Abstract

Consumers’ willingness to decarbonise depends on their understanding of both climate change and financial concepts, though the relationship is complex. We conducted a comprehensive survey with 1,079 representative Australians, aiming to understand how their climate literacy and financial literacy influence behavioural willingness to reduce their carbon footprint. To help answer this question, we created a new, more comprehensive measure of climate literacy. The study revealed that participants’ climate literacy was positively related to their willingness to decarbonise. In contrast, financial literacy was negatively related to their willingness to decarbonise, a relationship that was moderated by climate literacy and environmental values. Both individual and collective efficacy played significant mediating roles in the relationship between climate literacy and willingness to decarbonise, while only individual efficacy was a significant mediator in the relationship between financial literacy and willingness to decarbonise. This research provides a novel understanding of the distinct roles that different types of literacy play in willingness to decarbonise and highlights efficacy as an underlying mechanism.

Introduction

The looming threat of climate change poses unprecedented challenges to global sustainability and human well-being (IPCC, 2023). With rising temperatures, extreme weather events and ecological disruptions becoming increasingly prevalent, urgent action is needed to mitigate the impacts of climate change and transition towards a more sustainable future (Rockström et al., 2017). To address climate change, many countries have put in place emission targets and plans to get there. For example, the UK is targeting net zero by 2050 by focusing on phasing out coal power, promoting electric vehicles and investing in renewable energy and green technologies (Department for Business, Energy & Industrial Strategy, 2021). Similarly, the United States has set a goal of achieving net-zero emissions by 2050 (United States Department of State & Executive Office of the President, 2021). Meanwhile, Australia has established a Net Zero Plan with the goal of reducing greenhouse gas emission levels by 43% by 2030 compared to 2005 levels (Australian Government, 2022). These targets and plans require comprehensive efforts at both societal and individual levels. Thus, understanding the drivers of behavioural change is essential to encourage decarbonising actions (Whitmarsh et al., 2021).

Research aiming to understand what motivates individuals to engage in decarbonising behaviour has been a focal interest of scholars and practitioners (Hale, 2022). Factors that have been found to increase individuals’ willingness to decarbonise include environmental concerns (e.g. Diekmann & Preisendörfer, 2003), social norms (e.g. Bamberg et al., 2015) and climate change risk perception (e.g. van der Linden, 2015; Xie et al., 2019).

Despite the burgeoning research on predictors of decarbonising action, gaps remain in our understanding of how climate literacy and financial literacy are related to individuals’ sustainability behaviour (Kolenatý et al., 2022). For example, some research suggests that climate literacy is a key predictor of willingness to take decarbonising actions (e.g. Kolenatý et al., 2022). However, existing climate literacy measures often assess sectional components of climate literacy such as knowledge of scientific facts, which may explain the mixed findings on how climate literacy is directly or indirectly related to behavioural willingness (e.g. Carmi et al., 2015). For example, some studies found no direct relationship between climate change and climate action (Frick et al., 2004; P. Liu et al., 2020), while some found a direct positive relationship (e.g. Kolenatý et al., 2022)

Another type of literacy – and one that has been relatively overlooked in this literature – is financial literacy. We believe financial literacy is crucial to understanding willingness to decarbonise because decarbonising actions often involve financial decisions such as transitioning to an electric vehicle or purchasing solar panels. However, limited understanding exists of how financial literacy is related to willingness to decarbonise.

In this study, we examined different dimensions of literacy – namely, climate literacy and financial literacy – to elucidate how they contributed to consumers’ willingness to take decarbonising action. We also investigated the mechanisms underlying how climate and financial literacy might be related to behavioural willingness to decarbonise. Our research makes three major contributions. First, we introduced a new climate literacy measure that encompasses diverse components of climate change, including its causes, consequences, mitigation efforts and the organisations involved in advising on climate action. This combination of components allows for a more precise assessment of individuals’ climate literacy and enhances our ability to understand its impact on behavioural willingness to decarbonise. Second, our research revealed a somewhat counterintuitive negative relationship between financial literacy and willingness to decarbonise. Third, it found evidence for efficacy as a mechanism underlying the relationship between both climate change and financial literacy and willingness to decarbonise, thereby uncovering a new avenue to encourage decarbonising action.

Literature review

Climate literacy and financial literacy: Precursors to decarbonising action

Literacy plays a critical role in shaping beliefs, attention, intentions and behaviours, serving as a foundational precursor to informed action (Bandura, 1982). For example, one study found that the levels of information-related literacy – the literacy to search and utilise the information to create new knowledge – were associated with proactive academic behaviours such as using library resources (Pfundt & Peterson, 2024). Similarly, individuals with greater scientific literacy were less likely to hold conspiracy beliefs, which reduced their engagement in conspiracy-congruent behaviours such as avoiding vaccination (Allred & Bolton, 2024).

The role of literacy in driving action is often explained by perceived efficacy, as individuals who understand key concepts and know how to act, feel more empowered to take meaningful steps (Bandura, 1977). For instance, prior studies found that climate literacy enhances perceived efficacy in addressing climate change, fostering confidence in the ability to contribute to mitigation efforts ( N.Geiger et al., 2017). By providing individuals with foundational knowledge and skills, literacy influences how people perceive, prioritise and respond to complex issues, ultimately shaping their willingness to take action.

This principle – that literacy provides foundational knowledge and skills which shape perceptions, priorities and responses to complex issues, thereby influencing individuals’ willingness to take action – is particularly relevant to decarbonisation efforts as they require individuals to engage with complex information about climate change in order to make informed decisions and adopt new behaviours. It is important, however, to recognise that different forms of literacy are relevant for predicting decarbonising action. For instance, climate literacy fosters awareness and understanding of environmental challenges, which can enhance engagement in decarbonising action (e.g. Carmi et al., 2015), while financial literacy can shape decisions related to investments in sustainable technologies or decarbonising practices (Filippini et al., 2024). Recognising these forms of literacy in the context of decarbonising action is essential for understanding and empowering consumers to adopt decarbonising behaviours that address climate change.

Climate literacy and willingness to decarbonise

Climate change knowledge and climate literacy are often used interchangeably in the literature (see Table 1). However, recent research by Pan et al. (2023) defined climate literacy as a broader concept than climate change knowledge. While the literature has not yet reached a full consensus on the definition of climate literacy (Kolenatý et al., 2022), we defined it as the level of knowledge about climate change combined with the ability to apply this knowledge in actions that are directly or indirectly related to addressing, mitigating or adapting to climate change (Hiser & Lynch, 2021; Milér & Sládek, 2011). Accordingly, we contend that climate literacy should encompass not only knowledge of the causes and impacts of climate change but also understanding of the appropriate mitigation and adaptation efforts to address it.

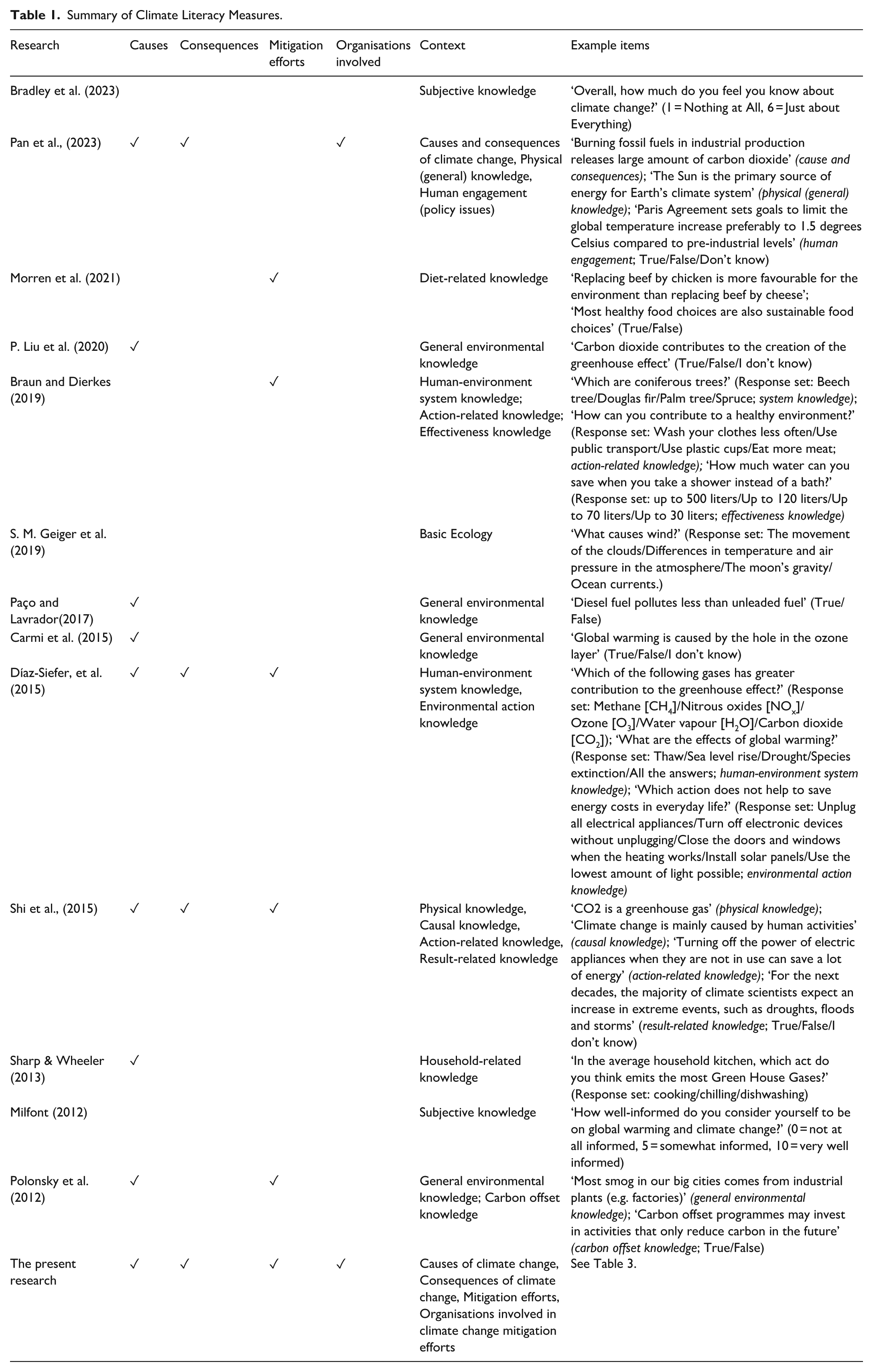

Summary of Climate Literacy Measures.

