Abstract

Firm political connections are widely recognized to have both positive and negative implications, but why do firms build political connections in the first place? Distinct from prior research that typically views firm political connections as capital stock, we focus on board political capital building—selecting new directors with political backgrounds—as a strategic decision. Drawing on the behavioral theory of the firm, we examine how board political capital building is driven by performance shortfalls based on the logic of problemistic search—seeking the potential benefits of political connections while undertaking the potential downsides. Using director selection data on Chinese listed firms, we find that firms with higher performance shortfalls are more inclined to select new independent directors with political backgrounds. We further demonstrate that it is more feasible for firms with performance shortfalls to build lower-level board political capital but infeasible for them to build upper-level political capital.

Keywords

Introduction

Firm political connections, the boundary-spanning linkages between businesses and governments, represent critical nonmarket capital for organizations (Hadani et al., 2017; Hillman and Hitt, 1999; Tihanyi et al., 2019), especially in countries where governments play an important role in the business sector, such as China (Sun et al., 2016; Zheng et al., 2015). Research usually emphasizes the benefits of firm political connections, including accessing state-controlled resources and buffering firms from unfavorable government interventions (Frynas et al., 2006; Mellahi et al., 2016). However, scholars caution that the value of political connections could be vulnerable because political capital is subject to possible devaluation and may even become a liability (Siegel, 2007; Sun et al., 2010, 2015). Recent research further reveals the dark side of political connections, which may have negative implications for firms, such as engendering government expropriation (Ge and Micelotta, 2019; Gounopoulos et al., 2020) and enabling blockholders’ appropriation of firm wealth (Sun et al., 2016).

These contradictory outcomes highlight a key puzzle—given that political connections have both potential benefits and downsides, why firms are motivated to build such connections in the first place? This critical issue remains underexplored because prior research typically treats firm political connections as the stock of political capital to examine the consequences, while firms’ motives behind their strategic decision to build political connections are largely overlooked (Hadani et al., 2017). Moreover, previous studies mostly explain political connection building from a resource dependence perspective, which views political capital as a key approach to mitigating the uncertainty led by the dependence on governments (Hillman, 2005; Lester et al., 2008). Nevertheless, research remains scarce in shedding light on the potential uncertainty (i.e. the coexistence of potential benefits and downsides) derived from board capital. In this study, we explain political capital building as a strategic decision with both potential benefits and downsides, which allows us to go deeper into firm decision-making and thus better elucidate firms’ motivations behind political capital building.

Specifically, we situate our inquiry in the context of director selection and examine the following question: Why are firms motivated to build board political capital—the selection of new outside directors (hereafter, we use directors to refer to new outside directors) with political backgrounds (PBs)? Individuals with PBs have previous work experience or current positions in government entities (Chizema et al., 2015; Sun et al., 2016). Appointing such individuals as board members is an approach that is commonly used by firms to build political ties (Hadani et al., 2017; Lester et al., 2008). Compared with other forms of political connections, such as state ownership and politically connected firm leaders, which usually reflect firms’ inherent political capital stock (Gounopoulos et al., 2020), the selection of directors with PBs better captures firms’ strategic decision to bring in outside political capital (El Nayal et al., 2019). Thus, director selection offers an ideal context for exploring political capital building.

Drawing on the behavioral theory of the firm (BTOF), we examine how board political capital building is driven by performance shortfalls (performance below the aspiration level) based on the logic of problemistic search. The BTOF represents an aspiration-directed logic that explains firm decision-making (Cyert and March, 1963; Greve, 1998). Firms with performance shortfalls are inclined to initiate problemistic search for solutions that can potentially solve the performance problems (Gavetti et al., 2012; Posen et al., 2018). Meanwhile, the search involves certain changes that represent risk-taking, defined as decisions with the potential for both gains and losses in the BTOF tradition (Bromiley, 1991). Overall, the potential gains from risk-taking offer the opportunity to address the focal problems and thus attain the aspiration level—that is, the objective of problemistic search. This logic has been used to explain an increasingly broad scope of decisions that create the potential for both gain and loss outcomes (i.e. risk-taking, Kotiloglu et al., 2021; Posen et al., 2018), including firm political activities (Rudy and Johnson, 2016; Xu et al., 2019) and board diversity (Jung et al., 2022). Thus, problemistic search logic offers an appropriate and fine-grained explanation for board political capital building.

Furthermore, we explore the heterogeneity within political capital regarding hierarchical ranks (i.e. upper versus lower levels). Directors with upper-level PBs usually represent more prestigious capital that benefits firm performance (Haveman et al., 2017; Magee and Galinsky, 2008), yet these directors are more difficult to access, especially for underperforming firms (Withers et al., 2012). We posit that building lower-level board political capital could be more feasible for firms with performance shortfalls. In contrast, to build upper-level political board capital, the more limited availability of candidates with upper-level PBs makes it infeasible for underperforming firms to target such candidates. Our theory thus extends problemistic search logic by incorporating a boundary condition imposed by the availability of target solutions.

We test our hypotheses in the Chinese context. Because of the strong presence of the government in the business sector, building board political capital is widespread and vital for Chinese firms (Haveman et al., 2017). Using director selection data on privately owned Chinese listed firms, we find support for most of our key arguments.

Our study contributes to the literature on both firm political connections and the BTOF. First, we illuminate the decision-making trade-off associated with board political capital building, thereby providing a fine-grained explanation for the appointment of politically connected directors based on the BTOF’s logic of problemistic search. Distinct from prior research on political capital stock, our study provides novel insights into firms’ motivation to appoint politically connected directors as a firm strategy. Furthermore, we explore the heterogeneity of board political capital in terms of hierarchical levels, thereby demonstrating how board political capital building is subject to political ranks. In this regard, our study extends research on firm political connections by illuminating the trade-off between upper- and lower-level political capital building. In addition, our study advances BTOF research by exploring problemistic search in the political domain within the novel and important context of director selection. More importantly, while problemistic search logic mainly explains underperforming firms’ motivations for seeking solutions, we offer the novel insight that the search for solutions to performance problems may be subject to the availability of high-quality resources.

Background and literature review

Board political capital building

Board political capital building is at the intersection of two critical management issues: firm political strategy and director selection. Firm political strategy refers to firms’ activities to influence government policies in their favor (Hadani et al., 2017; Hillman et al., 2004). This strategy has attracted considerable scholarly attention because of its important implications, especially in countries with powerful governments, such as China (Sun et al., 2016; Zheng et al., 2015). In particular, scholars recognize both the positive and negative influences of political connections (Luo et al., 2020; Yan and Chang, 2018; Zhang et al., 2016).

On the one hand, political connections help firms obtain government-endorsed legitimacy and state-controlled resources (Mellahi et al., 2016; Zheng et al., 2015), such as bank loans (Khwaja and Mian, 2005) and privileged market entries (Agrawal and Knoeber, 2001). In addition, political capital can buffer firms from unwanted interventions (Zhang et al., 2016). For example, research shows that firms use political capital to mitigate regulatory oversight (Correia, 2014) and secure favorable positions in lawsuits (Ang and Jia, 2014).

On the other hand, firm political capital involves risks with potential downsides. First, the value of political capital is vulnerable to adverse political shocks, such as unexpected regime changes, because such shocks could evaporate the value of political capital (Sun et al., 2010) or even turn political capital into a liability (Siegel, 2007; Sun et al., 2015). Moreover, firm political connections could have a co-optation or binding effect (Zhang et al., 2016), thus exposing firms to government pressure or expropriation (Ge and Micelotta, 2019). Research also shows that blockholders may use the buffering effect of political capital to facilitate rent appropriation of firm wealth (Sun et al., 2016).

Overall, firms face a trade-off between the potential benefits and downsides in building political connections, which is also reflected by the mixed findings in the literature on the performance outcomes of firm political connections. Some studies report positive outcomes (e.g. Frynas et al., 2006; Goldman et al., 2009; Hillman, 2005), while others find nonsignificant or even negative effects (e.g. Hadani and Schuler, 2013; Okhmatovskiy, 2010; Siegel, 2007). These contradictory findings reveal a dilemma in firms’ motivations behind political capital building and thus highlight the importance of developing a deeper understanding of the antecedents of firm political strategy (Hadani et al., 2017).

We address these knowledge gaps by examining board political capital building, an important firm political strategy (El Nayal et al., 2019; Lester et al., 2008; Sun et al., 2016). Extant research on director selection highlights the resource provision role of board directors (Hillman and Dalziel, 2003), viewing board capital—directors’ human and social capital—as a key selection criterion (Kor and Misangyi, 2008; Kor and Sundaramurthy, 2009). Although important and insightful, previous research typically emphasizes the anticipated benefits of board capital, such as mitigating the uncertainty due to resource dependence (Hillman, 2005; Lester et al., 2008), without paying adequate attention to the possible uncertainty (i.e. the coexistence of potential benefits and downsides) derived from board capital per se. Given the nature of political capital as a double-edged sword (Yan and Chang, 2018; Zhang et al., 2016), it is essential to incorporate both the potential benefits and downsides, thereby offering a more comprehensive explanation of board political capital building. The BTOF’s logic of problemistic search theorizes both the potential benefits and downsides of strategic decision-making, thus presenting a novel and fine-grained perspective for explaining why firms are inclined to seek the benefits of board political capital and undertake the involved risks.

Furthermore, previous research interprets poor firm performance as indicating a need for political capital building due to resource dependence on the government (Withers et al., 2012). Instead, we draw on the BTOF to articulate the influence of performance shortfalls—performance relative to aspirations—thereby better illuminating the implications of decision-makers’ performance evaluations (Mishina et al., 2010).

