divestiture behavior in private firms than state firms. State firms do not completely ignore all external performance signals; they selectively disregard those from private firms while still benchmarking against other state firms. These findings, robust to alternative explanations and specifications, support our hypotheses.

The study makes two primary contributions to theory. First, it contributes to the behavioral theory of the firm a greater understanding of feedback-response heterogeneity (Greve and Gaba, 2017). In particular, we provide an account of how ownership conditions organizational responses to performance feedback, complementing prior emphases on organizational leadership, scale, structure, experience, and networks (Desai, 2008; Hu et al., 2022; Rhee et al., 2019; Schumacher et al., 2020; Smulowitz et al., 2020; Zhang and Greve, 2019).

Second, our work leverages the BToF perspective to generate behavioral insights into the state-firm phenomenon. It turns out that state firms are not quite as inert as they are thought to be. On occasion, they more readily change their behavior than their private peers, particularly when seeing performance negatively deviate from historically formed aspirations. Thus, our work helps explicate the theoretical puzzle of why state firms, deemed as bureaucratic and inert, can occasionally outdo private firms (Musacchio and Lazzarini, 2014).

Theory and hypotheses

In the behavioral theory of the firm, performance declines relative to aspirations indicate problems, stimulate search, and engender change (Cyert and March, 1963). Despite a powerful theoretical narrative, empirical attempts at verifying it produced variegated results (Klingebiel, 2018; Kotiloglu et al., 2019), with supporting (Joseph et al., 2016), opposing (Iyer and Miller, 2008), contingent (Kuusela et al., 2017), nonlinear (Ref and Shapira, 2017), and insignificant (Blagoeva et al., 2020) results. This inconsistency has spurred interest in whether, and under what conditions, organizations might learn from performance feedback (Greve and Gaba, 2017).

Explanations of firm responsiveness to performance feedback fall into one of three camps (see Posen et al., 2018). The first emphasizes threat rigidity. Organizations with performance shortfalls refrain from changing when focusing on threats to organizational survival (Audia and Greve, 2006; Shimizu, 2007). A second line focuses on self-enhancement and attribution. Decision makers, who tend to view themselves positively, might perceive the negative performance feedback as less negative, and therefore, initiate less change (Jordan and Audia, 2012). The third line of research highlights sensemaking. Decision makers’ conception of what defines a problem influences the direction of feedback-driven search as well as the choice of alternatives rendered by the search. Organizational structure may play a role (Gaba and Joseph, 2013), as could managerial characteristics (Schumacher et al., 2020), organizational scale (Smulowitz et al., 2020), and firm experience (Desai, 2008).

Our study further extends the sensemaking perspective by examining how organizational ownership frames feedback and leads to responsiveness. The centrality of organizational ownership for information processing is well documented (Foss et al., 2021), but has not been integrated into BToF models of responses to feedback (Gavetti et al., 2007). For example, as Thornton (2004: 70) noted, ownership provides boundedly rational firm actors with “assumptions and values, usually implicit, about how to interpret organizational reality, what constitutes appropriate behavior.” Thus, ownership control might provide a frame for managerial processing of cues such as those that performance feedback might provide (Foss et al., 2021).

A particularly strong distinction in ownership is whether or not a firm is controlled by the state (Delios et al., 2006; Xu et al., 2014). State firms exist to provide financial stability, whereas private firms strive to outdo their competitors (Megginson and Netter, 2001). So if the sensemaking frame provided by organizational ownership indeed had an impact on firms’ responsiveness to change, it should be detectable in as stark a juxtaposition as that between state firms and private firms.

State and private firms: ownership frames

At first glance, conventional wisdom would suggest that firms protected by the state care less about performance. In recent decades, however, state capitalism adopted market mechanisms such as incentive-based pay, employee share ownership, and free-wheeling innovation units (The Economist, 2014). As a result, state firms have become “marketized” (Nee, 1992: 1) and performance-oriented (Musacchio and Lazzarini, 2014). Profit generation has become a common evaluation criterion for managers at state firms (Aharoni, 1981), on the basis of which they are promoted (Cao et al., 2019).

Yet, there is more to performance than its absolute level. One reason for why states maintain ownership is to ensure societal stability (Bruton et al., 2015). Disruptions in labor markets and external shocks can threaten social stability as well as political legitimacy (Wen, 2020). A stability mandate for state firms has been observed in countries as diverse as Italy and India (The Economist, 1994, 2017b), providing employment and thus preventing social unrest (Wen, 2020). One of state firms’ primary concerns, therefore, is variance—or rather its absence—in performance.

To attain the goal of societal stability, state firms need financial health (Wang and Luo, 2019). Rather than dictating specific strategies, governments often afford state firms sufficient autonomy to take necessary measures for their financial sustainability, and provide backstops like subsidies to struggling entities (Wen, 2020). This approach is grounded in the belief that financial health is a precondition for state firms’ ability to aid societal stability (Nee and Opper, 2012). State firms thus naturally focus on stabilizing their financial performance. For example, the statement of purpose for Zhongyuan Agricultural Industries Co., LTD, a Chinese state firm, includes “following government guidance” (in Chinese: 政府引导) and “preserving business stability” (in Chinese: 稳健经营). 4 Consequently, state firms attend to performance but seek to ensure continuity more so than other potential goals such as growth or industry leadership.

Although private firms might be subject to some state regulation, they have no comparable obligation to aim for stable performance. Private firms can thus tolerate greater performance swings in the pursuit of competitive advantage (The Economist, 2017a). State firms’ stability priority, by contrast, makes them more intolerant of performance shortfalls. Smaller negative deviations in their performance trajectory consequently weigh more heavily in decision-making at state firms than that at private firms. And when underperformance is recognized as a problem, state firms may respond through resource reconfigurations (Greve and Zhang, 2017; Li et al., 2017) or other changes to their business (Wang et al., 2018; Zhou et al., 2017).

As compensation for their nonmarket duties, the government often provides state firms with protections from market pressures, including government subsidies and favorable access to finance (Sapienza, 2004). Thanks to such protection, a majority of state firms trail their private peers in business activities such as investments (The Economist, 2017c), even if some state firms occasionally outpace their private counterparts (e.g. Hsu et al., 2023). Indeed, the government has been lenient about straggling state firms, since the primary role of state firms is not industry leadership but rather stability preservation. 5

The primacy of stability over competition, or vice versa, likely generates different frames for decision-making (Greve and Zhang, 2017). Although both private and state firms pursue performance goals, state firms might care more about the stability of their own performance trajectory and less so about performance signals in the competitive markets. Whether or not a firm considers performance shortfalls as problems thus hinges on ownership.

Framing historical performance shortfalls

A stability frame likely amplifies the perceived relevance of a negative performance deviation from historically formed aspirations. A shortfall deemed small by normative standards might be relevant enough for some firms to act on, depending on how much they prize performance stability. The more firms value stability, the more likely that they see shortfalls as problems in need of fixing. This is consistent with Lant et al.’s (2006) finding that deviations from expected performance levels lead to strategic changes more often in stable than turbulent environments. Their findings could be interpreted as firms accustomed to stability more readily framing small setbacks not just as anomalies, but as signals warranting strategic reassessment and potential changes.

State firms, in particular, fall into this category. Their broader objectives encompass social and, therefore, financial stability (Megginson and Netter, 2001). They might be particularly sensitive to even marginal downturns in performance, as these may be seen to be threatening the state owner’s political legitimacy, particularly in terms of maintaining employment and economic stability (Wen, 2020). Performance declines thus do not bode well for state-firm executives’ promotions to other government bodies (Cao et al., 2019).

