Abstract

Following a negative service experience, existing studies assert that consumers attribute blame either internally (self-blame) or externally (other-blame) with little indication that the attribution ever changes. This study explores blame to discover whether there are changes in attribution, specifically whether it may shift from self to other. Analysing qualitative data from borrowers in the payday lending market using I-/They-poems, this study finds firstly that blame oscillates between self and other and, secondly, that payday borrowers practice counterfactual thinking to alleviate negative emotions, which in turn prompts this blame oscillation. In revealing that blame attribution can act as a pendulum oscillating between self and other, this study makes a critical advance to existing blame research. The study also supports previous studies in I-/They-poems in uncovering novel insights into consumer theory. Evidence also emerges that the neoliberal view of the ‘empowered consumer’ interacts with the more traditional, organisation-oriented perspective, as from a consumer behaviour perspective, the attempts to improve psychological well-being and the oscillation of blame contribute to shifts in the perceived power in the loan market.

Keywords

Introduction

By the end of 2020, over three quarters of the UK adult population had some form of personal debt, with an estimated five million people owing over £10,000 in unsecured loans (Haqqi, 2019; Renaud-Komiya, 2020). While loans take many forms, one type of high-interest, short-term credit option is the payday loan, named for being repayable on the consumer’s next payday. This type of loan has gained a notorious reputation (Stone, 2019). In 2019, the Financial Ombudsman Service reported a five-year high in payday loan disputes, with 40,000 new complaints about payday lenders, up by 130% in 12 months (Jones, 2020; Little, 2019). Generally, more vulnerable consumers, such as young people, people with disabilities or long-term health conditions and those on low incomes or in insecure employment, are perceived as most at risk of falling into debt from this type of lending (Citizens Advice, 2016; Eabrasu, 2012; Inman and Treanor, 2017). Payday lenders have been accused of targeting vulnerable consumers through sophisticated, predatory practices (Brookes and Harvey, 2017; Rowlingson et al., 2016). An alternative, more neoliberal view however suggests that the responsibility lies with consumers, who should ensure that they fully understand their loan agreements and manage their finances more effectively (Henry, 2010).

Who, therefore, might be blamed for negative experiences with payday loans? According to Malle et al. (2014), blame refers to both a cognitive and a social process that influences people’s judgements and emotions. Scholars differentiate between the concept of blame and other concepts such as anger or negative evaluations of events, as although these concepts have certain similarities, for example, they can be caused by perceptions of injustice or unfair treatment (e.g. Meier and Robinson, 2004), they differ on some defining properties. Unlike blame, negative evaluations can be caused by impersonal events, where consumers might negatively evaluate a service experience due to unforeseen and uncontrollable events, such as unpleasant weather (Malle et al., 2014). Additionally, anger is an emotional state which can occur without accessible warrant or evidence of intentionality or rationale, for example, people might feel angry without knowing why (Gilbert and Miles, 2000). On the other hand, blame is targeted towards a specific agent, who is involved in the event and considered responsible for the outcome, and so requires warrant and justification (Malle et al., 2014).

The way that blame is attributed directly impacts consumers’ physical and mental well-being and can drive behaviours, such as consumer revenge, negative word of mouth and avoidance (Min et al., 2019; Souiden et al., 2019). Although the factors and processes behind attribution of blame in different situations, including negative consumption experiences (Yoon, 2013), service failure (e.g. Obeidat et al., 2017) and consumer misbehaviour (e.g. Harris and Dumas, 2009), are understood, we contend that exploring the attribution of blame in payday lending has the potential to unearth novel theoretical insights. We address the purpose of the research by capturing the complexity and depth of blame attribution through interviews with payday borrowers and presenting their experiences in the form of I-poems. I-poems are recommended as a methodology to unlock the ‘essence’ of individual voices in vulnerable or challenging situations (e.g. Bekaert, 2014; Koelsch, 2016). Husserl ([1931]1962) suggests that ‘essence’ is the central core of reality and refers to a common condition, quality or structure of meanings without which a phenomenon or an experience would not be what it is. Accordingly, this study responds to calls for innovative and interesting methodologies in consumer studies that may uncover new insights (Canniford, 2012; Sherry and Schouten, 2002; Takhar, 2020).

The article is organised as follows: first, the theoretical background to blame attribution and theories supporting internal (self) and external (other) blame are presented, followed by the qualitative methodology employed to address the research. Subsequently, we discuss the findings of our analysis and draw conclusions highlighting the theoretical and practical implications of the research.

Blame attribution

Rational approaches to blame attribution

Over several decades, a substantial body of theoretical and empirical work has emerged that attempted to elucidate the factors that influence blame attribution in different contexts (Janoff-Bulman, 1979; Shaver, 1985). Numerous studies have used attribution theory to investigate how blame is apportioned to different parties following the occurrence of negative events (Carvalho et al., 2015; Yoon, 2013). Attribution theory (Heider, 1958) explains the process by which individuals gather and analyse information to arrive at causal judgements and explanations for events. Attribution theory, arguably, adopts a rational approach, considering that people search for and process information to explain the events and use logical modes of sense to interpret them (Hirschberger, 2006). The result of this process is a dichotomous concept which can be differentiated in terms of internal attribution, in other words individuals behave in a particular way because of factors relating to themselves, and external attribution, where individuals behave in a certain way because of others/the situation in which they find themselves (Heider, 1958). Following this line of thinking, after rationally analysing available information, individuals may attribute blame to themselves, if internal attribution is utilised, whereas, in the case of external attribution, the blame may be placed on one or more of the other parties involved.

Rational explanations of blame attribution include Shaver’s (1985) theory of blame, which suggests that once an individual identifies one party as the cause of a negative outcome, moral judgments follow regarding the degree of responsibility that the party has for this outcome. These judgements are based on causality, prior awareness of the negative outcomes, intentionality, coercion and appreciation of moral wrongfulness. As in attribution theory, Shaver identifies causation as a dichotomous concept, that is, one party can be considered as having caused the negative experience. Once that party has been found responsible for an event, then it is considered as blameworthy, unless an excuse or justification is provided. As such, blame is often considered a uni-directional attitude, often discussed in only one direction (Zaibert, 2005), with few authors suggesting that blame may be attributed to multiple actors (e.g. Malle et al., 2014).

