Abstract

The COVID-19 pandemic forced Australian consumers to pay greater attention to how local supply chains intersect with global networks, but this emphasis on local provisioning was part of a larger pattern of growth in small-scale and local production. Presenting findings from a representative national survey, this article identifies who is willing to pay more for locally made goods and how motivations for buying locally differ by age, income and gender. We found that the desire to ‘buy local’ was not dominated by any one demographic. Indeed, while ‘localism’ may be more associated with progressive individuals and communities, what was clear was that post-COVID consumer willingness to buy local was shared across the political spectrum. Consequently, we need to be attentive to the ways in which the desire to support local products and economies can become a space in which more progressive environmental goals and growing xenophobia can potentially become political bedfellows.

Introduction

Local production and purchasing took on new and more diverse characteristics during the COVID-19 pandemic as disruptions to supply chains and global mobilities contributed to increasing attention on how and where we shop and produce. However, the enforced emphasis on local provisioning during COVID-19 was part of a larger and extended pattern of growth across much of the Global North of purchasing and interest in participating in small-scale and local production. This growth has been motivated by increasing geopolitical instability, climate crisis, and national calls to restore sovereign manufacturing capacities, which had been gaining momentum in the decade or so prior to the pandemic. In Australia, for example, the number of Australian farmers markets more than doubled between 2004 and 2015 (Nelan et al., 2017). Then, as markets and supply chains were reconfigured under COVID-19, broader and more diverse shifts towards local purchasing and production emerged. Accenture's 2020 Consumer Pulse survey found that 56% of people in the 20 international markets it surveyed (including Australia) bought more locally sourced goods during pandemic lockdowns; 84% said they would sustain their local purchasing habits post-pandemic (Accenture, 2021). More recent surveys have found that 76% of Australian consumers frequently purchase locally sourced and produced products (Statista, 2024), and 73% are willing to pay more for Australian-made goods (Roy Morgan Research, 2023). However, the frequently higher cost of locally made goods raises ongoing questions about equality and access. This has become all the more pressing in countries such as Australia as inflation and interest rate rises coupled with growing income inequality have, post-pandemic, created compelling cost of living pressures for a sizeable portion of the population.

Against this backdrop, this article presents findings from a nationally representative survey of Australians, exploring their motivations for wanting to buy local and their capacity to do so. The overarching research question driving this study was, ‘Which (intersectional) demographics are most likely to be motivated and able to buy locally made goods, and what are their key reasons for doing so?’. Despite the greater prominence of local production and provisioning in recent years, small-scale, locally produced goods have continued to be understood as an option only for a niche, middle-class consumer market due to their combination of greater cost and the ‘bourgeois’ tastes they are perceived to represent (Starr, 2010). With much previous writing on localised consumption practices marking it out as a largely white, middle-class, often gentrified and frequently politically progressive market (Alkon & McCullen, 2011; Mallory, 2013; Parkins & Craig, 2006; Zukin, 2008), this analysis examines whether this remains true in contemporary Australia. By identifying who is willing to pay more for locally made goods, and why, this analysis explores how motivations for buying locally differ by age, income 1 and gender.

Literature review: buying ‘local’

Most of the scholarship on motivations for ‘buying local’ has focused on local food. This work has primarily occurred in the context of alternative food networks, including farmers markets, farmgate sales and community-supported agriculture. Research has consistently shown that consumers perceive that the shorter supply chains and the more direct relationships between producers and consumers facilitated by local production results in food that is fresher, better tasting, better quality, more trustworthy and more environmentally sustainable than food produced and distributed over greater distances (Carfora & Catellani, 2023; Dukeshire et al., 2015; Goodman, 2003; Hinrichs, 2003; Kovács et al., 2022; Reich et al., 2018; Young, 2022; Zhang et al., 2022). Decisions to purchase local food have also been understood to be motivated by a sense of embeddedness in particular locales and places (Goodman, 2003), and a commitment to local communities, businesses and economies (Dukeshire et al., 2011; Hinrichs, 2003; Kovács et al., 2022; Pratt, 2007; Reich et al., 2018; Smith & Lawrence, 2022; Young, 2022).

