Abstract

Despite globalization’s distributional impacts, we know little about (potentially differential) tax preferences of trade winners and losers, especially within social classes. We assess tax burden preferences to sustain public good provision using a vignette experiment with randomized tax instruments in the context of a liberalizing economy. More specifically, we analyze data from an original, randomized household survey of 1008 individuals in Sao Paulo State, Brazil, in 2019. We study preferences for increases in personal income, value-added, or corporate income taxes to improve funding for the universal health care system after Brazil adopts its free trade deal with the European Union. Findings reveal that the trade-losing poor support progressive taxes, whereas the trade-winning poor favor regressive instruments. By dividing the poor, globalization may create a barrier against more progressive fiscal strategies in emerging economies.

Tax revenue is languishing in the Global South due to difficulties in implementing tax reform and raising domestic tax revenues (Besley and Persson, 2014). Reforming and ensuring broad compliance with taxes are politically contentious tasks wrought with bureaucratic and technical difficulties. Brazil is no exception. Total tax revenue, while higher than in the early 1990s, has been declining since the early 2000s (UNU-WIDER, 2021). Yet, politicians in Brazil face resistance to tax reform: President Rousseff saw extensive protests against her ‘economic quackery’ when she ‘proposed a new levy to help compensate plummeting tax revenues’ (Doce, 2016).

One critical, yet understudied, factor likely affecting citizens’ calculation of their tolerance for tax reform is how they are faring under the market liberalization undertaken by many of these developing and emerging economies. Trade liberalization has distributional impacts that create large-scale changes in individuals’ actual and prospective economic circumstances (Menéndez González et al., 2023). Signing a new free trade agreement affects the public’s economic outlook through its implications for employment opportunities, job security, and wages (Revenga, 1997). With the European Union (EU)–Brazil 2019 free trade agreement (FTA), for example, economists predict the expansion of primary product and low-technological manufacturing, but a decline in other industries (Megiato et al., 2016). 1 Such structural transformations associated with market integration create unequal gains and losses as not all sectors of production are equally affected (Menéndez González et al., 2023). Unequal distribution of gains and losses also differentially influences citizen’s risk perceptions (Ardanaz et al., 2013; Campello and Urdinez, 2021).

Building upon the globalization-welfare preference literature that identifies important implications of trade liberalization on welfare state preferences in advanced-industrialized economies (Hays et al., 2005; Schaffer and Spilker, 2016; Walter, 2017) and recent insights from cases in South and East Asia (Lim and Burgoon, 2020; Linardi and Rudra, 2020), we study tax attitudes in liberalizing Brazil. We ask, how does the economic context of trade liberalization, which brings prospective new gains to some and losses to others, affect attitudes on who should bear the burden of taxation to fund public goods? Does the public believe winners should pay a larger share via corporate income taxes (CITs) or are prospective, positive returns to trade a reason to free companies from paying more taxes, shifting the burden onto consumers via value-added taxes (VATs)?

In contrast to the tax preference literature’s focus on the rich, who admittedly pay relatively more tax contributions (Ballard-Rosa et al., 2016; Berens and von Schiller, 2017), we suggest turning toward the poor as this is where free trade generates a powerful divide. In contrast to classic income-based divides discussed in existing research, we post that all lower-income individuals are not equally supportive of progressive tax instruments, especially post-liberalization. Some of the poor are big winners from free trade as they are employed in export-oriented sectors and, as a result, might have divergent fiscal policy preferences than the trade-losing poor, working in the import-competing sector. While the poor are more likely to support relatively more progressive taxation to sustain public goods following the interest-based logic (Barnes, 2015; Meltzer and Richard, 1981), trade winners are more likely to support the relatively more regressive VAT increases (instead of relatively more progressive taxes like the CIT; see Bird and Zolt, 2004) to improve public good finances as they face prospective gains and upward mobility (Benabou and Ok, 2001). Taking both social class and trade welfare distributions into account, the trade-losing poor are expected to favor tax increases through progressive instruments relative to more regressive ones. Critically, however, there are crosscutting preference as some of the poor are trade winners. If upward mobility expectations related to free trade policies dominate preference formation on tax burden attitudes, we hypothesize that the trade-winning poor are more likely to be against progressive taxation relative to the VAT. Trade-induced inequality may thus create opposition to more progressive taxation from those who are unlikely suspects: the trade-winning poor.

To this end, we conducted a face-to-face survey in Sao Paulo State, Brazil, in August 2019 right after the agreement of a new EU–Brazil FTA. 2 We collected over 1,000 survey responses using probability-proportional-to-size-sampling across Sao Paulo State municipalities. We first primed all respondents with information about the EU–Brazil trade deal. 3 Then, we asked all respondents if they would support increased taxes to improve financing for Brazil’s broad-based public health care system, the Sistema Único de Saúde (SUS) (our dependent variable) with a survey vignette. We earmark the tax increase to further fund Brazil’s universal health care system to reduce uncertainty (see Flores-Macías, 2018). Moreover, since universal health care is widely available to all Brazilians, by focusing on this public good, we can reduce concerns of exclusion rationales and attitudinal differences due to unequal access. Following Korpi and Palme (1998) and the paradox of redistribution, universal social policies are most favorable to create cross-class coalitions between the poor and the rich as both groups benefit from the program as opposed to contribution-based or targeted programs. The survey setup hence challenges our theoretical argument because those who experience income gains should be generally in favor of universal programs. When asking about support for tax increases to improve funding for the SUS, we used a vignette experiment and varied the type of tax named, focusing on the three major tax instruments: personal income tax (PIT), CIT, and VAT. We analyze the heterogeneous treatment effects of the random assignment of the tax instruments by social class, trade winner–loser/status, and a combined indicator of class and trade winner/loser status on individual support for a tax increase to sustain the SUS. We operationalize trade winner status by looking at the respondent’s sector of employment (following the Ricardo-Viner model). As a robustness check, we also use an egotropic assessment of the respondent’s expected gains from the new FTA and skill level as an alternative measure of social class.

Our statistical estimations provide support for our hypotheses. While belonging to a lower social class is positively correlated with support for tax increases to sustain the SUS when the tax instrument is a progressive one, we find a divide among the poor once we identify poor trade winners and poor trade losers. Among the poor trade winners, opposition to regressive taxation loses an important share of its base. As Holland (2018) emphasizes, the poor already have ‘diminished expectations’ toward the distributive capacity of the state because of enduring inequality and the truncated nature of the welfare state. The distributional impact of trade liberalization might further explain some of this lack of expectations among the poor. In essence, globalization creates a barrier against the relatively more progressive fiscal strategies in emerging economies: we find that trade openness that benefits the poor and rich alike guards corporations from heavy taxation.

