Abstract

Current understandings of emotional value focus on integral affects that are directly related to present judgements and choices. This neglects recent research on the complexity of affect and dismisses affects triggered by situations, events, or persons encountered in daily life outside of the decision-making situation or process; that is, incidental affects. In this article, we analyse the interplay between customers’ incidental and integral affects in value experience during life transitions. Based on the qualitative data collected on real-estate services, we unveil the internal dynamics of affective value by showing the intrapersonal and interpersonal forms of interplay (spillover, ambivalence, divergence and convergence) between integral and incidental affects. This advances knowledge on the composition and dynamics of the concept of affective value and on the affective value experience in life transitions.

Introduction

Increasing customer value has generally been acknowledged to be the goal of firms (Woodruff, 1997). Currently, value is frequently considered in terms of well-being (e.g. Anker et al., 2015; Kelleher et al., 2020), and due to the experiential nature of services, the interactive and potentially emotion-laden roles of customers can influence the customers’ emotional and physical well-being (Anderson et al., 2013). This means that to create value for customers or co-create value with customers (cf. Tumbat, 2011), service providers need to generate positive well-being outcomes through their services.

The value discussion has spotlighted customers’ affects (Shaw, 2007), in line with the acknowledgement that affects (i.e. valenced feeling states, such as emotions and moods) influence customers’ evaluative processes, satisfaction and loyalty (Cohen and Areni, 1991; Cohen et al., 2008; Rychalski and Hudson, 2017). The affect-related nature of value formation is particularly highlighted in the contemporary literature concerning customer experience – consisting of emotional and social elements – and the subconscious level, in addition to cognitive and rational thinking, during the entire customer journey (Kranzbühler et al., 2020; Lemon and Verhoef, 2016).

Existing studies on affective value have focused on the affects aroused by the goods and services offered to consumers (e.g. Ayi Ayi Wong et al., 2020; Kranzbühler et al., 2020; Tumbat, 2011). These so-called integral affects are triggered by the consumer’s decision consideration or the judgemental target itself (Loewenstein and Lerner, 2003). However, the discussion neglects the vast majority of affects felt by individuals, including affects triggered by situations, events or persons encountered in daily life or by personality traits. They do not result from the consideration of the decision at hand and are therefore called incidental affects (Cohen et al., 2008; Loewenstein and Lerner, 2003). However, these affects are prevalent in customer interactions and thus influence customer behaviour (Kim et al., 2010). Sense making of value in customer experience is affected by the individual–social, past–future and imaginary–lived dimensions (Helkkula et al., 2012). This suggests the strong presence of incidental elements in determining experiential value formation. Incidental affects arguably relate to wider, overall consumer journeys (e.g. Hamilton and Price, 2019) that have an abstract, higher-level goal in a consumer’s life, and that may include several customer journeys with multiple service providers. For instance, pursuing well-being for one’s family by searching for a suitable new home exemplifies this. Hence, we argue that incidental affects should be considered in studies on customers’ value experience.

Even though it is acknowledged that incidental and integral affects may jointly influence consumer behaviour (Achar et al., 2016; Västfjäll et al., 2016), the current theorising on affective value does not elucidate how incidental and integral affects are inter-related in the value experience. This conceptual ambiguity is particularly problematic when the literature on value, as experienced by customers, is expanding rapidly (cf. Prebensen and Rosengren, 2016). Moreover, the recent human experience approach emphasises the central role of service in human life (Fisk et al., 2020), suggesting how the service and the lifeworld of a customer are tightly interwoven. This is why it is essential to gain a profound understanding of the interplay between integral and incidental affects in the formation of customers’ value experience in services. We are interested in how this interplay affects the value-creation process and what its outcomes are to gain insights about customers’ value-formation experiences (cf. Gummerus, 2013).

This interplay can particularly accentuate in life transitions. It is paradoxical that individuals often make the biggest consumption decisions (such as selling or buying a property) when they are passing through transitions in their personal lives (getting married or divorcing) and when both strong integral and incidental affects are present (cf. Gentry et al., 1995). Even though life transitions in consumer behaviour have been studied (see Yap and Kapitan, 2017) and it is suggested that marketers who understand the affective consequences of life transitions are expected to gain a stronger foundation of loyal customers (Mathur et al., 2008), little is yet known about the role of affects in this context.

To address these research gaps, this study aims to theorise on customer experiences of affective value. The specific research question is: How do customers’ incidental and integral affects interplay in value experience during life transitions?

Our study contributes to the existing literature in several ways. First, we expand the concept of affective value by showing that it also includes value influenced by incidental affects. Second, we reveal the internal dynamics of affective value by showing the intrapersonal and interpersonal forms of interplay between integral and incidental affects. Third, we expand the understanding of value experience in life transitions by showing how the incidental affects evoked by life transitions are in interplay with integral affects during consumption.

We approach the phenomenon by first providing a concise overview of the extant research on affects and value experienced by customers and incidental affects triggered by life transitions. In the methodology section, we describe the qualitative data-gathering process and analysis in an affectively intense business context in which customers experience transitions: real-estate services. We then proceed to present the findings, providing detailed analyses, followed by a discussion and conclusion section where we propose a dynamic model showing the interplay between customers’ integral and incidental affects in value experience during life transitions.