Integrated perspectives on blame attribution

An alternative perspective to blame attribution as discussed above is offered by Alicke’s (2000) culpable control model, which considers blame as an integration of rational analysis with cognitive and affective biases. This model also highlights the tendency to assign blame for harmful outcomes to people, as they are considered in control of negative events, while any environmental or situational factors that may mitigate blame are considered secondary. Alicke’s model proposes once again that blame is attributed rationally, based on the evaluation of the personal control of a party over the negative consequences, but with the important acknowledgement of the spontaneous, and in many cases biased, evaluations of the actions that led to the negative outcome. These spontaneous evaluations are based on stereotypes, emotions and attitudes, even when there is a lack of evidence to assign blame rationally. For instance, encoding bias and attribution bias may influence the attribution process (Carvalho et al., 2015), as they suggest that when an inconsistency exists between people’s expectations and the information provided, the inconsistent information is discounted rather than re-evaluated (Dawar and Pillutla, 2000). Furthermore, negativity bias, by which negative information is given more attention and memory than positive or neutral sources, may also influence blame attribution. This form of bias is particularly prevalent when blame is attributed based on the negative image of a specific party (e.g. Piatak et al., 2017). It is this negativity bias that may contribute to the poor image of payday lenders (Budd et al., 2018) and how negative experiences with them can lead to disproportionately greater blame attributions. The identification of different types of bias that can influence blame attribution supports the argument that blame is not necessarily assigned rationally, as the evaluation of a negative experience may well be influenced by an individual’s experiences, knowledge, attitudes and perceptions.

Within a marketing context, when consumers have a negative experience with a service, they may attribute blame to themselves, to the service provider or indeed to any other party that may be involved (Carvalho et al., 2015; Gelbrich, 2010; Yoon, 2013). Such attributions have damaging implications for the consumers themselves and/or for the service providers. If consumers blame themselves for the negative experience, they may engage in self-criticism, potentially leading to low evaluations of self-worth and feelings of shame, guilt, self-deprecation and depression (Carlsson, 2017). On the other hand, attributing blame to the provider may result in anger and frustration on the part of the consumer, which can lead to avoidance, but also actions against the provider such as revenge, negative word-of-mouth or even calling for tightened regulations of the industry involved (Joireman et al., 2013; Yoon, 2013).

Blame attribution and power

In the context of payday lending and, more broadly, consumer indebtedness, much discussion has taken place around the question of which party has the power to control the negative outcomes. According to blame attribution theories, it is the party perceived to have the power to control the outcome of a situation that is considered responsible and therefore blameworthy (e.g. Gravelin et al., 2019). Additionally, from a consumer behaviour perspective, there are two possible outcomes of blame attribution, depending on the locus of power in such circumstances. Consumers, who perceive themselves to have low power, may choose not to react to the negative event and suppress any complaining intentions, thus internalising their emotions, even when they think that a different party is blameworthy (Min et al., 2019). On the other hand, consumers with higher perceptions of power may seek to complain, look for revenge or take actions against the party considered blameworthy, therefore externalising their responses (Gravelin et al., 2019; Grégoire et al., 2010).

In the context of payday loans, borrowers are likely to see themselves as powerless consumers, owing to their lack of choice, their urgent need for money as well as the aggressive marketing and the contractual and ongoing nature of payday loans (Koku and Jagpal, 2015; Rowlingson et al., 2016). According to Denegri-Knott et al. (2006) this ‘traditional’ perspective considers businesses as powerful entities using marketing to manipulate and control consumers, who are considered ‘helpless’ against the power of businesses. Therefore, from this point of view, consumers may be more likely to attribute blame externally to the payday lenders as the party that has the power to control the negative outcome. At the same time, borrowers may internalise their emotions in the face of negative service experiences and avoid taking any action against the lenders, due to their lack of perceived power.

Equally, there has been a notable growth in studies that adopt alternative approaches to understanding power in the market, discussing power as a dynamic and ‘fluid’ concept and questioning the powerless nature of consumers (e.g. Denegri-Knott et al., 2006; Valor et al., 2017). Although there are many different definitions of consumer ‘empowerment’, one of the most dominant paradigms defines this concept as the freedom of consumers to make decisions and to act as rational and self-interested agents (Denegri-Knott et al., 2006; Wright et al., 2006). From this point of view, consumer power derives from the exercise of choice by free and rational individuals, who can influence businesses and markets, by accepting or resisting their offerings. From this perspective, the current format of payday loans and lenders is a reflection of the consumers’ wants and needs, as they are free to choose or resist the services of lenders, and ‘businesses are believed to produce goods/services in response to consumer demands’ (Valor et al., 2017: 75). This view is supported by existing research, which suggests that various aspects of payday loans are actually welcomed by consumers (Rowlingson et al., 2016). However, it also shifts the blame from businesses to the consumers and carries the implication that consumers act freely and process information rationally, overlooking significant factors, such as the effects of affective and cognitive biases, that might influence decision-making and, in the case of negative events, attribution of blame.

Particularly in the context of loans, there are several external factors, biases and market practices that can affect the decision-making of borrowers, such as financial vulnerability, credit ratings, borrowing history and optimism regarding their ability to repay (Koku and Jagpal, 2015; Rowlingson et al., 2016). For example, Francis (2010) identified a few cases where borrowers consciously decided to roll over their debt, due to optimism bias and imperfect self-control. Nevertheless, negative experiences due to rollover debt may not only be caused by an ‘empowered’ consumer decision, but by the lack of one. Although from a consumer empowerment perspective, offering people more freedom and choices should result in more empowered consumers, scholars suggest that this is not always the case, as it can potentially lead to choice paralysis, that is, the inability to make a choice, due to the need to process more information or fear of making the wrong choice (Shankar et al., 2006). Research reports that short-term credit options can offer too much information, which overwhelms consumers, and can make their decision making more difficult, oftentimes resulting in ‘irrational’ decisions and further indebtness (Mann and Hawkins, 2007). Choice paralysis provides an additional explanation as to why even borrowers ‘empowered’ with freedom and choice regarding their payday loans may not make the most rational financial decisions, such as prompt loan repayment.