Our study contributes to the scholarly debate in two ways. First, by focusing on the poor, who form a decisive voter group in Brazil (Zucco, 2013), we reveal an important possible obstacle to tax reform. Because of the divergent tax preferences among the trade-winning poor and trade-losing poor post-liberalization in Brazil, there is less broad-based support for relatively more progressive tax reform as might be theoretically anticipated in a country with high levels of inequality (in 2019, Brazil had a Gini coefficient of 53.5 (World Bank, 2022)). Researchers point to the role of contentious politics or broad popular support as a means to challenge or circumvent fiscal policies dominated by elites (Fairfield, 2013; Slater, 2010). Our predicted fractures among the poor’s preferences in liberalizing economies lend insight into why tax policies may continue to be dominated by elite interests in the Global South. However, an alternative perspective is that with less support for progressive taxation, more redistribution could occur post-taxation (Barnes, 2018). Taxation is only one redistributive tool and when progressive taxation faces obstacles – especially under international market integration – alternative forms of redistribution may be called for (see Barnes, 2018).

Second, we extend the comparative political economy literature that relies on domestic factors to understand tax preferences in developing countries (e.g., Berens and von Schiller, 2017; Fairfield, 2013, 2015; Flores-Macías, 2014, 2018). We connect international political economy’s research on the welfare implications of globalization (Menéndez González et al., 2023; Walter, 2017) to tax preference formation in the Global South (Lim and Burgoon, 2020; Linardi and Rudra, 2020). While our survey evidence is from Brazil, our findings may be fairly generalizable to other liberalizing, emerging economies with high levels of income inequality, extensive trade liberalization ongoing, and broad-based public services. Other Latin American countries, like Peru and Mexico, fit this description and are too struggling to build coalitions to engage in tax reform post-liberalization to sustain the provision of public goods. This analysis thus provides insight for policymakers in these countries engaging in taxpayer education or reform services.

Existing research on tax preferences: who should carry the tax burden?

In advanced, industrialized democracies, support for progressive taxation is generally widespread (Edlund, 2003). Support for progressive taxation declines with increased income or education following the classical self-interest-based rationale (Barnes, 2015; Edlund, 2003; Heinemann and Hennighausen, 2015) and increases with the risk of unemployment (Barnes, 2015). Support for progressive taxation crucially depends on the perceived or actual benefits returned by the government, corresponding to the ‘paradox of redistribution’ (Korpi and Palme, 1998). More targeted welfare states achieve less redistribution because those who pay for it – the middle class and rich – do not receive benefits and therefore withhold support for redistributive policies (Brady and Bostic, 2015). Broad-based support for tax progressivity may equally require a social policy that provides positive returns to taxpayers (Berens and Gelepithis, 2019). This can be achieved through universal social protection programs (Korpi and Palme, 1998). As Beramendi and Rehm (2016) find, the progressivity of the tax and transfer system strongly determines the relevance of individual income as a driver of redistributive preferences and, particularly, redistributive preferences of the rich. Yet, fairness considerations do play a role and, as a result, inequality aversion can affect the impact of self-interest on tax attitudes (Lü and Scheve, 2016). Instances such as financial crises, which are blamed on capital, have raised demands for more progressive taxation (Limberg, 2019). Taxpayers are sensitive to inequality and care about a fair distribution of burdens, which, for instance, lead to the introduction of progressive income in exchange for the poor fighting in war (Scheve and Stasavage, 2016).

In developing and emerging economies, citizens are similarly supportive of tax progressivity and it is indeed the high-income earners and firms who form the ‘under-tapped’ tax base in Latin America (Fairfield, 2013). Income inequality is deemed to be unfair by the general public and the middle class in particular in this region (Cramer and Kaufman, 2011). But especially those who have the capacity to pay – that is, the rich – are hesitant toward progressive tax schemes when the state seems incapable of providing adequate returns (Berens and von Schiller, 2017; Flores-Macías, 2014). Often, firms are viewed as quite resistant to (all) taxes as it ‘threaten[s] their core interest in protecting their wealth’ (Fairfield, 2015: 27). In liberalized market economies, taxing firms can be even more difficult because of the mobility of capital and resulting competition to attract it (Abramovsky et al., 2014). Multinational firms are notorious for using accounting practices (e.g., transfer pricing) to avoid taxes (Malesky, 2015) and so increased multinational production in a jurisdiction does not necessarily translate to increased CIT receipts there (Bartelsman and Beetsma, 2003). Yet, firms can and do pay (some) taxes, especially under credible assurances of government benefits (such as investments in infrastructure or education) in return.

Existing research on globalization and policy preferences

Scholars provide ample evidence of the crucial impact of trade on citizens’ cost–benefit ratios and preferences for the provision of welfare or individual demand for social protections (Hays et al., 2005; Linardi and Rudra, 2020; Mayda and Rodrik, 2005; Schaffer and Spilker, 2016). Specifically, those who lose from free trade are aware of such trade-induced loss and demand protectionism (Mayda and Rodrik, 2005). For example, Armijo and Kearney (2008) discuss the active and diverse groups organizing for and against trade policies in Brazil including but not limited to business organizations, labor unions, and anti-globalization civil society groups (see also Campello and Urdinez, 2021). Survey evidence further corroborates that the public in Latin America views trade as a politically salient issue (Baker, 2003) and has opinions on the welfare impacts (see LAPOP, 2010). 4 An increase in risk exposure due to trade liberalization, such as increased occupational unemployment, also raises individual demand for more generous social policies in high-income countries (Walter, 2017). Governments can thereby influence public support for free trade through social policy instruments, especially in advanced democracies (Hays et al., 2005).

According to Wren and Rehm (2013), workers weigh the benefits of unemployment insurance against the costs of taxation, and often, they are concerned about losses in economic competitiveness when taxation increases (Wren and Rehm, 2013: 254). Further disaggregating the implications of trade openness to better determine who wins and who loses from trade, Walter (2017) illustrates for the high-income country context that returns to trade do not only depend on worker’s skill level, as Wren and Rehm (2013) promote, but also depend on the combination of sector-specific exposure to free trade and the individual’s skill level. She asserts that the high-skilled who work in the tradable sector (the trade winners in the Global North) are more likely to oppose redistribution in comparison with the low-skilled who are similarly exposed to global trade (Walter, 2017: 60). 5 Moreover, as Linardi and Rudra (2020) reveal in the case of India, the trade-winning rich discount trade benefits for some segments of the poor and respond with reduced support for redistribution given the lower ‘need’ for it. Globalization thus drives a wedge into the classic high and low-skilled group dynamics because trade exposure cuts across the different skill levels.

Our argument: crosscutting cleavages and tax burden attitudes among the poor

We expect support for tax increases to finance public goods to not only vary by personal costs and benefits through the respective tax but also by an individual’s exposure to trade openness-related prospective benefits and risks and the trade-induced gains and losses for others (e.g., firms). 6 Ultimately, we expect that the structural transformation of trade liberalization will foster broad support for more regressive taxes in emerging democracies because of inequality of trade gains among the poor.

