Abstract

Measuring corporate contributions to climate change is often crucial for investors, policymakers and legal frameworks. Current methods use attributional carbon footprint metrics, which quantify emissions linked to a company's activities. Despite its widespread use, this approach faces challenges like ‘brown spinning’ and fails to account for substitution effects. In response, some advocate for consequential metrics, which consider alternative scenarios and counterfactuals to measure the impact of corporate actions on global emissions. This paper critically examines both approaches, arguing that while attributional metrics are flawed, consequential metrics often require infeasible levels of predictive precision and counterfactual analysis. We propose that different contexts and purposes warrant different approaches. For some purposes and contexts, like carbon taxation, a restricted attributional method that focuses exclusively on Scope 1 is suitable. For other purposes, like setting Environmental, Social, and Governance ratings, we suggest an elaborated attributional framework that also accounts for indirect causal contributions not captured by standard Scopes 1–3 emissions. In yet other cases, standard or elaborated forms of consequential metrics may be more suitable.

Keywords

Introduction

Determining a company's climate impact is often crucial for policymaking, investment strategies, corporate planning, legal accountability and more. Politically, we may want to reduce corporate emissions through carbon taxes, cap-and-trade systems, or mandatory carbon reporting, such as the EU's Corporate Sustainability Reporting Directive (CSRD). Financially, investors may seek to support sustainable companies – those with strong Environmental, Social, and Governance (ESG) ratings, including credible climate performance. Companies themselves may also aim to reduce their climate impact, for example, when developing new products or setting long-term strategies. Legally, the stakes are high. In Milieudefensie v. Shell, for instance, the environmental organization Milieudefensie demanded that Shell reduce its emissions to avoid causing climate-related harm to Dutch citizens. The case in part hinged on how Shell's climate impact should be assessed: is its impact equivalent to its carbon footprint? If so, Shell should reduce its footprint to reduce its climate impact. Or is its impact instead the difference it makes to global emissions? In that case, reducing its emissions might not make a difference, since competitors are likely to step in to meet consumer demand when Shell reduces operations. This illustrates how determining a company's climate impact is not only conceptually complex but also practically consequential.

Yet it remains unclear how a company's climate impact should be measured. Attributional metrics, currently dominant, quantify the total emissions linked to a company's activities, including carbon footprints and attributional life cycle assessments. These metrics describe a company's emissions profile. 1 However, when interpreted as measures of a company's climate impact, they are problematic, as they often ignore important indirect effects. For example, they can incentivize ‘brown-spinning’, where companies reduce their carbon footprint by selling off high-emission operations to less climate-conscious entities, potentially leaving global emissions unchanged or even increased (Brander, 2022; Gözlügöl and Ringe, 2022; Weidema et al., 2018), counteracting the aim of alleviating climate change.

These shortcomings have led some to advocate for consequential metrics, which assess how a company's activities influence global emissions. Unlike attributional metrics, consequential metrics do not treat footprint reductions as climate benefits unless they result in actual decreases in global emissions. However, consequential metrics also face serious challenges. They can be poor indicators of impact in overdetermined scenarios, where many actors contribute to the same outcome. They rely on counterfactual reasoning and predictions about future developments, making empirical estimation difficult. It is often unclear what the relevant baseline for comparison should be, which means results can vary significantly depending on the chosen reference point. Moreover, consequential metrics can lead to double-counting, making them unsuitable for certain applications like carbon taxation or cap-and-trade schemes. Finally, because emissions are typically reported using attributional methods, adopting a consequential framework can be too revisionary in many practical contexts. More sophisticated theories of causation could, in principle, improve the accuracy of consequential metrics. However, these approaches require even more detailed data and complex modelling of future scenarios, making them even harder to implement in practice.

This paper examines the merits and limitations of both attributional and consequential approaches to measuring corporate contributions to climate change. It argues that the choice of metric should be guided by the specific purpose of the assessment – whether for political policy making, ESG evaluation, legal responsibility, or deciding the emissions a company has causally contributed to. In doing so, we recognize that this choice must be made under conditions of uncertainty and imperfect information. 2

Building on Plevin et al. (2014), Brander and Ascui (2016) and Brander (2022), we argue that attributional approaches can be sufficient for certain purposes. For example, a limited attributional approach focusing on direct (Scope 1) emissions may be appropriate for carbon taxation or cap-and-trade schemes. In contrast, an expanded attributional approach – including indirect emissions beyond Scopes 1, 2 and 3 – may be more suitable for ESG ratings or assessments of corporate climate-friendliness. Consequential approaches, by comparison, may be better suited for other purposes. A standard consequential metric may be appropriate for evaluating the overall effects of carbon pricing or regulatory schemes on global emissions, while more elaborate consequential metrics – drawing on refined theories of causation – may be useful for determining which emissions a company causes. These may be particularly relevant in scientific, journalistic, or certain legal contexts.

The paper begins by introducing attributional approaches and examining why they fall short as metrics of climate impact, using the carbon footprint as a key example. It then turns to consequential approaches, highlighting both their conceptual and practical challenges. The section that follows after that explores the trade-offs between these two ways of measuring impact, emphasizing that the most appropriate metric depends on the context and purpose. The paper concludes by drawing together these insights.

An attributional metric: the carbon footprint

The concept of a carbon footprint encompasses diverse methods for measuring the impact of activities on Earth's climate, but lacks a universally accepted definition or standardized framework (Matuštík and Kočí, 2021). It is used in two general ways.

Originally, an entity's carbon footprint was understood as the forest area required to absorb its CO2 emissions, rooted in the broader ecological footprint framework introduced by Rees (1992) and Wackernagel (1994). The ecological footprint measures human appropriation of natural resources relative to Earth's carrying capacity, initially focusing on land needed for urban regions. It evolved into a metric quantifying the total land and water area required to produce consumed resources and absorb waste, particularly carbon dioxide, usually measured in ‘global hectares’ (Borucke et al., 2013). The ecological footprint highlights when human demand exceeds the planet's regenerative abilities, known as ‘overshoot’, and is widely used in academic research and public reporting, including tools like the annual National Footprint Accounts and Earth Overshoot Day.