These points regarding consumer empowerment provide a compelling argument for research that adopts both a contextual and innovative approach to explore blame attribution and empowerment in the case of negative service experiences with payday loans. In the following section, the method to achieve this type of approach is set out.

Methodology

Poetic witness is an exploratory, creative method of performing and presenting research, and as such might reveal insights previously unsuspected (Canniford, 2012). To explore from a holistic perspective how payday borrowers attribute blame, this study adopts the technique of I-poems so that the voice of ‘I’ comes to the fore (Edwards and Weller, 2012; Gilligan, 2015; Gilligan et al., 2003). I-poems are a method of analysing interviews, ‘a process that traces how participants represent themselves in interviews through attention to first person statements’ (Edwards and Weller, 2012: 203). Focusing on the use of the personal pronoun ‘I’ (the person telling the story) enables the notion of how informants see themselves to emerge from the data. Blame attribution and payday lending offers a rich environment for I-poem research, as the sensitive nature and stereotypes associated with payday loans and the negative emotions associated with blame create a complex balance of power and dynamics during this experience, which is difficult to trace in participant narratives which can be complicated, non-linear and often involve hypothetical discussions. The next sections describe how informants were selected and how the data were gathered and analysed.

Informant selection

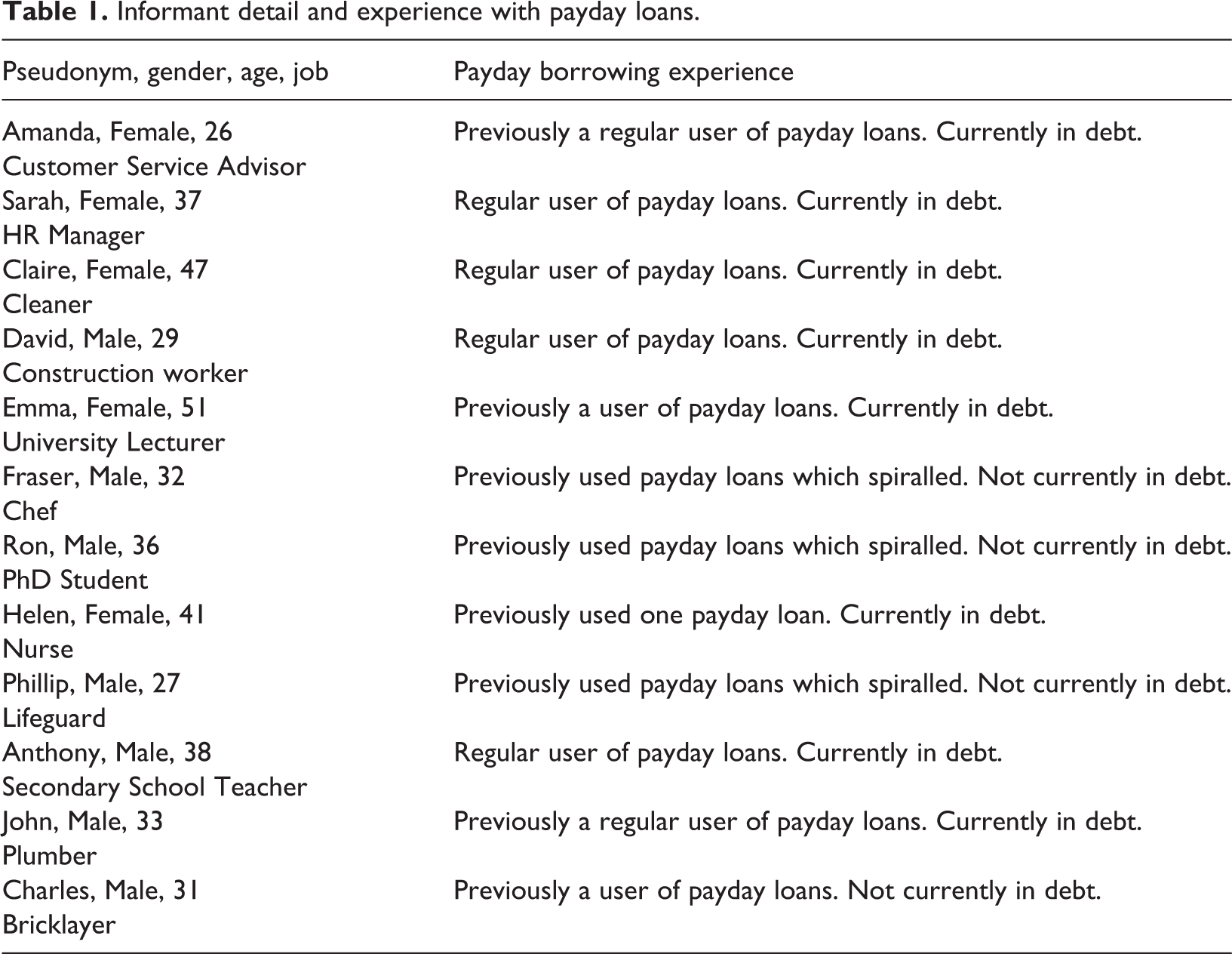

The study took place in the north east of England, where incomes and savings levels are often less than the rest of the county (Aldermore, 2019); ideal conditions for the payday loan product to thrive. Given the challenges for informant recruitment created by the sensitive and in many cases emotional nature of this research topic, a step-wise, dynamic process was adopted to secure appropriate informants for our study (Peticca-Harris et al., 2016). Initially, informants for the study were recruited through advertisements in local community spaces (halls, libraries, sports centres and health centres) as well as local credit unions, charity shops, payday loan companies, debt charities and independent pawn shops. Informants were also recruited through word-of-mouth referral from existing participants following their interviews. A group of 12 informants was recruited, in line with qualitative research approaches that emphasise in-depth analysis of a relatively small number of informants (Hatzithomas et al., 2016; Lee et al., 2008; Wang and Horng, 2016; Yam et al., 2017). Table 1 provides information about the informants, using pseudonyms to ensure anonymity, and detail of experiences with payday loans.