We consider three major tax instruments used in developing and emerging economies: the PIT, CIT, and VAT. The tax burden is either placed relatively more on the lower social classes through the relatively more regressive impact of the VAT (Bird and Zolt, 2004), or higher social classes, through the relatively more progressive structure of the PIT or CIT. We argue that trade liberalization and its subsequent effect on wages, employment opportunities, profit, and prices will also influence support for taxes to sustain a much-needed universal social policy, depending on which source of tax is offered as instrument. The VAT entails larger costs for the poor, the PIT – when structured as a progressive tax – raises costs for higher income earners while the CIT shifts costs not only onto firms but also employees. Firms can pass costs onto employees via wage reductions, withholding promotions, and by reducing employment opportunities. While citizens may not have a perfect understanding of the distributive impact of different tax instruments, we assume that citizens have a general sense about the regressive nature of the VAT and the progressive nature of the CIT and PIT (see Castañeda, 2024 on tax fairness in Latin America; Berens and von Schiller, 2017).

Building on the interest-based logic, social class is expected to affect tax burden preferences for sustaining public goods (Meltzer and Richard, 1981). We argue that the poor would support levying additional tax money through relatively more progressive rather than relatively more regressive taxes compared with the rich (especially in countries with skewed income distributions, like in our survey sample in Brazil (Tornaghi, 2021), where the poor are more like to be aware of their status, all else held constant. 7 The poor are likely to consider it fair to ‘go where the money is’ (Fairfield, 2013), which is, in this case, capital and corporations. Following this interest-based logic, the VAT would be expected to be the least preferred tax option by lower social classes, and the relatively more progressive instruments, either the PIT or CIT, would receive more support. 8

We expect the context of trade liberalization will critically change preferences on who should carry the tax burden. Not all citizens are equally exposed to trade liberalization and its actual and potential economic consequences. In Brazil, the distributional impacts of trade and corresponding political cleavages for trade policies have been found to be sector-based (Armijo and Kearney, 2008; Kingstone, 2001). Especially following a North–South trade agreement (as is depicted in our survey vignette on the EU–Brazil pact), the distributional impacts should follow the Ricardo-Viner model. North–South trade continues to be based on comparative advantage and inter-industry trade patterns, not intra-industry trade patterns like in North-North trade (Madeira, 2016). Especially in the short run, factors are not highly mobile in Latin America (Goldberg and Pavcnik, 2007; Jamal and Milner, 2019). Thus, we assume welfare gains from trade correspond to comparative advantaged and disadvantaged sectors, following Campello and Urdinez (2021) and Jamal and Milner (2019). 9

Following the Ricardo-Viner model and prospect of upward mobility (POUM) theory, we argue that working in sectors that produce exportable goods, such as agriculture or manufacturing, raises the likelihood one would benefit economically from trade openness through higher wages, employment opportunities such as promotion or increased profits (see also Menéndez González et al., 2023). Anticipating economic benefits from a new FTA, workers expect upward mobility. 10 Following the seminal work of Benabou and Ok (2001), such POUM is closely linked to preferences on redistribution: an optimistic POUM is associated with less demand- and a pessimistic POUM is associated with more demand for redistribution (Linardi and Rudra, 2020).

An individual’s prospective change in their income with trade liberalization or a reduced demand for goods and services offered by the government could drive their tax preferences. If trade winners were driven only by less need or desire for public goods, then their tax preference for any tax would be low. Trade winners – driven by a reduced demand for public goods (because, for example, they can receive such benefits through the private sector 11 ) – will not have a clear preference for one tax or another, they would support low taxes for all taxes to fund public goods. In contrast, if the prospective income changes associated with free trade matter, as the POUM logic suggests, winners will prefer regressive taxes and losers will prefer progressive taxes. Trade winners should be less willing to support a tax increase on the ‘hands which feed them’ (in this case, corporations and firms). Accordingly, we argue that workers in such export-oriented sectors should be in favor of increases to the relatively more regressive VAT to sustain public goods and in opposition to CIT or PIT levies, as they are optimistic about their POUM. We assert that trade losers, still dependent on public goods, would undoubtedly be motivated by income changes and support more progressive taxation.

In addition, trade winners might favor the VAT because it is ‘export-friendly’. The VAT can be rebated on exports, while the PIT and CIT cannot. Following such, trade winners support the VAT over the PIT and CIT because of their desire to promote and support free trade; this trade boosts export industries and helps their individual POUM perceptions. The CIT, for example, is not tied to such advancement of free trade and exports.

Building on Hypotheses 1 and 2, the trade-losing poor would face similar incentive structures when formulating tax burden preferences to sustain universal welfare policies in a liberalizing economy: their social class and the corresponding interest-based logic complement their trade-losing status and pessimistic POUM. Thus, we argue the trade-losing poor are likely to support relatively more progressive tax instruments over relatively more regressive ones compared with the trade-winning poor.

Yet, looking at the trade-winning poor, crosscutting preferences emerge (see also Rehm et al., 2012 for a similar discussion of crosscutting determinants of welfare policy). Does the interest-based or POUM logic drive their tax burden preferences for sustaining broad-based welfare policies post-trade liberalization? Following the paradox of redistribution, more affluent citizens should remain willing to make tax contributions for social protection policies that are broad-based and provide benefits for the better-off as well (Berens and Gelepithis, 2019).

We argue that upward mobility expectations and prospects of gains in income associated with trade liberalization (H2) will overrule purely social class-based preferences on taxation (H1), especially because the taxation preferences are linked to funding a universal welfare policy, that is less prone to create distributive conflicts (Korpi and Palme, 1998). 12

Consequently, we expect that the trade-winning poor, as the biggest potential winners of the trade liberalization, are likely to be most supportive (compared with the trade-losing poor) of relatively more regressive tax instruments over relatively more progressive ones. Individuals can and do change their welfare state and taxation attitudes following macroeconomic changes (see Naumann et al., 2016).

We assert that the liberalizing, developing country context provides a different perspective and reality for the poor. In this scenario, some of the poor are big prospective winners and highly optimistic on their economic upward mobility when they work in the export-oriented sector. These trade-winning poor may be likely to oppose tax increases on corporations that would provide such employment opportunities post-liberalization relative to increases of the VAT. Ultimately, we argue that the trade-winning poor have high potential rewards from free trade and a highly optimistic POUM.

Survey design and methodology

To test our hypotheses, we explore variation in support for raising revenue through different types of domestic taxes to sustain the under-financed public health care system in liberalizing Brazil. Public health care in Brazil is based on a universal program, called ‘Sistema Único de Saúde’ (SUS). While coverage massively increased with the introduction of the SUS in the Constitution of 1988 and its reform in 1996, public budget deficits and economic downturn strain the public system (Funcia, 2019). Although everyone has access to the SUS, higher-income earners also have access to private insurance, so the poor are more reliant on the SUS. However, the rich do return to the SUS in cases of severe health needs, such as cancer treatment (Castro et al., 2019). Thus, all Brazilians have an interest in seeing the SUS in better shape.

