Abstract

The widespread diffusion of digital technologies forces incumbent firms to drive their digital transformation. Digital transformation not only involves a change in strategy but also requires new institutional logics for firms helping to operate in digital business environments. Firms increasingly hire outsider CEOs to cope with this development, but the necessary institutional change questions whether outsider CEOs can indeed realize digital transformation. We draw on the institutional entrepreneurship perspective to make sense of the role of outsider CEOs in digital transformation. We theorize that digital transformation awareness stemming from prior experience with digital transformation enables outsider CEOs to act as institutional entrepreneurs and realize digital transformation. We further argue that outsider CEOs with digital transformation awareness particularly benefit firms facing abrupt rather than accumulative digital transformations. To test our hypotheses, we introduce a novel, machine-learning-based digital transformation measure. Panel data regressions provide support for our predictions. Our findings contribute to a more nuanced understanding of the role of outsider CEOs as change agents.

Introduction

Changing business environments due to the emergence and widespread use of digital technologies present both an opportunity for incumbent firms to thrive in the digital age and the risk of losing market share to new competitors, therefore forcing incumbent firms to react (Bharadwaj et al., 2013; Hess et al., 2016; Verhoef et al., 2021). Given the fundamental disruption caused in many industries (Lucas and Goh, 2009) and the ever-changing character of digital technologies (Yoo et al., 2012), firms need to organize for constant adaptation. Digital transformation (DT) thus goes further than a mere strategic reorientation (see also Adner et al., 2019) and can be defined as “a change in how a firm employs digital technologies, to develop a new digital business model that helps to create and appropriate more value for the firm” (Verhoef et al., 2021: 889). This transformation entails profound challenges, especially for incumbent firms from the pre-digital age. They need to fundamentally question their current beliefs about core assets and business models to break the status quo and initiate change (Bharadwaj et al., 2013; Hess et al., 2016; Vial, 2019). Furthermore, firms need to implement their digital initiatives within their prevailing business models to arrive at a new organizational mode going forward (Chanias et al., 2019; Correani et al., 2020). While DT is on the agenda of almost every firm (Björkdahl, 2020; Chanias et al., 2019), the required change, which challenges the established institutions of incumbent firms (Henfridsson and Yoo, 2014; Hinings et al., 2018), makes its realization, especially from inside the firm, difficult.

Firms increasingly turn to hiring outsider chief executive officers (CEOs) (Nickisch, 2016), as the “need to change their business model or do something they’ve never done before (. . .) is driving the desire to bring in outsiders” (Nickisch, 2016: 2). While this development aligns with prior studies emphasizing that outsider CEOs are more likely to initiate strategic change (Nakauchi and Wiersema, 2015; Zhang and Rajagopalan, 2010), it neglects how DT renders not only a perspective on firm strategy but also on institutional change relevant (Hinings et al., 2018; Menz et al., 2021). 1 Especially in the context of DT, CEOs need to account for the underlying shift in institutional logics 2 that incumbent firms experience in this process (Tumbas et al., 2018), such as changing belief systems with regard to existing business models (Bohnsack et al., 2021) and altering prevailing processes and routines for the implementation of digital technologies (Dremel et al., 2017). Therefore, outsider CEOs driving DT will have to act as institutional change agents, breaking with established institutional logics and introducing new ones suited for operating in digital business environments (Henfridsson and Yoo, 2014; Tumbas et al., 2018). Prior literature, however, has highlighted that outsider CEOs may, in particular, struggle to implement such institutional change (Berns and Klarner, 2017). Thus, it remains open as to whether and when outsider CEOs help drive DT in incumbent firms.

To answer this question, we apply institutional entrepreneurship (Battilana et al., 2009) as a theoretical lens to outsider CEOs, emphasizing their role in the institutional change of incumbent firms for DT (Hinings et al., 2018). We draw on recent studies applying the institutional entrepreneurship perspective to the introduction of digital technologies in firms (Henfridsson and Yoo, 2014) and especially the role of executives in that process (Tumbas et al., 2018). The institutional entrepreneurship perspective in the context of DT allows us to extend previous work on outsider CEOs and firm outcomes (Georgakakis and Ruigrok, 2017; Karaevli and Zajac, 2013) with a better understanding of their role in institutional change. In this regard, we also answer the call for more research on the role of outsider CEOs in the context of DT (Singh et al., 2020; Volberda et al., 2021).

Rooted in the theory of institutional entrepreneurship (Battilana et al., 2009; Maguire et al., 2004), we argue that outsider CEOs can possess both the motivation and the ability to mobilize sufficient resources to carry out institutional change. Scholars of institutional entrepreneurship further highlight that institutional change agents need to be able to identify opportunities, which requires an awareness of the specific topic of the change (Boxenbaum and Battilana, 2005; Kraatz and Moore, 2002). Therefore, we propose that the DT awareness of outsider CEOs, stemming from prior work experience in the context of DT, constitutes a critical prerequisite enabling them to act as institutional entrepreneurs. Outsider CEOs with DT awareness may identify opportunities for DT, as well as the institutional barriers inhibiting its realization and drive change toward new institutional logics for DT. On the other hand, the mere outsiderness of CEOs without such DT awareness may not be sufficient for identifying opportunities to drive DT as well as barriers inhibiting its initiation.

We further argue that the challenges firms face when carrying out DT differ considerably depending on the prevailing business model, rendering the influence of outsider CEOs with DT awareness more or less strong. Some firms face a rather abrupt DT if their business model can be digitized nearly entirely, resulting in a clearer pathway toward DT. In these firms, outsider CEOs with DT awareness can formulate a precise vision with a clear goal state for the firm, allowing for the easier mobilization of allies (Battilana et al., 2009) for institutional change. Other firms face a rather more accumulative DT if their business model is based on physical assets and products, requiring a fusion of digital initiatives with their core business, which will migrate toward a hybrid logic entailing both physical products and the integration of digital technologies and business models (Svahn et al., 2017). For these firms, the future state is rather ambiguous, thus rendering the creation of a precise vision and the mobilization of allies more difficult, as well as increasing the likelihood of upcoming internal resistance toward institutional change. In this scenario, the ability of an outsider CEO with DT awareness to act as an institutional entrepreneur will likely be inhibited.

We test our predictions with a novel quantitative DT measure by employing panel data regressions on a large sample of S&P 1500 firms from non-digital industries from 2006 to 2020, 3 consisting of 11,238 firm-year observations. Specifically, we leverage each firm’s annual requirement to provide a comprehensive account of its business’s present status and recent advancements in the business section of its 10 K reports and introduce a novel, machine-learning (ML)-based measure to assess the firm’s DT. In line with our first hypothesis, we find a significant positive relationship between outsider CEOs with DT awareness and the DT of firms, and do not find any positive relation for outsider CEOs without DT awareness. We further find that, in line with our second hypothesis, the DT type moderates this relationship. The positive relationship between outsider CEOs with DT awareness and DT is substantially enhanced for firms facing a rather abrupt transformation and is much weaker for firms facing a rather accumulative transformation.

We contribute to the academic literature in three ways. First, we add to the literature on CEO origin and firm outcomes (Berns and Klarner, 2017; Schepker et al., 2017) with its prevailing focus on the insider–outsider distinction. We extend the literature’s focus to the origins of outsider CEOs by differentiating between outsider CEOs with and without DT awareness. We further answer the call for a better understanding of the role of outsider CEOs for DT (Singh et al., 2020; Volberda et al., 2021). Specifically, we introduce the lens of institutional entrepreneurship to outsider CEOs and develop a perspective on outsider CEOs in institutional change processes, such as DT, that go beyond strategic change (Adner et al., 2019). In this regard, we provide a nuanced perspective on the divergent ramifications of outsider CEOs by introducing awareness of a specific change as an enabling factor for outsider CEOs to act as institutional entrepreneurs and drive such change. Second, we contribute to the literature on strategic leadership and DT that emphasizes the novel roles of executives, such as chief digital officers (CDOs) (Tumbas et al., 2018), or groups of managers, such as the top management team (TMT) (Firk et al., 2022), or the middle management of firms (Van Doorn et al., 2023), in DT. As little is known about the specific role of the CEO as the strategic leader for DT, we highlight the role of CEOs’ backgrounds in the identification of opportunities and institutional barriers, as well as the creation of a transformative vision for institutional change. Third, we contribute to DT research (Hanelt et al., 2021; Menz et al., 2021; Volberda et al., 2021) by developing and validating a quantitative measure capturing firms’ realization of DT. In light of the valuable qualitative studies and novel research questions emerging for strategy research in the digital era (Adner et al., 2019; Volberda et al., 2021), our measure enables large-scale archival research to empirically test such research questions.

