Abstract

Acquisitions are competitive moves that disrupt an industry’s competitive structure. As a result, firms are often not passive observers of their rival’s acquisitions, but actively retaliate against such competitive moves. In this study, we explore these dynamics by analyzing one way in which multimarket contact may influence acquisition strategies, namely, the type of targets acquired. We contribute to the acquisition literature by clarifying the role that pre-acquisition competitive interdependencies play in firms’ acquisition strategies. Specifically, we suggest that high multimarket contact firms do not necessarily avoid acquisition activity. Instead, these firms are more likely to acquire targets that are less likely to incur retaliation from interconnected rivals. We also explore two important boundary conditions to this relationship: (1) the market’s competitive structure and (2) the location of the target firm. Our empirical tests of a sample of 741 bank holding companies from 1995 to 2014 offer support for our hypotheses.

Introduction

Acquisitions are seen as aggressive competitive actions (Adams et al., 2009) that shift a market’s competitive structure (Hankir et al., 2011). This shift, even if usually beneficial for all firms, is particularly favorable for the acquirer (Eckbo, 1983; Kim and Singal, 1993; Singal, 1996; Stillman, 1983). It is therefore not surprising that firms are not passive observers of their rival’s acquisitions, but instead sometimes actively retaliate against such competitive moves (Berger et al., 2004; Keil et al., 2013; King and Schriber, 2016). Firms that operate in an increasing number of overlapping markets are especially likely to face retaliation following an acquisition (Uhlenbruck et al., 2017). This observation is broadly consistent with multimarket contact (MMC) research 1 (Baum and Korn, 1996, 1999; Fuentelsaz and Gómez, 2006; Haveman and Nonnemaker, 2000). In fact, from an MMC perspective, high MMC firms are expected to refrain from engaging in acquisitions altogether, as these firms generally avoid aggressive competitive behavior to lower the risk of any potential retaliation from their interconnected rivals (Bernheim and Whinston, 1990; Edwards, 1955). Contrary to this prediction, however, prior research demonstrates that high MMC firms continue to engage in acquisitions (Keil et al., 2013; King and Schriber, 2016; Uhlenbruck et al., 2017). In this study, we begin to address this empirical conundrum by exploring how MMC affects acquisition strategies (i.e. the type of targets these companies acquire) and the conditions that impact this decision.

The arguments presented in this article seek to show that high MMC firms may not necessarily avoid acquisition activity; instead, they are more likely to acquire targets that will reduce the threat of retaliation by interconnected rivals. In the context of our study, the size of the target is a particularly important characteristic when considering how rivals may react to acquisitions (especially if we consider acquisitions within the same industry) because it has important implications for the competitive position of a firm (Josefy et al., 2015). In acquisition settings, target size influences not only the potential synergies associated with a transaction (King and Schriber, 2016), but also how a deal shapes the acquirer’s market power (Hankir et al., 2011). We argue that while acquisitions of smaller target firms create firm-level benefits for the acquirer, it does not significantly impact the acquirer’s market power and hence does not significantly change the mutual forbearance equilibrium between the industry players. In contrast, acquisitions of larger targets result in both firm-level benefits for the acquirer (and other firms in the industry) and greater shifts in the mutual forbearance equilibrium in the acquirer’s favor (Markman and Waldron, 2014). It follows that high MMC firms most likely perceive a greater threat of retaliation from interconnected rivals should they acquire a large firm. To minimize the risk of retaliation, we thus predict that highly interconnected acquirers are more likely to choose a small target. Furthermore, we explore two important boundary conditions of the relationship between the level of MMC and the size of acquisition targets. Specifically, we argue that the threat to the mutual forbearance equilibrium and hence the risk of retaliation for high MMC firms depends on (1) the market’s competitive structure and (2) the location of the target firm.

We empirically test these theoretical predictions in the US banking industry, which provides an ideal context for two main reasons. First, much of the MMC literature has analyzed the service sector in general and the banking industry in particular (Fuentelsaz and Gómez, 2006; Greve, 2000, 2006; Hannan and Prager, 2004, 2009; Haveman and Nonnemaker, 2000) and has already shown that MMC influences strategic behavior. As such, we can assume that MMC is, indeed, a relevant phenomenon, and our research can focus on behavior specifically related to mergers and acquisitions (M&A). Second, the classic forbearance hypothesis rests on the perfect observability assumption (Bernheim and Whinston, 1990). Observability conditions are particularly well met in banking markets because of the stringent reporting requirements (Hannan and Prager, 2009). As such, firms can observe their rivals’ acquisitions, allowing them to monitor their compliance with forbearance effectively. Based on the analysis of the acquisition activity of 741 large bank holding companies (BHCs) from 1995 to 2014, we find support for our predictions.

Our study makes two contributions to the literature. First, we add to acquisition literature, which has recently started to consider (1) how competitive interdependencies affect the timing of a firm’s actions within periods of high merger activity or merger waves (Haleblian et al., 2012), (2) the likelihood of competitive responses to a focal firm’s acquisition strategy, as well as (3) focal firm’s tactics to mitigate the adverse effects of these competitive responses (Keil et al., 2013; King and Schriber, 2016; Uhlenbruck et al., 2017). While previous research offers important insights about the impact of acquisitions on an industry’s dynamics and rivals’ responses to the focal firm’s acquisition activity post-acquisition, these studies take little note of pre-acquisition competitive interdependencies. Our article focuses specifically on the pre-acquisition landscape, which allows us to complement the studies on the post-acquisition activity by clarifying the role of pre-acquisition competitive interdependencies on acquisition activity. In particular, we argue and empirically show that, while high MMC firms continue to engage in acquisitions, they do so carefully and acquire targets that minimize the risk of retaliation from their interconnected rivals. In addition, we also consider two boundary conditions of the relationship between the pre-acquisition competitive landscape and the acquisition strategy by investigating the effect of pre-acquisition market concentration levels and the location of the acquirer and the target.

Second, our study also has implications for the MMC literature. Prior research on the impact of MMC on firm strategy suggests that high MMC firms may reduce competitive activity due to the fear of retaliation (e.g. Yu et al., 2009). Though the mutual forbearance hypothesis has gained empirical support in many domains (Yu and Cannella, 2013), our study draws attention to the possibility that MMC may influence strategic choices in a greater variety of ways (e.g. Greve, 2008; Ryu et al., 2020). In other words, even if firms that have high levels of competitive interdependencies carry out acquisitions, MMC influences the type of acquisitions these firms are pursuing. At a broader level, therefore, our study suggests that high levels of MMC may not always deter firms from initiating certain competitive moves; instead, MMC may explain variety within these competitive moves.

Theory and hypotheses

Acquisitions are a vital organizational strategy and an important vehicle for firm growth, among others. Although previous research has studied various factors that influence corporate acquisitions (for a review, see Haleblian et al., 2009; Welch et al., 2019), the interest in the impact of competitive interdependencies on corporate acquisition strategies is more recent. For instance, some studies on this topic examine the implications of a focal firm’s acquisition on its rivals’ performance (Elango et al., 2018). They find that the value of rival firms increases if the focal firm’s value also increases after the acquisition announcement (e.g. Cai et al., 2011; Shahrur, 2005), since a positive market reaction to a focal firm’s acquisition announcement signals future growth potential (Gaur et al., 2013) or consolidation in a market (Clougherty and Duso, 2009). A related stream of literature focuses more specifically on rivals’ competitive reactions to the focal firm’s acquisition activity (Keil et al., 2013; King and Schriber, 2016; Uhlenbruck et al., 2017). These studies demonstrate that rivals are unlikely to be passive observers of other firms’ acquisitions; instead, they sometimes respond with competitive actions. This observation is largely consistent with prior research suggesting that firms competing in multiple markets are more likely to face competitive retaliation and escalation should they initiate a competitive move.

At the same time, MMC theory suggests that firms that interact with their rivals in more markets are less likely to act aggressively (Bernheim and Whinston, 1990; Edwards, 1955). The basic intuition behind this prediction is that as MMC increases, firms become more familiar with each other’s behavior, and they can also credibly threaten to retaliate against rivals’ aggression because they can respond not only in the markets in which they have been attacked but also in the other markets in which they compete. In line with this logic, it has indeed been shown that there are fewer competitive attacks involving high MMC firms (Young et al., 2000; Yu and Cannella, 2007; Yu et al., 2009), and if competitive action is undertaken, a possible reaction of the rivals is not only likely but also faster (Young et al., 2000). To deter competitive attacks, MMC firms often establish footholds in each other’s markets (Hsieh and Vermeulen, 2014; Upson et al., 2012), create spheres of influence (Baum and Korn, 1996), reciprocate contacts (Gimeno, 1999), and imitate each other’s market entry behavior to create contacts (Hsieh and Vermeulen, 2014). Considered together, previous MMC research suggests that competitive interdependencies soften competition, as high MMC firms are less likely to act aggressively toward their rivals.