Today, the carbon footprint is more commonly defined as the total greenhouse gas (GHG) emissions attributed to an entity, activity, or product. Wiedmann and Minx (2008) describe it as the ‘exclusive total amount of carbon dioxide emissions directly and indirectly caused by an activity or accumulated over the life stages of a product’, a definition echoed by the IPCC (2022). This measure, often expressed in carbon dioxide equivalents (CO2e), typically forms the basis for corporate GHG reporting through frameworks like the Greenhouse Gas Protocol (2004), which categorizes emissions into three scopes: Scope 1 (direct emissions from owned sources), Scope 2 (emissions from purchased energy) and Scope 3 (value chain emissions, including the emissions of suppliers and product users, and transportation). 3

The carbon footprint of a company (or a person, or nation) is best understood as a measure of its carbon emissions profile, but it is often taken to be a measure of its impact on climate change. This conflation occurs regardless of whether it is expressed in terms of the forest area needed to absorb CO2 emissions or total GHG emissions. For instance, Wackernagel (1994) says that the ecological footprint ‘stands for the impact on nature of the aggregate consumption per population’ (69), and Wiedmann and Minx (2008) describe carbon footprints in terms of environmental impact. Similarly, the Carbon Trust, a UK-based not-for-profit organization established by the government to promote low-carbon innovation and resource efficiency, writes that ‘Many businesses want to understand the impact they are having on climate change. Calculating a carbon footprint is an essential starting point’ (2023: 3). Encyclopedia Britannica (2025) also links the concept to environmental impact, noting that it grew out of the ecological footprint, which includes ‘environmental impacts, such as water use and the amount of land used for food production’. Moreover, it is not uncommon for research papers to equate an entity's carbon footprint with its climate impact. 4

The primary advantage of measuring a company's contribution to climate change in terms of its carbon footprint is the apparent clarity and simplicity of the metric – it seems clear what is being measured, and emissions are relatively straightforward to quantify. This makes it an easily understandable metric for stakeholders such as employees, consumers and investors (Alvarez et al., 2016; Matuštík and Kočí, 2021). While the carbon footprint metric appears clear and easy to quantify, this clarity can be misleading: it measures a company's emissions profile, yet is often mistaken for a measure of its actual climate impact. We soon return to the issue of why attributional approaches do not capture impact well.

Before doing so, we briefly note several issues with the attributional approach that we set aside in what follows. Firstly, there is little consensus on how to measure carbon footprints, particularly regarding which GHGs should be included. Approaches vary from focusing solely on fossil CO2 to including other gases like CH4 and N2O, or the six GHGs identified in the Kyoto Protocol (Wright et al., 2011). Secondly, the original method of calculating the carbon footprint based on the forest area required to absorb emissions has been criticized for considering forest absorption as the sole means of mitigating CO2 accumulation (Giampietro and Saltelli, 2014). Thirdly, there is a question of which scopes should be included (Pandey et al., 2011). Lastly, achieving accuracy in footprint calculations is challenging, especially with Scope 3 emissions, due to data gaps, uncertainty and other obstacles (Hettler and Graf-Vlachy, 2024; Patchell, 2018). Having set these issues aside, we want to focus on additional problems – or counterexamples – the carbon footprint approach faces when understood as a metric of climate impact, even if we agree on which GHGs and scopes to include, and even if we can calculate those emissions accurately.

First, we find the problem of brown spinning: companies might ‘go green’ by offloading dirty operations. For example, ConocoPhillips, a major U.S. oil company, reported a significant 22% reduction in emissions in 2017, primarily due to the sale of some oil and gas assets. This divestment led to a drop in the company's emissions that far exceeded reductions achieved through operational improvements by other companies. However, the buyer's intent to continue production raises doubts about whether ConocoPhillips achieved any real overall emissions decrease. The sale was more about what goes on their ledger than about curbing climate change. Generally, there is a surge in private companies acquiring assets from public carbon majors in the U.S., driven largely by private equity's appetite for these profitable assets. While these transactions may not be inherently harmful, they raise concerns about high-polluting assets moving to less transparent private markets, where limited disclosure and a lack of institutional investor engagement can shield owners from scrutiny and pressure to decarbonize (Berg et al., 2023; Gözlügöl and Ringe, 2022).

This trend is not unique to the U.S. In Europe, energy firms like E.ON and Vattenfall are offloading high-polluting assets, such as coal plants, to private buyers while presenting themselves as green. They often dramatically reduce their carbon footprint in the process. However, this practice does little to reduce overall emissions, as the plants continue to operate under new ownership, shifting the ownership of the polluting assets without addressing the climate crisis (Chatterjee et al., 2023). Extending the carbon footprint measure to include Scopes 2 and 3 emissions does not help attribute the emissions from the offloaded companies to the offloading ones. Since ConocoPhillips, E.ON and Vattenfall have sold the high-polluting operations, the upstream and downstream emissions of these operations no longer fall on their account. Thus, measuring climate contributions in terms of carbon footprints has counterintuitive implications in such cases. The carbon footprint of a company might decrease while its actions result in increased global emissions.

Second, although uncommon, we might consider the reverse scenario. Suppose an energy company invests in a high-polluting coal power plant and installs effective – but not completely effective – carbon capture equipment. We could call this an emission reduction acquisition. In this case, the company seems to ameliorate climate change, yet its carbon footprint increases, counterintuitively indicating a negative impact on the climate.

Third, a further potential problem with carbon footprint metrics is their failure to account for substitution effects. Consider a climate-conscious fossil fuel company that decides to reduce its production of fossil fuel products to alleviate climate change. However, due to persistent consumer demand, less scrupulous competitors step in and sell similar products or even more carbon-intensive products, with the result that global emissions stay the same or even increase. In this case, as in the case of brown-spinning, the company's carbon footprint decreases while its decision has no positive – or even a negative – impact on the climate. This illustrates how substitution effects might be said to undermine the reliability of carbon footprints as indicators of climate impact.

Still, it is unclear whether substitution effects are always problematic. One might argue that if a company reduces its emissions and competitors increase theirs in response, it is those competitors – rather than the original company – who contribute to the resulting emissions. There is an important difference between indirectly causing emissions, as when a company sells fossil fuels that consumers burn, and cases where competitors increase production to compensate for the reductions the company has made. In the latter case, the emissions occur despite the company's decision, not because of it. This reflects a familiar distinction in causal theory: some actions fail to be difference-making, even though more nuanced accounts still count them as causal contributors in preemption-like scenarios, where another agent would have produced the same outcome had the first not acted (we will consider such scenarios in the next section). Whether such substitution effects should therefore be attributed to the company is contestable. If the increased emissions merely reflect competitors scaling up, they may not undermine attributional metrics. Still, we remain undecided about whether all substitution effects should be excluded or whether some warrant inclusion. 5

In conclusion, the carbon footprint does not accurately measure impact. If you are a politician aiming to implement policies to reduce global climate change, it might be unwise to single-mindedly aim at implementing policies that target companies’ carbon footprints. 6 Likewise, if you are a company leader or owner seeking to help the environment, it might be a bad idea to single-mindedly aim to reduce the carbon footprint of your company.

Consequential metrics

The literature on product life-cycle assessments (LCAs) provides an alternative approach to measuring climate impacts. Since the 2000s, authors have distinguished between attributional and consequential accounting of LCAs (Brander, 2022; Brander and Ascui, 2016; Curran et al., 2005; Ekvall and Weidema, 2004; Finnveden, 2008; Plevin et al., 2014; Weidema et al., 2018). Attributional accounting aims to determine the environmental impact of a product's life cycle. Like carbon footprint measures, it focuses on describing and quantifying the emissions of processes directly associated with producing, using and disposing of the product, often based on current or historical data. For example, in the production of a car, attributional accounting would quantify the direct emissions and resource use from extracting materials, manufacturing parts, assembling the vehicle and its eventual disposal, attributing those emissions to the car without considering alternative scenarios or possible future consequences.