Most research suggests that climate literacy can increase willingness to decarbonise, with only a few studies suggesting a potential negative influence of climate literacy on willingness to decarbonise (e.g. Shi et al., 2015). This is because climate literacy enables individuals to understand the urgency of climate change and the severity of its impact (Meinhold & Malkus, 2005). It fosters a sense of responsibility for climate change, encouraging greater acceptance of climate change policies (Milfont, 2012; Pan et al., 2023). As a result, individuals are better equipped to make informed decisions about reducing their carbon footprint ( P. Liu et al., 2020). However, existing measures of climate literacy do not adequately capture all the components of climate change knowledge and mitigation efforts identified in prior research. For example, so-called climate literacy measures range from those focused on diet-related knowledge (Morren et al., 2021) to household greenhouse gas emissions (Sharp & Wheeler, 2013) to knowledge of basic ecology (S. M. Geiger et al., 2019). A study by Pan et al. (2023) attempted to incorporate a broader range of knowledge, including the causes and consequences of climate change and climate change-related policy actions. However, their measure omitted the knowledge of climate change mitigation, which is the key driver of decarbonisation efforts (Shi et al., 2015). Table 1 summarises existing measures of climate literacy.

The narrow and limited scope of existing measures could result in the potential mixed findings in the literature where some research found no direct relationship between climate literacy and decarbonising action (Carmi et al., 2015; Frick et al., 2004), while some research found a positive and direct relationship between the two constructs (e.g. Kolenatý et al., 2022). Furthermore, most of the items in existing measures are relatively easy. For example, a recent measure developed by Pan et al. (2023) showed that most participants correctly answered the scale items, with the highest correct response rate exceeding 90%. However, such high correct response rates may indicate a failure to effectively differentiate those who are genuinely interested in and understand climate change from those who are not. This practice could even lead to the misinterpretation that most people are climate literate. To address this concern, we developed a new measure of climate literacy that incorporates knowledge about causes, impacts, mitigation responses and organisations involved. We also ensured that the items were neither too easy nor too difficult, resulting in an approximately normal distribution of response accuracy (see Appendix A).

Financial literacy and willingness to decarbonise

Financial literacy refers to ‘ . . . the degree to which one understands key financial concepts and possesses the ability and confidence to manage personal finances through appropriate, short-term decision-making and sound, long-range financial planning, while mindful of the life events and changing economic conditions’ (Remund, 2010, p. 284). Those with higher financial literacy tend to be better equipped to navigate future financial challenges and opportunities (e.g. de Bassa Scheresberg, 2013) and less likely to be in debt (e.g. Gathergood, 2012).

Decarbonising action often involves making financial decisions. Examples include using public transport, transitioning to an electric vehicle and electrifying one’s house. Furthermore, for some consumers, the key reason to take decarbonising action could be for financial benefits rather than mitigating climate change impacts (Scheller et al., 2024). For example, many people invest in solar panels with high upfront cost because of a financial calculation that, in the long term, they will be financially ahead. To make such financial evaluations accurately, consumers are required to understand how to manage their money over time as they need to sacrifice upfront costs for long-term benefits. Some decarbonising actions may even necessitate financial assistance – for example, loans – which makes understanding consumers’ financial decision-making of critical importance.

The role of financial literacy in influencing decarbonising actions remains underexplored, with most research focusing on financial benefits that can motivate such actions (e.g. Allen et al., 1993; Steg & Vlek, 2009); however, the findings are mixed. On one hand, some research has found that financial literacy is positively related to decarbonising action, such as recycling, among young adults in Brunei (Hasnul & Wasiuzzaman, 2024). On the other hand, Cho et al. (2024) explored the relationship between numeracy and attitudes towards climate change. Numeracy, defined as the ability to understand and interpret numerical information, is often linked to financial literacy due to its application in financial decision-making (Lusardi, 2012; Skagerlund et al., 2018). However, their findings suggest that numeracy does not inherently make individuals more likely to accept the scientific consensus on climate change. This is significant because recognising the scientific consensus is a critical cognitive foundation for supporting decarbonising action. These findings indicate that there may be no relationship between financial literacy, which involves task-oriented cognitive skills as numeracy, and willingness to engage in decarbonising actions.

We can envision two different (and opposing) relationships between financial literacy and willingness to decarbonise. The argument for a positive relation is that decarbonising action involves financial decisions, and individuals with higher financial literacy should be better equipped to evaluate costs and benefits, allocate resources towards sustainable investments aligned with their financial goals (James et al., 2012), and navigate government incentives effectively (Australian Government, 2024a; Lusardi & Mitchell, 2008). By contrast, the argument for a negative relation is that financially literate individuals tend to maximise outcomes and minimise risks (Cokely et al., 2018; Traczyk et al., 2018) and may therefore avoid decarbonising actions involving any financial risks or large future financial uncertainties. Moreover, those with higher financial literacy may prioritise economic concerns over environmental considerations when making decisions, and this may further reduce their willingness to decarbonise (Bakan, 2024).

Efficacy and willingness to decarbonise

In the context of climate change, self-efficacy is often discussed as a potential mechanism underlying the relationship between literacy and behavioural willingness (e.g. Bostrom et al., 2019). Efficacy can be conceptualised at individual and collective levels. Individual efficacy refers to individuals’ belief that they have ability to reduce their own carbon footprint, and that their actions will result in a meaningful outcome. Collective efficacy refers to individuals’ belief that many others have ability to reduce their carbon footprint, and that the combined action of these many others will result in a meaningful outcome (Camilleri & Larrick, 2019). 1 The distinction between individual and collective level of efficacy is essential because it helps to delineate the possible pathways by which consumers may be motivated to engage in decarbonising actions. For example, individual efficacy may drive personal behaviours (e.g. driving an electric car) while collective efficacy could enhance engagement in community-based or large-scale initiatives where consumers believe that combined efforts can lead to meaningful changes (e.g. supporting a community solar bank).

Prior research suggests there exists a positive relationship between climate literacy and efficacy (e.g. N. Geiger et al., 2017). Specifically, one study found that greater knowledge of climate change was positively correlated with the efficacy level of individuals, which predicted their willingness to engage in climate actions (Xie et al., 2019). Presumably, when individuals possess a deeper understanding of climate change, they may feel more capable of taking action, as this understanding reduces aversive feelings such as uncertainty (Bandura, 1977; Peterson & Pitz, 1988). Meanwhile, the literature indicates that financial literacy can enhance perceived efficacy in taking financial decisions (e.g., L. Liu & Zhang, 2021); however, how this relationship influences actions within the domain of climate change remains unexplored.

Environmental values

The concept of environmental values has been defined as the ‘endorsement of an ecological worldview’, which primarily refers to environmental concern and attitudes (Dunlap et al., 2000, p. 426). Environmental values are often grounded in moral and normative considerations, arising from a sense of what is ethically responsible or social expectations regarding environmental stewardship (de Groot & Steg, 2007; Steg & Vlek, 2009). Hence, consumers with strong environmental values tend to prioritise environmental concerns over personal interests, fostering positive attitudes towards pro-environmental behaviours (Rausch & Kopplin, 2021) and engaging in more decarbonisation efforts (Steg & de Groot, 2012). It is, therefore, plausible that environmental values can moderate the aforementioned relationships, and we explored the role of environmental values in these relationships.

Research questions and study overview

The present study aimed to examine the role of climate literacy and financial literacy in predicting willingness to decarbonise. Additionally, it investigated the possible mediating role of individual and collective efficacy and explored the moderating role of environment values in the relationship between literacy and willingness to decarbonise. Accordingly, the research questions were as follows:

RQ1: How is climate literacy related to the willingness to decarbonise?

RQ2: How is financial literacy related to the willingness to decarbonise?

RQ3: To what extent do individual and collective efficacy mediate the relation between both climate literacy and financial literacy and willingness to decarbonise?

RQ4: To what extent do environmental values moderate the relation between both climate literacy and financial literacy and willingness to decarbonise?

Methods

A total of 1,079 participants, generally representative of the Australian adult population, completed a survey. Participants were recruited through an online panel called ‘Pureprofile’ in September 2023. The sample was 49.8% female, and the average age was 47.98 years (SD = 17.53). Although a significant proportion of respondents held higher education qualifications – such as a Bachelor’s degree (23.1%) and Master’s degree (10.2%) – a notable portion also reported high school completion or lower (21.7%). The median category for personal income was $70,000 to $99,999, and the median category for household income was $100,000 to $149,999. Full demographic information can be found in Appendix B. The median time to complete the questionnaire was 23.08 minutes. One attention-check question was included, and the participants who failed to answer correctly were directed out of the survey (N = 43).