Even though MMC theory has seen limited direct application in the acquisition literature (Yu and Cannella, 2013; for notable exceptions, see Arie et al., 2017, and Bilotkach, 2011), it has been established that acquisitions can be considered a competitive action (Keil et al., 2013) given that “any advantages to acquiring firms likely come at the expense of competitors that are also pursuing competitive advantage” (King and Schriber, 2016: 109). Hence, it could be expected that when announcing an acquisition, high MMC firms will be confronted with competitive responses. Furthermore, since high MMC firms’ acquisitions directly affect more rivals, a greater number of rivals will be aware of the acquisition and may perceive the acquisition as an aggressive move. In support of this logic, Uhlenbruck et al. (2017) show that rivals are more likely to retaliate if the acquisition affects one of its primary markets. Given that such competitive responses are likely to affect the value-creating potential of a given acquisition (Haleblian et al., 2009), and considering that high MMC firms are particularly likely to face retaliation, it would seem plausible that high MMC firms avoid engaging in acquisitions. However, as noted above, many firms—even high MMC firms—continue to engage in acquisitions despite the threat of retaliation. This observation raises important theoretical questions about the alternative avenues through which pre-acquisition competitive interdependencies are reflected in corporate acquisition strategies.

A particularly important consideration in the pre-acquisition phase relates to the target firm’s characteristics (Welch et al., 2019), especially its size. Indeed, when considering pre-acquisition competitive interdependencies, the target firm’s characteristics are particularly important because they influence both the competitive dynamics and the structure of a market following the transaction (Keil et al., 2013; Uhlenbruck et al., 2017). For example, Hankir et al. (2011) show that stock market reactions of bidders, targets, and rivals to acquisition announcements are positive if markets expect industry consolidation as a result of the deal. This effect is particularly strong when relatively large targets are acquired. In addition, organizational size is a key determinant of the visibility of a competitive move and hence how aware rivals may be of such a move (e.g. Baum and Korn, 1999), and target size is an especially prominent, clearly visible characteristic that indicates the acquirer’s relative market power increase (Josefy et al., 2015). Hence, the target firm’s size will influence the degree to which interconnected rivals will perceive a transaction as posing a competitive threat or whether the deal may be considered less disruptive to the status quo.

Moreover, focusing on target firm size is also meaningful as it captures the degree of the benefits that the acquirer can expect from a deal. That is, acquiring a smaller firm may allow the focal firm to realize some firm-specific economic gains associated with synergies and market power, albeit smaller in magnitude (Josefy et al., 2015; King and Schriber, 2016). Said differently, even if the focal firm may shy away from acquiring a larger target due to the fear of retaliation, some degree of synergies and gains in market power can also be achieved by acquiring a smaller firm, especially if we consider acquisitions within the same industry. Following these insights, we focus on analyzing how pre-acquisition competitive interdependencies are reflected in corporate acquisition strategies and, in particular, target size. We explain our reasoning in detail below.

MMC and acquisition target size

As noted above, existing research suggests that high MMC firms face a particularly high risk of retaliation from interconnected rivals should they initiate competitive action. Given that acquisitions can be seen as competitive moves, therefore, high MMC firms should perceive a high risk of retaliation should they engage in an acquisition. Although there is a general expectation that interconnected rivals retaliate to competitive moves, they may not respond to all competitive activity in the same manner. Specifically, interconnected rivals are unlikely to respond to less significant deviations from mutual forbearance norms (Greve, 2008) as there is less at stake for them (King and Schriber, 2016). Based on these insights, we propose that high MMC firms acquire smaller targets to avoid potential retaliation from interconnected rivals.

One explanation behind this proposition stems from MMC theory, which suggests that firms that compete in multiple markets recognize the benefits of allowing each other spheres of influence (Baum and Korn, 1996). In other words, high MMC firms partition the market in a way that reduces the risk of unwanted rivalry (Bernheim and Whinston, 1990; Edwards, 1955). In practice, this means that high MMC firms maintain only small positions in some markets (Baum and Korn, 1996; Hsieh and Vermeulen, 2014; Upson et al., 2012) and, in return, interconnected rivals do the same in other markets. The decision about which markets will be controlled by which high MMC firm depends on these firms’ relative efficiency in those markets (Baum and Korn, 1999; Bernheim and Whinston, 1990). Firms tend to let those markets in which interconnected rivals are relatively more efficient be dominated by those rivals, and vice versa (Gimeno, 1999); this situation can be defined as a mutual forbearance equilibrium (Bernheim and Whinston, 1990).

The acquisition of a large target firm has likely a greater potential to disturb the aforementioned mutual forbearance equilibrium because it could shift the focal firm’s efficiency across markets relevant to interconnected rivals (Josefy et al., 2015). For example, the acquirer may enjoy efficiency gains following the transaction that place rivals at a competitive disadvantage in both factor and product markets (Kim and Singal, 1993). In other words, while any horizontal acquisition may allow the acquirer to realize efficiency gains, these gains are higher as target firm size increases (Hankir et al., 2011; Josefy et al., 2015). As noted above, spheres of influence reflect the focal firm’s efficiency in a given market relative to its interconnected rivals. A potential significant efficiency gain associated with an acquisition of a large target may result in a situation where rivals lose their efficiency advantage relative to the focal acquiring firm. In other words, such a deal threatens the pre-acquisition mutual forbearance equilibrium. Since interconnected rivals are more likely to respond aggressively to competitive actions that pose a threat to the mutual forbearance equilibrium (Markman and Waldron, 2014), we expect that the focal firm perceives a relatively greater risk of retaliation should it acquire a large target firm. This suggests that high MMC firms that engage in an acquisition are more likely to acquire smaller target firms than low MMC acquirers. In support of this logic, King and Schriber (2016) argue that “smaller acquisitions or a blend of strategic moves that do not cross the threshold for a competitor response may desensitize competitors or make it less alarming” (pp. 114–115). Thus, the acquisition of a smaller firm is “likely to make a single acquisition (strategic move) less noteworthy to competitors” (King and Schriber, 2016: 115).

At the same time, it is important to note that the acquisition of large targets may result in a more consolidated market in which the remaining firms have greater market power (Sapienza, 2002), thereby softening market competition. As a result, all remaining firms are able to appropriate more economic value if their pricing power increases (Eckbo, 1983; Stillman, 1983). Kim and Singal (1993) show that while increases in market power should benefit the industry as a whole, firm-specific efficiency gains associated with horizontal acquisitions are more significant (see also Singal, 1996), particularly when the longer-term effects of acquisitions are taken into account (Focarelli and Panetta, 2003). As such, while all firms may benefit from a less competitive market following an acquisition, the acquirer enjoys additional benefits from firm-specific efficiency gains that could disturb an existing mutual forbearance equilibrium, especially if the target firm is relatively large (Hankir et al., 2011). Thus, although the acquisition of large target firms is often beneficial for all remaining firms in the market due to increased market consolidation, it is likely to be particularly favorable for the acquirer (Eckbo, 1983; Focarelli and Panetta, 2003; Kim and Singal, 1993; Singal, 1996; Stillman, 1983). Thus, interconnected rivals are expected to retaliate despite these industry-wide gains because of their perceived threat to the mutual forbearance equilibrium (Markman and Waldron, 2014).

In summary, from a mutual forbearance perspective, our discussion suggests that high MMC firms’ perceived risk of retaliation should be particularly high if they acquire a large target. The reason for this is that high MMC firms’ interconnected rivals are (1) more likely to consider the acquisition of large targets to be an aggressive competitive action that will disrupt the mutual forbearance equilibrium and hence (2) increase rivals awareness of the competitive implications of such a strategic move. At the same time, the acquirer is likely to enjoy some firm-specific efficiency gains that dominate market-wide market power gains and thus come at the expense of its rivals. Such firm-specific efficiency gains are likely to be present even if they acquire relatively smaller target firms, but the stakes for interconnected rivals are much smaller in these situations, thereby reducing the probability of retaliation (King and Schriber, 2016). These rivals are, therefore, more likely to retaliate to acquisitions involving large target firms. Given that any competitive responses will negatively affect the value-creation associated with acquisitions (Haleblian et al., 2009), high MMC firms seeking to engage in acquisitions may seek to mitigate the threat of competitive retaliation by acquiring smaller target firms. Formally,

Hypothesis 1. Among firms that engage in acquisitions, MMC is negatively related to target firm size.

