Abstract

Property values offer a lens through which to explain urban phenomena. It is therefore important to understand the theories and practices of property valuation as planners. This article brings together and advances planning and real estate fields by probing the meaning of value underlying a common valuation technique, the discounted cash flow analysis. When using this technique, income-generating properties are largely valued for their exchange value, while much of their use values are overlooked. Learning from the field of social entrepreneurship, I propose a framework for capturing the use values of a property, more specifically, its impact on existing socioeconomic inequalities.

Keywords

Introduction

Property values and the strong desire to protect them undergird the patterns of urban- and suburbanization in the US and beyond (Fischel, 2001). Property values are also indispensable for the operations of the public and the private sector, as a source of revenue stream for governments (Urban Institute, 2023) and as an investment asset for private enterprises (Hudson-Wilson et al., 2003). Given the centrality of property values, various valuation methods have been developed to accurately estimate them in the real estate field (Pagourtzi et al., 2003). By contrast, despite the importance of property values for the public sector, planning literature has paid little attention to the theory and practice of property valuation.

Planning scholars have repeatedly emphasized the need to understand the valuation of land and development for various reasons. For example, property values are a key point of consideration for determining if and how much public subsidy is needed for joint development projects with the private sector (Erie et al., 2010; Kim et al., 2020; Sagalyn, 1997; Wolf-Powers, 2013) and for providing critical public infrastructure and services (Crook et al., 2016; Smith and Gihring, 2006). On the flip side, public policies and land use regulations can alter current and future property values, which in turn determines where, when, and in what form property developments take place (Campbell et al., 2000; Kim, 2020). Planning and property valuation essentially has a circular and inextricable relationship.

Therefore, it is important for planners to have a firm grasp on the specific valuation techniques and processes to understand what is being valued, how, and for what purpose. Probing the meaning of value undergirding valuation techniques allows us to get a glimpse of what qualities and impacts are deemed valuable. From this understanding, we can start to challenge the concept of property value and start conceptualizing a different idea of value.

This article questions the meaning of value underlying the most widely accepted property valuation technique – the Discounted Cash Flow (DCF) analysis (Hoesli et al., 2006). DCF allows real estate to be integrated into the broader capital market because it is a technique that is ubiquitously used by all sectors of the investment and finance industries (Geltner et al., 2014). From a planner’s perspective, having a thorough understanding of how DCF works is critical because it is the method that is used to value large-scale urban redevelopment projects, for which significant public resources are deployed.

This article seeks to answers the following questions: what is the assumed meaning of value underlying the DCF technique? In other words, what is considered valuable when valuing income-generating properties? Does the existing DCF technique capture a development’s social impact, a dimension of central interest to planners? If not, how may the DCF technique be adapted to achieve this goal? Answers to these questions will be explored by reviewing existing literature on value and valuation within planning and real estate fields and by applying David Harvey’s interpretation of the Marxian theory of value to analyze the DCF technique. By doing so, it will be argued that the values of income-generating properties, calculated using DCF, only capture the exchange value, while overlooking the use values that a building might have on existing socioeconomic inequalities.

Taking lessons learned from the field of social entrepreneurship, the article further proposes a novel framework for capturing such “social” use values of a property. Adapting the conventional DCF technique, I propose a novel methodology to quantify the social value of real estate developments. This modified DCF technique considers how a development may have positive or negative social value by reducing or increasing 1) the costs of providing public service and social welfare benefits and 2) governments’ revenue base. Concrete dimensions of the impact that a development project may have on socioeconomic inequalities are discussed, along with potential strategies for calculating the costs and benefits of those impacts. The article brings together and advances planning and real estate fields and elevates the significance of value and valuation for planning scholarship.

Why is there a need to quantify the social value of real estate development?

This article develops and proposes a methodology for quantifying the social impacts of real estate development. However, before launching an effort to do so, I first establish the justification for the need to develop such a methodology. After all, quantification schemes of various stripes have been subject to criticism from sociologists, political scientists, and historians ever since the history of economic and social measurements came into its existence (Kelman, 1981; Muller, 2018; Porter, 1995; Scott, 2008). Given the perils, limitations, and uselessness of many quantification schemes, why create a methodology for calculating the social value of real estate development?

The answer to this question lies in the specificity of large-scale real estate developments and their relationship with the neighborhoods in which they are built. When large-scale changes of the physical environment, albeit through infrastructure projects or real estate developments, take place, conflicts inevitably arise among competing interests. This is particularly true for development sites in and around sensitive neighborhoods such as historically marginalized, disinvested communities and environmentally sensitive or vulnerable land.

In other words, large-scale interventions are poised to transform urban space, for better or for worse, raising the critical question of who bears the costs and benefits of such interventions (Saito, 2019; Tasan-Kok and Sungu-Eryilmaz, 2011). And an uneven power dynamic exists in such situations between the urban elites and the public, particularly those of under-served communities, due to the financial, political, and informational advantages enjoyed by the elites in a capitalist society (Farley, 2023; Searle and Legacy, 2021). In these moments of conflict, the logic, methodologies, and justifications of the urban elites are known to dominate the public discourse (Holden et al., 2015). One of the most illustrative examples of such dominance is the prevalence of the cost-benefit and DCF analyses used to justify public subsidy expenditures for infrastructure and redevelopment projects.

Searle and Legacy (2021) caution that the dominance of cost-benefit analysis used in infrastructure funding could “omit significant dimensions of the public interest” such as “community disruption” and “ecosystem survival.” The authors also note that the cost and difficulty associated with modeling such dimensions of public interest further deter the incorporation of these critical dimensions. Similarly, in the context of community benefits agreement negotiations, Farley (2023) emphasizes the need to scrutinize a developer’s proforma and develop “a metric that puts communities on the same footing with development interests at the front end of the planning process” (p.1).