Theoretical background

CEO origin and strategic change

Given the prominent position CEOs take on within firms (Hambrick and Mason, 1984), a vast stream of academic research has emerged covering the influence of their characteristics on firm outcomes. A profound focus in this stream of research lies in the effect of CEO origin on strategic change (Karaevli and Zajac, 2013; Nakauchi and Wiersema, 2015; Zhang and Rajagopalan, 2010). Splitting CEOs into those who are hired from within the firm and those hired from outside the firm, both theoretical considerations and empirical analyses provide evidence of the positive influence of outsider CEOs on strategic change (Finkelstein et al., 2009; Schepker et al., 2017). Explanations for this effect are manifold, stating that outsider CEOs are not plagued by typical limitation factors observable with insider successors, such as a high commitment to the status quo (Hambrick et al., 1993), a deep entrenchment in social relationships within the firm (Finkelstein and Hambrick, 1990; Wiersema and Bantel, 1993), and narrow information sources and processing routines (Finkelstein et al., 2009; Tushman et al., 1985). Similarly, outsider CEOs may also bring new perspectives from other industries to their new firms, enlarging their cognitive perceptions (Prahalad and Bettis, 1986) and strategic choices (Gunz and Jalland, 1996; Sutcliffe and Huber, 1998).

Despite the apparent positive influence of outsider CEOs on the initiation of change, scholars have pointed out numerous factors that could significantly diminish the ability of outsider CEOs to carry out that change (Berns and Klarner, 2017). For instance, it has been argued that the lower level of firm- and industry-specific knowledge of outsider CEOs makes implementing changes more difficult, as knowledge about key resources within the industry might be missing (Kotter, 1982; Zhang and Rajagopalan, 2010). Furthermore, outsider CEOs have a smaller social network within the firm (Chung et al., 1987; Finkelstein et al., 2009), depriving them of knowledge about key actors in the organization and exacerbating the challenge of mitigating upcoming internal resistance to change (Virany et al., 1992). However, while a nuanced perspective on outsider CEOs seems necessary, the existing literature generally prescribes a rather positive impact of outsider CEOs on strategic change (Berns and Klarner, 2017; Schepker et al., 2017).

DT as more than a strategic change

In recent years, many firms have faced a more fundamental change, as most incumbent firms aim to drive their DT (Hanelt et al., 2021). Hiring outsider CEOs constitutes a logical response to the need to accelerate DT, and firms increasingly do so (Nickisch, 2016). However, compared to a mere strategic reorientation, the DT of incumbent firms entails a fundamental shift in institutional logics (Henfridsson and Yoo, 2014; Hinings et al., 2018). Firms may need to fundamentally question their existing business models and thoroughly change established processes and routines (Chanias et al., 2019; Hanelt et al., 2021). This makes it difficult to transfer the extant knowledge about CEO origin and its influence on strategic change to the context of DT, especially since prior studies’ theorizing did not account for the peculiarities of DT that reconfigure the very institutions of a firm. Hence, to better understand the role of outsider CEOs in the shift in institutional logics underlying DT, we propose adopting a perspective on institutional change.

The widespread diffusion of digital technologies has disrupted many industries and has significantly changed the business landscape through new ways of customer interaction and the digitalization of products and processes, enabling new digital business models (Verhoef et al., 2021; Vial, 2019; Volberda et al., 2021). For incumbent firms, adapting to this new digital reality often presents a big challenge (Hacklin et al., 2018; He et al., 2020; Piccinini et al., 2015). The initiation of DT requires new knowledge and skills that are mostly unrelated to what has made the incumbent firm successful in the past (Svahn et al., 2017). Furthermore, implementing digital initiatives into a firm’s business model is essential to cope with the requirements of operating in digital business environments (Menz et al., 2021). Specifically, for many firms, it requires the dissolution of existing routines and structures and the creation of new ones that are better suited for continuous adaptation in the face of ever-changing and evolving digital technologies (Chanias et al., 2019; Hanelt et al., 2021). For example, introducing digital technologies requires moving from a waterfall model of product development to open-ended design practices, where functionalities develop after the product launch (Svahn et al., 2017). DT thus goes further than strategic change, as firms need to fundamentally question current beliefs about their core assets and business models (Bharadwaj et al., 2013), shaking the very institutions that constitute firms’ identities.

DT and institutional entrepreneurship

The challenge of firms navigating new institutional logics diverging from their established ones has recently drawn attention through researchers applying perspectives of institutional change to firms’ DT (Hinings et al., 2018). As such, Henfridsson and Yoo (2014) explain how shifts in firms’ innovation trajectories toward digital innovation create a liminality of coexisting institutional logics. Tumbas et al. (2018) similarly draw on such liminal periods to explain the role of CDOs in emerging institutional logics and digital innovation. These studies specifically leverage the lens of institutional entrepreneurship in this context, explaining how individual actors, such as CDOs, can foster DT. Applying this perspective of institutional entrepreneurship to outsider CEOs seems especially promising, given the combination of their impartial outside perspective on the institutional context of incumbent firms and their social status due to their role as the ultimate leaders of firms.

The concept of institutional entrepreneurship emerged as an explanation for how institutions change over time, building a bridge between the structural concept of institutional theory and the agency of individual actors (Battilana et al., 2009; DiMaggio, 1988; Dorado, 2005). This institutional change process was described by DiMaggio (1988), who stated that “new institutions arise when organized actors with sufficient resources (institutional entrepreneurs) see in them an opportunity to realize interests that they value highly.” Later, institutional entrepreneurs were defined as “actors who leverage resources to create new or transform existing institutions” (Battilana et al., 2009: 68). Both definitions describe two important conditions for an actor to be described as an institutional entrepreneur: the motivation for divergent change stemming from an identified opportunity to do things differently in an institutionalized context and the ability to mobilize resources to foster that change (Battilana et al., 2009).

Prior literature has studied the role of institutional entrepreneurship in various contexts, such as the introduction of new organizational forms (Greenwood and Suddaby, 2006), the transposition of managerial practices (Boxenbaum and Battilana, 2005), or the introduction of radically new technologies (Munir and Phillips, 2005). The common starting point is the identification of an opportunity for change (Leca et al., 2006) that may stem from prior experience in the context of the targeted change (Boxenbaum and Battilana, 2005; Kraatz and Moore, 2002). To implement their envisioned change, institutional entrepreneurs draw on certain practices, including the creation of a vision (Battilana et al., 2009) and the mobilization of allies (Dorado, 2005). In that regard, prior studies highlight the importance of institutional entrepreneurs for bridging the institutional past with its emerging future (Garud et al., 2002; Maguire et al., 2004). Institutional entrepreneurs are thus change agents who operate in the liminality between institutional logics (Henfridsson and Yoo, 2014), as they fundamentally challenge an existing institution in their quest to implement change (Battilana et al., 2009).

In recent years, institutional entrepreneurship has gained traction as a theoretical lens that explains the introduction and implementation of digital technologies in incumbent firms (Henfridsson and Yoo, 2014; Tumbas et al., 2018). In their DT, firms need to develop new institutional logics, including new organizational forms, belief systems, and processes (Hanelt et al., 2021; Volberda et al., 2021). Given the influential positions that top executives—and especially CEOs—occupy within these firms, such change needs to be driven by them (Siebel, 2018). Therefore, applying the lens of institutional entrepreneurship seems fruitful to better understand how (outsider) CEOs can bring about institutional change.

Hypotheses development

Outsider CEOs, DT awareness, and digital transformation

Given the change in institutional logics (Battilana et al., 2009; Henfridsson and Yoo, 2014) underlying the DT of incumbent firms, its initiation by actors within the firm seems challenging, as they are embedded in the institutional context themselves (Garud et al., 2007). In this regard, we argue that outsider CEOs are particularly suited to act as institutional entrepreneurs by challenging existing ways of doing business and driving such change toward DT. To act as an institutional entrepreneur, the prior literature highlights two important prerequisites. First, an actor needs to be motivated to introduce divergent change (Battilana et al., 2009). Outsider CEOs mostly come in with a mandate for change (Berns and Klarner, 2017), are urged to differentiate themselves from their predecessors (Cannella and Shen, 2001), and are not embedded in the institutional context of the firm (Zhang and Rajagopalan, 2003), thus rendering their motivation for divergent change particularly given. Second, an actor needs the ability to mobilize sufficient resources (Battilana et al., 2009). The prominent position and formal authority of top executives (Tumbas et al., 2018), and particularly CEOs, grant them access to resources within firms (Battilana, 2006). Therefore, given their motivation for divergent change and accessible resources, outsider CEOs seem to be in prime position to act as institutional entrepreneurs and induce divergent change in institutionalized contexts.

However, to actually act as an institutional entrepreneur, the motivation for divergent change needs to translate into perceiving opportunities for change (Dorado, 2005) that entails “the capability to take a reflective position towards institutionalized practices and [. . .] envision alternative modes of getting things done” (Beckert, 1999: 786). Being able to do this likely requires experience in that specific domain for its transfer into a new context (Asad et al., 2023; Boxenbaum and Battilana, 2005). Such experience can stem from outside industry experience (Gunz and Jalland, 1996), or from another organization, as “an organization will be more likely to engage in institutional change when its leader has migrated from another organization that has previously adopted that specific change” (Kraatz and Moore, 2002: 126). In the context of driving DT, this directly relates to the prior experience of an outsider CEO with regard to DT in firms or industries, creating an awareness of the required change processes for DT. In particular, such DT awareness will significantly help in identifying specific opportunities to drive divergent change toward DT (Abebe et al., 2024; Bohnsack et al., 2021), as well as identifying institutional barriers currently prohibiting DT (Svahn et al., 2017; Volberda et al., 2021). For instance, a TV broadcasting firm may profit from leveraging the large amounts of data within the firm through the creation of a digital platform, enabling additional digital business models (Hess et al., 2016). The realization of such a digital initiative may be constrained by outdated beliefs about the value of customer data, as well as old processes and routines relating to insufficient and systematic customer data collection. An outsider CEO with DT awareness may benefit not only from an impartial perspective on the firm and its institutions but also from prior experience with DT relating to data integration for novel business models. In this regard, DT awareness of outsider CEOs allows for the identification of such opportunities for digital business models and the underlying barriers inhibiting their initiation that may be missing for outsider CEOs without such DT awareness.