Much less is known about motivations for buying other kinds of ‘local’ goods. Research shows that those who buy local food tend to have an overall orientation to buying local in general (Dukeshire et al., 2015), underpinned by a desire to support local businesses, local economies and civic life (Schoolman, 2020), and to experience personalised relationships in the production and consumption process (Summers, 2022). Consumers’ motivations for buying locally produced beverages, such as craft beer and spirits, include a desire to maintain connections with local places, to position themselves against global (and national) markets and cultures, to differentiate their status through an emphasis on informed and carefully curated lifestyles, and to support environmental sustainability (Currid-Halkett, 2017; Flack, 1997; Graefe et al., 2018; Schnell & Reese, 2003). Environmental and ethical commitments are also a motivation for purchasing locally made household goods, clothing and other products (Diddi et al., 2019; Khan & Richards, 2021; Littler, 2008; Lusty & Richards, 2024; Summers, 2022). Beyond food and beverages, however, this only tends to be the case for ‘ethical consumers’: for other consumer groups, environmental factors hold little sway over local purchasing decisions (Schoolman, 2020).

Preferences for local production and purchasing are generally associated with high cultural and educational capital, though not always high income (Carfagna et al., 2014; Summers, 2022), despite the significant price premiums often associated with local purchasing (Chang et al., 2013). Consumers tend to be disproportionately white, female and older (45+ years) (Ashtab & Campbell, 2021; Bimbo et al., 2021; Dodds et al., 2014), although some studies also show increased local purchasing, particularly of local foods, by those under 30 (e.g. Kovács et al., 2022; Long & Murray, 2013). Schoolman (2020) found that, when exploring purchasing beyond local food, buying local is practised by a larger and more socio-economically diverse population than has been typically captured in previous studies, with even those with relatively low levels of education and income seeking to support jobs and businesses in their local communities.

Nonetheless, the generally higher cost of locally produced products has contributed to a growing literature focused on consumers’ willingness to pay more for local. A majority of studies have focused primarily on local food and beverages. Such studies tend to find a willingness to pay more for local food, particularly when local products are judged to be of greater freshness and quality, although willingness to pay can also depend on additional factors, such as convenience and accessibility (Chang et al., 2013; Feldman & Hamm, 2015; Mugera et al., 2017; Printezis et al., 2008). Older, wealthier people are typically more willing to pay more for local food (Feldman & Hamm, 2015). Australian research has found that women have higher willingness to pay than men (Mugera et al., 2017), although international meta-analyses (e.g. Feldman & Hamm, 2015) have found that, while women are more likely to purchase local food than men, men had a higher willingness to pay.

Studies of alcoholic beverages have found the greatest willingness to pay for craft beer produced in-state using local ingredients (Atallah et al., 2021), and a willingness to pay around 33% more for locally produced hard cider (Jensen et al., 2021). However, most studies of willingness to pay have focused on single products (e.g. cider, chicken) without capturing a more holistic view of people's purchasing motivations and decisions across a range of categories. Willingness to pay for locally produced products beyond food and beverages is largely unexplored in the literature, though research has found that women and highly educated people are more willing to pay for sustainably produced products such as clothing (Shah & Yang, 2022; Stringer et al., 2020), and people are willing to pay more for household goods and accessories when they are handmade (Fuchs et al., 2015).