Accordingly, this article proposes a framework to quantify how a real estate development project may affect existing socioeconomic inequality to counterbalance the dominance of the metrics and narratives used by those in power. The theoretical justification for such an approach can be found in critical urban theory. Marcuse (2009) once argued that a way to overcome the power imbalance in urban decision-making and reinstate the right to the city for the most marginalized urban population is to expose the power imbalance, propose alternatives, and politicize these issues and alternatives for getting their proposed alternatives adopted. In undertaking these actions, Marcuse was not against using the tools and methods of the capitalist system to challenge the status quo. He believed that advocates “will need to draw resources from the for-profit sector… but their driving force will be found in the general principles that are radically different from those motivating the for-profit economy” (p.195).

By calculating the social value of real estate developments, those who advocate for the marginalized members of society will have a more even footing with urban elites. In contrast, if community members and the public are not speaking the capitalist language, what’s valuable to them will always be marginalized or completely left out of the public discourse. Accordingly, despite the dangers associated with quantification, this article is based on the conviction that there is a need to develop a vocabulary that captures the social value of real estate development.

Questioning the theory and practice of valuation from a planners’ perspective

Place of value and valuation in planning studies

Planning scholars have yet to establish a significant body of knowledge that can help planners grapple with and harness property values for planning objectives. Scholars who analyzed land value capture have perhaps been most directly engaged with value and valuation. Land value capture is the idea that certain government actions uplift location values of real properties and thus some of this value increment should be recouped for the public benefit.

Valuation is important for land value capture because the justifiable amount of benefit that can be recovered from developers and landowners depends on how valuations are done, using what technique, and for and by whom. For example, Van der Krabben and Needham (2008) and Pettit et al. (2020) use an existing valuation technique, hedonic price modeling, to calculate the size of land value uplift resulting from large-scale public investments in transportation and transit. However, although these studies are concerned with valuation from the planning’s perspective, they are mainly interested in using existing valuation techniques, rather than questioning and improving the theories and techniques of valuation.

The UK planning scholarship offers by far the most extensive research regarding value and valuation techniques for planning practice (Dunning and Keskin, 2019). This is due to the country’s long history of negotiating with developers to extract public benefits, referred to as planning obligations, when granting development rights, which began with the 1974 Town and Country Planning Act and later amended by the 1990 Act (Wyatt, 2017). In 2010, a pre-determined impact fee, referred to as the Community Infrastructure Levy (CIL), was introduced. CIL was originally introduced to replace the negotiated planning obligations, but in reality, the two exaction approaches have been used in tandem ever since.

The CIL rates and the sizes of planning obligations are typically determined by the “financial viability assessment,” a calculation method used to determine the appropriate level of value that should be recaptured by the local government without making the project financially infeasible. In determining the development feasibility, one of the most, if not the most, important assumption is the value of the land (Crosby, 2019; McAllister, 2019). Accordingly, the valuation of land and development proposals have become vital to the provision of public goods in the U.K. (Dunning and Keskin, 2019).

The English experience suggests that both the financial viability assessment and the calculation of land value are fraught with uncertainty and inconsistency. This is largely due to the variations in the inputs and assumptions used for the calculations. Scholars have shown that inputs used for these analyses can vary significantly, leading to a wide variation in the calculated outputs (Coleman et al., 2013; Crosby and Wyatt, 2016; McAllister et al., 2016).

Moreover, scholars have further exposed how the actors that are performing the valuations may influence the value that is being calculated. For example, Adams and Tolson (2019) argued that property appraisers working in markets with very little demand for real estate were essentially acting as “market makers” by setting land prices that were much higher than their worth. Using a hypothetical case study in London, Crosby (2019) showed how these viability analyses may be gamed by developers. Similarly, in the U.S. context, Weber (2021) analyzed the DCF analysis used in tax increment financing schemes and demonstrated that local governments use low discount rates to inflate the estimated market values to borrow larger sums of money and justify larger public subsidies. Christophers (2014) and Kim (2023a) take this line of inquiry one step further to show how the calculative techniques themselves alter the very values they are used to calculate.

A review of planning scholarship on property values and valuation holds several implications for future research. First, it is concerning that despite the centrality of value for furthering planning objectives, so little work has been devoted to examine and improve valuation methods. Second, the malleability of value depending on the underlying assumptions and priorities further reinforces the importance of planners being versed with existing valuation practices and questioning its legitimacy when needed. Lastly, existing planning scholarship has yet to challenge the concept of property value as defined by neoclassical economists. Planning scholars can actively participate in the debates over value and valuation by developing and proposing an alternative concept of property value that is more aligned with planning.

Place of value and valuation in the real estate field

Having reviewed how planning scholars have examined the theories and practices of value and valuation, I now turn to the real estate field. When it comes to theories of valuation, two different roots exist: a supply-side one and a demand-side one. The supply-side theory originates from the classical school of economics of the 18th century that attributed value to the cost of production. The demand-side originates from the marginal utility school, which emerged later in the 19th century, and linked value to the utility of a marginal, additional unit of an item (Appraisal Institute, 2013: 19-21). Alfred Marshall, a neoclassical economist, is credited for synthesizing the supply and demand-side value theories, which undergirds the three traditional approaches to valuation: sales comparison approach, replacement cost approach, and income approach (Appraisal Institute, 2013: 21-22). The replacement cost approach can be seen as embodying the supply-side value theory, whereas the income approach and sales comparison approach can be seen as embodying the demand-side value theory. The income theory of value was further developed by an influential neoclassical economist, Irving Fisher (Wendt, 1974). These three valuation approaches still form the foundation of today’s property appraisal practice.