Measures 2

Climate literacy

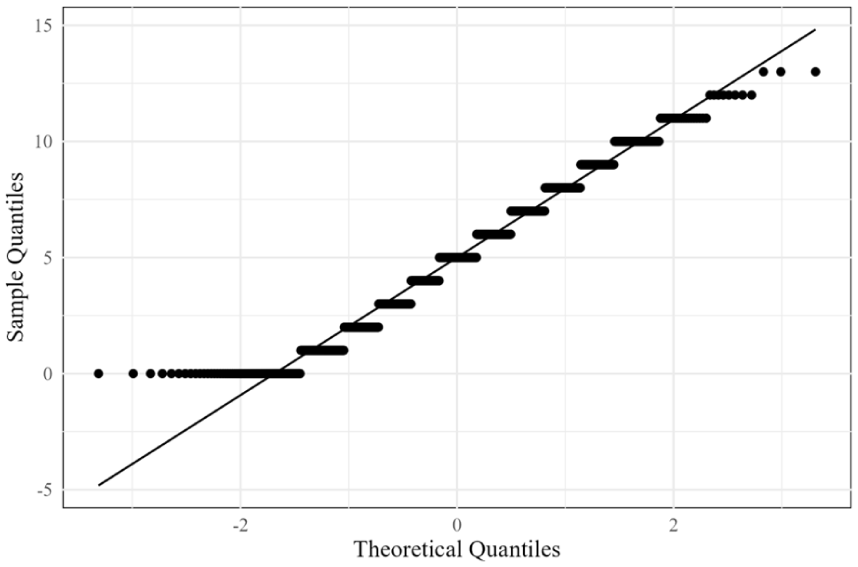

We developed a new, 13-item questionnaire to measure climate literacy, aiming to better capture the understanding of climate change across four components: the causes of climate change, the consequences of climate change, individual-level mitigation strategies for climate change and organisations involved in addressing climate change. We created the items based on the information in public reports, published papers (e.g. Duffy et al., 2022; Xiu et al., 2018) and official websites of the organisations. Our primary goal for this climate literacy measure was to ensure that the questions were neither too easy nor too difficult, allowing the scale to exhibit a normal distribution. With this aim, five pilot studies were conducted (total N = 250) to finalise the set of items (see Appendix A for further details). The Q-Q plot (Figure 1) provides a visual representation of the new climate literacy measure’s distribution by plotting the observed quantiles of the scores against the theoretical quantiles of a normal distribution (Wilk & Gnanadesikan, 1968). The alignment of the data points along the diagonal reference line suggests that the scale scores are approximately normally distributed, supporting the aim of ensuring that the scores are evenly distributed.

Q-Q plot for the climate literacy measure.

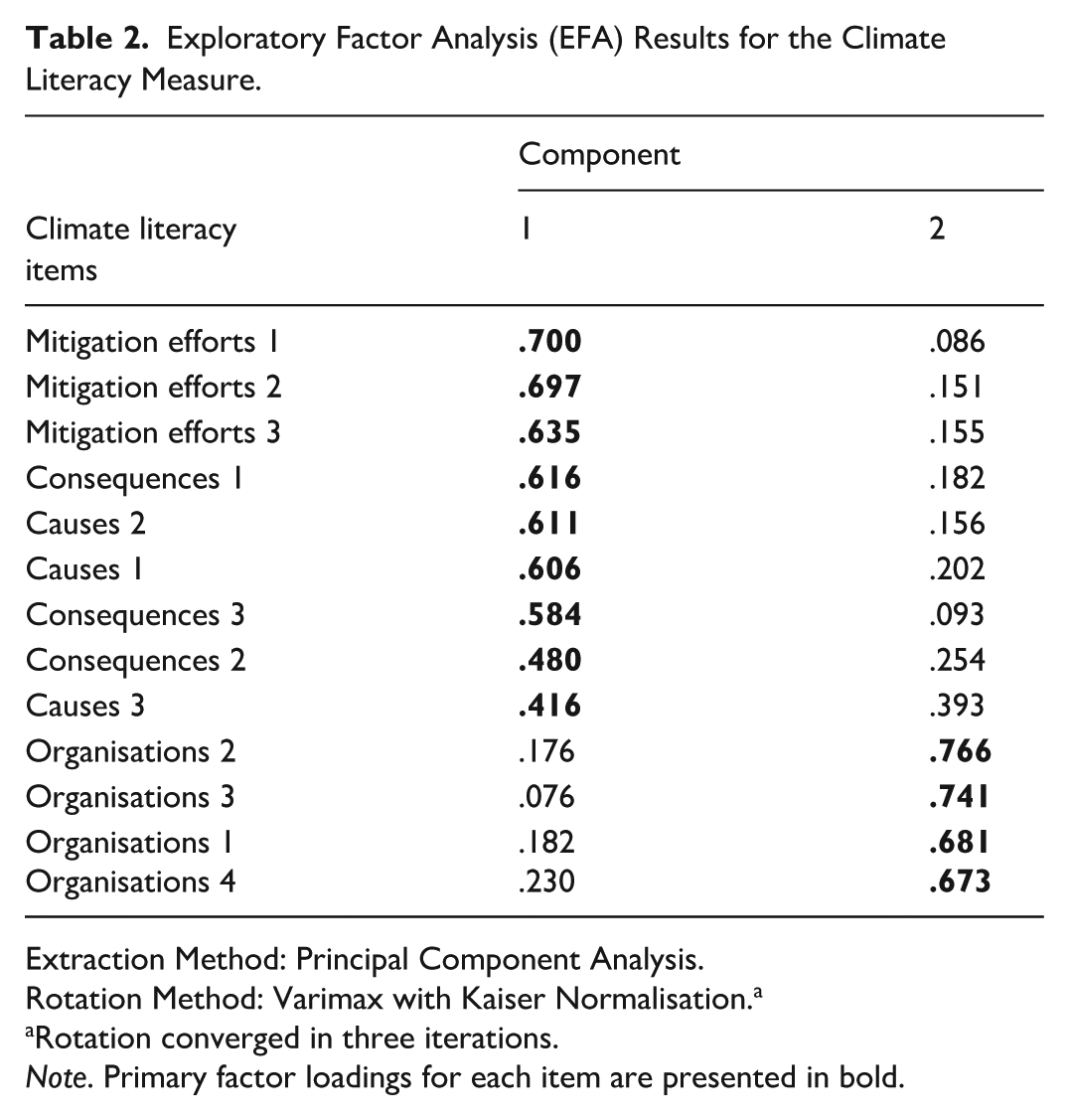

Factor analysis for the climate literacy measure

Bartlett’s test of sphericity was also conducted to assess whether the correlation matrix of the 13 items was significantly different from an identity matrix. The test was statistically significant (χ²(78) = 1,632.00, p < .001), indicating that the observed correlations were sufficiently large for factor analysis. Furthermore, the Kaiser-Meyer-Olkin (KMO) test was performed to assess the adequacy of the sample for factor analysis. The overall KMO measure was 0.82, suggesting that the dataset was well-suited for factor analysis (Kaiser, 1974).

Finally, Exploratory Factor Analysis (EFA) was conducted on the 13 climate literacy items using the maximum likelihood method of extraction with the varimax rotation. The results revealed a two-factor structure where the four items measuring organisation-level mitigation efforts loaded primarily onto one factor and the remaining items loaded primarily onto a second factor (see Table 2). These two factors explained 44.55% of the total variance. Given that the correlation between the two factors was strong (r = .49, p < .001) and our definition of climate literacy encapsulated the organisations involved in mitigating climate change, we combined these two factors to create a single climate literacy measure. Participants received 1 point for each correct answer, resulting in a total score ranging from 0 to 13. The average score was 4.96 (SD = 2.96), and the reliability score for the items was 0.73 (see Table 3 for the final items).

Exploratory Factor Analysis (EFA) Results for the Climate Literacy Measure.

Extraction Method: Principal Component Analysis.

Rotation Method: Varimax with Kaiser Normalisation. a

Rotation converged in three iterations.

Note. Primary factor loadings for each item are presented in bold.

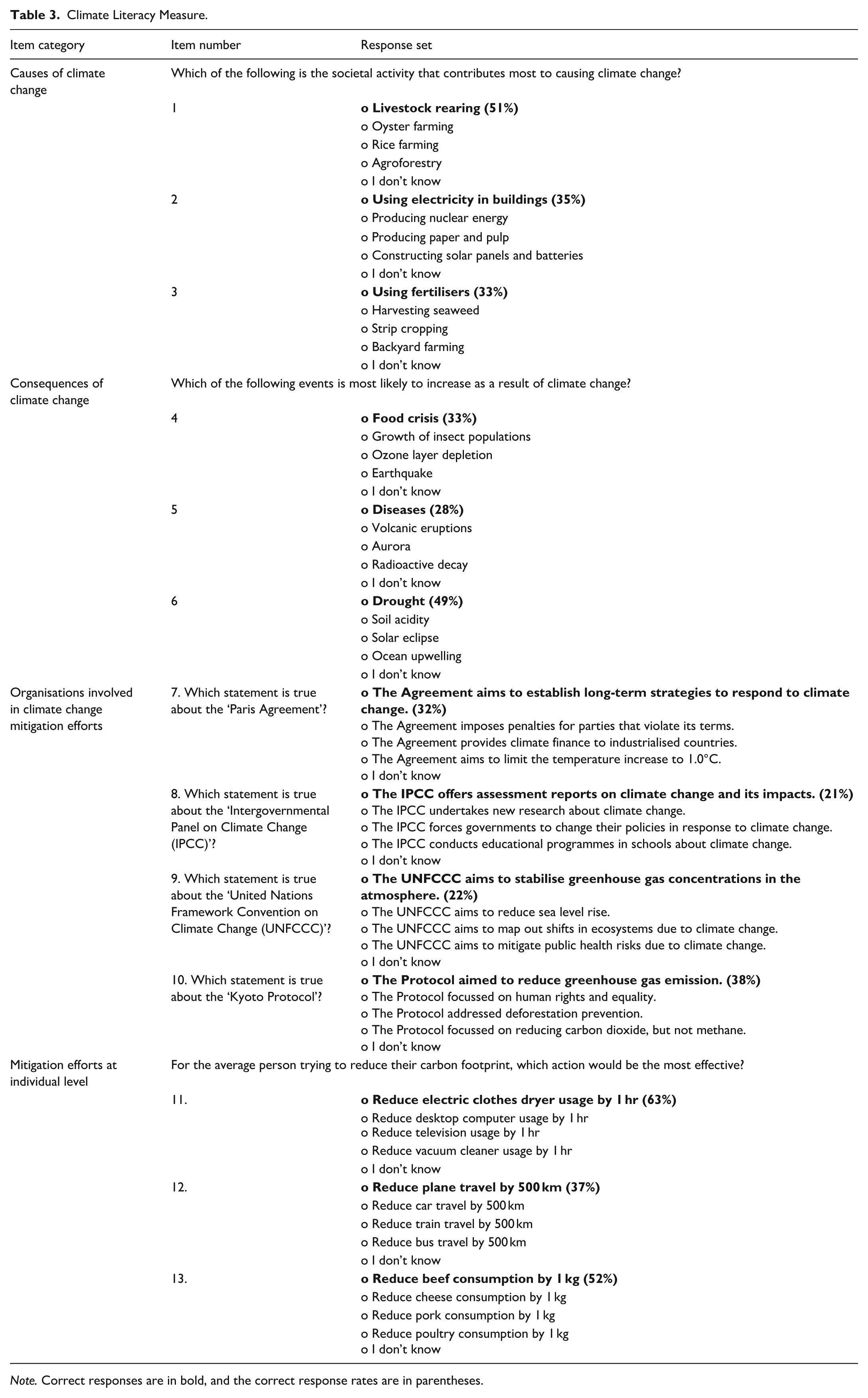

Climate Literacy Measure.