Private firms, conversely, tend to focus more sharply on profitability, with accountability mainly toward private investors interested in financial returns (Megginson and Netter, 2001). These investors may tolerate performance swings alongside the usual ups and downs of their industry and markets, as long as the long-term profit outlook is positive (Ref and Shapira, 2017). Hence, private firms might more likely perceive minor performance shortfalls as normal market dynamism (Jordan and Audia, 2012), warranting observation but not necessarily precipitating immediate changes (Blagoeva et al., 2020).

This suggests that a state firm, with its additional stability objective, may assign greater significance to small performance shortfalls. For state firms with a stability frame, a small deviation would “pack a big punch” (Parker et al., 2017: 2341). They more likely than their private peers see a dip in performance as reflective of a failing strategy. A heightened alertness to any disruptions that might affect their extensive responsibilities could lead to prompt changes aimed at reestablishing desired performance levels (cf. Lant et al., 2006). Their stability-oriented lens may lower the threshold for what is deemed a significant deviation.

Private firms might regard the same performance shortfalls as negligible and within the realm of normal business volatility, especially if peers experience the same. Such a stance is often underpinned by a strategy that prioritizes long-term financial gains and recognizes the influence of factors beyond the firm’s control (Fitza, 2014). In these firms, substantial changes might be reserved for more severe performance declines, or declines relative to competitive benchmarks, that signal a negative trend with potential long-term consequences (Joseph and Gaba, 2015). This is consistent with findings in prior research showing private firms’ unresponsiveness to performance shortfalls near historical aspiration levels (Jordan and Audia, 2012; Ref and Shapira, 2017).

Overall, a stability frame makes small deviations in performance trajectories meaningful for state firms. Therefore, we expect state firms to more readily perceive smaller shortfalls of historically formed aspirations as relevant than private firms. Once perceived as problematic, the deviations trigger adaptation decisions. 6 Orthogonal to the structural inertia that comes with state control (Greve and Zhang, 2017), we expect a behavioral response to negative performance deviation from historically formed aspirations—more so from state firms than from private firms. We, therefore, propose the following:

H1: State firms are more responsive than private firms to performance shortfalls relative to historical aspirations.

Framing social performance shortfalls

Performance over time is but one indicator of potential problems. Performance relative to competitors is indicative too (Cyert and March, 1963). Juxtaposing firm performance with that of industry peers—here defined as the “entire population of external marketplace competitors” (Hu et al., 2017: 1436)—helps decision makers evaluate their firms’ competitive position (Greve, 2003). Falling short of industry-peer performance might indicate a problem and the more firms value profit maximization, the more relevant a deviation from socially formed aspirations becomes.

Private firms often calibrate their strategies against industry benchmarks (Hu et al., 2017), mindful that falling behind bodes ill for profits and financing (Greve, 2003). The relative standing among industry peers thus is a crucial barometer for profit-oriented firms (Cyert and March, 1963), serving as a direct measure of their competitiveness (Joseph et al., 2016; Porter, 1985). Research shows private firms taking relative underperformance as cue to reassess their strategies or embark on strategic overhauls like divestitures to reclaim competitive advantage (Kuusela et al., 2017; Vidal and Mitchell, 2015).

State firms, by contrast, may disregard competitive metrics (Bruton et al., 2015). Their stability focuses on subordinates’ concerns over how they rank against industry peers (Aharoni, 1981). Thus, state firms may perceive performance deviations from competitive benchmarks as less relevant than their private peers do (Lin et al., 1998). Once perceived as less (if at all) problematic, state firms would be less likely to respond to evident gaps between industry performance and their own. We, therefore, propose the following:

H2: State firms are less responsive than private firms to performance shortfalls relative to industry peers.

Framing social performance shortfalls: state peers

State firms are not entirely ignorant of peer performance, however. They compare their performance against a different set of social referents. Firms, akin to individuals (Festinger, 1954), compare themselves with similar others to evaluate their own standing (Blettner et al., 2015; Moliterno et al., 2014). Specifically, rather than contrasting their performance against the entire industry, many firms tend to focus on a subset of competitors sharing similar characteristics such as size or segment focus (Baum and Mezias, 1992; Kalnins, 2016). This focused approach also features in Porac et al. (2007) work on cognitive groupings. Benchmarks are established within strategic groups characterized more by the depth of similarities and strategic relevance than by the breadth of the industry.

Building off these observations, we posit that state firms, although less concerned with their overall industry standing, do not entirely ignore external performance signals. Instead, state firms likely adopt a selective benchmarking approach, with a particular attention to a subset of peers that resemble their own organizational form, that is, other state firms that face similar governmental expectations (Bruton et al., 2015). Managers within these entities are attuned to the performance of other state firms that navigate a similar set of expectations and realities.

This alignment with state peers stems not merely from shared governmental expectations but also from the intra-industry competition that influences managerial career trajectories. Managerial promotions are often contingent upon the financial performance of their firms, with better-performing managers being more likely to ascend to prominent governmental positions (Cao et al., 2019). A competitive climate fosters robust internal benchmarking systems with managers highly responsive to how they stack up against their counterparts in other state firms.

We, therefore, expect state firms to perceive greater similarity and rivalry with other state firms. Performance shortfalls relative to this cognitive grouping of “state peers” matter more than those relative to other industry participants.

State firms observe the performance of private firms but frame this as less relevant. The difference in objectives—private firms being profit-driven and state firms additionally oriented toward broader political goals—creates a cognitive delineation wherein private firms’ performance is relegated to a lower tier of strategic relevance.

State firms thus monitor and respond to the performance trajectories of other state entities. Vying for political overachievement and progression, the relative performance of state entities fosters a distinctive competitive paradigm. Therefore, the strategic responses of state firms to performance metrics are more pronounced and immediate within this tightly knit group, underscoring a nuanced approach to benchmarking that privileges state-aligned entities over the broader, profit-driven private sector. We thus expect state firms, despite generally discounting peer benchmarks, to be sensitive to performance shortfalls relative to state peers. We, therefore, propose the following:

H3: State firms are more responsive to performance shortfalls relative to state peers than private peers.

Methods

Empirical setting

We examine our hypotheses by studying firms traded at Chinese stock exchanges. China allows for both state firms and private firms to coexist (Greve and Zhang, 2017). The Chinese economy has become one of the principal empirical settings for studying state ownership (e.g. Greve and Zhang, 2017; Zhou et al., 2017). Whereas, in the late 1970s, the Chinese economy was dominated by state firms (Xu et al., 2014), state firms today make up only 31% of firms on Chinese stock markets.

A process of marketization promoted the profit orientation of state firms (Naughton, 2006). For instance, since the 1990s, the central government mandated that state-firm CEOs must be knowledgeable about the principles of capitalism (Li, 1998). Since 2003, the State-owned Assets Supervision and Administration Commission (SASAC) monitors state firms and enforces performance evaluation guidelines. Criteria for annual appraisals include profitability measures of net income (Cao et al., 2019).

SASAC’s guidelines also ask state-firm CEOs to increase performance or face negative appraisals (SASAC, 2009). SASAC appraisals directly determine CEO compensation and may lead to dismissal. Such performance pressure is equivalent to the investor-led performance pressure of private firms. Thus, state firms stand to ignore performance no more than their private peers.

While political promotion based on state-firm performance is not explicit, empirical evidence suggests that CEOs at outperforming state firms are more likely to get promoted to leadership positions in the Communist Party and/or state agencies (e.g. Cao et al., 2019). For example, former Vice President of the People’s Republic of China, Qishan Wang, was the CEO of the state-controlled China Construction Bank before being appointed to the Politburo Standing Committee of the Communist Party in Guangdong Province in 1997.

