Abstract

How do board environmental experts influence corporate environmental performance? Drawing on the advisory role of the board, we examine this question and propose that board environmental expertise fosters attention toward stakeholders through the development of decision-makers’ knowledge structures and the identification of opportunities to address a wider range of stakeholders, ultimately contributing to stronger stakeholder orientation. In addition, we theorize that board environmental expertise fosters substantive actions toward environmental performance by reducing information asymmetry and accurately assessing the risks of investing in pro-environmental initiatives. We also consider how the effects unfold in different institutional contexts. We theorize and find that national stakeholder salience increases attention pressure toward stakeholders and that environment-oriented legislation adds to the action pressure toward environmental performance. Our results, based on 11,634 firm-year observations from 15 countries between 2003 and 2016, support our theoretical predictions.

Keywords

Introduction

Research on strategic management and corporate governance has recently emphasized the importance of boards’ advisory role in achieving superior environmental performance (Aguilera et al., 2021; de Villiers et al., 2011; Walls and Berrone, 2017). For example, Walls and Hoffman (2013) argue that boards of directors with specialized environmental experience lead their firms toward proactively adopting environmental practices that go beyond institutional norms. Similarly, Homroy and Slechten (2019) show that independent directors with previous experience in environmental issues are associated with lower greenhouse gas emissions. Recent business news also affirms the emphasis on the environmental expertise of directors, as the recent appointment of Joan MacNaughton to the board of Heathrow Airport, with the specific purpose of advising on decarbonizing the sector, demonstrates (Kearns, 2022). According to PwC’s 2022 Annual Corporate Directors’ Survey, 94% of the directors surveyed considered environmental expertise to be important on the board. Although board expertise is critical for environmental performance, the academic literature on the channels through which environmental experts on corporate boards benefit firm environmental performance is limited.

In this article, we aim to extend this emergent literature by theorizing on how board environmental expertise affects corporate environmental performance. First, we argue that directors with environmental expertise can play an advisory role by creating attention to increase their firm’s stakeholder orientation. We understand stakeholder orientation as the degree to which a firm’s top management incorporates the concerns and interests of various stakeholders into the decision-making process (Bettinazzi and Feldman, 2021; Bettinazzi and Zollo, 2017). We theorize that boards with environmental experts have the necessary knowledge structures that can spill over to other decision-makers and shift their attention away from a shareholder-centric focus toward a stakeholder-centric focus (Shepherd et al., 2017). In addition, directors with environmental expertise have the necessary information to recognize opportunities when catering to the interests of a broader set of stakeholders to improve environmental performance. Following this logic, we expect boards with a stronger representation of environmental experts to be more committed to shifting corporate attention to stakeholders and sustaining that shift.

Second, we propose that directors with environmental expertise can also play their advisory role by initiating substantive action to ensure better firm environmental performance. As Walls and Hoffman (2013) argue, “organizational actions toward environmental sustainability depend, in large part, on the direction given by the board of directors” (p. 254). Boards have the influence to initiate strategic changes (e.g. Boivie et al., 2021; Haynes and Hillman, 2010; Oehmichen et al., 2017). We theorize that board environmental experts can encourage substantive actions by bridging information gaps between firms and their ecological environments and assessing the risk of investing in pro-environmental measures. Thus, we posit a positive relationship between board environmental expertise and corporate environmental performance.

To gain a more nuanced understanding of how attention and action mechanisms operate, we carefully consider the institutional context. Prior research from institutional and neo-institutional perspectives has demonstrated that firms’ attention and actions vary based on the macro-institutional contexts shaped by distinct institutional logics (Ioannou and Serafeim, 2015; Martínez-Ferrero et al., 2016). Recognizing that individual governance mechanisms are intertwined with the country-level institutions in which they take effect (Ioannou and Serafeim, 2012), we incorporate country-level moderators in our analyses. Specifically, we incorporate countries’ stakeholder salience as a measure of attention pressure and countries’ environment-oriented legislation as a measure of action pressure. We anticipate that the influence of board environmental experts in directing attention toward stakeholders will be more pronounced in countries with higher stakeholder salience. Similarly, we expect that the facilitative role of environmental experts in driving substantive actions to improve environmental performance will be amplified in countries with stronger environment-oriented legislation. This consideration accounts for the regulatory framework, policies, and enforcement mechanisms that exert pressure on boards to prioritize environmental concerns.

Our empirical analysis of 11,634 firm-year observations from 15 countries between 2003 and 2016 supports our predictions. We find board environmental expertise to be positively associated 1 with stakeholder orientation, confirming our proposition of an attention effect. We also find that board environmental expertise is positively associated with corporate environmental performance, confirming our proposition of an action effect. Furthermore, our results document a positive moderating role of countries’ institutional effects. We find that national stakeholder salience strengthens the relationship between board environmental expertise and stakeholder orientation. In addition, we find environment-oriented legislation to strengthen the relationship between board environmental expertise and corporate environmental performance.

Our study contributes to an emerging stream of literature on the relationship between board expertise and environmental performance in the following ways. First, building on prior work that focuses on whether board characteristics influence environmental performance (de Villiers et al., 2011; Dixon-Fowler et al., 2017; Walls et al., 2012), we provide detailed insights into the mechanisms by which directors with environmental expertise create attention to increase stakeholder orientation and initiate action toward environmental matters. In doing so, we respond to increasing calls that point to the need to elucidate the processes through which directors manage their firm’s attention toward broader sets of stakeholders needed for better environmental performance (Delmas and Toffel, 2004; Kassinis and Vafeas, 2006). In addition, we respond to the call for more research on “what is actually required to implement environmental initiatives” (Dowell and Muthulingam, 2017: 1288).

Second, our study contributes to the literature on the board’s advisory function, particularly in the context of environmental expertise. While prior research has emphasized the importance of directors’ command and control duties, we argue that the expertise of directors in advising can enhance the quality of information available to the board (Faleye et al., 2011). Finally, we provide cross-country empirical evidence on the role of the board’s environmental expertise in influencing corporate environmental performance. Compared to previous studies that were based on single-country samples (Homroy and Slechten, 2019; Walls and Hoffman, 2013), our large international sample of firms based on 15 countries allows us to gain a more nuanced perspective on how the relationship between board expertise and environmental performance unfolds in different institutional contexts. The cross-country sample allows us to identify important institutional moderators—country-level stakeholder salience and the presence of environment-oriented legislation—which is likely to improve our understanding of when board environmental expertise is most likely to be effective.

Theoretical background and hypotheses

The advisory role of the board

While research has extensively argued that the board’s primary role is to monitor executives to curb their opportunistic behavior (Forbes and Milliken, 1999; Hambrick et al., 2015) and provide the necessary resources in the form of their personal ties and capital (Hillman et al., 2000; Pfeffer and Salancik, 1978), boards also play a critical advisory role (Bankewitz, 2018; Chen et al., 2020; Westphal, 1999). At the core of the advisory role is the idea that “the board draws upon the expertise of its members to counsel management on the firm’s strategic direction” (Adams and Ferreira, 2007: 218). Directors possess highly developed, complex decision-making and problem-solving skills in their respective domains of expertise, and these special capabilities arise from the nature of the knowledge that experts possess (Kor and Sundaramurthy, 2009; McDonald et al., 2008). Therefore, boards with the necessary expertise in a particular domain are likely to provide more effective guidance to a firm’s top management team and facilitate strategic change (Schnatterly et al., 2021).

Governance and strategy scholars have explored the relationship between directors’ expertise and firm strategy by examining how directors’ specialized knowledge can contribute to strategic decision-making. For example, Diestre et al. (2015) described the relevance of directors on the board who can provide expertise on specific markets and found that directors’ market experience increases the likelihood of market entry. Oehmichen et al. (2017) found that directors with greater industry expertise were associated with more strategic change. Moreover, they proposed that the relationship between board members providing expertise and strategic change is less pronounced in contexts where institutional quality requires directors to fill the void brought about by missing resources. Kirkpatrick (2009) argued that the presence of directors with financial expertise on banks’ boards could have mitigated excessive risks taken by management and potentially minimized the impact of the 2007–2008 financial crisis on these institutions. Using a grounded theory approach to underscore the importance of the advisory role, Boivie et al. (2021) interviewed directors and found that they placed more emphasis on their advisory role in setting firm strategy rather than on monitoring the firm’s top management.

Despite calls for more research on the board’s advisory role in the corporate governance and strategic organization fields (Dass et al., 2014; Tuggle et al., 2010), limited attention has been given to exploring how board expertise can effectively steer a firm’s management toward achieving superior environmental performance. Walls and Hoffman (2013) provide an important exception. Their research shows that boards of directors with specialized environmental experience are more likely to drive their firms to adopt proactive environmental practices that exceed institutional norms. However, we do not know much about the mechanisms through which board expertise leads to better environmental performance.