Note. Correct responses are in bold, and the correct response rates are in parentheses.

Financial literacy

Financial literacy was measured by using the Financial Knowledge Scale (FKS) by Houts & Knoll (2020), which is an expansion of the 3-item financial literacy measure by Lusardi and Mitchell (2008). Three items were revised to align with Australian financial concepts, including ‘Housing prices in Australia can never go down’ (response options: true/false/I don’t know). The items are commonly used to measure financial literacy in the literature because they assess not only individuals’ understanding of financial concepts but also their ability to manage their financial resources. For example, the scale asks questions such as ‘Suppose you owe $3,000 on your credit card. You pay a minimum payment of $30 each month. At an Annual Percentage Rate of 12% (or 1% per month), how many years would it take to eliminate your credit card debt if you made no additional new charges?’ Hence, although the scale’s name may suggest a focus solely on knowledge, its items capture broader aspects of financial literacy by examining practical applications of financial understanding in real-world contexts. Participants received 1 point for each correct answer, thus a total score ranging from 0 to 10. The average score was 5.87 (SD = 2.40), and the reliability score for the items was 0.72 (see Appendix G for the full list of items).

Willingness to decarbonise

To measure willingness to take decarbonising actions, we adapted the items developed by Bradley et al. (2023) and provided a set of twenty-two decarbonising actions and asked participants to indicate the extent to which they are willing to take these actions to help reduce climate change. Examples of the actions include greatly reducing one’s energy use, installing solar energy for one’s home, using public transportation more often and participating in climate protests, rallies or other public demonstrations dedicated to fighting climate change. The items were rated on a 5-point scale where 1 indicated ‘strongly disagree’ and 5 indicated ‘strongly agree’. Additionally, there was an option of 6, which allowed participants to indicate that the item was not applicable to them. For example, installing solar panels might not be applicable to those who are renting. In the analysis, responses of 6 were treated as missing values. Responses were averaged to produce an overall willingness to decarbonise score. The average score was 3.25 (SD = 0.94), and the reliability score for the items was 0.95 (see Appendix H for the full list of items).

Individual and collective efficacy

We measured individual and collective efficacy by assessing participants’ perceived ability – either their own or that of others – to reduce their carbon footprint, as well as their belief that such reductions can contribute to addressing climate change. Individual and collective efficacy were measured using items adapted from Camilleri and Larrick (2019); two items asked about a participant’s personal ability to reduce their carbon footprint (individual ability efficacy) and the extent to which this reduction would contribute meaningfully to addressing climate change (individual outcome efficacy). Additionally, we measured collective efficacy by asking about participants’ perception of others’ ability to reduce their carbon footprint (collective ability efficacy) and the potential meaningful contribution of such actions to addressing climate change (collective outcome efficacy). The items were rated on a 5-point scale, with 1 being completely unable (no contribution) and 5 being completely able (enormous contribution). The reliability score for the two items measuring individual ability efficacy and outcome efficacy was 0.65, which was slightly below the conventional threshold, but still sufficient to aggregate the items into a single variable, individual efficacy (Nunnally & Bernstein, 1994). Collective efficacy was also aggregated into a single variable, collective efficacy, with the reliability score of 0.76 for two items measuring collective ability efficacy and outcome efficacy (see Appendix I for the full list of items). The average values of individual and collective efficacy were 3.11 (SD = 0.89) and 3.26 (SD = 0.95), respectively.

Environmental values

Environmental values were measured by using the New Ecological Paradigm (NEP) Scale developed by Dunlap et al. (2000). An example item was ‘If things continue on their present course, we will soon experience a major ecological catastrophe’. The items were rated on a 5-point scale, with 1 indicating ‘strongly disagree’ and 5 indicating ‘strongly agree’. Responses were averaged to produce an overall environmental values score. The reliability score was 0.63, falling slightly below the conventional threshold yet remaining acceptable (Nunnally & Bernstein, 1994). The average score was 3.60 (SD = 0.65) out of 5 (see Appendix J for the full list of items).

Results

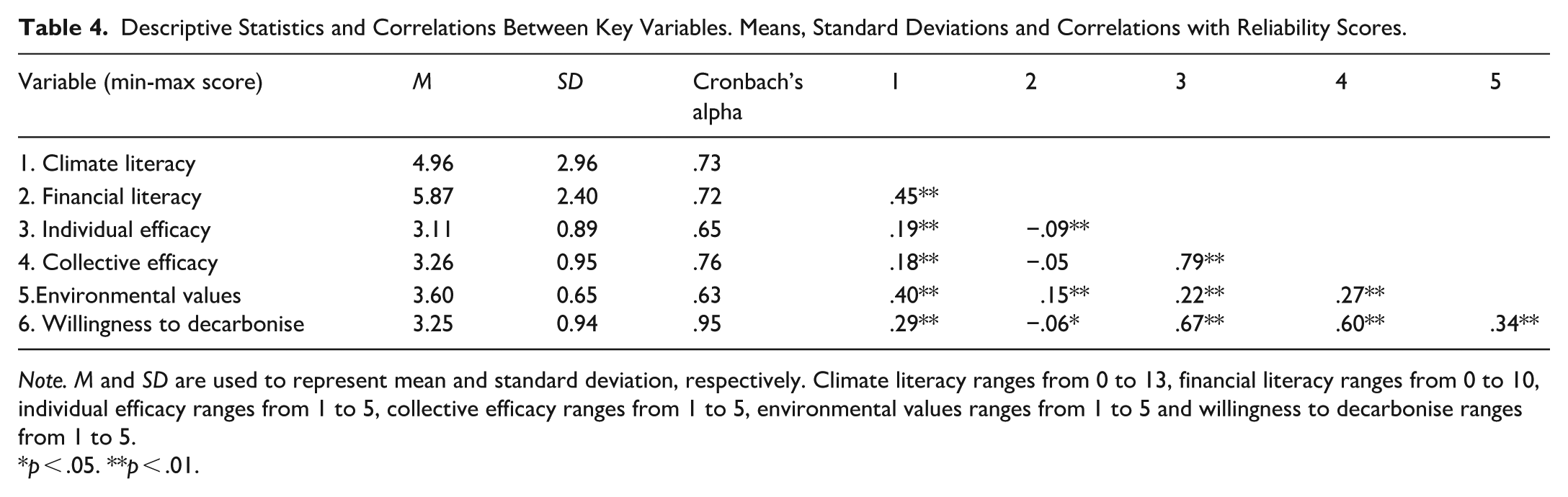

Means, standard deviations and correlations between the variables of interest are provided in Table 4.

Descriptive Statistics and Correlations Between Key Variables. Means, Standard Deviations and Correlations with Reliability Scores.

Note. M and SD are used to represent mean and standard deviation, respectively. Climate literacy ranges from 0 to 13, financial literacy ranges from 0 to 10, individual efficacy ranges from 1 to 5, collective efficacy ranges from 1 to 5, environmental values ranges from 1 to 5 and willingness to decarbonise ranges from 1 to 5.

p < .05. **p < .01.