In addition to a strong performance orientation, Chinese state firms fulfill a political mission (Wang and Luo, 2019). The State Council of the People’s Republic of China (2015), for example, asks state firms to “correctly handle the relationship between reform, development, and stability” (in Chinese: 正确处理改革、发展、稳定的关系). In the interest of preserving societal stability, state firms duly stabilize their performance. For example, state firms resumed operations in the wake of the coronavirus outbreak (The Wall Street Journal, 2020), so as to fulfill the government’s stability mandate.

The Chinese government offers state firms public-procurement contracts, access to credit, and direct government subsidies (Nee and Opper, 2012), as long as state firms reliably serve the stability mandate. Such government protection partly explains state firms’ relative inertia (Zhou et al., 2017). Indeed, competitiveness is neither explicitly mentioned in SASAC’s performance evaluation guidelines nor empirically linked with the compensation and promotions of state-firm CEOs. Success in competitive markets is a bonus, not a must. Thus, competitiveness often ranks below stability in the set of goals at Chinese state firms.

Despite some political influence through party cells, private owners are the principal decision makers at private Chinese firms. Private owners have no obligations to preserve stability beyond following industry regulations such as the new law on preventing minors from consuming electronic games (The Economist, 2021). Consequently, the decision rationales of Chinese private firms are more similar to those of their international peers than to compatriot state enterprises. Performance at Chinese private firms is a function of market share just as it is at their international peers (Xia and Liu, 2017). Competitiveness thus is the prime concern for Chinese private firms.

Sample and data

We analyze a longitudinal data set of all publicly traded firms in mainland China, that is, the A-share 7 market of Shenzhen and Shanghai Stock Exchanges. The observation window ranges from 2003 to 2019, with the year 2003 being the earliest in which state-control information is systematically available. We collected our data from the China Stock Market and Accounting Research (CSMAR) and Wind databases, both of which have found prior use in strategy research (e.g. Greve and Zhang, 2017; Haveman et al., 2017).

The initial sample includes 37,536 firm-year observations of 3741 firms. We lagged our models by 1 year to minimize the possibility of reverse causality, dropping 3741 first-year outcome observations from our data set. An additional 1667 firm-year observations drop out due to missing values. Furthermore, since we use a within-firm specification, 999 firms with non-varying divestitures (mostly zero) drop from our sample, removing 4141 firm-year observations. This is in line with established practice in research on organizational change (Clough and Piezunka, 2020; Eggers and Suh, 2019), and ensures that our estimation method matches the longitudinal nature of our behavioral predictions (Gavetti et al., 2012; Posen et al., 2018). Our final sample comprises 27,987 firm-year observations for 2459 firms. Among these, 1155 firms are state-controlled (13,375 firm-year observations).

The 2459 firms selected for our analysis are 25 percentage points more likely to be state-owned ( p < 0.001) than the 999 firms excluded from our analysis. Therefore, our coefficient estimates for the effect of state control on change might be positively biased. Selected and excluded firms show no significant differences in those tests. In particular, performance shortfalls differ insignificantly (Δp = 0.54 for historical performance shortfalls; Δp = 0.66 for social performance shortfalls).

Dependent variable

Among the most significant, well-understood, and measurable forms of change are resource reconfigurations, including divestitures and acquisitions. As a BToF baseline, we expect firms to divest more (and, conversely, acquire less) in response to performance shortfalls (Kuusela et al., 2017).

Divestitures represent a strategic tool for corporate renewal (Vidal, 2021) and organizational change (Moliterno and Wiersema, 2007), wherein firms free up resources from underperforming peripheral businesses and reallocate them to core businesses for productive usage that can ensure performance growth (Vidal and Mitchell, 2018). Such reconfiguration approach aims to improve internal efficiency (Bergh and Lim, 2008), as it “extend[s] positive life cycles by eliminating operations that are no longer attractive within the firm because they do not offer high-priority trajectories for growth” (Vidal and Mitchell, 2015: 1104). While divestitures eliminate operations from their books, these are not actually eliminated but transferred to a new owner.

Divestitures driven by privatization do not necessarily lead to employment losses. Often, they result in increased employment (and enhanced productivity) in the divested entities (Todo, 2016). This positive outcome largely stems not only from gains to specialization but also from the organizational revitalization that accompanies privatization (Estrin et al., 2009). Newly privatized firms adopt competitive business practices (Zahra et al., 2000). Consequently, privatization-driven divestitures can maintain or even boost employment levels, rather than diminishing them.

Contrary to conventional expectations, state firms often divest as frequently as private firms, sometimes influenced by government privatization initiatives (Liao et al., 2014). Our empirical data, as highlighted later, suggest no statistically significant disparity in baseline divestiture rates between state and private firms, highlighting this trend.

By contrast, acquisitions are inherently more uncertain, generating superior as well as inferior returns (Haleblian et al., 2009). While the purpose and usefulness of divestitures do not vary with ownership, uncertain acquisitions sit uncomfortably with state firms’ stability mandate. Thus, divestitures are a more suitable resource-configuration pathway for testing our hypotheses. We, therefore, check for differences over time in divestitures among private and state firms.

We measure divestitures as the total number of divestitures announced each year. 8 Firm-years without divestiture receive a value of zero (Kuusela et al., 2017). Because firms can make multiple divestitures a year, each impacting ongoing organizational activities, a count measure, rather than a dummy measure, best captures variation in the degree of organizational change as conceptualized in the BToF (Vidal and Mitchell, 2015). A count measure is also more robust than an alternative based on transaction values, because the exact value of each transaction is not always available; We test for robustness to these design choices.

We include all deals CSMAR classifies as divestitures irrespective of deal value, so as to preserve variation in our dependent variable. In the robustness check section, we restrict our analysis to deals with transaction values of $1 million (roughly ¥7 million) or more, a threshold level commonly employed in resource-reconfiguration research (e.g. Shi et al., 2017). Our sample firms often made between zero and five divestitures a year over the observation window. Zero-divestiture years constitute 66% of firm-year observations.

Independent variables

Performance feedback

Our measure of firm performance is return on assets (ROA), which is a widely employed metric (e.g. Bromiley and Harris, 2014), thanks to its comparability across industries and across firms operating on different scales (Haveman et al., 2017). Chinese state firms use ROA as a key metric for annual performance appraisals (Cao et al., 2019), so do their private peers (Zhang and Greve, 2019). In addition, employing ROA rather than ROE (i.e. return on equity) is more appropriate in our setting as it limits measurement errors. In contrast to Western countries, China does not require firms to disclose the proportion of untradable shares, a split-share structure that makes computing average returns to equity ambiguous (Liao et al., 2014). In China, accounting for assets is more accurate and less ambiguous than accounting for equity (Haveman et al., 2017; Peng and Luo, 2000). We, therefore, focus on ROA.

To approximate firms’ performance feedback over time, we use the canonical measure for historical aspirations: a weighted average of previous historical aspirations and the most recent performance of the focal firm (Joseph et al., 2016). Specifically:

To approximate performance feedback through social comparisons, we again use an established measure: the average performance of all non-focal firms in the same CSRC (China Securities Regulatory Commission) 3-digit industry category in a given year (Bromiley and Harris, 2014). Specifically,

We compute feedback as performance minus historical aspiration, and performance minus social aspiration, respectively. We then split each feedback variable at zero to permit different slopes on either side (for a discussion, see Bromiley and Harris, 2014). We reverse-code the below-aspiration variables so that a higher value indicates a more negative gap between the firm’s performance and its aspirations (Joseph et al., 2016). The split variables are performance below historical aspirations, performance below social aspirations, performance above historical aspirations, and performance above social aspirations. Performance below historical aspirations and performance below social aspirations are the independent variables of interest, while performance above historical aspirations and performance above social aspirations serve as control variables.