Informant detail and experience with payday loans.

All informants identified as working or middle class and were in employment with a weekly or monthly salary when they were using payday loans.

Data collection

As a method for understanding another person’s experiences (Thompson et al., 1989), interviews can be considered a construction site of knowledge (King and Horrocks, 2012; Kvale, 1996). In-depth interviews were conducted owing to their flexibility to accommodate a variety of scenarios, allow a natural narrative and elicit first-person, subjective descriptions of specific experiences, providing comprehensive insight into the topic (Finlay, 2009; Fossey et al., 2002; Thompson et al., 1989). During the sessions, the interviewer facilitated an open-ended dialogue and encouraged the informants to describe in detail their actual experiences, general perceptions and associated issues in relation to payday loans. The interview style was intentionally conversational to encourage informants to set the dialogue with the researcher and to allow questions to emerge from the conversation rather than from a predetermined list. Each interview lasted for approximately 60 minutes, with the longest being 141 minutes. Informants consented to the digital recording of the interviews in line with the ethical codes of the researchers’ institutions. This length, we assert, enabled informants to relax and allowed them to reflect and express their perceptions and feelings in relation to their experiences with payday loans and lenders. In line with qualitative data analysis practice (Patton, 2015), preliminary analysis took place at the same time as collection, prompting further avenues of enquiry. These avenues were pursued during a further 15 follow up interviews with eight of the informants. Overall, 26 hours and 12 minutes of audio were generated which were subsequently transcribed verbatim.