Climate and financial literacy and willingness to decarbonise

Regression analysis

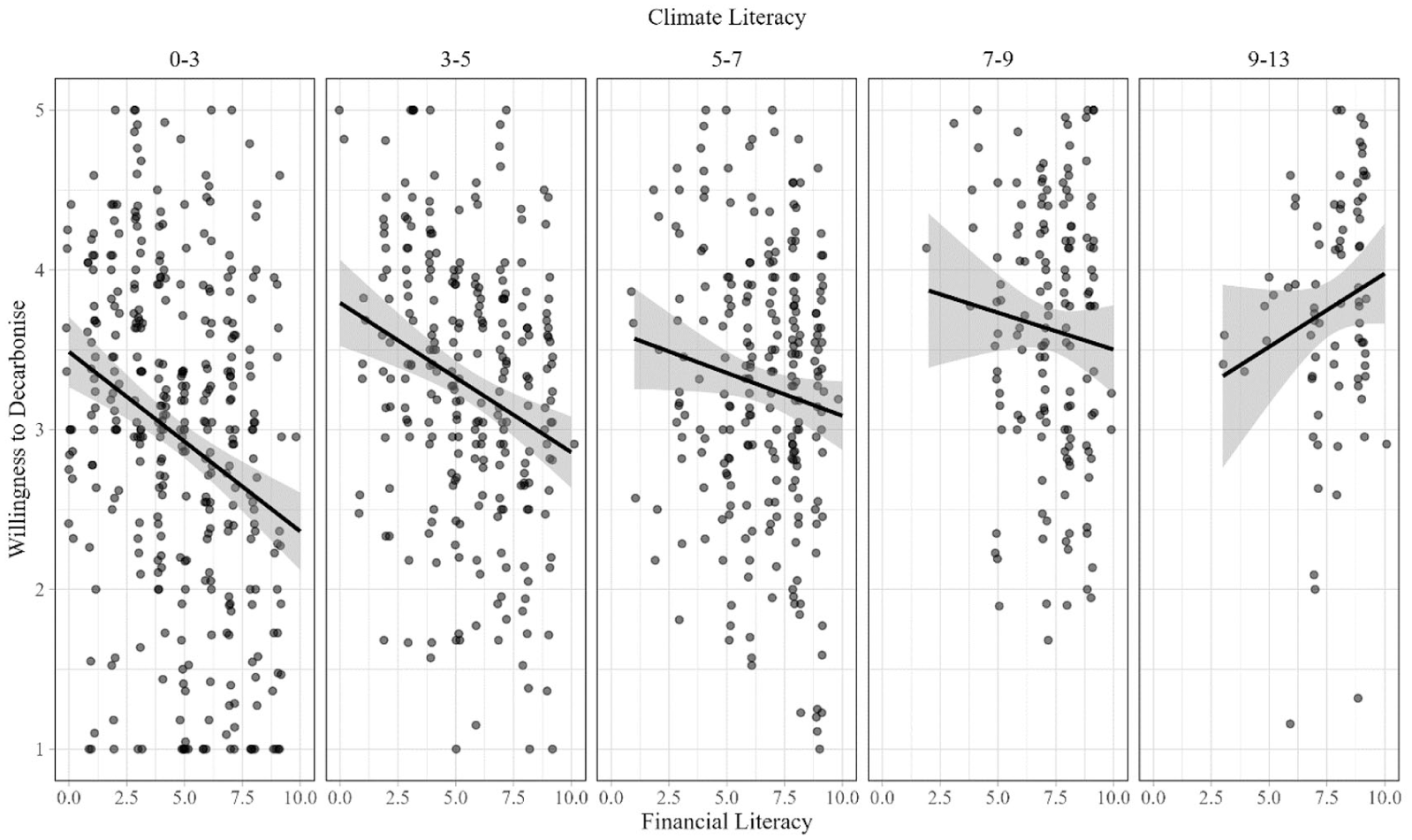

A multiple regression model was used to examine the effects of climate literacy and financial literacy on decarbonising action willingness. The regression model including both literacy variables as predictors was statistically significant (F(2, 1,071) = 79.33, p < .001, adjusted R2 = .127). The analysis revealed that climate literacy positively predicted willingness to decarbonise (b = 0.126, t(1,071) = 12.41, p < 0.001). In contrast, financial literacy negatively predicted willingness to decarbonise (b = −0.094, t(1,071) = −7.51, p < .001). These observations suggest that, on average, individuals with a good understanding of climate change are more willing to take decarbonising action, whereas individuals with a good understanding of financial concepts are less willing to take decarbonising action. There was also a significant interaction between climate literacy and financial literacy on willingness to decarbonise (b = 0.010, F(3, 1,070) = 55.02, p = .017). Specifically, for those with high (vs. low) climate literacy, the negative effect of financial literacy on willingness to decarbonise was smaller or may even have reversed (see Figure 2). 3

Interaction between climate literacy and financial literacy on willingness to decarbonise.

Mediating effect of individual and collective efficacy

Climate literacy and willingness to decarbonise

To examine the mediating effect of individual and collective efficacy, parallel mediation analyses were conducted using the PROCESS macro (Hayes, 2022) . A 95% bias-corrected confidence interval based on 5,000 bootstrap samples indicated that climate literacy was indirectly related to decarbonising action willingness through its relationships with individual and collective efficacy (individual efficacy: b = 0.03, SE = 0.005, 95% CI [0.020, 0.040], collective efficacy: b = 0.01, SE = 0.003, 95% CI [0.006, 0.018], total effect: b = 0.09, SE = 0.009, p < .001; see Table 5).

Mediation Analyses.

Financial literacy and willingness to decarbonise

Parallel mediation analyses were conducted using the PROCESS macro (Hayes, 2022) to examine the mediating effect of efficacy on the relationship between financial literacy and decarbonising action. The results with 95% bias-corrected confidence interval based on 5,000 bootstrap samples indicated that only individual efficacy was a significant mediator in the relationship between financial literacy and decarbonising action willingness (b = −0.02, SE = 0.006, 95% CI [−0.031, −0.007], total effect: b = −0.024, SE = 0.012, p = .046; see Table 5). The results suggest that individuals with a good understanding of financial concepts had lower beliefs in the effectiveness of their individual efforts in reducing their carbon footprint and addressing climate change, thus making them less willing to take climate action.

Moderating effect of environmental values

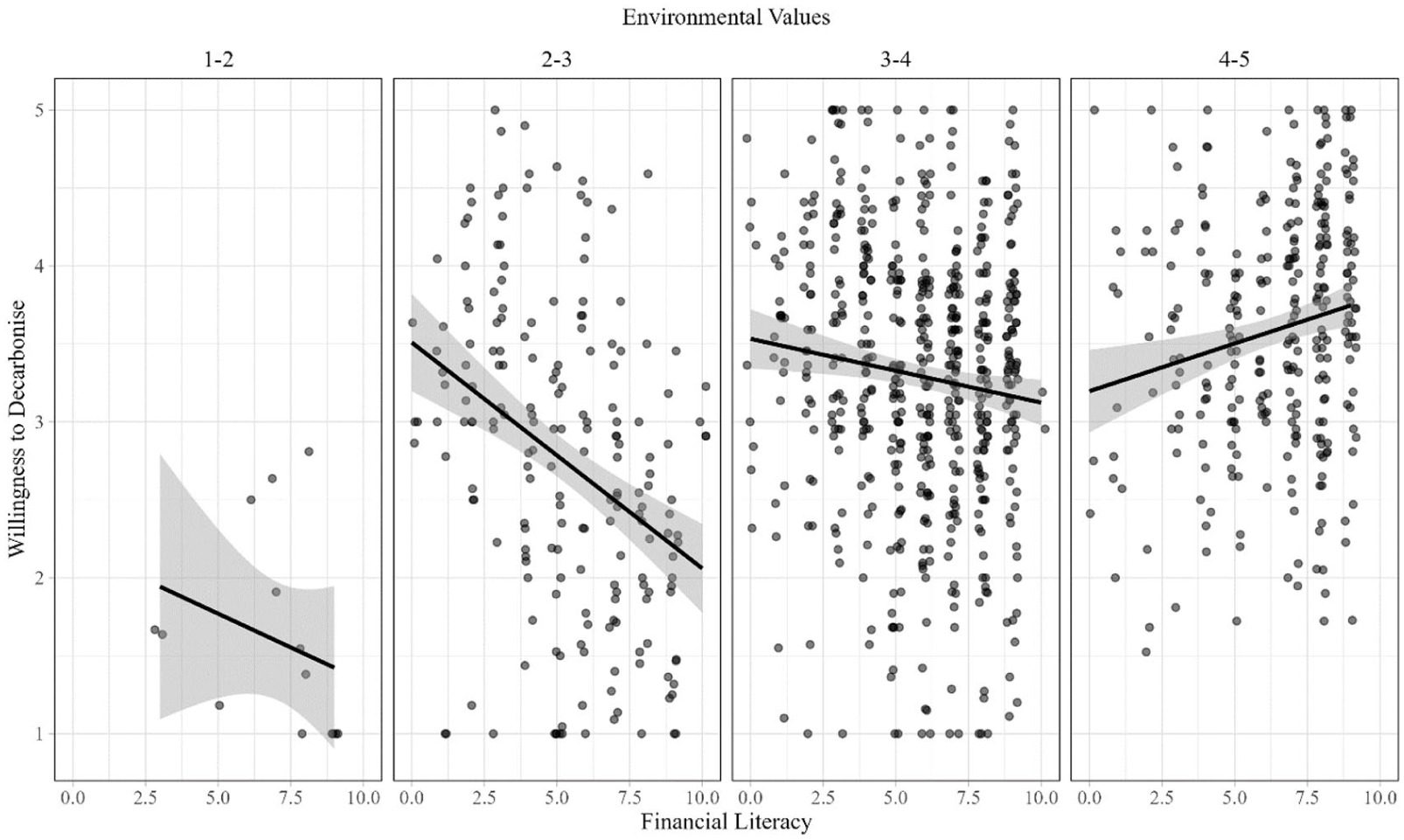

To explore the moderating effect of environmental values, moderation analyses were conducted using the PROCESS macro (Hayes, 2022). A 95% bias-corrected confidence interval based on 5,000 bootstrap samples indicated that environmental values did not moderate the relationship between climate literacy and willingness to decarbonise (b = −0.006, F(1, 1,070) = 0.17, p > 0.1). By contrast, the results revealed that environmental values significantly moderated the relationship between financial literacy and willingness to decarbonise (b = 0.11, F(1, 1,070) = 37.19, p < .001). Individuals with higher environmental values demonstrated a positive relationship between financial literacy and willingness to decarbonise, while those with lower environmental values showed a negative relationship between financial literacy and willingness to decarbonise (see Figure 3).

Interaction between financial literacy and environmental values on willingness to decarbonise.