State firm

Prior research employs alternative measures of ownership: ownership shares and controlling shareholder identity (Boyd and Solarino, 2016). An ownership-share measure is less reliable in our setting. China requires state ownership reporting for tradable shares only, not for non-tradable shares (see Delios et al., 2006; Shen et al., 2016). Reporting of the controlling shareholder’s identity, by contrast, is more reliable. Controlling shareholders are the dominant shareholders that own the highest number of shares to vote. Controlling shareholders can thus dominate voting and set logics of appropriateness for firm decision-making (Jia et al., 2018). When controlling shareholders do not have the majority shares (i.e. over 50%), firms typically follow Chinese Corporate Law to include the Acting in Concert clause in their corporate statutes, so as to ensure the unity of command when ownership is dispersed across major shareholders. In this case, non-controlling shareholders, even if they collectively own more shares than the controlling shareholder, cannot block controlling shareholder motions (Bertrand et al., 2002). Therefore, identifying the controlling shareholder better denotes state influence (Xu et al., 2014) than the share of state ownership. Privately controlled firms with a share owned by the state are not regulated by the SASAC and thus more likely prioritize financial over societal returns (Luo et al., 2017).

Specifically, our state-firm variable takes the value of 1, when CSMAR reports the controlling shareholder as a government entity or another firm controlled by a government entity (e.g. Liang et al., 2015; Meyer et al., 2014). Our variable takes the value of zero (a private firm) otherwise. The disclosure of controlling shareholder information in annual reports is mandated by the Law of the People’s Republic of China on Securities. Of our 2459 sample firms, 364 see a change of controlling shareholder identity during our observation window, either from state control to private control (229 firms) or vice versa (135 firms). We analyze these rare transfers of ownership for corroborating indications of the proposed mechanisms.

Control variables

Our estimation is within-firm, across-years, which controls for unobserved firm heterogeneity. We then additionally include time-varying firm and industry observables. Evidence suggests that divestiture decisions are influenced by CEO characteristics (Shimizu and Hitt, 2005). We, therefore, control for CEO turnover (binary 1/0 variable, with 1 representing that the CEO identified in CSMAR changed), CEO age (in years), and CEO duality (binary 1/0 variable, with 1 denoting the same individual served as CEO and board chair). To account for board characteristics influencing responsiveness to performance feedback (Lim and McCann, 2014), we control for board size (number of board members), board independence (ratio of independent directors), and female board (percentage of women directors).

To permit cleaner inference, we further control for a series of variables that are indicative of a firm’s ability to change in response to performance shortfalls (Audia and Greve, 2006; Chen and Miller, 2007; Kuusela et al., 2017), including firm age (natural-log transformation of years since incorporation), firm size (natural-log transformation of total assets), working capital (working capital per sale), and three different forms of slack—absorbed slack (the ratio of selling, general, and administrative expenses to sales), unabsorbed slack (the ratio of current assets to current liabilities), and potential slack (the ratio of equity to debt). Altman’s Z additionally captures a firm’s distance to bankruptcy, a survival reference point that may impact propensity to change (Shimizu, 2007). Following established practice (Altman, 1968), Altman’s Z is computed as (0.012 × working capital per asset) + (0.014 × retained earnings per asset) + (0.033 × income before interest expense and taxes per asset) + (0.006 × market value of equity per liability) + (0.999 × sales per asset). A greater Altman’s Z denotes a lower threat of bankruptcy. Overall, these control variables help rule out alternative explanations that feedback–divestiture link might be confounded by a firm’s ability to reconfigure its resource base.

To further account for state influence on divestitures, we control for political connection (proportion of politically connected board members) 9 and government subsidy (a percentage of total assets). We also calculate the abnormal tax rate, proxying the degree to which firms pay heed to political concerns. State-firm CEOs focus on political promotion and thus tend to pay higher taxes (Bradshaw et al., 2019), and even private-firm CEOs may look for political appointments (Li and Liang, 2015) and thus pay higher taxes. Abnormal tax is the residual in a model of tax rate as a function of state control, firm age, firm size, firm performance (ROA), and industry competition.

To additionally account for firm-specific characteristics that may constrain divestiture decisions, we control for divestiture experience (Shimizu, 2007) and past divestiture performance (Bergh and Lim, 2008). Divestiture experience is measured as the total number of divestitures done in the previous 3 years by a firm. Past divestiture performance is measured as the cumulative abnormal return (CAR), where we compute the CAR from one trading day before to one trading day after the announcement of a divestiture (–1, +1). Our results are robust to alternative event windows (i.e. (–3, +3), (–5, +5)).

At the industry level, we control for industry-level divestiture frequency, measured as the average number of divestitures implemented by CSRC’s 3-digit industry peers in a given year, so as to control for impact of heterogeneity in divestiture frequency across industries. We also control for the intensity of industry competition through a Herfindahl–Hirschman index of concentration, using sales-based market share, of all the publicly traded firms in each CSRC 3-digit industry in a year (Haveman et al., 2017; Zhou et al., 2017). 10 We reverse-code the index so that higher values mean fiercer rivalry. Finally, we include year dummies to address contemporaneous correlation (Certo and Semadeni, 2006). To minimize the influence of extreme observations, all continuous variables are winsorized at the 1% level in both tails (Dixon, 1960).

Empirical specification

We use a firm fixed-effects Poisson regression model 11 to test our hypotheses, lagging input variables by 1 year. We employ Stata 18 to conduct our analysis with the specific code being “xtpoisson, fe” (StataCorp, 2015). Since the dependent variable, the number of divestitures in a given year, is a count variable with non-negative integer values only, the linear regression assumption of homoscedastic, normally distributed error terms would be violated. Poisson regressions can alleviate this concern (Hausman et al., 1984).

Fixed effects account for such unobserved firm-level heterogeneity as in risk preferences and growth orientation. Firms with conservative management, for example, may both experience a smaller performance feedback gap and make more divestitures. Due to the risk of such omitted-variable biases, fixed-effects models are considered best practice for assessing the impact of feedback on change (e.g. Eggers and Suh, 2019; Gaba and Joseph, 2013).

We chose a split-sample approach (rather than including interaction terms) to examine the between-firm effect of state control. Using interactions may generate inappropriate inferences for nonlinear models (Shaver, 2007), since the coefficients of the interaction terms provided by nonlinear models are not indicative of the magnitude of the effect (Hoetker, 2007). Furthermore, the split-sample approach allows for the whole estimation model (i.e. all coefficients) to have different parameters, accounting for distinct-group settings (Chow, 1960). It means that the effect of government subsidies, for example, can be reasonably assumed to differ between state and private firms. The interaction item approach, by contrast, assumes all variables that are not interacted have the same effect across groups (government subsidies, for example, would be assumed to not structurally differ between state and private firms). The split-sample approach channels Bruton et al. (2015: 93; parentheses in original): “it cannot be assumed that SOEs [state-owned enterprises] will behave (or should be managed) in the same manner as private firms.”

We use Chow tests to assess differences in the variable coefficients of state-firm and private-firm models (Chow, 1960). Using split-sample approach to examine between-firm variations follows prior BToF studies of contingencies to feedback responsiveness (Shipilov et al., 2011; Tarakci et al., 2018; for example, Eggers and Kaul, 2018; Makarevich, 2018).