Yet, there is no agreed definition in the literature as to what constitutes ‘local’ with respect to food and other products. Definitions of local food include distances (e.g. number of miles or kilometres), geographic boundaries (e.g. state, region or country), and ‘more holistic approaches’, such as the capacity for a personal connection with the producer (Feldman & Hamm, 2015; Zhang et al., 2022), though research suggests that locality (e.g. state or county) predominates in consumer understandings (Brune et al., 2023), with state, county, province or geographical area considered more ‘local’ than country (Carfora & Catellani, 2023; Dukeshire et al., 2011). For other products, such as clothing, household goods and furniture, definitions of ‘local’ are even more complex. This is in part due to the greater diversity and complexity of sourcing practices for goods like clothing and jewellery, as well as the ways in which digital technologies enable connections – and sales – of ‘local’ goods across geographic borders (Brown, 2014). In the case of clothing, personal accessories and household goods, for many Australians concerns over where an item is made tend to focus less on the local, and more on whether something is made overseas, particularly China, given that all too frequently ‘being an ethical consumer means holding and sharing racial stereotypes about Asian retailers and products made in Asia’ (Pham, 2022, p. 73). That much of the clothing available in Australia is made overseas can also lead to local consumers distancing themselves from the responsibility for working conditions, including the presence of modern slavery in the global fashion supply chain (Stringer et al., 2022). Nonetheless, most studies tend to understand ‘local’ as a smaller geographical unit than ‘country’, such as town, region or state (e.g. Schoolman, 2020).

Approach and methods

The survey data informing this article comes from the larger Australian Research Council Discovery Project DP220100110.

Survey and sample

This quantitative part of the larger mixed-methods research study was centred on a survey administered by ACSPRI (Australian Consortium for Social and Political Research Incorporated) through their Australian Survey of Social Attitudes (AuSSA, Wilson et al., 2025), which included custom research questions provided by the authors. The AuSSA draws upon a representative sample of adult Australians based on a random sample from the Australian electoral roll. The AuSSA comprised 5000 surveys administered across four waves between May 2022 and May 2023. Notably, this period marked the beginning of increasing cost of living pressures in Australia largely driven by rising interest rates.

The final survey sample included a total of 924 responses across four waves of data collection. Response numbers across Waves 1 (n = 235), 2 (n = 229), 3 (n = 226) and 4 (n = 234) were relatively consistent. Several socio-demographic variables of interest were collected within the survey including year of birth, total weekly income, gender (male, female, non-binary or ‘I use another term’) and subjectively rated class. Here, for brevity, ‘I use another term’ has been grouped with ‘NA' (not applicable).