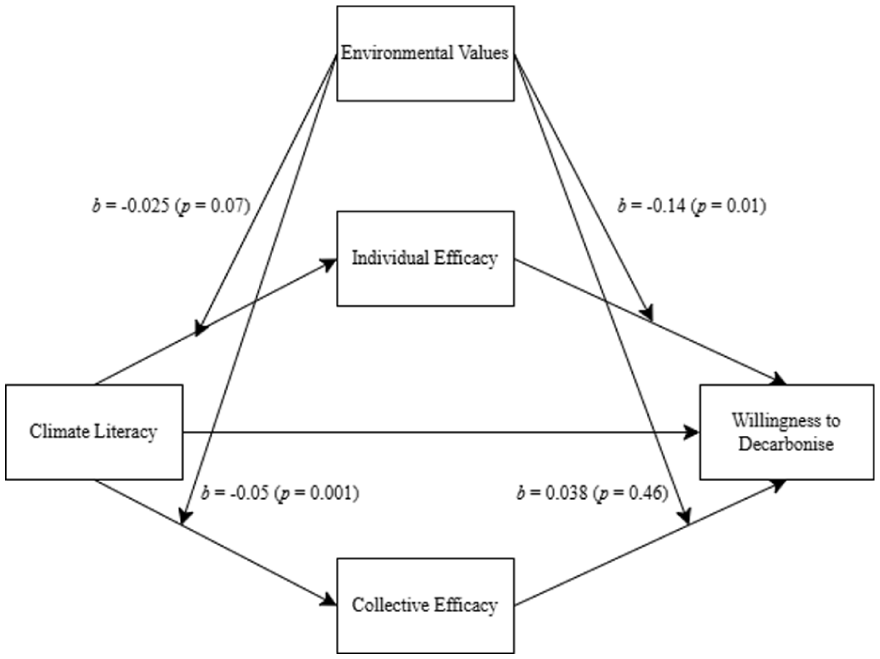

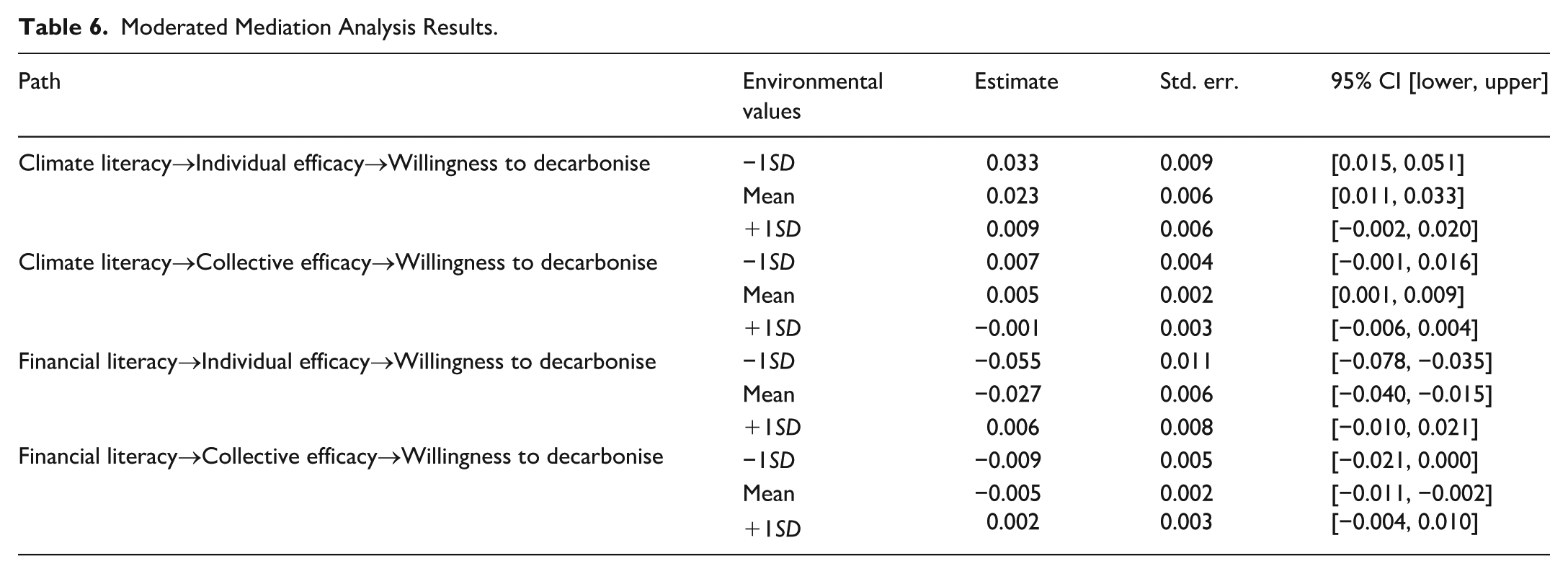

We examined the moderating effect of environmental values on the relationships between both climate and financial literacy and willingness to decarbonise via individual and collective efficacy. Results revealed that environmental values moderated the relationships between climate literacy and both types of efficacy (see Figure 4). The results also revealed that the path from individual efficacy to willingness to decarbonise was moderated by environmental values (b = −0.14, F(1, 1,069) = 6.35, p = .01), but no significant moderation was found for the path from collective efficacy to willingness to decarbonise (see Figure 4). The mediating effect of individual efficacy was significant only for those with low levels of environmental values (b = 0.03, SE = 0.009, 95% CI [0.015, 0.051]), while no moderation effect was observed on the mediating path from climate literacy and collective efficacy (see Table 6).

Moderated mediation analysis results: the moderating role of environmental values on the relationship between climate literacy and willingness to decarbonise via individual and collective efficacy.

Moderated Mediation Analysis Results.

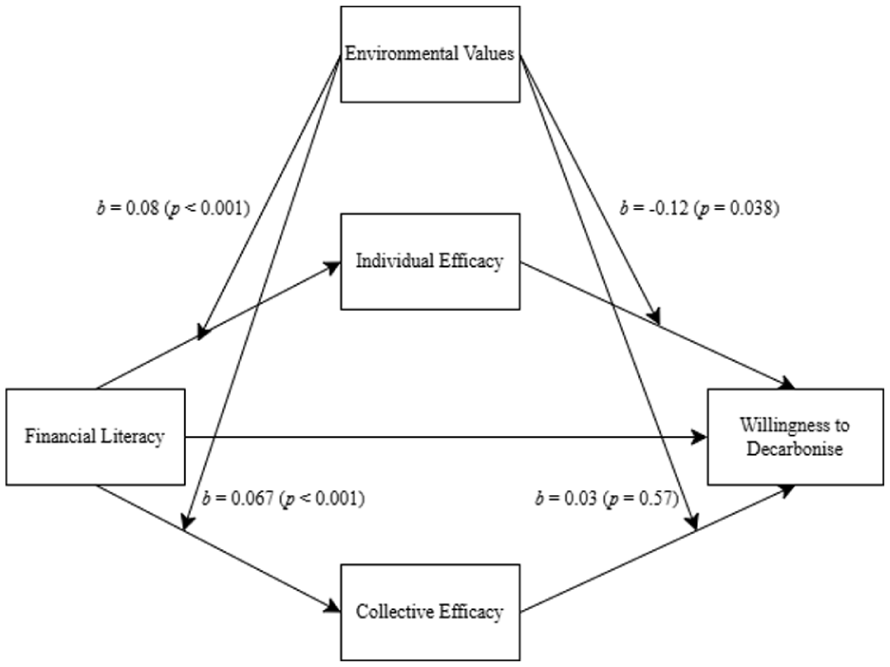

Finally, environmental values moderated the relationships between financial literacy and both individual and collective efficacy (see Figure 5). The path from individual efficacy to willingness to decarbonise was significantly moderated by environmental values (b = −0.12, F(1, 1,066) = 4.23, p < .05); the path from collective efficacy to willingness to decarbonise showed no significant moderation (see Figure 5). The mediating effect of individual efficacy was significant only for those with low environmental values (b = −0.06, SE = 0.011, 95% CI [−0.078, −0.035]; see Table 6).

Moderated mediation analysis results: the moderating role of environmental values on the relationship between financial literacy and willingness to decarbonise via individual and collective efficacy.

Discussion

Using the data from a representative sample of Australian adults, we tried to understand the role of climate and financial literacy in willingness to decarbonise. The results revealed that climate literacy positively predicted willingness to take decarbonising action, and this was mediated by individual and collective efficacy. This finding suggests that those with good knowledge of climate change – including its causes, consequences, ways to mitigate it and organisations involved – tend to have a relatively high level of belief that their own and others’ efforts can significantly reduce their carbon footprint, as well as successfully address climate change. This belief further encourages them to take decarbonising action. Our finding also replicates the evidence from the literature that climate literacy is a significant factor that motivates decarbonising action, and thus education for a better understanding of climate change is important to encourage consumers to take decarbonising actions (Kolenatý et al., 2022). This is critical considering evidence that individuals are poor at gauging the most impactful decarbonising actions they can take (Camilleri et al., 2019; Johnson et al., 2024).

On the other hand, financial literacy negatively predicted behavioural willingness via decreased individual efficacy. This indicates that those with good knowledge of financial concepts tend to have a relatively low level of belief that their own efforts can successfully address climate change, which may lead them to be less likely to take decarbonising action. These lines of thinking could be based on their primary concern being more related to financial benefits rather than addressing climate change, as they tend to maximise their financial gains and minimise their financial sacrifices (e.g. Cokely et al., 2018).

Environmental values moderated the relationship between financial literacy and willingness to decarbonise. Our findings suggest that individuals with higher environmental values are more likely to overcome the negative impact of financial literacy on their willingness to decarbonise. These results provide supporting evidence for prior research that pro-environmental values can motivate decarbonising action by prioritising environmental well-being over personal gains (Steg & de Groot, 2012). We also found that environmental values moderate the relationships between climate and financial literacy and willingness to decarbonise, which are mediated by individual efficacy. Collectively, these findings highlight the complex interplay between literacy, efficacy and values in shaping decarbonisation efforts.

Theoretical implications

We introduced a new measure of climate literacy that incorporates the causes, consequences and mitigation efforts at both individual and collective levels, finding that climate literacy was a significant precursor to willingness to take decarbonising action. In doing so, it confirmed a direct and positive relationship between climate literacy and willingness to decarbonise (e.g. Johnston, 2020).

Importantly, we found evidence that financial literacy was negatively related to behavioural willingness in a large sample of respondents. In contrast, some studies identified a positive correlation between financial literacy and pro-environmental behaviours, such as recycling (e.g. Han et al., 2025; Hasnul & Wasiuzzaman, 2024). This discrepancy may be due to differences in how the decarbonising actions were measured and the sample populations. While Hasnul and Wasiuzzaman (2024) used around 190 youths in a developing country, Brunei, and Han et al. (2025) focused on rural residents in China, our research was conducted with a representative sample of Australian adults. The representative Australian sample, given its higher socioeconomic status and greater exposure to environmental policies and education, offers a potentially more robust context for examining the dynamics between financial literacy and willingness to decarbonise. Furthermore, we used more established and refined measures for both financial literacy and behavioural willingness (e.g. Bradley et al., 2023; Houts & Knoll, 2020). Thus, our findings provide an arguably more comprehensive and reliable understanding of the relationship between financial literacy and willingness to decarbonise.