We conducted a representative face-to-face survey in Sao Paulo State, Brazil, in August 2019. Sao Paulo State is the most populous state in Brazil, with a strong economic sector but also variation in income inequality, urbanization, and number of inhabitants (IBGE, 2018). Given our funding constraints, we chose Sao Paulo State for the survey because of the broad range of economic sectors and variation in productivity, which allows us to cover both potential winners and losers from the new FTA. However, Sao Paulo State is wealthier than other Brazilian states, so the share of the poor is smaller as compared with Northern Brazil, for instance. By choosing Sao Paulo State we put our argument to a conservative test as the poor are underrepresented.

The survey with 1,008 participants was collected by IBOPE based on probability-proportional-to-size-sampling, in which municipalities were randomly selected by taking into account the gender and age of the respondents (quota sampling). 13 The dataset is thereby adjusted to weights. 14 Interviewees were informed about the scientific nature of the survey and that participation was completely voluntary. 15 We employed several quality control mechanisms to ensure the validity of our measures (Lupu and Michelitch, 2018); see Supplemental Materials (SM) section A for further information.

First, we primed all respondents with information about the recent EU–Brazil FTA. All respondents received the following sentence: ‘After 20 years of slow-moving negotiations a new trade deal between the European Union and Brazil has finally been reached this June’. 16 We subsequently asked respondents how far they expect to benefit financially from the FTA to raise cognitive salience for the implications of trade liberalization (expected benefits).

We conducted an additional priming experiment on the economic benefits of this deal, which was meant to reinforce positive expectations of the FTA among those who consider themselves to be trade winners. This additional experiment and the statistical findings associated with it are detailed in the SM Section B. The priming experiment influenced respondent’s self-judgment regarding economic gains from the new FTA but did not affect public goods preferences that we studied with the subsequent tax vignette. This result could be because either the prime was too mild to influence individual attitudes, prior expectations on trade liberalization were already quite strong (and therefore not malleable), or the public was already primed to think positively about the FTA through media reports on the advancements of the new trade deal during the fielding of the survey in July 2019. As the priming experiment has no effect on our main DV, we report results with a control for this additional priming experiment. Estimation results which report sub-group findings by treatment and control group (and as interaction) are displayed in Figures S3–S7 in SM.

Given this primed context of trade liberalization in Brazil, we focus on analyzing the attitudes of different types of respondent groups (by social class, export-oriented vs import-competing sector workers, and a combined indicator distinguishing poor trade winners from poor trade losers) toward different types of tax increases to sustain universal health care. We conduct this analysis with a vignette experiment that varies the tax instruments, thereby studying heterogeneous treatment effects. All respondents received the following statement: The SUS grants all Brazilians access to health care, but the program suffers from budget cuts and economic recession. [The <tax type>] should be increased to generate higher tax revenues to better sustain the SUS. How much do you disagree or agree with this statement on a scale of 1 to 10, where 1 is totally disagree and 10 is totally agree?

The response to this question is the dependent variable in our main model predicting support for tax burden increases to sustain the SUS. We randomly varied PIT, CIT, and ‘tax on products that you buy in the shop’ (to comprehensively describe the VAT) with a simple randomization strategy (p = 1/3). Our independent variable is the randomly assigned tax type in the vignette. Using a vignette experiment instead of observational preference items on tax types allows us to rule out a range of biases that can occur in observational studies (e.g., adjusted response behavior in survey situation, survey fatigue following form repetition of similar questions, etc.).

Although tax instruments are randomized and, thus, the groups receiving the various tax instruments should be indistinguishable on covariates, we add standard control variables after estimating the baseline model to improve the accuracy of the point estimate. We include the respondent’s gender (female), age, urban residence (binary operationalization), and education in our statistical analyses. Adding a control for social trust (to account for horizontal reciprocity), perceived income situation and institutional trust (to factor in vertical fiscal reciprocity) does not change the substantive results (see Table S5 in SM). 17

We analyze (1) social class, (2) trade winner and loser status, and (3) a combination of social class and trade welfare status on tax preferences to sustain the SUS that were collected prior to the priming experiment and the survey vignette. First, to measure social class, we make use of a social class indicator based on the possession of assets (e.g., washing machines, cars, and refrigerators, see Critério de Classificaçáo Econômica Brasil, ABEP, 2018), living conditions (e.g., pavement of the street), and education status of the respondent and the spouse. 18 This additive indicator is rescaled into four social class categories: poor, lower middle class, middle class, and wealthy (ABEP, 2018). We selected this indicator because asset information has fewer non-responses and less response bias compared with income questions (Filmer and Pritchett, 2001). As a robustness check, we also make use of an alternative asset indicator based on principal component analysis (PCA) on asset items only to measure respondents’ wealth. 19 We also employ skill level as an alternative measure of class. Using education as a proxy for skill (see Ardanaz et al., 2013), we differentiate across high- (equal or above complete high school education) and low-skilled (incomplete high school and below) workers.

Second, our measure of trade winner-loser status relies on the sector in which the respondent works (following Ricardo-Viner) and, as a robustness check, an egotropic self-assessment of expected benefits following from the FTA. Respondents indicated their sector of employment from one of the following: agriculture, manufacturing, construction, commerce, transport/communication, services, social services, public administration, domestic services, or other. These sectors used in the empirical analysis represent the most fine-grained industrial category data available in the survey.

We then separate these sectors into export-oriented and import-competing categories. We rely on the Ricardo-Viner model assumptions that export-oriented sectors win under trade liberalization, while import-competing and non-tradable sectors do not. Exporting sectors in Brazil are agriculture, manufacturing, commerce, and transport/communication (World Trade Organization [WTO], 2019). Brazil’s top exports are primary products such as soybeans, sugar, meat, iron ores, and oil (WTO, 2019). With liberalization (and recent trade with the EU), Brazil has seen an increase in manufactured exports such as footwear and power generators (Hubbard and Fothergill, 2022; Moschini, 2022).

We acknowledge that more fine-grained sector data might reveal import-competing sectors within the broader sectors that we have information on for the survey respondents (for example high-technology manufacturing would be import-competing), yet we maintain that individuals working in the sectors identified here (such as manufacturing) have a relatively greater POUM because of the export-oriented nature of the broader sector in which they work (i.e., mobility within that sector for employment) and the broader gains for that sector with trade liberalization. All other sectors are either import-competing or not in the tradable sector and thus the respondents working in those sectors are considered to be relative losers under trade liberalization; the POUM is low for both such sectors (either because of expected losses in the import-competing sectors or because of the limited opportunities for any gains in the non-tradable sector). We exclude the ‘other’ category.