Results

Descriptive statistics

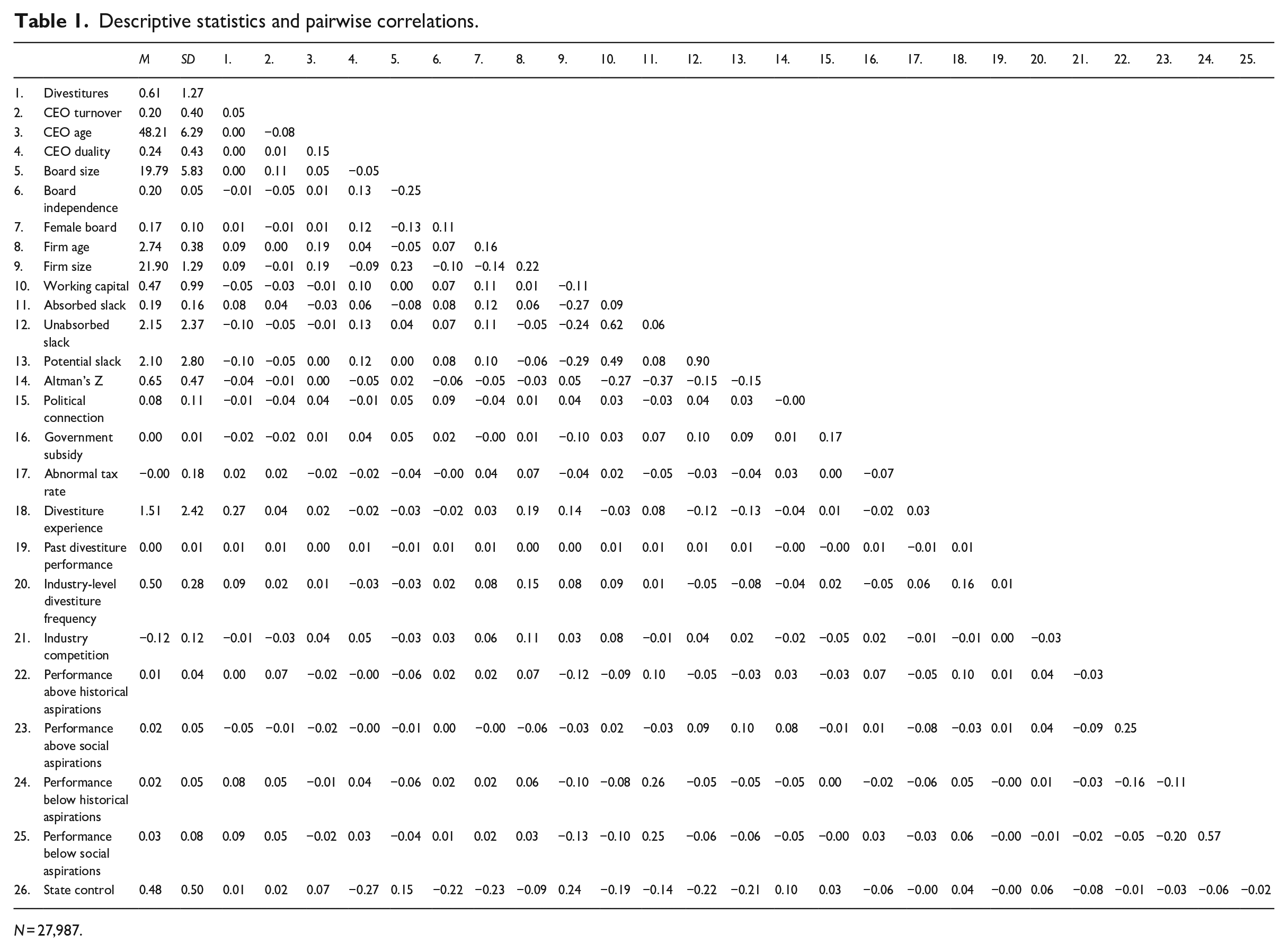

Descriptive statistics and pairwise correlations for all variables are shown in Table 1. State and private firms are similarly represented in our sample, with 48% and 52%, respectively. The yearly divestiture rate (i.e. the proportion of firms with divestitures in a given year) is 0.3 percentage point higher (p < 0.001) among private firms than that among state firms, suggestive of a descriptively lower overall rate of change at state firms. The independent and dependent variables exhibit considerable variance, and the correlation matrix shows low correlations among them. The variance inflation factors (VIFs) for all coefficients in our models indicate little bias from multicollinearity, with the average and maximum values far below the recommended cut-off value of 10 (Kutner et al., 2004).

Descriptive statistics and pairwise correlations.

N = 27,987.

Regressions

Divestitures in response to performance shortfalls relative to historical aspirations