Some research suggests a positive relationship between financial literacy and willingness to decarbonise, based on the argument that financially literate consumers are well-positioned to benefit from decarbonisation efforts (e.g. Lusardi & Mitchell, 2011). From this perspective, financially literate individuals might be expected to engage in decarbonising initiatives as they recognise financial advantages such as direct cost savings from reduced energy consumption, increased long-term asset value through sustainable investments (e.g. green superannuation options) and reduced exposure to regulatory or carbon pricing risks. This expectation aligns with benefit segmentation theory (Haley, 1968), which proposes that consumers can be segmented based on the specific benefits they prioritise when making behavioural decisions. Financially literate consumers, in this sense, represent a target segment that would reasonably be receptive to decarbonising initiatives, particularly those that bring potential financial gains or losses.

However, our findings suggest that such benefit-based segmentation may offer a limited insight into financially literate consumer groups and their decarbonisation efforts, as financial acumen does not appear to directly translate into their willingness to decarbonise. We suggest, therefore, that motivational constructs such as perceived individual efficacy should be considered as a central explanatory process within benefit segmentation models.

While previous studies have shown that efficacy can influence pro-environmental behaviours (e.g. Lin & Hsu, 2015), our results provide additional insight into the distinct roles of individual efficacy and collective efficacy (e.g. Jugert et al., 2016). The two forms of efficacy – individual efficacy, the belief in one’s own capacity to reduce a personal carbon footprint and address climate change and collective efficacy, the belief in others’ capacity to reduce their carbon footprint and address climate change – differently explained the relationship between financial literacy and willingness to decarbonise, providing a deeper understanding. Future studies could focus on distinguishing different levels of efficacy to better target underlying mechanisms and possible interventions.

Our new measure and the insights from our results can be used to help build our understanding of when efforts to induce decarbonisation may or may not work. A potential method for facilitating this integration is to use the ‘representational alignment’ framework recently proposed by Szollosi et al. (2025). This framework emphasises the need for both cognitive and motivational alignment between an individual and a choice-architect who is trying to drive behaviour change. In terms of decarbonisation efforts, cognitive alignment would be achieved by ensuring that a person has a good factual understanding of the most effective emissions-reducing behaviours. Motivational alignment refers to both parties sharing the same goal of a desired behaviour, such as both seeing the value (financial or otherwise) in driving down individual carbon footprints. By providing a baseline measure of climate literacy – and how it links to other measures such as financial literacy – our work can contribute to efforts for achieving these kinds of alignments.

Practical implications

Despite the acknowledged gap between action and intention (Gifford et al., 2011), the findings from the present research provide practical guidelines on how to motivate consumers’ decarbonising action. Throughout the study, we confirmed the critical role of climate literacy in enhancing willingness to decarbonise. Marketing practitioners would benefit from climate literacy education as an intervention to increase the adoption and sales of their decarbonising products, such as electric vehicles and solar batteries. By effectively communicating the positive impact of decarbonising products on reducing carbon footprints and combating climate change, marketers could foster greater consumer engagement and drive higher sales.

At the same time, the negative effect of financial literacy emphasises the need for a different approach in current interventions. For example, institutions generally educate financial concepts for individuals to enhance their financial well-being (Tahir et al., 2021), however, our results showed that financial literacy was negatively related to their willingness to engage in decarbonising actions. Similarly, emphasising financial benefits of decarbonising behaviours (e.g. ‘ . . . rooftop solar, household batteries and electric vehicles . . . will unlock further savings and benefits for all energy customers ($27.7 million over 4 years)’; Australian Government, 2024b) could result in decreased engagement in those actions, especially for consumers who have weak environmental values. Instead, practitioners may need to enhance consumers’ climate literacy through education, alongside their financial education programmes (Bouman et al., 2021), as our study found that enhanced climate literacy can buffer the negative effect of financial literacy on willingness to decarbonise. For example, Commonwealth Bank Australia, the largest bank in Australia, offers ‘Financial Well-being Seminars’ for its members (Commonwealth Bank Australia, 2024). We suggest these efforts should be accompanied by climate literacy education to mitigate the potential negative impact of financial literacy on willingness to engage in decarbonising actions.

Our results revealed that environmental values moderate the relationship between literacy and perceived efficacy, and thus, interventions to promote decarbonising action could be tailored to consumers’ environmental values. For example, campaigns focusing on building efficacy to bridge the gap between literacy and action could be effective for those with lower environmental values.

While it is well established that consumers with high levels of climate literacy and strong environmental values are more likely to engage with decarbonisation initiatives (e.g. Hu et al., 2025), our findings complicate assumptions about the role of financial literacy. For marketing practitioners, particularly those working in sustainability, this highlights the need for strategic communication tailored to high-financial-literacy segments. Messaging should emphasise efficacy-enhancing narratives, for instance, by providing clear pathways showing how individual actions contribute to broader decarbonisation outcomes. In particular, for those with high levels of financial literacy but low environmental values, campaigns should especially focus on enhancing perceptions of individual efficacy (White et al., 2011). Such framing may help bridge the motivational gap without oversimplifying the message for this audience. However, as our study was based on survey data and correlational analyses, these implications should be interpreted with due caution.

Again, we do not wish to overstate our implications; however, our findings also hold important relevance for branding positioning, particularly for financial institutions that promote sustainable investment products, such as green loans, green deposits and fossil-free super investments, offered by banks, superannuation funds and fintech platforms (e.g. AustralianSuper, 2023; National Australia Bank, 2024). Given that financially literate individuals are likely to represent a core target segment for these institutions, it is important to craft brand narratives that resonate with their financial knowledge and capacity while enhancing their sense of individual efficacy. Brands could further enhance individual efficacy by providing regular feedback on the environmental impact of consumers’ actions. In doing so, these institutions can cultivate efficacy-based brand associations, positioning themselves as platforms that empower individuals to contribute meaningfully to addressing climate change.

Finally, our new measure of climate literacy offers a comprehensive approach, enabling practitioners and scholars to gain a broader view of the public’s understanding of climate change. Our measure could be used to identify gaps in climate change knowledge and inform more effective communication strategies, policies and education initiatives. For instance, findings from our new climate literacy measure revealed that the knowledge regarding organisations involved in climate action was relatively underdeveloped among participants, with the lowest correct response rate being 21%. This suggests that consumers may lack awareness of the efforts and roles of global institutions and organisations in addressing climate change (e.g. the UN IPCC). Such gaps in knowledge could lead to an underestimation of the importance of collective action and the impact of regulatory and organisational contributions, thereby limiting consumer engagement in broader climate initiatives and climate-related policies. To address this issue, targeted educational programmes focusing on institutional and organisational roles in climate action would be essential to empower consumers to actively participate in global policies and regulations, and support coordinated decarbonisation strategies.

Limitations and future research

Despite its theoretical and practical implications, the present research has limitations. The reliance on a correlational design precludes causal inferences, and the modest effect sizes (e.g. correlation between financial literacy and willingness to decarbonise) suggest that the findings should be interpreted with caution. Hence, further experimental studies are necessary to replicate the findings and make causal conclusions. For instance, an experimental study that manipulates efficacy levels could isolate the relationship between climate literacy and behavioural willingness and buffer the decreased effect of financial literacy on behavioural willingness. Such an experiment might provide a clearer understanding of the nexus between climate and financial literacy and the willingness to decarbonise.

As we found the importance of climate literacy in encouraging decarbonisation, future research should explore the optimal educational programmes for consumers. For example, studies could investigate the most effective content and delivery methods for climate literacy education (Climate Change Education Network, 2024). Additionally, researchers could examine the long-term impact of different educational interventions on consumers’ decarbonising behaviour.

Future research will benefit from exploring potential moderators of the relationship between climate and financial literacy and willingness to take decarbonising action and purchase behaviours. For instance, personal values such as benevolence and universalism could enhance the relationship between climate literacy and behavioural willingness to decarbonise, while hedonism could weaken it (de Groot & Thøgersen, 2018). Additionally, demographic factors such as political ideology and affiliation could serve as another potential moderator (e.g. McCright et al., 2016).

Conclusion

The present research investigated the roles of climate and financial literacy in predicting willingness to decarbonise. In doing so, we introduced a new and comprehensive measure of climate literacy that captures knowledge of the causes, consequences and mitigation of climate change, as well as the roles of organisations involved in climate action. Our findings demonstrated that while climate literacy enhances individuals’ willingness to decarbonise by strengthening their sense of efficacy, financial literacy, in contrast, may undermine this willingness by diminishing individual efficacy, particularly among those with weaker environmental values. These insights offer significant theoretical and practical contributions, underscoring the need to integrate climate literacy education into broader educational and marketing interventions – alongside financial education – to promote decarbonising action. Finally, our climate literacy measure provides an important basis for identifying gaps in public understanding of climate change, thereby informing more targeted communication strategies and policy initiatives to enhance collective engagement in decarbonisation efforts.