BTOF and problemistic search

The BTOF suggests that organizations adapt decision-making by learning from performance feedback (Cyert and March, 1963; Greve, 1998). With bounded rationality, firm decision-makers evaluate firm performance based on aspiration levels, “the smallest outcome that would be deemed satisfactory by the decision-maker” (Schneider, 1992: 1053). Aspirations are formed based on firms’ prior performance and the performance of comparable peers (Berchicci and Tarakci, 2021). When firms perform below their aspirations, such performance shortfalls trigger a problemistic search. That is, performance shortfalls signal to firm decision-makers the existence of certain problems, and thus, they become motivated to search for performance-improving solutions (Banerjee et al., 2019; Cyert and March, 1963; Kim and Rhee, 2020). Meanwhile, the desire to seek solutions encourages decision-makers to initiate certain changes and to undertake potentially higher risks associated with the search or change (Bromiley, 1991; Lant et al., 1992). Indeed, the search will inevitably require changes in certain issues identified as potential sources of the performance shortfalls and introduce the risk of failing to fulfill the desired benefits or even engendering additional losses (Jung et al., 2022; Posen et al., 2018).

Empirical research has tested the logic of problemistic search by demonstrating the linkage between performance shortfalls and the two general behavioral consequences of problemistic search (see Posen et al., 2018 for a detailed review)—that is, strategic risk-taking (e.g. Kolev and McNamara, 2020; Mount and Baer, 2021) and organizational changes (e.g. Kacperczyk et al., 2015; Kim and Rhee, 2017). Moreover, this logic has been used to explain firm decision-making in various domains that entail changes and/or risk-taking, including innovation or research and development (R&D) (e.g. Blagoeva et al., 2020; Greve, 2003; O’Brien and David, 2014; Saraf et al., 2021), acquisitions (e.g. Kim et al., 2015; Kuusela et al., 2017; Lee et al., 2021), capital investment or divestment (e.g. Arrfelt et al., 2013; Desai, 2016; Shimizu, 2007), and market expansion (e.g. Audia and Greve, 2006; Barreto, 2012; Greve, 2008; Ref and Shapira, 2017). More recently, scholars have applied the logic of problemistic search to explain an increasingly broad scope of decisions that reflect search, change, or risk-taking (i.e. decisions with both potential benefits and downsides), including board diversity (e.g. Jung et al., 2022), corporate social responsibility (e.g. Smulowitz et al., 2020; Wang et al., 2021), financial misconduct (e.g. Harris and Bromiley, 2007; Mishina et al., 2010), interorganizational network building or termination (e.g. Clough and Piezunka, 2020; Kavusan and Frankort, 2019; Martínez-Noya and García-Canal, 2021), and internationalization (e.g. Deng et al., 2022; Dong et al., 2022; Xie et al., 2022; Xu et al., 2020).

In particular, an emerging yet nascent stream of research explores firms’ problemistic search in the political domain. For example, Rudy and Johnson (2016) show that performance shortfalls lead to increases in corporate lobbying, a risky change with potential benefits for firm performance. Xu et al. (2019) demonstrate that in the Chinese context, firms with performance shortfalls are more likely to engage in bribery, which also represents a change in searching for political solutions with both potential benefits and downside risks. Zhang and Greve (2019) suggest that for Chinese firms whose boards are dominated by a state coalition, performance shortfalls usually lead to more state-related actions for problemistic searches, such as conducting state-bridged acquisitions and seeking state bank loans. Our study extends this line of inquiry by examining how firms build political connections based on director selection in response to performance shortfalls. We also delve more deeply into the heterogeneity within board political capital in terms of hierarchical levels, thereby providing fresh insights into how problemistic search is subject to the availability of high-quality solutions.

Hypothesis development

Performance shortfalls and board political capital building

We posit that firms with higher performance shortfalls are more motivated to build board political capital. According to the BTOF’s logic of problemistic search, performance shortfalls trigger decision-makers’ desire to seek performance-enhancing solutions (Cyert and March, 1963; Posen et al., 2018). Specifically, unsatisfactory performance indicates the need to identify certain problems that have led to the underperformance, thereby triggering a search for solutions that can potentially address the problems. As noted above, such search actions are often reflected as changes that inevitably involve risks (Bromiley, 1991; Lant et al., 1992).

Given its potential benefits, building board political capital could be perceived as a possible form of search in response to performance shortfalls. Previous studies reveal that when facing performance shortfalls, firms are likely to search for solutions in the political domain, typically based on building certain forms of connections with officials in power (e.g. Rudy and Johnson, 2016; Xu et al., 2019). In particular, appointing new directors with PBs represents a common strategy for building firm political connections that can bring in outside political capital to change or enhance firms’ existing capital (El Nayal et al., 2019; Sun et al., 2016). As articulated above, research has widely recognized the performance benefits of political connections in terms of obtaining resources from the state and managing resource dependence on the state (Zhang et al., 2016). For example, politically connected firms have better access to valuable government-controlled resources, such as state bank loans (Khwaja and Mian, 2005) or exclusive market entry opportunities (Agrawal and Knoeber, 2001). Moreover, political connections can buffer firms from unfavorable political or regulatory interventions (Correia, 2014). Accordingly, the decision-makers of underperforming firms are likely to identify problems in the political domain (e.g. a lack of sufficient or appropriate political capital) and therefore select new directors with PBs as a possible search for solutions. Xu et al. (2019) suggest that “bribery provides a quick, short-term solution for firms’ problems by securing favorable treatment from officials and other people in power” (p. 1230). Consistent with this logic, underperforming firms could seek similar benefits from relevant government officials by appointing them as board directors, which may provide the firms with greater possibilities to reach their performance aspirations.

Furthermore, in line with the nature of problemistic search, board political capital building involves potential risks. Firms with performance shortfalls—because of the desire to seek performance-enhancing solutions—usually have a higher willingness or tolerance for taking such risks (Greve, 1998, 2003; Lim and McCann, 2014). As noted above, building board political capital is a risky strategy with uncertain gains and potential downsides (Siegel, 2007; Sun et al., 2012; Zhang et al., 2016). First, hiring directors with PBs could be costly for firms. Candidates with PBs are valuable capital for firms, and thus, they have more opportunities or a higher likelihood of obtaining board directorships (Lester et al., 2008). Higher demand usually means higher costs for firms seeking directors with PBs. This observation holds especially for underperforming firms because directors joining such firms might face a reputational loss and thus ask for extra compensation (Withers et al., 2012). From the perspective of potential directors with PBs, a directorship in listed firms represents an attractive opportunity because it could signify their social status and market value (He and Huang, 2011). Meanwhile, given their role in providing firms with connections with government entities, they usually have stronger bargaining power, especially against underperforming firms, which underlies their higher compensation when joining the boards (Lester et al., 2008; Withers et al., 2012). Second, the value of board political capital is uncertain. Indeed, such value is embedded in directors’ political power and networks, which are highly dynamic and vulnerable to unexpected political shocks (Siegel, 2007; Sun et al., 2010, 2015). The combination of high costs and uncertain value underlies the risks of building board political capital. The dark side of political capital could also reinforce such risks. Specifically, politically connected firms are subject to stronger political expropriations (Ge and Micelotta, 2019; Gounopoulos et al., 2020). Moreover, board political capital may be used by certain shareholders to pursue private interests at the expense of firm wealth (Sun et al., 2016). These potential downsides represent firms’ risks in selecting directors with PBs. Thus, based on problemistic search logic, firms with higher performance shortfalls—because of their desire to search for solutions—are more likely to undertake such risks.

In addition, consistent with the nature of problemistic search logic, selecting new directors with PBs reflects the changes needed to initiate the search for solutions. The selection of new directors often triggers changes in board composition, regardless of whether extra board members are added or previous members are replaced (Withers et al., 2012). Appointing directors with PBs to corporate boards brings in new political capital, thus changing the overall capital configuration within the boards (El Nayal et al., 2019; Sun et al., 2016). For underperforming firms, this change may be needed as a solution for certain performance problems and thus create the potential for these firms to reach their aspirations. More generally, selecting new directors with PBs also exhibits firms’ greater attention or resource allocation to the political domain, thereby representing changes in strategic orientation. Jung et al. (2022) demonstrate that given the deep involvement of board directors in a firm’s strategic reorientation, “negative performance feedback affects board diversity, which is instrumental in shaping a firm’s strategic change” (p. 1). Similarly, selecting a director connected with a government agency may reflect a firm’s new orientation to cultivate the connection with that agency to obtain favorable treatment. In response to performance shortfalls, such changes are usually driven by firms’ desires to search for solutions that potentially address performance problems (Xu et al., 2019). Even for firms with preexisting political connections, selecting new directors with PBs provides additional, typically distinct connections with governments. Such selection thus represents a form of local search in the vicinity of firms’ current practice or experience, leading to incremental and path-dependent changes, as commonly characterized by problemistic search logic (Posen et al., 2018).

Hypothesis 1 (H1). Firms with higher performance shortfalls are more inclined to build board political capital—that is, select directors with political backgrounds.

Heterogeneity within board political capital

We further explore the heterogeneity within board political capital by examining different hierarchical levels (upper level and lower level as two separate categories). In the political regime, upper-level individuals access greater resources, thus potentially presenting more benefits for connected firms than lower-level individuals (Haveman et al., 2017; Magee and Galinsky, 2008). However, the political system is typically structured like a pyramid, with far fewer upper-level positions, suggesting that the pool of director candidates with upper-level PBs is considerably smaller and that such candidates require more resources to acquire (Sun et al., 2015). Thus, balancing board political capital building at upper versus lower levels presents an additional trade-off between the potential value and availability of political capital.

We argue that firms with higher performance shortfalls are less likely to select directors with upper-level PBs and more likely to select directors with lower-level PBs based on the joint consideration of potential value and availability. The problemistic search logic mainly explains why underperforming firms seek solutions (Posen et al., 2018). However, we suggest that the search does not simply concern firms’ motivations to address performance problems; rather, it also depends on the availability of solutions to firms. Indeed, despite their stronger motivations to search for solutions, firms with higher performance shortfalls usually find it more difficult to access high-quality resources or solutions (Kuusela et al., 2017). In director selection, research also suggests that poorly performing firms have greater difficulty attracting resourceful directors (Withers et al., 2012). Accordingly, although directors with upper-level PBs potentially open doors with larger payoffs, accessing such upper-level political connections may be less feasible for underperforming firms. Director candidates with upper-level PBs are more prestigious and, thus, more selective when deciding to join corporate boards (Lester et al., 2008). They may also have stronger concerns about possible reputational losses if they join the boards of underperforming firms, making it more challenging for such firms to target these candidates. This situation is especially likely in countries where upper-level political officials are sensitive to their reputation, such as China (Wang et al., 2019; Zheng et al., 2015).

