Abstract

The article challenges the universal assumption in the literature that corporate tax rates constrain growth-aspiring entrepreneurs. The strength of financial intuitions may be a stronger predictor of growth aspirations than corporate tax rates. With the support of strong financial institutions, countries possessing norms supportive of individual success and risk-taking will lead growth-aspiring entrepreneurs to persist in the face of corporate tax rate increases. For countries with weak financial institutions, it does not matter whether norms are supportive or not of individual success and risk-taking behaviour; entrepreneurs do not have the means to grow their enterprises and thus do not show a strong response to corporate tax rate increases. This argument is supported by an analysis of 394 country-year observations for 77 countries from the GEM and World Bank databases. The study contributes to understanding the contextual conditions required for growth-aspiring entrepreneurs to overcome tax constraints and, more broadly, formal institutional constraints. Our qualifying condition in performance-oriented norms points to the importance of informal institutions in promoting entrepreneurial resilience and persistence. This also points to the importance of the interdependency between formal and informal institutions when explaining economic behaviour.

Introduction

Growth-aspiring entrepreneurs may not be satisfied with owning small businesses; they wish to own large and successful companies. Across the globe, how they respond to adverse circumstances – in this instance, the burden posed by corporate tax rate increases – is of practical and scholarly importance. Psychological perspectives recognize them as a resilient group of ambitious individuals who are likely to be undeterred by adverse circumstances in their environment. This led us to question the universal assumption in the literature that corporate tax rates constrain growth-aspiring entrepreneurs.

Current literature argues that for new ventures to grow, they must not be severely constrained by legal and regulatory systems (Nyarku and Oduro, 2018). Within this formal system, taxes play a significant role (Block, 2016; Shirokova and Tsukanova, 2013). Compared to large established firms, the costs due to high corporate tax rates will disproportionately burden young firms (Fogel et al., 2006). For example, Asoni and Sanandaji (2014) provide evidence indicating that entrepreneurs will abandon their growth aspirations. In addition, Bowen and De Clercq (2008) controlled for corporate tax rates in their study on the effect of the institutional context on entrepreneurial growth aspirations; their results showed a negative sign for tax rates. Notably, both these studies comprised small samples – a cross-section of at most 40 countries – represented by mainly wealthy economies with high availability of financial resources.

In addition to our concern about the limited samples used in prior research, we remain concerned about omitting psychological perspectives characterizing growth-aspiring entrepreneurs as resilient and ambitious (Bullough and Renko, 2013; Stam et al., 2011). Although tax burdens exacerbate the risk of growing one's new venture, the subset of growth-aspiring entrepreneurs is likely less risk-averse. Characteristics such as personal ambition and risk averseness can be represented by performance-oriented (PO) norms (Stephan and Uhlaner, 2010). From an institutional theory perspective, such norms have been recognized as informal institutions (North, 1991). Considering the financial resources required for firm growth, financial institutions also have a significant role to play (Autio et al., 2013). Strong financial institutions extend entrepreneurial career opportunities to people lacking personal or family wealth and may raise a country's growth-aspiring share of entrepreneurs. This leads to our argument that in the presence of strong financial institutions underlying high availability of financial resources for growth-aspiring entrepreneurs, strong PO norms will lead growth-aspiring entrepreneurs to persist in the face of increases in corporate tax rates. Thus, we do not expect a universally strong negative of corporate tax rates on a country's growth-aspiring share of entrepreneurs.

We test our argument on 394 country-year observations for 77 countries from the GEM and World Bank databases. Our sample includes countries with a wide range of institutional contexts, which allows us to increase the variance available for each of our study's explanatory variables: tax rates, performance-oriented norms and financial resource availability. In addition, changes in the context of a single country and subsequent changes in an entrepreneur's aspirations can be detected by the data's longitudinal attributes. We assume entrepreneurs with growth aspirations have the option to change their expectations from ‘growth’ to ‘no growth’ when the state increases tax rates, which gives rise to a lesser share of entrepreneurs with growth aspirations.

In societies with high levels of financial resources, our findings support our argument that PO norms promote the persistence of aspiring entrepreneurs’ growth amid corporate tax rate increases. This study contributes to an understanding of the contextual conditions required for growth-aspiring entrepreneurs to overcome tax constraints and more broadly, formal institutional constraints. Our qualifying condition – PO norms – points to the importance of informal institutions in promoting entrepreneurial resilience and persistence (Bullough and Renko, 2013; Delmar et al., 2003; Holland and Garret, 2015). We go beyond the common assumption that entrepreneurs use mainly economic logic to develop their response to formal institutions such as corporate taxation (e.g., Asoni and Sanandaji, 2014). This also points to the importance of the interdependency between formal and informal institutions when explaining economic behaviour. Contextual influences are processed jointly and not independently in the mind of growth-aspiring entrepreneurs; a mechanism also being increasingly recognized by entrepreneurship scholars who use institutional theory (Estrin and Prevezer, 2011; Estrin et al., 2013; Krasniqi and Desai, 2016; Puffer et al., 2010; Stephan et al., 2015). We commence with institutional theory and our hypotheses, followed by our methods. We then describe our findings and discuss our contributions.

Corporate taxation and entrepreneurial growth aspirations

The growth aspirations of entrepreneurs can be defined as their goal to expand their young firms (Delmar and Wiklund, 2008). These aspirations manifest in different ways because entrepreneurs across the globe have a wide range of needs and face different contextual influences. A contextual influence that may disproportionately burden young firms is corporate taxation (Fogel et al., 2006).

Approaches to corporate taxation are shaped by institutional forces: ‘the humanly devised constraints that structure political, economic and social interaction. They consist of both informal constraints (sanctions, taboos, customs, traditions and codes of conduct) and formal rules (constitutions, laws, property rights)’ (North, 1991: p97). The institution arises from shared expectations of actors to conform to rules or norms. The violation of an institution results in an external sanction (Helmke and Levitsky, 2004).