MMC, market concentration, and target size

So far, we have argued that high MMC firms are at a greater risk of retaliation when they acquire larger targets, and thus, should they decide to engage in an acquisition, they prefer smaller targets. However, the threat to the mutual forbearance equilibrium, hence the probability that rivals retaliate, most likely differs across markets (Bernheim and Whinston, 1990; Jans and Rosenbaum, 1997; Singal, 1996). In particular, we argue that industry-wide gains due to increases in market power are more pronounced in more concentrated markets (Haveman and Nonnemaker, 2000; Heggestad and Rhoades, 1978; Jans and Rosenbaum, 1997; Singal, 1996) and, thus, the perceived risk of retaliation associated with the acquisition of larger target firms should be lower in such markets. In other words, MMC’s effect on target size should become weaker as industry concentration increases.

We have argued above that acquirers can achieve efficiency gains when acquiring a firm, and thus acquisitions tend to threaten existing mutual forbearance equilibria. However, economic literature has long discussed the two countervailing effects of market power (Stigler, 1950) and efficiency (Williamson, 1968) that acquisitions can have on rivals (Duso et al., 2013). Specifically, research shows that the extent to which the acquirer’s firm-specific benefits (due to efficiency gains) dominate the collective benefits (due to an increase in market power) depends on the pre-acquisition market structure. That is, acquirers’ firm-specific benefits are less dominant if the structure of the market allows all firms to benefit from more market power (Prager and Hannan, 1998)—this is the case when there are fewer competitors in the market (Gugler and Szücs, 2016). In line with this idea, Clougherty and Duso (2009) show that firms experience significant abnormal returns to rivals’ acquisition announcements, especially if such acquisitions increase market concentration. Thus, in markets that are already more concentrated prior to the focal acquisition, all remaining firms benefit to a larger extent from the fact that the market becomes less competitive as a result of this acquisition (relative to firms in markets with low levels of market concentration before an acquisition). This effect is even stronger if larger targets are acquired (Gugler and Szücs, 2016) or when banks acquire targets with larger market shares (Sapienza, 2002).

Taken together, these arguments suggest that when market concentration before an acquisition is high, the acquirer’s potential efficiency gains following an acquisition are less dominant since all market participants achieve significant increases in market power. In contrast, in markets with low market concentration before an acquisition, remaining firms’ increase in market power is less consequential, and firm-specific efficiency gains that accrue to the acquirer will thus be even more dominant. Therefore, the degree to which large acquisitions disrupt the mutual forbearance equilibrium is lower in markets characterized by high concentration before an acquisition. It follows that the acquisition of a relatively larger target poses a lower threat to the focal firm’s interconnected rivals. In turn, high MMC firms’ perceived risk of retaliation is lower in such markets. We thus expect that, if the target firm is operating in a highly concentrated market, high MMC firms perceive less need to mitigate rivals’ competitive responses by acquiring smaller targets. Formally,

Hypothesis 2. Among firms that engage in acquisitions, there is a weaker negative effect of MMC on target firm size if the target operates in a market characterized by higher market concentration.

MMC, target location, and target size

Above, we have argued that the relationship between MMC and target market size depends on target market concentration. Another salient factor that is likely to influence the perceived threat of retaliation associated with acquiring a large target is the target firm’s geographic location because it is likely to affect the acquirer’s firm-specific efficiency gains. Specifically, the acquirer’s firm-specific efficiency gains are likely to be greater if the target is located in the same state as the focal firm.

The reason for this is that, when acquiring in a different state, the acquirer faces a novel, unfamiliar institutional environment, and, as such, it is more difficult to realize firm-specific gains. The institutional environment is often assessed at the national level, yet it also varies between states (Pe’er and Gottschalg, 2011). These institutional differences are ever more pronounced for banks because of the dual banking system in which most banks are regulated by state and federal regulators (Agarwal et al., 2014). Thus, entering a new state exposes banks to different regulatory requirements and interpretations of the same regulatory rules (Agarwal et al., 2014). Such differences between states can hinder firm-specific gains by making it more challenging to integrate the target firm fully. For instance, increased coordination costs have been shown to negatively impact integration and impede the flow of complementary resources between acquirers and targets (Chakrabarti and Mitchell, 2013). For acquisition integration to be successful, the acquirer must achieve full cooperation from both top management and employees, more efficient decision-making, and reduce the chances of conflict, which is particularly important when managing subsidiaries in distant locations (Gomes-Casseres, 1990). A lower level of integration, in turn, implies that potential benefits are not realized, or resources need to be duplicated, which again lowers the efficiency gains for the acquirers (Haspeslagh and Jemison, 1991). In line with these conjectures, Kim and Finkelstein (2009) found that complementarities between acquirer and target do not necessarily result in efficiency gains if the target is located in out-of-state markets.

Second, being located in a different state can increase information costs (Bertrand et al., 2007). In turn, information cost impacts initial awareness of potential acquisition targets (Rangan, 2000). Indeed, it has been shown that the greater the distance between the acquirer and the target, the fewer targets are acquired (Chakrabarti and Mitchell, 2013; Chen et al., 2018; Ragozzino and Reuer, 2011). Moreover, higher information costs make it difficult for an acquirer to assess the target’s true worth and incentivize the target to misrepresent its value. To obtain credible information, acquirers need contacts with important agents, such as other buyers, suppliers, and market intermediaries, with firsthand access to such information, which are easier to obtain if the potential target is nearby (Ragozzino, 2009). Frequent visits and informal talks with employees and managers of the target firm can offer important information about the true worth of the target and the difficulties of managing an acquired entity (Kang and Kim, 2008). Thus, Ragozzino and Reuer (2011) show that remote acquirers face a greater risk of adverse selection due to heightened information asymmetry. Also, Grote and Rucker (2007) find that acquirers earn greater returns on proximate targets because they have access to superior information, which helps them minimize the ex-ante problems of adverse selection and the ex-post problems of moral hazard. This suggests that acquirer and target location, by mitigating information asymmetry for the acquirer, may influence several facets of the acquisition, which in turn impact efficiency gains for the acquirer.

In sum, these arguments suggest that the firm-specific efficiency gains are even more likely to dominate any industry-wide gains (due to an increase in market power) if the target is located in the same state. Hence, when acquiring a large target, a high MMC firm’s perceived risk of retaliation from interconnected rivals should be even greater if the target firm is located in the same geographic market—in our case, the same state. In this situation, large acquisitions disrupt the mutual forbearance equilibrium to a greater extent. Therefore, acquirers will perceive a greater need to mitigate rivals’ competitive responses by acquiring smaller targets. As such, we expect that the negative relationship between MMC and target firm size is stronger if the target is located in the same state as the focal firm. Formally,

Hypothesis 3. Among firms that engage in acquisitions, there is a stronger negative effect of MMC on target size for in-state acquisitions than for out-of-state acquisitions.

Methodology

Research context and sample

We tested our theoretical predictions on a sample of large-top holder United States (US) BHCs 2 that engaged in at least one acquisition of another bank between 1995 and 2014. Although existing research already explores the effect of MMC on bank strategy (Fuentelsaz and Gómez, 2006; Greve, 2000, 2006; Hannan and Prager, 2004, 2009; Haveman and Nonnemaker, 2000), our empirical approach differs from this work in two significant ways. First, we focus on corporate parents because major strategic decisions such as acquisitions are likely to be made at this level. Others (e.g. Hannan and Prager, 2004, 2009) have analyzed commercial banking organizations even if they form part of the same BHC. However, these approaches do not consider that decisions about forbearance are most likely taken at the highest levels of the organization (Sengul and Gimeno, 2013). Second, we include all domestic-top holders that are registered as either BHCs or financial holding companies (FHCs) with the Federal Reserve Board (FRB). In contrast, previous studies have focused on either a subset of BHCs (e.g. Heggestad and Rhoades, 1978) or banks in a subset of markets (Barnett et al., 1994; Greve, 2000, 2006; Haveman and Nonnemaker, 2000; Mester, 1987). Focusing on such subsets can be problematic since this might underestimate the level of MMC that firms experience and ignore possible interdependencies that influence competitive behavior in markets that have not been included in the analysis (Sengul and Gimeno, 2013). Drawing on the entire domestic population of BHCs thus allows us to overcome some of these shortcomings.