Footnotes

Appendix A

Appendix B

Descriptive Statistics.

| Gender | N | % |

|---|---|---|

| Female | 539 | 45.6 |

| Male | 542 | 45.9 |

| Other | 1 | 0.1 |

| Prefer not to say | 2 | 0.2 |

| NA | 97 | 8.2 |

| Education level | N | % |

| Doctorate | 21 | 1.8 |

| Master’s degree | 120 | 10.2 |

| Graduate diploma | 48 | 4.1 |

| Graduate certificate | 25 | 2.1 |

| Bachelor’s degree with honours | 43 | 3.6 |

| Bachelor’s degree | 273 | 23.1 |

| Associate degree | 7 | 0.6 |

| Advanced Diploma | 54 | 4.6 |

| Diploma | 54 | 4.6 |

| Associate diploma | 15 | 1.3 |

| Advanced certificate | 23 | 1.9 |

| Certificate IV (or post-trade) | 46 | 3.9 |

| Certificate III (or trade) | 79 | 6.7 |

| Certificate II | 13 | 1.1 |

| Certificate I | 6 | 0.5 |

| High school graduate or equivalent | 187 | 15.8 |

| Some high school | 70 | 5.9 |

| NA | 97 | 8.2 |

| Marital status | N | % |

| Married | 496 | 42.0 |

| Widowed | 35 | 3.0 |

| Divorced | 87 | 7.4 |

| Separated | 19 | 1.6 |

| Never married | 320 | 27.1 |

| Living with partner (De facto) | 127 | 10.8 |

| NA | 97 | 8.2 |

| Employment status | N | % |

| Employed full time | 484 | 41.0 |

| Employed part time | 170 | 14.4 |

| Unemployed looking for work | 32 | 2.7 |

| Unemployed not looking for work | 12 | 1.0 |

| Self-employed/Freelancer | 60 | 5.1 |

| Retired | 230 | 19.5 |

| Student | 36 | 3.0 |

| Homemaker | 43 | 3.6 |

| Other | 17 | 1.4 |

| NA | 97 | 8.2 |

| Personal income | N | % |

| Less than $50,000 | 411 | 34.8 |

| $50,000–$69,999 | 169 | 14.3 |

| $70,000–$99,999 | 210 | 17.8 |

| $100,000–$149,999 | 161 | 13.6 |

| $150,000–199,999 | 47 | 4.0 |

| $200,000–$299,999 | 19 | 1.6 |

| $300,000 or more | 8 | 0.7 |

| Prefer not to say | 59 | 5.0 |

| NA | 97 | 8.2 |

|

|

N | % |

| Less than $50,000 | 219 | 18.5 |

| $50,000–$69,999 | 146 | 12.4 |

| $70,000–$99,999 | 170 | 14.4 |

| $100,000–$149,999 | 224 | 19.0 |

| $150,000–199,999 | 151 | 12.8 |

| $200,000–$299,999 | 78 | 6.6 |

| $300,000 or more | 29 | 2.5 |

| Prefer not to say | 67 | 5.7 |

| NA | 97 | 8.2 |

Appendix C

Results Related to Decarbonising Purchases and Purchase Intention

We asked whether participants had purchased products such as solar panels, an electric car, carbon offsets for travel and sustainable tourism to reduce their carbon footprint. If they indicated that they had not yet purchased these products, we then asked if they had considered doing so (in the binary choice option: yes [coded as 1] or no [coded as 0]). Four items related to their engagement in decarbonising action through purchases were provided, and the average score was used, which ranged between 0 and 1 (Mdecarbonising purchase = 0.19, SD = 0.239; see Appendix H for the full list of items).

If there were decarbonising purchases the participants had not done yet, then we asked their intention to purchase the option. The calculation for the intention was therefore: (the total number of ‘yes’ indications)/4 − (the total number of decarbonising purchase engagements). For example, if the participant had already engaged 3 of the given decarbonising purchases and was willing to take the remaining option, their intention score was 1 (i.e. 1/[4 − 3]). Those who had engaged all four decarbonising purchases from the option were treated as missing values in this calculation (N = 22). The average purchase intention score was 0.36 (SD = 0.363). The reliability score for mitigation purchases was 0.51, and the average purchase intention was 0.66 (see Appendix H for the full list of items).

A parallel mediation analysis using decarbonising purchases as an outcome variable was also conducted. The results with 95% bias-corrected confidence interval based on 5,000 bootstrap samples revealed that climate literacy was indirectly related to decarbonising purchases through its relationships with individual efficacy (total effect: b = 0.10, p < .001, indirect effect: b = 0.005, SE = 0.001, CI: 0.003, 0.007). However, collective efficacy wasnot the significant mediator of this relationship.

The indirect effect of climate literacy on decarbonising purchase intention was also examined. The results with 95% bias-corrected confidence interval based on 5,000 bootstrap samples indicated that climate literacy was indirectly related to mitigation purchases through its relationships with individual ability and outcome efficacy (total effect: b = 0.03, p < .001, indirect effect: b = 0.008, SE = 0.002, CI [0.005, 0.011]). However, collective efficacy wasnot the significant mediator of this relationship.

Financial literacy was not a significant predictor for decarbonising purchases (b = −0.001, F(3, 1,075) = 18.38, p > .1) or purchase intention (b = 0.001, F(3, 1,051) = 23.84, p > 0.1).

Appendix D

Decarbonising Purchase Engagement and Intention Items (Developed by the Authors)

Engagement: Have you previously ever purchased any of the following products? (yes/no)

Intention: Have you considered purchasing any of the following products? (yes/no)

Appendix E

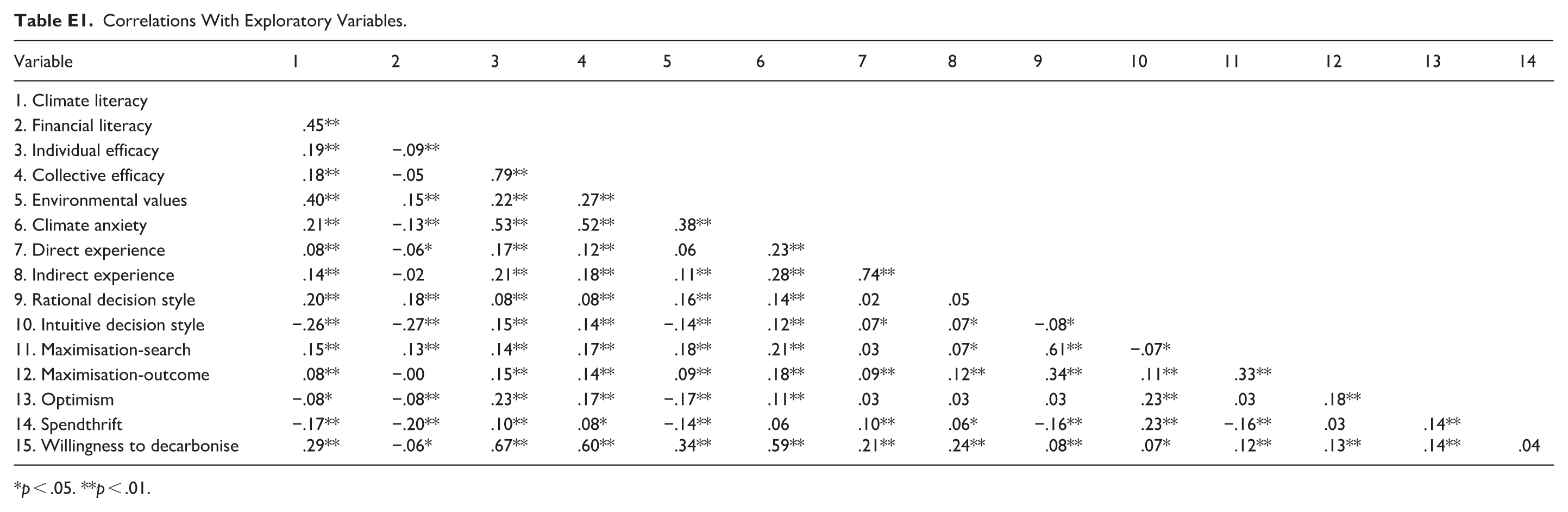

Correlations With Exploratory Variables.

| Variable | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. Climate literacy | ||||||||||||||

| 2. Financial literacy | .45** | |||||||||||||

| 3. Individual efficacy | .19** | −.09** | ||||||||||||

| 4. Collective efficacy | .18** | −.05 | .79** | |||||||||||

| 5. Environmental values | .40** | .15** | .22** | .27** | ||||||||||

| 6. Climate anxiety | .21** | −.13** | .53** | .52** | .38** | |||||||||

| 7. Direct experience | .08** | −.06* | .17** | .12** | .06 | .23** | ||||||||

| 8. Indirect experience | .14** | −.02 | .21** | .18** | .11** | .28** | .74** | |||||||

| 9. Rational decision style | .20** | .18** | .08** | .08** | .16** | .14** | .02 | .05 | ||||||

| 10. Intuitive decision style | −.26** | −.27** | .15** | .14** | −.14** | .12** | .07* | .07* | −.08* | |||||

| 11. Maximisation-search | .15** | .13** | .14** | .17** | .18** | .21** | .03 | .07* | .61** | −.07* | ||||

| 12. Maximisation-outcome | .08** | −.00 | .15** | .14** | .09** | .18** | .09** | .12** | .34** | .11** | .33** | |||

| 13. Optimism | −.08* | −.08** | .23** | .17** | −.17** | .11** | .03 | .03 | .03 | .23** | .03 | .18** | ||

| 14. Spendthrift | −.17** | −.20** | .10** | .08* | −.14** | .06 | .10** | .06* | −.16** | .23** | −.16** | .03 | .14** | |

| 15. Willingness to decarbonise | .29** | −.06* | .67** | .60** | .34** | .59** | .21** | .24** | .08** | .07* | .12** | .13** | .14** | .04 |

p < .05. **p < .01.

Appendix F

Appendix G

Financial Literacy Scale (Adapted from Houts & Knoll, 2020)

Instruction: In this section of the study, we will ask you questions about financial concepts. Please do your best to select the correct answer. There is no consequence to getting a question wrong. Each question is multiple choice and if you really don’t know and don’t want to guess, then you can select the option ‘I don’t know’.

Appendix H

Willingness to Take Decarbonising Action Measures (Adapted from Bradley et al., 2023)

To what extent do you agree or disagree with the following statements?

(1 = Strongly Disagree, 5 = Strongly Agree, NA = Not applicable)

Appendix I

Efficacy Measures (Developed by Camilleri & Larrick, 2019)

Individual ability efficacy

Individual outcome efficacy

Collective ability efficacy

Collective outcome efficacy

Appendix J

Environmental Values Measure: New Ecological Paradigm (NEP) Scale (Dunlap et al., 2000)

To what extent do you agree or disagree with the following statements?

(1 = Strongly Disagree, 5 = Strongly Agree)

Ethical considerations

This study was approved by the University of Technology Sydney Behavioural Lab Research Ethics Committee (approval no. ETH23-8040) on August 30, 2023.

Consent to participate

Respondents gave consent for review before starting the survey.

Consent for publication

Not applicable.

Data availability statement

The datasets generated during and/or analysed during the current study are available from the corresponding author on reasonable request.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article:

Funding support for this study was provided by a financial institution that played no role in study design, analysis, or interpretation of the data.