Third, and crucially, to account for both social class and the distributional impacts of trade, we combine the previous information on the respondent’s social class and sector of employment. For instance, individuals within each economic sector have relatively more to gain or lose depending on their social class. The poor who are employed in an export-oriented sector have more to gain with increased wages under liberalization, while the poor in an import-competing sector have more to lose in lost wages and the poor in the non-tradable sector do not have POUM either under trade liberalization (following Ricardo-Viner).

Given the structure of production in Brazil and individual social class factors, we argue that it is low-income earners in the export-oriented sectors who are the biggest winners from the FTA. We also assert that employment opportunities will result from the FTA. Therefore, the unemployed can ultimately make a big leap in their income (potentially going from unemployed to employed), so we consider them to also be big winners from the FTA. 20 In contrast, we consider respondents who are poor and working in import-competing sectors to be the biggest losers of the FTA. We create a similar indicator for skill instead of social class to test for robustness.

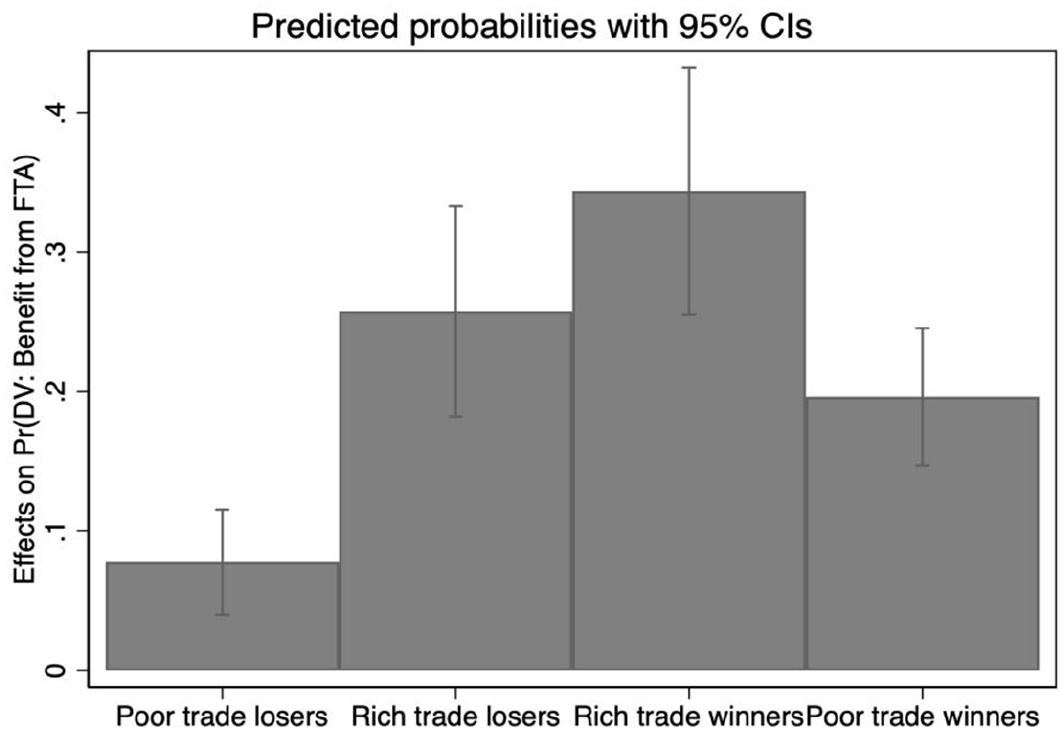

Finally, how do we know the respondents are motivated by egotropic welfare changes post-FTA and not broader macroeconomic or consumption changes? While we cannot rule out sociotropic expectations of our prime, we can test if our coded trade winners expect more personal benefits than the trade losers from the FTA. More specifically, we test the assumption that trade winners indeed expect economic gains from the new FTA with a simple logistic regression (for a detailed description, see SM Section B) on egotropic expected benefits. We find that the trade-winning poor are significantly more likely to see themselves as benefiting from the FTA compared with poor trade losers (see Figure 1). Notably, 40% of the poor trade losers expect to lose out from the FTA as opposed to 35% of the trade-winning poor. Only 8% of the trade-losing poor expect to benefit from the FTA, whereas 20% of the trade-winning poor express a clear expectation of increased gains. A t-test reveals a statistically significant difference (p-value < 0.001) in expected benefits from the FTA across the poor trade winners and poor trade losers. The estimates corroborate our assumption, but the empirical data also reveal that citizens struggle to derive economic implications from FTAs to their own financial situation, especially in this context, where the FTA was new and the consequences far from being realized. Some respondents misplaced themselves. After all, FTAs are complex macroeconomic policies which consequences are not perfectly predictable. This needs to be kept in mind when interpreting the results. Descriptive statistics are reported in Table E.

Predicted probabilities of trade winner/loser status on egotropic expected benefits from FTA.