On the other hand, although individuals with lower-level PBs are less powerful or resourceful in the political regime, they are likely to provide specific benefits or solutions to address the corresponding performance problems of underperforming firms. Moreover, these individuals tend to be less selective and subject to weaker reputational losses when joining the boards of underperforming firms. While most people prefer to join the boards of prestigious or well-performing companies, the director selection of such companies may be competitive (Withers et al., 2012). Consequently, people with lower-level PBs may not be sufficiently attractive for well-performing firms as director candidates, while joining the boards of underperforming firms could be a wise decision to start or develop their director careers. Overall, for underperforming firms, targeting candidates with lower-level PBs could be a more realistic way of conducting a problemistic search.

In summary, extending the logic of problemistic search based on the boundary condition imposed by the availability of solutions, we predict that firms with higher performance shortfalls are more likely to appoint directors with lower-level PBs and less likely to select directors with upper-level PBs, as they are discouraged by their more limited availability.

Hypothesis 2a (H2a). Firms with higher performance shortfalls are more likely to build lower-level board political capital—that is, select directors with lower-level political backgrounds.

Hypothesis 2b (H2b). Firms with higher performance shortfalls are less likely to build upper-level board political capital—that is, select directors with upper-level political backgrounds.

Methods

Research context, sample, and data

We test our hypotheses in the Chinese context for three reasons. First, the Chinese government has an influential role in the business sector, making the potential benefits and downsides of firm political connections prominent (Haveman et al., 2017). Second, building political capital is a common strategy of Chinese firms (Zheng et al., 2015), including those with performance shortfalls. Third, appointing independent directors (IDs) with PBs is a critical channel through which Chinese firms obtain political capital (Sun et al., 2016).

We use Chinese-listed firms in manufacturing industries (China Securities Regulatory Commission three-digit industry codes: C13–C43) as the population for our data analysis to make their industry backgrounds comparable, consistent with prior research (Chen, 2008; Iyer and Miller, 2008). Indeed, given the significant difference (e.g. asset scales) between manufacturing and nonmanufacturing firms (e.g. financial, agricultural, mining, construction, and retailing firms), their standards of profitability (e.g. returns on assets (ROAs)) are hardly comparable. We collect data on director selection from 2008 to 2013. Chinese listed firms were required to use a new version of the Corporate Accounting Codes in 2007. Hence, we collect financial and governance data from 2007 to ensure reporting consistency (Xu et al., 2019). We collect director selection data from 2008 to allow a 1-year lag. In 2013, the Chinese government implemented “Rule No. 18,” which suspended the directorships of incumbent government officials and precluded those who retired within the past three years from serving as IDs in listed firms. Thus, our data on director selection end in 2013 to avoid this policy impact.

Our initial sample includes 1399 manufacturing firms publicly listed on the main boards of the Shanghai and Shenzhen Stock Exchanges during the empirical time window. We exclude 599 firms with state-owned equity, which are usually born with political connections through the ownership channel. Thus, our sample includes 800 firms owned by private entities. The panel data on these firms are unbalanced, with 3437 firm-year observations, because many of them are listed after 2008, and their information before being listed is unavailable. We exclude 214 firm-year observations without information on director selection. We also exclude 421 observations that lack information in four continuous years, which is necessary to calculate historical aspirations. Furthermore, we exclude 157 observations with missing values of the control variables. Our final sample includes 2645 firm-year observations.

Chinese listed firms must disclose board directors’ biographical information in annual reports, which allows us to identify their backgrounds. GTA Information Technology, a Chinese database provider, quantified this individual-level director information—including directors’ political experiences—by employing well-trained specialists to code all the biographical sketches (Sun et al., 2016). We further verify these data and transform these individual-level data at the firm level to measure board political capital. Other firm-level financial and governance data are from the China Stock Market and Accounting Research database, a commonly used database provided by GTA (Ma and Khanna, 2016).

Variables and measures

Board political capital building

Our dependent variable, board political capital building, is measured by the number of new IDs with PBs in the selected year, consistent with prior research (e.g. Haveman et al., 2017; Sun et al., 2016).

Specifically, based on our conceptualization of board political capital building that focuses on the PBs of newly selected IDs, we identify new IDs if their names are first reported in the appointing firms’ board member lists in a given year, in line with prior research (Zhu and Chen, 2015). We also recognize that the selection of new IDs usually means the departure of previous IDs (i.e. replaced by new IDs), which may lead to a loss of board political capital. Therefore, we identify departing IDs if their names were reported in a firm’s board member list in the previous year but not in the focal selecting year. We account for the loss of board political capital by controlling for the number of departing IDs with PBs in the selecting year. To check robustness, we account for this loss in two alternative ways. First, we alternatively measure board political capital building by the number of new IDs with PBs minus the number of departing IDs with PBs, capturing the net increase or decrease in board political capital. Second, we run data analysis on an alternative sample of firm-year observations with zero loss of board political capital (N = 2525, representing a 4.54% loss in sample size). In this alternative sample, the number of new IDs with PBs directly captures the net increase in board political capital.

We code IDs’ PB based on their biographical sketches. We code 1 for IDs with PBs, including current positions or previous work experience in political entities, and 0 otherwise, consistent with previous research (Faccio, 2006; Sun et al., 2016). In the Chinese political hierarchy, there are 10 levels: chief and deputy officers at each of five administrative ranks—state/central (Guo), ministry/province (Bu), department/prefecture-level city (Ju), division/county (Chu), and section/township (Ke). Our main analysis counts PBs at all levels to comprehensively capture board political capital. In a robustness check, we adopt a stricter coding approach that counts only PBs at or above the deputy-Chu level (Haveman et al., 2017).

We next transform the individual-level PB coding into a firm-level variable—the number of new IDs with PBs. In our final sample, a zero value for this variable means either (1) zero new IDs were selected in a given year or (2) one or more new ID(s) were selected, but none of them has a PB. To further distinguish between these two scenarios, we run an additional analysis by constructing an alternative sample of firm-year observations with (nonzero) new ID appointments (N = 922 for 582 firms). In this alternative sample, a zero value for the board political capital building variable means that although the number of new IDs is nonzero, none of them has a PB.

In addition, the number of new IDs with PBs is a function of the number of all new IDs, which may be affected by performance shortfalls. Thus, we conduct robustness checks based on alternative measures that are not subject to this issue: (1) the ratio of new IDs with PBs to all new IDs and (2) a binary variable indicating whether any new IDs have PBs in a focal year.

Board political capital building at lower and upper levels

We divide the new IDs’ PBs into upper versus lower levels based on the deputy-Bu level as the threshold. In the 10-level political hierarchy of China, officials with positions at or above the deputy-Bu level (the fourth highest level) are commonly seen as upper-level officials. In a robustness check, we use the chief-Ju level (the fifth highest level) as an alternative threshold between upper- and lower-level PBs. We extend the coding rule of IDs’ PBs to code two additional individual-level dummy variables—new IDs with upper-level and lower-level PBs. Accordingly, we calculate firm-level new ID numbers with upper-level and lower-level PBs. In robustness checks, we alternatively use ratio-based and dummy-based measures.

Performance shortfalls

Performance shortfalls are indicated by the difference between actual performance and aspirations when performing below aspirations (Desai, 2016; Kuusela et al., 2017). Consistent with prior research, we use profitability, measured by ROA, to indicate performance and construct aspirations (Iyer and Miller, 2008; Lim and McCann, 2014). We separately measure historical aspirations (HAs) and social aspirations (SAs) to provide nuanced evidence (Chen and Miller, 2007; Lim and McCann, 2014). Following prior research (O’Brien and David, 2014), we construct HAs as the adaptive average of focal firms’ prior profitability in the last 3 years (HA(t − 1) = 0.7 × ROA(t − 2) + 0.2 × ROA(t − 3) + 0.1 × ROA(t − 4)), where the subscript t refers to the appointing year. An alternative measure (HA(t − 1) = ROA(t − 2)), used in prior research (Chen and Miller, 2007; Iyer and Miller, 2008), generates consistent results. SAs are indicated by the average profitability of a focal industry and a focal province (excluding the ROA of the focal firm) in the prior year (O’Brien and David, 2014). Indeed, research suggests that both industry similarity (Reger and Huff, 1993) and physical proximity (Baum and Lant, 2003) are important for forming reference groups in social comparison. The results remain unchanged when using the prior average profitability only in focal industries (excluding the ROA of the focal firm). We obtain historical (social) performance feedback by subtracting the HA (SA) of ROA from the actual ROA. We divide each performance feedback into two sides. Following prior studies (Iyer and Miller, 2008; Lim and McCann, 2014), we incorporate an indicator, I1, which equals 1 if the feedback is negative, and (1 − I1) refers to positive feedback. Accordingly, negative feedback = I1 × performance feedback, while positive feedback = (1 − I1) × performance feedback. We use negative feedback to indicate performance shortfalls (more negative feedback means higher performance shortfalls) while controlling for positive feedback (Kuusela et al., 2017).