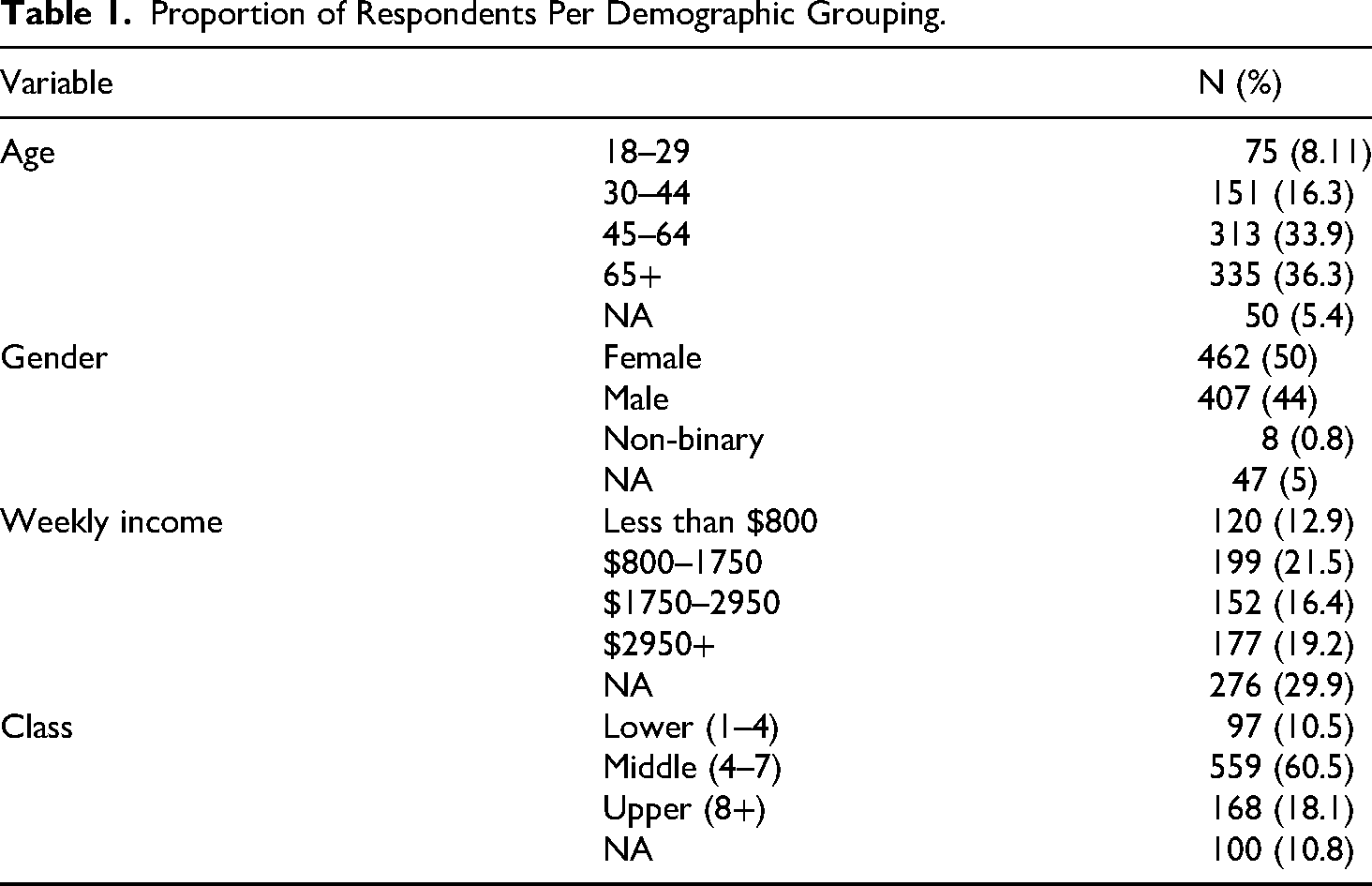

Respondents reported their weekly household income in an open-ended question, which was then categorised based on the Australian Bureau of Statistics (ABS) median household income statistics from 2022 (Australian Bureau of Statistics (ABS), 2022). Respondents were asked to rate themselves on a scale from 1 to 10 with the question: ‘In our society there are groups which tend to be towards the top and groups which tend to be towards the bottom. Where would you put yourself on this scale?’ This subjective class variable, which aims to capture self-assessed socio-economic class, has previously been used as a useful proxy measure of an individual's perceived social standing. This approach is seen as especially useful in the Australian context where there is a tendency for a large proportion of the population to identify as ‘middle-class’ regardless of income or other forms of capital (Jones, 2009; see also Tranter & Grant, 2018). The demographics of the final total sample are summarised in Table 1. Given 805 respondents identified as either ‘middle’ (60.5%) or ‘upper’ (10.8%) class, to identify local consumption as a ‘middle-class’ endeavour would have revealed little about the complex decision-making around what it means to ‘buy local’. Therefore, this analysis explored a wider range of intersectional demographic variables to more deeply investigate the interrelationships associated with local purchasing.

Proportion of Respondents Per Demographic Grouping.

Survey questions

Building upon the extant literature, the following questions were included in the survey to explore the individual motivations behind local purchasing, as well as to determine how much more people are willing to pay for locally produced goods. All the questions were designed to provide nuance around how decision-making occurs across varying kinds of household goods. The first question (Q1) aimed to capture differences in consumer considerations across nine product categories: Our household reliance on global supply chains has been made all too evident by the impacts of the COVID-19 pandemic. The Australian government has sought to boost the production of locally-made goods. Reflecting upon your household, what is your main consideration when buying products in the following product categories?