Data analysis

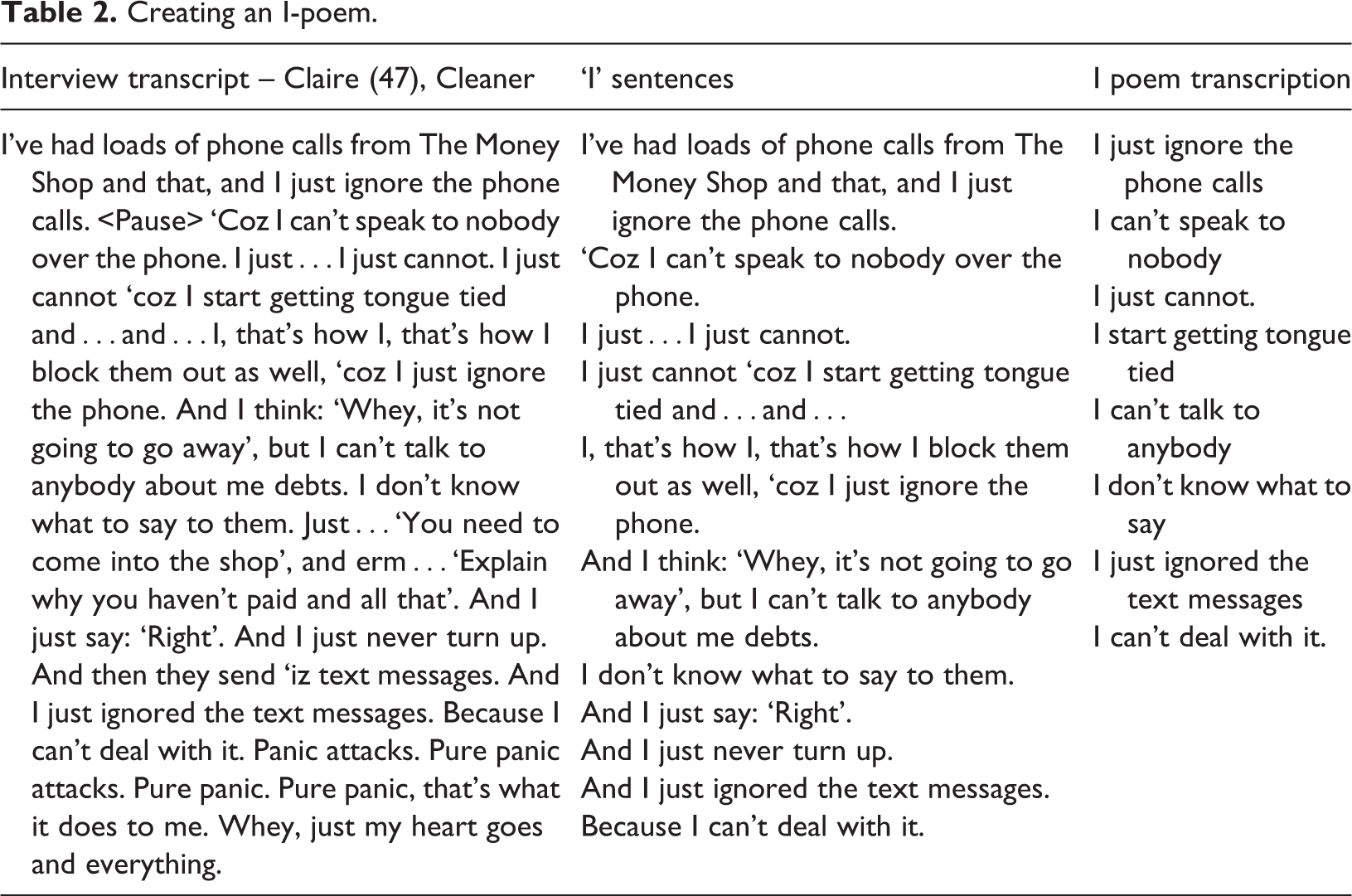

The transcripts were analysed using I-/They-poems, which focus on a concentrated listening to the voice(s) of the participant. I-poems, derived from the Listening Guide (Gilligan, 2015; Gilligan et al., 2003), ‘trace how participants represent themselves in interviews through attention to first person statements’ (Edwards and Weller, 2012: 203). I-poems have been mostly used in medical psychology or educational psychology contexts; we suggest this method translates positively into consumer behaviour studies. We followed the recommendations of the Listening Guide, also known as Voice-Centred Relational Method (Brown and Gilligan, 1992), of four distinct stages of readings though the transcript narratives (Mauthner and Doucet, 1998). Particular emphasis was given to the second reading, the purpose of which is to ‘…attend to silenced voices and, in particular, to pay attention to the multiplicity of a single voice’ (Koelsch, 2016: 170). Focusing on the use of the personal pronoun ‘I’ (the person telling the story) enables the notion of how informants see themselves to emerge from the data, while highlighting and clarifying where they may emotionally or intellectually struggle to clearly articulate a complex experience (Doucet and Mauthner, 2008) and revealing an introspective, inner dialogue representing the informant. The I-poems which are presented in the findings were written using the method described by Edwards and Weller (2012), where the narrative is stripped down to the selected pronoun and next one or two words (Gilligan et al., 2003; Koelsch, 2015). This process is illustrated in Table 2:

Creating an I-poem.

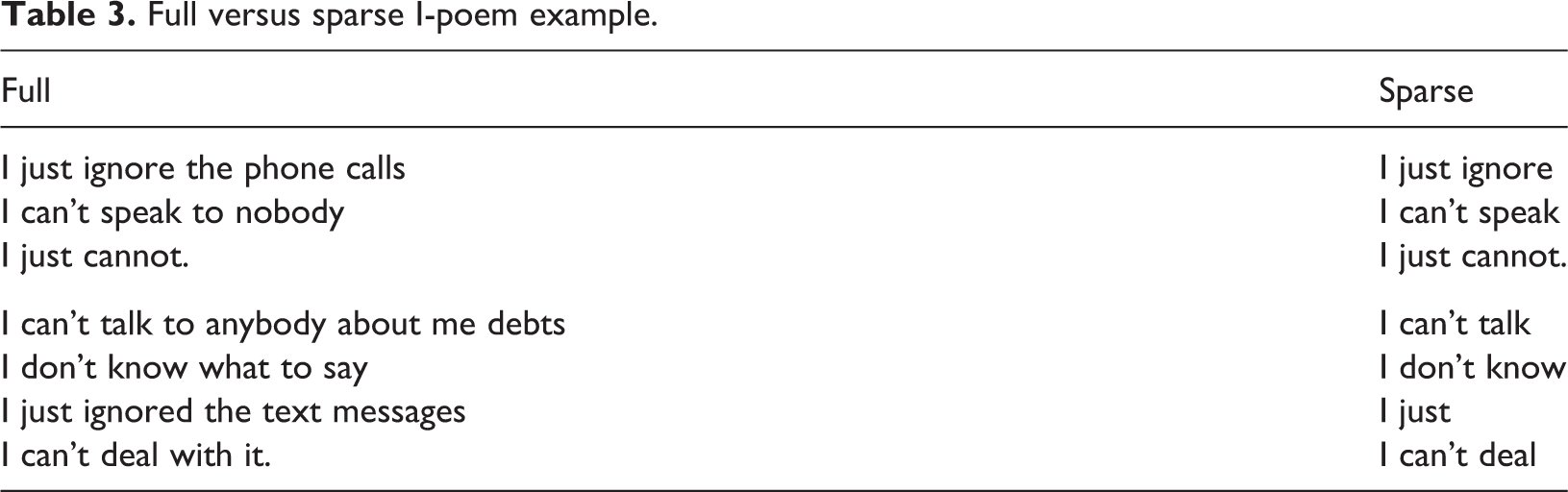

This sparse presentation helps focus the researcher on the storyteller, rather than the story (Koelsch, 2016) although we found merit in leaving more content in the I-poems, providing a deeper understanding of a complex phenomenon (Balan, 2005; Edwards and Weller, 2012; Zambo and Zambo, 2013). In the literature, the finished design of poems varies. For example, some researchers advocate stripping the narrative down to the selected pronoun and next one or two words (Gilligan et al., 2003; Koelsch, 2015; Woodcock, 2005). Koelsch (2015) names the resulting poetry ‘sparse’ I-poems. Longer sentences can be seen in other I-poem examples (Balan, 2005; Zambo and Zambo, 2013). Koelsch (2016: 171) suggests that ‘…this strays from the original intent and structure of I poetry’. Gilligan et al. (2003) suggest that lengthening the lines loses focus on the usage of ‘I’, investing the reader instead in plot details. Invariably, ‘…the reader can become invested in the story rather than the storyteller’ (Koelsch, 2016: 172). An attempt to illustrate the different styles can be seen in Table 3, using the extract of Claire’s transcripts demonstrated in Table 2.

Full versus sparse I-poem example.

The sparse I-poems have potential to provide a clearer voice. In omitting the ‘content’, a much more beautiful, stark image is presented, and the internal voice of the participant can be heard with precision. Koelsch (2016: 172) admits that ‘…it is difficult to create poems that leave out the details of their stories; however, over time I have found the value and beauty in repetitive, simple I phrases’. The method used to analyse these is known as an ‘I-poem voice approach’ (e.g. Edwards and Weller, 2012), which focuses heavily on listening to the voice presented, and considering the position as the researcher alongside the presented data. Gilligan (2015: 72) explains what the method achieves: The logic of the poems is not linear…Listening for the I can also lead to discerning patterns in the way the I moves, as for example when statements of assertion (I know, I want) are regularly followed by the statements of negation (I don’t know, I don’t want)…In this way, one can come to predict how the I will move.