Corporate taxation is applied formally by governments and is therefore regarded as a formal institution (Spencer and Gomez, 2004). Economic perspectives suggest that expected returns have a strong positive influence on the entry of growth-oriented entrepreneurs. As an institution, corporate tax rates constrain this economic behaviour. They reduce these returns and thus raise the costs and the risks of entrepreneurial growth behaviour (Darnihamedani et al., 2018). Notably, entrepreneurs may use these returns to finance their growth endeavours (Henrekson and Sanandaji 2011). Overall, an increase in corporate taxes has been shown to have a negative effect on growth-oriented entrepreneurship (Asoni and Sanandaji, 2014; Bowen and De Clercq, 2008; Venâncio et al., 2020). For this reason, entrepreneurs in countries that increase corporate tax rates are likely to abandon their growth aspirations. Accordingly, we hypothesize:

The moderating role of PO norms

Formal corporate taxation rules can limit entrepreneurs’ belief that firm growth may result in rewards of personal financial success and personal achievement. But, considering a wide range of country contexts, we do not expect entrepreneurs to abandon their growth aspirations at the same rate. In many countries, entrepreneurs adapt to their institutional context (van Stel et al., 2007; Acs et al., 2008). Growth-oriented entrepreneurs have been recognized as a resilient group of ambitious individuals (Bullough and Renko, 2013; Holland and Garret, 2015; Stam et al., 2011), which raises doubts about whether they abandon their growth aspirations in a prohibitive institutional context. If personal ambition is the norm in such societies, decision-makers will likely emphasize individual success (Holland, 2011; Kahneman and Miller, 1986; Shah and Higgins, 1997). Because they are used by society to judge individual behaviour, norms form part of informal institutions.

Societal norms conducive to personal ambition may include PO norms that support personal achievement (Stephan and Uhlaner 2010), personal initiative, risk-taking, creativity and innovativeness and individual responsibility (Hopp and Stephan, 2012). The importance of personal achievement, personal initiative and innovativeness has been supported by research on growth-oriented entrepreneurship (Cassar, 2007; Davidsson, 1989). They have a non-linear relationship with small firm growth (Kreiser et al., 2013). Beyond a certain threshold, innovativeness and personal initiative appear to be positively related to firm growth; below a certain point, risk-taking seems to be positively associated with firm growth. Specifically, when encumbered by financiers and other suppliers at the beginning stages of growth, entrepreneurs may also appreciate the independence that growth and resultant financial success brings (Davidsson, 1989).

In PO norms, one finds an essential informal institution that does not constrain behaviour involving efforts to achieve individual success and taking personal risks to achieve this success. Part of risk-taking consists in taking on activity with prohibitive costs. One must be confident that one can make returns that exceed the costs. In nations with strong PO norms, we expect the growth-aspiring share of entrepreneurs not to decrease as steeply as in countries with weak PO norms when corporate tax rates increase. Accordingly, we hypothesize:

The moderating role of financial resource availability

But, up to now, we have omitted a vital component of entrepreneurs’ confidence in their growth aspirations: their ability to mobilize the required resources for their growth projects (Autio et al., 2013; Liao and Welsch, 2003). Financial resources are particularly salient (Fraser et al., 2015). Whitley (1999) argued that a country's financial system is an essential formal institution for proving credit and capital to facilitate economic behaviour.

Even with the support of strong PO norms, growth aspirations are of little use in an economy with few financial resources. Thus, we expect the strong interaction effect between PO norms and tax rates to be present mainly under high levels of financial resources. In countries with low levels of financial resources, this interaction effect is weak, which means that corporate tax rates’ impact on growth aspirations does not differ much between weak and strong PO norms. Accordingly, we hypothesize:

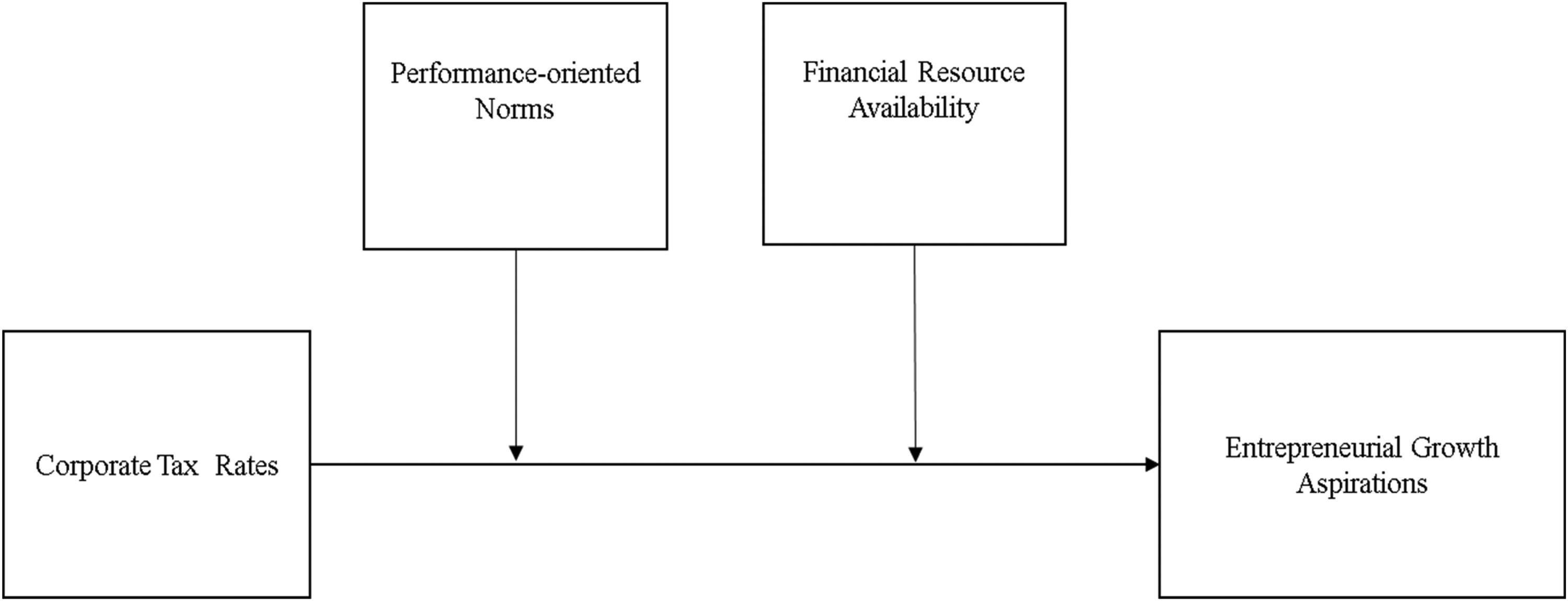

From the above hypotheses, we need to analyze entrepreneurial responses to increased tax rates for both PO norms and financial resource availability. Consequently, we arrive at a model in which the effect of corporate tax rates on entrepreneurial growth aspirations is moderated by PO norms, which is moderated by financial resource availability. This is illustrated schematically in Figure 1.