Possible responses were: ‘the best price or availability’, ‘produced as locally as possible’, ‘produced anywhere in Australia’, ‘produced overseas’, or ‘I don’t buy this’. Responses were sought across the following product categories: fruit and vegetables; meat, including smallgoods; wine and/or beer; spirits; clothing; furniture; other household goods (e.g. manchester/household linen, tableware); decorative items for the home; and personal accessories (jewellery, bags, etc.). The questions and responses were framed in this way to accommodate differing understandings of the ‘local’ across product categories. For example, as evidenced by the rise of farmers markets, which in Australia are focused on local fruit, vegetables, meats and dairy, ‘local’ for fruit and vegetables can mean hyper-local for those who live near major food-producing regions. In contrast, for goods less likely to be sourced in Australia such as clothing, furniture and other household goods, the emphasis on supporting ‘local’ can see the ‘local’ becoming equated with the ‘national’, that is, ‘Australian made’.

Questions 2, 3 and 4 aimed to investigate respondents’ underlying motivations for buying local by asking them to report their top-three reasons for buying Australian-produced goods, by numbering three boxes in their order of preference. These questions narrowed into three areas of interest: alcoholic beverages (beer, wine and/or spirits; Q2), furniture and household goods (Q3), and clothing and personal accessories (Q4). In further sections of the report, these are abbreviated to ‘alcohol’, ‘furniture’ and ‘clothing’. Drawing upon the extant literature, here, the available options to choose from were, ‘to support local economy and jobs’, ‘I wish to minimise the environmental impact of what I consume’, ‘better quality’, ‘more unique product’, ‘safer or more trustworthy’, ‘I prefer to support small business’, ‘I am concerned about labour conditions’, and ‘I like to know where and how it is produced’. In later sections, these are condensed into the following categories: ‘support local economy and jobs’, ‘environment’, ‘quality’, ‘uniqueness’, ‘trust’, ‘small business’, ‘labour conditions’, and ‘knowledge’, respectively.

The final question (Q5) aimed to determine how much more (if at all) respondents were willing to pay to buy local: An important part of access to locally grown or Australian produced products is the cost. Reflecting upon what your household is willing and able to spend, how much more (if at all) are you willing to pay for the following types of goods to buy local? (Please cross one box on each line.)

The full list of food and goods options was available, as for Q1. The possible responses were: ‘I do not pay more to buy local’, ‘Up to 25% more’, ‘Up to 50% more’, ‘Up to 100% more’, ‘More than double the price’, and ‘I do not buy this product’.

Analytical approach

All statistical analyses were conducted using R version 4.2.1 in RStudio (RStudio Team, 2020) with packages tidyverse v.1.3.2 (Wickham et al., 2016), car v.3.0.8 (Fox & Weisberg, 2019), effects v.4.2.2 (Fox & Weisberg, 2019) and oddsratio v2.0.1 (Schratz, 2017). Type II Wald χ2 tests from the car package (Fox & Weisberg, 2019) were used to provide p-value estimates. The results are presented in both beta estimates and odds ratios. In order to examine the complex intersectional attitudes and behaviours revealed by the survey responses, and to enable comparison across motivations for buying artisanal products (or not) or how much more respondents are willing to pay, this article presents an analysis of the findings in two blocks. The first brings together Q1 and Q5, while the second analyses the responses to the similar questions posed by Q2, Q3 and Q4. Bringing together the results from Q1 and Q5, binomial logistic regressions were used to provide an indicative picture of whether the respondents were willing to pay more for locally made goods, and how demographic factors predicted decision-making around buying different products. To investigate who prioritised buying locally, we modelled binomial responses (i.e. 1 = ‘produced as locally as possible’ or ‘produced anywhere in Australia’, 0 = all other options) by demographic variables (age, income and gender). Secondly, to examine who was willing to pay more for local produce, we modelled binomial responses (coded as 1 = ‘willing to pay more’, whether 25%, 50%, 100% or 200% more, and 0 = ‘I do not pay more to buy local’). For the ranking questions (Q2, Q3 and Q4), we used only first preferences for motivations to buy local to simplify the analysis process. Some 212 participants did not appropriately rank their preferences and were thus removed from the analyses. All models included sum contrast coding (see Brehm & Alday, 2022), whereby each group's responses were compared to the grand mean (instead of a reference to a ‘normative’ group). Exploratory analyses aimed to further understand the potential underlying motivations of willingness to pay more, by combining Q5 with considerations reported in Q2, Q3 and Q4.