Theoretical Background

The concepts of integral and incidental affects

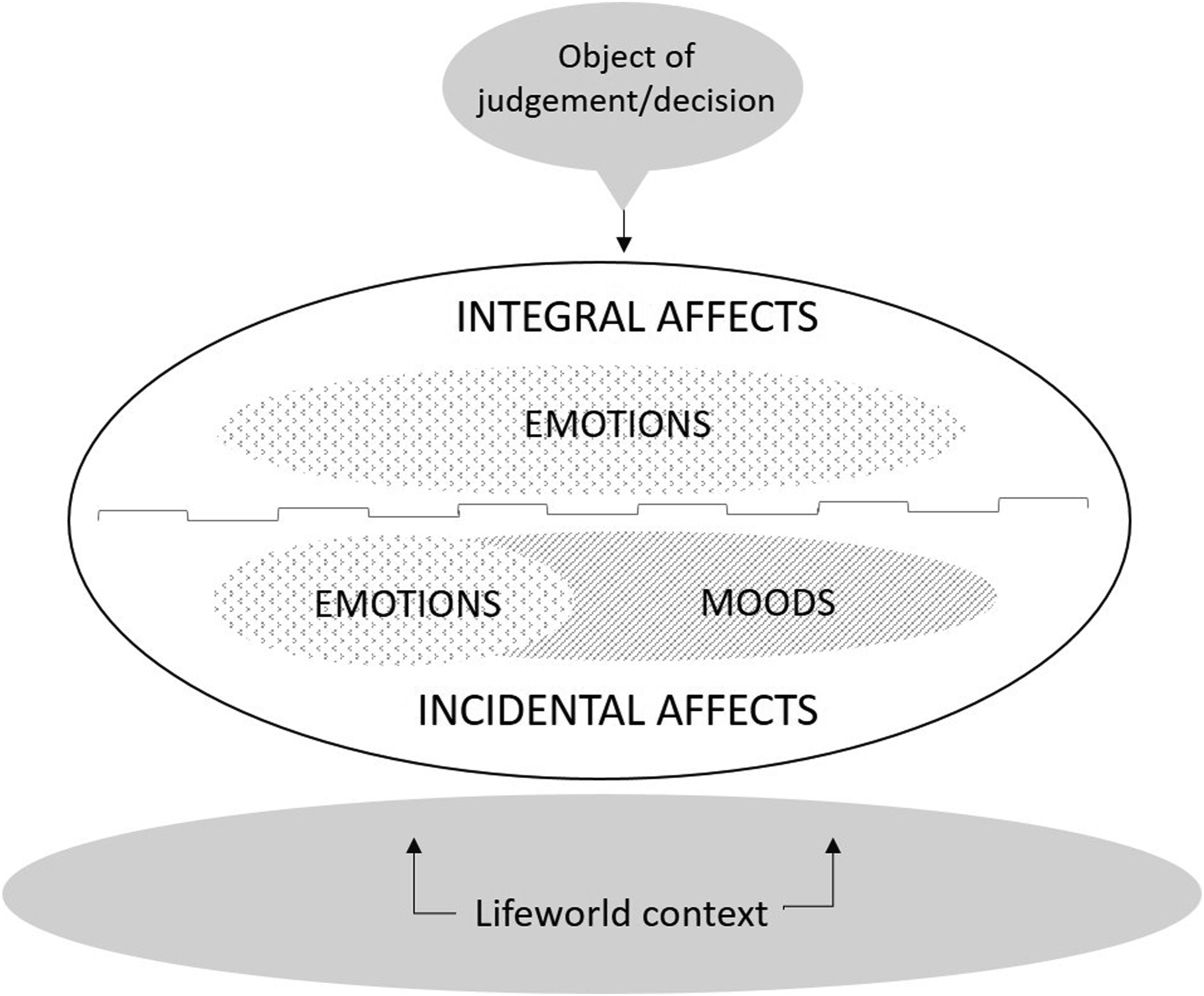

Both emotions and moods can be regarded as affects (Cohen and Areni, 1991). Emotions are short-term feelings triggered by something, and they influence behaviour, whereas moods (i.e. states of mind) are subtler, do not have a definite trigger or definite influence on behaviour, and tend to last longer (e.g. Frijda, 1993; Rank and Frese 2008).

Emotions and moods have been analysed through the division of basic affects segregated into several categories (see Laros and Steenkamp, 2005) that tend to follow a division between positive (pleasant) affects and negative (unpleasant) affects. In consumer behaviour research, these are often divided into eight basic categories, of which four are positive (contentment, happiness, love and pride) and four are negative (anger, fear, sadness and shame) (e.g. Laros and Steenkamp, 2005). Experienced positive and negative affects influence consumer behaviour, with positive affects being linked to positive purchase outcomes (such as positive word-of-mouth communication) and negative affects being connected to negative purchase outcomes (such as purchase avoidance) (Namkung and Jang, 2010). However, the causality is not always straightforward: Positive affects do not automatically lead to positive outcomes, and negative affects may not necessarily generate negative outcomes. Furthermore, recent research has shown that customers often experience ambivalent affects and feel positive and negative affects simultaneously or in a rapid vacillation (Manthiou et al., 2020; Vaccaro et al., 2020).

When affects are contemplated in relation to customer experiences, they can be divided into integral and incidental affects. Integral affects refer to the affective responses that are directly related to the object of judgement or decision (Bodenhausen, 1993; Ferrer and Ellis, 2021). Since they have a certain trigger and are momentary, they can be considered emotions (Figure 1). They may be experienced through direct exposure to the object (such as meeting a real-estate agent) or through exposure to a representation of the object (such as thinking of a real-estate agent or seeing his/her advertisement). Integral affects are triggered by features of the object, regardless of whether these features are existent, perceived, or imagined (Cohen et al., 2008). Integral and incidental affects consisting of emotions and moods.

Incidental affects are affective experiences that are also experienced at the moment of judgement or decision, but they arise from dispositional sources unconnected to the object of judgement or decision (Bodenhausen, 1993; Ferrer and Ellis, 2021). They can usually be regarded as moods since moods arise from several – often unidentified – sources. Incidental affects may also arise from an individual’s emotional disposition (such as chronic anxiety) and temperament (such as general optimism or pessimism) or from other contextual stimuli (such as the weather) (Cohen et al., 2008).

Incidental affects are ‘not related to the stimuli that are the focus of the cognitive task’ (Blanchette and Richards, 2010: 562), but research has shown that they nevertheless influence decision-making: Discrete incidental affects activate ‘relatively automatic processes that guide subsequent perception and judgement’ (Lerner and Keltner, 2000: 489). For instance, positive incidental affects tend to decrease systematic information processing, whereas negative incidental affects seem to lead to more systematic and careful information processing (see Blanchette and Richards, 2010). Economic decisions may also be influenced by incidental affects (Slovic et al., 2002), and prices in economic transactions may be influenced by affects evoked by prior irrelevant triggers (Lerner et al., 2004).

Existing research on the role of affects in value experienced by customers

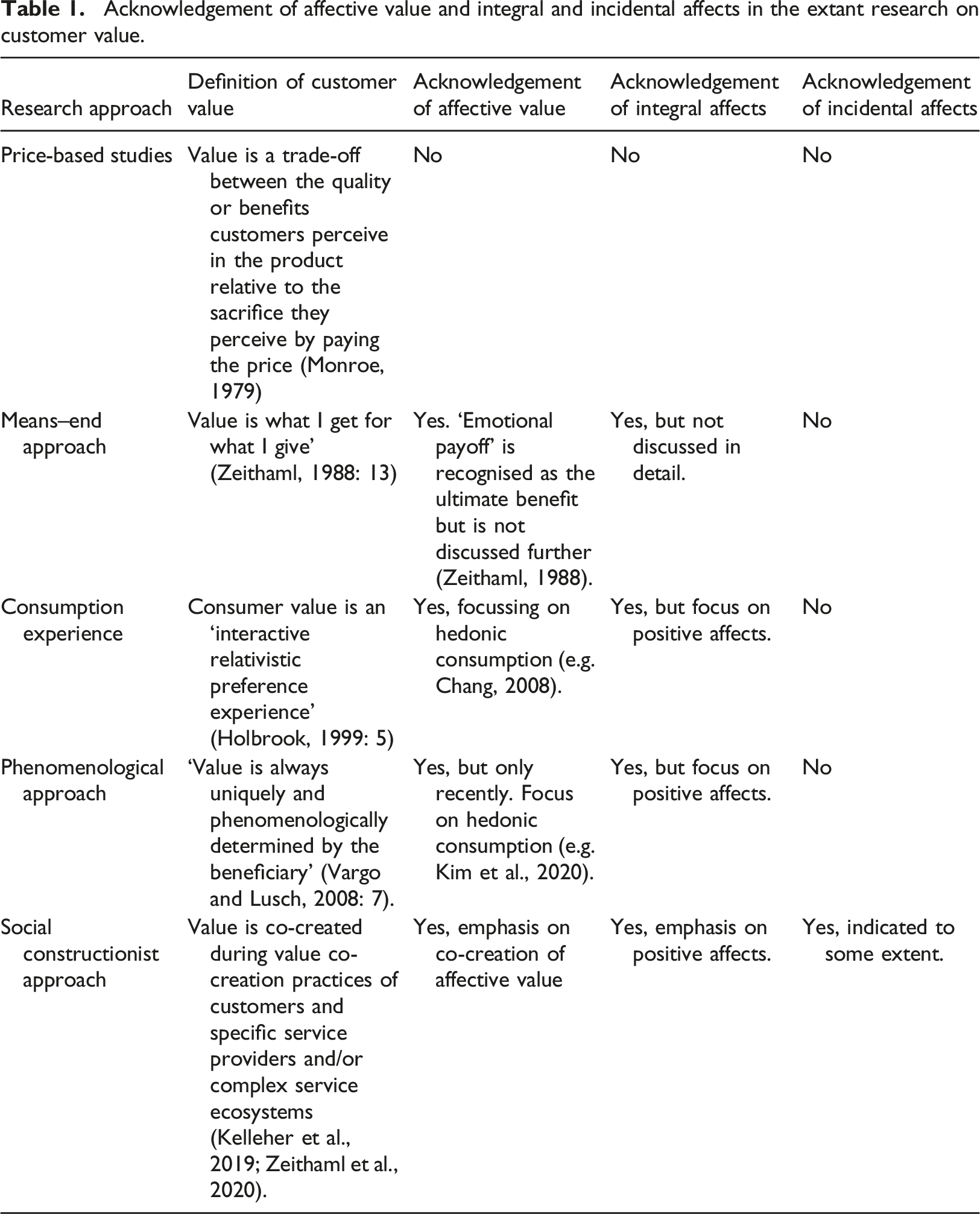

Acknowledgement of affective value and integral and incidental affects in the extant research on customer value.