Therefore, we argue that outsider CEOs with DT awareness not only have the motivation for divergent change and the ability to mobilize resources but also perceive specific opportunities and institutional barriers for DT, allowing them to act as institutional entrepreneurs and drive DT in incumbent firms. Consequently, we state the following hypothesis:

H1a. Outsider CEOs with DT awareness are positively associated with firms’ digital transformation.

Following our previous arguments, the mere “outsiderness” of outsider CEOs is not sufficient to drive DT in firms. Specifically, while outsider CEOs without DT awareness may also be motivated for change and have the ability to mobilize resources, they likely struggle with identifying the specific opportunities for DT as well as the institutional barriers preventing DT. Prior experiences shape more or less reflective positions toward institutionalized practices (Beckert, 1999) and contribute to CEOs’ sensemaking of opportunities and challenges. Lacking experience with DT could thus hamper outsider CEOs from identifying the emerging paths for incorporating digital technologies into business models as well as prioritizing among them. Moreover, an awareness of tackling the institutional barriers that may inhibit DT in incumbent firms, such as outdated beliefs or entrenched processes and routines, likely stems from prior experience in this regard. DT awareness thus constitutes a necessary prerequisite for outsider CEOs to act as institutional entrepreneurs and promote DT. Outsider CEOs without DT awareness may thus not realize the same level of DT progress as outsider CEOs with DT awareness. Consequently, we state the following hypothesis:

H1b. The influence of outsider CEOs with DT awareness on firms’ digital transformation is stronger than that of outsider CEOs without DT awareness.

The role of DT types

Firms differ strongly with regard to their typical DT journey (Hanelt et al., 2021). Some firms operate on a business model that can be digitized nearly entirely and can arrive at a new fully digital organizational mode. For instance, a newspaper firm can leverage digital technologies to build digital platforms for users and advertisers, and thus transfer a core of its analog business model to a digital environment (Abebe et al., 2024; Karimi and Walter, 2016). We conceptualize this as a rather abrupt DT journey. Other firms will face a more accumulative DT journey, where the goal state of the firm is ambiguous and where digital business model initiatives and the legacy business will coexist (Chanias et al., 2019). As such, large automotive firms experiment with digital business models and initiatives and aim to implement digital technologies in their cars. At the same time, they will still manufacture a physical product that cannot be digitized and will therefore arrive at a hybrid mode, combining their physical products with digital business models (Bohnsack et al., 2021; Svahn et al., 2017). While an institutional change is inevitable, regardless of the type of DT journey, the challenges that firms face in this change process may differ considerably, rendering the impact that an outsider CEO with DT awareness can have more or less strong.

To implement an institutional change in their firms, outsider CEOs need to create a transformative vision for change and mobilize resources (Battilana et al., 2009). Creating a transformative vision for change entails the ability to emphasize the shortcomings of the status quo and highlight the benefits of the future state (Henfridsson and Yoo, 2014). For firms facing an abrupt DT, the future state of the firm can be relatively clearly defined. This allows an outsider CEO with DT awareness to create a precise vision for divergent change and highlight its distinct benefits. Furthermore, while these firms equally endeavor to shift toward a diverging institutional logic, the clear vision for divergent change and the apparent benefits likely deflate upcoming resistance (Battilana et al., 2009), thus rendering an outsider CEO’s quest for the mobilization of allies comparably easy. However, for firms facing an accumulative DT entailing a rather hybrid and combinatorial transformation process, the envisioned future state of the firm is more ambiguous. For outsider CEOs to mobilize resources and allies for the implementation of divergent change, upcoming internal opposition from managers committed to the status quo of the firm, the so-called institutional defenders, needs to be countered (Levy and Scully, 2007). Outsider CEOs aiming to counter this resistance with a compelling and clear vision for divergent change and by emphasizing the benefits of the future state face significant complications if the future state of the firm is uncertain and entails a complex transformation process. However, given the inevitable coexistence of physical product manufacturing and digital business models in firms experiencing such accumulative DT endeavors (Björkdahl, 2020; Svahn et al., 2017), mitigating and solving these conflicts seems to be similarly inevitable for the success of DT implementation (Correani et al., 2020).

Taken together, we argue that the creation of a compelling vision and the mobilization of resources—two central prerequisites for the shift in institutional logics inherent in DT—is significantly complicated for outsider CEOs with DT awareness in firms facing a rather accumulative transformation. Thus, the effect of outsider CEOs with DT awareness on the DT of such firms is likely inhibited. 4 Consequently, we state the following hypothesis:

H2. The influence of outsider CEOs with DT awareness on firms’ digital transformation is lower for firms facing a rather accumulative digital transformation compared to firms facing a rather abrupt digital transformation.

Methodology

Sample and data

We test our hypotheses using a longitudinal panel dataset of non-digital S&P 1500 firms in the timeframe of 2006–2020. 5 Starting in 2006 seems appropriate as it coincides with the introduction and subsequent proliferation of several business services and products built on digital technologies (e.g. Amazon Web Services as a cloud technology or the first iPhone as a mobile technology). All firms included in our sample had to be listed at least once in the S&P 1500 during our sample period. We exclude all firms from digital industries 6 from our sample and include only those observations where data on all used variables is available. We collect data for our regression models from various sources. For our DT measure, we obtain 10 K reports from the Security and Exchange Commission’s (SEC’s) website. We further collect CEO and board data from BoardEx and data on financial information from Refinitiv DataStream. Our final sample consists of 11,238 firm years from 1340 firms.

Variables

Digital transformation—variable measurement

We measure DT as the integration of digital technologies into the firm’s business model (Verhoef et al., 2021). Specifically, we follow a recently more common practice of employing textual analysis on firms’ publicly available documents, namely, firms’ annual 10 K reports, to quantify written information (Hoberg and Phillips, 2016; Li et al., 2021). As a representation of the business model, we use the business section (Item I. Business) of the annually filed 10 K report with the SEC and employ a partly ML-generated dictionary. The business description in 10 K reports is especially suitable in this context, as firms are legally obligated by § 229.101 (Item 101) of the Code of Federal Regulation to describe the current state of the firm’s business as well as recent developments on an annual basis. Therefore, a description of key revenue-generating activities, products, and business models is available annually in an organized and regulated form (Hoberg and Phillips, 2016). At the same time, any planned digital initiatives of firms that are not yet realized and thus are more susceptible to window-dressing are not included in this section, rendering the business section of 10 K reports a particularly dependable source for firms’ digital business activities (Chen and Srinivasan, 2023).

The development of the ML-assisted dictionary involved two major steps: (1) an initial selection of seed words that matches the definition of our construct and (2) the subsequent expansion of seed words to create a full dictionary. In the first step, similar to Li et al. (2021), we diligently created a list of seed words related to our DT construct. As the integration of digital technologies into firms’ business activities forms the basis of DT (Vial, 2019), we focused on digital technologies and derived distinct categories from the commonly used SMACIT (an acronym for social media, mobile, analytics, cloud, and the Internet of Things) technologies (Sebastian et al., 2017; Vial, 2019). The SMACIT acronym “is intended as shorthand for the entire set of powerful, readily accessible digital technologies” (Sebastian et al., 2017: 197). In this regard, a recent literature review on DT emphasized that “most of the digital technologies mentioned within our sample fit with the popular SMACIT acronym” (Vial, 2019: 122). Therefore, SMACIT technologies are widely regarded as covering the most relevant and influential digital technologies in the business context, thus constituting an appropriate basis for deriving a framework for structuring our seed word selection. In addition to the categories included in the SMACIT acronym, we added a category covering words that relate to the general concept of digital technologies and DT (e.g. “digital,” “online,” and “cyber”). In selecting the individual words for each category, we carefully searched the existing body of research on DT to identify words that are commonly used in the respective context of our six categories (e.g. “artificial intelligence,” “machine learning,” and “big data” for the category “analytics”). We then presented our approach twice in a research seminar with researchers focused on DT and adjusted our dictionary accordingly. The resulting word lists 7 were then re-assessed with regard to their suitability and discussed among the authors, which led to the exclusion of ambiguous words.