Statistical model and results

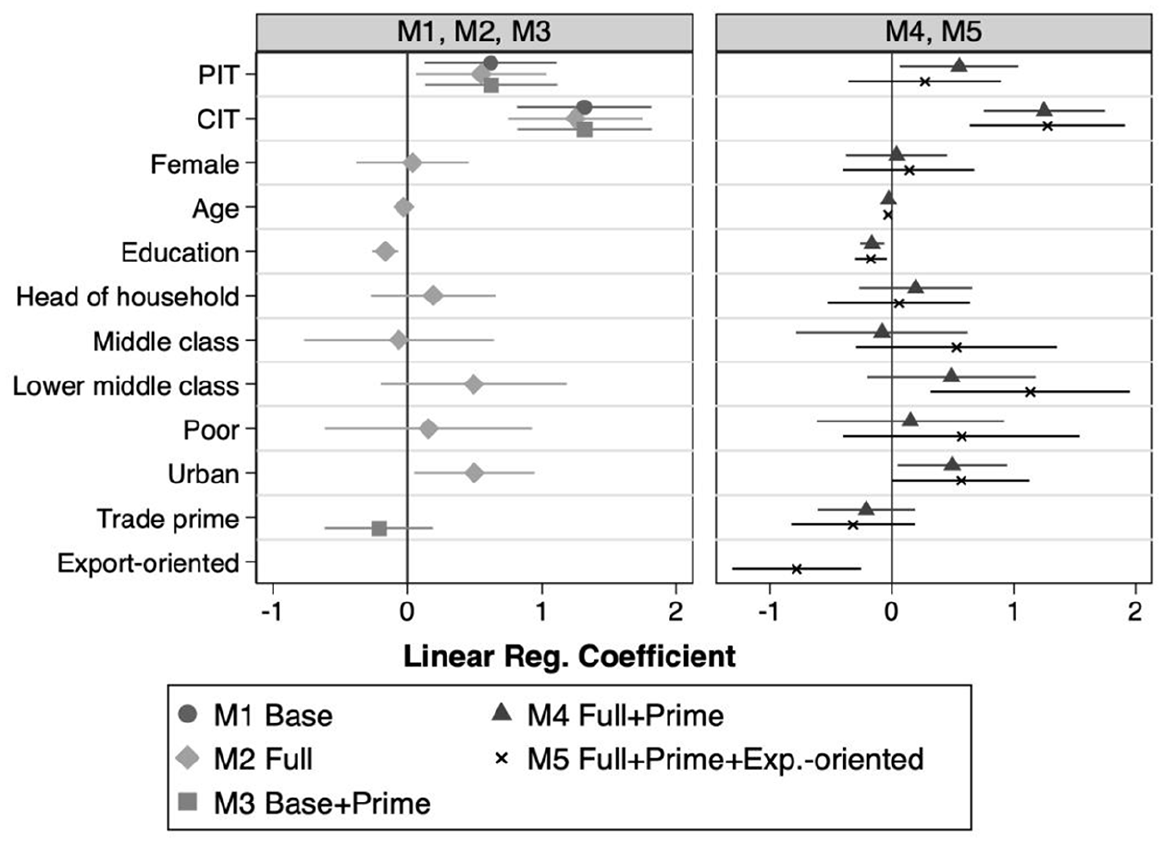

In order to analyze the tax vignette experiment, we use an OLS regression model predicting tax preferences to support financing for the SUS (the scale ranges from 1 – strongly disagree to 10 – strongly agree with a mean of 4.75 and a standard deviation of 3.29, see Figure S2 in SM). Unsurprisingly, the majority of respondents dislike a tax increase, but the opposition is most pronounced when the tax instrument is the VAT (40% ‘strongly disagree’, as opposed to roughly 30% for the PIT and approximately 20% for the CIT). The independent variable is the type of tax the respondent received in the vignette at random: CIT, PIT, and as the reference category, we use the VAT. We start with a baseline model analysis because of the randomization of the vignette. In subsequent estimations, we include additional control variables including a control for the trade benefits prime (1 = treatment, 0 = control).

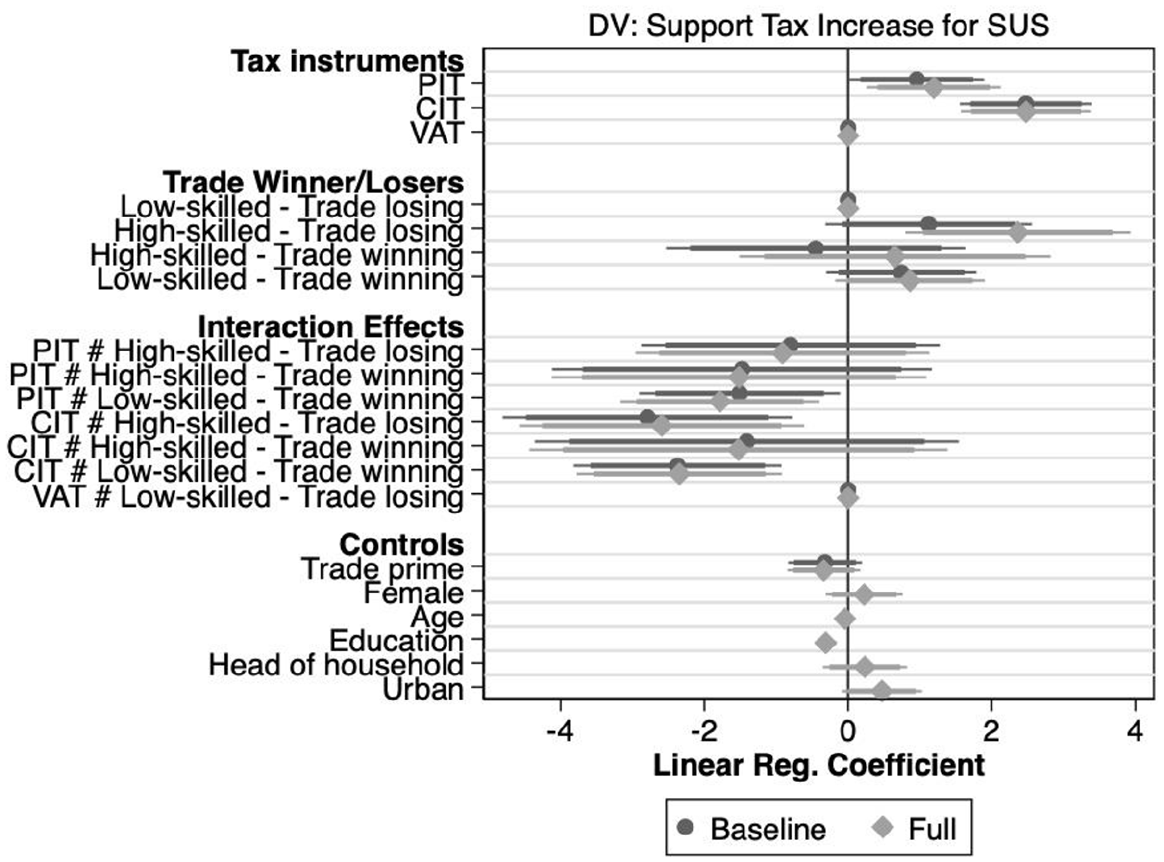

Figure 2 visualizes the estimation results of the average respondent before presenting heterogeneous treatment effects (see Table B in SM). Holding the VAT as the reference category, the average respondent is more willing to support a tax increase to sustain the SUS when the additional tax revenue is levied through tax increases on personal income or corporate wealth. While both the CIT and PIT are statistically significant, the magnitude of the CIT effect is larger compared with the PIT. Given Brazil’s history of corporate protectionism and tax breaks, support for taxing firms more among the public is unsurprising (Bastiaens and Rudra, 2018).

Coefficient plot: Support for tax increase for SUS for the average respondent (M1, M2) and priming experiment included (M3–M5).