Conceptual framework.

Method

Overview of the sample and data sources

We collated data from GEM and World Bank databases on 77 countries 1 from 2005 to 2015. This dataset comprised 394 country-year observations, with 196 developed and 198 developing country-year observations. Developing countries were classified by the World Bank's Low-Income, Lower-Middle-Income and Upper-Middle-Income Economies. Our evenly spread distribution of developed and developing country contexts ensured our sample represented a variety of economic and social circumstances experienced by growth-aspiring entrepreneurs.

From the GEM panel, we collected data on job growth expectations, cultural practices and the availability of finance. GEM data comprised annual country-level measures computed as national averages (Reynolds et al., 2002). GEM collected over 2000 adult-population responses per country per year. A separate survey provided data from about 36 expert interviews per country per year. National experts, consisting of at least one entrepreneur, two suppliers and an observer, such as an academic with expertise in a specific area, provided their views about the entrepreneurial framework conditions (EFCs) in participating countries. The survey assesses the experts’ views on the institutional environment through standardized questions and validated measurement scales. The aggregation of the expert survey is from the mean of 36 expert responses per country. Finally, the World Bank Doing Business database collected data on each nation's per capita domestic product, per capita growth, regulatory burdens and total tax rates.

Among others, the EFC measure identifies financial support, policy and regulatory condition and cultural and social norms as essential conditions for entrepreneurial activity. GEM measures each with multiple-item scales comprising three to seven questions. The standard expert survey contains 88 questions, with responses collected on a five-point Likert scale: Completely false (1), Somewhat false (2), Neither true nor false (3), Somewhat true (4) and Completely true (5). We weighted the multi-item scale with the factor loadings of individual scale items.

Dependent variable

We measure growth aspirations by a nation's early-stage entrepreneurs with job growth expectations as a proportion of the entire population of early-stage entrepreneurs: those with growth and ‘no growth’ expectations (Levie and Autio, 2011). We assume if a nation increases corporate tax rates, entrepreneurs with job growth expectations will change their expectations from ‘growth’ to ‘no growth’, giving rise to a lesser proportion of total early-stage entrepreneurs with job growth expectations.

Specifically, entrepreneurial growth aspirations were operationalized by the proportion of total early-stage entrepreneurial activity (TEA) who expect to employ at least five employees five years from now. The TEA index measures the proportion of a country's population aged 18–64 either in the start-up phase or managing/owning a business less than 42 months old. GEM also asks each new entrepreneur to estimate the number of people they expect to employ within five years. From this, it determines the number of entrepreneurs who expect to hire at least five employees.

Explanatory variables

Corporate tax rates

This served as our primary explanatory variable. To measure the tax rate of each country, we used data from the World Bank Doing Business project. The project measures the total effective tax rate, which includes government-mandated costs paid by corporates into both state accounts as well as private accounts for workers' compensation and pensions. Value-added tax and that withheld on behalf of employees are not included.

To get to this effective tax rate, the World Bank uses the notion of commercial profit. To compute conventional profit before tax, many of a firm's taxes are deductible. However, these taxes are not deductible when computing commercial profit (PWC, 2016). Essentially, commercial profit is the profit when adding back both taxes paid into national state accounts and those government-mandated payments into other non-state accounts such as workers’ compensations, pensions run by the private sector and municipal taxes.

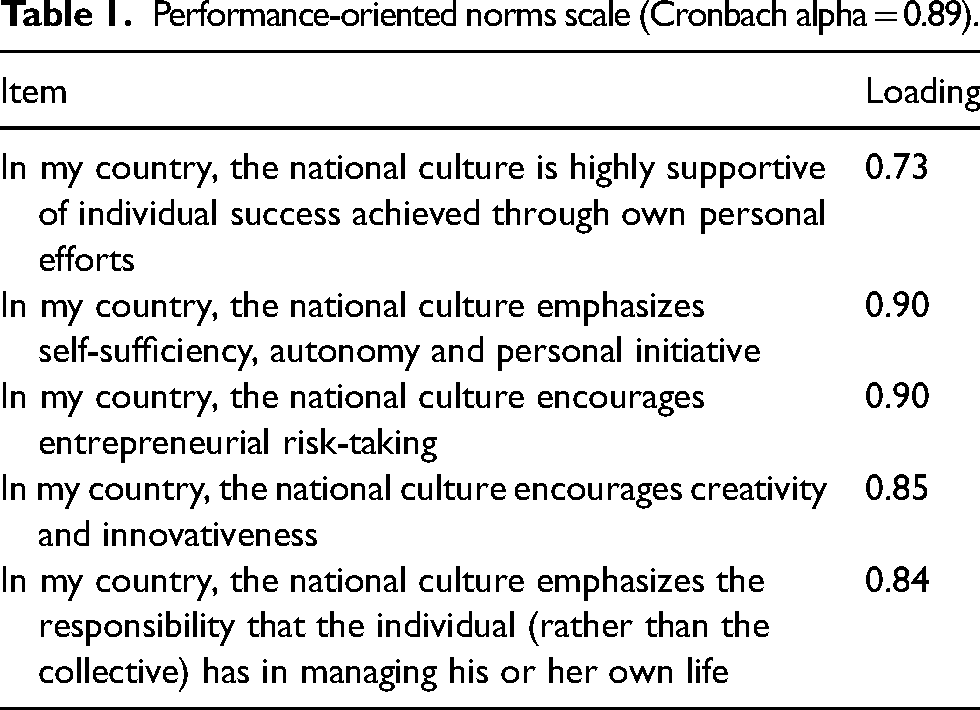

Performance-oriented norms

This served as our primary moderating variable. Norms represent the shared understanding of behaviour within a society. We operationalized them through GEM's cultural and social norms EFC (see Table 1). This probes expert perceptions about the extent social and cultural practices approve of individual choices to make their effort to succeed and take personal risks that could lead to new business methods or activities. Essentially, this GEM EFC can represent societal approval of individual performance. To illustrate, one of the five items in the EFC scale's cultural and social norms asks experts to respond: ‘In my country, the national culture is highly supportive of individual success achieved through personal efforts’. In this five-point scale, low values indicated success practices that remained socially embedded.

