Abstract

Unrecorded alcohol is defined as alcohol that is consumed but not registered in official statistics for sales, production or trade (Lachenmeier et al., 2021; Rehm et al., 2014; World Health Organization, 2018), sometimes referred to as “non-commercial alcohol” (Adelekan, 2008). While data on recorded alcohol can be retrieved from official statistics, the level of unrecorded alcohol can only be estimated with a substantial degree of uncertainty. For the World Health Organization's European Region, unrecorded alcohol per capita consumption in 2016 was estimated to be 1.8 L per adult aged 15 years and above, accounting for almost 20% of total adult per capita consumption (World Health Organization, 2018; see also Probst et al., 2019). Hence, unrecorded alcohol accounts for a substantial share in total per capita consumption in Europe, thereby contributing significantly to alcohol's significant health burden (Shield et al., 2020).

There are different types of unrecorded alcohol, including legally produced but untaxed alcohol, alcohol products recorded but not in the jurisdiction where consumed, surrogate alcohol, illegal homemade artisanal production, and illegal production or smuggling of alcohol (Lachenmeier et al., 2021; Rehm et al., 2014). The first group – legally produced but untaxed alcohol – falls under an European Union (EU) legislation that allows the production of alcohol products for personal use (Council Directive 92/83/EEC, 1992; Council Directive (EU) 2020/1151 of 29 July 2020 Amending Directive 92/83/EEC on the Harmonization of the Structures of Excise Duties on Alcohol and Alcoholic Beverages, 2020). This tax exemption is part of a series of special regulations on the minimum excise tax rates of commercially produced alcohol set by EU law. These special regulations further include reduced tax rates for small independent producers (e.g., reduced rates for annual production volumes below 200,000 hL for beer and 20 hL for spirits) and a tax rate of zero for low strength alcohol products (e.g., for low-strength beer: zero tax rates in Denmark and Sweden for beer with alcohol content <2.8%, and in Ireland and Spain for beer with alcohol content <1.2%) (European Commission, 2022).

As EU Member States have the freedom to adopt special provisions for small producers, the extent to which legally produced but untaxed alcohol contribute to unrecorded alcohol within Member States may differ across countries. To date, there has been little research interest in this type of alcoholic product, and it remains largely unknown to the scientific community how Member States act within this legal framework. In this report, we therefore provide an overview of the legal framework of legally produced but untaxed alcohol among EU Member States. For this purpose, we have reviewed the national excise duty legislations to identify relevant tax exemptions for the production of alcohol for personal use and complemented this search by an alcohol expert mapping survey.

Methodology

Review of national excise duty legislations

We searched national excise duty legislations to identify tax exemptions for alcoholic beverages for all 27 EU Member States. Specifically, we conducted an online search to identify national legal texts specific to alcohol production and distribution on national legislative databases and the websites of the Ministries of Finance for each individual Member State and screened them for information on tax exemptions referring to personal use. All text passages detailing exemptions from the standard regulation of alcohol taxation were of interest. If no indication for tax exemptions for personal or professional use were identified in the relevant legal texts, secondary documents were consulted for validation, if available. These were identified through an additional online search using search terms such as “tax exemption” and “alcohol for personal use”.

Alcohol expert mapping survey

An online alcohol expert mapping survey was developed to collect additional information on the extent and legal framework of legally produced but untaxed alcohol in EU Member States. The mapping survey followed an online workshop on unrecorded alcohol conducted as part of the “Alcohol Harm – Measuring and Building Capacity for Policy Response and Action” (AlHaMBRA Project) in June 2021. The questions were developed based on the experiences shared in the online workshop and discussions within the project consortium and author group. The final mapping survey consisted of five sections asking for the following: (1) information about the expert's professional background; (2) the two most important types of unrecorded alcohol in the expert's country; legally produced but untaxed alcohol from (3) non-professional and (4) professional producers; and (5) personal views on needs for EU action on untaxed alcohol in the expert's country (for the full survey, see Supplementary information).