Traditionally, the conceptualisation of value was dominated by price-based studies. Relying only on the economic perspective, value was seen as a trade-off between costs/sacrifices and the price/quality of a product (Monroe, 1979) and did not consider affective value. Zeithaml (1988) developed the value conceptualisation further, suggesting that perceived sacrifice and quality are more important when estimating a product’s value. By using a means–end approach, she shows how consumers’ perceptions of ‘what is received and what is given’ (Zeithaml, 1988: 14) determine the product’s quality. Affective value is not directly discussed, but an ‘emotional pay-off’ (Young and Feigin, 1975:74) is presented as the highest benefit level in the chain of benefits consumers derive from a specific product (Zeithaml, 1988). Thus, it can be considered to be related to positive integral affects, even though they have not been explicitly stated.

The third stream of studies saw value as formed through consumption experience (Carù and Cova, 2003), where the concept of value became multidimensional. For example, Sweeney and Soutar (2001) divided value into functional, social and emotional dimensions. Emotional value was acquired from the offering’s capacity to arouse affect (Sheth et al., 1991; Sweeney and Soutar, 2001). It is notable that the studies on consumption experience and affective value tend to concentrate largely on hedonic consumption and luxury products (e.g. Holbrook, 2006) or on the hospitality industry (e.g. Prebensen and Rosengren, 2016), emphasising affects related to the products/services consumed and thus focussing on positive integral affects, such as pleasure, fun, enjoyment (e.g. Holbrook, 2006), excitement (e.g. Prebensen and Rosengren, 2016) and happiness (e.g. Prebensen and Rosengren, 2016), with a few exceptions (cf. Kranzbühler et al., 2020).

The fourth stream, the phenomenological approach, sees value as experiential but additionally emphasises that it is idiosyncratic and contextual. Each customer experiences and determines value in a unique way (Vargo and Lusch, 2008) or as value-in-use (Grönroos, 2011), which emerges via behavioural and mental processes as the customer interprets, experiences, or reconstructs reality in which value is embedded (Heinonen et al., 2013). Affective value is increasingly discussed, but only in relation to voluntary consumption, largely focussing on positive integral affects (e.g. Kim et al., 2020).

However, Malone et al. (2018) consider affects as part of customer value and, although they did not explicitly distinguish between integral and incidental affects, the findings show the existence of both. Furthermore, the suggestion that customer experience should be understood in the context of the customer’s ongoing life (Heinonen et al., 2010) indicates the increasing interest in incidental affects. Heinonen et al. (2013: 14) state that ‘if customers live a hectic and stressful time of life the requirements for the service process are different than for another customer who has too much time’, and mention the ‘emotional foundation of the customer’, referring to emotions related to customers’ everyday lives. These can be interpreted as incidental affects.

The fifth stream employing the social constructionist approach emphasises value co-creation in interaction between the customer and other economic and social actors (Zeithaml et al., 2020). These studies recognise affective value, but tend to see it as emerging in the service process, thus largely focussing on integral positive affects (Kelleher et al., 2019; Tumbat, 2011). However, some studies also indicate the existence of incidental affects. For example, Plewa et al. (2015) discussed a customer being anxious about his or her financial situation, thus implicitly referring to incidental negative affects.

In conclusion, the existing research on customer value, to a certain degree, recognises the importance of affects, but only recently has there been increasing interest in the role of incidental affects in customers’ value experience. Furthermore, the focus has largely been on positive affects, with studies on negative affects being scarce.

Consumers’ incidental affects triggered by life transitions

Transitions are periods of change for an individual (or group) from one social state to another (Tonner, 2016). Life transitions can be defined as events that dramatically and profoundly change one’s daily routines, priorities and/or coping strategies, and consequently they influence consumer behaviour (Yap and Kapitan, 2017). Depending on the individuals and their circumstances, the same transition may be experienced as extremely positive or deeply negative (Hopkins et al., 2014), or even as both at the same time (Tonner, 2016).

Reviewing prior studies, Yap and Kapitan (2017) identified seven major life transitions that also reflect on consumption: the passage from childhood into adulthood, job-related changes (such as changes in employment status and career changes), changes in relationships (such as marriage, divorce and loss of loved ones), transition to parenthood, ageing (such as retirement, widowhood, downsizing and facing death), relocation and general life events (such as major role transitions or lifestyle changes). The list can be further complemented with personal injury or illness (cf. Holmes and Rahe, 1967). It is also likely that an individual may experience more than one life transition at a time, which makes their influence on consumption even more complicated (Hopkins et al., 2014).

Extant studies have shown that intensive affects that an individual experiences in his/her personal life cannot be switched off when decisions are made, even if these affects are incidental to such decisions. Life transitions evoke intensive incidental affects alongside the integral affects on consumer behaviour. Affects are particularly intensive in the liminal stage, which is the mid-transition phase – ‘a threshold, which once passed over irrevocably changes the individual’ (Tonner, 2016: 101). This can be characterised by high uncertainty; consumers face a new situation and do not necessarily know how to consume in it, resulting in affective ambiguity and consumption uncertainty (VOICE Group, 2010). However, the discussion on how incidental and integral affects interplay in customer value experiences in life transitions is limited.

Methodology

To incorporate incidental affects into the value-experience concept, we chose to analyse affective value comprising both integral and incidental affects. We analysed them in a life-transition context where an array of distinct positive and negative integral and incidental customer affects are likely to be present: selling or buying a home. Home is a subjectively experienced, complex and multidimensional concept that usually represents something positive (Parsell, 2012). It fosters ‘a sense of belonging, “rootedness,” continuity, stability and permanence’ and satisfies people’s affective, social and psychological needs by giving them a physical framework for self-expression and family life (Fox O’Mahony, 2013: 162). As many life transitions of consumers relate to home, either through a need to sell or buy one, this context serves the research purpose well.