Performance-oriented norms scale (Cronbach alpha = 0.89).

Notably, this EFC also has an item of independence and self-sufficiency, which may seem contrary to growth (e.g., Douglas, 2013). However, while a small firm struggles with internal controls when it grows, at the same time, it begins dealing with a broader set of customers, suppliers and lenders and reduces its dependence on any single stakeholder (Davidsson, 1989).

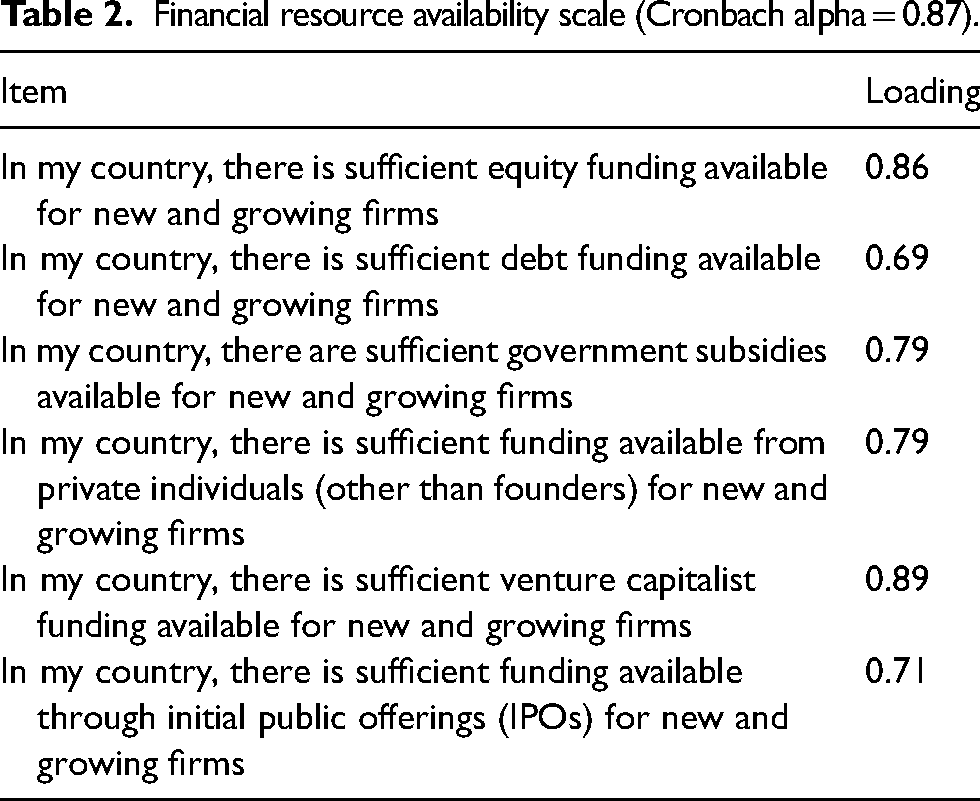

Financial resources availability

We chose the GEM EFC on the availability of finance for entrepreneurs (see Table 2). The GEM measure is comprehensive in it captures various financial sources from government, private individuals and financial markets. We recognize differences in financial resources as also indicative of differences in the capacity of entrepreneurs to procure skilled human resources and other technological-type resources.

Financial resource availability scale (Cronbach alpha = 0.87).

Control variables

We included control variables to increase the robustness of our models. Previous research on growth aspirations used our primary predictor variable – corporate tax rate – as a control (Bowen and De Clercq, 2008). Since our dependent variable pertains to entrepreneurs’ aspirations of high employment growth, a higher rate of growth of domestic output would be expected to support such motivations (Bowen and De Clercq, 2008). Therefore, we controlled for a country's GDP growth and used the lagged value of real GDP growth to prevent potential reverse causality. These data were extracted from the World Bank's World Development Indicators database.

We also controlled for per capita GDP, representing many differences in country contexts. For instance, we attempted to control for tertiary education enrollment per country available from the World Bank, and we established it was correlated strongly with GDP. Individuals with higher education are likely to have higher aspirations stemming from an ability to spot growth opportunities and the self-confidence to manage a large enterprise (Davidsson, 1989).

Data analysis

Due to the panel structure of the data, standard applications of ordinary least squares regression were unsuitable for this study. Ordinary least squares regression assumes observations are independent, but with panel data, observations are linked by repeat observations of entrepreneurs from the same country across time. If these linkages are not addressed, they will be transferred into the error term, resulting in biased and inconsistent coefficient estimates. Therefore, we used specific panel regression techniques to test the significance of the three-way interaction between tax rates, performance-oriented norms and financial resource availability.

To test whether the coefficients estimated in both random and fixed effects models are the same, we used a Hausman-like test of fixed versus random effects: the Stata xtoverid command (Schaffer and Stillman, 2006). Unlike the Hausman version, the xtoverid test enabled us to use the coefficients of the cluster-robust panel regression. Following the test, we found that fixed and random effects were similar, so we chose random effects. Finally, we used panel-clustered robust standard errors to control for serial correlation and group-wise heteroscedasticity.

Given the importance of the interaction effects, we consider the consequence of introducing multiplicative interaction terms into my models. The full three-way interaction model included all main effects and two-way interaction terms (Cohen et al., 2013). Bearing in mind our hypothesis on the nature of the interaction, the significance of the interaction term also signalled the importance of examining the particular interaction further. We, therefore, plotted the simple slopes (Dawson and Richter, 2006) to examine the nature of the interaction.