We aim to fill this research gap by relying on the board’s advisory role to theorize how boards of directors’ environmental expertise influence corporate environmental performance. We do so by building two main arguments. First, we argue that an important function of the board within its advisory role is to direct the firm’s attention toward its stakeholders, which is a prerequisite for building a commitment to environmental matters (Hart and Ahuja, 1996). Second, another way the board’s advisory role can play a significant part in affecting the firm’s environmental performance is that it bridges information gaps and provides accurate risk assessments that can enhance managerial action toward environment-related targets.

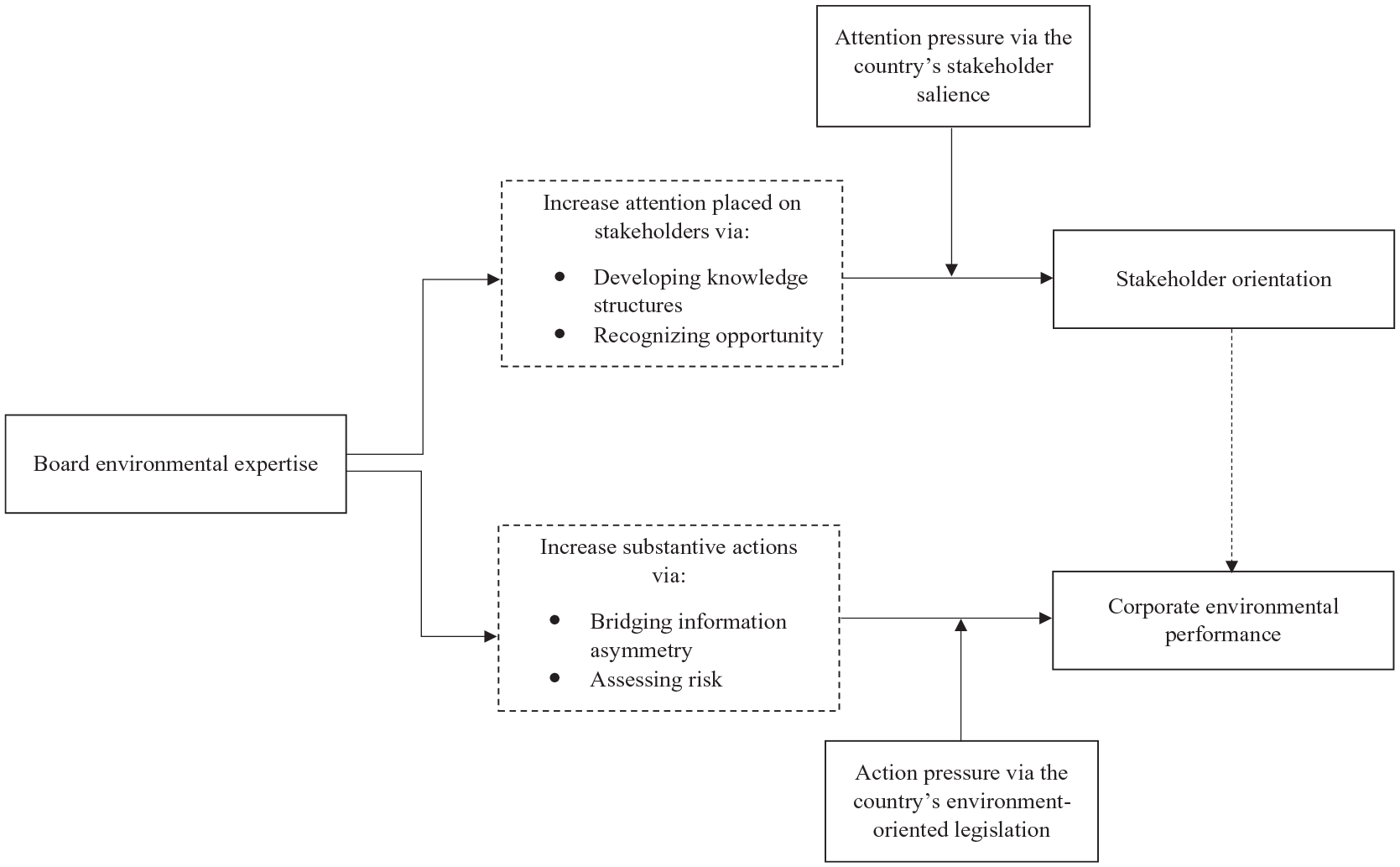

In the following sections, we extend previous research by theorizing on the importance of board environmental expertise and how it improves environmental performance through attention and action channels. In addition, we also consider the institutional context in which these effects unfold. We focus on stakeholder salience and environment-oriented legislation as important factors that create attention and action pressures, respectively. Our theoretical framework is presented in Figure 1.

Theoretical framework.

Board environmental expertise and stakeholder orientation

In his seminal work, Freeman (1984) defined stakeholders as “any group or individual who can affect or is affected by the achievement of the organization’s objectives” (p. 46). Stakeholder orientation, defined as the extent to which a firm integrates the interests of multiple stakeholders in its decision-making (Bettinazzi and Feldman, 2021), is paramount for the successful implementation of environmental strategies (Buysse and Verbeke, 2003). For example, Henriques and Sadorsky (1999) stress that successful environmental strategy implementation requires firms to work closely with stakeholder groups and to understand their perspective on environmental issues. Similarly, Bansal and Clelland (2004) emphasize the importance of environmental performance conforming to stakeholders’ expectations in order to gain environmental legitimacy. Berrone and Gomez-Mejia (2009: 107) highlight that effective environmental strategies are “complex and risky” and “involve diverse stakeholders at different levels,” thus requiring expertise on the board to mitigate risk. The importance of addressing stakeholders’ interests is also underscored by social movement theorists, who emphasize that collective action is necessary to create social change and to influence firms to improve their environmental performance (King and Jasper, 2022; Vasi and King, 2012).

The growing awareness of environmental sustainability among a broad spectrum of stakeholders has placed the environment at the top of the agenda for many stakeholders. At the same time, environmental sustainability is a topic that affects almost all stakeholders. Therefore, solutions regarding environmental issues frequently require considering multiple stakeholders and cannot be solved by focusing on only one stakeholder group. This heightened and also encompassing awareness is compelling firms and their leadership to pay closer attention to the needs of stakeholders and prioritize efforts to enhance environmental performance (Guerci et al., 2016; Kassinis and Vafeas, 2006). In summary, to advance environmental performance, a firm should pay attention to its broad set of stakeholders and integrate their interests by calling on board experts to assess the risks involved.

We argue that board environmental expertise will facilitate a firm’s stakeholder orientation by directing focused and sustained corporate attention toward the stakeholders through the following two mechanisms: (1) developing the knowledge structures of decision-makers and (2) recognizing opportunities to cater to a broader set of stakeholders. According to Walsh (1995), a knowledge structure can be viewed as a mental template that individuals use to organize and give meaning to an information environment. In this sense, it serves as a cognitive framework that allows individuals to make sense of new information and integrate it into their existing knowledge (Shepherd et al., 2017). Directors with environmental expertise can develop the knowledge structures of decision-makers by clarifying the expected relationships between the firm and its stakeholders in terms of the goal salience, behaviors, and actions required to maintain those relationships. They can also ensure that management devotes appropriate effort to effectively address stakeholders’ interests.

Another way board environmental expertise is likely to improve firm attention toward stakeholder orientation is by identifying opportunities for meeting the interests of various stakeholders to enhance environmental performance. Opportunities exist in the external environment (Grégoire et al., 2010), requiring a nuanced understanding of the stakeholder landscape. Boards with environmental expertise are equipped with specialized knowledge and skills that uniquely prepare them to recognize opportunities for engaging with stakeholders. As managers are confronted with a multitude of demands, and given their limited attentional capacity, they focus selectively on the topic(s) and groups they consider important (Golden and Zajac, 2001; Ocasio, 1997). Much of their focus is narrowly targeted toward the maximization of shareholder interests, which creates a blind spot for advancing long-term social agendas (King and Lenox, 2002). Directors with environmental expertise have the relevant cognitive capacity to understand the need to address a broader set of stakeholders, such as governments, the community at large, and investors, and to identify meaningful patterns that may lead to new opportunities.

As such, boards with greater environmental expertise are more likely to direct firm attention toward stakeholders by enhancing the relevant knowledge structures and identifying opportunities to meet stakeholders’ needs, which, in turn, are prerequisites for firms’ environmental performance. This leads to the first hypothesis:

H1. There is a positive association between board environmental expertise and a firm’s stakeholder orientation.