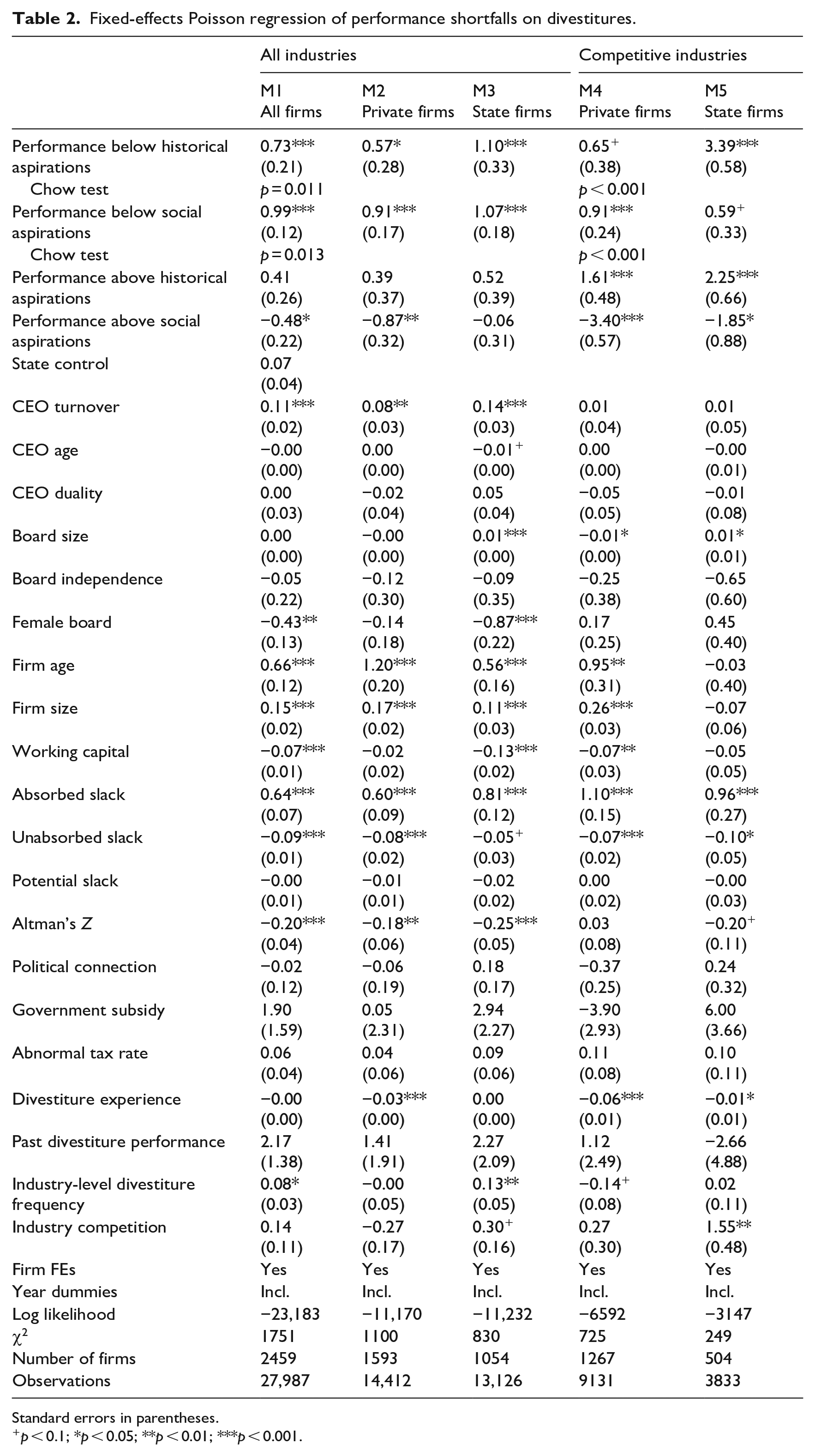

The direct effect of performance shortfalls relative to historical aspirations on divestitures (Model 1, Table 2) are positive (β = 0.73, p < 0.001), which is consistent with prior behavioral studies (e.g. Kuusela et al., 2017). To inspect feedback-response heterogeneity, we separate private firms from state firms (Models 2 and 3, respectively). Both types of firms are sensitive to performance shortfalls relative to historical aspirations. The coefficient in the state-firm sample is larger, suggesting greater responsiveness (Chow test: p = 0.011). This supports H1. To assess economic significance, we follow prior research (e.g. Kuusela et al., 2017) and convert the regression coefficients into incidence rate ratio (IRR). The corresponding IRRs in private-firm sample (Model 2) and state-firm sample (Model 3) equal 1.77 and 3.01, respectively. State-firms’ responsiveness to that feedback consequently is 70% (3.01/1.77 − 1 = 0.70) higher than private-firms’ responsiveness.

Fixed-effects Poisson regression of performance shortfalls on divestitures.

Standard errors in parentheses.

p < 0.1; *p < 0.05; **p < 0.01; ***p < 0.001.

Divestitures in response to performance shortfalls relative to industry peers

The direct effect of performance shortfalls relative to industry peers on divestitures (Model 1) is also positive (β = 0.99, p < 0.001). This summary effect again hides heterogeneity: unexpectedly, state firms are more responsive to this feedback (β = 1.07, p < 0.001, Model 3) than their private peers (β = 0.91, p < 0.001). A Chow test (p = 0.013) supports the converse of Hypothesis 2.

We additionally run our analysis on a sample restricted to industries in which private firms make up more than 38% of the market share, the median. Here, state firms appear less responsive to performance shortfalls relative to industry benchmarks (β = 0.59, p = 0.076, Model 5) than their private peers (β = 0.91, p < 0.001, Model 4). A Chow test (p < 0.001) confirms such a difference in responsiveness. The corresponding IRRs in private-firm and state-firm samples are 2.48 and 1.80, respectively. State-firms’ responsiveness to feedback against industry peers consequently is 38% (2.48/1.80 − 1 = 0.38) lower than private-firms’ responsiveness. Thus, Hypothesis 2 holds in industries with private competitors but not in industries without. This finding already hints at the plausibility of Hypothesis 3, which we examine next.

State firms’ divestitures in response to performance shortfalls relative to state peers

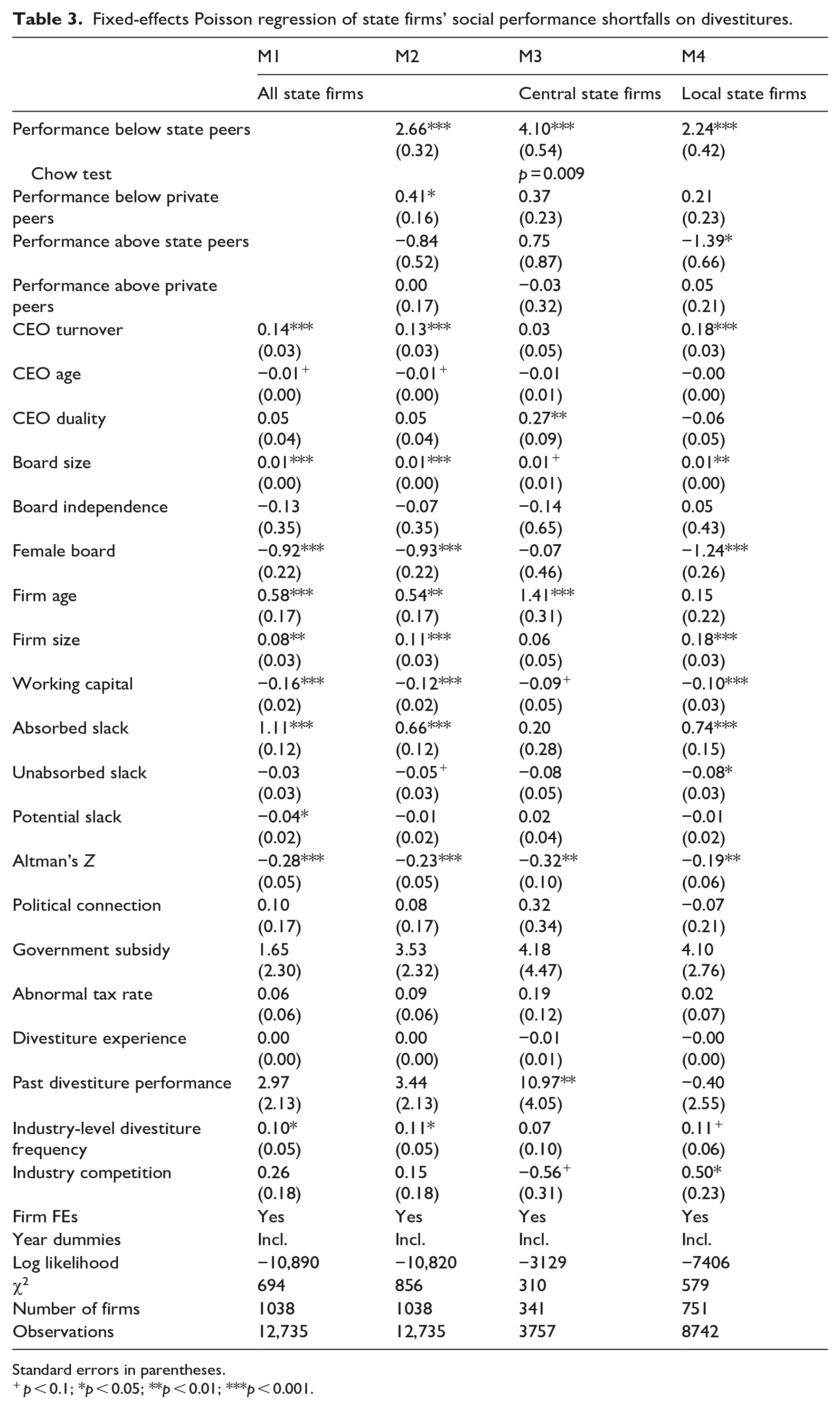

The previous analysis already suggests that state firms attend to social referents when these are not private firms. This observation is consistent with Hypothesis 3, in which we argue state firms care less about private peers than state peers. To examine Hypothesis 3 more directly, we limit our analysis to the subsample of state firms only. For each state firm, we create two different variables of social performance shortfalls: (1) performance shortfalls relative to state peers in the same industry (excluding the focal firm), and (2) performance shortfalls relative to private peers in the same industry. The regression results in Table 3 suggest that state firms strongly respond to other state firms’ performance (Model 2: β = 2.66, p < 0.001) but only mildly to private peers’ performance (Model 2: β = 0.41, p = 0.010). State firms thus do not completely ignore social referents altogether. They instead focus on peers with organizational identities similar to their own. State firms’ selective attention to fewer industry participants, however, means that many competitive signals go unheeded, explaining their lower propensity to respond to gaps between generic industry benchmarks and their own performance in competitive environments. This provides support for Hypothesis 3.

Fixed-effects Poisson regression of state firms’ social performance shortfalls on divestitures.