Results

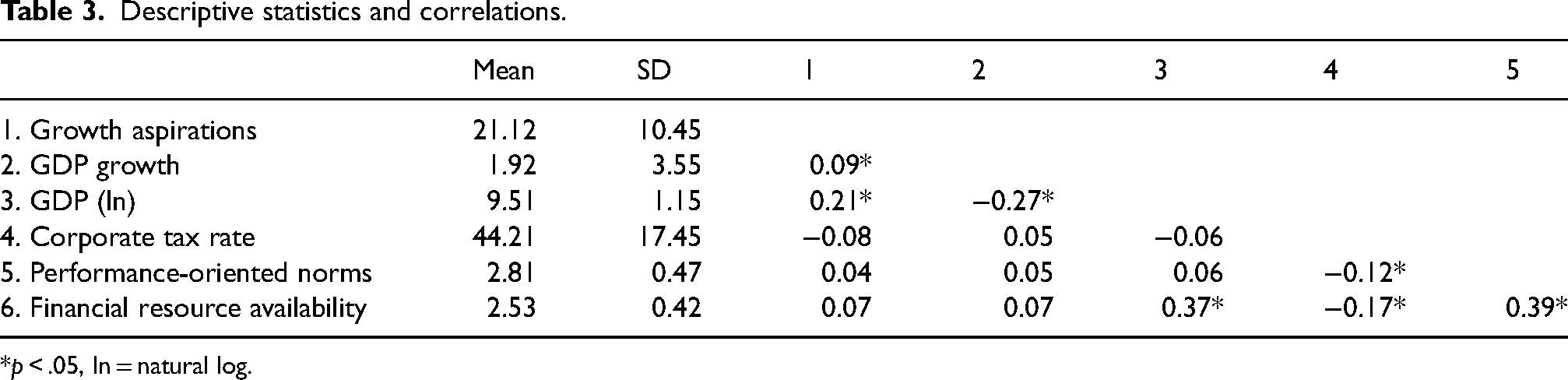

Table 3 illustrates the variables’ means, standard deviations and pairwise correlations. Poor discriminant validity is indicated by the pairwise correlations above .85 (Kline, 1993), leading to multicollinearity problems. We did not find high collinearity between our independent variables. Multicollinearity causes estimation problems when independent variables are highly correlated with one another, not when they are highly correlated with a multiplicative interaction term (Dalal and Zickar, 2012). Notably, the Stata software also omits severe collinear terms from a model.

Descriptive statistics and correlations.

*p < .05, ln = natural log.

Nevertheless, we followed convention in management journals by mean-centering all variables before the interaction terms were created (Aiken and West, 1991). Both total and individual item variation inflation factors were well below the recommended value of 10 (Hair et al., 1998). Our values were less than five.