Board environmental expertise and corporate environmental performance

We contend that board environmental expertise is positively associated with corporate environmental performance as it enables the management to take substantive actions toward improving environmental performance. We propose two mechanisms in this regard. First, board environmental experts effectively bridge the information asymmetry between the firm and its ecological environment (Dass et al., 2014). Leveraging their expertise and command of environmental matters, these experts contribute to overcoming information gaps by predicting environmental developments, and understanding regulatory laws and policy changes. This, in turn, mitigates uncertainty and enables management to align more effectively with stakeholder concerns regarding environmental norms (Haynes and Hillman, 2010). Consequently, we posit that an environmental expert brings critical information to the boardroom, enhancing the willingness of other board members and top managers to take substantive actions to improve environmental performance (Durand et al., 2019).

Furthermore, board environmental experts also play a vital role in improving corporate environmental performance by enhancing management’s ability to take substantive actions (Durand et al., 2019). These experts are prepared to accurately assess the risks and perform a cost–benefit analysis of investing in pro-environmental actions, such as emission reduction, pollution abatement, resource reduction, and environmental innovation. Previous research suggests that such investments can be risky because of the lag between initiating such actions and realizing their benefits (Aguilera et al., 2021; Hart and Ahuja, 1996). Dowell and Muthulingam (2017) note that decision-makers often shy away from adopting environmental initiatives due to the significant investments required to upgrade a firm’s production line, equipment, and human capital, with benefits that may not be immediately apparent and may only materialize in the long term. Similarly, as Berchicci and King (2007) noted,

“the difficulty of evaluating the value (and cost) of environmental performance weakens the force of objective analysis and encourages managers to resort to rules of thumb. Biases in these heuristics then cause some types of profit opportunities to be overlooked systematically” (p. 524).

However, a more environmentally knowledgeable board can conduct a more accurate assessment of risks and opportunities in environmental actions, along with a cost–benefit analysis of resource mobilization, which enhances the ability of the management to act (Durand et al., 2019).

In sum, by influencing management to take substantive environmental initiatives, firms with higher board environmental expertise are likely to have better environmental performance. Therefore, we hypothesize:

H2. There is a positive association between board environmental expertise and corporate environmental performance.

The role of the institutional context

If increased attention and increased action are the underlying mechanisms of our main relationship, we would expect them to be specifically pronounced in contexts where either one of them is specifically needed. We build this theorizing on the idea that firms are economic entities that operate within institutional contexts that shape their behavior and impose expectations on them, including environmental performance (Campbell, 2007; Hartmann and Uhlenbruck, 2015). Research based on institutional and neo-institutional perspectives has also documented that firms’ attention and actions vary across macro-institutional contexts due to differences in institutional logics (Ioannou and Serafeim, 2015; Martínez-Ferrero et al., 2016). For example, Ocasio (1997) noted how “the situation shapes individuals’ focus of attention and how, through this focus of attention, the situation influences individuals’ actions” (p. 191). Thus, the level of firm attention on stakeholders could also be affected by the countries’ institutional context. In addition, the likelihood of firms undertaking substantive actions to foster environmental sustainability also depends on country-level institutions (Ortiz-de-Mandojana and Bansal, 2016). For example, Marquis et al. (2016) found that firms avoided symbolic actions (i.e. appearing to be committed) toward the environment when they operated in civil societies that were more likely to mobilize citizens and speak up to limit symbolic activity. In another study, Pucheta-Martínez et al. (2019) found that firms located in liberal and developed economies were more likely to disclose environmental information.

Based on these arguments, we posit that in order to understand how board environmental expertise drives firms’ attention toward stakeholders and substantive actions to improve environmental performance, it is essential to consider the institutional context in which the effect unfolds. In this regard, we focus on countries’ stakeholder salience and environment-oriented legislation, and argue that the former generates an attention pressure toward stakeholders and the latter creates an action pressure toward substantive actions to improve environmental performance.

Stakeholder salience in a country can be defined as a measure of the perceived power, legitimacy, and urgency of stakeholders at societal levels (Tashman and Raelin, 2013). Variations in the roles of stakeholders exist within different national institutional environments, leading to differences in the perception of stakeholders’ importance (Ioannou and Serafeim, 2012; Jackson and Apostolakou, 2010). In countries with high stakeholder salience, there is a heightened expectation from the external environment and civil society that the firm should recognize and meet the unique interests of various stakeholders (Crilly, 2011). Thus, the issue of enhancing stakeholder orientation will become more salient to those board environmental experts in countries with high stakeholder salience, and the pressure for environmental attention will become even higher, facilitating the attention task of the environmental expert. Therefore, we expect that board environmental experts will face higher attention pressure to direct corporate attention toward stakeholders. Thus, we hypothesize:

H3. The positive association between board environmental expertise and a firm’s stakeholder orientation is strengthened in countries with a higher level of stakeholder salience.

We also posit that environment-oriented legislation serves as an important contextual factor that creates an action pressure for board environmental experts to push firms to engage in substantive environmental action. Regulatory pressures imposed by laws and rules often create a sense of urgency and accountability for decision-makers to take active measures toward environmental sustainability (Chan and Welford, 2005; Ortiz-de-Mandojana and Bansal, 2016). These pressures, formalized in the form of legal sanctions, guide organizational actions toward compliance and deter firms from noncompliance (Kostova and Zaheer, 1999). As such, board environmental experts are incentivized to bridge information gaps, provide risk assessments, and push decision-makers to take substantive environmental action due to the threat of penalties, as well as the potential reputational damage associated with noncompliance. Therefore, environment-oriented legislation serves as a critical institutional factor that increases the pressure on board environmental experts to foster substantive actions toward environmental sustainability. Formally:

H4. The positive association between board environmental expertise and corporate environmental performance is strengthened in countries with a higher level of environment-oriented legislation.

Methods

Sample and data

To test our hypotheses, we used a multi-country sample consisting of firms from the United States, Canada, and 13 European countries, namely Cyprus, Denmark, Finland, France, Germany, Greece, Italy, the Netherlands, Norway, Spain, Sweden, Switzerland, and the United Kingdom. The sample was created by matching publicly available data from archival sources, such as BoardEx, Thomson Reuters’ ASSET4 ESG, and Datastream. We excluded firms from the financial service industry (SIC 6000–6999) due to their unique regulatory environment and the particularities of their assets and liabilities, which may affect the relationship between accounting numbers and market value (Clacher et al., 2013; Dahmash et al., 2009). In addition, many environmental policies do not apply to this industry (Eccles et al., 2014). After removing observations with missing data, our final sample comprised an unbalanced panel of 1517 unique firms and 11,634 firm-year observations from 2003 to 2016.

Main variables and measures

Board environmental expertise

We calculated information on the environmental expertise of directors from BoardEx. Based on prior work by Walls and Hoffman (2013), we collected comprehensive information about each director’s experience regarding environmental issues, which was then aggregated at the board level. To gauge a director’s expertise in environmental matters, we leveraged information on any accolades or awards they may have received for their environmental initiatives, their involvement in environment-related activities at non-corporate institutions, such as foundations, non-governmental organizations (NGOs), government entities, and local communities, their past employment history, and memberships in board subcommittees specifically focused on environmental matters.

To extract information on relevant environmental awards, activities, employment, and board positions in subcommittees held by directors, we conducted searches using specific keywords related to environmentalism, such as “environment,” “ecology,” “nature,” “sustainable,” “remediation,” “renewable,” “pollution,” and “energy,” including variations of the words, such as “ecological” instead of “ecology” or “sustainability” instead of “sustainable.” Because the automated search for these keywords also leads to outcomes not relevant to environmental expertise (e.g. positions related to “gynecology” when searching for “ecology”), we manually reviewed the coded material and removed any items that were irrelevant or misrepresented the director’s environmental experience. After that, we created a dummy variable for each of the four categories to indicate whether a director had experience in that area. Thus, a director could have a maximum value of 4. We then summed up the expertise scores of all supervisory directors on the focal board for each year in the dataset.

Corporate environmental performance

Corporate environmental performance assesses the impact of a firm’s operations and products on the ecosystem. Following previous research, we used the Thomson Reuters ASSET4 ESG database to obtain information on a firm’s environmental performance (e.g. Baboukardos, 2018). ASSET4 provides auditable and systematic information about environmental issues in the form of 71 performance indicators for over 4000 global public companies. A primary advantage of the ASSET4 data is its broad and longitudinal coverage, sourced from a variety of different sources, including annual reports, sustainability reports, NGO websites, and firm surveys. In addition, the ASSET4 database’s selection methodology differs from that of other ESG (environmental, social, and governance) databases, as it is based on market capitalization rather than sustainability performance (Bettinazzi and Zollo, 2017). This partly mitigates potential self-selection biases, which could result in biased coefficient estimates, whereas a disadvantage is sometimes seen in ASSET4 being partly based on corporate disclosure and therefore depending on firms’ sincere reporting.