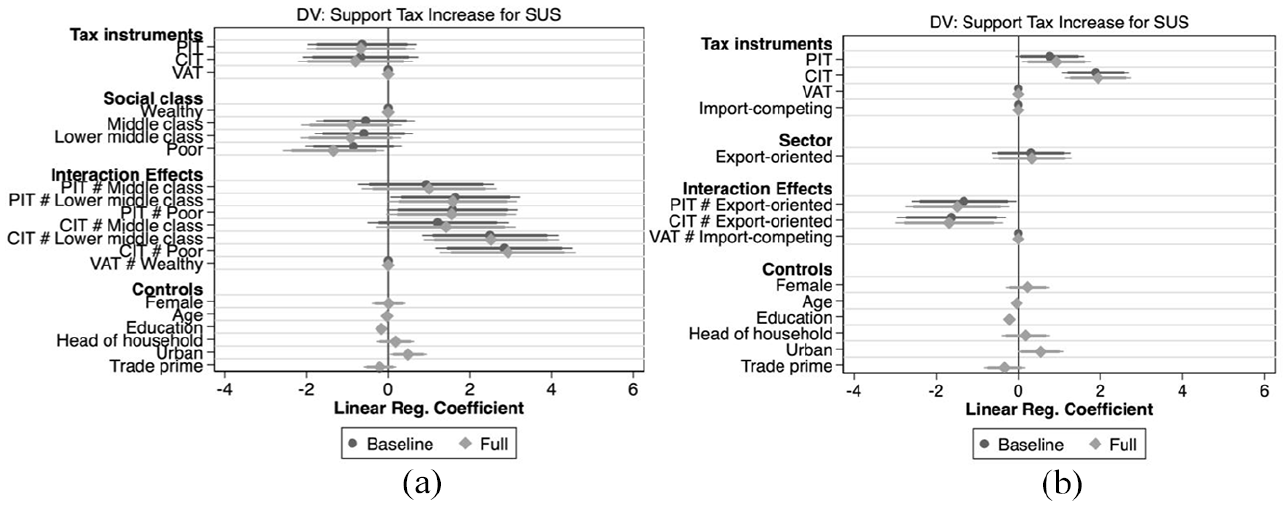

Figure 3(a) presents a coefficient plot of social classes and the corresponding tax type preferences to test H1 (estimation results are reported in Table D in SM). We find that the poor are more supportive of tax increases when the increase is financed through the PIT (coef. = 1.57) or CIT (coef. = 2.84) as opposed to the VAT, but the effect for the CIT is larger in size (Table C, Model 1, SM). Considering that the average support for the tax increase is 4.76, a unit change of 2.84 when receiving the CIT vignette is a substantive effect. The effect for the poor is statistically significantly different from the preferences of the wealthy, who oppose tax increases when levied through the CIT compared with the VAT. To test H2, we look at the impact of trade and its distributional effect on support for a tax increase to sustain the SUS. Figure 3(b) shows the coefficient plot for working in an export-oriented sector (dichotomous variable) and the corresponding tax type preferences (estimation results are reported in Table D in SM) in the fully specified model and a baseline model. We find that those who are working in an export-oriented sector (following Ricardo-Viner) are significantly less supportive of a tax increase when tax types vary between CIT (coef. = –1.63) and PIT (coef. = –1.33) as opposed to VAT. Trade winners might be driven more by reduced demand for public goods and not as much by prospective income changes. Trade winners possibly feel optimistic about opting out of the SUS for private health care and therefore do not support taxes to fund the SUS, regardless of the tax type (PIT or CIT). However, in support of our hypothesis, those who are in an import-competing sector are significantly more supportive of tax increases for the SUS when the increased tax revenue is levied from corporations as opposed to VAT (see average marginal effects, Figure E in SM). We also find a positive effect for PIT (coef. = 0.894, p = 0.035) for those in the import-competing sector, but the average marginal effect of CIT is twice the size (coef. = 1.934, p > 0.000).

Coefficient plot: Support for tax increase for SUS for baseline model (dark gray) and priming experiment + controls included (light gray diamond) among social classes (a) left panel (see Table C in SM) and among workers in the export-oriented versus import-competing sector (b) right panel (see Table C in SM).

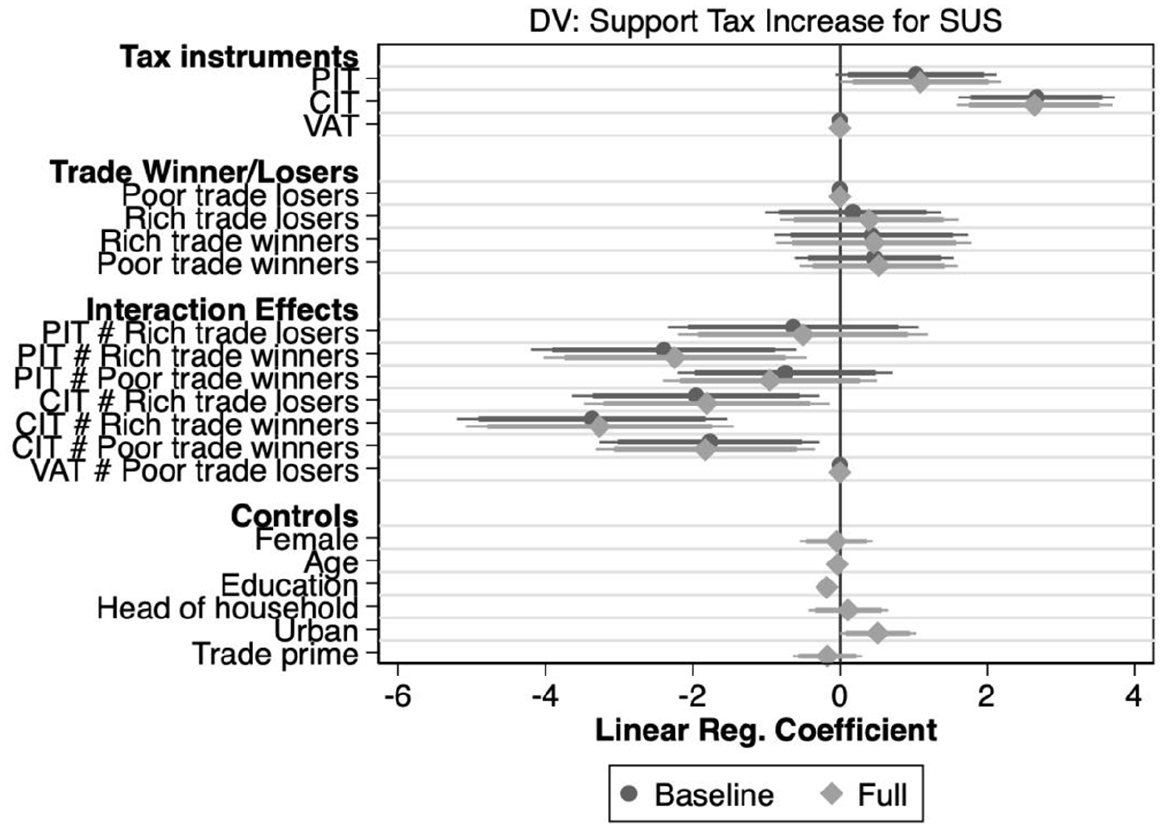

Finally, following H3, we explore the impact of the tax vignette for SUS financing support among respondents when distinguishing poor trade winners from poor trade losers. Recall that we expect the trade-winning poor to be in support of welfare state expansion when the instrument is the VAT compared with the CIT or PIT. In contrast, we expect the trade-losing poor to be in support of welfare state expansion when the instrument is the CIT or PIT compared with the VAT. Estimation results largely corroborate H3, see Figure 4 (Table E in SM; average marginal effects are displayed in Figure F in SM). Holding the VAT and poor trade-loser respondents constant, we see a statistically significant negative effect among the poor trade winners who received the CIT vignette (coef. = –1.77), this group representing the biggest winners from trade liberalization. 21

Coefficient plot: Support for tax increase for SUS for baseline model (dark gray) and priming experiment + controls included (light gray diamond) among poor trade winners and poor trade losers.