We invited workshop participants, alcohol researchers and representatives from EU Member States with expertise in the field, including members of the former EC-run Committee on National Alcohol Policy and Action (CNAPA) group, to respond to the survey. As workshop participation was not limited to EU Member States, alcohol experts from associated countries were also invited (e.g., Iceland, Norway). On 4 April 2022, 72 experts with 1–3 experts per EU Member State received an email invitation to participate in the online survey. Data were collected between 4 April and 3 May 2022. Participation in the survey was voluntary and respondents were able to stop the survey at any time. Respondents were given full information on the purpose of data collection and the use of their data.

Data analysis

The results of the review and the alcohol expert mapping survey were summarised descriptively. Further details and all supporting references can be found in the Supplementary information. In cases where no conclusive information on national excise duty legislations was identified, this has been indicated. With regard to the alcohol expert mapping survey, no account was taken of reports on wine (n = 1), which is not taxed in several EU Member States but is not of interest for the current investigation.

Results

Legal regulations for the production of alcohol for personal use

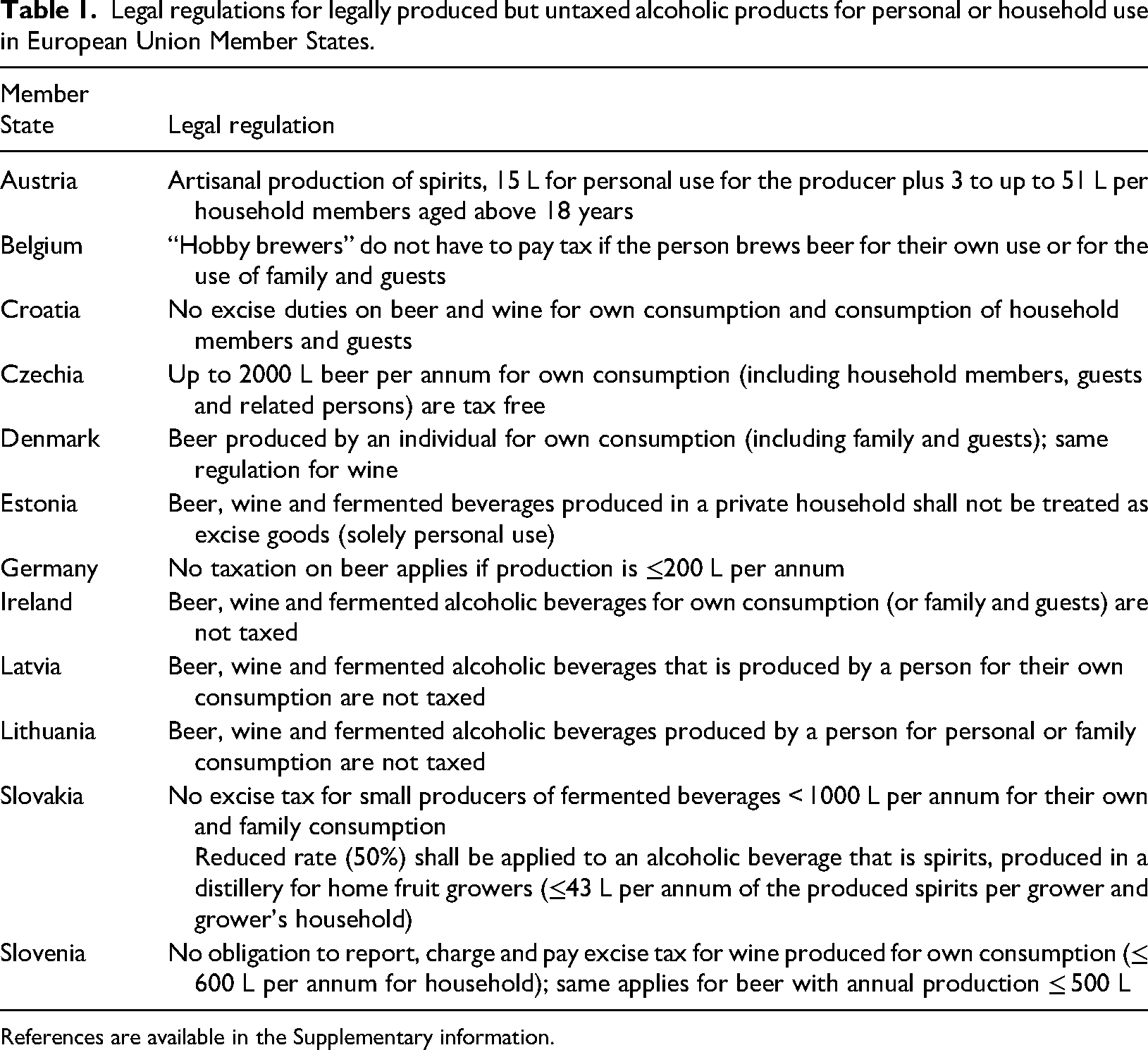

We identified legal information on tax exemptions for the production of alcohol for personal or household use in 12 of 27 EU Member States (see Table 1). The most common alcoholic beverage concerned was beer (9 out of 12 countries), followed by wine (8 out of 12 countries). Spirits were covered in only one country (Austria), where the artisanal production of spirits up to 15 L for personal use is tax exempt.

Legal regulations for legally produced but untaxed alcoholic products for personal or household use in European Union Member States.

References are available in the Supplementary information.

Most countries have not defined a certain volume as an upper threshold for tax exemption. These countries have merely stipulated that no excise duties apply to alcohol produced for personal or household use. Only four countries established maximum quantities for artisanal or personal production, which vary substantially (Austria: ≤ 15 L of spirits for personal use, Germany: ≤ 200 L of beer, Slovakia: < 1000 L of fermented alcoholic beverages, Slovenia: ≤ 600 L of wine and ≤ 500 L of beer).

No sufficient information on legal exemptions were identified in Bulgaria, Cyprus, Finland, France, Greece, Hungary, Italy, Luxembourg, Malta, the Netherlands, Poland, Portugal, Romania, Spain and Sweden (see Supplementary information).