Nevertheless, beyond having roots in the classical and marginal utility school, existing valuation literature and practice have largely neglected to engage with the theory of value and valuation. Valuation practices have evolved without questioning the meaning of value underlying valuation techniques, focused on refining and perfecting the calculative techniques to best predict how much a property should trade for in the market (Canonne and Macdonald, 2003).

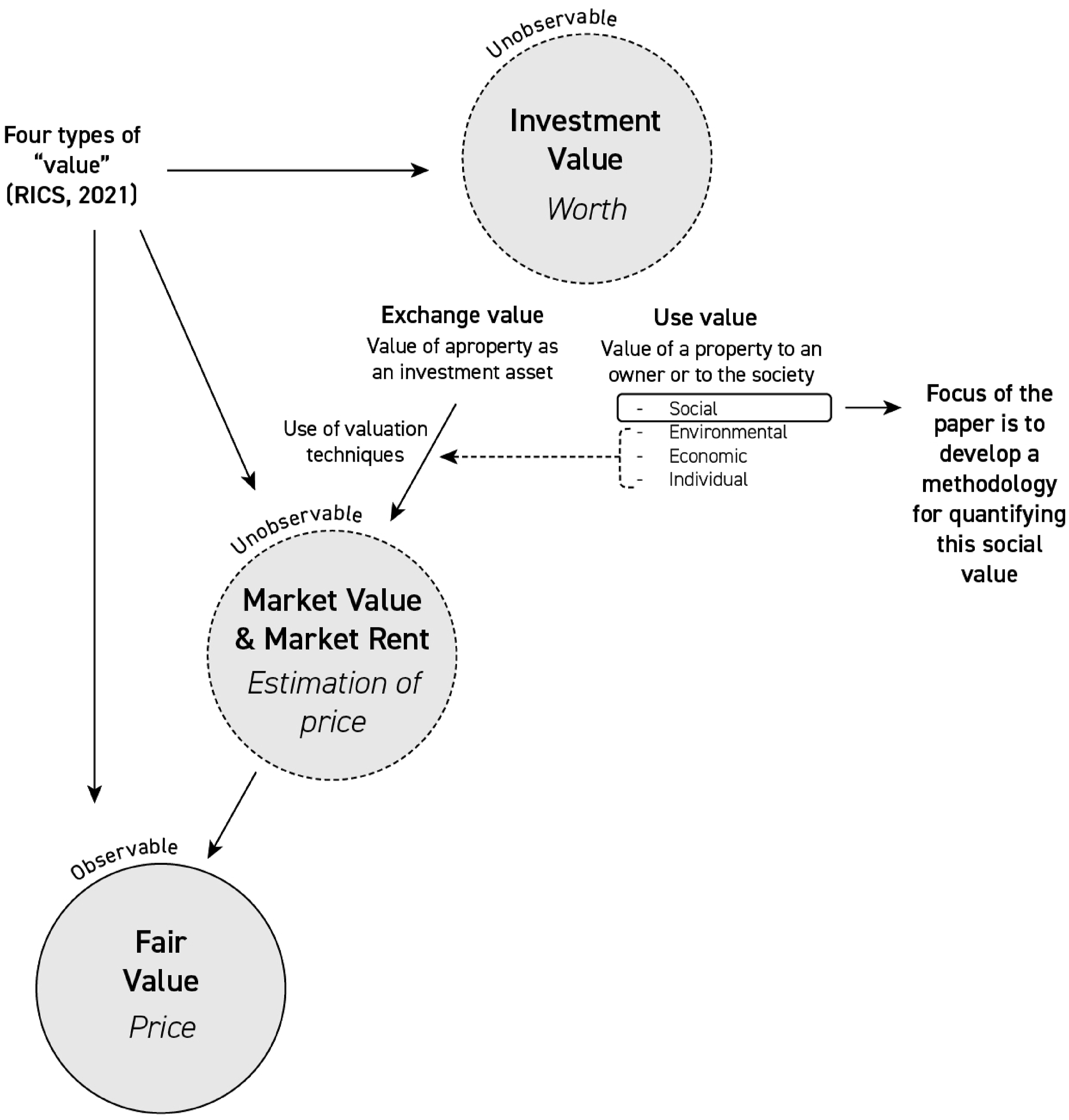

In real estate appraisal practice, property appraisers are introduced to different types of value in their training. The Royal Institution of Chartered Surveyors (RICS), a professional organization that originated in the UK but now has a global footprint and impact, acknowledges four distinct types of value: market value, market rent, investment value, and fair value (RICS, 2021: 64-66). This classification conceptualizes market value and market rent as an estimation of the price for which a property should be exchanged between a buyer and a seller; investment value as worth, the value of a property to an investor or the value of the benefits to the owner; and fair value as price, which are observable through market transactions. This article is specifically concerned with the valuation of investment value, the worth of a property to an investor or an owner/user.

Recent developments in the field of real estate investment suggest that there is an appetite for acknowledging the values of properties beyond strictly their financial profitability. This is best exemplified by the rise of Environmental, Social, and Governance (ESG) initiatives in real estate (Friede et al., 2015; Larsen, 2010; Urban Land Institute, 2021). ESG, as a principle guiding responsible corporate investment, took off in the mid-2000s when the UN picked up the terminology (Mueller, 2023). However, it wasn’t until the mid-2010s that ESG started to make an appearance in the real estate industry. In 2014, ESG first appeared as an “emerging trend” in real estate for European countries (PwC and Urban Land Institute, 2014) and then later in 2017 for the U.S. (PwC and Urban Land Institute, 2017). Since its emergence, ESG-conscious investments and corporate governance have become increasingly common in the real estate industry, particularly for national and global real estate firms.