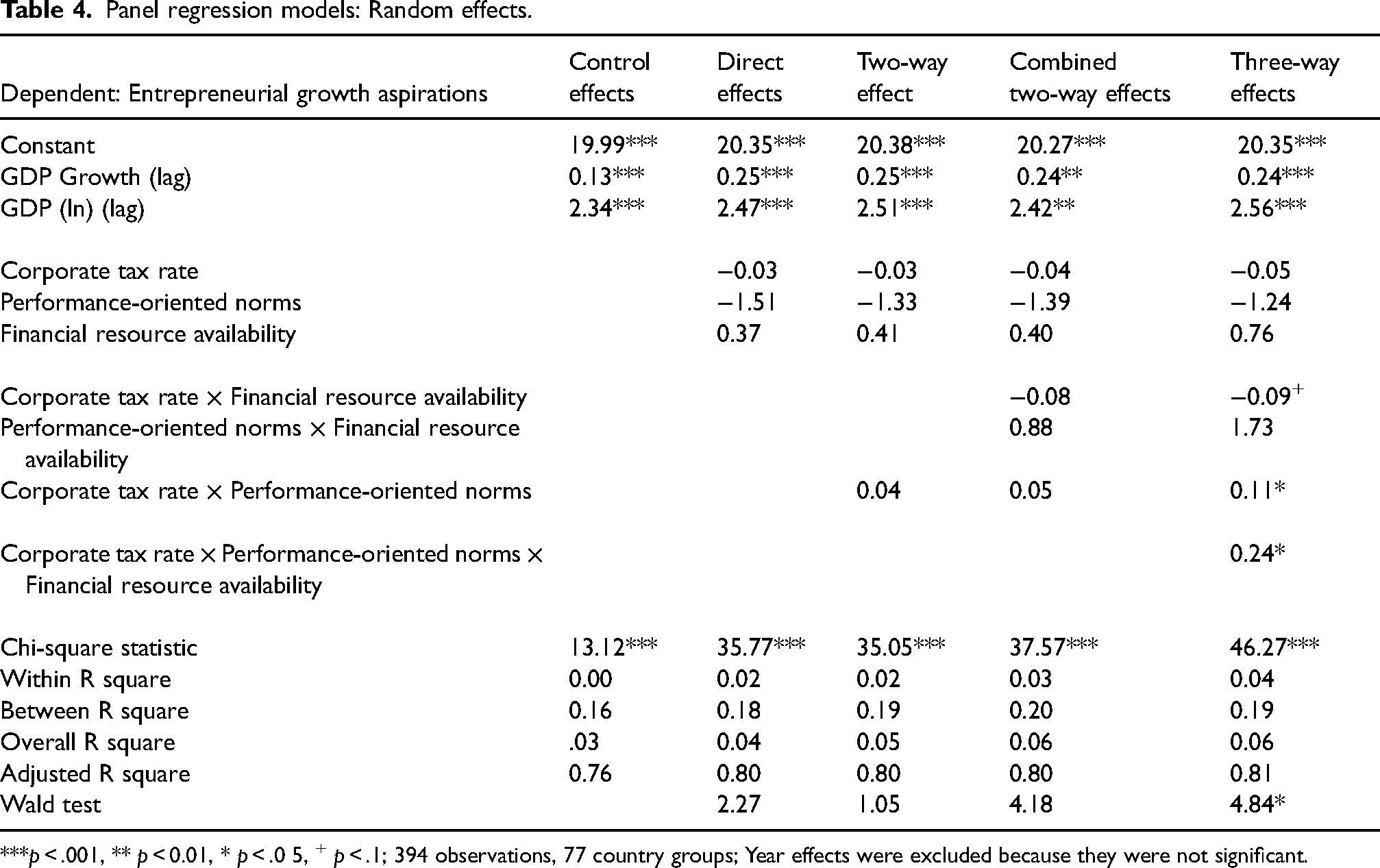

Table 4 presents the results of our panel regressions. Although we follow convention and present control, direct and interaction effects in stages, we wish to draw attention to recent arguments that the full three-way interaction model shows the true effects of all our variables. According to Aguinis et al.'s (2016), the ‘three-way interaction’ model, unlike the ‘direct effects’ and two-way interaction models, accommodates the expected real-world changes in their effects at different levels of one another. They advise scholars to test a direct effect for any predictor in the full interaction model when that predictor interacts with a moderator variable. Their argument becomes particularly evident when one tests for an antagonistic interaction, where an increasing moderator effect reverses the sign of the predictor that would have been estimated in a direct effects-only model. Also, note due to its inclusion with the interaction terms, the statistical insignificance of a lower order variable does not mean it lacks practical effect on the dependent variable (Braumoeller, 2004).

Panel regression models: Random effects.

***p < .001, ** p < 0.01, * p < .0 5, + p < .1; 394 observations, 77 country groups; Year effects were excluded because they were not significant.

From the ‘three-way effects’ model in Table 4, we note the direct effect of tax rates was not significant (b = −0.05, p > 0.1). Notably, the sign of this effect is negative, which confirms our practical expectations. However, hypothesis 1 was not supported.

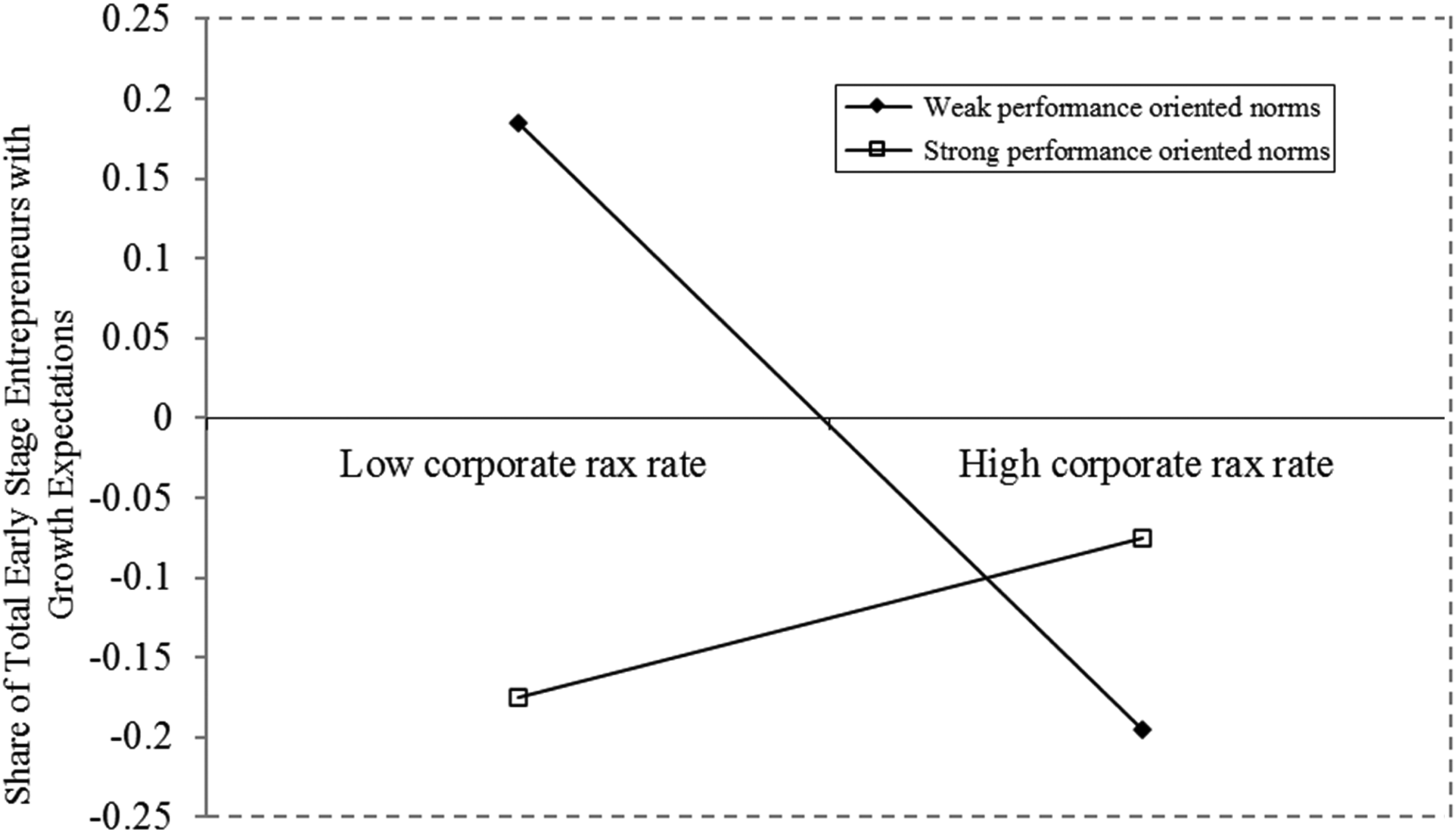

Our hypothesis 2 suggested that PO norms moderate the negative relationship between tax rates and entrepreneurial growth aspirations such that the negative relationship is stronger for individuals from societies with weak PO norms. Again, from the ‘three-way effects’ model in Table 4, we note the interaction effect between tax rates and PO norms is significant (b = 0.11, p < 0.05). As depicted in Figure 2, this interaction confirms that the negative relationship is stronger for individuals from societies with weak PO norms. The significance and nature of our two-way interaction between tax rates and PO norms support Hypothesis 2.