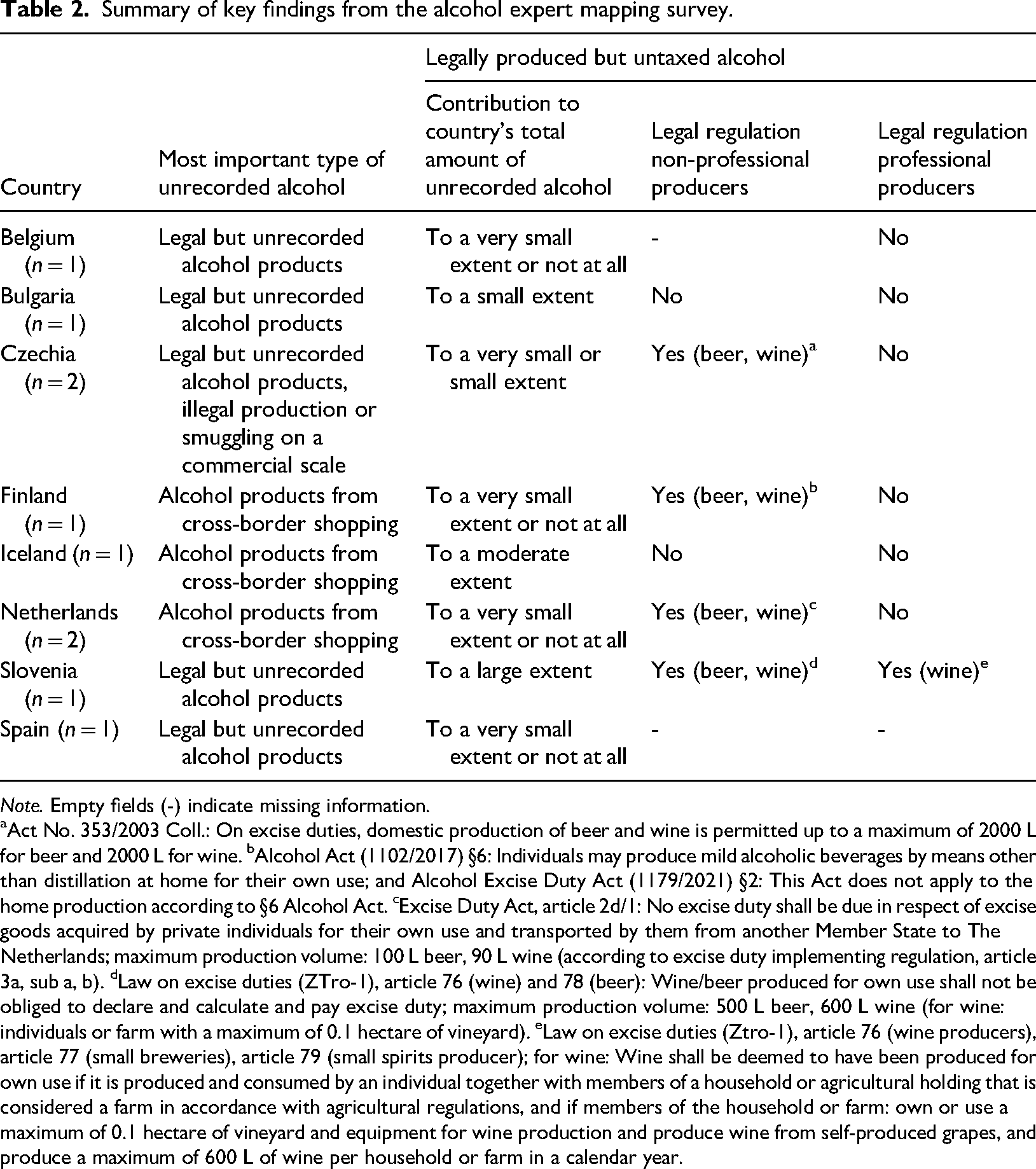

Participation in the alcohol expert mapping survey

In total, 10 alcohol experts from seven EU Member States (Belgium, Bulgaria, Czechia, Finland, the Netherlands, Slovenia, Spain) plus Iceland completed the online mapping survey. The majority of experts have worked on alcohol-related topics for at least four years. Key findings of the mapping survey are depicted in Table 2.

Summary of key findings from the alcohol expert mapping survey.

Note. Empty fields (-) indicate missing information.

Act No. 353/2003 Coll.: On excise duties, domestic production of beer and wine is permitted up to a maximum of 2000 L for beer and 2000 L for wine. bAlcohol Act (1102/2017) §6: Individuals may produce mild alcoholic beverages by means other than distillation at home for their own use; and Alcohol Excise Duty Act (1179/2021) §2: This Act does not apply to the home production according to §6 Alcohol Act. cExcise Duty Act, article 2d/1: No excise duty shall be due in respect of excise goods acquired by private individuals for their own use and transported by them from another Member State to The Netherlands; maximum production volume: 100 L beer, 90 L wine (according to excise duty implementing regulation, article 3a, sub a, b). dLaw on excise duties (ZTro-1), article 76 (wine) and 78 (beer): Wine/beer produced for own use shall not be obliged to declare and calculate and pay excise duty; maximum production volume: 500 L beer, 600 L wine (for wine: individuals or farm with a maximum of 0.1 hectare of vineyard). eLaw on excise duties (Ztro-1), article 76 (wine producers), article 77 (small breweries), article 79 (small spirits producer); for wine: Wine shall be deemed to have been produced for own use if it is produced and consumed by an individual together with members of a household or agricultural holding that is considered a farm in accordance with agricultural regulations, and if members of the household or farm: own or use a maximum of 0.1 hectare of vineyard and equipment for wine production and produce wine from self-produced grapes, and produce a maximum of 600 L of wine per household or farm in a calendar year.

Contribution of legally produced but untaxed alcohol to unrecorded alcohol

According to the expert's assessment, legally produced but untaxed alcohol products were the most important type of unrecorded alcohol in five out of eight countries, followed by cross-border purchases of alcohol. The latter was considered to be particularly important in Finland, Iceland and The Netherlands. The illegal production or smuggling of alcohol on a commercial scale was pointed out by one expert in Czechia. Although legally produced but untaxed alcohol was the most frequently reported type of unrecorded alcohol, its contribution to the total amount of unrecorded alcohol was considered to be small in most jurisdictions. Only in Iceland and Slovenia did this type of alcohol account for a moderate and large share, respectively.