Attributional accounting provides a clear and straightforward snapshot of a product's life-cycle emissions, using historical and current data that is typically more accessible than predictive or scenario-based data. In these respects, it resembles the carbon footprint measure. However, it faces similar problems: uncertainty about which GHGs and activities to include, difficulties in accurately measuring emissions – especially Scope 3 – and, most importantly for our purposes, it does not offer a reliable metric of climate impact, as it cannot account for substitution effects or analogues of brown spinning and emission reduction acquisition.

In contrast, consequential accounting considers indirect emissions, alternative scenarios and future consequences, focusing on the marginal effects on climate change from developing and marketing a product. It measures the impact of a product by comparing the global emissions if the product were introduced to a baseline scenario, such as global emissions before the introduction or global emissions if the product had never been introduced. While attributional accounting measures absolute emissions (e.g. CO2e from a product's development and marketing), consequential accounting measures changes in emissions (e.g. whether emissions will increase or decrease due to the introduction of the product). Attributional accounting typically estimates emissions over time for entities like companies or nations, whereas consequential accounting estimates the emissions caused by specific actions or decisions, such as developing a product. However, consequential accounting can also estimate the emissions of an entity over time, namely by comparing actual emissions during a time period to some baseline scenario. In sum, consequential accounting aligns with the economic notion of ‘impact’, comparing actual outcomes to a baseline of counterfactual or historical scenarios (Curran et al., 2005; Imbens and Rubin, 2015; Plevin et al., 2014).

Weidema et al. (2018) argue that responsible decision-makers who seek improvements and have a focus on what they can influence should use consequential accounting. They should do so since it is wider in scope, taking all consequences into account, including indirect effects. To illustrate, they offer the following example (here presented in abbreviated form), which basically is a substitution effects example: Dairy dilemma: Say that a dairy farmer could reduce the direct emissions from milk production by changing the composition of the fodder. As a side-effect, this would reduce the meat production from dairy cows. Since meat demand remains unchanged, the shortfall would be met by an increased beef cattle production elsewhere. As a result, the direct emissions from producing milk would decrease, but the global emissions would increase.

Here, attributional accounting implausibly suggests that changing the fodder composition would be good for the climate, since doing so would reduce the direct emissions from milk production. In contrast, consequential accounting correctly implies the opposite, since changing the composition of the fodder would increase global emissions. Similarly, Plevin et al. (2014) advocate consequential accounting in decision-making because it accounts for broader, indirect system-wide effects. This metric, they argue, helps policymakers implement strategies that are less likely to create perverse incentives and more likely to lead to effective climate mitigation.

This raises the question of whether we should adopt a consequential approach not only when conducting LCAs of products, but also more broadly. For instance, consequential metrics can be used to evaluate the climate impact of companies or nations – understood as the difference they make to global emissions. A similar method might even be applied to assess the climate impact of decisions and policies, such as carbon pricing or regulatory interventions. However, since such evaluations do not involve a standardized, repeatable measurement, it may be misleading to call them metrics. It is better to describe them as a consequential approach – a broader methodological framework that includes, but is not limited to, metrics. This approach focuses on estimating the difference an action, decision, or policy makes to global emissions.

Doing so would let us avoid counterintuitive results in cases of brown spinning, emission reduction acquisition and (where relevant) substitution effects. In the case of brown spinning, the offloading of dirty assets by one company to another – that continues the operations – would not count as having a positive impact on the environment, since global emissions remain the same. In cases of emission reduction acquisition, a company's purchase of high-emission operations followed by improvements that reduce their climate impact would not count as having a negative impact. Instead, it would be recognized as a positive contribution, since global emissions decrease. 7 Finally, substitution effects would matter. For instance, if a climate-conscious fossil fuel company reduces its production to lower emissions, but competitors step in to meet the unchanged demand – potentially with more carbon-intensive products – global emissions may increase. A consequential metric would capture this dynamic, showing that the company's decision, despite reducing its own emissions, did not have a positive impact on the climate. 8

However, consequential approaches also face significant challenges, particularly because they rely on the notion of counterfactual difference-making. This dependence creates issues similar to those encountered by ethical consequentialists and proponents of the ‘but-for’ condition in causation theory, which states that an earlier event is a cause of a later event if and only if it makes a difference to whether the later event occurs. Most of the objections we raise in this section apply regardless of whether consequential approaches are interpreted as measures of climate impact or simply as tools for estimating the difference an action makes to global emissions. However, one objection in particular – that consequential approaches can be poor indicators of impact – only arises if we assume that these approaches are intended to capture climate impact in a broader, causally robust sense.

Empirical challenges

A first problem with consequential approaches is their reliance on counterfactual scenarios and future consequences, making it difficult to estimate climate impacts empirically. While attributional metrics require measuring actual emissions, consequential approaches also require evaluating emissions that would have occurred under different circumstances. Methods like randomized control trials (comparing outcomes between treated and control groups), synthetic control methods (creating a ‘synthetic’ comparison group by weighting data from similar entities that were not exposed to the intervention) and structural models and simulations (theoretically modelling scenarios with and without the intervention) can estimate counterfactuals, but they have significant limitations. These methods need robust, high-quality data, rely on assumptions that can introduce bias and struggle to capture the complexity of real-world interactions (Imbens and Rubin, 2015). Consequently, estimating counterfactual scenarios is more challenging and uncertain than measuring actual outcomes. As Suh and Yang (2014) warn, while consequential accounting might seem ideal in theory, it is less obvious that real-life consequential LCAs are accurate.

Additionally, using counterfactual scenarios to assess causation often requires projecting far into the future, which is particularly challenging. As projections extend, data and assumptions become less reliable, and small inaccuracies can compound over time, increasing speculation. Estimating long-term impacts involves subjective decisions about prioritizing factors and valuing future outcomes (e.g. through discount rates or cut-off points). 9 These choices can make us include some indirect effects but not others, making certain decisions appear more favourable and potentially misleading to policymakers. Moreover, consequential metrics can yield misleading results if applied inconsistently. For instance, Dale and Kim (2014) caution that including indirect effects when evaluating biofuels, but not when evaluating petroleum fuels, could make the latter appear more climate-friendly, despite their higher direct emissions.

Finally, as Brander et al. (2019) point out, if we consider the entire range of possible actions available to a company at any given moment, the scale of the challenge of estimating counterfactuals becomes evident. We must account not only for actions taken but also for actions that could have been taken but were not. So, at any given moment, there are plenty of counterfactuals to consider, each of which requires meticulous measurements and calculations. Beyond empirical difficulties, consequential metrics also face conceptual challenges in how they represent impact, which brings us to the next problem.

Poor indicator of impact

Second, even if we could estimate the relevant counterfactuals, the standard consequential metric (that adopts the but-for condition of causation) gives a poor indicator of climate impact. As Brander et al. (2019) highlight, an agent can still be causally responsible for an outcome even if their actions do not make a counterfactual difference to it. Consider the following overdetermination case: Extra Enterprise: Three fishing companies deliberate whether to start catching fish in a lake. However, there are not enough fish in the lake for everyone. If two or more companies proceed with their plans, the fish will go extinct. As it turns out, all three companies proceed with their plans, and the fish go extinct.