The rise of ESG in real estate investment and valuation is a step in the right direction for acknowledging the aspects of value that historically have not been accounted for in the DCF analysis. Nevertheless, ESG consciousness provides little guidance for capturing the impacts of a property on existing and future socioeconomic inequalities for several reasons. First, the current ESG practices have primarily focused on environmental substantiality, the “E” of ESG, with little attention given to the “S” of ESG. Moreover, even if the social component is considered, the focus is rarely, if ever, on the impacts of a real estate development on social equity, such as how a project may lead to displacement, gentrification, race and class segregation. When the social aspects are discussed, the consideration focuses on the enhanced experiences of the users of the buildings. For example, CBRE’s global survey of real estate investors lists five “social” features that investors consider in making their ESG-informed investment decisions: 1) proximity to transit, 2) features that improve the physical and mental health of the users of a building, 3) health and well-being certifications, 4) inclusive building design, and 5) proximity to an area that the organization can assist socially or economically (CBRE, 2023). This fifth feature is the only one that is loosely linked to the building’s relationship with socioeconomic inequality.

Moreover, the state-of-the-art ESG investing practices incorporate the environmental, social, and responsible governance features by quantifying their impacts into positive future cash streams for the owner and the investors (Lorenz and Lützkendorf, 2008; ULI Learning, 2023). This approach is problematic for the features and qualities of real estate developments that may have positive impacts on socioeconomic inequality but negatively impact future cash flow. Such features and qualities will be deemed as de-valuing developments when using the traditional DCF technique. For example, if a building will have income-restricted affordable housing units, this has a direct negative implication for the value of the property as the future stream of cash flow is significantly reduced. In other words, features that positively impact society may diminish the property’s value if using the current ESG-conscious valuation approaches.

Applying the Marxian theory of value to real estate development

By contrast, the Marxian theory of value, based on the concepts of use and exchange values, takes into consideration the political economic implications of value and valuation practices. Use value is the usefulness of a commodity, buildings in the context of this paper, to the user, owner, and society; Exchange value is the usefulness of the same commodity as an investment asset. The concept of investment value, as disseminated by RICS (2021), encompasses both the use and exchange values of a property. The glossary section of the RICS Red Book defines investment value as “The value of an asset to the owner or a prospective owner given individual investment or operational objectives (20.11).”

When use values and exchange values are alienated from each other, the political economy of property development in the urban process goes unnoticed. David Harvey, in Social Justice and the City (2009), made this point clear by pointing out that neoclassical economists are only concerned with exchange value, resulting in an incomplete theory of land use, whereas geographers, planners, and sociologies are only concerned with use value, resulting in conversations disconnected from the sphere of political economy. By contrast, Harvey argues for the reconsideration of the “Marxist” device for bringing use value and exchange value into a dialectical relationship with each other (Harvey, 2009: 157).

Despite the utility of differentiating and understanding the dialectic relationship between use and exchange values, existing valuation practices have largely ignored the use values of properties from its nascent stages. For example, the National Association of Real Estate Boards, in 1927, stated that the value of an income-generating property should not be determined by “the personal comfort or enjoyment that may be derived” from using the property but rather “the amount of income which it is capable of yielding” (National Association of Real Estate Boards, 1927).

Modern DCF technique does exactly that. The Net Present Value, calculated using the DCF technique, is the sum of the discounted future rents expected to be collected, plus the final sales revenue. It is the anticipated value of a property that investors are willing to pay for, today, given the future stream of cash flows. The value of a property calculated using the DCF method is essentially the

Harvey sees use values as multifaceted. Use value can emerge from furthering the physical and mental well-being of the occupants. Use value is also generated from the economic impact of a development project, such as adding new jobs, adding new homes to the housing market, and increasing the tax base. Development projects, in particular, may have negative or positive use value to society by reducing or exacerbating existing socioeconomic inequities (Tasan-Kok and Sungu-Eryilmaz, 2011). Illustratively, if a real estate development offers income-restricted affordable housing units as a benefit, this is a social value added from the societal perspective; by contrast, if a development project demolishes existing cheap housing units and displaces previous low-income residents, this is diminishing the social value of the property. Figure 1 illustrates how RICS’s four concepts of value relate to each other and with Harvey’s use and exchange value concepts. How different concepts of value, as defined by RICS and David Harvey, relate to one another.

Several methods exist to capture the individual, environmental, and economic dimensions of use values. For example, a post-occupancy user evaluation of a building captures the levels of satisfaction of the building’s user. The use value of a building as a source of local economic development is oftentimes expressed as the increases in the number of jobs created and the taxes that can be collected. By contrast, the social dimension of use value, the impact a building may have on the broader society by reducing or exacerbating the existing socioeconomic inequalities, is the least understood and quantified.

Real estate development projects constantly disrupt and rearrange who benefits from and pays the costs of urban transformations. For planners to guide the urban process in a direction that leads toward more equitable outcomes, they must understand the redistributive effects of real estate development and communicate these effects to advocate for outcomes that can increase equity (Kim et al., 2020). I thus argue that there should be a way to quantify and communicate this last dimension of use value. I term this use value the

Identifying and quantifying the social impacts of real estate development

Learning from the social entrepreneurship field

Theories, methods, and experiences accumulated in the social entrepreneurship/social enterprise field offer guidance for conceptualizing and calculating the impacts of real estate development on socioeconomic inequality. This field has long been concerned with measuring the social impacts of non-profit and philanthropic organizations to capture and quantify a business’ impact beyond that of financial ones (Emerson et al., 2000). A multitude of methods has been developed thus far (Perrini et al., 2020) but the Social Return On Investment (SROI) framework is widely accepted as the most prominent and well-developed. SROI has already made its way into the studies of the built environment, such as the effort to evaluate the impacts of social (public) housing (HACT, n.d.) and the post-occupancy user satisfaction of buildings (RIBA and University of Reading, 2020; Watson et al., 2016).