In addition, the US banking industry saw significant deregulation following the introduction of the Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994, as it lifted restrictions on interstate banking and branching. As a result of these regulatory shifts, BHCs were allowed to acquire banks in any state after 29 September 1995, even if state laws had formerly prohibited this. Furthermore, after 1 June 1997, BHCs could merge banks from different states into the same branch network. Banking markets were hence not constrained anymore (Hannan and Prager, 2004). The restrictions on BHCs’ operations before deregulation also meant that MMC across states might have been comparatively low. Indeed, only 3.2% of BHCs active in 1993 operated in multiple states; of those, about 62% were only active in two states, while only about 3% were active in ten or more states (Savage, 1993). Thus, our observation period begins after 29 September 1995, when the Act became effective and ends in 2014.

We collected data from the regulatory filings submitted by BHCs to the FRB and the Federal Deposit Insurance Corporation. In particular, we used the Business Combinations database, which is part of the Reports of Structure Changes resource, to obtain information about the acquisition activities of BHCs. We also gathered information from the end-of-year Consolidated Financial Statements for Holding Companies (as reported on the FR Y-9 forms) and the Consolidated Reports on Conditions and Income (also known as the Call report) filed by each bank. Data on the sector acquisitions variable, which we used in our selection equation (see Online Supplementary Materials), were obtained from Thomson Reuters’ SDC Platinum database. The Bureau of Economic Analysis provided information for constructing the state-level variables from the regional accounts data.

Operationalization of variables

Dependent variable

The dependent variable, target size, is measured as the target bank’s total value of assets in millions of dollars at the time of acquisition. We used the total number of full-time equivalent employees as an alternative measure of target size in sensitivity tests. The results remain consistent and are available in the Online Supplementary Materials.

Independent variable

The independent variable used in this study is MMC. Gimeno and Jeong (2001) argue that MMC needs to be measured at a theoretically relevant level. Our theoretical arguments and predictions imply a firm-level measure of MMC. As such, we followed prior research (Boeker et al., 1997; Gimeno and Jeong, 2001) by constructing a firm-level measure by aggregating dyadic contacts to the firm-in-market-level and then aggregating this measure to the firm level. However, in the context of acquisitions, the most relevant contacts are likely to be those with rivals that are directly affected by the acquisition, rather than all rivals that the firm faces in all of its markets. To account for this, we only compute the MMC of the focal firm with rivals that are present in the target state and with whom the focal firm meets in at least one state prior to the transaction. MMC for BHC i at time t–1 is given by

where Iin is an indicator variable set to 1 if BHC i is active in the focal market n and to 0 otherwise. Ijn is an indicator variable set to 1 if BHC j is active in the focal market n and to 0 otherwise, but only if BHC i and BHC j share at least one market prior to the acquisition and if BHC j is present in the state in which the target is headquartered. Iim is an indicator variable set to 1 if BHC i is active in market m and to 0 otherwise. Ijm is an indicator variable set to 1 if BHC j is active in market m and 0 otherwise but only if BHC i and BHC j share at least one market prior to the acquisition and if BHC j is present in the state in which the target is headquartered. NFm is the number of BHCs in market m. To measure MMC, we considered both deposit and loan markets at the state level in each state in which the focal firm is active (see Table A16 in the Online Supplementary Materials for the full list of markets).

Moderating variables

The first moderating variable, target market concentration, is measured in line with the Herfindahl–Hirschman Index, based on asset concentration in the state in which the acquisition target is headquartered. We combined assets held by the same firm in different banks and branches in the same state. Target market concentration for state k at time t–1 is given by

where Si is the market share of bank i in market k and N is the number for banks in market k.

The second moderating variable is target location. This variable was operationalized using an indicator variable that takes the value of 1 if the acquiring bank and the target bank are headquartered in the same state and 0 otherwise.

Control variables

We measured all but the transaction-level control variables at time t–1. We controlled for acquirer acquisition experience, measured as an exponentially weighted rolling sum of acquisitions by focal BHC i. By applying an exponential weighting to the sum (with a discount factor of alpha = 0.3), this measurement reflects that more recent experiences may have a stronger effect than older experiences (Ingram and Baum, 1997; Shipilov, 2009). To control for resource availability, we used three different variables (Lee and Lieberman, 2010): acquirer size, measured as the logarithm of total assets of BHC i; acquirer age, measured as the number of years since BHC i became active; and acquirer past performance, measured as the average performance of BHC i from time t–3 to time t–1. To account for the possibility of managerial self-interest, we included acquirer slack, measured as the ratio of the BHC’s total assets to total liabilities. We further controlled for acquirer resource flows, measured as the net cash flow in billions from investing activities of the BHC i in all its subsidiaries. If the net cash flow is negative, this indicates that the focal BHC is constraining resource flows; a positive net cash flow indicates that the focal BHC is delegating more decision-making authority to its subsidiaries (Sengul and Gimeno, 2013). We also included a variable that accounts for the difficulty in coordinating activities between multiple units: acquirer bank count, measured as the total number of banks in the BHC. Furthermore, we included a dummy variable, financial holding indicator, which is set to 1 if the firm was registered as an FHC with the FRB and to 0 otherwise.

We also controlled for the focal BHC’s strategic similarity, measured as the Mahalanobis distance from the industry average for each BHC i where the reference values are derived from the percentage of assets held in the 23 loan and deposit markets listed in Table A16 in the Online Supplementary Materials. It could also be the case that sequences of competitive interactions reveal tit-for-tat acquisition moves (Karnani and Wernerfelt, 1985). We, therefore, included the variable competitor acquisitions, which is measured as the number of acquisitions by firms other than the focal BHC i in the 2 years before the focal acquisition. By taking into account the 2 years before the focal acquisition, this measurement allowed for the possibility that firms may take some time to respond to rivals’ acquisitions.

To account for the market condition that a focal BHC i faces in the state markets in which it is active, we included state-level control variables. In particular, the macroeconomic environment could influence acquisition activity (Choi and Jeon, 2011; Harford, 2005). As such, we used the year-on-year gross domestic product (GDP) growth rate in each state in which the focal BHC i had a market presence. The variable average state GDP growth averaged these growth rates across states. Similarly, we created a variable called average per capita state income growth. In addition, we included several state fixed effects to mitigate estimation bias resulting from time-invariant heterogeneity between states; we included target state, acquirer state, and BHC headquarter state fixed effects to account for heterogeneity across states.

We also included several factors at the transaction level. Banking activities are often concentrated in urban centers, so BHCs may acquire larger targets to access a certain urban area. Therefore, we included an indicator variable, target is urban, taking the value of 1 if the target is headquartered in a core-based metropolitan statistical area and 0 otherwise. It may also be the case that after an acquisition, a BHC may acquire further–possibly smaller–targets. To control for this effect, we included a variable called time since last acquisition, which is operationalized as the number of years since the acquirer’s last acquisition. For the first acquisition of a focal firm during the observation period, we use a value of 0 (we also use the number of years since the beginning of the observation period for these observations and obtain consistent results in sensitivity tests). To account for the effect of information asymmetries on target size (Chakrabarti and Mitchell, 2016), we included a variable labeled distance to target to control for geographic distance, measured as the great-circle distance (WGS84 ellipsoid) between the headquarters of the acquirer and the target in thousands of kilometers. Finally, it may be easier for a firm to acquire a larger target when the target is failing. Thus, we include an indicator variable called target is failing that takes the value of 1 if the target failed and 0 otherwise. Finally, we include year fixed effects.