We used the corporate environmental performance score in ASSET4. It is based on the average of the following three environmental categories: emission reduction, resource reduction, and environmental innovation; each ranging from 0 to 100, with higher values indicating better corporate environmental performance. The emission reduction category score reflects a firm’s capability to reduce environmental emissions in its production and operational processes. The score assigned to the resource use category indicates a firm’s effectiveness in minimizing the consumption of resources, such as materials, energy, and water, and finding eco-friendly alternatives by enhancing its supply chain management. Finally, the environmental innovation category score reflects a firm’s ability to lower the environmental impact and costs for its customers, which in turn creates new market opportunities through the development of new environmental technologies and processes or eco-friendly products.

Stakeholder orientation

We used Bettinazzi and Feldman’s (2021) approach to measure stakeholder orientation, focusing on a firm’s orientation toward the following five key stakeholder categories: employees, customers, suppliers, local communities, and shareholders. To assess each category, we relied on the ASSET4 database, which provides the most comprehensive information on the extent to which a firm’s management implements practices to address the specific groups of stakeholders and integrates their interests into the firm’s decision-making. For employee orientation, we used 10 dummy items (e.g. does the company monitor or measure its performance on employment quality?); for customer orientation, we used six dummy items (e.g. does the company have a policy to strive to be a fair competitor?); for supplier orientation, we used five dummy items (e.g. does the company have a policy to treat suppliers and contractors as key business partners?); for community orientation, we used nine dummy items (e.g. does the company monitor its reputation or its relations with communities?); and for shareholder orientation, we used four dummy items (e.g. does the company monitor shareholder rights?).

We normalized the scores for each stakeholder category on a scale from zero to one, and then calculated the average of the normalized scores for the five categories. This approach allows us to capture variations in stakeholder orientation, which can range from low (indicating that the firm pays attention to fewer stakeholders) to high (suggesting that the firm is attentive to more stakeholders).

Moderating variables

National stakeholder salience

We assessed the level of stakeholder salience at the national level using a principal factor analysis of four metrics proposed by Dhaliwal et al. (2012). These metrics gauge different aspects of a country’s institutional framework that influence stakeholder focus, including (1) the legal framework for safeguarding labor rights and benefits, (2) the presence of disclosure laws that reflect societal expectations regarding sustainability matters, (3) the extent of public awareness of sustainability issues, and (4) the attitudes of corporate executives toward sustainability activities. These four metrics signify the significance that a country accords to its diverse stakeholder groups. A higher value for this measure implies a greater degree of stakeholder salience for the country in question.

Environment-oriented legislation

We assessed the level of regulatory pressure regarding environmental topics at the national level using the power of the national green party in each country (Hennig et al., 2020). As part of national parliaments and thus of the representation of the people, national green parties have the ability to initiate and enforce regulations regarding environmentalism, including charges, sanctions, and regulatory standards. We collected data from websites and press releases on the outcomes of national elections to identify the power of green parties in the different institutional environments. Specifically, we employed the percentage of overall seats won in the last national election.

Control variables

We included a number of time-varying control variables in our analyses. At the firm level, we controlled for financial performance using the firm’s annual return on assets, and firm size, calculated as the natural logarithm of the total assets. Previous literature suggests that larger firms typically have deep pockets and are more likely to focus on long-term initiatives such as environmental performance (Berrone et al., 2010; Flammer and Bansal, 2017). Similarly, profitable firms are also more likely to have better environmental performance (Iatridis, 2013). We included financial slack, calculated as cash divided by total assets, because firms with greater financial resources are likely to invest more in environmental performance (de Villiers et al., 2011). We also controlled for capital expenditures, measured as capital expenses divided by total assets, because this can have an impact on environmental damage and firms’ responses to it (Marquis et al., 2016). To account for a firm’s debt structure, we controlled for firm leverage by calculating the logarithm of long-term debt to total assets (Homroy and Slechten, 2019). In line with previous research, we also accounted for firms’ sales growth, measured as a 1-year change in sales (Walls et al., 2012). We further controlled for institutional investors’ monitoring by calculating the percentage of shares held by institutional investors among the largest owners (institutional ownership).

To isolate the effects of governance effectiveness, we controlled for board size as the number of supervisory directors on the board. Larger boards may have an advantage when providing expertise as part of their advisory role (Chancharat et al., 2012). In the same vein, we controlled for board independence as the percentage of outsiders on the board, and board busyness as the proportion of independent directors who held three or more directorships outside the focal company. Both variables are linked to effective board functioning, and can potentially influence environmental performance (Boivie et al., 2016). We also controlled for the average board tenure due to its association with directors’ general experience (Hafsi and Turgut, 2013).

In order to capture industry influences on environmental performance, we created a dummy variable of environmentally sensitive industries, with a value of 1 for firms with the primary SIC (standard industry classification) codes of mining, oil exploration, paper, chemical and allied products, petroleum refining, metals, or utilities, and zero otherwise. On the country level, we controlled for shareholder rights (country shareholder rights), as they are often considered as an opposing force regarding broader stakeholder orientation and environmentalism (Jensen, 2001; Sundaram and Inkpen, 2004) by including the Anti-Director Rights Index proposed by La Porta et al. (1998). 2 Finally, we accounted for time effects by including year dummies.

Model specification

To assess the main effects, we conducted a panel regression analysis at the firm-year level using random effects. Thereby, we follow (Walls et al., 2012), as we are interested in both within- and between-firm variance to explain the postulated relationships. In addition, regarding the within-firm variance, we know from prior studies and excerpts of our own data that our variables of interest are highly sticky over time, which makes it next to impossible to estimate firm fixed-effects regressions (Certo et al., 2017). We estimated all models with robust standard errors. To attenuate concerns about reverse causality or simultaneity between board expertise and environmental performance, we forwarded the latter by 1 year.3,4 As a post hoc analysis, we examined the impact threshold of a confounding variable (ITCV) to address concerns about a potentially omitted variable bias driving our results (Busenbark et al., 2022). In unreported tests (available upon request), we run OLS (ordinary least squares), GEE (generalized estimating equations), and firm fixed-effects models, which widely confirm our results.