Standard errors in parentheses.

p < 0.1; *p < 0.05; **p < 0.01; ***p < 0.001.

Corroborating evidence

Ownership and responsiveness changes

A total of 229 state firms were privatized during our sampling period. We leverage this longitudinal variation in ownership to explore how it affects sensitivity to performance shortfalls. To do so, we limit our sample to firms that started as state firms, regardless of whether they are privatized or not by the end of our sampling period. We then create a treatment variable, privatization, a dummy variable that equals one if the firm has been privatized by year t. In addition, we interact privatization with performance below historical aspirations and performance below social aspirations, respectively, and see how firm responsiveness to performance shortfalls varies before and after the ownership change.

The results in Online Appendix 1 suggest that, once privatized, firms become less responsive to historical performance shortfalls than they do when they are under state control (Model 2: β = −0.84, p = 0.080), which supports our assumption that state firms’ greater responsiveness stems from the state’s stability mandate. Privatization does not significantly impact state firms’ responsiveness to social performance shortfalls (Model 4: p = 0.261). These findings further support our theoretical interpretation of the results.

The magnitude of shortfalls and corresponding changes

Our theory centers on firms’ sensitivity of responsiveness to performance shortfalls. We have thus been agnostic to the magnitudes of performance shortfalls and divestitures at state and private firms. We here explore nuances in magnitudes, and Online Appendix 2 summarizes the key statistics for this post hoc analysis. The magnitude of historical performance shortfalls at private firms (0.021) is 31% larger than that at state firms (0.016), underlining state firms’ stability focus. The magnitude of social performance shortfalls at private and state firms is largely similar (0.030 vs. 0.032), given they compete in the same markets and thus receive similar feedback about their industry peers.

The IRR for state firms in response to performance below historical aspirations is 3.01, which means that state firms increase their divestitures by 201% (3.01 − 1 = 2.01) more than they normally do when they see performance drops below historical aspirations. The magnitude of performance shortfalls at state firms is about 0.016. Taking these two parameters together, a typical performance shortfall below historical aspirations will trigger state firms to increase divestitures by about 0.032 ((3.01 − 1) × 0.016 = 0.032). Analogously, divestitures triggered by a typical performance shortfall at private firms equal 0.016. Thus, the magnitude of changes at state firms is about 2 times that at private firms in response to a typical shortfall in performance trajectories.

The magnitude of changes at state firms (0.026) is about 59% of that at private firms (0.044) in response to a typical shortfall in performance comparisons. Thus, state firms change more in response to historical performance shortfalls, but change less in response to social performance shortfalls.

State-firm types

Prior research highlights distinctions among Chinese state firms, with some controlled by central and local governments, respectively (Luo et al., 2017). Our Hypothesis 1 would suggest that both central and local state firms exhibit greater responsiveness to historical performance shortfalls than their private peers, because both have a stability frame when assessing the performance relative to historical aspirations. We find empirical support for this (see Models 1–3, Online Appendix 3). In addition, since central state firms have a more pivotal role than local state firms in fulfilling governmental political mandates, we expect a larger effect among central state firms than among local state firms, and we find supportive evidence (Chow test: p = 0.064).

Regarding Hypothesis 2, in competitive environments, we would expect both central and local state firms to exhibit irresponsiveness to industry benchmarks, because their focus on satiability mandates will crowd out their concerns over industry competition. We find empirical support for this (see Models 4–6, Online Appendix 3). Since neither central nor local state firms exhibit responsiveness to social performance shortfalls, we do not further compare their difference in responsiveness.

Regarding Hypothesis 3, we anticipated that both central and local state firms would benchmark against state counterparts rather than private-sector firms in addressing social performance deficiencies. Our empirical findings substantiate this expectation (see Models 3–4, Table 3). Moreover, central state firms, due to their pivotal role in fulfilling governmental political mandates and the prospect of political promotions, are likely to be more responsive to their state counterparts’ performance than local state firms. This enhanced responsiveness is empirically supported (Chow test: p = 0.009).

Alternative explanations

Political coercion

One may wonder whether direct political pressure explains state firms’ greater responsiveness to historical performance feedback. In Table 2, none of the relevant control variables (state control, political connection, government subsidy, abnormal tax rate) show a statistically significant and positive effect on divestitures. Subsidies do not explain the results either: re-running our models with historical feedback net of subsidies does not materially affect results (see Online Appendix 4). Overall, direct political coercion is unlikely to drive our findings.

Strategic alternatives

One may also wonder whether state firms have few options to respond to feedback, other than to divest. To alleviate this concern, we control for common alternative responses to performance shortfalls (Eggers and Kaul, 2018; Lu, 2018; Ref and Shapira, 2017), including diversification (a count of CSRC 3-digit industries in which the firm operates), innovation (a natural-log-transformed count of yearly patent applications), and internationalization (the percentage of sales achieved in foreign markets). Our results remain (see Online Appendix 5). This alleviates the concern that state firms’ greater responsiveness to historical performance shortfalls is for lack of strategic alternatives.

Baseline probabilities

Our state firms make slightly fewer divestitures overall than private firms. To account for a heterogeneous baseline, we first predict a firm’s divestiture likelihood through a probit model with one exclusion restriction: detections of corporate misconduct limit firms’ ability to divest. We then derive the inverse Mills ratio from the probit results and include it as a control in all models. Our results remain (see Online Appendix 6). A heterogeneous baseline thus does not provide a credible alternative explanation.

Empirical robustness

Aspiration adjustment

We examine to which extent our results are contingent on the alpha parameter with which historical aspirations update. We alternatively analyze our data with alpha values from 0.1 to 0.9, respectively. Findings remain qualitatively consistent (Online Appendix 7 shows results for α = 0.3).

Historical aspiration

To inspect whether our results are artifacts of operationalization choices, we consider alternative measures, including Vidal and Mitchell (2015). Results remain robust to operationalizing historical aspirations as an average of three preceding years (Online Appendix 8).

Divestiture value

We use all reported divestiture deals for analysis, including many minor transactions. For robustness checks, we follow prior research (e.g. Shi et al., 2017) to set an inclusion threshold of $1 million (roughly ¥7 million). Thresholds make it more likely that divestitures represent decisions of strategic importance. Our data include 11,124 such divestitures, corresponding to 7219 firm-year observations. Findings remain robust (Online Appendix 9).

The dispersion of dependent variable

While the fixed-effects Poisson regression model has the advantage of imposing true fixed effects (Allison and Waterman, 2002), it might suffer from overdispersion in the count of divestitures. For further robustness checks, we re-run our analysis using fixed-effects Poisson quasi-maximum likelihood regressions. This estimation method, proposed by Wooldridge (1999) and coded for Stata by Simcoe (2008), can deal with overdispersion while estimating the true fixed-effects models (Chatterji and Fabrizio, 2012). Our results remain qualitatively robust (Online Appendix 10).

Foreign ownership

In our sample, a few firms are controlled by foreign companies, accounting for 6% of total observations. As a robustness check, we exclude those observations, and re-specify our analysis. Results are consistent with our prior analysis (Online Appendix 11).

Lag structure

Our time lag between independent variables and dependent variable is 1 year. We repeat our analyses with a 2-year lag. Results remain stable for state firms. Private firms become increasingly irresponsive to older social performance shortfalls (see Online Appendix 12).

Generalizability and extensions

We restricted the analysis to Chinese listed firms, ensuring granularity and internal validity. Governments marshall state firms in the pursuit of societal stability elsewhere, too, including in Brazil and India (Hu et al., 2019; Inoue, 2020). Therefore, our theoretical framework likely generalizes beyond China and can facilitate research in further emerging economies.