Control variables

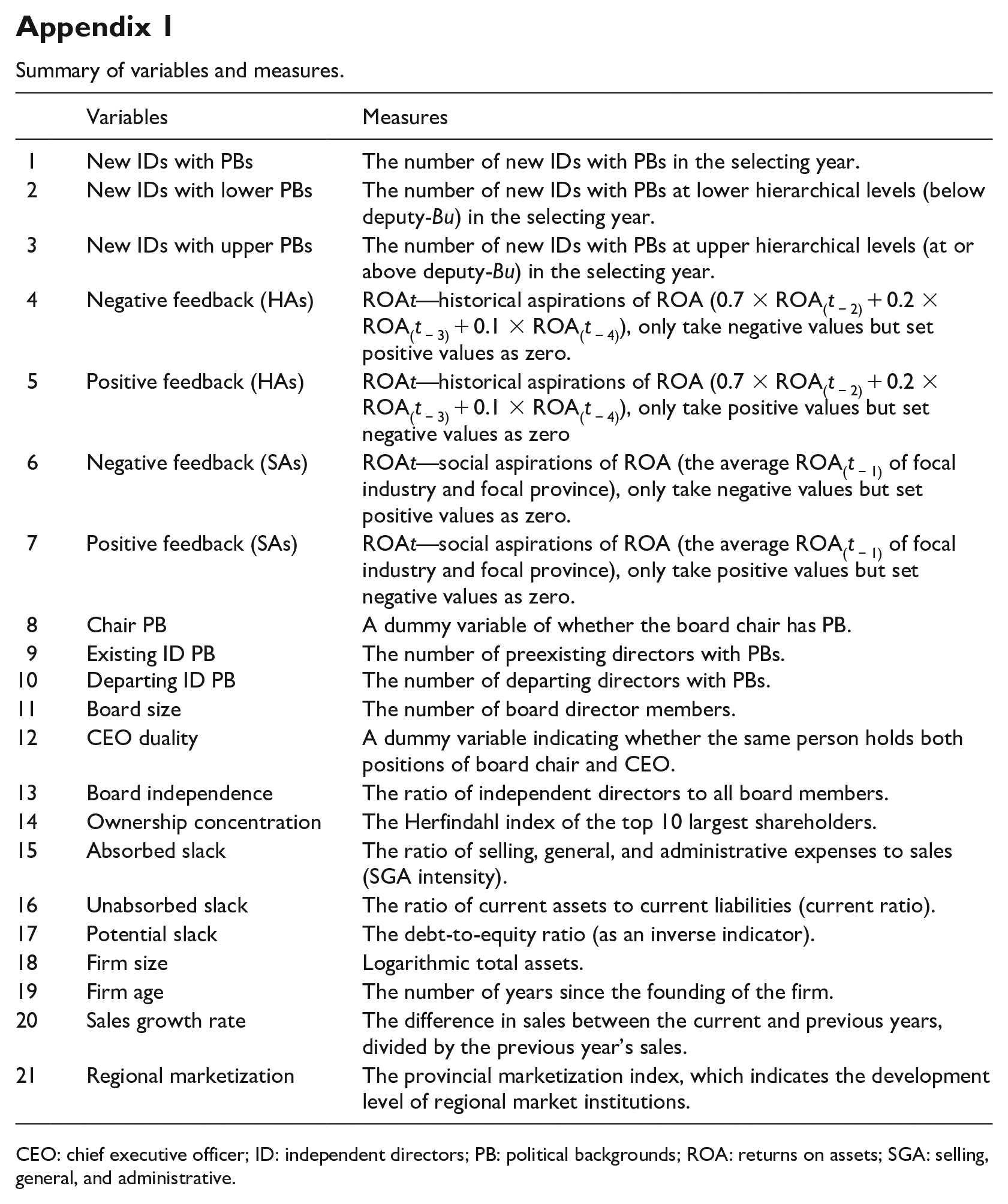

First, in addition to the loss of board political capital noted above, we control for the influence of firms’ preexisting political capital, represented by board chairs’ PBs and existing directors’ PBs. In Chinese listed firms, board chairs are usually the most influential decision-makers in the ID selection process (Ma and Khanna, 2016; Shen et al., 2015). They may decide whether to appoint new IDs with PBs based on their own PBs. Thus, we add chairs’ PBs to control for the influence of firms’ preexisting political capital. Following the same rules above, we code a dummy variable to capture chairs’ PBs. We also add the number of existing directors (i.e. neither new nor departing) with PBs to further control for preexisting political capital. Second, we include several governance factors to control for board and ownership effects: (1) board size, that is, the total number of board members; (2) CEO duality, that is, whether the same person holds the positions of CEO and board chair; (3) board independence, that is, the ratio of IDs on the board; and (4) ownership concentration, which is measured by the Herfindahl index among the top 10 largest shareholders. Third, consistent with BTOF research, we control for slack resources in three categories: (1) absorbed slack, that is, the ratio of selling, general, and administrative expenses to sales (SGA intensity); (2) unabsorbed slack, that is, the ratio of current assets to current liabilities (current ratio); and (3) potential slack, that is, the debt-to-equity ratio (Greve, 2003). We further control for several general firm-level factors, including firm size (logarithmic total assets), firm age, and sales growth. In addition, the potential value and risks of political capital depend on government power in regional markets, which is determined by the regional marketization level. Thus, we control for the provincial marketization index, which was developed by the National Economic Research Institute (Fan et al., 2011) and is widely used in the literature (Sun et al., 2016). Finally, we include year and industry dummies to control for unobservable time effects and time-invariant industry-level effects. We lag the independent and control variables by 1 year to mitigate reverse causality. To mitigate possible biases created by outliers, we winsorize continuous variables at the first percentile on both sides of their distributions (Kuusela et al., 2017). All variables and measures are summarized in Appendix 1.

Estimation methods

We test our hypotheses based on the following equation, in which the performance shortfall of firm i in year t − 1 explains its board political capital building (at lower/upper levels) in appointment year t.

The dependent variable, board political capital building (at lower/upper levels), is measured by count variables that are not overdispersed (general/lower/upper: mean = 0.56/0.43/0.13, SD = 0.71/0.63/0.37). Thus, we run Poisson regressions. The results based on negative binomial models are consistent. We also run zero-inflated Poisson (ZIP) models and find that Vuong tests cannot be rejected, suggesting that the standard Poisson model is more appropriate. Our unbalanced panel data may suffer from firm-level heteroscedasticity. To address this issue, we report robust standard errors clustered at the firm level.