After the creation of our list of seed words, which formed the basis for the subsequent expansion with the ML algorithm, we implemented the Python scripts introduced by Li et al. (2021) and used the ML algorithm to find synonyms for our seed words. This approach is based on word embedding and, specifically, the technique of word2vec (Mikolov et al., 2013), which is particularly suited for understanding the context of words and thus identifying words that are similar to each other (Mikolov et al., 2013). From the resulting list of words, all words with a similarity score of 0.5 or higher compared to the seed words in the categories were included in the expanded dictionary. We then manually screened all words in the expanded dictionary and deleted words with overly broad meanings (Li et al., 2021) to ensure the affiliation of words with the topic of DT. Afterward, three raters (two researchers with experience in DT and textual analysis research and a consultant focused on DT) diligently checked the words in the expanded dictionary for their affiliation with digital technologies and DT. We excluded words from the dictionary that were discarded by at least two of the three raters, resulting in the exclusion of three words and a final dictionary of 618 words. 8 We used these results and followed the approach set forth by Holsti (1969) and recommended by Short et al. (2010) in calculating the inter-rater reliability between the raters’ assessments, resulting in a score of 0.97, which exceeds critical thresholds (Krippendorf, 2004) and indicates substantial agreement. 9

Using the final dictionary and computer-aided text analysis, we calculate the term frequency scores for our sample firms’ annual business sections. The scores of our six categories are added up to obtain an overarching DT score, and we divide it by the document length (Loughran and Mcdonald, 2016). 10 Finally, the measure of DT is forwarded, capturing the three future years (t + 1 to t + 3) to account for the longer lead times of digital initiatives.

Digital transformation—validity tests

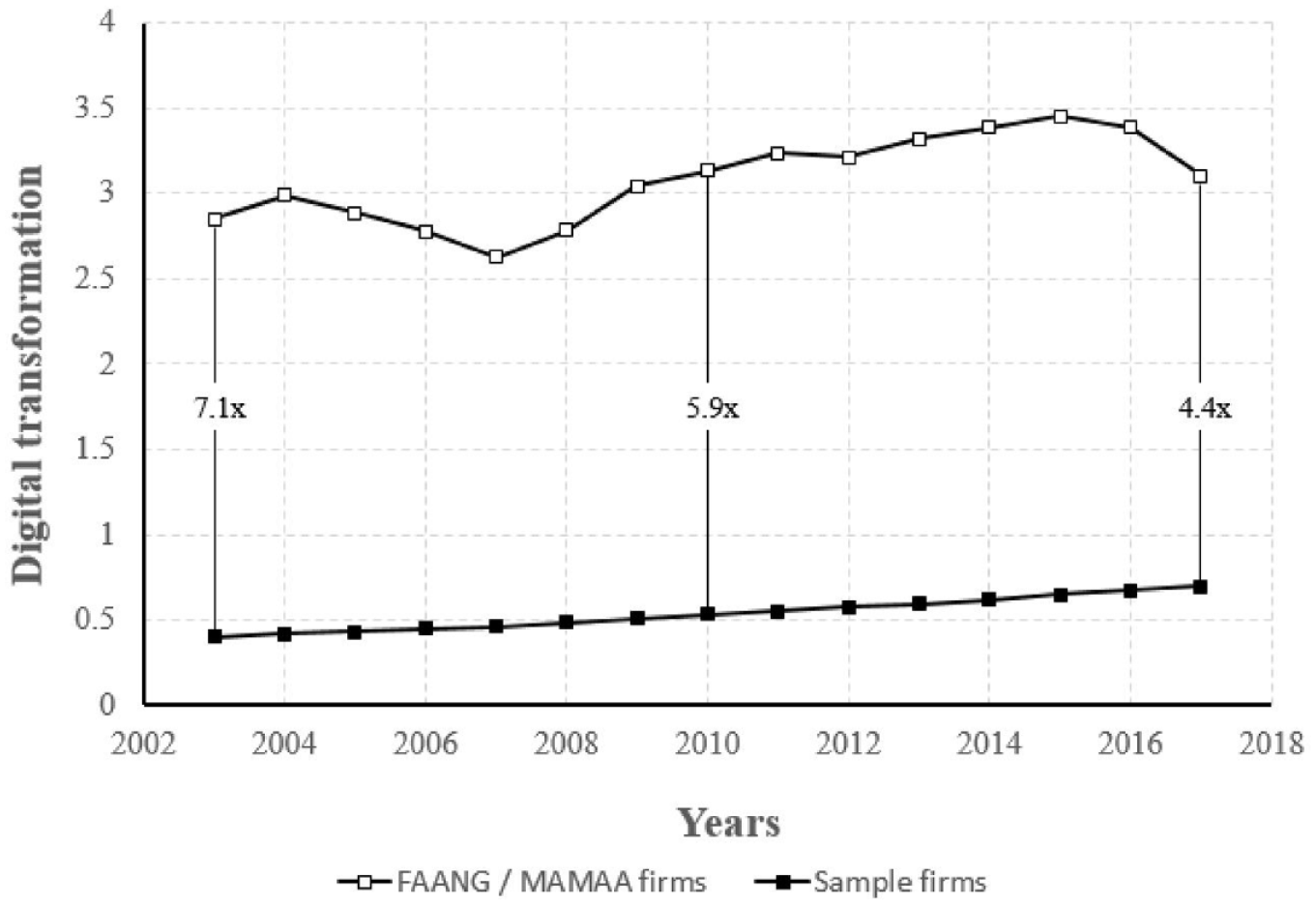

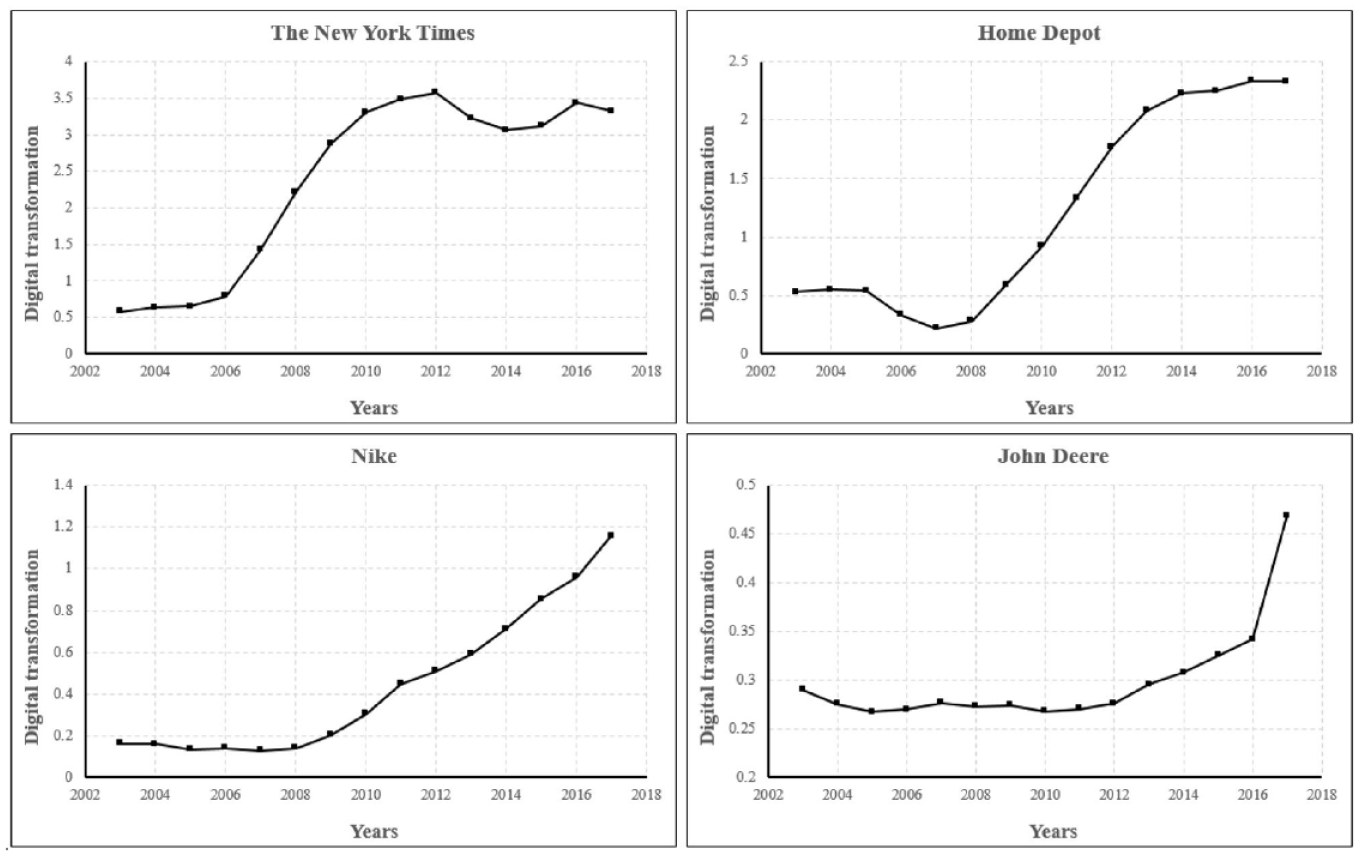

We conduct several quantitative and descriptive tests to validate our measure. First, we calculate the mean DT score of commonly known digital firms, often referred to as “FAANG” or “MAMAA,” as those firms should naturally score higher on our measure and would likely not become much more digital over time, and compare their score with our sample firms over time. We indeed find that these firms score significantly higher than our sample firms (on average, 3.12 versus 0.55), while our sample firms continuously closed the gap over time, as displayed in Figure 1. Second, we analyze the business section and corresponding DT measures of firms that are frequently highlighted for their DT in the business press. As a first example, we check the firm John Deere, which has recently made strides in its DT (O’Marah, 2022). As a second example, we check a firm from the newspaper industry, an industry that has been described as being significantly disrupted by digital technologies (Abebe et al., 2024; Karimi and Walter, 2016). We choose the example of the New York Times, as it is known to have significantly shifted its business model toward digital news outlets (Doeland, 2019). As a third and fourth example, we check Nike and Home Depot, as these firms have been repeatedly highlighted for their continuous DT achievements (Barsky, 2021; Giles, 2019). We find that our measure resembles the advancements in the DT of these firms during our sample period. We provide graphical illustrations of the DT scores of the above-mentioned firms in Figure 2, and the corresponding excerpts of their business descriptions in Table A2 of the Online Appendix.