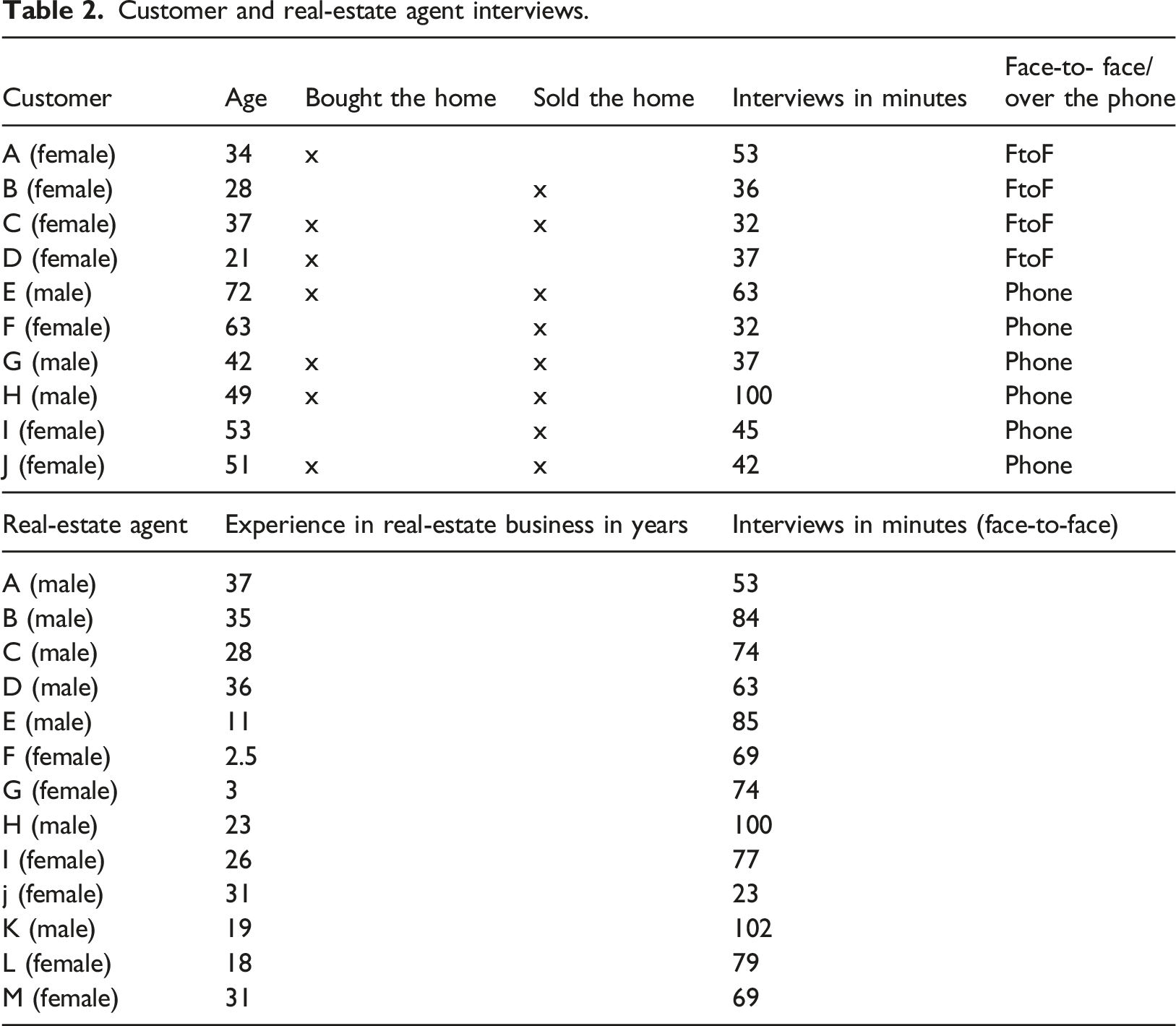

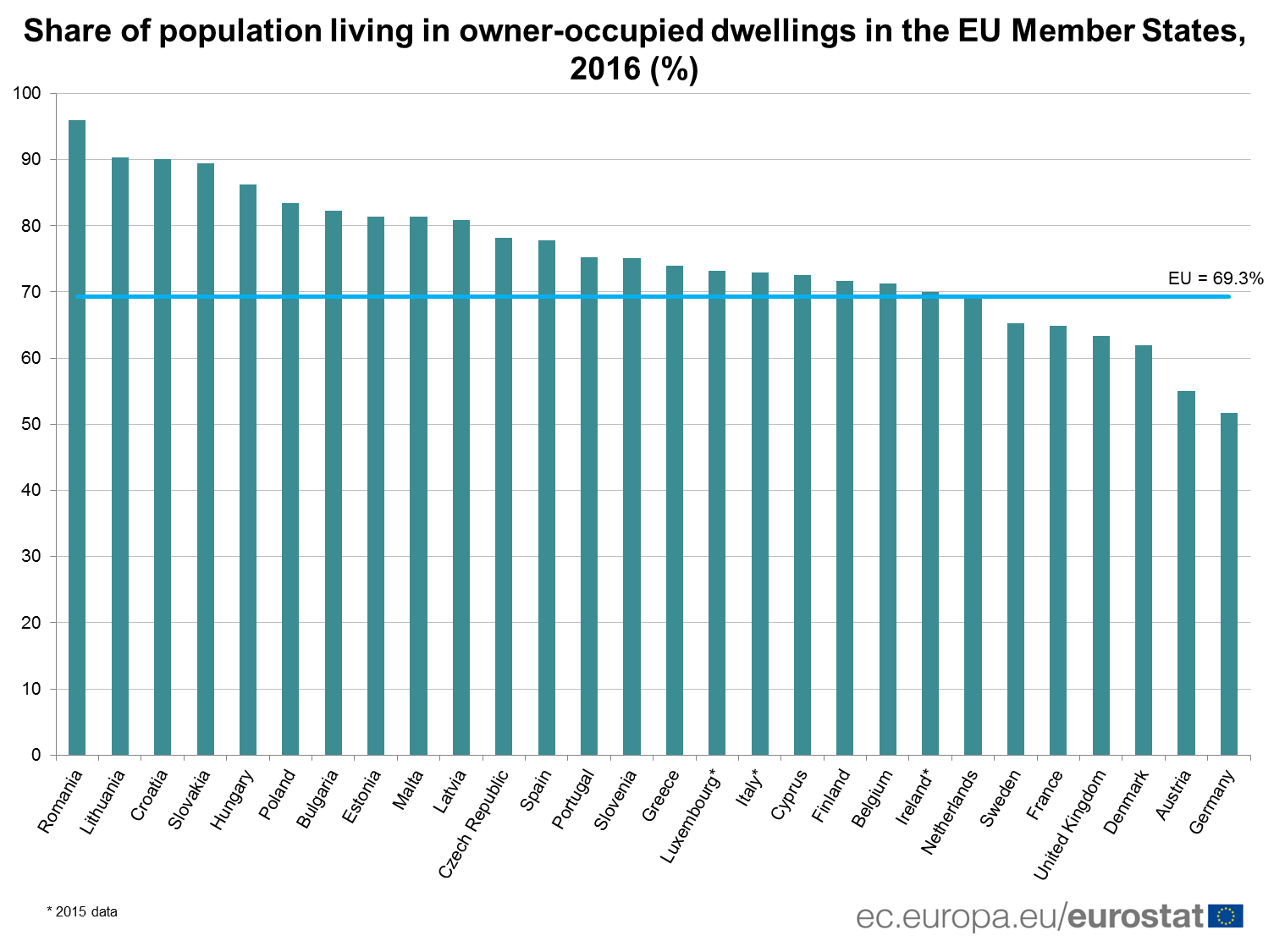

Our exploratory research approach guided us towards a qualitative approach that is well-suited to research on personal experiences and affects (Strauss and Corbin, 1990). We collected data in Finland, where over 70% of the population are homeowners (Eurostat, 2020), making it an excellent research ground. Although cultural context may produce constructs that enable and guide individual agency and behaviour in life-transition situations with individual constraints (a context within a context; see Askegaard and Linnet, 2011), experience of affects is more or less independent from cultural context (Ortony and Turner, 1990). To obtain a comprehensive view of affects in a real-estate context, we chose both private customers (i.e. households) and real-estate agents as informants. Thus, we had two different datasets. Unlike a typical business, in a real-estate business, customers may be either home buyers or sellers; in some instances, a customer can assume both roles in the interactions with a single agent.