Results

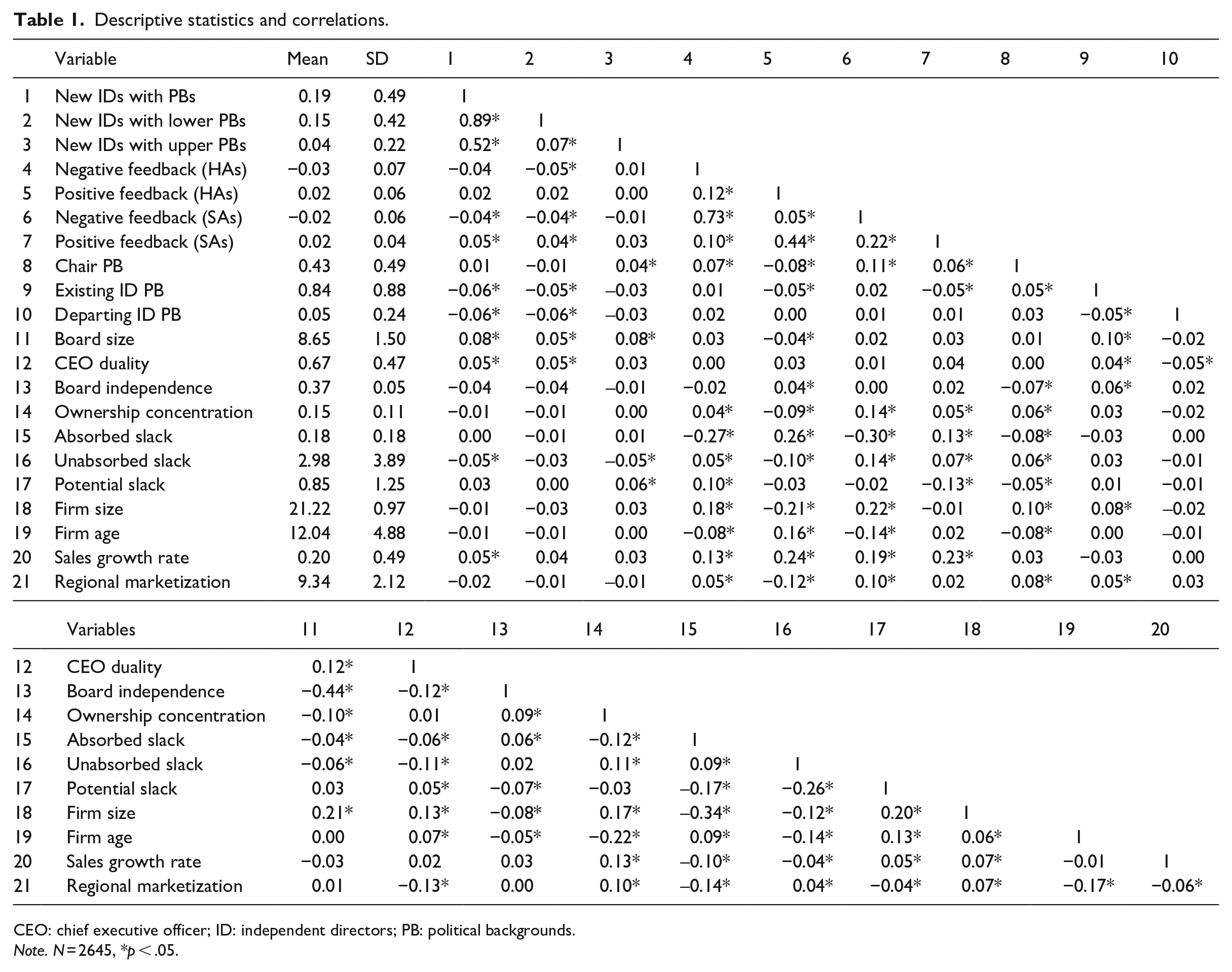

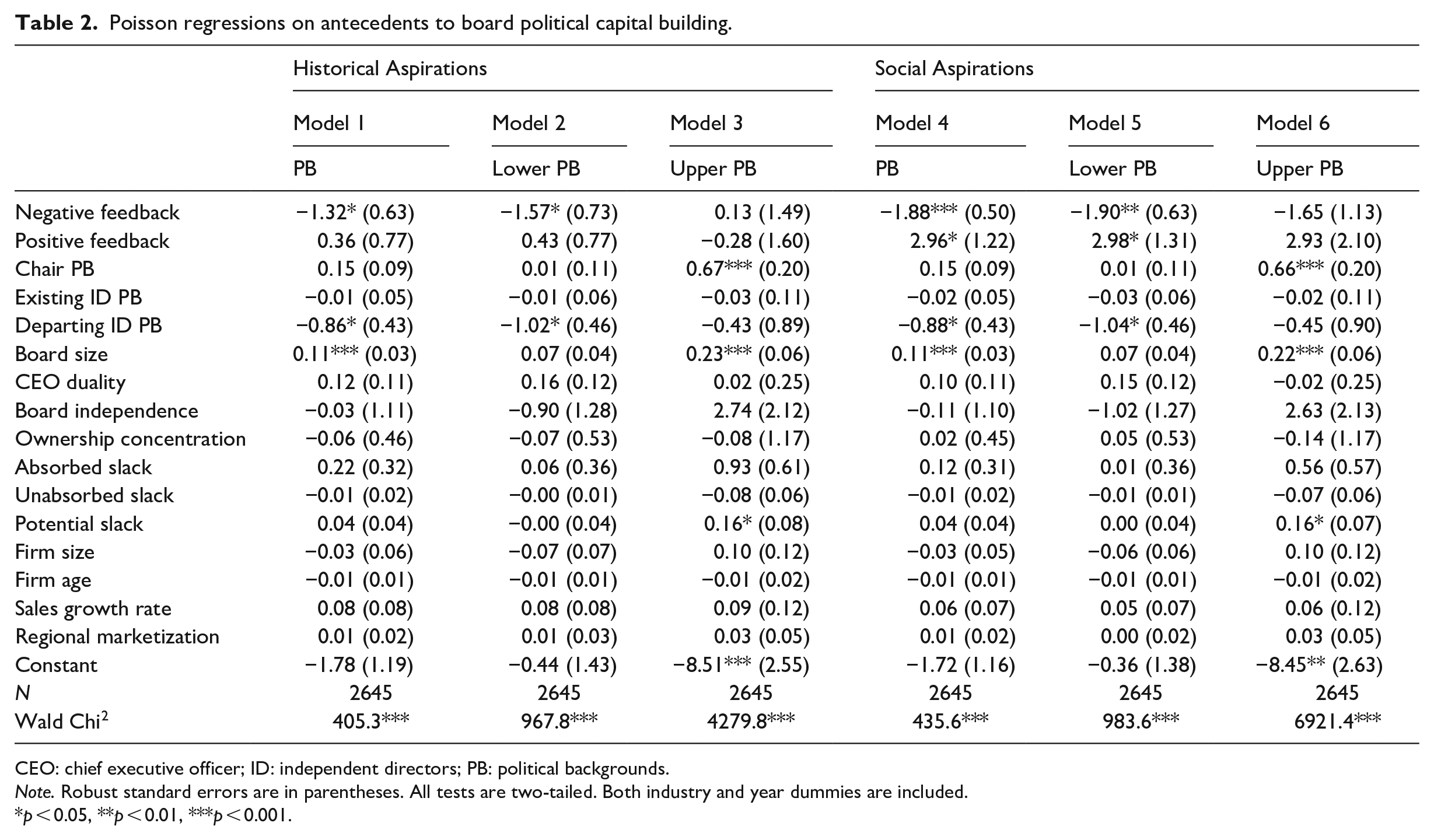

Table 1 presents the descriptive statistics and correlations of all variables. Table 2 presents the results of the Poisson regressions in the main analysis. Models 1–3 include performance feedback based on historical aspirations (hereafter, HA models), while Models 4–6 are based on social aspirations (hereafter, SA models). Models 1 and 4 test the effect of performance shortfalls on board political capital building, while Models 2 and 5 (3 and 6) are for lower-level (upper-level) board political capital building. The variance inflation factors in all the models are lower than 4.83, suggesting multicollinearity is not a serious issue.

Descriptive statistics and correlations.

CEO: chief executive officer; ID: independent directors; PB: political backgrounds.

Note. N = 2645, *p < .05.

Poisson regressions on antecedents to board political capital building.

CEO: chief executive officer; ID: independent directors; PB: political backgrounds.

Note. Robust standard errors are in parentheses. All tests are two-tailed. Both industry and year dummies are included.

p < 0.05, **p < 0.01, ***p < 0.001.