Analyses and results

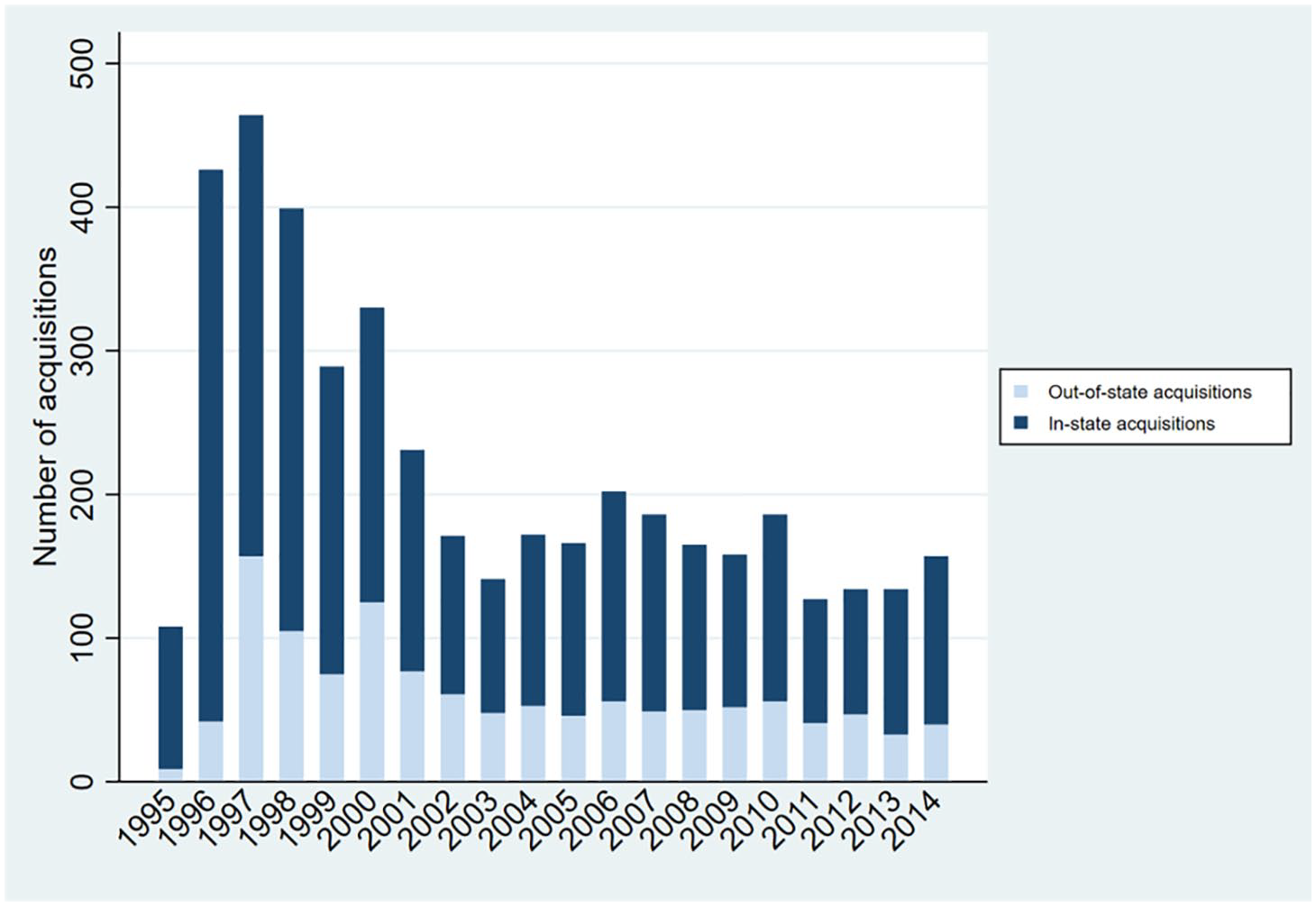

Table 1 presents the descriptive statistics for all variables, and Figure 1 provides a visual summary of the acquisition activity in the sample. The sample consisted of 741 firms that carried out a total of 4346 acquisitions. 3 As can be seen in Figure 1, the number of acquisitions per year ranged from 108 (in 1995) to 464 (in 1997). 4 Firms in the sample conducted between 1 and 169 acquisitions during the study period. In addition, in-state acquisitions (3124) were more frequent than out-of-state acquisitions (1222). However, the number of both in-state and out-of-state acquisitions dropped notably after 2001.

Descriptive statistics.

SD: standard deviation; GDP: gross domestic product.

Log-transformed; N = 4346; In-state acquisitions N = 3124; out-of-state acquisitions N = 1222.

Distribution of acquisition activity (1995–2014).