First, we conducted thematic interviews with 10 private customers that also served as our primary data. This was followed by interviews with 13 real-estate agents to complement the primary data. Customer informants provided rich information on their recent personal experiences, but it was seen as necessary to also include real-estate agents, since buying or selling a home is a unique occasion for most individuals and accomplished real-estate agents have seen hundreds of ‘unique experiences’. Thus, they enabled us to find patterns in affective value and to validate information gained from the customers. The number of interviews in both categories was considered sufficient when the last two interviews did not yield any new information that could add to our understanding of the concept (cf. Bowen, 2008).

Customer and real-estate agent interviews.

The interviews were conducted in Finnish and they lasted from approximately 0.5–1.5 h, producing eight hours of recorded customer data and 16 h of recorded agent data in total. Studying affects is empirically difficult because they are sensitive issues that individuals recognise and express in various ways. The theme interview method helped us to track down affects (cf. Oplatka, 2018). It provided a basic structure for data collection but also allowed for new issues to emerge. Themes, both for customers and real-estate agents, included positive and negative customer affects, their triggers (to distinguish incidental from integral affects) and the dynamics that exist between affects and decision-making. The agents were particularly asked to itemise, through examples, how they had recognised affects, their triggers and influence.

All the interviews were transcribed. The data analysis proceeded in cycles: Iterations through the data, emerging insights and a theoretical pre-understanding of affective value construction and formation guided our analysis, as follows (cf. Srivastava and Hopwood, 2009). First, we reviewed the data from customer interviews to achieve an initial understanding of customer affects. Our preliminary understanding was then complemented and validated with the analysis of data collected from real-estate agents.

To organise the data, we focused on elements identified above in the theoretical background section (i.e. incidental and integral affects). Our analysis revealed a variety of customer affects generated in the context of real-estate business. When distinguishing between incidental and integral affects, it becomes important to define what the customer’s decision-making actually concerns or what the object of judgement is in the real-estate business (cf. Ferrer and Ellis, 2021). It seems logical to define the ultimate object to be the house that is either sold or bought. However, the decision itself takes time and involves interaction with various actors that can be seen as essential actors in the decision-making process (e.g. agents or other customers/sellers), and thus they can be regarded as triggers of integral affects. In contrast, triggers of incidental affects are those that would exist without the decision-making process (e.g. life situations that led to house buying/selling or the weather).

When analysing affects further, we relied on Laros and Steenkamp’s (2005) classification scheme, which divides them into basic negative affects (anger, fear, sadness and shame) and basic positive affects (contentment, happiness, love and pride). Our analysis of affects – integral and incidental, positive and negative – soon showed various sequel and parallel dynamic interlinks between the concepts that reflected on customers’ behaviour and decision-making. The latter also surfaces customers’ affects for service providers, here real-estate agents. The above enabled the integration of single categories of incidental/integral and positive/negative affects into some more abstract patterns, also illustrating their interplaying relationships, either at the intra- or interpersonal level.

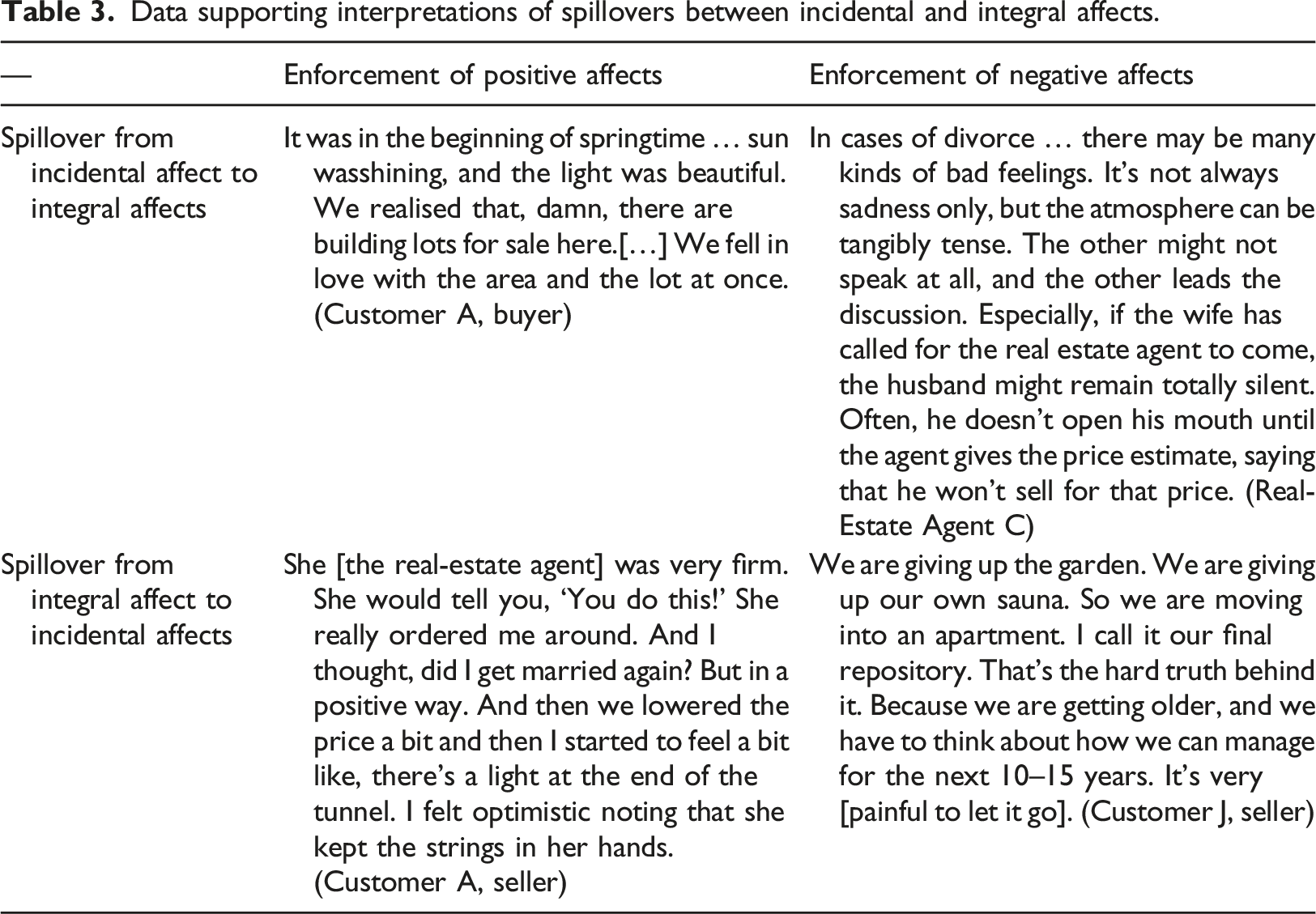

Data supporting interpretations of spillovers between incidental and integral affects.