Each company seems to have contributed to the extinction of the fish. However, according to the standard consequential metric, this is not the case. The fish would have gone extinct irrespective of any individual company's actions. Therefore, according to standard consequential metrics and the but-for condition for causation, none of the companies caused the extinction of the fish.

It is disputed what the accurate judgment about the impact is in cases of overdetermination (Lewis, 1973a).

10

Nevertheless, the standard consequential metric also produces counterintuitive outcomes in less controversial instances. For example, consider a scenario often referred to as a ‘pre-emption case’ in discussions of causation and ethics, where the first agent serves as a pre-emptive cause of the outcome. The following version is inspired by Weidema et al. (2018): Backup Business: A fishing company plans to catch all the wild fish in a lake using high-impact bottom trawling, while a second company is ready to do the same if the first abstains. These are the only two fishing companies in the area, so if neither acts, the ecosystem of the lake will continue thriving. As things turn out, the first company proceeds with the catch, driving the fish to extinction.

Intuitively, it seems clear that the first company caused the extinction – this was the result of its actions. Yet, the standard consequential metric would entail that these actions had no impact since the same outcome would have occurred regardless, due to the second company's readiness to act.

To some extent, these problems can be resolved. The causation literature offers more nuanced ways of measuring causal contributions or impact. For instance, taking their cue from the causal modelling approach to causation (Hitchcock, 2001; Pearl, 2000; Woodward, 2003), Halpern and Pearl (2005) suggest that, roughly, C is a cause of an effect E if C is a but-for condition for E under some contingency in which the actual path leading from C to E is the same as in the actual world. On this definition, the first company caused the fish to go extinct in Backup Business. In the contingency where the second fishing company will not catch the fish regardless of what the first company does, the fact that the first company catches the fish is a but-for condition for the extinction. If they had not caught it, the fish would not have gone extinct. Moreover, the actual causal path leading from their catching the fish to the fish going extinct is the same as in the actual scenario. So, this account accurately entails that the first company caused the fish to go extinct. The account also gives the right verdicts in Extra Enterprise. Wright’s (1985, 2013) Necessary Element of a Sufficient Set (NESS) condition for causation and Touborg's (2018) security account of causation might also deliver accurate verdicts in these cases.

Thus, the standard consequential metric proposed by Brander and Ascui (2016) and Weidema et al. (2018) could be updated using more precise accounts of causation. This illustrates that the consequential approach is not merely one approach, but many. It encompasses several possible metrics, informed by different accounts of causation. 11

Still, there are grounds to believe that more accurate consequential approaches, building on more nuanced accounts of causation, will be even harder to apply. These more accurate accounts of causation typically require even more elaborate estimations of counterfactuals, making them even harder to pin down empirically than the standard consequential approach. While the standard consequential approach requires us to compare what happens if the action under evaluation is performed to what happens if it is not, the other approaches require us to consider what would happen in further contingencies. For example, in Backup Business, the standard approach requires us to compare what would happen to the fish if the first company catches all the fish to what would happen if it does not. However, Halpern and Pearl's approach requires us not just to consider these possibilities but also, on top of this, what would happen if the first firm catches all the fish, given that the second will not, and what would happen if the first firm does not, given that the second will not.

Generally, the more accurate accounts of causation can deliver correct verdicts about causation in cases like this because they are sensitive to more counterfactuals. While taking additional counterfactuals into account is straightforward in our thought example, it will require even more elaborate estimations in real cases, introducing even more uncertainty about the results. It seems we need something like a Laplacian demon to get this right.

So, in circumstances where estimations of counterfactuals are difficult, there is an assessment to be made: should we opt for a simpler counterfactual approach that might give inaccurate verdicts about the consequences of the companies’ decisions, or should we opt for a more complex approach that requires more counterfactual estimations and that might be inaccurate if not done properly? Regardless of which we choose, we must be aware of the downsides.

Difficulties in setting the relevant baseline

A third challenge is how to establish the relevant baseline for comparison. In ethical theory, consequentialists argue that we should choose the actions that yield the best outcomes. Applied to emissions accounting, this means the baseline should reflect the best possible actions a company could take to minimize emissions. For example, if global emissions were 53,000 Mton CO2e in a given year, but would have been 52,000 Mton CO2e if a major fossil fuel company had invested in renewable energy instead of continuing business as usual, the ledger of the company would show a difference of 1000 Mton CO2e. This approach requires that any deviation from the optimal action be recorded on the company's emissions ledger, making it a demanding criterion.

Alternatively, the baseline could be what would have happened if the company had not acted as it did. This approach, common in evaluating counterfactuals (Lewis, 1973b), compares actual global emissions to the emissions that would have occurred if the company had not acted in the way it did. The challenge with this baseline is that the emissions ledger can vary significantly depending on what the company would have done otherwise. For instance, if a major fossil fuel company continued business as usual, this might be seen positively if the alternative was extracting and selling even more fossil fuel. Conversely, if the alternative were investing in renewable energy, continuing business as usual would be viewed negatively for the climate.

The two baselines considered so far are counterfactual. Using a historical baseline might avoid these issues, but as Moore (2003) argues, it often yields unreliable results. For example, measuring global emissions before and after the introduction of a product can be misleading. Implementing energy-efficient processes may counterintuitively appear to have a negative impact on the climate if global emissions rise overall. Conversely, if global emissions decline, implementing less energy-efficient processes might seem environmentally friendly.

You might think the problem with the baselines we have considered so far is that they concern global emissions rather than the emissions of the company. However, focusing solely on the company's emissions without considering global emissions might also be misleading. For instance, a company adopting energy-efficient technology might reduce production costs, leading to lower product prices and increased consumption of its products. The increased production could result in higher emissions for the company, even though global emissions decrease due to reduced consumption of competitors’ less climate-friendly products. In such cases, focusing only on the company's emissions would make the adoption of energy-efficient technology appear harmful to the climate, when it is actually beneficial. In other words, we would reencounter many of the problems associated with attributional approaches.

In addition, even when there is a set baseline, there are (as stated earlier) empirical challenges in measuring the relevant counterfactuals. This uncertainty creates room for manipulation. For example, Reducing Emissions from Deforestation and forest Degradation (REDD+) projects, which aim to reduce emissions from deforestation and forest degradation, often use these projected reductions to generate carbon credits that can be bought to offset emissions. Here, the baseline is set: it is the emissions that would have occurred without the REDD+ project. However, West et al. (2023) examined 26 such project sites across six countries using synthetic control methods and found that all had significantly exaggerated their impact. The exaggeration stemmed from inflated estimates of baseline deforestation, meaning the actual reductions were far smaller than claimed. In a similar manner, it is possible for companies to exaggerate the emissions that would have occurred without their products, making their products seem beneficial for the climate.

In sum, establishing a relevant baseline for emissions comparison is challenging. Both counterfactual and historical baselines can yield unreliable results, and focusing solely on the emissions of companies without considering global emissions can be misleading. Additionally, while consequential metrics might initially seem clear, they become ambiguous upon closer scrutiny. For instance, does it measure the difference between what actually happened and what would have happened if the company had taken green measures? Or does it measure the difference between later and earlier levels of emissions? Finally, since it is difficult to estimate the relevant counterfactuals, there is a risk that companies choose a baseline that either exaggerates their climate efforts or plays down their impact.