Country-specific tax exemptions within the EU legal framework

According to the expert's reports, no tax exemption exists for the professional or non-professional production of alcohol for personal use in Bulgaria and Iceland. However, in Czechia, Finland, The Netherlands and Slovenia, beer and wine can be produced by individuals for their own consumption without being taxed. A maximum production volume is defined in Czechia (2000 L per annum for beer and wine), The Netherlands (100 L for beer, 90 L for wine) and Slovenia (500 L for beer, 600 L for wine), but not in Finland. While such an exemption does not seem to exist for professional producers in these countries, farmers with a vineyard of 0.1 hectare or less and a wine production volume of a maximum of 600 L per annum are also exempt from alcohol excise tax in Slovenia.

Experts’ opinion on actions to be taken by the European Commission

In the final section of the survey, the experts were invited to express their views on what the EU can do to support Member States lowering the burden of unrecorded alcohol in their countries. Three key areas for action were indicated by the experts: (1) revising the current pricing regulations, including an increase in excise duties on alcoholic beverages in general and the introduction of a minimum excise tax on wine, and the imposition of minimum pricing; (2) strengthening the legal framework on alcohol cross-border trading; and (3) improving the monitoring of unrecorded alcohol within the EU.

Discussion

The EU has established a legal framework on alcohol taxation defining beverage-specific minimum excise taxes for all Member States. However, at the national level, exemptions to this regulation exist for alcohol that is produced for personal use. In this report, we provide an overview of the formal regulation of legally produced but untaxed alcohol in EU Member States. Tax exemptions for the production of alcohol for personal use were identified in 14 Member States, concerning mostly the production of beer and wine. Maximum production volumes were defined in some but not all countries, with pronounced variations in the production limit.

For interpretation, three major limitations need to be accounted for. First, not all countries provide English versions of their law texts online and we used multilingual neural machine translation services (Google Translate, DeepL Translator) to translate documents not available in English. These automatically generated translations are susceptible to translation errors that may have prevented us from capturing all relevant information. Second, the number of experts who completed the mapping survey is relatively low and, in most countries, only one expert participated. A greater representation of countries and multiple experts per country would have been beneficial to enhance the scope and validity of our mapping survey. Third, it is beyond the scope of this study to establish the extent to which the regulations and limits on personal use were enforced, limiting the degree to which conclusions can be drawn for public health. Case studies seem to be most appropriate for examining law enforcement in specific countries.

How is untaxed alcohol for personal use produced? Three different possibilities seem to exist. First, there are a number of different commercial homebrew sets, which are legally sold in most EU jurisdictions. Of course, fermentation and distilling without such sets is also possible but seems to be rare in EU countries. Second, producers of commercial alcohol, particularly in wine regions, may produce alcohol for their own or their family's needs. For example, in Slovenia, an area of 0.1 hectare can be declared as family property to produce a family's own wine for up to 600 L per year. Finally, village wineries or distilleries can produce alcohol for family use.

The identified legal tax exemptions appear to follow cultural traditions of alcohol production, with traditional beer-brewing (e.g., Czechia, Germany) and wine-producing countries (e.g., Croatia, Slovenia) having special regulations on beer and wine for personal and family use, respectively. More recently, with the 2020 Council directive, such exemptions will also be allowed for alcoholic beverages from fruits. These legislations are intended to reflect the interest of regional producers in this regulation and their relevance to local community (Council Directive (EU) 2020/1151 of 29 July 2020 Amending Directive 92/83/EEC, 2020). It should be noted that for wine and fruits, this is often in form of cooperatives of small producers, which has been a traditional form of organising production in particular in Southern Europe with overall about 40% of the production for the EU and 20% of the wholesale market (European Commission Directorate-General for Competition, 2016).