The Roberts Enterprise Development Fund (REDF) is credited as the first entity that proposed and developed the SROI framework in 1996 (Emerson et al., 2000). The underlying idea is to quantify the positive social impacts of an enterprise’s activities. REDF envisioned two distinct ways in which this can happen. A firm may reduce the cost burdened by the government for providing social services and public goods and thus, such cost savings could be quantified as positive value. A firm also generates positive value to society by increasing tax revenues and spending money to advance social mission. REDF acknowledges the following four ways of generating positive social values: 1) additional tax dollars generated, 2) reduction in unemployment costs, 3) new wages of the employees, and 4) dollars used by the enterprise to advance social mission. These four impacts are quantified, discounted back to the present dollar, and added up to calculate the total positive social value generated. Any grant and philanthropic investments are subtracted from it to arrive at the net positive social value (Emerson et al., 2000: 140).

This modified DCF method differs fundamentally from the conventional one because it questions the meaning of value underlying the DCF valuation technique. In a conventional DCF analysis, taxes and wages paid by the enterprise are considered as negative cash flows for the company and thus, reducing their value. The modified DCF approach, instead, posits that such cash outlays should be seen as providing benefits to the society at large. What is considered valuable in the valuation process is upended in the modified framework.

This idea to quantify the future cost savings and benefits to society and discount them to calculate the social value can be adopted for the valuation of real estate development projects. Such an approach would allow for capturing the value of real estae development to the society at large, not just to investors and the property owners. Taking this idea one step further, this article focuses specifically on capturing the use values of a property for reducing socioeconomic inequalities.

The reason for such focus is that the parameters and definition of the social impacts of properties can vary widely (Sairinen and Kumpulainen, 2006) and as demonstrated by the ESG practices, the social side is often translated as the satisfaction and comfort of individuals and groups occupying the building. This, in turn, means that the direct and indirect impacts a building may have on the broader society are unaccounted for when in fact social inequality in and around large-scale urban regeneration projects oftentimes increases because of the redevelopment (Tasan-Kok and Sungu-Eryilmaz, 2011). Moreover, this is the dimension of use value most at odds with exchange value and thus the least understood and investigated.

Accordingly, the following pages of the paper will develop a valuation technique that would allow for capturing a project’s impacts on the broader society and, particularly, on social equity. Following Avni and Fischler (2020), I understand equity as the “absence of systemic differences—for example, in access to health services, employment opportunities, housing, and so forth—between social groups.” Real estate developments can further social equity when the most disadvantaged groups are prioritized as beneficiaries of the development.

Adapting the modified DCF framework for real estate developments

Existing theoretical and empirical literature, particularly those influenced by the critical political economy theory, has proven that large-scale urban development projects can perpetuate and exacerbate existing inequalities (Tasan-Kok and Sungu-Eryilmaz, 2011). In this way, real estate developments are adding costs to society by having to address increased income, education, and employment gaps. However, such an impact is indirect, and thus difficult to pinpoint the marginal cost burden generated by one development project.

By contrast, real estate developments can also directly impact existing socioeconomic inequalities. Contributions made by real estate developers, such as adding housing units that are affordable to low-income households, providing direct employment opportunities for the members of low-income communities, and ensuring living wage jobs have direct and positive impacts on society. Displacing incumbent low-income residents and businesses or demolishing moderately priced housing units has a direct negative impact.

These direct positive and negative social impacts of real estate developments are yet to be systematically acknowledged and quantified in existing valuation practices. Following the REDF’s SROI framework, such impacts can be translated into cost savings or additional cost burdens on the government. For example, the value of providing income-restricted affordable housing units can be quantified as cost savings in the federal housing subsidy programs. Providing job training opportunities for low-income residents that lead to new employment or transitions to higher-paying jobs can be translated as increases in federal income tax from adding additional wage hours or higher income.

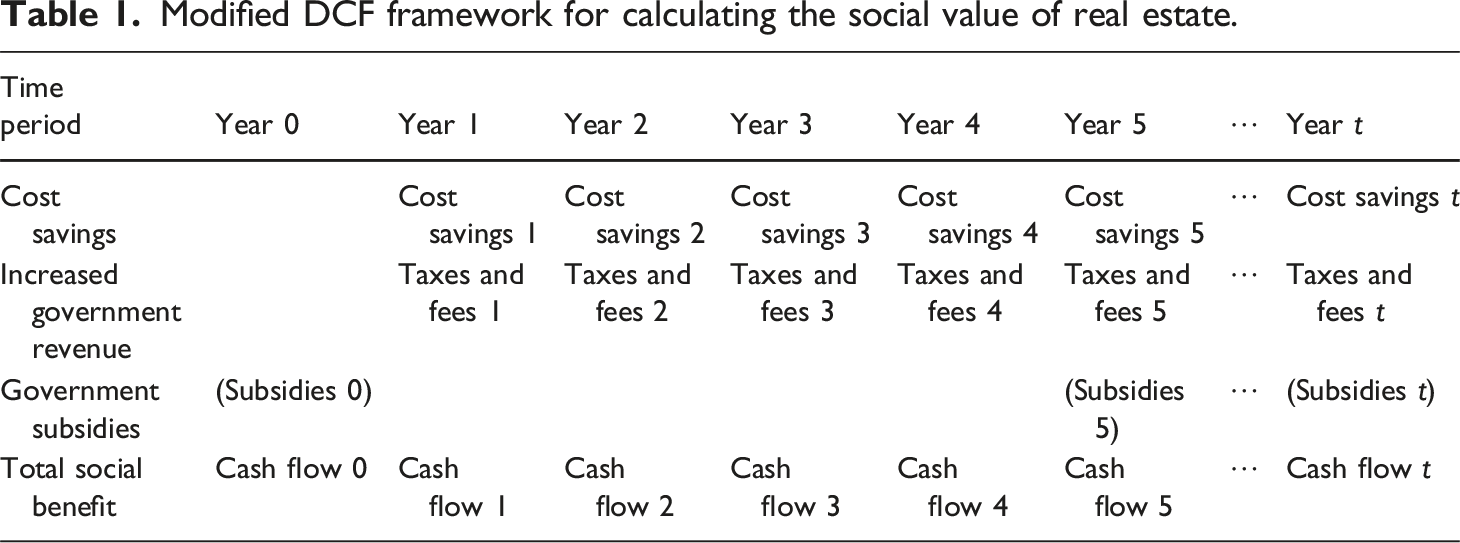

Modified DCF framework for calculating the social value of real estate.