Results

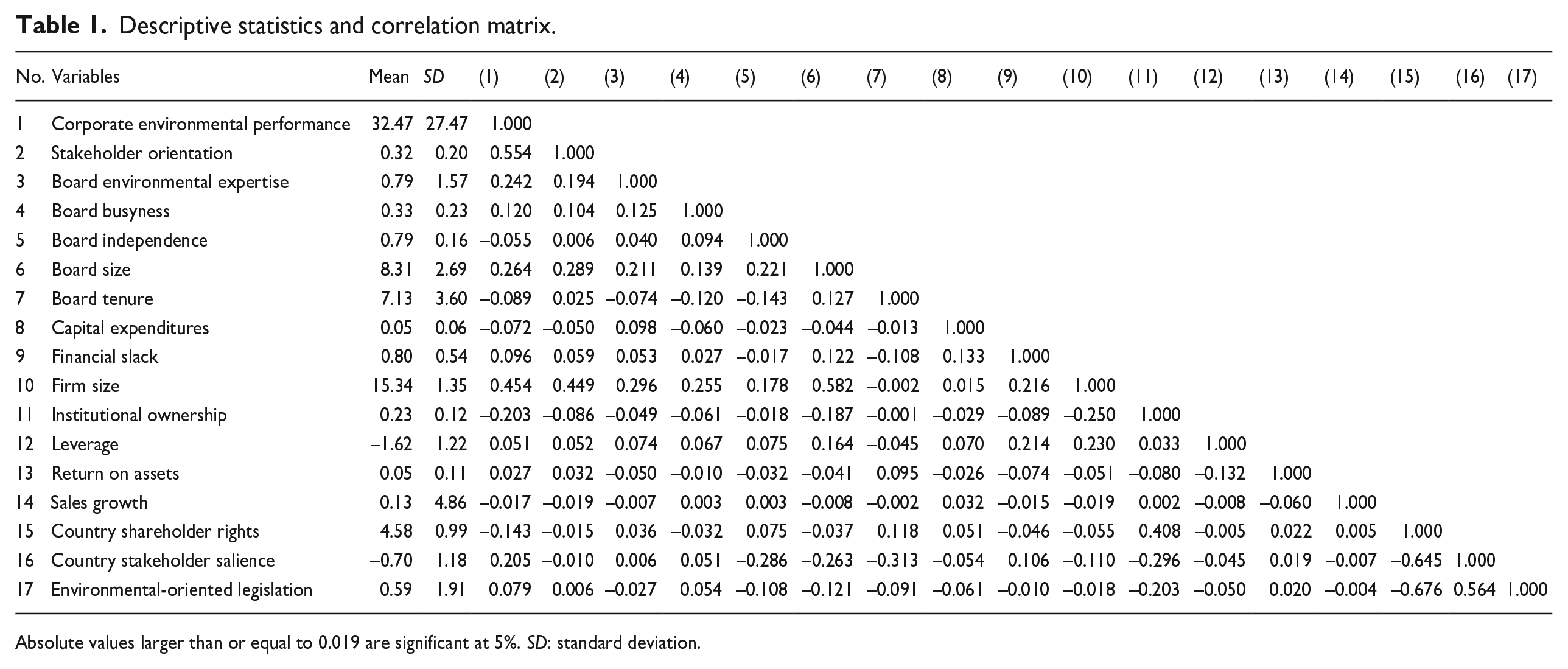

Table 1 displays the descriptive statistics and correlations for the variables in our models. Our main variable of environmental expertise has a mean of 0.79, indicating that environmental expertise is scarce on boards. At the same time, the standard deviation of 1.57 shows quite some variation in its degree. The positive and significant correlations between board environmental expertise and corporate environmental performance, as well as stakeholder orientation, already provide the initial indications for our first two hypotheses. The correlations, in general, suggest that multicollinearity should not be of high concern, except between corporate environmental performance and stakeholder orientation. For this reason, we used these variables in separate regression models. However, if we test the assumed relationship between stakeholder orientation and corporate environmental performance, we find the expected positive and significant relationship (results available upon request). The variance inflation factor (VIF) for all variables was less than 5 and thus below common thresholds.

Descriptive statistics and correlation matrix.

Absolute values larger than or equal to 0.019 are significant at 5%. SD: standard deviation.

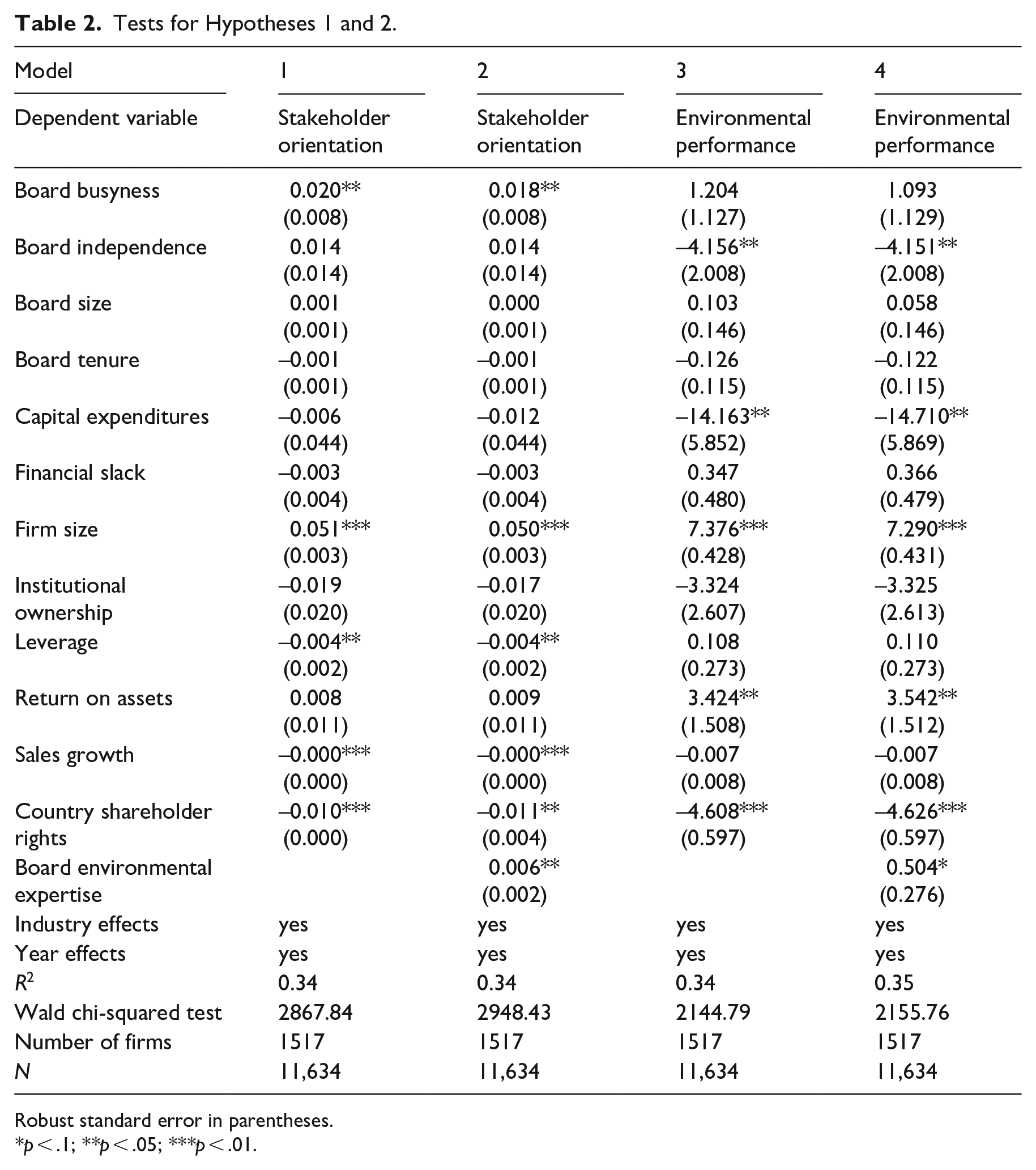

Table 2 presents the results of the regressions testing Hypotheses 1 and 2. Model 1 is the baseline model for Hypothesis 1, which only includes the control variables and the dependent variable (i.e. stakeholder orientation). We find that larger firms with busier and thus better-connected directors positively relate to firms’ stakeholder orientation, whereas fast-growing firms in countries with stronger shareholder rights tend to engage less in stakeholder orientation. In Model 2, we add our explanatory variable (i.e. board environmental expertise) and find a positive and significant coefficient. The results thus support Hypothesis 1 of a positive relationship between boards’ environmental expertise and firms’ stakeholder orientation.

Tests for Hypotheses 1 and 2.

Robust standard error in parentheses.

*p < .1; **p < .05; ***p < .01.

Model 3 is the baseline model for Hypothesis 2 and thus tests the dependent variable, corporate environmental performance. We observe that larger, more profitable firms have higher environmental performance, while more capital-intensive firms tend to score lower in environmental performance. In Model 4, we include board environmental expertise, for which we find a positive and significant coefficient. Thus, we find evidence for Hypothesis 2 of a positive relationship between boards’ environmental expertise and firms’ environmental performance.