Not only at the country level, but also in the EU, there have been amendments to change the original legislation on alcohol taxation (Council Directive 92/83/EEC, 1992 of 19 October 1992) with a directive to allow Member States more flexibility to regulate small-scale and home-based production with reduced tax rates, or even with no taxation at all (Council Directive (EU) 2020/1151 of 29 July 2020 Amending Directive 92/83/EEC, 2020). This seems to constitute one of the classic potential conflicts between public health interests, which try to reduce availability of low-cost alcohol, which further increases the already high availability of affordable alcoholic beverages in the region (Neufeld et al., 2022), and economic interests to stimulate and support local small-scale production. From a public health perspective, such tax exemptions are discouraged and if pursued, they should at least be limited to a specific, reasonable production volume. For example, the Czechian limit of 2000 L of beer per annum for personal and family use reflects a daily amount of more than 200 g or 20 standard drinks at 10 g of pure alcohol per day (for a beer with 5% ABV and density of 0.789 g/cm3, this translates into 216 g of pure alcohol per day). Given the restriction to personal use, these quantities appear unreasonably high, if not alarming from a public health perspective (for an overview of alcohol's health harms, see Rehm et al., 2017). Moreover, and irrespective of such limits to the production volume, it remains questionable how governments enforce compliance with these regulations.

Overall, given the already high local exemptions and a clear tendency to allow more, we consider it likely that an increasing percentage of this alcohol is not only untaxed, but also unrecorded (i.e., that the authorities do not include untaxed alcohol for personal use in their statistics as recorded alcohol), and that therefore the current estimates of unrecorded alcohol may be underestimates (Probst et al., 2019; World Health Organization, 2018). In light of the considerable health burden attributable to alcohol use in Europe (Shield et al., 2020), consideration should be given to how public health interests can be included in future directives and amendments of the current legislation. This does not only concern tax exemptions and reduced tax rates but should also include an increase of the minimum tax levels, given the high affordability of alcoholic beverages within EU Member States (Angus et al., 2019; Kilian et al., 2023). Raising the minimum tax level for wine from zero would be an important first step in this direction, especially given the Europe's Beating Cancer Plan (European Commission, 2021), as all alcoholic beverages can cause cancer (International Agency for Research on Cancer, 2012).

Supplemental Material

sj-docx-1-nad-10.1177_14550725241246133 - Supplemental material for The legal framework for the production of alcohol for personal use within the European Union

Supplemental material, sj-docx-1-nad-10.1177_14550725241246133 for The legal framework for the production of alcohol for personal use within the European Union by Carolin Kilian, Fleur Braddick, and Jürgen Rehm in Nordic Studies on Alcohol and Drugs

Footnotes

Acknowledgements

We sincerely thank the alcohol experts participating in the unrecorded mapping survey, among others, Miroslav Barták (research fellow, 1st Faculty of Medicine, Charles University, Czechia), Jan Cibulka (Coordination of Alcohol and Tobacco Policy, Office of the Government of the Czech Republic), Wil de Zwart and Manouk Smeets (senior policy advisor and policy officer, Ministry of Health, Welfare and Sport, the Netherlands), Rafn M Jonsson (project manager Alcohol and Drug Prevention, Directorate of Health, Iceland), Sandra Radoš Krnel (national expert, National Institute of Public Health, Slovenia), Sandra Tricas-Sauras (researcher, Eurocare, Belgium) and Ismo Tuominen (ministerial counsellor, Ministry of Social Affairs and Health, Finland).

Data availability statement

The dataset generated during the current study is available from the corresponding author on reasonable request.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the AlHaMBRA (Alcohol Harm – Measuring and Building Capacity for Policy Response and Action) project under contract of the Consumers, Health, Agriculture and Food Executive Agency (CHAFEA) acting under the mandate from the European Commission (EU Health Programme 2014–2020 under Service Contract 2019 71 05). JR was supported by the Canadian Institutes of Health Research – Institute of Neurosciences, Mental Health and Addiction (CIHR-INMHA; No. REN 477887). The views presented are those of the authors, their sole responsibility, and cannot be considered to reflect the views of all AlHaMBRA Project consortium members, or the European Commission and/or the Health and Digital Executive Agency (HaDEA) or any other body of the European Union. The European Commission and HaDEA do not accept any responsibility for use that may be made of the information contained therein.

Supplementary material

Supplementary material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.