The direct cost savings can include, but are not limited to, savings resulting from reducing: housing needs for low-income households and the homeless population; poverty; and pressures on existing health and educational systems. The direct economic benefit to society comes in the form of increased productivity resulting from adding previously unemployed populations into the workforce, as well as upskilling low-wage workers. Increases in property taxes can also be captured here. These direct cost savings and benefits can be incorporated into the DCF analysis as positive future cash flows that can be discounted and added up to calculate the present social value of the development. By contrast, public subsidies, in the form of grants, tax abatements, land, or fee waivers, should be discounted and subtracted from the value. Equation for calculating the Net Present Social Value.

Learning from case studies of large-scale developments

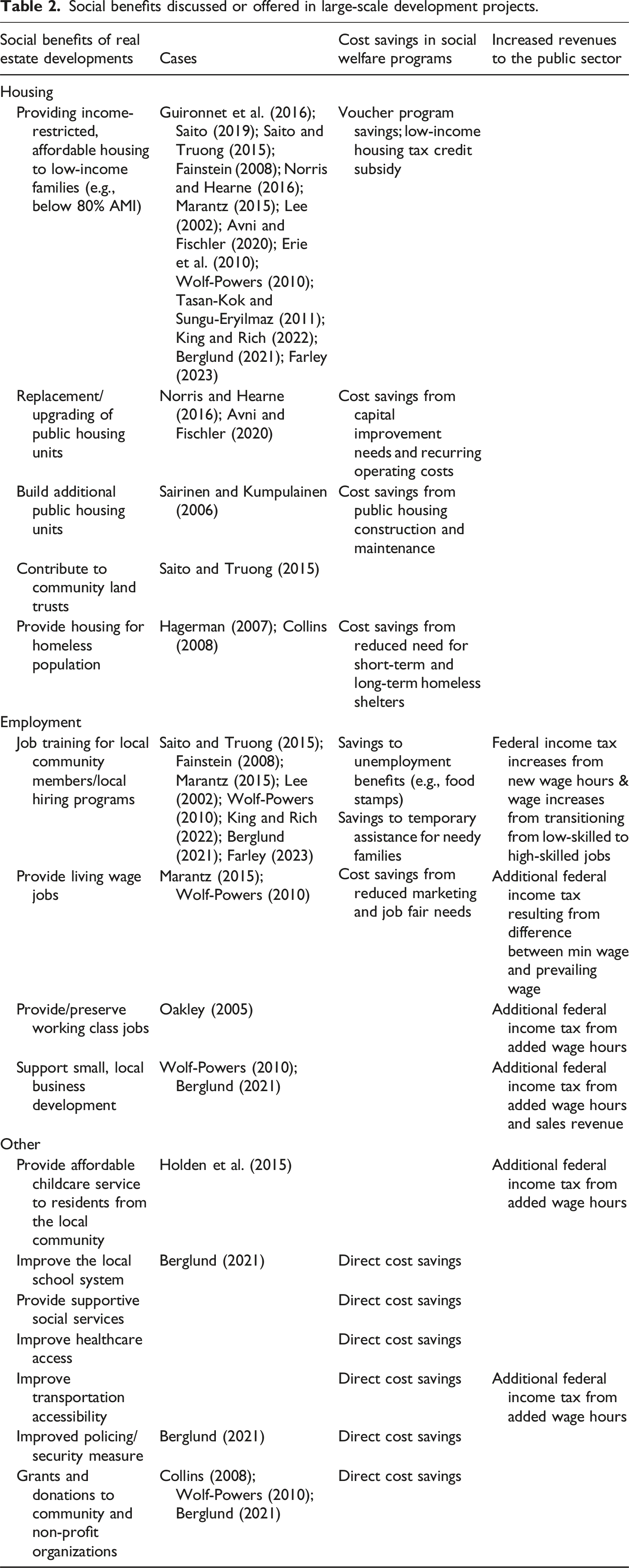

To identify the concrete and direct ways in which real estate developments affect socioeconomic inequalities, I tap into the existing repository of case studies on large-scale real estate developments. Kim (2023b) undertook a systematic review of existing empirical research on large-scale urban development projects by scanning for peer-reviewed articles published between 2000 and 2020. The author identified 82 articles that examined the politics and processes of such projects. 1 Among these articles, the author further identified 31 that were concerned with the question of who benefits from large-scale developments, the equity impact, which is central to this paper’s concern. I took these 31 articles as a starting point and added five additional ones given that Kim’s (2023b) review ends in 2020.

Social benefits discussed or offered in large-scale development projects.

Next, I illustrate the practicality and challenges of assigning a monetary value to the social benefits identified above, using income-restricted affordable units as an example. 2 With regards to housing as a social benefit, building new residential units could in and of itself benefit society by bringing down the price of housing. However, such an effect would strongly depend on the market context. As such, I focus on quantifying the social value of income-restricted affordable housing units.