Comparison of DT score development of “FAANG”/“MAMAA” firms and sample firms.

DT score (average of 3 future years) of example firms from different industries.

Third, we analyze competing firms within an industry to check whether our measure can differentiate between firms that are known to be ahead of or lagging behind in their DT. We choose the retail trade industry, as we find this industry to have made significant advancements in DT within our sample period, and it entails multiple comparable S&P 1500 firms with available data on their DT scores. While we find the retail trade firms to score low on our DT measure early in our sample, the DT score of firms strongly diverged over time, starting around 2010, as firms known to be ahead in their DT in this industry, such as Home Depot (Giles, 2019) and Bed, Bath, & Beyond (McCoy, 2021), started to score higher for our measure. On the other hand, we find firms known to be lagging behind in their DT, such as Lowe’s (Cain, 2019), to score much lower. 11 The results are graphically illustrated in Figure 3. Fourth, we check the mean DT score for different industries, as the score should differ between, for instance, firms in the services industries and firms in the mining or construction industries. As expected, we find such differences between industries, both in terms of their mean score and in terms of increases over our sample period. We present these numbers in Table OA1 of the Online Appendix. Finally, we regress our DT measure on the proportion of digital product releases (captured via Ravenpack) of the same firm. Higher DT levels should be reflected in a larger proportion of digital products. We find that our DT measure strongly predicts the proportion of digital product releases (p < 0.01), as presented in Table OA2 of the Online Appendix.

DT score (average of 3 future years) of example firms from the retail trade industry.

Outsider CEO with DT awareness

For the operationalization of our outsider CEO with DT awareness variable, we follow a two-step approach. First, we follow prior literature in defining successor CEOs as outsiders if they had held a position in another firm during the previous two years prior to the succession and 0 if otherwise (Shen and Cannella, 2002; Zhang, 2006). Second, to arrive at our variable, we aim to identify outsider CEOs with DT awareness. A large stream of research elaborates on the influence of managers’ prior work experience on their decision-making (e.g. Fondas and Wiersema, 1997; Zhu and Shen, 2016). These studies regularly highlight the effect that outside industry experience has on managers’ awareness of specific topics and their subsequent tendency to foster such topics in their firms (Gunz and Jalland, 1996). Applying this lens to the context of DT, we suggest that outsider CEOs obtain DT awareness from prior work experience in the context of DT. Therefore, we searched the employment history of appointed outsider CEOs for prior employment in industries that faced high levels of DT during their time of employment. We choose a rather restrictive approach and classified industries as experiencing high levels of DT if they ranked among the highest quantile of industries with regard to the change in the average DT score over a 3-year span. 12 Our variable of outsider CEOs with DT awareness is then coded as 1 if an appointed outsider CEO had at least 2 years of prior work experience in such an industry and 0 if otherwise. 13

DT type

Assessing the anticipated type of a firm’s DT journey is challenging, and the literature provides no established measure. In our approach, we focus on the characteristics of the existing business model that relate to the potential of digitizing the business model. Depending on this potential, firms have very different starting points that likely differentiate their DT journey. However, we also acknowledge that this can only be an approximation and that we might not capture the full heterogeneity in DT journeys. Specifically, we differentiate between firms that primarily base their business model on physical assets, such as production equipment and machinery, rather than on information and knowledge, such as copyright-protected content. We follow prior research in its argumentation that business models based on information and knowledge can be more easily digitized (Firk et al., 2021; Zmud et al., 2010) than business models based on physical assets. To operationalize our variable, we create a continuum that combines the capital intensity and extent to which firms leverage intangible assets. 14 The lower end of this continuum represents firms that rank high in intangible assets and low in capital intensity, thus basing their business model rather on information and knowledge (Alimov and Officer, 2017). We suggest that these firms face a rather abrupt DT, as their business model can be digitized fairly easily, resulting in a shift toward a new fully digital organizational mode and digital business model. On the other hand, the upper end of the continuum represents firms ranking high in capital intensity and low in intangible assets, thus basing their business model rather on physical assets. 15 We suggest that these firms face a rather accumulative type of DT, as their business models cannot be easily digitized, requiring these firms to combine their physical asset-based business model core with digital initiatives over time that result in the digitization of their business models.

Control variables

We include a broad set of control variables in our models, covering firm, board, CEO, and industry effects. At the firm level, we include firm size, R&D intensity, prior firm performance, leverage, sales growth, and TMT size. Regarding board controls, we include board size, average time on board, and outsider percentage. To control for potentially confounding influences at the CEO level, we include CEO age, CEO duality, CEO functional background, and CEO educational level. At the industry level, we include industry growth. We also include an inverse Mills ratio from a first-stage probit model as a CEO selection control in our models. A detailed list with the descriptions and calculations of the included variables can be found in Table A1 of the Online Appendix.

Empirical strategy

As firms might be more inclined to hire outsider CEOs with DT awareness if a stronger focus on DT is aimed at, appointments of outsider CEOs with DT awareness do not occur randomly. To mitigate the risk of receiving misleading results based on this source of endogeneity, we employ a Heckman (1979) two-stage model that is widely used in studies on outsider CEOs and subsequent firm outcomes (Georgakakis and Ruigrok, 2017; Karaevli and Zajac, 2013; Quigley et al., 2019).

Stage I

In the first stage of the model, we predict the likelihood of an outsider CEO with DT awareness being appointed by employing a probit regression with an exclusion criterion. We select director exposure as our exclusion criterion, capturing the exposure of the supervisory directors of the firm toward other outsider CEOs with DT awareness prior to the succession event through other board mandates. Given the influence of supervisory directors on the selection of new CEOs (Westphal and Fredrickson, 2001), their prior exposure to outsider CEOs with DT awareness likely influences the selection of such CEOs. At the same time, we expect that the exposure of directors to a specific kind of outsider CEO in other board mandates should be plausibly exogenous to the focal firm and not affect DT in another way than via the selection of the CEO. In line with this, our exclusion criterion is significantly correlated to outsider CEO with DT awareness (0.129; p < 0.01) and not significantly correlated to our DT measure (−0.002; p > 0.1). We use the predicted values of this first-stage probit model to calculate the inverse Mills ratio that is included in all subsequent models (Heckman, 1979). Other variables included in the first stage are listed and described in Table A1 of the Online Appendix. The results of the first-stage probit regression are displayed in Table OA3 of the Online Appendix.

Stage II

For the second stage, we exploit our panel dataset and estimate firm-fixed effects regressions with the inverse Mills ratio from the first stage as a correction factor (CEO selection control). Controlling for firm-fixed effects seems especially appropriate in our case, as firms strongly investing in digitally transforming themselves will differ significantly from firms that do not. This source of endogeneity is also addressed by including control variables at the firm level. However, as unobserved differences could remain, controlling for firm-fixed effects additionally addresses this issue. In all our models, we include year-fixed effects and employ robust standard errors by considering the Huber–White standard error correction (White, 1980). All control and moderator variables as well as the independent variable, are measured in t, and the dependent variable is measured from t + 1 to t + 3.

Results

Descriptive results

An illustration of the average yearly values of our DT measure is presented in Table 1. In the first year of our sample period, the average DT score is 0.43, while for the last year, the average DT score is 0.69. The score increases every year during our sample period, highlighting the increasing importance and proliferation of DT during the sample period.

Digital transformation (DT) over time.

The score thus covers the years until 2020. To facilitate interpretation, standardized values of DT are used in the regression analyses.

Average of the DT score for t + 1 to t + 3.