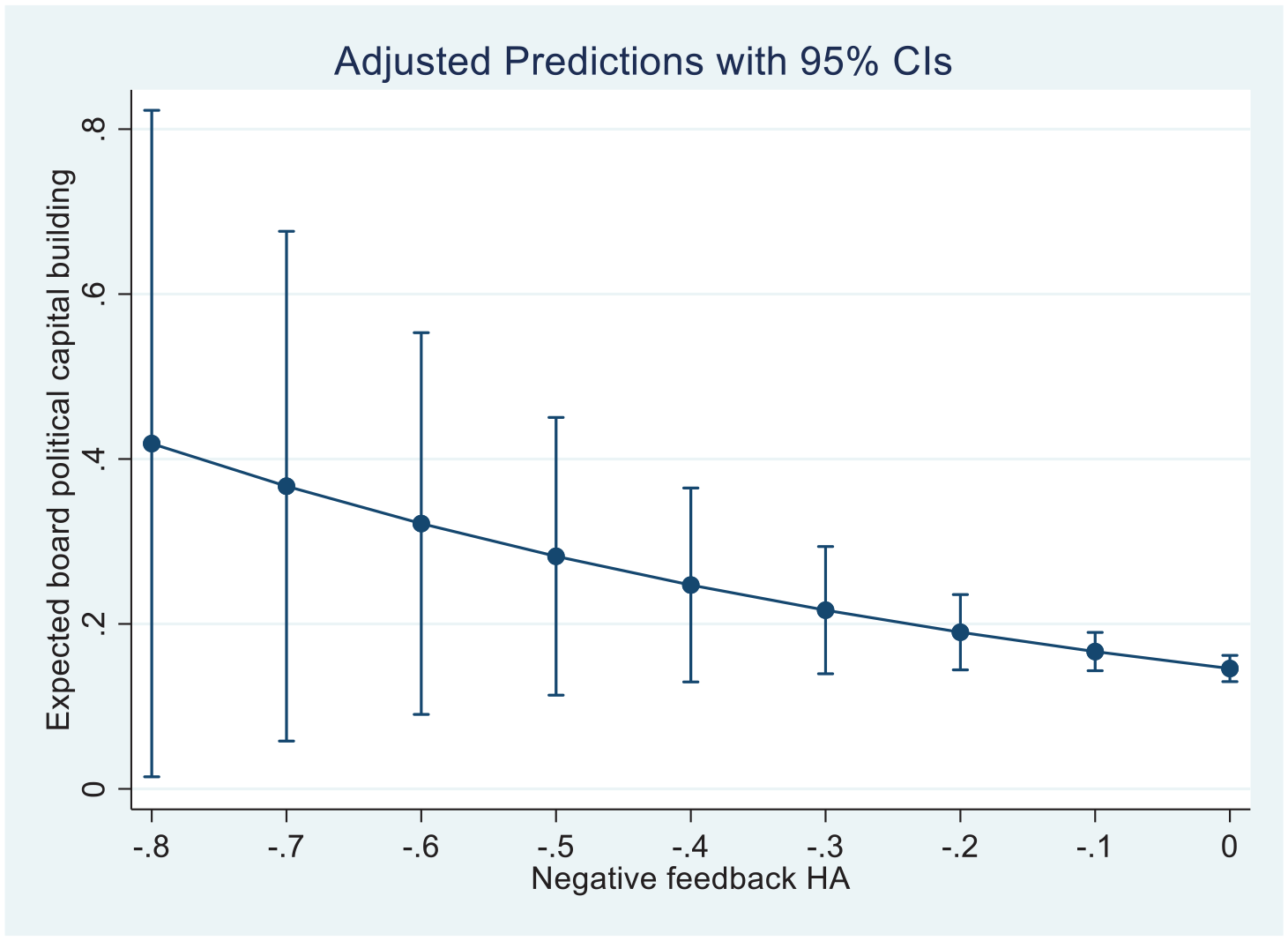

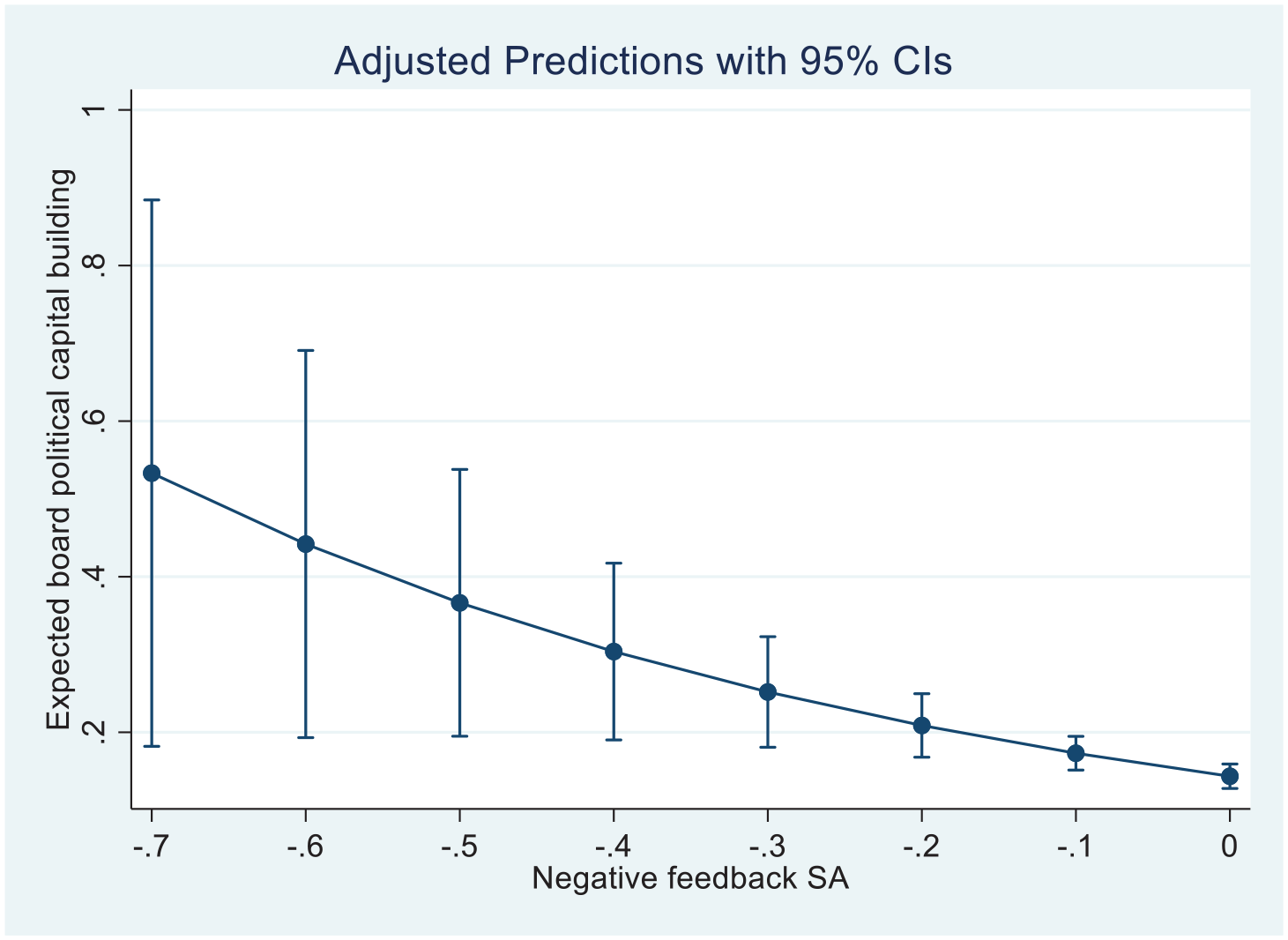

H1 states that firms with higher performance shortfalls are more likely to build board political capital. This hypothesis is supported, as the coefficients of negative feedback (which inversely indicates performance shortfalls) are negative and significant in both Model 1 (b = −1.32, SE = 0.63, z = −2.09, p = 0.037, CI95% = (−2.55, −0.08)) and Model 4 (b = −1.88, SE = 0.50, z = −3.78, p = 0.000, CI95% = (−2.85, −0.90)). These findings suggest that firms with more negative feedback (which indicates higher performance shortfalls) are more inclined to appoint new IDs with PBs, thus supporting the logic of problemistic search in the form of board political capital building. To demonstrate the effect size, we calculate the absolute value of standardized negative feedback (based on HAs and SAs) and run Poisson regressions with incidence rate ratios (IRRs). The results based on HAs (SAs) show that as performance shortfalls increase by one standard deviation, the likelihood of building board political capital will increase by 9.04% (8.73%), indicating the economic significance of the relationship between performance shortfalls and board political capital building. We visualize the effects of performance shortfalls on board political capital building based on the HA and SA models in Figures 1 and 2, respectively. These figures further demonstrate that firms with higher negative feedback tend to build more board political capital.

Expected board political capital building in response to negative feedback (based on historical aspirations).

Expected board political capital building in response to negative feedback (based on social aspirations).

Although without formal hypotheses, we notice that positive feedback (performance above aspirations) is positively related to board political capital building but is significant only in the SA model (b = 0.36, SE = 0.77, z = 0.46, p = 0.644, CI95% = (−1.16, 1.87)) and not in the HA model (b = 2.96, SE = 1.22, z = 2.42, p = 0.015, CI95% = (0.57, 5.36)). These findings suggest that firms are more likely to build board political capital when performing better than comparable peers. This finding is consistent with the slack search logic that outperforming firms are more capable of accumulating slack resources to support their selection of new IDs with PBs.