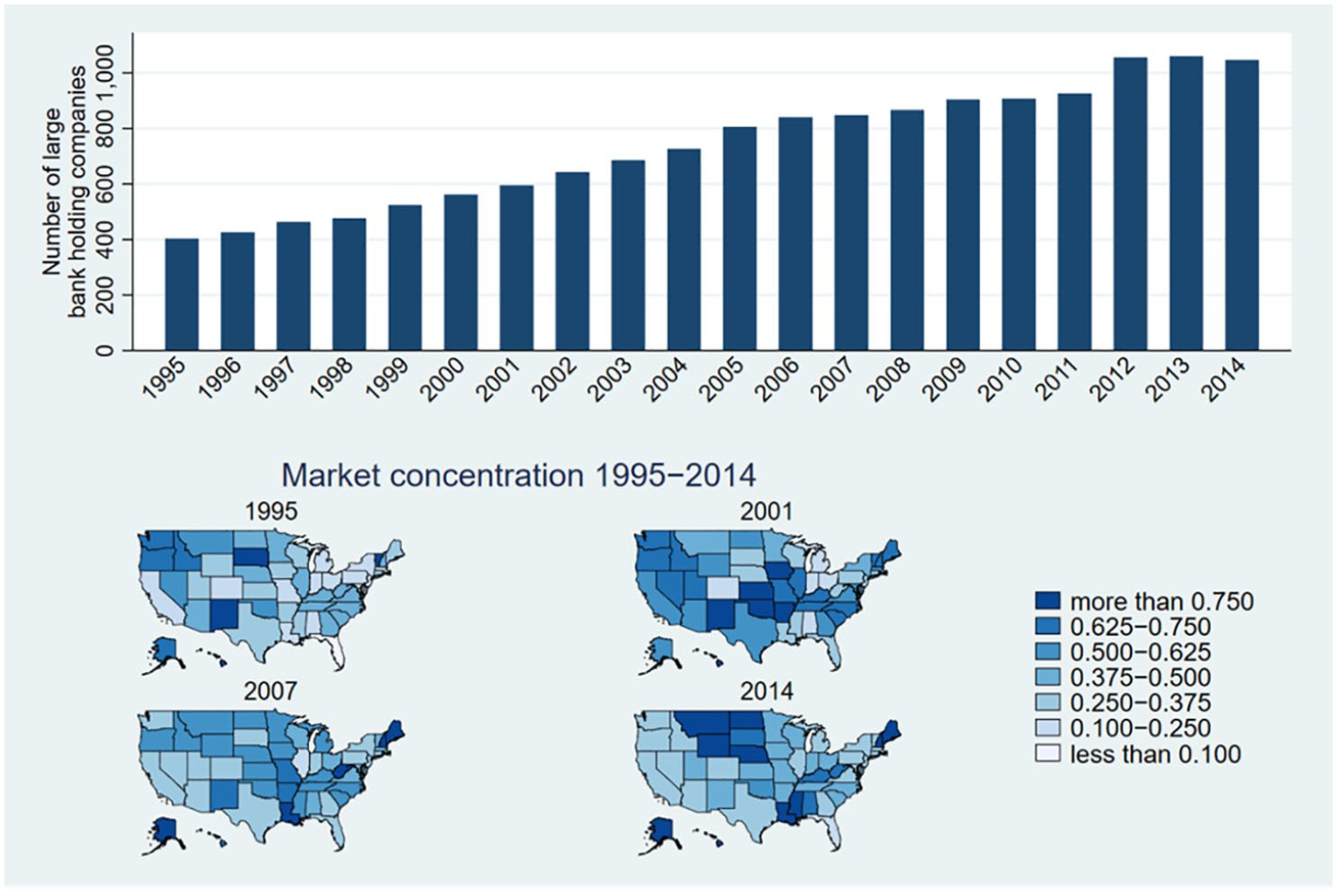

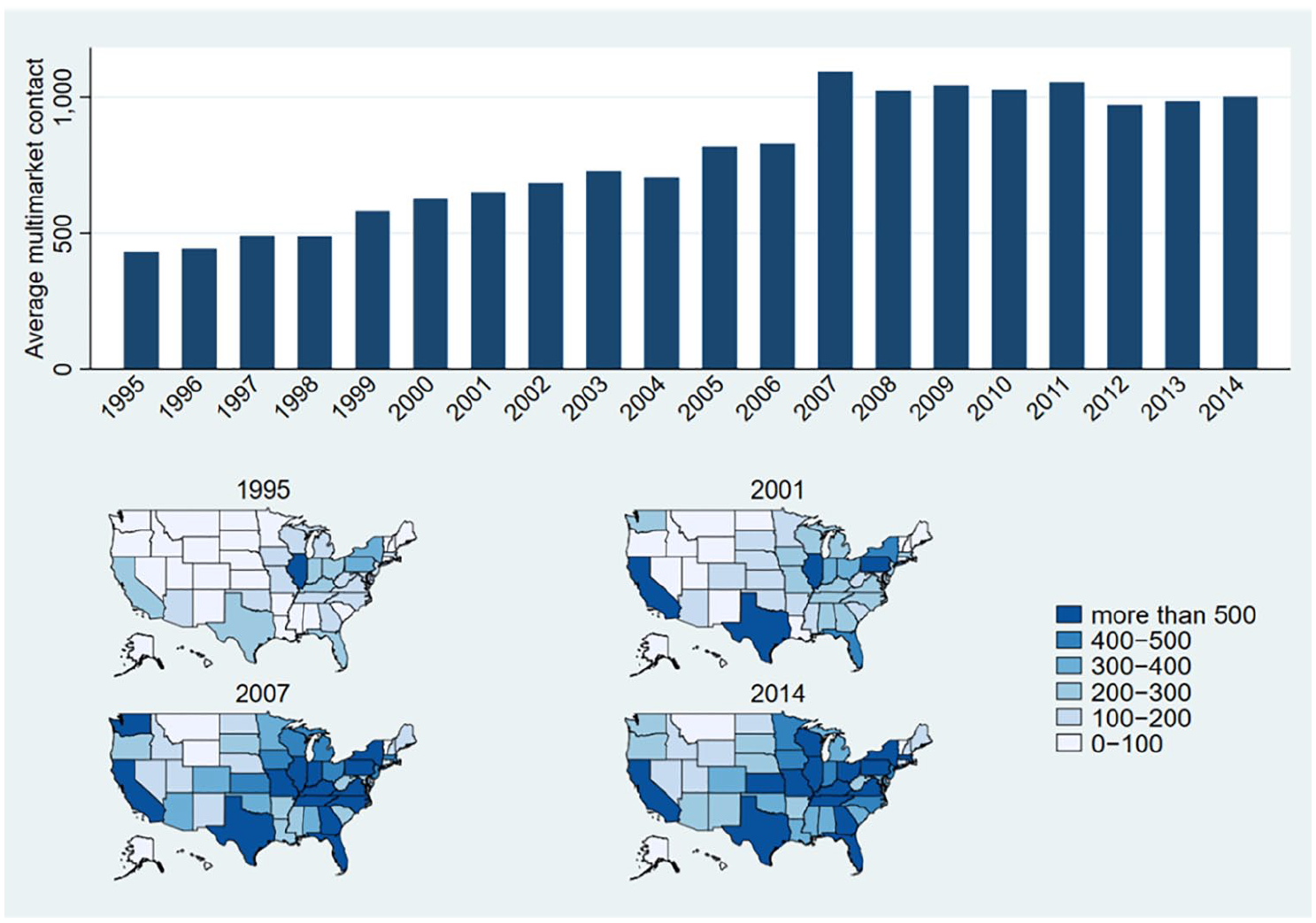

We further explore how the competitive environment has changed over the sampling period in Figure 2. The number of large BHCs increased substantially from 403 in 1995 to 1047 in 2014. Figure 2 also shows that market concentration has increased in most states over time. To complement this analysis, we also investigated how MMC developed over the sampling period. 5 Figure 3 highlights that at the same time as the number of large BHCs increased, BHCs’ average MMC also increased steadily until 2007 and remained relatively stable since. Looking closer at how average MMC is distributed across states, it is clear that while average MMC also increased in most states, it increased particularly in eastern states.

The competitive environment in the banking industry (1995–2014).

Multimarket contact among large bank holding companies (1995–2014).

In Table 2, we present the pairwise correlations. As can be seen from this table, we observe some significant correlations between variables, with the correlation between competitor acquisitions and MMC (r = 0.86) being the highest. To further investigate whether these correlations were likely to affect our results, we assessed collinearity using variance inflation factors (VIFs). One widely used threshold for serious multicollinearity is a VIF of 10 (Cohen et al., 2003). Our test demonstrated VIFs ranging from 1.03 to 5.52, with a mean VIF of 1.87.

Correlations.

GDP: gross domestic product.

Log-transformed; N = 4346; All correlations greater than ± 0.03 have a p-value < 0.05.

As can be seen from Table 1, our dependent variable, target firm size, is not normally distributed (mean = 1628.09, SD = 12,706.16, minimum = 0.79, and maximum = 510,083.00). This posed challenges in modeling the dependent variable using standard regression approaches, such as ordinary least squares regression (Santos Silva and Tenreyro, 2006). For example, using a log-transformed-dependent variable can lead to biased estimates, especially in the presence of heteroscedasticity. A modified Wald test for groupwise heteroscedasticity suggested that heteroscedasticity was present in our data. In addition, as outlined above, we needed to account for various fixed effects. An effective way to deal with such a data structure is to use a maximum likelihood generalized linear model with a log link function, such as Poisson pseudo-likelihood regression (Correia et al., 2019; Santos Silva and Tenreyro, 2006, 2010). It is also worth noting that these models are suitable for non-count data (Verdier, 2016; Wooldridge, 1999). We thus used Poisson pseudo-maximum likelihood regression in our estimation (implemented using the ppmlhdfe command in Stata 16).