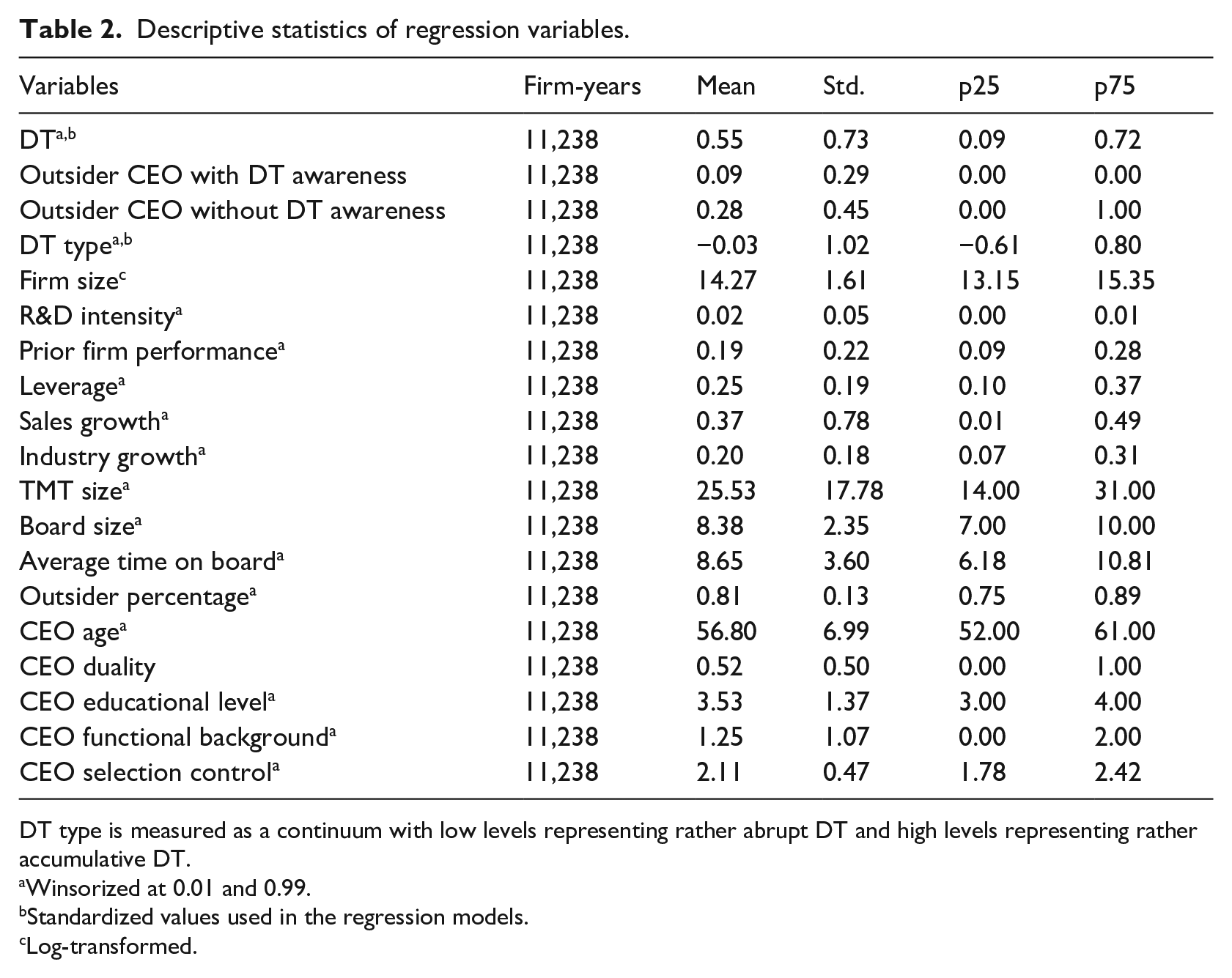

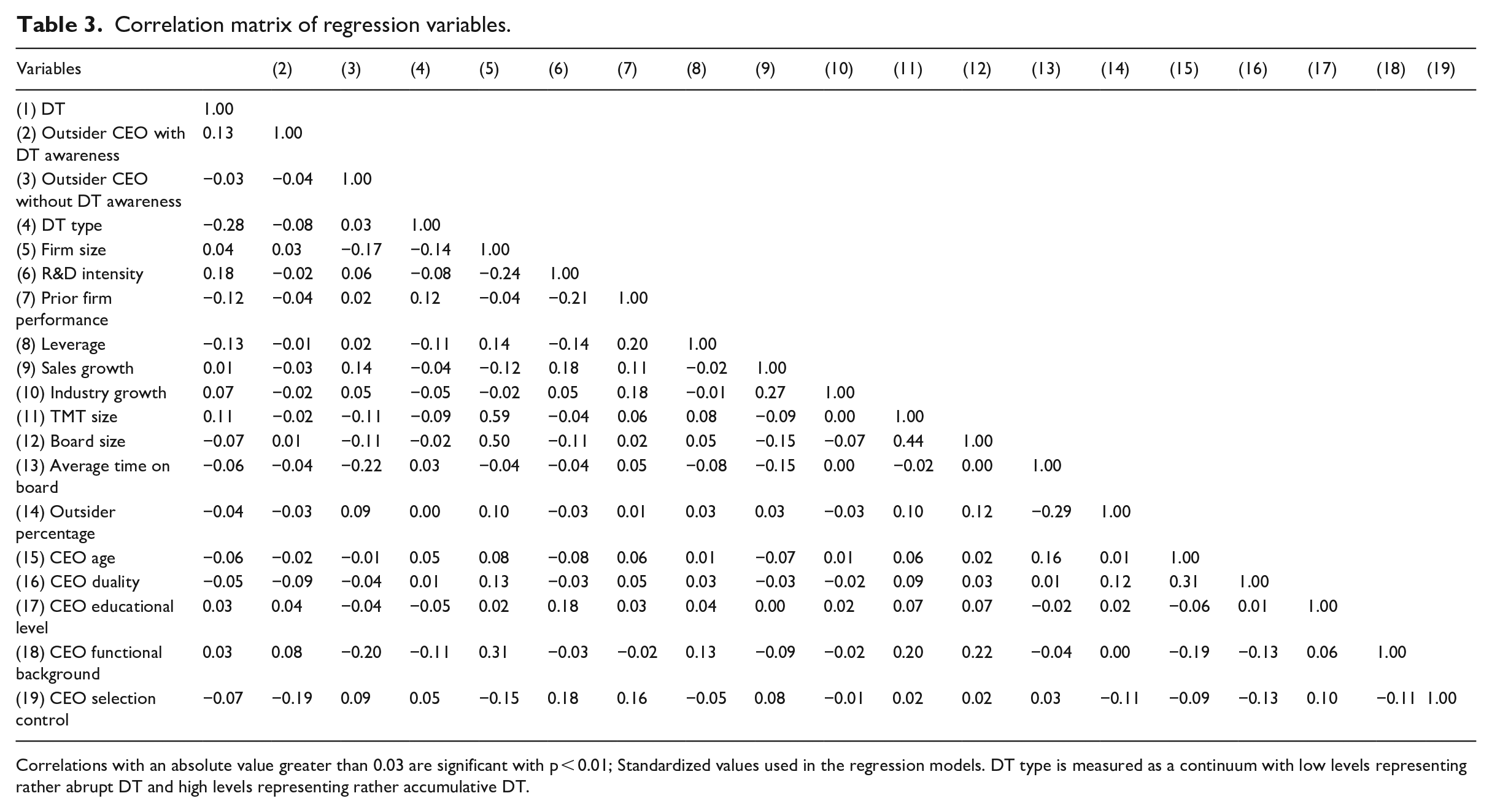

In Table 2, the summary statistics of all variables included in the regressions are provided. For our measure of outsider CEO with DT awareness, we find that such CEOs are present in 9% of our sample years. In contrast, outsider CEOs without DT awareness constitute 28% of our sample years. The combined number of 37% of outsider CEOs is in line with other studies on CEO origin (Quigley and Hambrick, 2012; Zhang and Rajagopalan, 2010). The correlations of the included variables are displayed in Table 3. The correlation between outsider CEO with DT awareness and DT is positive and significant. We find some fairly high correlations between other variables, for example, firm size and board size. Therefore, we tested the corresponding variance inflation factors and obtained results below the critical threshold of 5.

Descriptive statistics of regression variables.

DT type is measured as a continuum with low levels representing rather abrupt DT and high levels representing rather accumulative DT.

Winsorized at 0.01 and 0.99.

Standardized values used in the regression models.

Log-transformed.

Correlation matrix of regression variables.

Correlations with an absolute value greater than 0.03 are significant with p < 0.01; Standardized values used in the regression models. DT type is measured as a continuum with low levels representing rather abrupt DT and high levels representing rather accumulative DT.