Problems of additivity and double counting

Even if we could determine the relevant baseline, calculate the relevant counterfactuals in an accurate manner, and resolve issues of overdetermination and preemption, consequential approaches might still not fit our purposes. In life-cycle accounting, we often need additivity – the ability to sum the climate impacts of multiple products or actions to get a meaningful total. Tillman (2000) emphasizes that additivity is crucial for applications like environmental product declarations, where each producer must report impacts that can be summed across the supply chain, and for national or sectoral inventories, where the total environmental impact should equal the sum of its parts. Brander et al. (2019) add that without additivity, it becomes difficult to assign responsibility or design effective policy instruments. In particular, non-additivity can lead to double-counting, where the same emissions are attributed to multiple actors. This is especially problematic in carbon taxation and cap-and-trade schemes, where emissions are tied to financial obligations. Double-counting in such contexts can distort incentives and allow companies to appear more climate-friendly – or less liable – than they actually are while doing nothing to reduce global emissions. So, in some contexts, lack of additivity is problematic.

The problem is that consequential approaches do not provide additivity. The differences made by individual actions do not necessarily add up to the total impact of the full set of actions, including those individual ones. For example, in Extra Enterprise, no single firm caused the extinction of the fish, but the combined actions of three firms did. Conversely, the combined actions might make less of a difference than their individual parts, as illustrated in the following case: Corporate Complacency: A carbon recapture facility offers ten major airline companies the chance to offset emissions from 1000 flights per year. This is the maximum capacity of the facility. All the companies decline, the facility goes bankrupt, and no carbon dioxide is recaptured.

We get similar results with more elaborate consequential metrics, building on other accounts of causation. For example, in Extra Enterprise, each firm would be seen as causing the extinction of the fish. Adding these outcomes suggests that the firms could save the fish in three lakes, which they cannot. Moreover, in Corporate Complacency, each airline would be seen as causing the extra emissions from 1000 flights per year, leading to the same issue as the standard metric did. Thus, consequential metrics fail to provide additivity whenever the impact of each action does not sum to the impact of all actions combined.

As Brander et al. (2019) point out, this lack of additivity can lead to double-counting. In Corporate Complacency, the emissions that are not offset are recorded on the ledger of each company, resulting in tenfold accounting. If a carbon tax or cap-and-trade scheme is introduced, this creates bad incentives. For example, two airline companies could merge to reduce their emissions ledger without reducing global emissions. The merged company could still only offset emissions equivalent to 1000 flights, cutting the combined emissions that go on its ledger in half, while global emissions remain unchanged.

Consequential metrics are too revisionary

Finally, even assuming that a consequential framework would be viable in theory, there are pragmatic reasons not to give up on attributional metrics. The current international framework is framed in terms of carbon footprints. For example, ESG ratings of companies, which are often regarded as crucial for investors and stakeholders, rely heavily on carbon footprint data to assess the environmental impact of these companies (Bose, 2020). These ratings influence investment decisions, corporate strategies and regulatory compliance. Moreover, international agreements and policies, such as the Paris Agreement, are structured around carbon footprint metrics. Carbon pricing mechanisms, including carbon taxes and cap-and-trade schemes, also depend on attributional metrics to set emission reduction targets and track progress. Although the prominence of attributional metrics partly reflects historical convention, their continued use is not entirely unwarranted: they offer a standardized, transparent and relatively tractable basis for emissions reporting, which is essential for comparability and accountability. Shifting to consequential metrics would require a fundamental overhaul of these established frameworks, which is a complex and resource-intensive process.

Changing the international framework from carbon footprints to consequential metrics presents several challenges. First, it requires developing new methodologies and standards for measuring and reporting emissions, which involves significant time, effort and coordination among stakeholders like governments, corporations and international organizations. Given the urgency of addressing climate change, it may be more effective to focus on reducing emissions and making moderate improvements to the current framework rather than a complete overhaul. Second, there is a risk of inconsistency and confusion during the transition period, as different entities might adopt different approaches to measuring, leading to a lack of comparability and reliability in emissions data.

Navigating attributional and consequential approaches

It seems we are stuck between a rock and a hard place. Attributional measures are practical but often fail to capture key indirect contributions to climate change, even when including Scope 3 emissions. Conversely, consequential measures, while more accurate in assessing the climate impacts of decisions, are often impractical due to their complexity and heavy data requirements. This creates a trade-off: a feasible but less precise approach versus an accurate yet impractical one.

Given these considerations, our choice of method must be guided by context and practicality, especially when we lack perfect information, including information about counterfactuals. As Brander and Ascui (2016), Brander (2022) and Plevin et al. (2014) suggest, attributional approaches to measuring emissions can be sufficient for certain purposes, providing a workable approximation when complexity or data constraints limit more advanced methods. Attributional metrics are suitable for estimating the emissions directly associated with a specific product or entity, making it useful for allocating carbon budgets and setting reduction targets, but they often fail to accurately represent companies’ main impacts on climate change, at least if they are indirect. Conversely, consequential metrics, despite all their difficulties, are indispensable in other circumstances. It provides information on system-wide or global changes caused by actions, making it ideal to assess decisions aimed at reducing emissions on a broader scale by understanding the overall impact beyond the emissions directly associated with a specific product or entity.

Still, Brander's, Brander and Ascui's and Plevin et al.'s approach is too coarse-grained. There are several versions of each method. Firstly, the attributional method, including Scopes 1, 2 and 3, should be supplemented by more limited versions focusing only on Scope 1 and by expanded versions that can deal with brown spinning, emission reduction acquisition and substitution effects. Secondly, as we have already seen, there are consequential methods beyond the standard difference-making model that may be preferred in certain contexts. In this section, we develop these ideas further.

A limited attributional metric

A limited attributional metric can be suitable when measuring emissions for carbon pricing. For example, carbon tax schemes typically focus on direct (Scope 1) emissions, as observed in countries like Sweden, Finland, Canada and Singapore, where the tax primarily targets emissions from fossil fuel combustion and industrial processes (UNDP, 2025). Similarly, cap-and-trade schemes also target direct emissions, as seen in the European Union Emissions Trading System (EU ETS) scheme (European Commission, 2024).

These limited attributional approaches are practical but often overlook the indirect emissions of companies and so fail to fully capture some of their important contributions to climate change. However, depending on our purpose for measuring climate impact, this may not be a significant issue. Implementing a carbon tax does not require consideration of indirect emissions. For instance, oil producers may not be seen as major contributors to climate change when only Scope 1 emissions are analysed, while consumers of their products are. Nevertheless, indirect emissions are addressed through the ripple effect of a carbon tax, which raises gasoline prices, potentially leading to reduced consumption and encouraging a shift toward alternative energy sources. Similarly, the increased costs for polluting companies under a cap-and-trade regime are usually passed on to the consumers of their products or services, resulting in decreased demand and, consequently, lower emissions. Therefore, if reducing emissions is our motivation for implementing a carbon tax or cap-and-trade scheme, it may not matter that it targets only Scope 1 emissions.