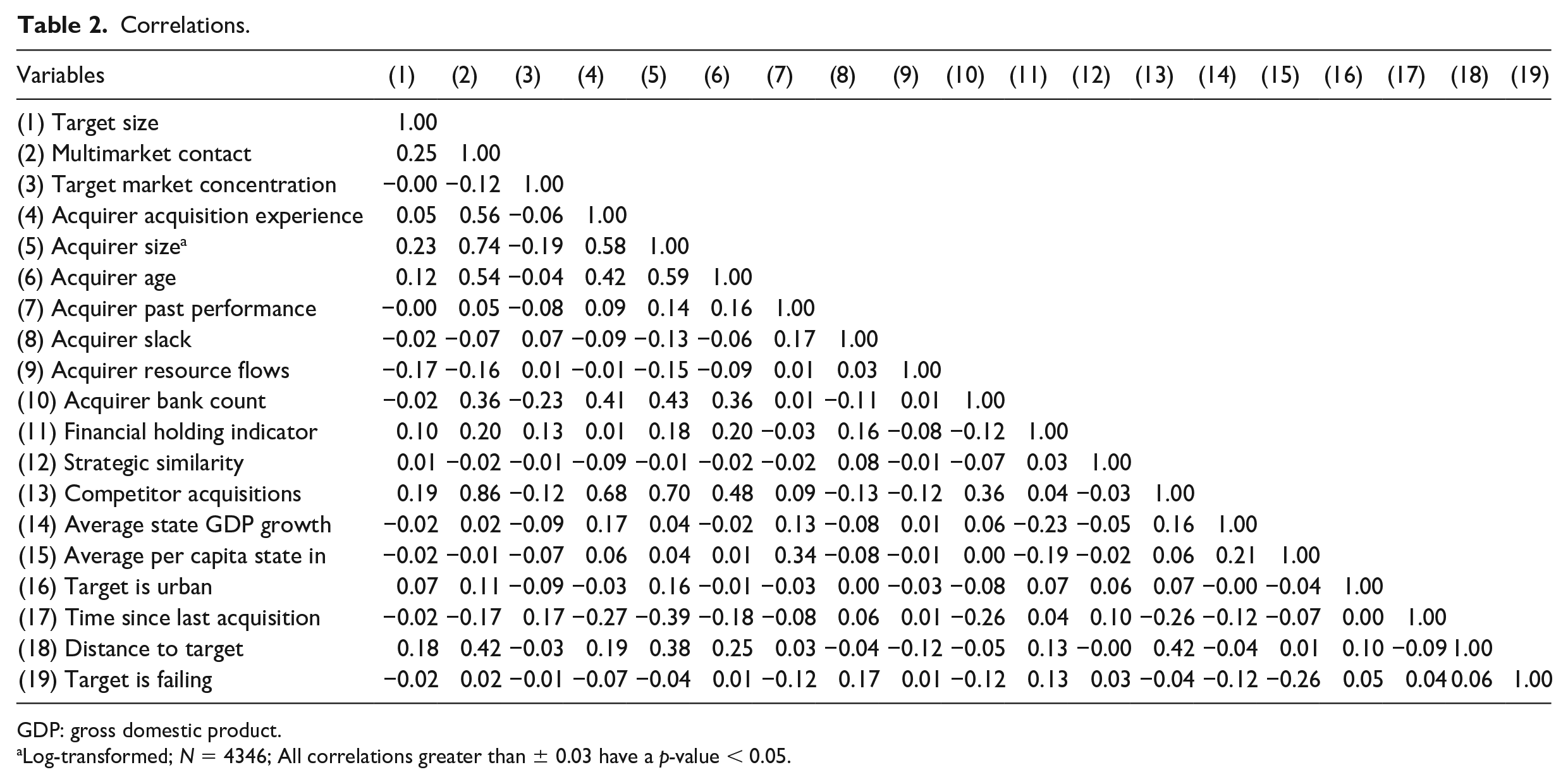

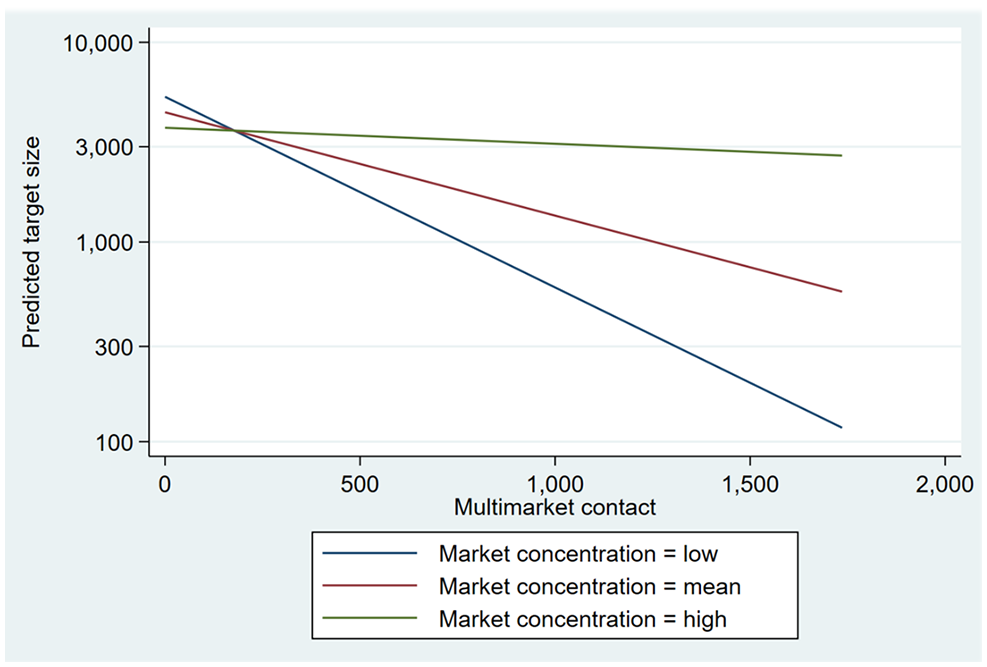

Table 3 presents the Poisson pseudo-maximum likelihood regression results. Hypothesis 1 predicts a negative effect of MMC on target size. In Model 2, the coefficient of MMC is negative (β = −0.001), and the effect is significant, with an estimated p-value of 0.006. In terms of effect size, as MMC increases by one standard deviation from the mean, the predicted target size reduces by 21.5%. Hypothesis 1 is thus supported. Model 4 presents the fully specified model, including the interaction of MMC and market concentration. Hypothesis 2 suggests that the negative effect of MMC on target size becomes weaker as market concentration increases. The coefficient of the interaction term of MMC and market concentration is positive (β = 0.006), and the estimated p-value of the effect is less than 0.000. To illustrate the interaction effects, we plot the predicted target size across the range of the MMC variable for market concentration at low (mean–SD = 0.086), mean (0.260), and high (mean + SD = 0.435) values of market concentration (see Figure 4). As MMC increases along with an increase in market concentration, the effect of MMC on predicted target size becomes less negative. In terms of effect size, when market concentration increases from the mean by one standard deviation, the predicted target size increases by 4.4% (keeping MMC at its mean). Therefore, we conclude that Hypothesis 2 is supported.

Poisson pseudo-maximum likelihood regression multimarket contact on target size and target market concentration.

GDP: gross domestic product.

Log-transformed.

Not hypothesized; robust standard errors in parentheses clustered by acquirer; p-values in brackets.

Interaction effect of multimarket contact and target market concentration on target size.

Table 4 presents the results for in-state and out-of-state acquisitions. Hypothesis 3 suggests that there is a stronger negative effect of MMC on target size for in-state acquisitions than for out-of-state acquisitions. In Model 2, the coefficient of MMC is negative (β = −0.002), and the effect is significant, with an estimated p-value of 0.001. In Model 5, the coefficient of MMC is negative (β = −0.001), and the effect is significant, with an estimated p-value of 0.028. In terms of effect size for in-state acquisitions, as MMC increases by one standard deviation from the mean, the predicted target size reduces by 36.7%. For out-of-state acquisitions, as MMC increases by one standard deviation from the mean, the predicted target size reduces by 25.4%.

Poisson pseudo-maximum likelihood regression multimarket contact on target size and target market concentration, in-state and out-of-state acquisitions.

GDP: gross domestic product.

Log-transformed.

Not hypothesized; robust standard errors in parentheses clustered by acquirer; p-values in brackets.

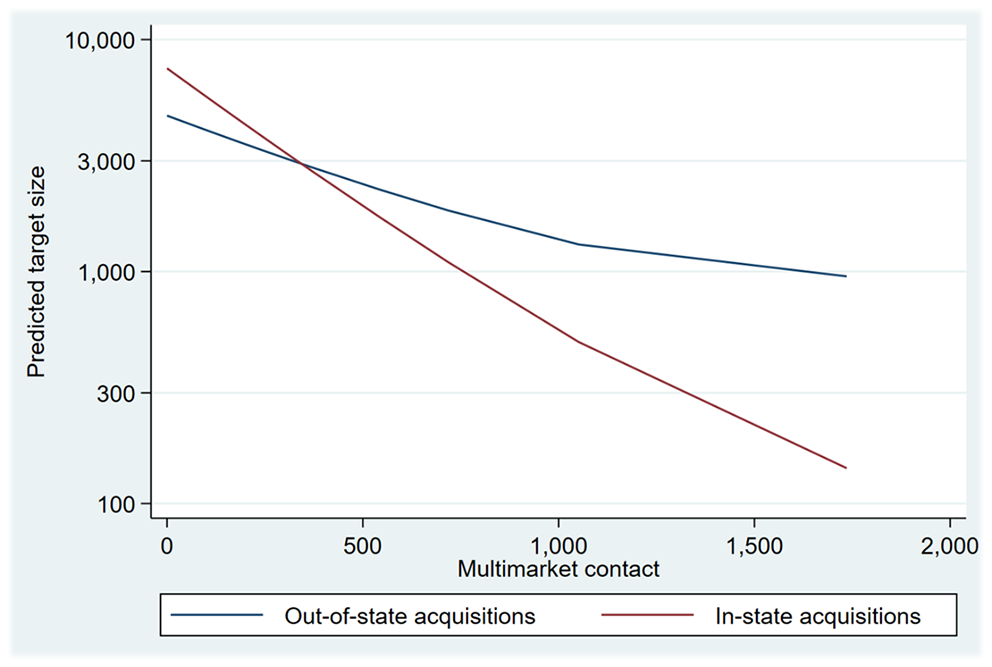

To formally test Hypothesis 3, we stacked the subsamples used in estimating Model 2 and Model 5 and re-estimated the model on the combined sample. In this estimation, we included the target location moderator variable as well as the interaction of this variable with the MMC variable. The result of this estimation is presented in Model 9. To test whether the difference in the effect of MMC across subsamples is significant, we conducted a Wald test of the joint effect of the target location dummy and the target location dummy × MMC interaction variables. This test indicated that the negative effect is stronger for in-state acquisitions (χ2 = 14.95, p = 0.0006, df = 2). To illustrate this effect, we plotted the predicted target size in Figure 5. It is evident that increases in MMC have a more negative effect on target size for in-state acquisitions than for out-of-state acquisitions, providing support for Hypothesis 3.

Effect of multimarket contact on target size for in-state and out-of-state acquisitions.

Robustness tests and supplementary post-hoc analyses

We conducted several robustness tests and supplementary analyses to verify our results (full results for all tests are available upon request). A more detailed discussion of some results is presented in the Online Supplementary Materials. First, firms are likely to self-select into acquisitions (Shaver, 1998), and this is may also the case in this context. If this is the case, we needed to account for this in our estimation, or our estimates could be biased. To control for selection in our estimates, we used all large BHCs to estimate a probit model. From this, we computed the inverse Mills ratio (Heckman, 1979) and then included this ratio as a control in all our models. When including this variable, our results remain consistent. In the probit model, the dependent variable takes the value of 1 if a BHC engaged in an acquisition in a given year and 0 if not. The independent variables used in this model were the same variables as described above (excluding the transaction-level control variables and state fixed effects), as well as an instrumental variable that measured the total financial services sector acquisition activity. The full results are presented in Table A1 in the Online Supplementary Materials.