Using skill as an alternative for social class to acknowledge the importance of skill for trade preferences, we find support for our previous result. The low-skilled trade winners are significantly against a tax increase when the tax instrument is CIT (see Figure 5).

Coefficient plot: Support for tax increase for SUS for baseline model (dark gray) and priming experiment + controls included (light gray diamond) among low- and high-skilled trade winners and losers.

Testing the robustness of our findings, we make use of the egotropic measure on expected benefits from the FTA, although this measure comes with restrictions. We limit the model to the sample of the control group that was exempt from the prior priming experiment to receive unbiased estimates. 22 This reduces the sample to N = 456 (see Figure C in SM). Although the coefficient for the benefits-expecting poor is statistically insignificant, we do find statistically significant support for taxes to be increased for the non-expecting poor, if the instrument is the CIT (coef. = 1.789, p = 0.003), which confirms the divide across the poor. The reduced sample size might account for the weaker effects. In addition, what might explain the stronger finding for the poor who are reminded by our survey item that they lose out from the FTA is that losses loom larger than gains (Kahneman and Tversky, 1979).

As a further robustness check, we include the informal economy within our empirical analysis as that could be a determining factor of tax preferences (especially among the poor) or a proxy for the trade-losing poor as informal workers do not pay PIT, can potentially evade the VAT, and are less likely working in export-oriented firms. First, we estimated an interaction of tax type and informality status of the respondent (measured by a self-reported lack of a working card), 23 and the results were statistically insignificant (available upon request). Second, we created an indicator for those respondents working in the informal or formal economy and export-oriented or import-competing sector. Respondents working in the informal economy who are trade winners (i.e., in the export-oriented sector) are significantly against tax increases of the CIT (coef. = –3.836, p = 0.021) compared with the VAT (note that this is a small group of individuals in our sample; see SM Section 1, Figure D). Informal workers are also sensitive to the trade-winning/losing status of their sector of employment and reveal preferences similar to the trade-winning poor: they do not prefer to shift the tax burden onto the PIT which they do not pay (coef. = –2.787, p = 0.070). Hence, our results for the poor also extend to the economically vulnerable.

Discussion

Countries in the Global South are struggling to pursue ‘hard’ redistribution because they lack an electoral majority to support such welfare state reforms (Holland and Schneider, 2017). Our findings corroborate this observation and reveal a much-overlooked cleavage and possible obstacle from the revenue side: that among the poor. In liberalizing, developing economies, the poor are not a homogeneous group, they are divided into trade winners and losers. The poor who are also losing out from free trade hold relatively more progressive tax preferences and favor the tax instrument of the CIT to improve social protection. Yet, poor trade winners hold the opposite view: they oppose improvements of the universal health care system when this means placing a greater tax burden on corporations. Universal social policies, which are particularly beneficial for the most vulnerable groups in the population, the low-income earners, thus lack support from those that they are meant to protect most. Instead, poor trade winners may form cross-class coalitions with the rich in opposing relatively more progressive taxation.

These findings echo work by Orgeira Pillai et al. (2024) that points to the ‘complex politics of taxation in times of crises’ (p. 3) and, in particular, how broad support for progressive taxation may be fleeting under changing economic conditions. Our contribution is that in addition to factors such as fairness (Fairfield, 2013), service delivery (Jibao and Prichard, 2015), and international forces (Sanchez, 2006), support for tax progressivity depends on individual perceptions of upward mobility during or after globalization. Objective measures of trade-winning and losing status (social class/skill, occupational sector, and labor informality) yielded stronger results than the measure of self-identified expected benefits (which was tested on a reduced sample size). The mechanism might therefore run through a more diffuse prospect of gains rather than through purely egotropic economic expectations associated with the FTA. Our empirical data also revealed that respondents struggle to perfectly derive economic consequences from an FTA as the economic consequences were not felt yet in Brazil at the time of the survey. Following our empirical findings, however, a better understanding of these gains and losses in the population is likely to create even more polarization among the poor. Further research on the implications of individual understanding of the sources of economic prospects for fiscal preferences poses an interesting avenue of future research.

One limitation of our study is that the survey experiment is bound to the Brazilian context. Of course, the universal SUS health care system in Brazil can be compared with the former Seguro Popular (now INSABI) in Mexico. However, many other developing countries instead rely on contribution-based or means-tested social policies, if any social protection is provided at all. Many developed countries, on the contrary, do have such universal health care systems. In that regard, Brazil represents an important and critical case to explore with implications for understanding social and fiscal policy preferences across some emerging and many developed economies.

Supplemental Material

sj-docx-1-gsp-10.1177_14680181241246769 – Supplemental material for Divisions among the poor: A survey experiment of tax preferences in liberalizing Brazil

Supplemental material, sj-docx-1-gsp-10.1177_14680181241246769 for Divisions among the poor: A survey experiment of tax preferences in liberalizing Brazil by Sarah Berens and Ida Bastiaens in Global Social Policy

Footnotes

Acknowledgements

We thank Franziska Deeg, Clara Baues, and Facundo Salles Kobilanski for research assistance on the collection of the survey data. We would like to thank Andy Baker, Lucy Barnes, Pablo Beramendi, Matthew Carnes, Patrick Emmenegger, Ana Isabel López García, Xabier Garcia Fuente, David Hope, Hanna Lierse, Julian Limberg, Ari Ray, Damien Räss, Laura Seelkopf, and Alice Xu for critical feedback. The article has been presented at the Workshop ‘The Politics of Taxing the Rich’ November 2020, at the SPSA conference 2021 in Bern, and at REPAL 2021.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The project is funded by the Deutsche Forschungsgemeinschaft (DFG, German Research Foundation) – Project number 374666841 – SFB 1342.

Information on IRB and pre-analysis plan

IRB approval was obtained from the German Association for Experimental Economic Research e.V. on July 9, 2019 (No. 92AR1Pyh) and from the University of Cologne on August 19, 2019 (Reference: 19019SB). The hypotheses were pre-registered on EGAP as predictions 14 and 15 in the PAP 20190724AC, project 2.3.

Availability of data

The survey data are available from the repository Harvard Dataverse: doi:10.7910/DVN/Z8FSNR.

Supplemental material

Supplemental material for this article is available online.

Notes

Author biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.