For income-restricted units built by a real estate developer, the cost savings to the government will vary depending on which government programs are assumed to be replaced by the units built. For each moderately affordable income-restricted unit, e.g., targeting households earning between 50-80% of the Area Median Income (AMI), the savings can be equated to the amount that the federal government uses to subsidize the Low-Income Housing Tax Credit (LIHTC) program, which is a subsidy offered by the U.S. federal government for the development of income-restricted affordable housing units. The 9% LIHTC program is designed to subsidize 70% of per unit construction cost, which would be the cost savings for the federal government if the same unit is built by a private developer. Accordingly, the social value of the project can encompass such cost savings. For example, the five-year (2019-2023) average per-unit development cost for LIHTC projects is reported to be $330,357 in Denver, Colorado (Colorado Housing Finance Authority, 2023). If 70% of such a construction cost is estimated to be public subsidy, each income-restricted unit offered by a developer is adding $231,250 to the net present social value of the project.

Alternatively, the social value of new income-restricted units can be quantified as the cost savings in the federal housing voucher program, commonly referred to as Section 8. According to a study of administrative data from 1995 to 2015, the average duration that a household will stay on the voucher program was 6.6 years (U.S. Department of Housing and Urban Development, 2017). The average annual cost of the housing voucher program, per household, is $10,929 in 2023 (U.S. Department of Housing and Urban Development, 2023). Assuming a $10,929 per household savings for 6.6 years, the total cost savings for the federal government would be $72,137, not adjusting for inflation. This figure is significantly lower than the value calculated by the LIHTC unit equivalent approach as the LIHTC approach represents the cost of building new income-restricted units, whereas the housing choice voucher program does not add more to the existing stock of affordable housing. The two different cost savings estimates clearly indicate that depending on what assumptions are used to calculate NPSV, the output value will vary significantly.

Moreover, calculating the social value of new income-restricted units will also vary by the specific geographic and temporal contexts. Taking the LIHTC program as an example, the construction costs of providing LIHTC units can range from $104,000 in Georgia to $606,000 in California according to a 2018 study conducted by the US Government Accountability Office (GAO, 2018). The timing of NPSV estimation will also matter because construction costs and the maximum rents that can be charged change over time.

The magnitude of social value will also need to be adjusted based on the affordability of the units. Those serving households earning extremely low income, defined by the U.S. Department of Housing and Urban Development (HUD) as households earning below 30% of area median income, will have a greater social value than those serving higher income levels (e.g., households earning below 80% AMI). However, how to account for deeper affordability is not a straightforward question because the extremely low-income population is served by the voucher program in the U.S., which would mean that if the value of deeply affordable units is equated as savings in the voucher program, the estimated cost savings would be lower than the units that will be serving higher income households.

Similarly, the social benefit of providing housing for the homeless population can be captured by estimating the cost savings of providing a homeless shelter. Based on HUD’s Housing Inventory Count data compiled in 2015, it costs approximately $14,064 per bed in 2015 for single adults, while those providing shelter with additional services like behavioral and mental health services, case management, or legal services, cost $25,806 per bed (Culhane and An, 2022). If taking $16,000 as the average cost saving and assume that this cost will grow at a constant rate (e.g., 2% inflation rate) in perpetuity, where the expected rate of return is 7%, the net present social value of the benefit would be $320,000. 3

These examples are provided to inspire more research and experimentation and are neither definitive nor conclusive. The questions that emerged from just this simple exercise—which program is being replaced, what time and place calculations take place, and how to account for deeper affordability—clearly suggest that a lot more research and collective thinking is needed to establish and refine the NPSV technique.

Avoiding the perils of quantification

The current effort to quantify the social value of real estate development must not ignore the perils of quantification. Numerous academic studies have advised against efforts to assign numeric figures to qualities that defy simplification for several different reasons. For example, putting dollar values on non-marketed benefits and costs will inevitably be imperfect and may even diminish the values of the non-market benefits (Kelman, 1981). Simplification and quantification schemes have been the tools of those in power for controlling and ruling, which have led to disastrous results (Scott, 2008). Fixating on quantified metrics for performance evaluation has led to counter-productive results (Mueller, 2018). Is there a way to avoid, or at the least mitigate, these pitfalls?

Scott (2008) and Mueller (2018) collectively provide some guidance for finding an answer. Scott (2008) posited that the main reason why authoritarian, high-modernist schemes have failed is because they ignore and suppress the practical skills that underwrite any complex activity, referred to as “mētis” in the book. Mētis, Scott writes, is a wide array of practical skills and acquired intelligence developed in responding to a constantly changing natural and human environment. Most importantly, “knowing when and how to apply the rules of thumb in a concrete situation is the essence of mētis” (p.319).

In other words, it is not the quantification schemes themselves that are inherently problematic, but that their authoritarian application is. Ignoring specific temporal and geographic contexts, which constantly evolve, and instead applying rigid rules and methods is what has made quantification schemes destructive. Similarly, Mueller (2018) also argued that problems with quantification arise when measures and metrics become alienated from sound judgments. Measurement demands judgment. A judgment about “whether to measure, what to measure, how to evaluate the significance of what’s been measured, whether rewards and penalties will be attached to the results, and to whom to make the measurements available” (p.176).

Calculating NPSV inevitably requires judgments over what to count, how much value to assign, and where to stop, and such judgments must be based on experience and local knowledge. Moreover, this metric should not be seen as an absolute, objective figure, but rather a fluid one that will need to be adapted to the specific time and local contexts in which the calculations take place. As demonstrated in the previous section, cost savings from building affordable housing will differ by region and time, as well as the depth and duration of affordability. The quantified metric should also be interpreted with caution and within concrete policymaking contexts. For example, even if two projects have the same NPSV and are competing for public subsidy, they may not deserve equal distribution depending on the priorities and objectives of the local government.