Findings

What products, what ‘local’?

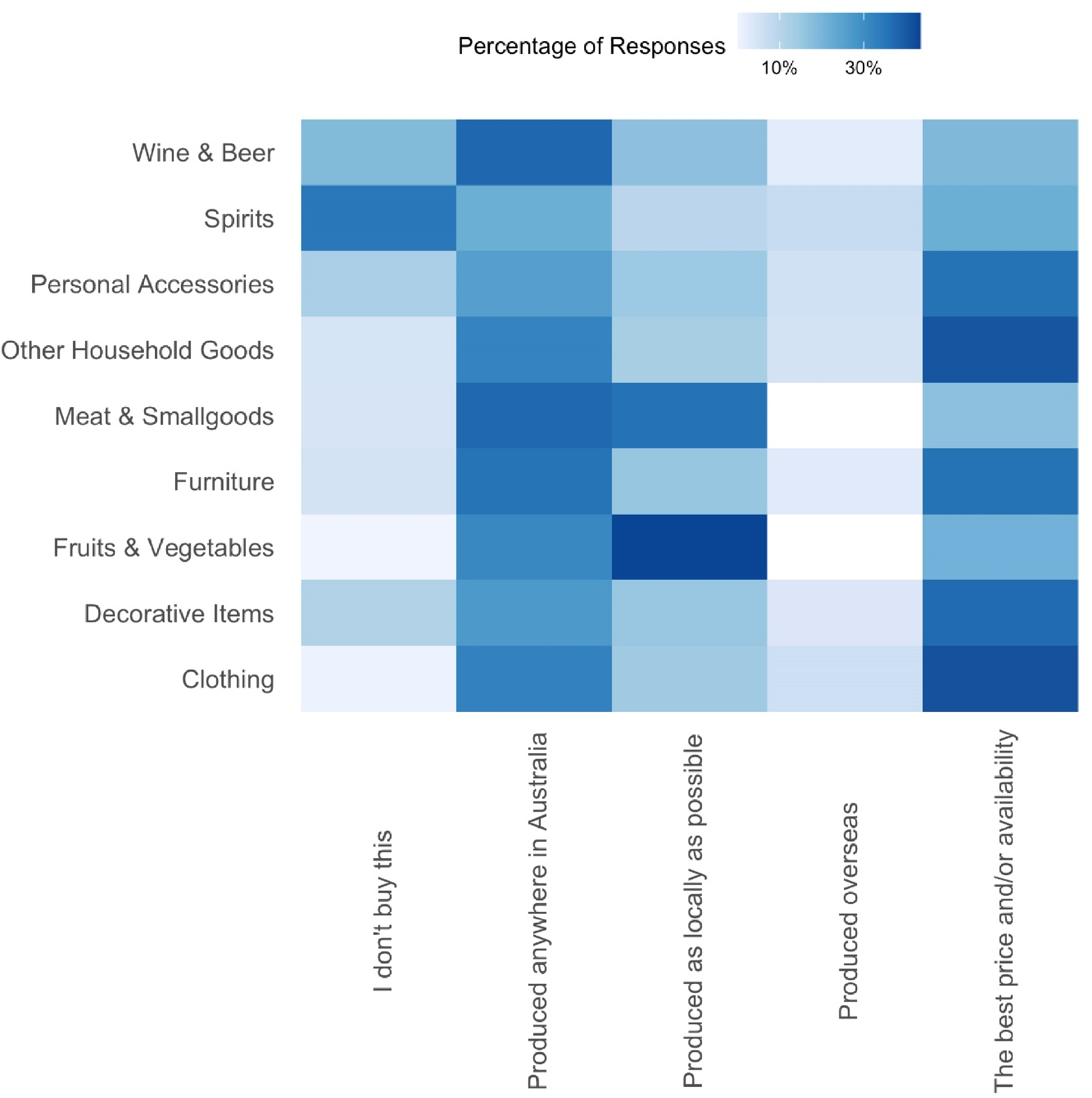