In addition, another development to the I-poem method we propose is not only to reveal the internal voice (borrower/I), but we found merit in considering the external insights (lender/they). Variations of the ‘I’ pronoun are possible if relevant to the data set (Kara, 2015). Specifically, in considering ‘…the interpersonal, group and community levels [and] the dimensions of power in relationships both within and external [to the participant]’ (Lovell and Akhurst, 2017: 7–8), for example, we-poems (Kayser et al., 2007), she-poems (Bekaert, 2014). This study is a departure from the traditional method of focusing on one voice, but considers two, and the interplay between them within the narrative. There are few studies that utilise multiple pronoun-poetry (e.g. Lovell and Akhurst, 2017, who briefly consider the merits of I-, You-, We- and Your-poems), which appears to be an opportunity for development. The traditional I-poem analysis revealed the key voice was the one relating to self-blame but during the other stages of the Listening Guide, the voice of other-blame was heard in the relationship between the ‘voice of I’ and also the ‘voice of they’. This second voice contrasted quite distinctly with the emerging self-blame voice from the I-poems and indicated that blame attribution is not fixed but appeared to shift back and forth between self-blame and other-blame. Following an iterative, back-and-forth approach (Thompson et al., 1989), we studied the transcripts to uncover the oscillation between ‘I’ and ‘They’, incorporating the ‘They’ pronoun into the work (They-poems). All informants seemed to experience this shifting from self- to other-blame to a greater or lesser degree. After considerable deliberation, we labelled this shifting back and forth the ‘oscillating voice of blame’.

The third stage of the analysis, following the Listening Guide, was an exploration of how the informant speaks about their relationship with the lender, a reading for ‘they’ was also conducted. Both ‘I’ and ‘they’ statements are ‘…powerful speech acts embedded in everyday talk’ (Parsons and Pettinger, 2017: 173). According to existing studies, other pronouns are acceptable to produce alternatives to the narrated self, so ‘they’ is acceptable within the parameters of the Listening Guide (Kara, 2015). Accordingly, we present our I/They pronouns within one poem, with the ‘They’ lines indented for clarity, for example: They don’t care They’re all in the same dirty game. I’m reckless I don’t care

Findings and discussion

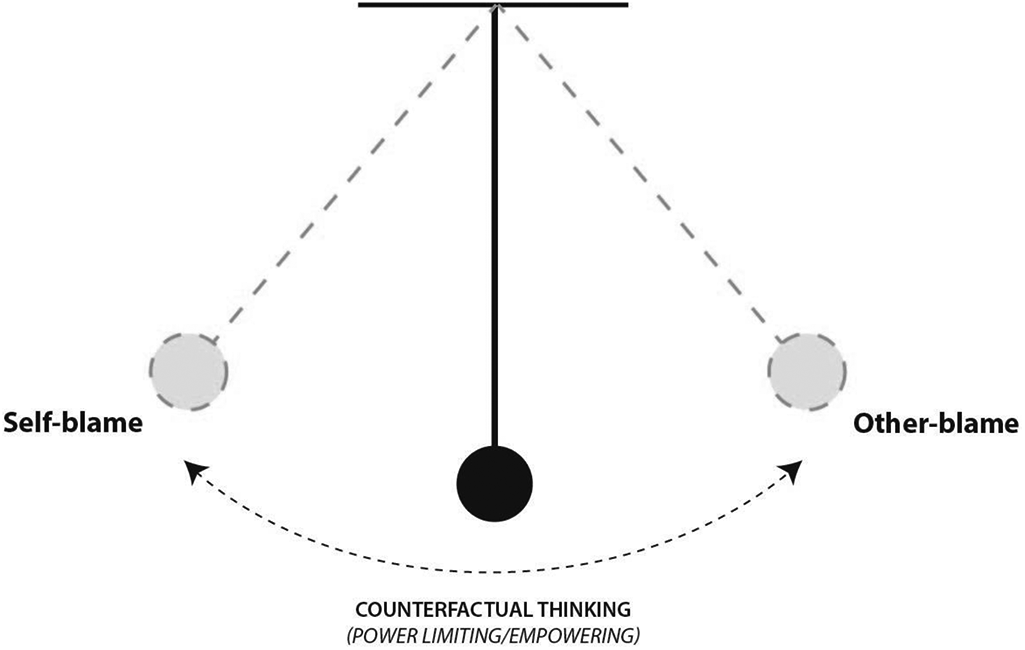

The findings are organised around whom the informants believe is to blame for their negative experiences with payday loans and how they attribute blame to the parties, with I-poems evoking their voices. Figure 1 prefaces this discussion by depicting the major finding of the study, which is that blame attributions oscillate between ‘who’, that is the borrower, who self-blames and the payday lender (other), owing to counterfactual thinking, that is the ‘how’.

Pendulum of oscillating blame in payday lending.

Who is to blame?

In conducting our pronoun poetry analysis, an interplay of voices emerged when considering blame attribution. Our analysis surfaces a self-blame voice where borrowers blame themselves for the negative experiences with payday loans, alternating with an other-blame voice that attributes blame to the lender. Blame attribution was sometimes more heavily weighted in one direction, but with an oscillation that meant blame was never finally attributed to one party or the other. This finding appears to be quite novel and is evoked in the following I-poem: I think, well, it was me that walked in. I knew that whatever I borrow I have to pay back! They exacerbate the problem They’re disgusting because They know They are the only people who some people can turn to for credit. They should be more responsible. (Anthony)