Simple slopes: Two-way interaction between corporate tax rate and performance-oriented norms.

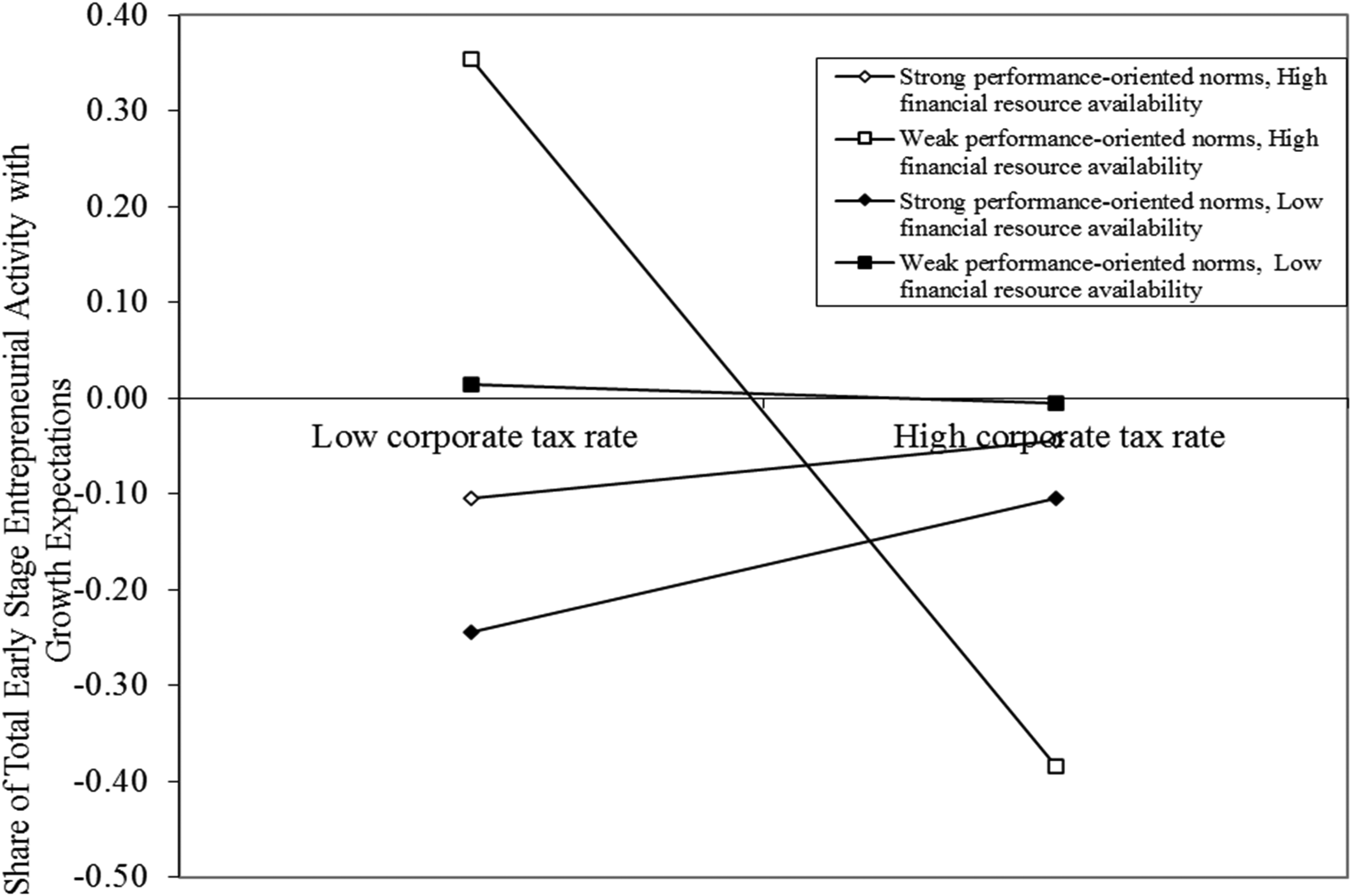

Hypothesis 3 suggested that financial resource availability moderates the combined effect of corporate tax rates and PO norms on entrepreneurial growth aspirations. This combined effect is weaker when financial resource availability is low than when it is high. As a result, for low financial resource availability, we can expect the large differences in the strength of entrepreneurs’ negative response to reduce to a minimum. The ‘three-way effects’ model in Table 4 shows that the interaction effect between tax rates, PO norms and financial resources availability is significant (b = 0.24, p < 0.05). This interaction, as depicted in Figure 3, confirms that the large differences in entrepreneurs’ negative response strength reduce to a minimum for low financial resource availability. Together, the significance and nature of our three-way interaction between tax rates, PO norms and financial resources availability lend support to Hypothesis 3.

Simple slopes: Three-way interaction between corporate tax rate, performance-oriented norms, and financial resource availability.

Finally, we ran robustness checks. Specifically, we tested our model with perceptions of corporate taxation instead of actual tax rates. We used GEM's Regulations EFC, which covers the administrative burden and the associated compliance costs. This EFC includes an item: ‘In my country, the amount of taxes is NOT a burden for new and growing firms’. We also tested the model with regulatory burdens more broadly, using the World Bank's survey of business leaders’ perceptions of the burden of government regulations. When we substituted these measures for our actual tax rate measure, we arrived at similar patterns to those shown in our simple slope graphs.

We also conducted a matching procedure that estimates the average treatment effect of corporate taxation by regression adjustment. All the remaining variables appearing in our regression models served as controls. We arrived at the negative sign for the corporate taxation effect, but this was not significant at the 5% level. The corporate taxation effects in all our original random effects models were also negative but not significant. We also used the two-way interaction between corporate tax and performance orientation as a treatment effect and reached a significant effect at the 5% level. Similarly, the three-way interaction between corporate tax, performance orientation and financial resources availability was also significant.