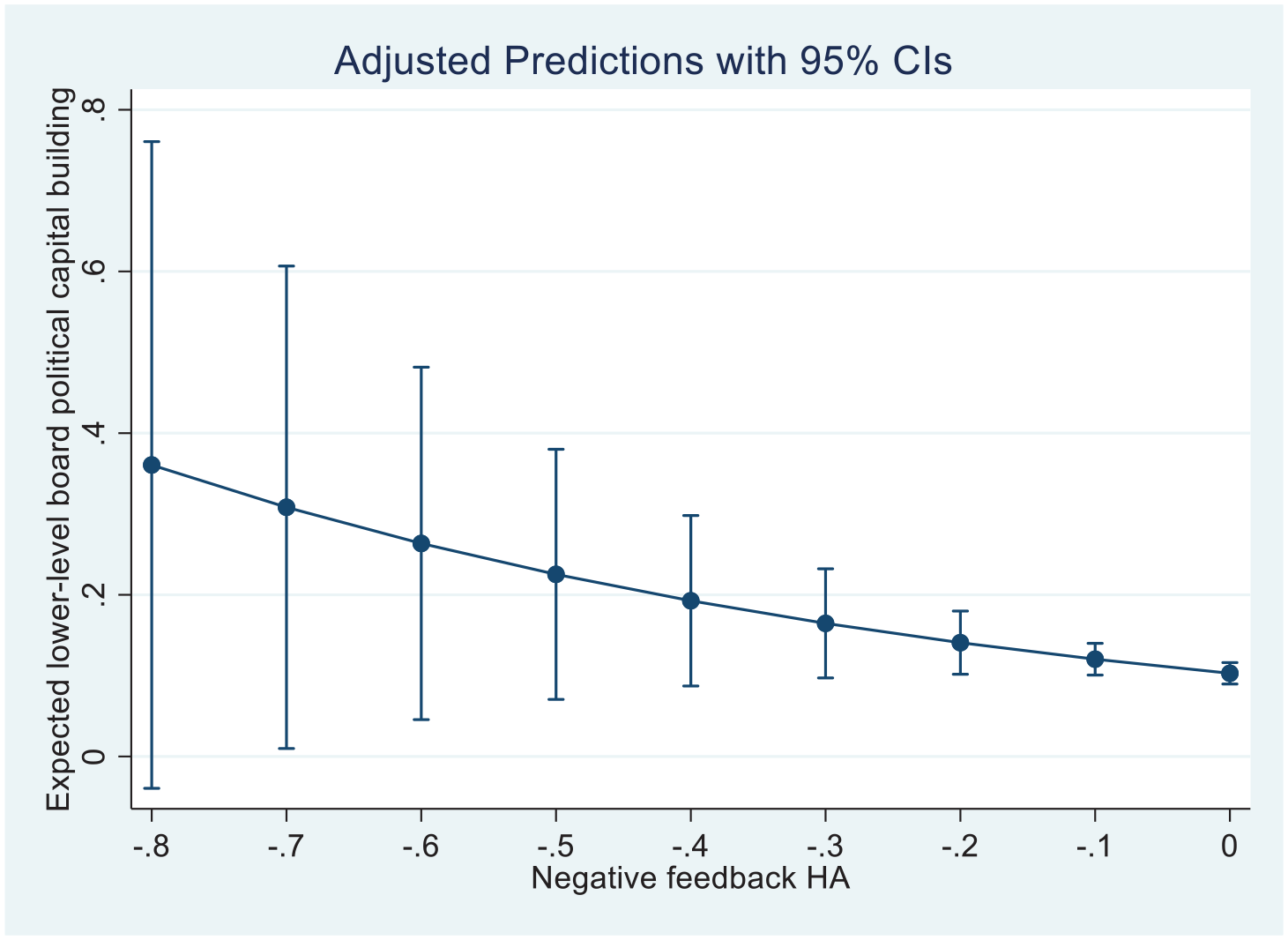

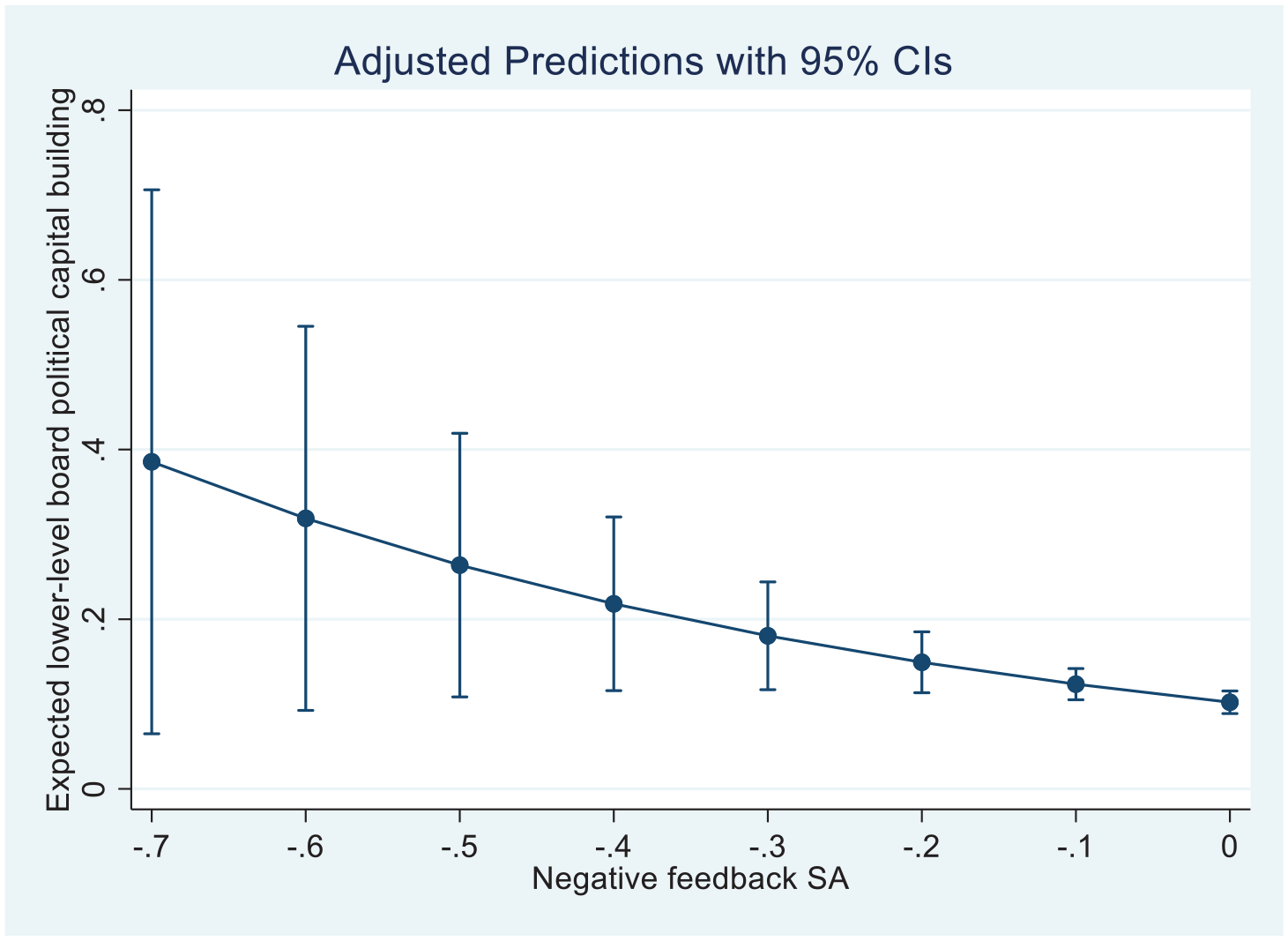

H2a predicts that firms with higher performance shortfalls are more likely to build lower-level board political capital. The results support this hypothesis. The coefficients of negative feedback are negative and significant in both Model 2 (b = −1.57, SE = 0.73, z = −2.16, p = 0.031, CI95% = (−2.99, −0.14)) and Model 5 (b = −1.90, SE = 0.63, z = −3.02, p = 0.003, CI95% = (−3.13, −0.67)). These results are consistent with the logic of problemistic search that firms performing further below aspirations are more inclined to build lower-level board political capital. Selecting new IDs with lower-level PBs thus represents a feasible way of conducting a problemistic search. Again, we calculate the effect size. The HA (SA) model suggests that as performance shortfalls increase by one standard deviation, the likelihood of building lower-level board political capital will increase by 10.85% (11.30%), showing the economic significance of the relationship between performance shortfalls and lower-level board political capital building. We visualize the effects of performance shortfalls based on the HA and SA models on lower-level board political capital building in Figures 3 and 4, respectively. These figures show that firms with higher negative feedback tend to build more board political capital at the lower level.

Expected lower-level board political capital building in response to negative feedback (based on historical aspirations).

Expected lower-level board political capital building in response to negative feedback (based on social aspirations).

H2b predicts that firms with higher performance shortfalls are less likely to build upper-level board political capital. We find that the coefficients of negative feedback are not significant in either Model 3 (b = 0.13, SE = 1.49, z = 0.08, p = 0.933, CI95% = (−2.80, 3.05)) or Model 6 (b = −1.65, SE = 1.13, z = −1.46, p = 0.145, CI95% = (−3.87, 0.57)). Although they do not support H2b, these results generally align with our prediction that it may be infeasible for underperforming firms to appoint new IDs with upper-level PBs as a form of problemistic search.

Supplementary analyses

Robustness checks

We account for the loss of board political capital in two alternative ways. First, we capture the net increase or decrease in board political capital by calculating the number of new IDs with (upper/lower level) PBs minus the number of departing IDs with (upper/lower level) PBs. Given that these dependent variables may have negative values (i.e. net decrease in board political capital), we cannot use the Poisson model. Instead, we use feasible generalized least squares (FGLS) regressions with firm-level heteroscedasticity (Zhu and Chen, 2015), as this model helps address the influence of common firm-level unobservable factors on different observations within a firm (Krariya and Kurata, 2004). The results are consistent with those of the main analysis, except that the HA result for lower-level board political capital is weaker. Second, we run the analysis by using an alternative sample with zero loss of board political capital (N = 2525). The results based on Poisson regressions are essentially the same as those of the main analysis. Taken together, these robustness checks suggest that our findings are not sensitive to the loss of board political capital.

In addition, we use (1) the ratio of new IDs with PBs to all new IDs and (2) a binary variable of new PB IDs as two alternative measures of board political capital building. Accordingly, we use (1) FGLS and (2) logit models as estimation methods. The results are unchanged. Therefore, our findings are not sensitive to the alternative explanation that performance shortfalls may influence the number of IDs with PBs by affecting the number of all new IDs. Moreover, we alternatively measure board political capital building by counting only PBs at or above the deputy-Chu level (Haveman et al., 2017). The results are also robust. Finally, we distinguish between upper- and lower-level PBs based on an alternative threshold of the chief-Ju level. The results are generally consistent, except that the HA results for upper-level board political capital become marginal. These results suggest that our findings regarding upper- and lower-level board political capital building are not sensitive to specific thresholds.

Propensity score matching analyses

Firms’ propensities to appoint new directors may not be exogenous and could be affected by unobservable factors that also influence board political capital building. To address this endogeneity concern, we run propensity score matching (PSM) analyses.

Based on the propensity score of new ID appointments, we match firms with appointments of new IDs (the treatment group) with those without new appointments (the control group). The propensity score is calculated by a logit model with the control variables listed above, indicating the likelihood of a firm appointing new IDs (i.e. being selected into the treatment group). We eliminate 37 firm-year observations in the matching process, leaving a sample size of 2608 firm-year observations. The t tests of most variables between the treatment and control groups are nonsignificant (p > 0.10), suggesting no systematic difference between them and thus indicating the good quality of our matching. The results remain robust, suggesting that our findings are not sensitive to the propensity of new ID appointments.

An additional analysis in an alternative sample of firms with nonzero new IDs: the Heckman two-stage approach

Within the firms that select (nonzero) new IDs in a given year (N = 922 for 582 firms), we further explore whether those with higher performance shortfalls are more inclined to build board political capital. In this alternative sample, zero in the board political capital building variable means that although the number of new IDs is nonzero, none of them has PB. We recognize that the likelihood of selecting new IDs in a given year may be influenced by certain factors affecting board political capital building, which indicates a potential sample-induced endogeneity. Therefore, we address this issue by using the Heckman two-stage approach (Certo et al., 2016). In the first stage, we use a dummy variable of new ID appointments (i.e. if a firm appoints any new IDs in a given year) as the dependent variable and run a panel logit regression in the full sample (N = 2645). In addition to the control variables listed above, we add the average age of existing IDs as an exclusion restriction. The age of existing IDs may influence whether firms appoint new IDs because older IDs are more likely to retire, thus calling for new IDs (empirically verified in the first stage: b = 0.015, SE = 0.005, p = 0.006). Nevertheless, there is no apparent reason to predict that existing ID average age affects whether newly selected IDs have PBs (also verified if included in the second stage: b = 0.005, SE = 0.01, p = 0.605). We calculate the inverse Mill’s ratio and add it to the Poisson regressions in the second-stage analysis in the smaller alternative sample. The results are essentially the same as those in the main analysis (in the full sample), suggesting that our findings are not sensitive to the sampling issue.

An additional analysis exploring the performance consequences of board political capital building

We theorize board political capital building as a form of problemistic search triggered by performance shortfalls. Our findings support this theorization by showing that firms with higher performance shortfalls are more likely to select new IDs with PBs. To provide a more complete framework of board political capital building and to solidify our theorization based on the logic of problemistic search, we empirically explore the performance consequences—that is, whether board political capital building, as expected based on the logic of problemistic search, leads to (1) greater performance improvement, that is, the benefits of a performance solution and (2) higher performance volatility, that is, the risks involved in the search.

We measure performance improvement by the ROA difference between the next 2 years after new IDs are appointed (ROA(t + 2) − ROA(t + 1)). Performance volatility is measured by the standard deviation of quarterly ROA over the next 2 years after new IDs are appointed (Miller and Chen, 2004). Alternatively, we calculate both performance consequences over longer time frames (3 or 5 years) to capture the longer-run implications of board political capital building. In addition to the control variables listed above, we include negative and positive feedback (based on HAs) to account for the effect of regressions to the mean (i.e. firms with more performance deviation from the previous years, or HAs, may bounce back in subsequent years). We use FGLS regressions with firm-level heteroscedasticity to address the potential influences of firm-level unobservable factors (Zhu and Chen, 2015).

Our results show that board political capital building is not significantly related to subsequent performance improvement in Model 1 (b = −0.01, SE = 0.07, z = −0.15, p = 0.879, CI95% = (−0.14, 0.12)) but is positively and significantly related to subsequent performance volatility in Model 2 (b = 0.50, SE = 0.14, z = 3.49, p = 0.000, CI95% = (0.22, 0.78)). These results are consistent with the insights that board political capital carries both positive and negative performance implications, thus leading to equivocal performance enhancement effects (Sun et al., 2016). On the other hand, consistent with the downside risks involved in problemistic search, board political capital building may lead to higher performance volatility.

Lower-level board political capital building is also not significantly related to subsequent performance improvement in Model 3 (b = 0.14, SE = 0.08, z = 1.62, p = 0.105, CI95% = (−0.03, 0.30)) but is positively and significantly related to subsequent performance volatility in Model 4 (b = 0.74, SE = 0.23, z = 3.23, p = 0.001, CI95% = (0.29, 1.20)). These results are similar to those for general board political capital building and are consistent with our argument that lower-level board political capital building represents a feasible form of problemistic search. Upper-level board political capital building, on the other hand, is negatively and significantly related to subsequent performance improvement in Model 5 (b = −0.31, SE = 0.14, z = −2.22, p = 0.026, CI95% = (−0.58, −0.04)) but is not significantly related to subsequent performance volatility in Model 6 (b = −0.38, SE = 0.55, z = −0.68, p = 0.494, CI95% = (−1.46, 0.70)). These effects are different from those for general board political capital building, in line with our argument that upper-level board political capital building may not be a feasible form of problemistic search. One possible reason for the negative effect on performance improvement is that appointing firms may spend too much money attracting upper-level PB IDs, such as extra entertainment or even bribery (Xu et al., 2019), while the benefits may be appropriated by blockholders and, thus, cannot be explicitly reflected by firm performance (Sun et al., 2016).