The analysis suggests that blame is attributed internally as borrowers assume an inability to manage their finances, their frivolous spending and/or their risk-taking approaches to financial matters. This finding is broadly supported in the existing literature on payday loans (Brown and Woodruffe-Burton, 2015; Jappelli and Padula, 2013) and is in line with the neoliberal, consumer-empowering view of the payday loan market outlined previously. Furthermore, informants engage in self-blame, because according to them, they failed to search sufficiently for the relevant information prior to taking the payday loans or they were overly optimistic about their situation, which suggests that optimism bias (Weinstein, 1980) may have a significant impact on borrowers’ decision making. The following I-poem voices these reasons for self-blame. I first got it [payday loan] out and I thought, “Oh, it’ll be fine”. I just needed the extra, I’ll pay it at the end of the month and just really strictly budget You find that, actually, You haven’t got anything left, You’d paid out the extra hundred pound, on top of what You would have been paying out for the rest of your bills. (Amanda) I do sit on a night time, I panic. I’ve had the sleepless nights. I owe this money, you know? It just makes Me ill. Pure panic, it’s a horrible feeling. […] You’re depressed, You just think that there’s nobody wants to know. (Claire) They [lenders] are making money from people’s misery. I blame [name of lender]. They are like organised crime – that’s why They [government] have decided to close them down. (Charles) I was expecting kind of, like… Bailiffs banging on the door and like: “Let us in! We’re going to take what you’ve got” I’ve just got this vision in my mind, They’re gonna come in heavy… The bailiffs banging on the door and They’re so ruthless, just barging Their way through people’s houses and taking stuff, People are like, distressed to hell, I thought: “Oh God. This is going to happen”. (Sarah)

The essence of the voice in external blame attribution, on the other hand, leans towards feelings of annoyance and anger or helplessness and fear towards the lender (see, e.g. Gravelin et al., 2019; Grégoire et al., 2010; Obeidat et al., 2017), as voiced in this poem: Villainous bastards! You’re just getting people into debt! They’re unscrupulous They don’t care who they lend to, They want to make money, don’t they? (David)

How blame is attributed

The oscillation of blame attribution occurs as informants consider alternatives that may have led to more positive outcomes, if either of the parties had behaved differently. Existing literature calls the process of imagining the actions that could lead to a more positive outcome ‘counterfactual thinking’ (Roese, 1997). According to the theory of counterfactual thinking, individuals imagine possible alternative courses of action that they or others could have taken, comparing the more positive outcomes with the outcomes that actually occurred (Branscombe et al., 2003; Miller et al., 1990; Nicklin and Williams, 2009; Roese, 1997). For example: I think I probably didn’t look as hard as I could have done for it [The Ts & Cs]. I think it possibly would have been there, but in small print, if I’d wanted to find it. (Amanda)

In addition to improving one’s psychological state, counterfactual thinking influences consumer behaviour, as by considering what ‘might have been’, individuals construct meaning for an event (Kray et al., 2010). In our study, counterfactual thinking is activated when borrowers reflect on how their experience with payday loans may have been different. Our findings indicate that counterfactual thinking creates an oscillation of blame, as the borrowers contemplate different ways that they or the payday lenders would, should or could have acted. This process results in changes in the blame attributions for their negative experiences, for example: I felt bad borrowing more money of my mam n dad and my sister. I went to get a payday loan. I went in and just asked for a hundred pound initially. [They said]: “Oh you can have all this extra money”, I was like: “No, don’t tell me that” I walked out just with a hundred pound. The day after I was back there and got another hundred pounds. Because she told me it was there I was back down the following day for a hundred pound. That naughty woman [shouldn’t] have told me there was more there! (Sarah)

In our study, this blame-shifting or counterfactual thinking is arguably perpetuated by the notion of disempowerment and the resultant negative feelings associated with payday loans (Citizens Advice, 2016; Eabrasu, 2012; Inman and Treanor, 2017). Interestingly, our informants did not fall into the traditional vulnerable consumer categories, such as bottom-of-the-pyramid or unemployed (Grotlüschen et al., 2019). A payday loan cannot be sought without a guaranteed payday, and all of the participants were employed at the time of taking the loan. Participants reported that owing to unforeseen personal or situational changes, they experienced temporary disempowerment they were unable to repair due to financial vulnerability. This situation led them to turn to payday lenders, in an effort to empower themselves and escape from this temporary vulnerable state: I was in a desperate situation I need a payday loan. (Anthony)

In line with the discussion around disempowerment and blame, our analysis also unearths two different types of counterfactual thinking: empowering and power-limiting. In the first case, counterfactual thinking may increase the perceived power of the borrowers and encourage them to either take control of their finances and avoid similar situations in the future (when blame is attributed internally) or take actions against the payday lenders (in the case of external blame attribution). This empowering type of counterfactual thinking relates to the neoliberal view of the loans market, which supports consumer power and freedom of choice (Bradshaw and Ostberg, 2019; Valor et al., 2017). On the other hand, the power-limiting counterfactual thinking process leads to the gradual disempowerment and negative emotions manifested by either acceptance (in the case of internal blame) or avoidance behaviour (other-blame). Both empowering and power-limiting voices can be heard in the poems. For example: I always say “You made your bed and you have to lie in it”. I have no one else to blame but Myself for spending My money on alcohol […] I’m to blame for my wrong decisions and not being more careful with my money - but if They [payday lenders] wanted They could have made it easier for me. I know They are in this to make money, but sometimes I think “That’s not fair. You know that people are in a difficult position and You take advantage of it”. (John)

Our findings on how blame is attributed in the payday lending market represent a noteworthy contribution to theory in this area as we detail in the next section.

Conclusion

This study set out to explore blame attribution and uncover whether it may shift from internal (self) to external (other), by using I/They-poems to analyse qualitative data from borrowers in the payday lending market. Our research offers several key theoretical implications and extends theory in this area, as it demonstrates that, to deal with negative service experiences, borrowers shift blame back and forth, from self to other, due to counterfactual thinking. This process affects the perceived power of the consumer and can lead to changes in their emotions, behaviour and decision-making. To the best of our knowledge, this study constitutes the first attempt to explore holistically the concepts of blame and self-blame and their impact on consumer behaviour in the services industry. In the next section, we discuss in more detail the theoretical and practical implications of this research.