Regression results

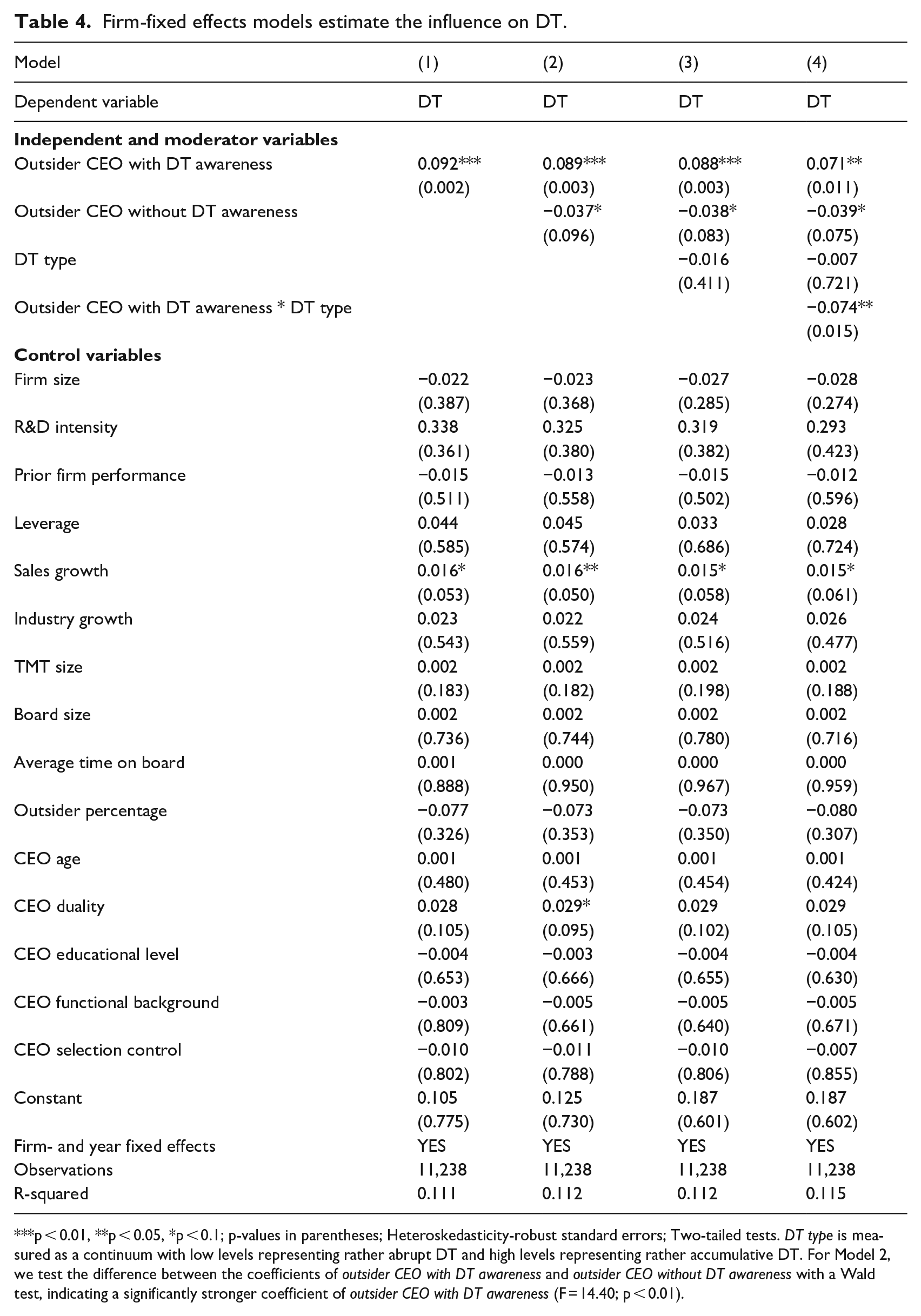

Table 4 presents the results of our hypotheses testing. In Model 1, we test H1a by regressing our dependent variable DT on the dummy variable outsider CEO with DT awareness while including our control variables. Thereby, Model 1 reflects the association between outsider CEOs with DT awareness and DT when compared against all other CEOs. In Model 2, we additionally include the dummy variable outsider CEO without DT awareness. As a result, the coefficients of the variables outsider CEO with DT awareness and outsider CEO without DT awareness reflect the association between the two types of outsider CEOs and DT when compared to all insider CEOs. To test H1b regarding whether the association between outsider CEOs with DT awareness and DT is stronger than for outsider CEOs without DT awareness, we compare the coefficients of outsider CEO with DT awareness and outsider CEO without DT awareness and assess whether their association with DT (when compared to insider CEOs) is significantly different from each other. 16 Finally, to test H2 in Models 3–4, we stepwise include the moderator variable DT type as well as an interaction term between DT type and outsider CEO with DT awareness.

Firm-fixed effects models estimate the influence on DT.

p < 0.01, **p < 0.05, *p < 0.1; p-values in parentheses; Heteroskedasticity-robust standard errors; Two-tailed tests. DT type is measured as a continuum with low levels representing rather abrupt DT and high levels representing rather accumulative DT. For Model 2, we test the difference between the coefficients of outsider CEO with DT awareness and outsider CEO without DT awareness with a Wald test, indicating a significantly stronger coefficient of outsider CEO with DT awareness (F = 14.40; p < 0.01).

In line with our arguments in H1a, Model 1 shows a significant positive coefficient for outsider CEO with DT awareness on DT (β = 0.092; p = 0.002) suggesting that hiring an outsider CEO with DT awareness is related to a 9.2% increase in DT. This result stays robust in Model 2 (β = 0.089; p = 0.003), where we simultaneously include the variable outsider CEO without DT awareness. For the variable outsider CEO without DT awareness, we do not find a positive influence (even negative and marginally significant) on DT (β = −0.037; p = 0.096). We further test the difference between the two coefficients with a Wald test, indicating a significantly greater coefficient of outsider CEO with DT awareness (F = 14.40; p < 0.01), thus supporting H1b.

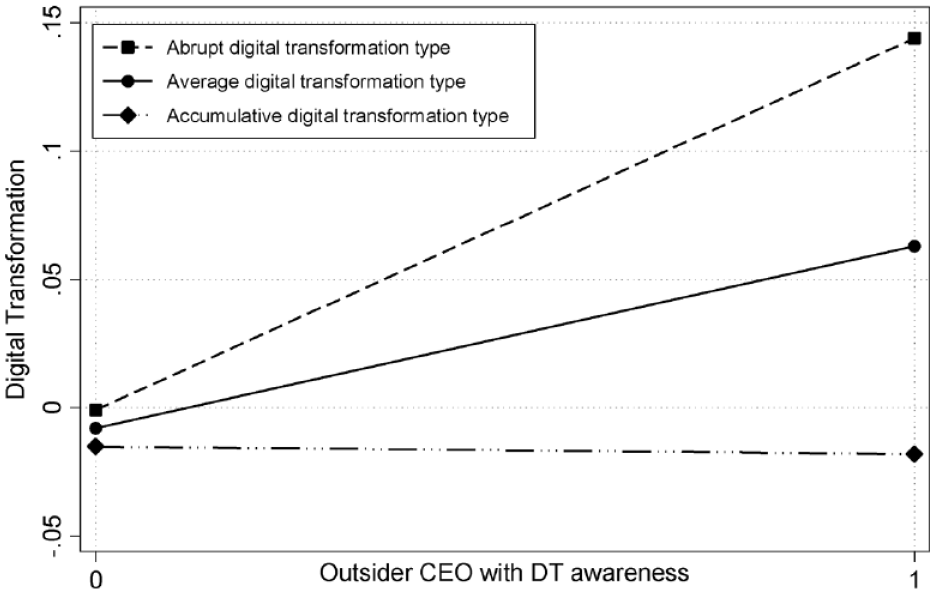

In H2, we argue that the influence of outsider CEOs with DT awareness is restricted in firms facing a rather accumulative DT. Therefore, we include an interaction term between the variables DT type and outsider CEO with DT awareness in Model 4. Before being included in the model, the variable DT type was standardized (Aiken and West, 1991). In line with our hypothesis, we find a significant negative coefficient for the interaction term (β = −0.083; p = 0.008), suggesting that the influence of outsider CEOs with DT awareness is less pronounced when firms face a rather accumulative DT. This result is also graphically supported in Figure 4, which displays the association between outsider CEOs with DT awareness and DT for a more abrupt DT type (mean minus one standard deviation), the average DT type (mean), and a more accumulative DT type (mean plus one standard deviation).

The moderating influence of DT type on the relationship between Outsider CEOs with DT awareness and DT.

Robustness analyses

We conduct several tests to validate the robustness of our results. First, we test alternative specifications of our dependent variable DT. Given the term frequency (TF) score employed in our main models, a possible concern arises in that such a score does not attribute different weights to words that may be more or less important in the context of digital technologies. To address this concern, we use a term frequency score that is adjusted for the inverse document frequency of words (TF-IDF). This score attributes a higher weight to words related to digital technologies that are less frequently used in the text corpus and thus may reflect more unique DT strategies. We further use only the created list of seed words instead of the full dictionary and tested a different timeframe for the measurement of our dependent variable (t + 1 to t + 2). All tests with alternative specifications of our dependent variable yield results similar to our main models and are presented in Table OA4 of the Online Appendix.

Second, we test alternative specifications of our independent variable of outsider CEO with DT awareness. Specifically, we alter the threshold for industries experiencing high levels of DT to those in the highest decile, quartile, and tertile. We further alter the timeframe for the calculation of industries experiencing high levels of DT to 5 years and 7 years. The association between outsider CEO with DT awareness and DT remains robust, as all tests yield similar results to our main models. The results are displayed in Table OA5 of the Online Appendix.