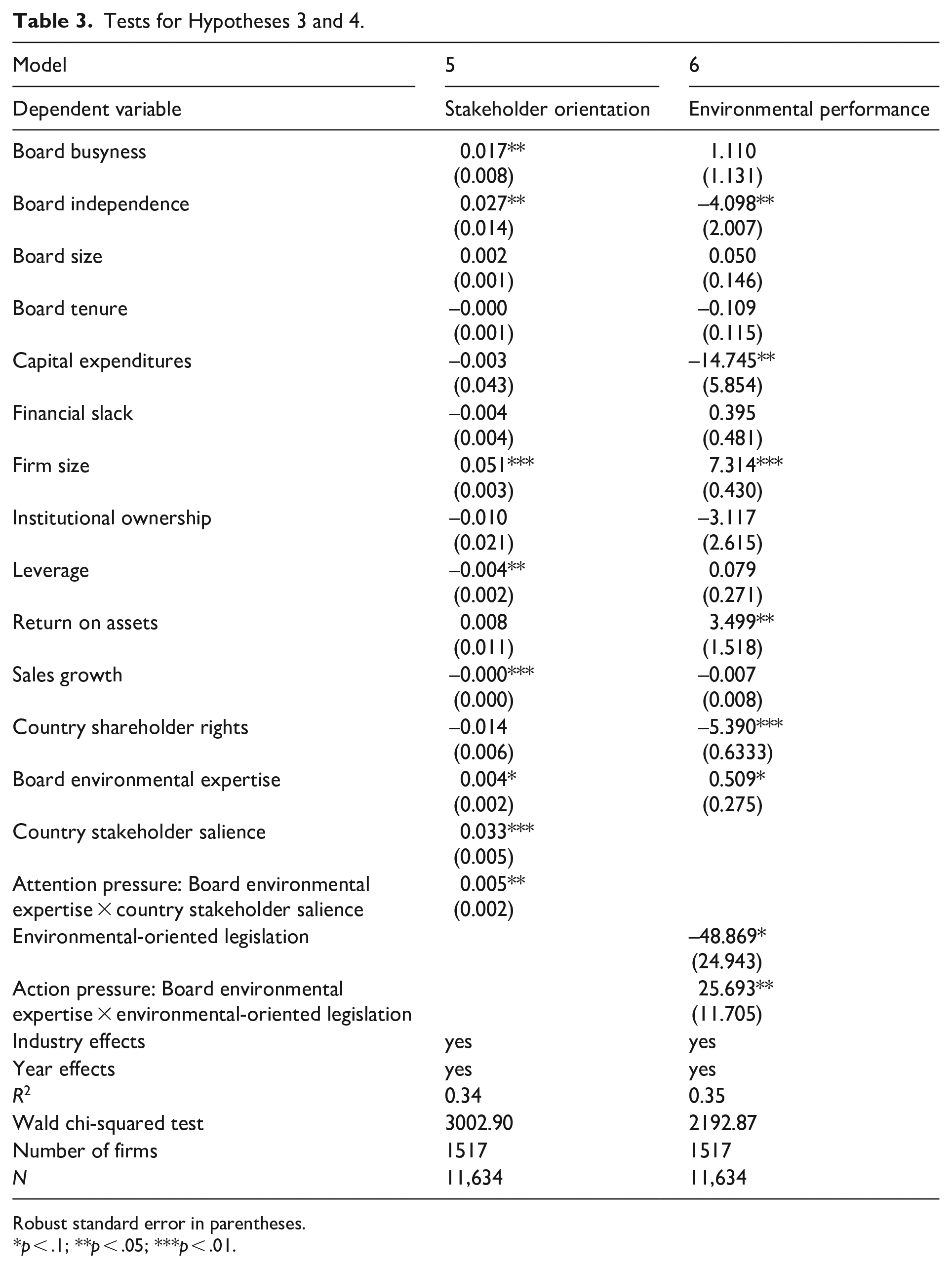

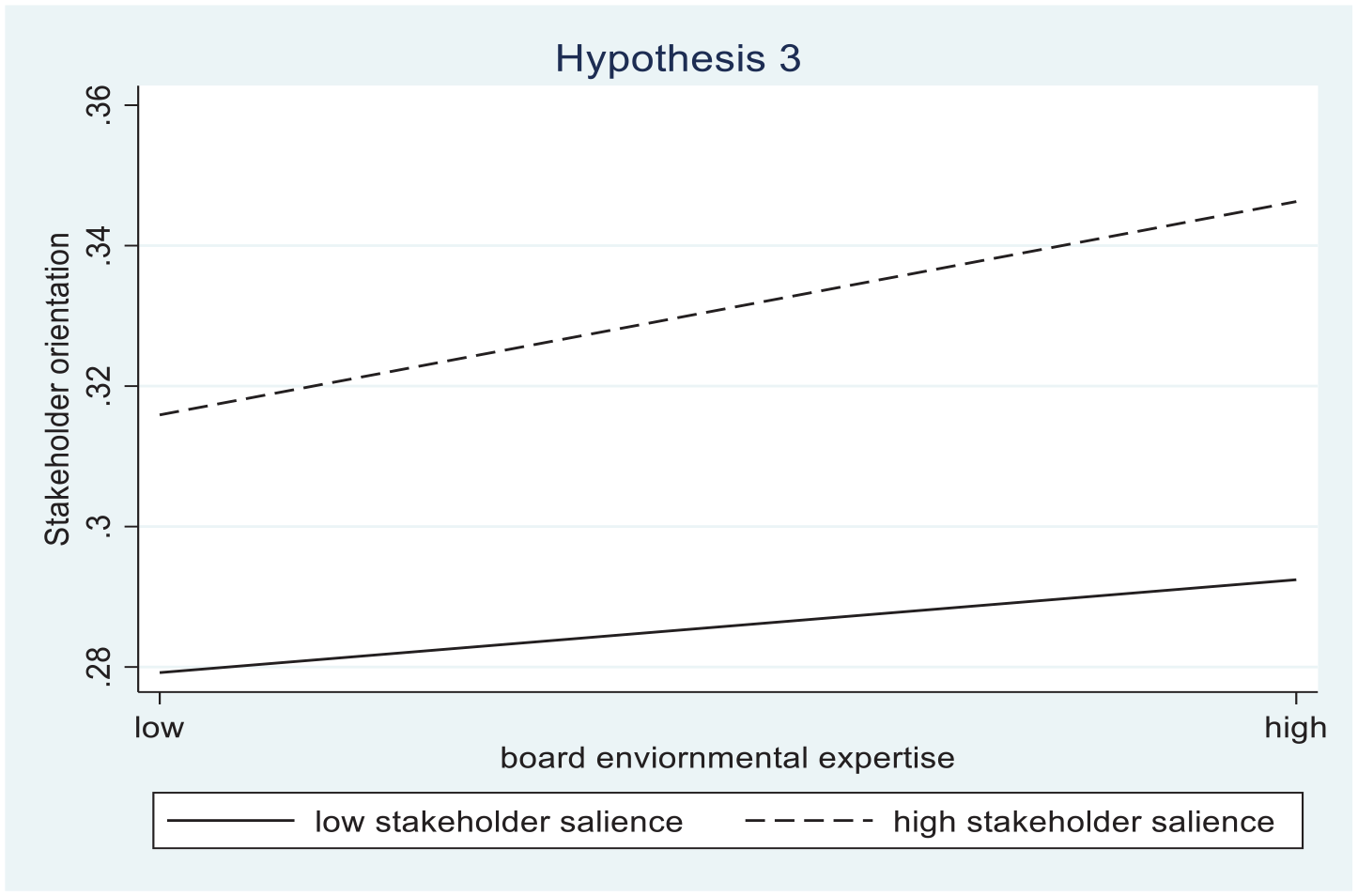

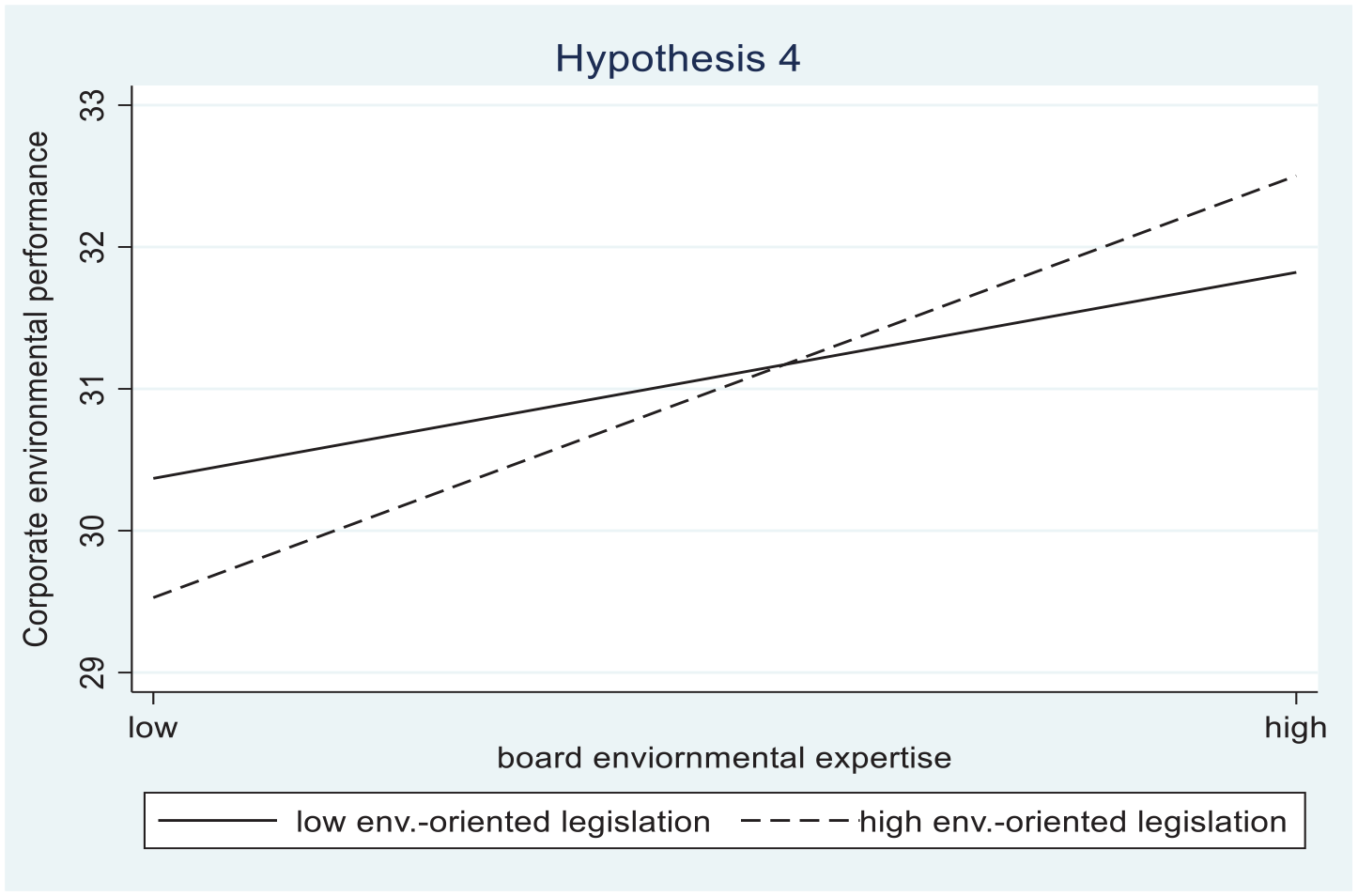

Table 3 shows our moderation analyses. In Model 5, we test Hypothesis 3, in which we propose that stakeholder salience in firms’ institutional context positively moderates the positive relationship between boards’ environmental expertise and firms’ environmental performance. In line with our theoretical considerations, we observe a positive moderating effect. In other words, the results underline the increased attention effect in institutional contexts with higher stakeholder salience. Figure 2 further illustrates this result. In Model 6, we investigate Hypothesis 4, which proposes that environment-oriented legislation positively moderates the positive relationship between boards’ environmental expertise and firms’ environmental performance. Supporting the hypothesis, we find a positive and significant coefficient for the interaction term. Thus, our results demonstrate that our theorized action effect is stronger in institutional contexts with stronger environmental-oriented legislation. Figure 3 further illustrates this result.

Tests for Hypotheses 3 and 4.

Robust standard error in parentheses.

*p < .1; **p < .05; ***p < .01.

Plot of Hypothesis 3.

Plot of Hypothesis 4.

Supplementary analyses

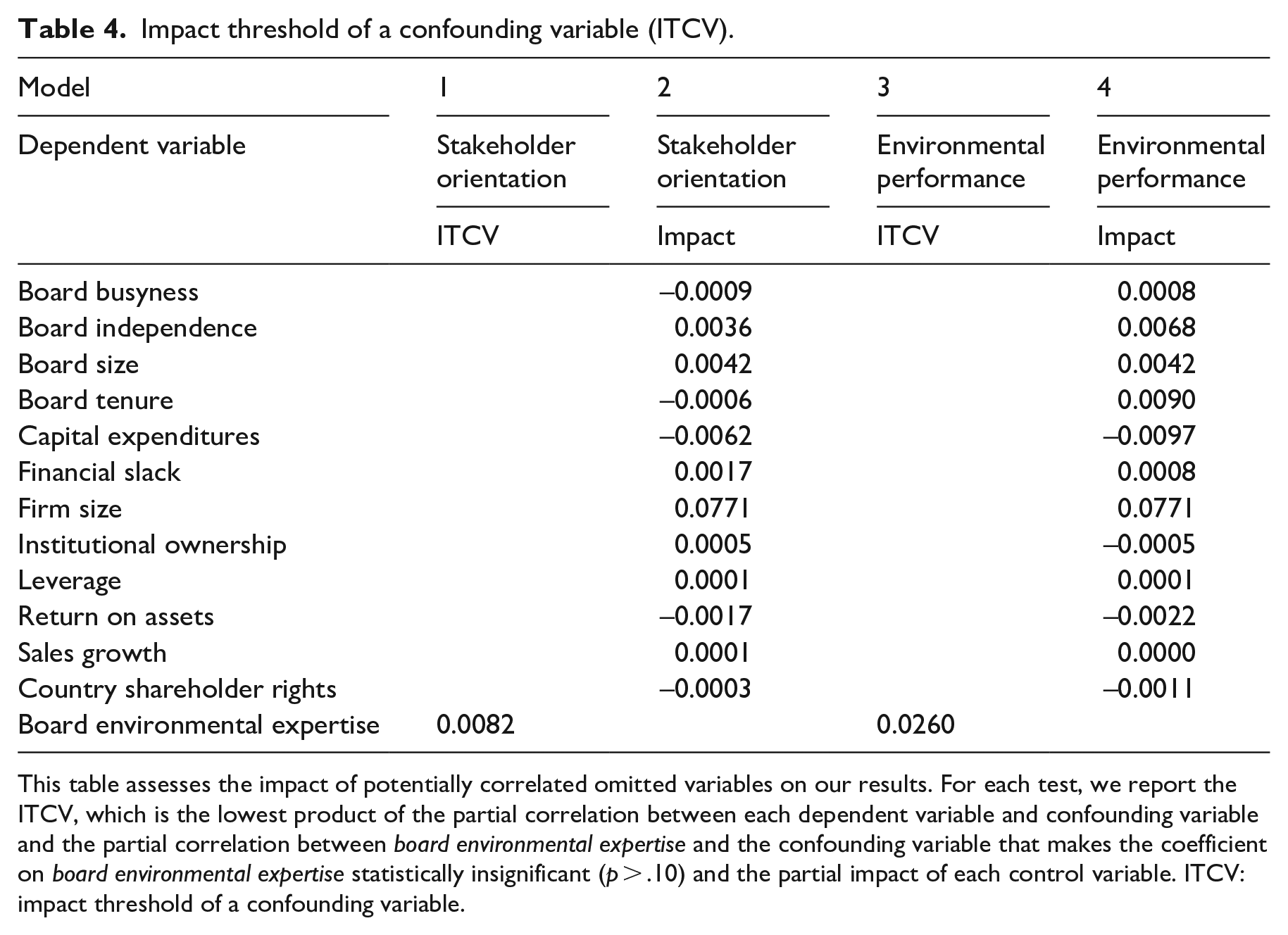

Impact threshold of a confounding variable (ITCV)

The risk of omitted variables confounding the results has long been recognized in the management literature (Hill et al., 2021). However, as it is next to impossible to rule out all potential sources of omitted factors, researchers have recently advocated for a more pragmatic approach (Busenbark et al., 2022). The ITCV calculates the extent to which a confounding variable would need to be correlated with both factors—the independent and dependent variables—to make the coefficient statistically insignificant and, thus, to alter the results (Frank, 2000). We follow this approach, which has been widely applied in recent literature (e.g. Harrison et al., 2018; Hennig et al., 2022; Lee, 2020; Lovelace et al., 2022) by using the konfound command in Stata. Table 4 reports the results. In line with Larcker and Rusticus (2010), we compare the ITCV with the impact of our control variables. The results suggest that a potential omitted variable would have to be correlated more strongly with both board environmental expertise and stakeholder orientation or corporate environmental performance, respectively, than any of the control variables in the regression models, except firm size. Given the large predictive power of firm size for a plethora of firm characteristics (e.g. board environmental expertise) and outcomes (e.g. stakeholder orientation and board environmental expertise), we are confident that it is very unlikely that our results can be confounded by an omitted, correlated variable.