Additionally, within carbon pricing schemes, issues such as brown spinning, emission reduction acquisitions and substitution are not problematic. The new owner of ‘dirty’ assets remains subject to the carbon tax or cap-and-trade scheme, ensuring global emissions are reduced regardless of ownership. Emission reduction acquisitions are encouraged by lower carbon taxes or fewer emission allowances. Finally, substitution effects are handled as carbon taxes or a cap-and-trade scheme targets all emissions equally, regardless of the emitter. Therefore, these schemes effectively manage emissions across the board. Focusing solely on Scope 1 is acceptable as long as the goal is to incentivize decreased emissions. 12 However, this scope is far too narrow if our purpose is different.

Elaborate attributional metrics

If our purpose instead is to evaluate the overall climate impact of a company (e.g. for ESG ratings 13 or setting Science Based Targets 14 ), its moral responsibility for climate change, or simply whether it is climate-friendly, indirect effects such as those arising from sold assets matter, and depending on one's view of substitution effects and their causal relevance, some of these may need to be included as well. ESG ratings and Science Based Targets are intended to guide investment decisions, corporate strategy and public accountability by signalling whether a company is aligned with climate goals. In such contexts, an elaborate attributional metric that considers more indirect effects may be appropriate, especially when a consequential metric is infeasible due to the challenges of calculating counterfactuals and deciding the relevant baselines.

We suggest that attributional metrics face challenges in cases like brown spinning because they adopt an overly restrictive view of when companies contribute to emissions through the actions of others. While these metrics may include some indirect effects – such as emissions from purchased energy (Scope 2) and other value chain emissions (Scope 3) – they typically focus on just two types of influencing acts: purchasing (e.g. energy from coal power plants or goods from high-emission suppliers) and selling products whose use generates emissions. Although this is beginning to change, as we will see shortly, the restriction remains arbitrary. As we have already seen, other indirect impacts – such as buying or selling entire operations – can be just as relevant. In certain contexts, and for specific purposes, these impacts should be considered as well, at least for some time after the event, as we discuss later.

To illustrate this point further, we can draw a comparison with legal theory. In law, proximate causation typically limits liability to harms directly linked to a defendant's actions. For example, if a driver runs a red light and causes a collision, the injury is a direct result of that action, making the driver legally responsible. Applied to brown spinning, this reasoning implies that companies are not causally responsible for emissions from offloaded assets, since those emissions are no longer a direct result of their actions. However, the law also recognizes complicity: one can be liable for harm even without directly causing it. If you aid or abet another's wrongdoing, you are complicit in their actions (Moore, 2009). The problem is that current attributional approaches lack a corresponding mechanism for attributing many important indirect emissions to the appropriate agents. This suggests that attributional metrics should evolve to better reflect forms of indirect impact – beyond the narrow scope of proximate causation.

There are several ways to refine attributional metrics to address problems like brown-spinning. These include retroactively adjusting historical emissions data when assets are bought or sold, expanding the carbon footprint to include more indirect emissions, or conducting case-by-case assessments of a company's climate-friendliness.

First, one approach is to retroactively adjust a company's historical emissions data – removing emissions from sold assets and adding those from acquired ones. This practice is permitted and encouraged by the Greenhouse Gas Protocol (2004), 15 the EU CSRD and the European Sustainability Reporting Standards. It helps counteract brown-spinning by preventing companies from appearing to reduce emissions simply by selling high-emitting assets. It also addresses emissions-reduction acquisitions: companies that buy polluting assets and reduce their emissions will appear climate-friendly, since the previous year's emissions from those assets are included in the data. While this metric does not account for indirect effects beyond Scope 3, it compensates by retroactively adjusting emissions data, thereby mitigating some of the most problematic consequences of attributional metrics.

Second, another approach is to include indirect emissions from sold assets in the company's emissions data. This prevents offloaded carbon-intensive assets from disappearing from the record, so divestment only appears climate-beneficial if the buyer subsequently reduces emissions. However, including these emissions indefinitely is problematic: the new owner may operate the assets longer or invest more in them than the seller intended. If assets are repeatedly transferred, emissions might be counted multiple times, distorting the data. A practical solution is a successive write-off – e.g. phasing out emissions over five years – which balances the extremes of excluding or indefinitely including sold assets. This would reduce incentives for climate-conscious companies to offload polluting assets. Instead, it would encourage improvements like efficiency upgrades or carbon capture.

To avoid the counterintuitive implications of emission reduction acquisitions in ESG ratings, the successive write-off approach should be paired with another: just as emissions from sold assets can be gradually written off, emissions from acquired brown assets could be gradually phased in rather than added all at once. The exact implementation is open to debate, but immediate inclusion penalizes climate-conscious buyers aiming to reduce emissions, while excluding them entirely allows companies to acquire and operate polluting assets without accountability. A balanced approach – gradually adding emissions – would give climate-conscious buyers time to improve asset efficiency or install carbon capture before the emissions affect their ESG ratings. Brown buyers, by contrast, would face unchanged incentives, making the approach more favourable to those seeking to reduce emissions. Still, for this approach to be broadly useful and comparable across contexts, standardized methods for attributing these indirect emissions will need to be developed.

The ideal climate outcome is for brown assets to be retired, not transferred. Still, the two refinements to attributional metrics we propose may not discourage the continued use of polluting assets. Our aim, however, is not primarily to design a metric that incentivizes climate action, but to improve the accuracy of attributional metrics when asset transfers do occur – and we believe the suggestions achieve that. Moreover, in practice, many brown assets are likely to remain in operation regardless of ownership. In such cases, incentivizing climate-conscious buyers to acquire and improve them may be preferable to leaving them in the hands of less climate-conscious actors.

These two elaborations of the attributional metric address the counterintuitive implications that arise when assets are bought or sold. However, they do not account for other indirect effects – most notably, substitution effects, should such effects be included at all (recall our earlier hesitation on this point). If they are to be captured, revising attributional metrics to capture substitution effects would require including more indirect emissions. For example, if one company reduces emissions by selling fewer fossil fuel products, enabling others to sell more, its direct emissions decline while its indirect emissions rise. Attributing such effects is challenging, as it requires determining which emissions the company caused – necessitating a complex consequential analysis. This analysis involves calculating complex counterfactuals and focuses on the impact of specific actions rather than the emissions profile of a company over time. Since incorporating substitution effects into attributional metrics may be infeasible, corroborating any claimed footprint reductions with a consequential measure, as Brander (2022) suggests, may be the most practical solution. 16

In the end, we leave open the question of how to best revise the attributional approach to account for indirect effects in cases of brown spinning and emission reduction acquisitions and to make it sensitive to substitution effects. What we propose here are just a couple of steps in the right direction – improvements over attributional approaches that ignore such effects and ones that avoid the problems faced by consequential metrics. 17

A standard consequential approach

Turning to consequential approaches, the standard difference-making metric sometimes used in product life cycle assessments could be applied to evaluate the climate impact of companies or nations. It can similarly be used by policy-makers and others to assess the expected climate impact of carbon pricing policies or other climate measures, even though it might be misleading to call this a metric, since it does not involve a standardized, repeatable measurement.