Third, we consider a different regression analysis. As employed in prior studies on CEO succession and subsequent firm outcomes (Quigley and Hambrick, 2012), we use generalized estimation equations (GEE). This alternative regression analysis approach yields results consistent with our main models and is presented in Table OA6 of the Online Appendix.

Fourth, we apply an alternative approach by testing the two components of DT type (intangible assets and capital intensity) independently. Our results remain robust, as we find a significant negative interaction term for capital intensity and a significant positive interaction term for intangible assets. We present the results in Table OA7 of the Online Appendix.

Discussion and conclusion

In this study, we investigated the role of outsider CEOs in the DT of firms. Specifically, we proposed that DT awareness of outsider CEOs stemming from prior work experience in the context of DT enables outsider CEOs to act as institutional entrepreneurs and drive divergent change toward a new institutional logic for operating in digital business environments. We further argued that this influence is stronger for firms facing a rather abrupt DT compared to those facing a rather accumulative DT. Our findings, derived from employing a novel measure for firms’ DT in a firm-fixed effects regression of more than 11,000 firm-year observations, support these arguments.

Contributions to the literature

We contribute to the literature in three ways. First, we extend the literature on CEO origin and firm outcomes (Berns and Klarner, 2017; Schepker et al., 2017) by moving beyond the insider–outsider distinction and delving into the differences between outsider CEOs. Focusing on the recent call for more research on the role of outsider CEOs in DT (Singh et al., 2020; Volberda et al., 2021), we explain why certain outsiders may not only be more effective than insider CEOs in accelerating DT, but also more effective than other outsider CEOs. While there is rich literature on the relationship between outsider CEOs and strategic change (Nakauchi and Wiersema, 2015; Zhang and Rajagopalan, 2010), DT typically goes hand in hand with a fundamental shift in institutional logics (Henfridsson and Yoo, 2014) and thus exceeds the logics of strategic change (Adner et al., 2019; Ndofor et al., 2013). A perspective constrained to firm strategy is thus likely to fall short in accounting for the institutional challenges that outsider CEOs face in DT. Hence, we theorize how outsider CEOs can act as institutional entrepreneurs, driving not only strategic change, but also institutional change in firms to foster DT. We particularly emphasize that outsider CEOs are well positioned to “take a reflective position towards institutionalized practices and [. . .] envision alternative modes of getting things done” (Beckert, 1999: 786). However, envisioning alternative modes depends on their ability to identify specific opportunities for DT, which cannot be explained by mere outsiderness. Specifically, we introduce the role of outsider exposure to the specific change that creates an awareness of such opportunities as an important enabling factor. We show that outsider CEOs with such awareness of DT, stemming from prior work experience, drive DT in incumbent firms, in contrast to outsider CEOs without such experience. Thereby, we provide a nuanced perspective of the diverging ramifications of outsider CEOs depending on the kind of outside experience they possess. This allows us to point to the boundaries of deriving implications from prior studies focused on CEOs’ mere outsiderness in explaining specific institutional change processes, such as DT. This highlights the benefits of combining concepts rooted in institutional theory, such as institutional entrepreneurship, with the strategic management literature to provide a better understanding of the CEO role within the phenomenon of DT.

Second, we contribute to the literature on strategic leadership and DT. While this stream of research emphasizes both the novel roles of executives emerging in DT, such as CDOs (Firk et al., 2021; Singh et al., 2020; Tumbas et al., 2018), and the influence of existing groups of managers for DT, such as the TMT (Firk et al., 2022), or the middle management of firms (Van Doorn et al., 2023), little is known about the role of the CEO as the primary strategic leader in an organization for DT. We complement prior studies by emphasizing the importance of CEOs in creating a transformative vision for divergent change and by identifying institutional barriers that inhibit this change. However, we also point to the boundary conditions of this influence. Some firms face a more accumulative DT process, as they aim to achieve a hybrid mode that combines physical products with digital business models. These firms particularly warrant an integrative force that enables a combination of new and preexisting organizational modes. Our results suggest that outsider CEOs with DT awareness struggle in implementing their transformative vision in firms facing a more accumulative DT process. Thereby, we point to the importance of considering the heterogeneity in DT types, which may help to better understand the divergent demands on strategic leadership in the context of DT.

Third, we develop and validate a quantitative measure capturing firms’ DT that paves the way for future research to carry out calls for more strategy research in the context of DT (Hanelt et al., 2021; Menz et al., 2021; Volberda et al., 2021). Our measure enables researchers to capture firms’ realizations of DT, allowing them to empirically test novel research questions derived from the vast stream of theoretical work covering the DT phenomenon. In particular, it facilitates large-scale archival research on, for instance, drivers of DT and its implications, and thus complements prior conceptual (Menz et al., 2021; Volberda et al., 2021) and qualitative studies (Abebe et al., 2024; Warner and Wäger, 2019). Moreover, our measure extends prior research that has developed patent-based measures related to the concept of digital innovation (Firk et al., 2022; Miric et al., 2023). Compared to these approaches, our measure is more universal and allows for its application in firms from all industries, while patent-based digital innovation measures are usually subject to downsides, such as a lack of transferability to non-patenting industries.

Managerial implications

In addition to the theoretical implications mentioned above, our study has important practical implications. In light of the increasing appointments of outsider CEOs (Nickisch, 2016), our results offer valuable empirical insights into their influence on DT. In particular, our results suggest that the mere “outsiderness” of such CEOs is not sufficient to drive DT. Board members may thus learn from our results that the institutional change required for DT requires the specific prior experience of outsider CEOs. Furthermore, our study emphasizes the importance of understanding that pathways toward DT differ significantly between firms. Our results highlight that a flawed assessment of a firm’s challenges for DT can significantly derail prospect of an outsider CEO appointment driving such a change.

Limitations and future research

As with any study, ours has limitations that may yield interesting opportunities for future research. First, our approach to building a quantitative measure for DT based on external disclosure is not without limitations. While our validation tests suggest strong support for the applicability of our measure in the context of DT, our measure mainly captures changes within the firm’s business model. Integrating digital technologies into the business model typically requires broader institutional change in an organization (Hinings et al., 2018). However, we acknowledge that our measure cannot directly capture these institutional changes within an organization, and we encourage future studies to further test the validity and limitations of our DT measure. Second, in our study, we specifically analyzed the role of CEOs for DT. However, recent studies have also found heterogeneous responses of middle managers in DT (Van Doorn et al., 2023) and employees (Firk et al., 2024). Therefore, future studies could specifically focus on the role of middle managers and how job requirements change for employees with DT to incorporate their role as a contingency factor into our understanding of the influence of C-level executives on DT. Third, our measure to differentiate DT types has limitations. To explore the heterogeneity in firms’ DT journeys, we decided to focus on firms’ existing business models and, specifically, whether firms rely more on physical or intangible assets. DT for firms with more physical assets likely entails a more accumulative journey aiming for a hybrid mode combining physical products with a digital business model, while firms with more intangible assets may follow a more abrupt journey, transferring the core of their analog business model to a digital environment. However, there is probably still additional heterogeneity in firms’ DT journeys that cannot be captured by this distinction. For example, some firms relying on physical assets may also envision a more abrupt DT that shifts the firm to a purely digital business model. Future research could further expand on classifying and characterizing the modes of DT to better capture the heterogeneous challenges firms are facing. Fourth, given that our sample exclusively consists of US firms, the transferability of our results may be limited. Similar to prior studies that emphasized the relevance of country-level institutional factors for firms’ strategic actions (Steinberg et al., 2023), our results may differ in, for instance, countries with weaker digital infrastructures that may require more coordination with external stakeholders (Firk et al., 2021) or in those with strong labor unions that require a delicate approach when it comes to automation ambitions (Nissim and Simon, 2021; Verma and de Vynck, 2023). In this regard, differences in economic and cultural contexts offer interesting avenues for future research on the drivers of DTs.

We hope to inspire future research in the growing field of DT to study the role of CEO characteristics and firm-level contingency factors in the DT success of firms. In particular, we trust that our DT measure will pave the way for large-scale research based on archival data. Research on DT constitutes an intriguing intersection between strategy research and institutional theories, offering exciting avenues for future studies. Such research can help us better understand why some firms prosper in the face of new digital environments while others flounder.

Supplemental Material

sj-docx-1-soq-10.1177_14761270241242905 – Supplemental material for Institutional entrepreneurship and digital transformation: The role of outsider CEOs

Supplemental material, sj-docx-1-soq-10.1177_14761270241242905 for Institutional entrepreneurship and digital transformation: The role of outsider CEOs by Sebastian Firk, Jan C Hennig, Julian Meier and Michael Wolff in Strategic Organization

Footnotes

Acknowledgements

The authors wish to thank the editor, Margarethe Wiersema, and the reviewers for their excellent guidance. We are further grateful for helpful comments by Marko Reimer, Alejandro Escribá-Esteve, and participants of the 1st EIASM Paper Development Workshop on TMT and Business Strategy Research (December 2021) and the Annual Meeting of the Academy of Management (August 2022).

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

Notes

Author biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.