In other words, the quantification methodology developed in this paper should be administered by an experienced practitioner who can determine what, when, and how to include the non-market benefits and costs of real estate development and how to interpret and use the quantified metric. Taking these cautionary notes seriously would allow the proposed metric to avoid some of the most common pitfalls of quantification. In an ideal world, planners can perhaps serve as the experienced practitioner who knows “how and when to apply the rule of thumb,” in the words of Scott (2008).

Conclusion

Thought experiments, such as the one undertaken here, hold value because they allow us to “imagine how it is to be (and think) in a different situation” (Harvey, 2000: p.238). In Spaces of Hope (Harvey 2000), Harvey envisioned that political change can be brought about not by “some radical revolutionary break,” but rather a “long revolution” undertaken by “insurgent architects.” These architects would act out their socially constructed roles in their daily lives but would desire, think, and dream of a different world. Harvey further argued that utopian thinking can empower these architects to imagine entirely different systems of property rights and living and working arrangements. NPSV turns the orthodox neoclassical quantification methodology on its head and posits an entirely different concept of property value.

How may the reconceptualized idea of property value be used in practice? Should NPSV be combined with NPEV to arrive at a property value that is more comprehensive? I believe a better use of NPSV is to consider it as a parallel concept to NPEV. Combining the two would essentially be mixing up two very different concepts of value, further confounding the debates over the values of real estate.

NPSV should be used to counter the disproportionate focus on exchange value when valuing real estate developments. By juxtaposing NPSV and NPEV, we can follow the three steps for bringing political change in urban resource distribution suggested by Marcuse (2009). We can expose which development proposals are more or less exploitative, propose measures that can increase their NPSV, and politicize so that these measures could be incorporated into project proposals; certain projects may be found to have significant NPSV and thus warrant a greater allocation of public subsidies for implementation. Harvey (2009) once argued that “catalytic moments in urban land use decisions process when use value and exchange value collide to make to make commodities out of land and improvements thereon” are the moment in which to generate an adequate theory of urban land use (Harvey, 2009: 160). NPSV will enable balanced debates weighing the exchange and use values of real estate when these different concepts of value collide. Contrasting NPSV and NPEV will bring use value and exchange value into a dialectical relationship with each other, as advocated by Harvey (2009: 157).

There are of course limitations to the proposed usage of NPSV. First, by creating a metric that is parallel to the conventional NPEV, the generalizability of the proposed metric and how it will impact investment decisions is questionable. Perhaps one way of improving this limitation is to explore the ways in which NPSV could be integrated into emerging ESG practices. Second, some planning systems may have very few opportunities to employ the metric and shape development outcomes. For example, European countries have two distinct planning styles: those that adhere as strictly as possible to pre-conceived plans (i.e., conformative) and those that are based on a more discretionary regime (i.e., performative) (Janin Rivolin, 2017). Planners in a performative system may utilize NPSV to identify proposals that may be exploitative and thus require measures to compensate the public interest, whereas those in a conformative system would not have such an opportunity to do so on a project-by-project basis. In places where planning is less discretionary, focusing efforts to introduce NPSV to the real estate sector may be more effective.

Scholars have called for planners to more actively engage with the impacts on the sociospatial inequality generated by large-scale urban developments (Searle and Legacy, 2021). To do so, planners must understand the theories and practices of valuation and value, but existing planning scholarship provides little guidance. This article attempted to fill such a gap by questioning the meaning of value underlying the conventional DCF valuation technique. By reviewing existing literature on value and valuation within planning and real estate fields and by applying David Harvey’s interpretation of the Marxian theory of value, I demonstrated how DCF predominantly captures the exchange values of a property, its worth to the investors, and proposed developing an alternative framework to capture the use values of a property to the society, its worth to the society at large.

I then engaged in a thought experiment by developing a method for calculating the social values of real estate development. I adapted the SROI framework developed and established in the social entrepreneurship field to conceptualize how this social value may be quantified. Recently, Farley (2023) suggested a somewhat analogous approach to calculate the financial benefits of income-restricted affordable housing. The author suggested discounting the future savings in rent for future residents to calculate the present value of affordable housing. The proposed framework differs from Farley’s approach in that it is the benefit to the society that is being calculated, not to individual households.

Finally, I used empirical studies that have documented the types of positive social benefits that could be provided in the context of real estate development and created an exhaustive list of possible benefits discussed in these studies. I further demonstrated how these social benefits can be quantified as cost savings to government programs. The goal was to illustrate how NPSV can be calculated in practice.

Before concluding the paper, I would like to propose ideas for future research. First, because this was an attempt to balance theory and practice, I was not able to engage deeply with either side. While the paper could have been very well split into two papers, one focused on theory and another focused on practical methodology and its application, I believed that there was a strong merit in writing a single paper that could bridge theory and practice. Accordingly, future research can take up either the theoretical debates on urban development or the practical application of NPSV and investigate these lines of inquiry to a greater depth.

A follow-up theory paper should engage more comprehensively with the existing literature on urban development. For example, well-established theories such as the rent gap theory (Smith, 1987) and the literature on the financialization of real estate (Harvey, 1978) should be engaged to identify how planning and urban scholars have conceptualized value and valuation as a force guiding urban processes. A practice-oriented paper could take a concrete example of an urban development project and calculate the NPSV to expose the challenges of applying this framework in a real-world context and evaluate the usefulness of the metric. Such efforts would allow for the establishment of a body of knowledge on the theories and practices of value and valuation that is sorely needed in planning scholarship.

My hope is that this paper inspires planners and community members to conceptualize and effectively communicate the social impacts of real estate developments and allow them to have a more equal footing in evaluating the merits of these projects. NPSV also holds the potential to alter the conversation in the real estate world by enabling investors to understand and clearly see the social impacts of real estate development. Such an acknowledgment may lead to more socially responsible investing and development practices. In the least, I hope this paper has sufficiently convinced the readers on the importance of understanding how and why property values and valuation practices matter for planning practice.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.