This approach is particularly useful for evaluating policies such as carbon taxes, cap-and-trade schemes, or mandatory ESG reporting. It is well-suited for use by states, international bodies like the EU and third parties such as journalists, think tanks and scientists. By focusing on the climate impacts of a single decision, policy, or scheme, it is often feasible to estimate the relevant counterfactuals that the approach requires. Moreover, such evaluations typically have a natural baseline – what would have happened if the policy or scheme were not implemented – which helps avoid the baseline problem.

The standard consequential metric could be used by companies that prioritize making a tangible difference to the climate over optimizing their ESG ratings. For this purpose, however, the relevant baseline is less clear. One option might be global emissions under a business-as-usual scenario. Another would be to compare the company's projected future emissions per unit of production to those of similar companies under comparable scenarios. A third option would be to use a historical baseline, such as emissions levels before the implementation of a policy.

Importantly, while consequential metrics and approaches focus on estimating emissions outcomes, a broader consequentialist analysis – understood as a decision procedure – evaluates actions or policies based on a wider range of considerations. These include not only climate impact but also practicality, political achievability, fairness and wider societal consequences. 18 For example, implementing a carbon tax – including a tax on petrol – might be estimated to have a larger positive impact on global emissions than a cap-and-trade system. So, a consequential metric would say the carbon tax has a higher positive climate impact. Still, such a tax might be difficult to implement for political reasons. The fossil fuel industry might lobby against it, and people dependent on their cars might protest it. In addition, such a tax might be unfair to people living in the countryside since they will be hit harder by the tax than people living in cities. 19 Such additional considerations are part of a consequentialist analysis, which uses the climate impact estimated by a metric as one input among others in a broader decision-making process.

While the evaluation of a scheme's climate impacts might be consequential in nature, the measurement approach adopted within the scheme itself will often be attributional, targeting corporate or individual emissions. In such cases, a consequentialist decision procedure – which weighs climate impact alongside other considerations – might recommend implementing an attributional metric with limited scope, such as a carbon tax on direct (Scope 1) emissions, a cap-and-trade scheme, or an indirect carbon tax via a fuel tax. This reflects a form of higher-level consequentialism, which evaluates the systemic effects of adopting particular rules or metrics, even if those rules are not themselves consequential in structure. In other words, a consequentialist rationale may support the use of attributional metrics when they are more feasible, transparent, or effective in practice.

One practical example of higher-level consequentialism is found in target-based initiatives, such as the Science-Based Targets initiative. These schemes use consequentialist reasoning to determine appropriate emissions reduction trajectories – often sector-specific and aligned with global climate goals – but rely on attributional metrics to monitor progress.

It might seem paradoxical that a consequentialist framework could lead us to adopt an attributional metric. However, it is not unusual for consequentialist reasoning to recommend non-consequentialist rules. As Parfit (1984) notes, consequentialism can be self-effacing if it is used as a decision procedure, meaning it might suggest abandoning consequentialist reasoning if following it leads to worse outcomes. For other instances, Mill (1861) advocates legal rights on utilitarian grounds, we might argue for a penal system where only the guilty are punished on similar grounds, and Jamieson (2007) contends that utilitarians might better serve their objectives by embracing virtue ethics in the context of climate change. Our idea is similar: for some purposes, a consequentialist reasoning might lead us to adopt an attributional metric.

Next, to ensure effective climate action, the legal system must uphold the laws that have been implemented, whether they are based on a limited attributional metric, an extended attributional metric, or a consequential metric. Clear legislation is crucial; if laws are ambiguous and do not specify how emissions should be measured, the power of the courts may become too large, and their guidelines may be unclear.

This ties back to the example of Milieudefensie v. Shell. The Hague District Court ordered Shell to reduce its CO₂ emissions by 45% by 2030, but the Dutch Court of Appeal overturned this ruling, arguing that a specific reduction target for Shell was not justified. The court's reasoning highlighted that an increase in Shell's emissions could, in some scenarios, result in a net decrease in global emissions – for example, if Shell supplies gas to a company previously reliant on coal. This shift from assessing Shell's carbon footprint to evaluating its impact on global emissions reflects a transition from attributional to consequential metrics. 20 The case illustrates the importance of having a clearly defined and agreed-upon framework for measuring contributions to climate change suitable for legal purposes. Without such agreement – whether in legislation, regulation or policy – conflicting interpretations of what counts as ‘impact’ can be used selectively, leading to inconsistent or contested outcomes.

An elaborated consequential metric

Finally, an elaborated consequential metric, building on more accurate accounts of causation, might be our best choice if our purpose is to sort out the actual consequences of a company's actions. This approach would involve detailed modelling of the causal pathways and interactions that lead to changes in global emissions. By incorporating more sophisticated methods, such as structural equation modelling or agent-based simulations, we can better understand the complex dynamics and indirect effects of corporate decisions.

For instance, in the case of a fossil fuel company considering investing more in renewable energy, an elaborated consequential metric would not only consider the direct emissions from its operations but also the broader impacts of its decisions on global energy markets, technological advancements and policy changes. This could include an evaluation of how the company's investment in renewable energy might influence other companies to follow suit, or how its continued fossil fuel production might affect global emissions through market shifts and regulatory responses. While challenging, an elaborated consequential metric offers the potential for more precise and actionable insights into the climate impacts of corporate behaviour.

Conclusion

Measuring corporate contributions to climate change is a complex task that requires careful consideration of the context and purpose of the evaluation. This paper has examined the merits and limitations of both attributional and consequential approaches to emissions accounting. Attributional approaches, while practical and widely used, often fail to capture key indirect contributions to climate change, such as brown spinning and substitution effects. While many of the problems we identify with attributional metrics stem from their misinterpretation as measures of climate impact rather than merely as descriptions of companies’ emissions profiles, this misinterpretation is widespread in both academic and policy contexts. As such, these problems are not merely theoretical but have practical implications for how emissions data is used in decision-making. Consequential approaches offer a more comprehensive assessment of the impact of corporate actions on global emissions but require infeasible levels of predictive precision and counterfactual analysis.

Given these challenges, we propose that different contexts and purposes warrant different metrics. For carbon taxation or cap-and-trade schemes, a restricted attributional metric measuring only Scope 1 emissions is practical and aligns with the goal of incentivizing low emissions within a defined boundary, such as a country or region. However, for purposes like setting ESG ratings or evaluating a company's overall climate impact, an extended attributional framework that incorporates indirect effects beyond Scopes 1, 2 and 3 emissions is necessary. This expanded approach at least partly addresses issues like brown spinning and emission reduction acquisition, providing a more accurate representation of a company's contribution to climate change.