We further explore the longer-run performance consequences in 3 years (ROA(t + 3) − ROA(t + 1); the 3-year standard deviation of quarterly ROA) and 5 years (ROA(t + 5) − ROA(t + 1); the 5-year standard deviation of quarterly ROA) after the new ID selection. However, the results are mostly nonsignificant, suggesting that the performance consequences of board political capital building may not be maintained in these longer time frames. Another possible reason is that the longer time windows may include more noise, thus making it more difficult to identify the performance consequences of appointing new IDs with PBs.

All the results of these supplementary analyses are available upon request.

Discussion

Drawing on the BTOF, we theorize board political capital building as a form of problemistic search in response to performance shortfalls—performance below aspirations. We find that in the Chinese context, firms with higher performance shortfalls are more motivated to build board political capital—that is, select new IDs with PBs. We further demonstrate that selecting new IDs with upper-level PBs may be infeasible for underperforming firms, whereas selecting new IDs with lower-level PBs is more feasible for firms with performance shortfalls.

Contributions to theory and practice

First, our study contributes to the firm political connection literature in the following ways. While extant research typically treats firm political connections as capital stock (Mellahi et al., 2016), we take a fresh perspective to examine the building of political connections as a firm strategy. This new perspective allows us to more deeply examine firms’ motives behind this strategy in balancing its potential benefits and downsides. Drawing on the insights of the BTOF, we show that board political capital building represents a form of problemistic search in response to performance shortfalls—seeking potential benefits as a performance-enhancing solution while undertaking potential downsides. Considering both the positive and negative sides, our study presents a novel and more fine-grained explanation for firm political connection building based on its nature as a double-edged sword. A key implication of our study is to highlight the trade-offs involved in the strategic decision to build political connections.

Furthermore, recent research has recognized the importance of understanding the antecedents and implications of heterogeneous political connections, given the substantial differences across distinct types of political connections (e.g. Sun et al., 2015; Zhang et al., 2016) or different parties within the political regime (e.g. Kozhikode and Li, 2012; Zhu and Chung, 2014). However, less is known about how firms balance different hierarchical ranks in building political connections. By illuminating the trade-off of potential value and availability between upper-level versus lower-level political connections, our study extends the political connection literature by revealing the heterogeneous implications of political capital at various hierarchical levels. As a critical implication of our study, it illustrates the importance of exploring the heterogeneity of corporate political connections in different dimensions, such as vertical ranks, horizontal types, and different or rival political parties.

Second, our study makes several contributions to the BTOF literature. While scholars have applied the logic problemistic search to explain firm decision-making in various domains (Gavetti et al., 2012; Posen et al., 2018), applications in nonmarket domains remain nascent (Nason et al., 2018; Rowley et al., 2017). Consequently, we lack an adequate understanding of whether and how firms initiate political strategies by learning from performance feedback. Political strategies are important for firms, especially in countries where governments play a key role in the business sector, such as China (Mellahi et al., 2016). Our findings demonstrate that firms with performance shortfalls are motivated to increase board political capital building. In doing so, our study extends BTOF research by identifying a novel form of problemistic search in the political domain. While recent research has started to explore problemistic search in nonmarket forms (e.g. Rudy and Johnson, 2016; Xu et al., 2019), our study further advances this line of inquiry by linking performance shortfalls with a prevalent strategy based on the political connections of new IDs. Our study offers the important insight that underperforming firms may search for performance-enhancing solutions in the political domain and the context of director selection, thereby enriching the BTOF literature by offering new insights into where to search. A key insight of our study is the importance of further broadening the scope of problemistic search logic in explaining additional and novel firm strategies (Posen et al., 2018).

Moreover, we illustrate that building lower-level board political capital is a more feasible form of problemistic search for underperforming firms, while building upper-level board political capital could be bounded by the availability of director candidates with upper-level PBs. As discussed, prior studies have explored several political forms of problemistic search (e.g. Rudy and Johnson, 2016; Xu et al., 2019), yet thus far, the heterogeneity of political solutions in response to performance shortfalls remains unexplored. In this regard, our study extends previous research by providing the novel insight that the decision-makers of underperforming firms need to manage the trade-offs of different levels of political capital when initiating a problemistic search. More importantly, our study advances the logic of problemistic search by identifying a boundary condition derived from the feasibility of target solutions for firms with performance shortfalls. An important implication of our study is that problemistic search does not simply concern firms’ motivations to address performance problems; rather, it depends on the availability of resources and solutions to the problems. We reveal that underperforming firms find it more challenging to access higher-quality solutions. Consequently, performance shortfalls could be stickier than we expected—firms that are more motivated to seek solutions are also bounded by the more limited availability of high-quality solutions.

From a practical perspective, our study provides firm decision-makers with a deeper understanding of the potential positive and negative implications of firm political strategy. Our study theorizes board political capital building as both a potential performance-enhancing solution and an action that increases firm risks. These theoretical insights have the practical implication of helping firm decision-makers more comprehensively evaluate the benefits and downsides of their strategic decision to establish political connections. For director selection, our study suggests that candidates’ potential benefits and risks should be considered simultaneously. In this regard, our findings can help firm leaders make the most appropriate selection decisions, especially when appointing politically connected directors.

Limitations and future research

First, our study examines board political capital building as a form of problemistic search in nonmarket domains, which may not capture the full picture of firms’ nonmarket responses to performance feedback. A promising direction for future research is to explore other forms of nonmarket strategies based on the BTOF, such as corporate social responsibility (Wang et al., 2021). Similarly, firms with performance shortfalls may seek other forms of political solutions to address performance issues, such as bribery (Xu et al., 2019). In this regard, more research is needed to explore various political strategies in response to performance shortfalls.

Moreover, we use the BTOF to explain board political capital building, which focuses on an internal driver of this important firm strategy. A performance shortfall is not the only antecedent to board political capital building, which could be determined by many internal and external factors. We believe it is a significant direction for future research to further explore the environmental drivers of board political capital building, especially the institutional factors that shape the value of board political capital. It would also be intriguing to explore how board political capital building is jointly influenced by behavioral and institutional factors.

Finally, we test our hypotheses in a sample of Chinese listed firms. Although China represents an appropriate and important research context for examining board political capital, our findings based on a single country may raise questions about their generalizability to other contexts. Prior research shows the general value and risks of firm political connections in various settings (Faccio, 2006; Hillman, 2005; Okhmatovskiy, 2010; Siegel, 2007). Moreover, BTOF research shows that US firms tend to search for political solutions in response to performance shortfalls, such as corporate political lobbying (Rudy and Johnson, 2016). These findings imply that firms’ intention to search for political solutions, particularly building board political capital, in response to performance shortfalls is not specific to the Chinese context. Thus, we encourage future research to explore how firms initiate problemistic search in political or nonmarket domains when performing below aspirations in various research contexts, including China and other countries, to provide more evidence.

Conclusion

Why do firms embrace the double-edged sword of board political capital building? Drawing on the BTOF’s logic of problemistic search, we offer a novel and fine-grained explanation based on underperforming firms’ desires to seek the potential benefits of board political capital as well as their higher tolerance for its potential downside risks. We further demonstrate that due to the lack of high-quality solutions for underperforming firms, the problemistic search logic is more applicable for building lower-level board political capital and not for building upper-level board political capital. Moving beyond previous research that typically focuses on the stock of political capital, our study provides novel insights into firms’ motives behind their strategy of political capital building.

Footnotes

Appendix

Summary of variables and measures.

| Variables | Measures | |

|---|---|---|

| 1 | New IDs with PBs | The number of new IDs with PBs in the selecting year. |

| 2 | New IDs with lower PBs | The number of new IDs with PBs at lower hierarchical levels (below deputy-Bu) in the selecting year. |

| 3 | New IDs with upper PBs | The number of new IDs with PBs at upper hierarchical levels (at or above deputy-Bu) in the selecting year. |

| 4 | Negative feedback (HAs) | ROA t —historical aspirations of ROA (0.7 × ROA(t − 2) + 0.2 × ROA(t − 3) + 0.1 × ROA(t − 4)), only take negative values but set positive values as zero. |

| 5 | Positive feedback (HAs) | ROA t —historical aspirations of ROA (0.7 × ROA(t − 2) + 0.2 × ROA(t − 3) + 0.1 × ROA(t − 4)), only take positive values but set negative values as zero |

| 6 | Negative feedback (SAs) | ROA t —social aspirations of ROA (the average ROA(t − 1) of focal industry and focal province), only take negative values but set positive values as zero. |

| 7 | Positive feedback (SAs) | ROA t —social aspirations of ROA (the average ROA(t − 1) of focal industry and focal province), only take positive values but set negative values as zero. |

| 8 | Chair PB | A dummy variable of whether the board chair has PB. |

| 9 | Existing ID PB | The number of preexisting directors with PBs. |

| 10 | Departing ID PB | The number of departing directors with PBs. |

| 11 | Board size | The number of board director members. |

| 12 | CEO duality | A dummy variable indicating whether the same person holds both positions of board chair and CEO. |

| 13 | Board independence | The ratio of independent directors to all board members. |

| 14 | Ownership concentration | The Herfindahl index of the top 10 largest shareholders. |

| 15 | Absorbed slack | The ratio of selling, general, and administrative expenses to sales (SGA intensity). |

| 16 | Unabsorbed slack | The ratio of current assets to current liabilities (current ratio). |

| 17 | Potential slack | The debt-to-equity ratio (as an inverse indicator). |

| 18 | Firm size | Logarithmic total assets. |

| 19 | Firm age | The number of years since the founding of the firm. |

| 20 | Sales growth rate | The difference in sales between the current and previous years, divided by the previous year’s sales. |

| 21 | Regional marketization | The provincial marketization index, which indicates the development level of regional market institutions. |

CEO: chief executive officer; ID: independent directors; PB: political backgrounds; ROA: returns on assets; SGA: selling, general, and administrative.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.