We currently assume that state and private firms establish their historical aspirations similarly, using this as a baseline to compare their responses to performance deviations. However, future research may find it fruitful to explore whether there are inherent differences in the aspiration levels set by state versus private firms. Such studies could help clarify how differences in aspirations may result in different performance trajectories, and therefore, structurally different gaps in attainment of the benchmarks used in our empirical design.

Our research cannot offer ultimate causal identification, a typical challenge in performance-feedback research. Although we have addressed several alternative explanations, other potential endogeneity may remain unexplored. Future research would benefit from using quasi-experimental approaches, if available, to more definitively establish the mechanisms we lay out.

Discussion

Our research helps address a BToF gap in explaining heterogeneity in responsiveness to feedback (Greve and Gaba, 2017). We extend knowledge about the role of state ownership in feedback responsiveness. We argue that state-firm and private-firm responsiveness depart because different decision frames guide their feedback sensemaking. Scholars have called for the employment of a multiple-goal perspective in conceptualizing the feedback-response relationship (Audia and Greve, 2021), and our study of ownership-based responsiveness answers this call.

Contrary to popular conceptions of cosseted and inert leviathans, we find that state firms are more responsive to feedback about their own historical performance than private firms are. Overall, however, state firms conform to expectations of inertia, changing less than their private peers in response to competitive comparisons. Revealing such heterogeneity in responses to feedback both nuances the behavioral theory of the firm and enriches the state-firm literature.

Contributions to the behavioral theory of the firm

Our study contributes to an emerging body of BToF work devoted to understanding the heterogeneity in feedback responsiveness (Greve and Gaba, 2017). Scholars have investigated the organizational contingencies as organizational leadership, scale, structure, experience, and networks might provide (e.g. Desai, 2008; Gaba and Joseph, 2013; Hu et al., 2022; Rhee et al., 2019; Smulowitz et al., 2020); we add richness to this growing literature by examining how organizational contingencies might arise as a result of divergent owner interests. We showcase how two qualitatively different types of firms, operating with different frames, react to particular types of feedback.

By looking into the ownership-led contingency in feedback responsiveness, such as value proposition circumscribed by owners, our work underscores the importance of feedback relevance across firms with different decision frames. For example, future research may be able to document similar patterns of feedback responsiveness when comparing unionized and non-unionized firms. The integration of decision frames into feedback-responsiveness models provides a theoretical leverage to explicate, despite in the same institutional environment, why some firms are responsive to performance feedback (e.g. Chen, 2008) while others do not (e.g. Blagoeva et al., 2020).

Our finding of state firms’ heightened sensitivity to small fluctuations in historical feedback extends a small but growing, body of behavioral literature devoted to feedback interpretation (e.g. Gaba and Joseph, 2013; Joseph et al., 2016; Kacperczyk et al., 2015; Vissa et al., 2010). Such work has focused on how responsiveness varies with the situated interpretation of performance feedback—decision makers either misinterpret performance signals due to subconscious biases (e.g. Fang et al., 2014; Jordan and Audia, 2012) or disregard feedback due to personal interests that conflict with the firms’ (e.g. Gaba and Joseph, 2013; Joseph et al., 2016). Our findings, by contrast, suggest decision makers prioritize attention to particular types of feedback in a way that appears in the interest of the firm.

Beyond selective attention to feedback types and sensitivity to their magnitude, our findings further increase understanding of the duality of historical and social aspirations. While many studies assume feedback types’ equivalence in triggering behavioral responses (e.g. Baum et al., 2005; Greve, 1998), a few studies have shown that historical and social aspirations can drive firm behavior in distinctive directions (e.g. Kacperczyk et al., 2015; Kim et al., 2015). Our research further extends this front, suggesting that ownership type determines firm responses to historical and social feedback.

Last but not least, our study highlights that state firms primarily benchmark against similar state-owned entities rather than the broader industry peers. This nuances the BToF research practice of using industry-wide benchmarks. Our research emphasizes the impact of ownership type on the formation of social reference points, extending beyond the realms explored in existing studies that focus on structural (Hu et al., 2017), operational (Moliterno et al., 2014), and size similarities (Kuusela et al., 2017). This finding adds depth to the BToF literature by illustrating how ownership identity critically influences benchmarking behavior, opening up new avenues for future research to explore the intricate dynamics between ownership types, social benchmarking, and firm adaptation.

Contributions to the state-firm literature

We contribute behavioral insights into the phenomenon of state-firm inertia. Our proposed feedback mechanisms operate separately from known mechanisms of agency costs (Zhou et al., 2017), conflicting logics (Greve and Zhang, 2017), and bureaucratic hierarchy (Lioukas et al., 1993), all of which primarily explain how state control results in state-firm inertia. In doing so, we nuance the inertial view by highlighting how state firms actually change more under certain circumstances. As state firms aim for lower performance fluctuations than their peers (Megginson and Netter, 2001), smaller performance-aspiration gaps trigger changes more readily at state firms than private firms. The counterintuitive finding may explain anomalies found in the formal-structure stream (e.g. Hsu et al., 2023; Mariotti and Marzano, 2019) that, despite structural inertia, state firms sometimes outdo their private peers. Behavioral research thus stands to aid the quest to understand the advantages and disadvantages of state-directing enterprises, extending the agenda of state-firm scholarship beyond the “structure-conduct-performance” paradigm in studies of industrial organization (Bain, 1959). Performance expectations determine state-firm behavior.

Relatedly, recent research started to reconceptualize state firms as hybrid organizations that embrace both state and market logics (Bruton et al., 2015; Chen et al., 2019; Okhmatovskiy et al., 2021). Despite the great strides made in this area, extant research tends to focus on the tensions in these hybrid structures, particularly how state logic negatively affects competitiveness in the market (e.g. Genin et al., 2021; Zhou et al., 2017). Our work takes a different, complementary, route to show that hybrid state and market logics can make state firms more agile than their private peers, evidenced by their greater reconfiguration responsiveness to historical feedback. We enrich the literature by highlighting the benefits of hybridity, complementing the literature’s prevailing focus on vulnerability.

Moreover, our research extends our understanding of decision frames in state-controlled firms. While prevailing studies suggest that state firms disregard market competition, our findings indicate a different approach. Specifically, we observe that state firms are indeed concerned about their competitive performance, but they focus this concern on their state counterparts, often overlooking similar metrics from private peers. This selective processing of peer information offers valuable insights into how state firms navigate their environments, shaped by the combined influences of state and market logics.

Conclusion

We test the role of ownership in organizational responses to performance shortfalls. State firms disregard competitive benchmarks but are sensitive to fluctuations in their own performance. State-firm inertia is not all it seems—state firms actually adapt more readily when they see performance deviate from historical aspirations. The heterogeneity in feedback responsiveness we document helps nuance the behavioral theory of the firm and informs our understanding of the state-firm phenomenon.

Supplemental Material

sj-docx-1-soq-10.1177_14761270241261141 – Supplemental material for A behavioral theory of Leviathan Inc: State firms’ responses to performance shortfalls

Supplemental material, sj-docx-1-soq-10.1177_14761270241261141 for A behavioral theory of Leviathan Inc: State firms’ responses to performance shortfalls by Zhiyan Wu and Ronald Klingebiel in Strategic Organization

Footnotes

Acknowledgements

We thank the editor Glen Dowell and three anonymous reviewers for their developmental and constructive feedback that improved this paper. We also appreciate the helpful comments from Radina Blagoeva, Xena Welch Guerra, Songcui Hu, Korcan Kavusan, Helge Klapper, Tomi Laamanen, Taco Reus, and seminar participants at Erasmus University, Frankfurt School of Finance & Management, and University of Southern Denmark.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

Notes

Author biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.