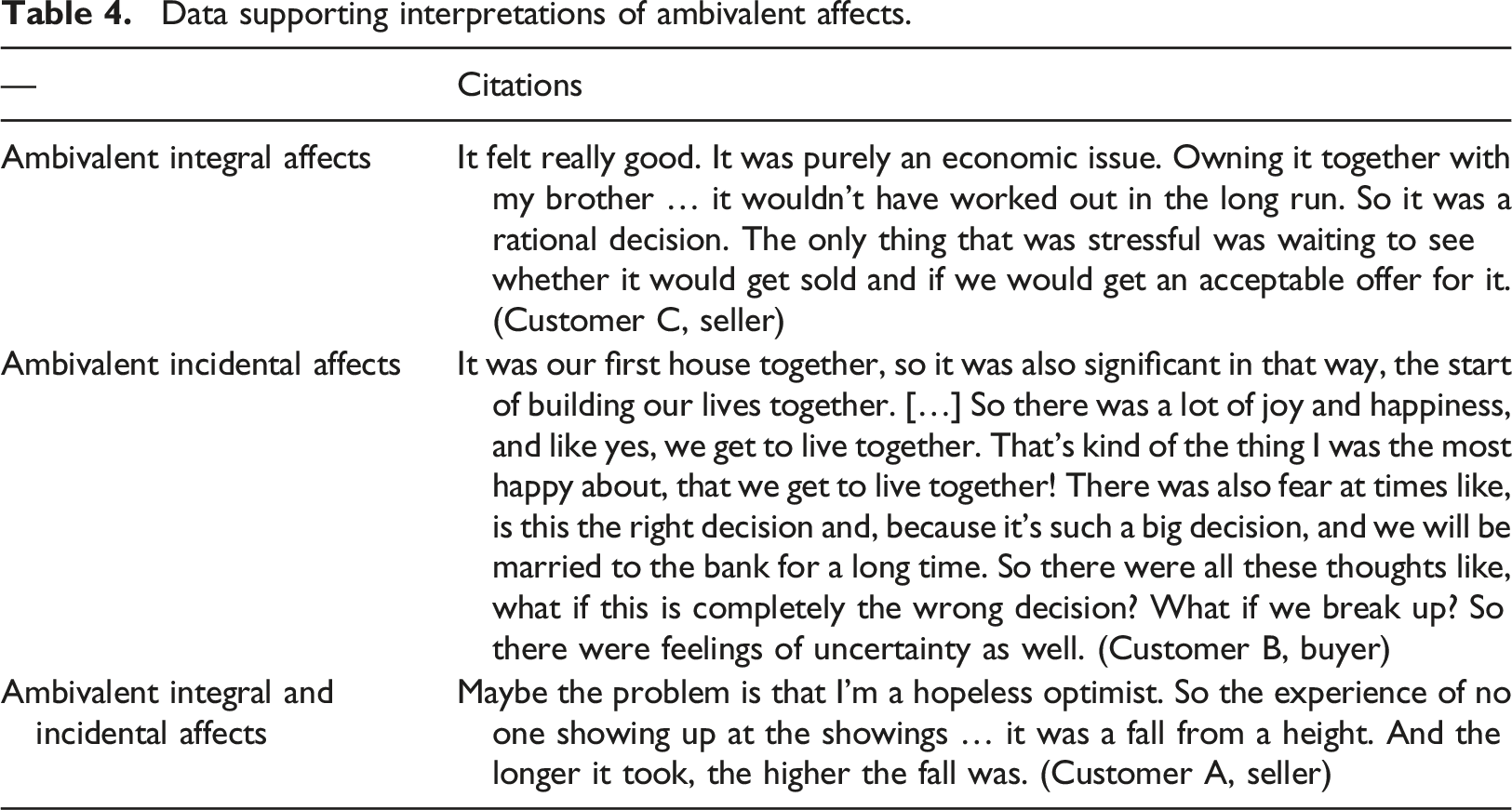

Data supporting interpretations of ambivalent affects.

Data supporting interpretations of convergence and divergence of affects.

Findings

The analysis of integral and incidental positive and negative affects revealed their various interplays. We sorted them into intrapersonal and interpersonal interplay and distinguished between two types of intrapersonal interplay (spillover and ambivalence) and two types of interpersonal interplay (convergence and divergence) of incidental and integral affects. They are presented in the following sections.

Intrapersonal interplay of affects

The interplay of affects felt by the real-estate customer seems to take place via spillover or ambivalence. In cases of spillover, a positive incidental affect enhanced positive integral affects, or vice versa, and a negative incidental affect enhanced negative integral affects, or vice versa (Table 3). Thus, the interplay between incidental and integral affects may generate self-enforcing valence cycles.

Incidental affects seemed to tune individuals to also feel the same kind of affects towards issues related to the decision-making process. This is illustrated by an example of a customer who entered the office to finalise a transaction when he had just heard worrying news concerning his work: We were just going to go sign the papers when the other party had just been told at work that he was going to be made redundant. In this kind of case, when you get negative news from work and you’re just about to buy [a house or apartment], maybe discrepant, even fearful emotions can appear regarding how to cope in the future. (Real-Estate Agent B)

This kind of situation where incidental affects enforce either the positive or negative affective customer experience may also take place in case of positive affects, for example, when sunny weather made the prospective buyers cheerful, and they made an offer instantly without considering whether they wanted an expensive house located on an island or not.

However, the spillover can also take place in another way: integral affects increasing incidental affects. For instance, one house buyer reported that he liked the style of the real-estate agent, and this made him feel more serene and optimistic. On the other hand, disappointment caused by a few interested buyers enhanced the overall anxiety of a seller: It feels a bit stressed because not too many people have visited the showings. What if it won’t get sold? Will I be able to rent it out in that case? It’s like, well, an economic pressure. Maybe I’m concerned about how I’ll manage if I have a double mortgage for a longer time. What will the bank think of it, then… (Customer B, seller)

The previous examples showed how affects fuel the same kinds of affects. However, the data also revealed ambivalent affects, such as mixed integral and mixed incidental affects (Table 4). For instance, the decision to buy a new home was often characterised by mixed integral affects: [The decision to buy a home evoked] a good feeling, joyfulness, of course, but also fear, naturally. It’s a huge responsibility, after all, to have such a huge mortgage by oneself. Maybe it’s positive fear, however … knowing that I’ll be able to obtain the mortgage. (Customer F, buyer)

The data also showed mixed incidental affects related to positive or negative life events, such as divorce, widowhood, or family growth, leading to a decision to sell or buy a home. The following citation illustrates the bittersweet affects related to a divorce and a new beginning: ‘Related to the divorce, [I felt] sort of nostalgia and, like, sadness. But when the selling of the house proceeded, I was excited about the new…’ (Customer E, seller)

There were also occurrences where a positive integral affect was felt together with a negative incidental affect or where a negative integral affect was felt together with a positive incidental affect. In some cases, the personality of the buyer or seller was inclined towards feeling certain moods, and the integral emotions evoked by home selling/buying clashed with those moods. In other cases, the life situation leading to the decision to buy or sell a home evoked incidental affects that clashed with the affects stemming from the decision or home itself. One interviewee stated that she felt touched when thinking of selling the home that was the first home that she and her husband set up together, but on the other hand, she was satisfied with the deal: ‘It was a good deal. And I made such a good profit on it that it made me happy’ (Customer I, seller).

Consequently, the intrapersonal interplay of affects took place in various ways. Incidental and integral affects caused spillovers within them or between them. Affective ambivalence was present in both integral and incidental affects and also between them.