Second, we used an alternative measure for our dependent variable (target size): the total number of full-time equivalent employees at the time of acquisition. When re-estimating all our models with this variable, we obtained consistent results. Third, we used different ways to measure our main independent variable: MMC. As can be seen from Table 1, MMC exhibits a large spread (minimum = 0 and maximum = 1735.79). To investigate if observations that take extreme values on this variable were driving our results, we re-estimated all our models with a winsorized version of the MMC variable (winsorized at 0.5% on each side of the distribution). When re-estimating our models with this variable, the hypotheses are still supported. It is of note, however, that the coefficient of MMC in the in-state acquisitions subsample is negative (β = −0.002), with an estimated p-value of 0.001, while the coefficient of MMC in the out-of-state acquisitions subsample is negative (β = −0.001), with an estimated p-value of 0.239. The test for difference in the effect of MMC across subsamples remains significant (χ2 = 14.49, p = 0.0007, df = 2). In the main analysis, we have computed the focal firm’s MMC with rivals present in the target state and with whom the focal firm meets in at least one state prior to the transaction. However, it could be that the overall level of MMC that the firm faces from all its rivals influences the choices around target size. To test this possibility, we also computed an MMC measure in which we capture MMC that the focal firm has with all rivals in all states. When re-estimating our models using this independent variable, we obtain consistent results.

Although we did not theorize about effects within firms and we included a range of firm-level control variables to control for alternative explanations, it is possible that omitted firm-level variables may have driven the results presented in the analysis. To check whether this was the case, we re-estimated all models with firm fixed effects, which should control for time-invariant omitted firm-level variables. It needs to be noted that the interpretation of these models differs from the models presented in the main analysis; specifically, the results no longer represent effects between firms but within firms. The patterns of results demonstrate that even when considering changes within firms, our results remain consistent.

As noted above, there was a relatively large correlation between MMC and competitor acquisitions (r = 0.86). To test whether this correlation influenced our results, we orthogonalized the competitor acquisitions and MMC variables to “separate” these two variables’ effects and received consistent results when using the orthogonalized variables (full results available upon request). We also orthogonalized the acquirer size and MMC variables (r = 0.74) and received consistent results when using the orthogonalized variables (full results available upon request). Finally, we tested how different sampling weights influenced our estimation—specifically, we weight observations by the number of firms in the target state in the year of the acquisition and the total number of BHCs and firms in the target state of the acquisition. We obtained consistent results using both approaches.

Discussion and conclusion

This study’s objective has been to advance the emerging discourse in the acquisition literature regarding the effect of competitive interdependencies on firms’ acquisition behavior (e.g. Keil et al., 2013; Uhlenbruck et al., 2017) and specifically how pre-acquisition competitive interdependencies influence corporate acquisition strategies. The starting point was the observation that high MMC firms continue to engage in acquisitions despite the potentially high risk of retaliation from interconnected rivals. To address this empirical conundrum, we developed an original theoretical framework that explains a possible way through which MMC may influence acquisition strategies: namely, the size of the target firm. Furthermore, we show that this effect is weaker if the target operates in highly concentrated markets but is stronger if the target firm is headquartered in the same state as the focal acquirer. We believe that our findings have important implications for both acquisition and MMC literature.

In a very broad sense, our study documents the importance of considering pre-acquisition competitive interdependencies when studying corporate acquisition strategies. The few studies that have already considered competitive interdependencies in the acquisition context (e.g. Keil et al., 2013; King and Schriber, 2016; Uhlenbruck et al., 2017) have focused on the post-acquisition phase, thereby neglecting the possibility that firms, and especially high MMC firms, may have already considered the possibility of retaliation by interconnected rivals when designing acquisition strategies. Previous research in the acquisition literature has already considered the trade-off between firm-specific efficiency gains and gains to the industry as a whole (Eckbo, 1983; Focarelli and Panetta, 2003; Kim and Singal, 1993; Singal, 1996; Stillman, 1983). Nonetheless, we add to this discussion by highlighting how—through target firm size, target market concentration, and target location—firms strategically consider these gains to avoid retaliation from interconnected rivals.

In addition, our findings can help understand how an acquisition event influences the share price of rivals. In this regard, our findings could also help to explain why, contrary to expectations, there are no differences in rivals’ share price reactions in high-density versus low-density contexts (Clougherty and Duso, 2009: 1382). In low-density contexts, firms may acquire smaller targets to mitigate negative effects on rivals. In contrast, in high-density contexts, collective gains may be helped by acquisitions—especially if larger targets are acquired. Overall, our findings suggest that, in the presence of pre-acquisition competitive interdependencies, firms are willing to adapt acquisition strategies rather than altogether forgo these strategies if such adaptations reduce the threat of retaliation. Corporate-level strategy researchers focusing on the pre-acquisition phase (e.g. Welch et al., 2019) should, therefore, consider how competitive interdependencies influence the strategy design phase. In this sense, with our focus on corporate-level strategies, such as acquisitions, we also contribute empirically to the small amount of literature that analyses MMC at this level (e.g. Golden and Ma, 2003; Sengul and Gimeno, 2013).

An important insight for MMC literature that emerges from our focus on the pre-acquisition phase is that MMC may determine to what degree firms are focused on generating firm-specific efficiency gains as opposed to further market consolidation. High MMC firms seem to consider how far their acquisitions not only create firm-specific gains but might also benefit the market as a whole. As such, our study goes beyond existing work by suggesting that firms may not only use strategies that soften competition (Bernheim and Whinston, 1990) but also consider how these strategies influence structural conditions that could create future firm-level benefits for those high MMC firms. By thus considering how high MMC firms influence the structural conditions of a market, our study also has implications for recent approaches that show the effect of MMC on rival firms (e.g. Gómez et al., 2017; Hsieh and Vermeulen, 2014). For instance, by engaging in acquisitions that create collective benefits, high MMC firms may aim to avoid negative spillover from competition among rivals.

Moreover, our study shifts the conversation in the MMC literature away from examining the effect of competitive interdependencies on a firm’s likelihood of engaging in certain competitive moves and toward using MMC to explain heterogeneity within certain strategic moves—in our case, acquisitions. Most of the existing literature has focused on explaining why high MMC firms might avoid certain strategic moves altogether due to the fear of retaliation (Yu and Cannella, 2013). However, in this study, our approach is based on the notion that high MMC firms may not entirely avoid strategic moves that could be perceived as aggressive, but rather MMC influences how these high MMC firms design their strategic moves. In this respect, our findings complement Greve (2008), who shows that firms are most likely to avoid competitive moves when detection probability is high and less likely to do so when it is lower.

Limitations and future research

Our study has a number of limitations that may be addressed by future research. First, we focus on US BHCs and their domestic interdependencies. While banking markets in the US tend to be domestic, future research could seek to confirm our findings in other contexts and take into account international interdependencies. Second, we assume that internal coordination mechanisms allow firms to coordinate actions across markets. While we follow previous research and include several controls in our statistical tests pertaining to this assumption (Sengul and Gimeno, 2013), we do not directly observe these internal coordination mechanisms. Future research may be able to identify the degree to which BHCs have such internal coordination mechanisms in place. Third, consistent with prior work (e.g. Van Reeven and Pennings, 2016), our theory assumes that decision-makers act rationally. Future research may explore how individual differences or relaxing the assumption of rationality may influence our findings. For example, several studies show that compensation of boundedly rational agents influences acquisition strategies in response to external stimuli (e.g. Benischke et al., 2019, 2020); and that CEO tenure influences market entry decisions in the presence of MMC (Stephan et al., 2003). Exploring such individual-level contingencies may further refine our theory. Finally, we assume that acquisition targets of various sizes are readily available, and they fit within the overall acquisition program (or portfolio) of a focal acquirer. This assumption seems reasonable in our study’s empirical context, given that many banks of different sizes operate in the US. Future work could still investigate the role the supply of acquisition targets and acquisition portfolio characteristics play when high MMC firms engage in acquisitions.

Supplemental Material

sj-docx-1-soq-10.1177_14761270211009745 – Supplemental material for Multimarket contact and target size: The moderating effect of market concentration and location

Supplemental material, sj-docx-1-soq-10.1177_14761270211009745 for Multimarket contact and target size: The moderating effect of market concentration and location by Grigorij Ljubownikow, Mirko Benischke and Anna Nadolska in Strategic Organization

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

Notes

Author biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.