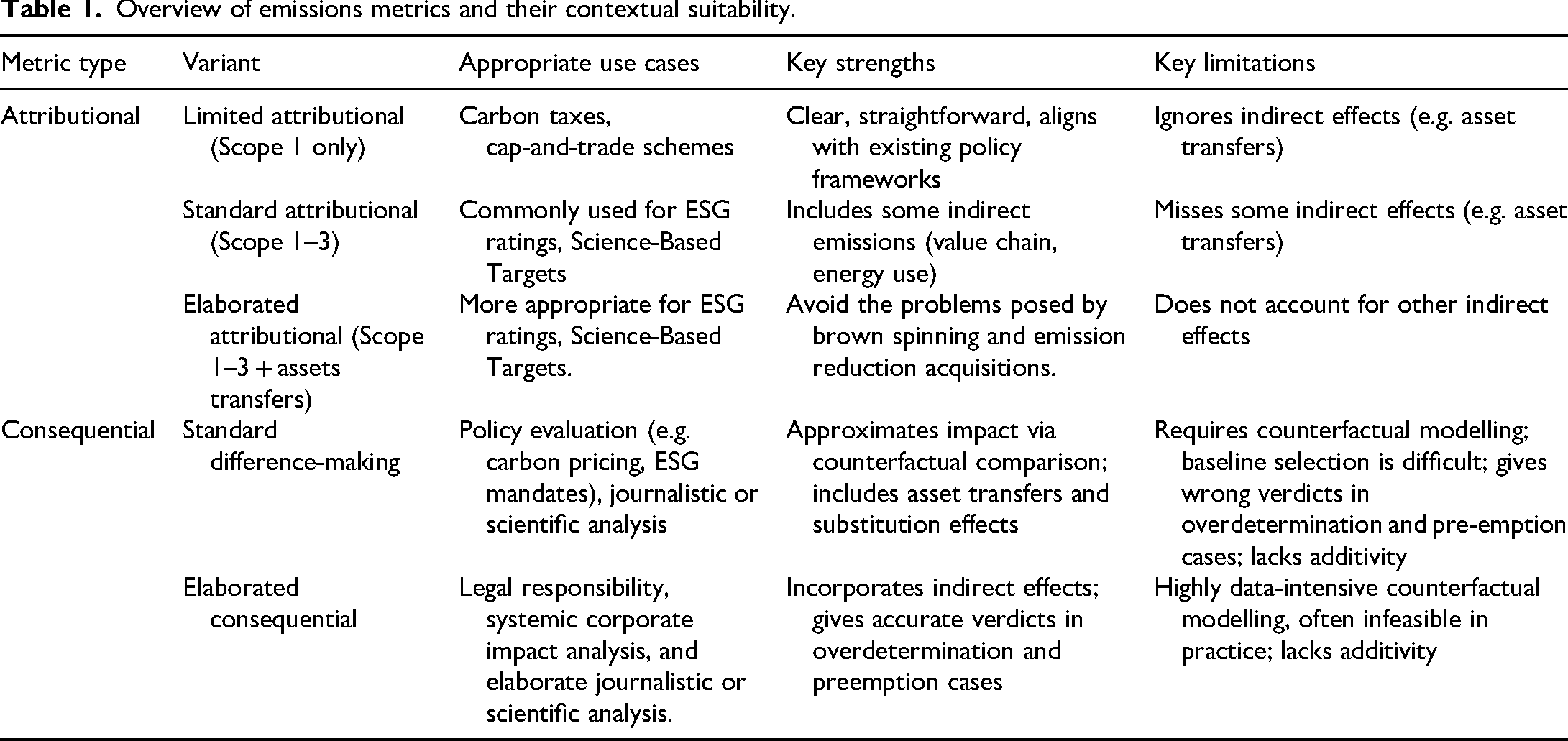

Overview of emissions metrics and their contextual suitability.

In some cases, a standard consequential metric may be appropriate, particularly when evaluating decisions, acts and policies. This metric can provide valuable insights into the broader climate impact of different carbon pricing policies on global emissions. It is important to recognize that consequentialist reasoning that builds on consequential measurements of impacts (and other considerations) might recommend implementing non-consequentialist rules, such as an attributional metric, if it leads to better outcomes. Moreover, in cases where emissions are overdetermined or where backups guarantee the emission of GHGs, the standard consequential metric will yield inaccurate verdicts of climate impact. In such instances, more accurate consequential metrics, informed by more precise accounts of causation, must be used. The results are summarized in Table 1.

Future research could explore the potential of hybrid approaches that combine attributional and consequential metrics. It remains an open question whether such hybrids can offer more accurate or context-sensitive assessments of the climate impact of companies, or whether they simply inherit the limitations of both frameworks.

Another important avenue for future research is to examine whether investments in companies or funds with high ESG ratings actually lead to improved environmental outcomes. This question ties into a broader issue we intend to explore: what kind of information should guide investment decisions? In this paper, we have not only assumed that ESG ratings, Science Based Targets and similar evaluations are relevant for corporate strategy – we have also treated them as relevant for investment decisions. But how justified is this assumption? As noted (see footnote 15), it is far from clear to what extent investor transactions influence corporate behaviour or emissions. This casts doubt on the practical significance of ESG ratings for real-world climate impact. The same concern applies to any performance-based metric, including consequential ones, since the climate impact of a portfolio cannot be reduced to the performance of its constituent companies. Ethically motivated investors may not only aim to avoid complicity or reward good behaviour – they may also consider the potential for constructive engagement with companies. We believe there is a strong need to investigate how, and to what extent, investment decisions should be based on company performance metrics versus other considerations.

We have set aside in this paper the question of how causal and moral responsibility relate in emissions accounting. Sometimes, companies clearly cause emissions that are not attributed to them – perhaps because the emissions were unforeseeable or unavoidable. This may reflect a normative judgment that companies are not always morally responsible for all emissions they causally contribute to. In typical cases, however, we assume moral responsibility aligns with causal responsibility, especially when companies knew or should have known about the consequences of their actions. Clarifying when this alignment holds is an important task for future research.

Ultimately, the choice of emissions allocation criterion should align with the specific goals we aim to achieve, whether it is to incentivize corporate responsibility, provide guidelines for investors, reduce global emissions, or hold companies legally accountable. By adopting a flexible and context-sensitive approach to emissions accounting, we can better address the challenges of measuring corporate contributions to climate change and promote more effective climate action.

Footnotes

Acknowledgements

We wish to thank the audiences at the Financial Ethics Seminar and the Higher Seminar of Practical Philosophy, both at the University of Gothenburg, and at the 2025 Annual Meeting of the Society for Business Ethics in Copenhagen. In particular, we want to thank Alexander Andersson, Olle Blomberg, Boudewijn de Bruin, Richard Endörfer, John Eriksson, Ragnar Francén, Erik Malmqvist, Pia Nykänen, Simon Rosenqvist and Joakim Sandberg. We also want to thank Lina Eriksson, Fredrik Hedenius and Martin Persson for their valuable comments on an earlier version of the paper at an informal seminar and Caroline Torpe Touborg and two anonymous reviewers for their close reading and valuable comments on earlier versions of the paper.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors gratefully acknowledge the financial support provided to the Financial Ethics Research Group at the University of Gothenburg, from Vinnova (Sweden’s innovation agency) for the Sustainable Finance Lab (2020-04660) and the project Science-Based Metrics for Sustainable Finance (2023-03456), and from Mistra (the Swedish Foundation for Strategic Environmental Research) for the Finance to Revive Biodiversity program (Mistra FinBio, 2020/10).

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.