Contributions of the study

Research has portrayed blame attribution as a broadly fixed concept, driven by rational thinking and spontaneous evaluations, influenced by stereotypes and cognitive and emotional bias (Alicke, 2000; Shaver, 1985). This study, using the novel approach of I-poems to explore blame, extends existing theory by finding evidence to the contrary, in that blame attribution may also be dynamic. In revealing these counter effects, we argue that theoretical contributions are made to several relevant literatures.

The first contribution of this study is that we reconceptualise blame attribution in novel ways, as a dynamic process, shifting between self- and other-blame. Specifically, our framework extends the scope of theoretical models of blame (e.g. Alicke, 2000; Shaver, 1985), showing that blame attribution may be dynamic, irrespective of whether the ‘blamers’ blame others or themselves first. Viewing blame as constant may limit its potential to explain consumer reactions and emotions following negative experiences (Antonetti, 2016). Therefore, we introduce a novel construct, blame oscillation, and suggest factors that trigger the shifts between internal and external attribution of blame. As earlier studies have highlighted the importance of blame attribution, due to its influence on consumer emotions and behaviour (e.g. Yoon, 2013), the identification of this blame pendulum offers an alternative approach to the traditional theories of internal versus external blame attribution and is arguably a more appropriate framework for consumer research particularly in the context of negative service experiences.

Furthermore, our study adds to the attribution literature by clarifying how the direction of the oscillations between self- and other-blame appears to be the result of counterfactual thinking, which the borrowers employ to alleviate some of the negative feelings resulting from their negative experience. Although existing studies suggest that the primary focus of counterfactual thinking is improving the psychological well-being of the individual (e.g. Kray et al., 2010; Nicklin and Williams, 2009; Roese, 1997), our findings demonstrate that the feelings of disempowerment before and after acquiring the payday loan, may perpetuate the process of counterfactual thinking and blame oscillation, as individuals fail to identify more ‘positive’ alternatives to their actions. This process may also lead to changes in the nature of the negative emotions, for example, from stress and shame to fear and anger, due to the oscillation of blame that is created during this process.

A third theoretical contribution offered by our framework is that the process of counterfactual thinking also has an impact on the individual’s perceived power and control of the situation, which influences not only the attribution but also the consequences of blame. This finding supports the ‘fluid’ view of power in the market adopted by earlier studies (e.g. Valor et al., 2017), as we identify counterfactual thinking as a potential cause of the shifts in the borrowers’ perceived power, which may result in changes in blame attribution. Additionally, contributing to the literature that links perceived power and consumers’ emotions and reactions following a negative experience (e.g. Gravelin et al., 2019; Grégoire et al., 2010; Min et al., 2019), our findings indicate that by either increasing or limiting the perceived power of the borrowers, counterfactual thinking can also lead to changes in consumer emotions, behaviour and decision-making. Therefore, using our blame oscillation framework, we propose a novel approach to exploring blame and its consequences, as the amplification or the attenuation of the perceived power through counterfactual thinking can result in changes in blame attribution, but also consumers’ emotions and the way they react to negative experiences.

Uncovering these insights highlights the value of employing a research methodology that focuses on exploring the essence and the meanings of a phenomenon (e.g. I-/They-poems). This enabled better insights of the blame attribution process and the further development of blame theories, which allows a more in-depth understanding of consumer behaviour following a product or service experience. In this instance, this method permitted the researchers to clearly hear the oscillating essence of the informants’ voices when discussing blame, from the outset. The amount of rich data generated in the study was significant, so the I-poem method enabled a logical and clear way of focusing on particular, relevant dialogue. An aspect of discussing complex issues such as negative financial experiences is that the informants often discuss hypothetical situations, perhaps to distance themselves or protect privacy (Dollahite et al., 2019) and/or ‘over’ conversing and taking narrative detours (Corbin and Morse, 2003), perhaps as a form of counterfactual thinking. More traditional forms of analysis may get waylaid with considering the broad dialogue, whereas I-poems enable a much more focused experience.

Limitations and further research

This study has a number of limitations, which we detail as follows. Firstly, payday loan borrowers are a particular type of consumer, who owing to their financial circumstances have limited choice about their choice of lender. This situation may influence their blame attributions, as these borrowers are often stigmatised and subjected to negative social stereotyping, which may exacerbate their feelings of disempowerment and influence the blame oscillation process. Furthermore, the contribution of this study is constrained by the chosen in-depth, qualitative methodology but at the same time suggests a number of avenues for further exploration as set out below.

Secondly, the investigation is concerned with a particular experience, that is payday lending with informants who are experiencing and have experienced very challenging circumstances. Further research is needed to investigate whether the theoretical framework developed in this study holds up in the case of other negative experiences, where the circumstances may be less difficult. Additionally, using I-poems has engendered some powerful theoretical insights in blame attribution and payday borrowing. This method can be used more widely to further develop theoretical frameworks to explain consumer behaviour following negative service experiences, including research in other areas, for example, gambling. Thirdly, this study has revealed that blame attribution is linked to wider connotations of where blame lies in markets and industries, specifically relating to consumer empowerment and industries that have a poor reputation.

This study also opens up some further areas for research. We have referred to counterfactual thinking as a cause of blame oscillation. However, this is such an important construct that it needs much deeper investigation than that we are able to give it within this particular study. Our research suggests that there is a need to examine further the differences between empowering and power-limiting counterfactual thinking and investigate any links with the language used by the payday lenders, or other industries with poor reputations, in their communications with their consumers. Furthermore, as the study is located within a specific geographical area, with strong cultural, socio-economic and industrial overtones, a more detailed investigation into blame attribution within this context could enrich understanding. 1 The data also reveal the impact of the negative stereotypes of payday lenders and the social stigma of using payday loans on consumer behaviour and decision-making. In our study, we allude to the poor reputation of payday lenders, but there are other providers of finance who fall into this category. Is there scope for improving such reputations? If such lenders are able or willing to burnish their reputation, the impact of reducing stigma at the consumer, community and social level could have wide reaching, complex implications.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.