Interpersonal interplay of affects

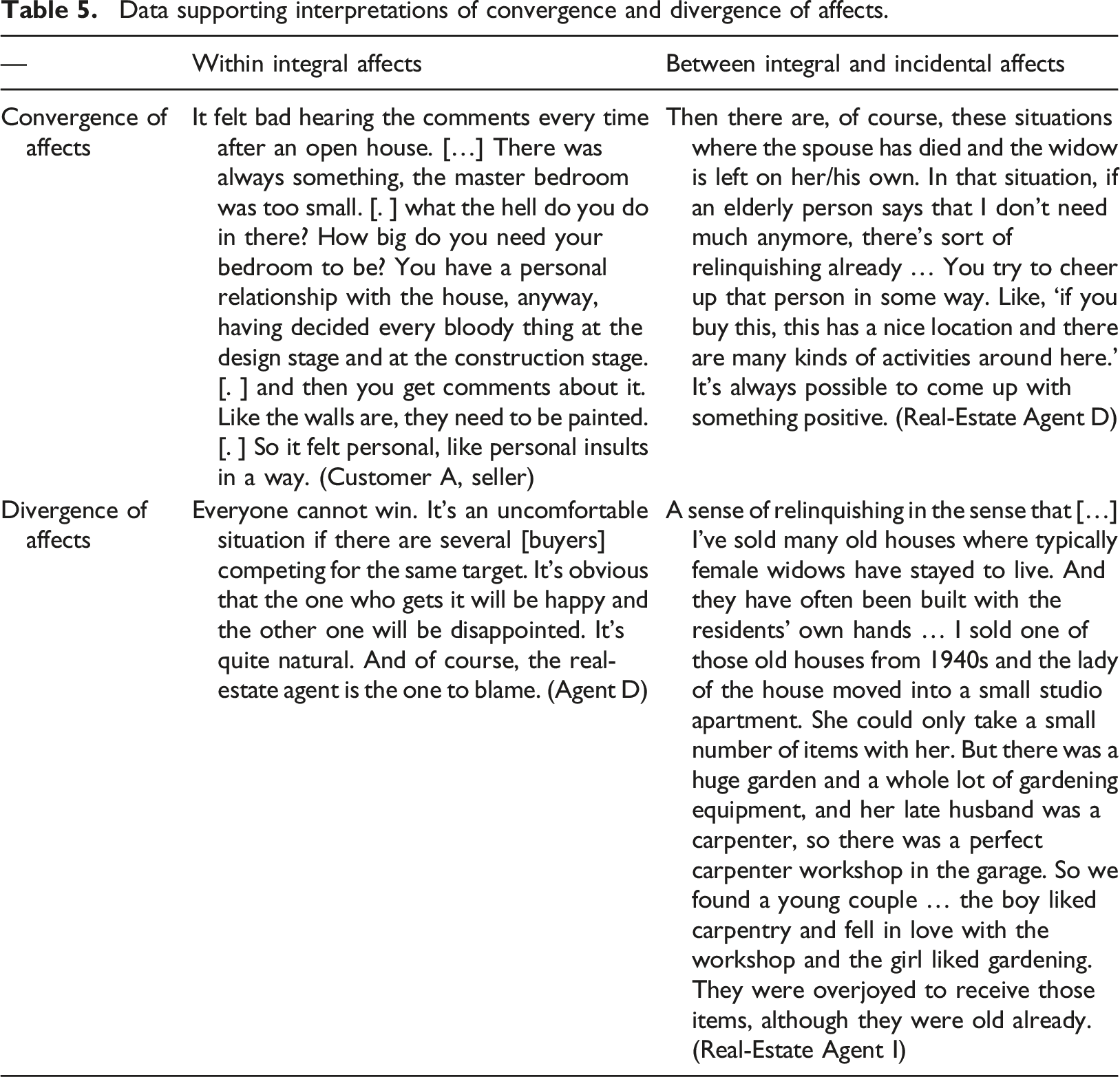

The interplay of affects took place through social interaction and was manifested in both affect convergence and divergence (see Table 5). Convergence of integral affects was often seen in situations when other customers fuelled either negative or positive affects in the home seller. Below is an example of the latter: They [the buyers] were so excited to be able to live there. And I was excited to sell. I had a really good feeling about these guys. They were curious about the history and about everything really. And it felt bloody good that it was bought by someone who appreciates it and is interested in the environment and the neighbourhood. (Customer A, seller)

Real-estate agents also explicitly fostered affect contagion. For instance, in a situation when the home buyer wanted to withdraw from the deal due to feeling sad because he had lost a loved one, the real-estate agent deliberately highlighted the positive integral affects related to a new house: ‘Let’s go and have a chat over there in the garden. Let’s discuss these issues … the things you’re buying here’ (Real-Estate Agent C). Thus, even though real-estate agents are unlikely to alleviate the customers’ negative incidental affects, they can at least highlight their own integral affects related to the transaction and thus strive to make customers’ integral affects positive.

The data also revealed some divergence of affects. This was the case, for example, when a buyer showed overly intense positive integral emotions by being very enthusiastic and neglecting the information given by the estate agent, which made the agent angry: I’ve yelled at a customer. There was a man and a woman who were looking for an island property at the archipelago. We had a boat of our own, so we went to see three or four pre-determined places. The male customer always jumped over the neighbour’s border saying, ‘This one I want to buy! This is good!’ He wasn’t listening to my presentation about the actual place at all. So before arriving at the last place, I said to him, ‘Look, here’s the deal, if you jump over the neighbour’s border in this place, too, I’ll leave you here. You can’t do that.’ He got so upset. (Real-Estate Agent H)

To sum up, the interplay between incidental and integral affects takes place in various ways, both inter- and intrapersonally.

Conclusions

Theoretical implications

By analysing the interplay of customers’ incidental and integral affects, our study advances research on the affective value experienced by the customer. It reveals the composition of, and dynamics involved in, the affective value experience and, by focussing on life transitions, it adds to our understanding of the role of intensive incidental affects in value experience and consumer behaviour.

Past research (e.g. Kim et al., 2020; Sheth et al., 1991) viewed affective value experience as consisting of value provided by integral affects. Our findings significantly extend this perspective and show that affective value also includes value generated by incidental affects. This observation is important because a large range of affective value may be ignored if only integral affects are considered (cf. Bailey et al., 2001). As acknowledged by the Consumer Culture Theory, customer experiences are shaped in the context of everyday life (e.g. Thompson et al., 2013). Considering both incidental and integral affects enables us to see the whole spectrum of customer experiences and to understand customers’ often seemingly irrational behaviours; for instance, when customers suddenly withdraw from closing a deal or are willing to pay unrealistic prices. Customer expectations stemming from incidental affects may often be unrecognised even by the customers themselves, and thus the expectations may stem from customers’ latent needs (cf. Hurmerinta and Sandberg, 2015).

Although past research has acknowledged that affective value is a dynamic and constantly changing concept, the change has been seen to be triggered by factors external to the concept, such as firm offerings (e.g. Lemon and Verhoef, 2016) or interaction in service encounters (e.g. Bailey et al., 2001). Our study contributes to the understanding of dynamics and adds a completely new layer to it: internal dynamics of the affective value. This echoes Cavanaugh et al.’s (2007) call to study interactions between integral and incidental affects.