Discussion and conclusions

We questioned the universal assumption in the literature that corporate tax rates constrain growth-aspiring entrepreneurs. Instead, we argued that in the presence of high availability of financial resources, strong PO norms would lead growth-aspiring entrepreneurs to persist in the face of increases in corporate tax rates. Our literature review revealed arguments based on the assumption that entrepreneurs use economic logic to develop their response to corporate taxation and that they are unlikely to tolerate such burdens (Asoni and Sanandaji, 2014). Nevertheless, we remained concerned about omitting psychological perspectives characterizing growth-aspiring entrepreneurs as resilient and ambitious (Bullough and Renko, 2013; Davidsson, 1989; Stam et al., 2011). With growth-aspiring entrepreneurs depicted as ambitious, we wondered if they might take in their stride the burdens posed by increases in corporate tax rates. At a country level, we put forward PO norms as a societal or institutional indicator of ambition. We found that we cannot view tax rates in isolation for corporate tax rates negatively affecting a country's growth-aspiring share of entrepreneurs. The effect of tax rates on growth aspirations had a strong negative effect when PO norms were weak: for example, when the local society does not support individual success and risk-taking, when PO norms are supportive of entrepreneurial ambition, entrepreneurs remained undeterred by increases in corporate tax rates: the negative slope was less steep than that under conditions of weak PO norms.

But we remained concerned about omitting the importance of financial resources for enterprise growth (Autio et al., 2013). We thus tested the effect of financial resource availability as an essential condition for the interaction between tax rates and PO norms. We found this to be significant. The tax rate and PO interaction were strong only under conditions of high levels of financial resource availability.

Contributions and implications

Apart from understanding the phenomenon of a country's growth share of entrepreneurs, we contribute to institutional theory by clarifying how formal and informal institutions interact. To understand differences within and across countries of growth-aspiring share of entrepreneurs, a focus on tax rates limits us to formal institutions and responses arising from economic logic. At an individual level, arguments abound that psychological perspectives characterize growth-aspiring entrepreneurs as resilient and ambitious (Bullough and Renko, 2013; Davidsson, 1989; Stam et al., 2011). At a societal level, this psychological view can be represented by informal institutions. We chose PO norms to represent informal institutions because these norms are supportive of individual ambition and may accommodate formal constraints (Helmke and Levitsky, 2004). Increasingly, it is being recognized that the effect of formal institutions is contingent on informal institutions (Smallbone and Welter, 2012; Aparicio et al., 2016). Formal institutions coexist with informal ones, and often the design of formal institutions is influenced by prevailing informal institutions (Helmke and Levitsky, 2004; Williamson, 2000).

Our qualifying conditions reveal entrepreneurs’ ambitions in response to the adverse circumstance brought about by corporate tax rate increases, likely to build on entrepreneurial resilience and persistence conversations (Bullough and Renko, 2013; Delmar et al., 2003; Holland and Garret, 2015). Specifically, our qualifying conditions reveal that entrepreneurs from strong PO societies and those from poorly resourced contexts are indifferent to increases in the burdens posed by corporate tax rates. Strong PO norms instill, in entrepreneurs, personal ambition and the will to persist despite adversity (Holland, 2011; Shah and Higgins, 1997).

We confirm that the motivation-related assumptions of the institutional theory appear to hold when resources are highly available (Autio et al., 2013; Fraser et al., 2015). Resource considerations and financial institutions more narrowly play an essential role in theorizing institutions’ incentive mechanisms (Barney et al., 2011; Stephan et al., 2015).

Finally, to promote growth-oriented entrepreneurship, policymakers may strengthen performance-oriented social norms by celebrating and promoting the success of entrepreneurs behind outstanding enterprise growth. This might take the form of awards delivered by the state and a media intervention to communicate the story of the successful entrepreneurs who might have created several hundred jobs during their journey. Social norms may also be influenced by education policy. Cases of high-growth enterprises can be included in the business syllabus. Notably, all these efforts must be accompanied by improving the entrepreneurs’ access to financial resources. Strong financial institutions extend entrepreneurial career opportunities to people lacking personal or family wealth, helping policymakers reach out to more individuals.

Limitations and further research

Our study has the following limitations. First, we have operationalized entrepreneurship growth aspirations with job growth expectations. But unlike prior research, our analysis does not limit high growth expectations to a minimum of 20 employees expected over five years. We measure growth expectations more generally by using publicly available GEM data on the percentage of TEA who expect to employ at least five employees five years from now. McKelvie and Wiklund (2010) have argued the choice of growth measure represents a different type of growth that may or may not reflect growth represented by other metrics. This must be tested in future research using different thresholds of job growth and the operationalization of growth in sales and profitability.

Second, our PO norms data are from impressions of experts rather than ‘hard’ data. Even though the process proposed by the model appears to work at the population level, it needs to be tested to determine whether different patterns might be observed when using longitudinal individual-level data. Researchers may wish to replicate our study using individual-level desires.

Third, we did not control employee tax. Entrepreneurs may likely persist with their growth aspirations, mainly when corporate tax rates are substantially below personal income tax rates (Haufler et al., 2014). Returning to paid employment and high personal income tax rates is not a favorable alternative to those growth-aspiring entrepreneurs facing difficulties in their environment. We recommend that future work in this area control employee tax.

Readers will also note from our pairwise correlations (Table 3) that financial resource availability is positively related to GDP but negatively related to tax rates. Notably, higher GDP has been used to indicate higher stages of economic development. Although we treat tax rates and access to finance independently, future studies might explore this collinearity between these variables. For instance, one might explore whether countries with higher tax rates may be less developed, and therefore, have less developed financial institutions. Finally, further research will also do well to test models that control for cultural acceptance of non-compliance or levels of tax avoidance prevalent in a country. These factors may also affect whether the tax rate presents a barrier to growth.

Conclusion

The effect of corporate tax rates on a country's growth-aspiring share of entrepreneurs is contingent on the country's performance-oriented norms. Strong performance-oriented norms equate to celebrating individual success over group success. But considering that growth-aspiring entrepreneurs require resources to implement their plans, this strong interaction between corporate tax rates and performance-oriented norms exists mainly in countries with high financial resource availability. The interaction does not exist in countries with low financial resource availability. Given the rapid changes in contemporary business environments, we hope this research stimulates further investigations into explaining individual differences in responding to environmental cues as it goes through these changes.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.