Impact threshold of a confounding variable (ITCV).

This table assesses the impact of potentially correlated omitted variables on our results. For each test, we report the ITCV, which is the lowest product of the partial correlation between each dependent variable and confounding variable and the partial correlation between board environmental expertise and the confounding variable that makes the coefficient on board environmental expertise statistically insignificant (p > .10) and the partial impact of each control variable. ITCV: impact threshold of a confounding variable.

Stakeholder orientation as a link between board environmental expertise and corporate environmental performance

At the core of our article, we focus on the attention-related and action-related outcomes of boards’ environmental expertise in the form of firms’ stakeholder orientation and environmental performance. In our theorizing, the arguments implicitly build on the assumption that firms’ stakeholder orientation as a critical outcome of boards’ environmental expertise, in turn, might help firms to obtain higher environmental performance. In this supplemental analysis, we test this implicit assumption. The results (available upon request) complete the picture of stakeholder orientation as the link between environmental expertise and environmental performance. From our main analysis, we know that board environmental expertise is positively and significantly related to stakeholder orientation and corporate environmental performance. The results of this analysis show that stakeholder orientation is positively and significantly related to corporate environmental performance. Thus, the results complete the picture by adding the missing link.

Discussion

Due to the urgency and intensity of public policy interest in environmental challenges, such as biodiversity loss, climate change, global warming, and an increased carbon footprint, ensuring sound environmental performance constitutes a grand challenge for firms today. Directors with environmental expertise have the necessary domain-specific knowledge acquired from their prior experience to advise management on tackling this grand challenge. Whereas prior research has offered views as to whether board experience in environmental matters leads to better environmental performance (Homroy and Slechten, 2019; Walls and Hoffman, 2013), our study sought to extend this budding stream of literature to theorize on the specific mechanisms associated with how board environmental expertise influences corporate environmental performance.