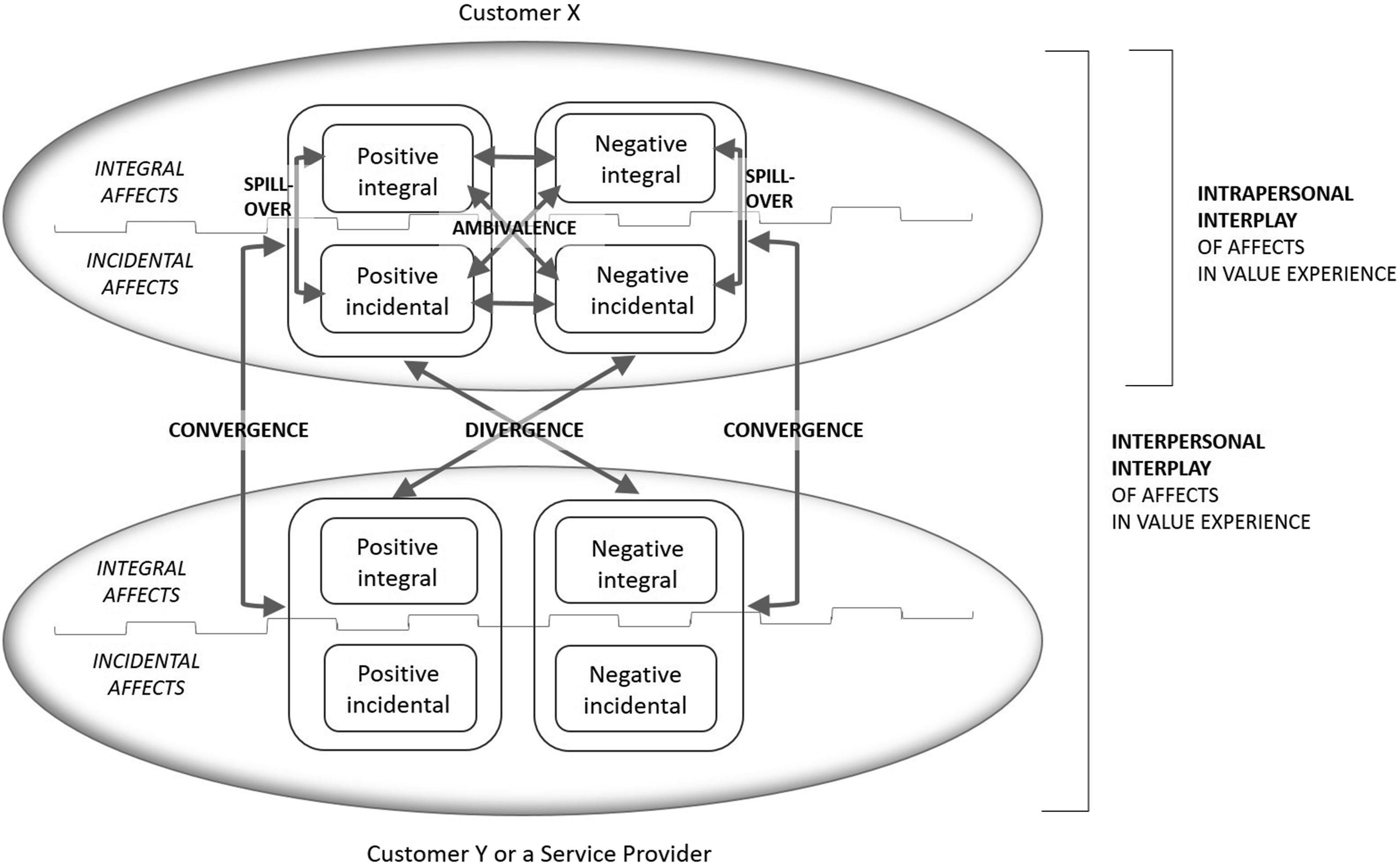

We show that in affective value experience, integral and incidental affects interplay both within an individual and between individuals. More specifically, we detect two types of manifestations of intrapersonal interplay: spillover and ambivalence. In addition, we identify two types of manifestations of interpersonal interplay: convergence and divergence of incidental and integral affects. Figure 2 depicts the detected multidimensionality and dynamism of affective value experience. Both actors illustrated in the figure can be customers, or one of them can be a service provider. Even though we did not study service providers’ incidental affects, past research (e.g. Fowler and Bridges, 2012; Frank and Lynn, 2020) has shown that they are present in the service interaction and thus may reflect on the affective value experience. The interplay between customers’ incidental and integral affects in value experience.

Acknowledging the intrapersonal and interpersonal interplay of integral and incidental affects is important because it allows us to examine the formation of affective value experience in more depth. For example, if the seller of a house receives a price that makes him or her satisfied (positive integral affect), but the cause of the transaction was a divorce triggering sadness and anger (negative incidental affects), then neither the transaction nor the service encounter will necessarily create positive affective value.

Scholars (e.g. Hopkins et al., 2014; Yap and Kapitan, 2017) tend to agree that life transitions are reflected in consumer behaviour. Our findings provide a contribution by showing how this occurs. More specifically, we introduce how the incidental affects evoked by life transitions interplay with integral affects in consumption. This allows us to expand our understanding of value experience in life transitions (e.g. VOICE Group, 2010) by making explicit how life transitions and the affects evoked by them are reflected in customer transactions. Life transitions put individuals in situations with which they are unfamiliar (Altmaier 2020), and our study demonstrates how this is reflected in consumer behaviour. We show how these incidental affects create uncertainty and distinct expectations for transactions, and suggest that a customer is especially prone to experiencing affective ambiguity in the liminal stage of a life transition when remarkable decisions need to be made and permanent changes take place. We complement the previous research that has investigated affective ambivalence in customer behaviour (e.g. Gaur et al., 2014) and noted the hierarchy of objects (e.g. the affects evoked by the salesperson versus the affects evoked by the product) in the buying experience (Sipilä et al., 2018) and add to that knowledge by showing that consumers’ life transitions contribute to such ambivalence.

Managerial implications

This study has been primarily conceptual, but our findings also suggest a number of practical implications, as discussed below.

First, instead of focussing solely on customers’ integral affects, service providers should also consider incidental affects and their role in customers’ value experience. If needs relating to incidental affects are not met, then success in meeting a customer’s expectations in terms of integral affects will not necessarily end up producing a positive value experience. This is of paramount importance for those providers interacting with customers who are going through significant life transitions.

Second, the emotional intelligence of service providers has been stated to be important for dealing with customers’ integral affects (e.g. Gabbott et al., 2011), but we argue that it is even more essential when dealing with customers’ incidental affects. Because incidental affects are more subtle and may be unrecognised even by the persons themselves, they are sometimes extremely hard for service providers to perceive and to take into account.

Third, the intrapersonal interplay of affects requires service providers to account for both affect spillover and ambivalence. Spillovers can lead to self-reinforcing cycles of affects (cf. Fredrickson, 2013). When these cycles are detrimental and increase negative affects, service providers could try to purposefully break the cycles and spark positive affects. Affective emotional ambivalence requires service providers to continuously monitor customers’ affects and not to focus on the first impression of their affects.

Finally, the interpersonal interplay of affects highlights the importance of interaction in the convergence and divergence of affects between individuals. Therefore, we recommend that service providers pay particular attention to the social dimension of the servicescape (cf. Rosenbaum and Massiah, 2011). Understanding the formation of affective value can assist service providers in managing the negative outcomes that stem from intrapersonal and interpersonal affective reactions. The capability to facilitate these situations can essentially contribute to generating positive well-being outcomes from the service, which is currently considered a prerequisite for value creation (cf. Anker et al., 2015; Kelleher et al., 2020).

Limitations and suggestions for further studies

Our study provides many new insights into the concept of affective value. However, there are some limitations. First, the distinction between integral and incidental affects depends on what one considers to be connected to the object of judgement or decision. This division is not always easy to make. We addressed this issue by regarding incidental affects to be those that would exist without the decision-making process. While these affects are distinct in theory, they are often difficult to demarcate in practice and therefore require further conceptual elaboration.

Furthermore, our data is retrospective, relying on the memory of informants and including only those occasions that could be recalled during the interviews. Even though those easily memorable stories presumably contained the most intense affects, we may have ignored many subtler and temporary affects that were not recalled afterwards. Thus, in pursuing a more complete understanding of the dynamic nature of the value experienced, we encourage future studies to use real-time observations.

Lastly, our findings highlight the interplay of affects, and we assume that over time this could lead to integral affects forming moods (i.e. incidental affects). Thus, we encourage longitudinal studies that would enable us to perceive more closely the cumulative and multidimensional nature of affective value experiences.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors are grateful to the Emil Aaltonen Foundation for providing a project grant that enabled this research.

{kind=link}