We theorized that board environmental experts, as part of their advisory role, enhance environmental performance through two channels: attention and action. First, through the attention channel, environmental experts increase the firm’s orientation toward stakeholders, which is vital to attaining the desired level of environmental performance (Kassinis and Vafeas, 2006). Board environmental experts develop the knowledge structures of decision-makers and identify opportunities to cater to a broader set of stakeholders, which will increase firm attention toward stakeholders. Second, through the action channel, board environmental experts push decision-makers to take substantive actions in order to be more environmentally conscious. Board environmental experts reduce information asymmetry and assess risk to increase management’s willingness and ability to invest in uncertain environmental initiatives (Durand et al., 2019). Our predictions were supported by empirical analyses of 1517 unique firms and 11,634 firm-year observations from 2003 to 2016. Specifically, the results indicate that board environmental expertise is positively associated with stakeholder orientation and environmental performance.

Furthermore, we find an important role for the institutional context in the form of countries’ stakeholder salience and environment-oriented legislation. We find that countries’ stakeholder salience positively moderates the relationship between board environmental expertise and stakeholder orientation. This is in line with our expectation of the attention pressure that environmental experts face in directing firm attention toward a broader set of stakeholders. This finding can be explained by the fact that environmental experts in countries with higher stakeholder salience face increased expectations regarding the difficulties in directing managerial attention toward stakeholders. We also found that in countries with higher environment-oriented legislation, the board environmental experts’ influence on corporate environmental performance is stronger. This may be due to the higher pressure to engage in the substantive actions these experts face in ensuring that their respective firms have a sound environmental footprint. Thus, in these countries, environmental experts could have a greater chance of directing managerial attention and action toward ensuring better corporate environmental performance.

Implications for theory

Our findings have some important theoretical implications for research at the nexus of corporate governance, strategy, and environmental performance (Walls et al., 2012; Wiersema and Koo, 2022; Zaman et al., 2022). First, we contribute to the literature by providing detailed insights into the mechanisms through which board environmental experts create attention and initiate action toward environmental matters. There has been emerging literature on corporate governance structures and their influence on corporate environmental performance (de Villiers et al., 2011; Karn et al., 2022; Kock et al., 2012; Post et al., 2011). While these studies point to different effective corporate governance characteristics in the context of environmental matters, we lack a deeper understanding of how the described corporate governance mechanisms unfold their effects on environmental performance. Our findings respond to the increasing calls for research to elucidate processes through which directors, as strategic decision-makers, manage the firm’s attention toward a broader set of stakeholders needed for better environmental performance (Boivie et al., 2021).

Second, our study highlights the importance of the board’s advisory role, particularly in the context of environmental expertise. Much of the prior research has commonly drawn on agency theory to highlight the board’s monitoring role in curbing managerial opportunism (e.g. Boivie et al., 2016; Haynes and Hillman, 2010; Oehmichen et al., 2017). We emphasize the advisory role of the board with which boards effectively guide strategic decision-making (Schnatterly et al., 2021). Specifically, we theorize that by developing the necessary knowledge structures, identifying the relevant opportunities in the stakeholder landscape, bridging information gaps, and assessing the risks of making pro-environment investments, board experts can direct managerial attention toward stakeholders and push them to take substantive actions to improve environmental performance.

Finally, our study provides cross-country empirical evidence of board environmental expertise influencing corporate environmental performance. Our large international sample based on 15 countries allows us to gain a more nuanced perspective on how the relationship between board expertise and environmental performance unfolds in different institutional contexts. This makes an important contribution to research on the interface between firm-level corporate governance mechanisms and country-level institutions, as we highlight how the environmental expertise among firm-level corporate governance actors has to go hand in hand with an environmentally favorable institutional environment to be most effective.

Implications for practice

Our findings have significant implications for policymakers, board chairs, and other decision-makers seeking to address environmental issues. Policymakers can assess whether corporations—major contributors to environmental degradation—are equipped with the expertise to enable them to pay the necessary attention and take the necessary actions to be environmentally responsible. Expertise is not only relevant to orient firms to perform better environmentally, but also to monitor such performance. At the same time, our study also shows policymakers that having appointed environmental experts on corporate boards is not enough. These experts still need a nourishing environment—with respect to environmental attention and action—to be successful in their job.

Our findings are also relevant to board chairs and other critical decision-makers. The nomination of environmental experts, resulting in stakeholder orientation and increased environmental performance, is likely to help firms gain stronger legitimacy. In addition, an increasing number of managers are joining causes that promote stakeholder-oriented goals (such as the Business Roundtable) and thus are diverging from traditional shareholder primacy. At the same time, an increasing number of investors are pushing for long-term-oriented corporate behavior. We show that the composition of the board and the nomination of environmental experts, in particular, can be the right measure to address these concerns.

While it is already a valuable insight for owners and stakeholders to have identified directors with environmental expertise as a way to resolve environmental challenges, we also show that we should not just stop at appointing these experts. Instead, we also need to generate an institutional playing field that allows them to prosper. We need to build contextual settings that support these experts in being effective. Alone, they cannot be the cure for everything. Hence, our general message to shareholders and stakeholders is that for environmental performance to be high, knowing who is in charge matters, but what context they are in also matters.

Limitations and future research

Our findings are subject to certain limitations that also provide avenues for future research. First, in calculating stakeholder orientation (Bettinazzi and Feldman, 2021), we assigned equal weight to all stakeholders. However, it is possible that specific stakeholders, such as local communities or governments, wield more influence and can put more pressure on firms (Kassinis and Vafeas, 2006), prompting the board to prioritize them. Future research should delve deeper into this aspect by examining how the board responds to particular stakeholder groups regarding specific environmental decisions or scandals.

Second, while our focus on stakeholder orientation as a vital path for board members to influence environmental performance (Tang and Tang, 2012) is insightful, there might be other channels through which environmental expertise drives positive outcomes. For example, previous studies have highlighted the positive impact of environmental management control systems on environmental performance (Hennig et al., 2020; Henri and Journeault, 2010). Relatedly, the literature recognizes the significance of appropriate incentive schemes in fostering sustainability initiatives (e.g. Flammer et al., 2019). Exploring these alternative channels and mediating influences in future research could provide a comprehensive understanding of how boards can effectively contribute to improved environmental performance. In addition to identifying these channels, future studies could also benefit from integrating insights from the board dynamics literature (e.g. Bjørnåli et al., 2023; Pugliese et al., 2015) into this process by, for instance, investigating the influence of directors’ status (see, for example, Weck et al., 2022) and psychological safety (Veltrop et al., 2021) on the effectiveness of environmental experts on boards.

Third, although we use the institutional setting to tease out our mechanisms of attention and action, institutional influences are not our main focus. While one might think that these effects are straightforward, the endogenous relationship between institutional factors, such as green party presence and environmental expertise, seems to call for a deeper investigation into the complex role of institutional environments.

Finally, as with most corporate governance studies based on archival data, our study is not free from concerns about endogeneity. While we are confident that our ITCV approach points in a convincing direction, we cannot fully claim causality since there is no external shock to provide full exogeneity to our mechanisms. In a related vein, this also applies to the possibility of reverse causality, despite running some tests that point in the direction of our hypothesized effects. Hence, we would like to ask our readers to handle causality within our model with caution.

Overall, our article unveils the transformative potential of directors with environmental expertise in driving firms’ environmental performance, underscoring the pivotal role of stakeholder attention and substantive actions. Yet, the relationship between boards and environmental performance invites further exploration and qualitative insights. Future research should explore the intricate dynamics by delving into board dynamics, decision-making processes, and institutional influences. Embracing this challenge, we can unlock important insights that will empower organizations to create successful environmental strategies. As we venture into this burgeoning stream of research, the fruits of our collective efforts promise to shape a more environmentally conscious business landscape, serving as a key ingredient for forging prosperous paths toward sustainability and propelling us toward a greener future.

Footnotes

Acknowledgements

The authors wish to thank the editor, Glen Dowell, and the reviewers for their guidance. The authors are grateful to Sebastian Firk, Faryda Lindeman, Björn Mitzinneck, Jordi Surroca, and Peer Stiegert for helpful comments and suggestions. In addition, they appreciate the feedback from the participants at a research seminar at WHU (October 2018) and the Annual Meeting of the Academy of Management in Chicago (August 2018).

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Jana Oehmichen wants to thank Dr Werner Jackstädt-Stiftung for supporting her research about environmental experts on boards.