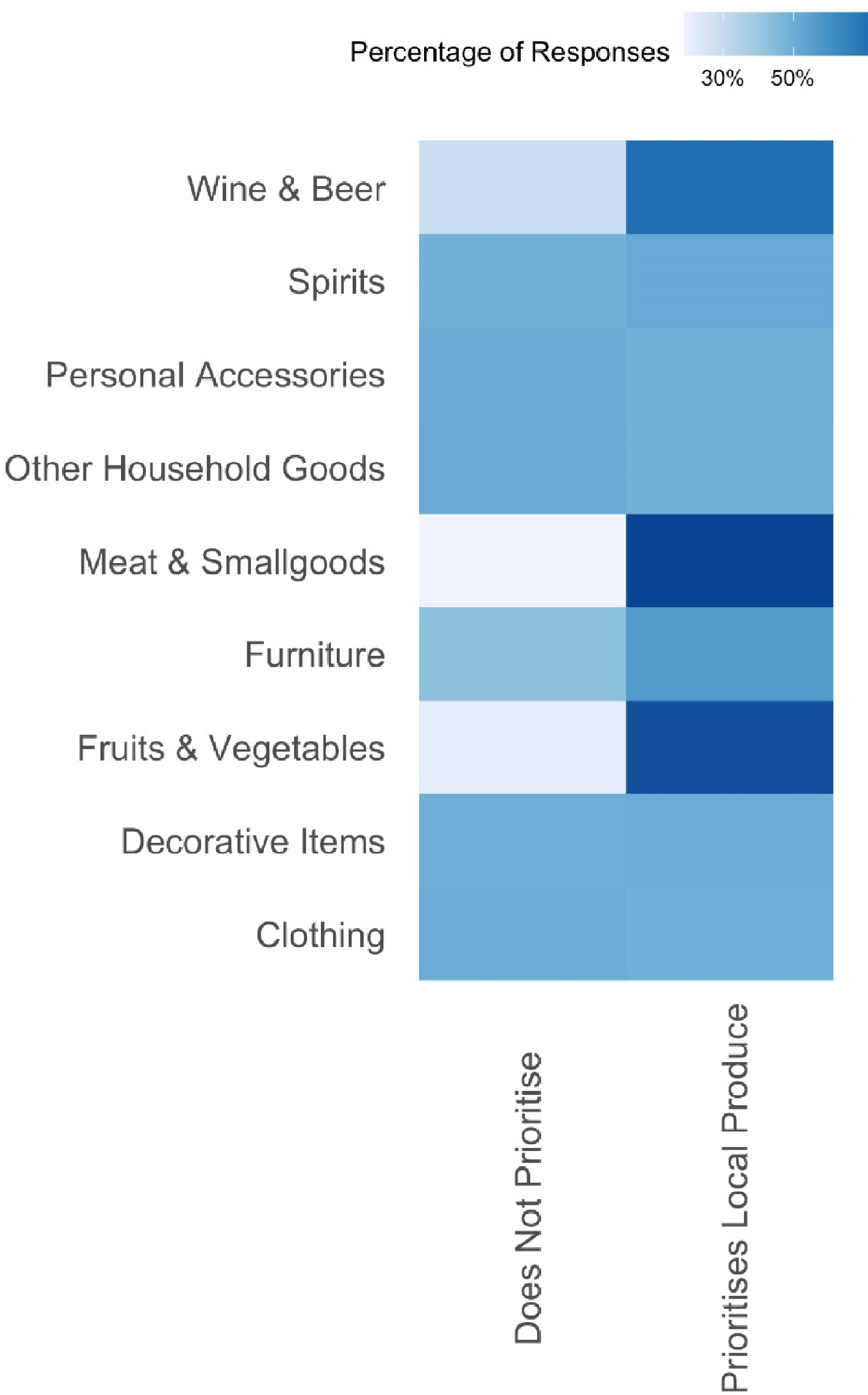

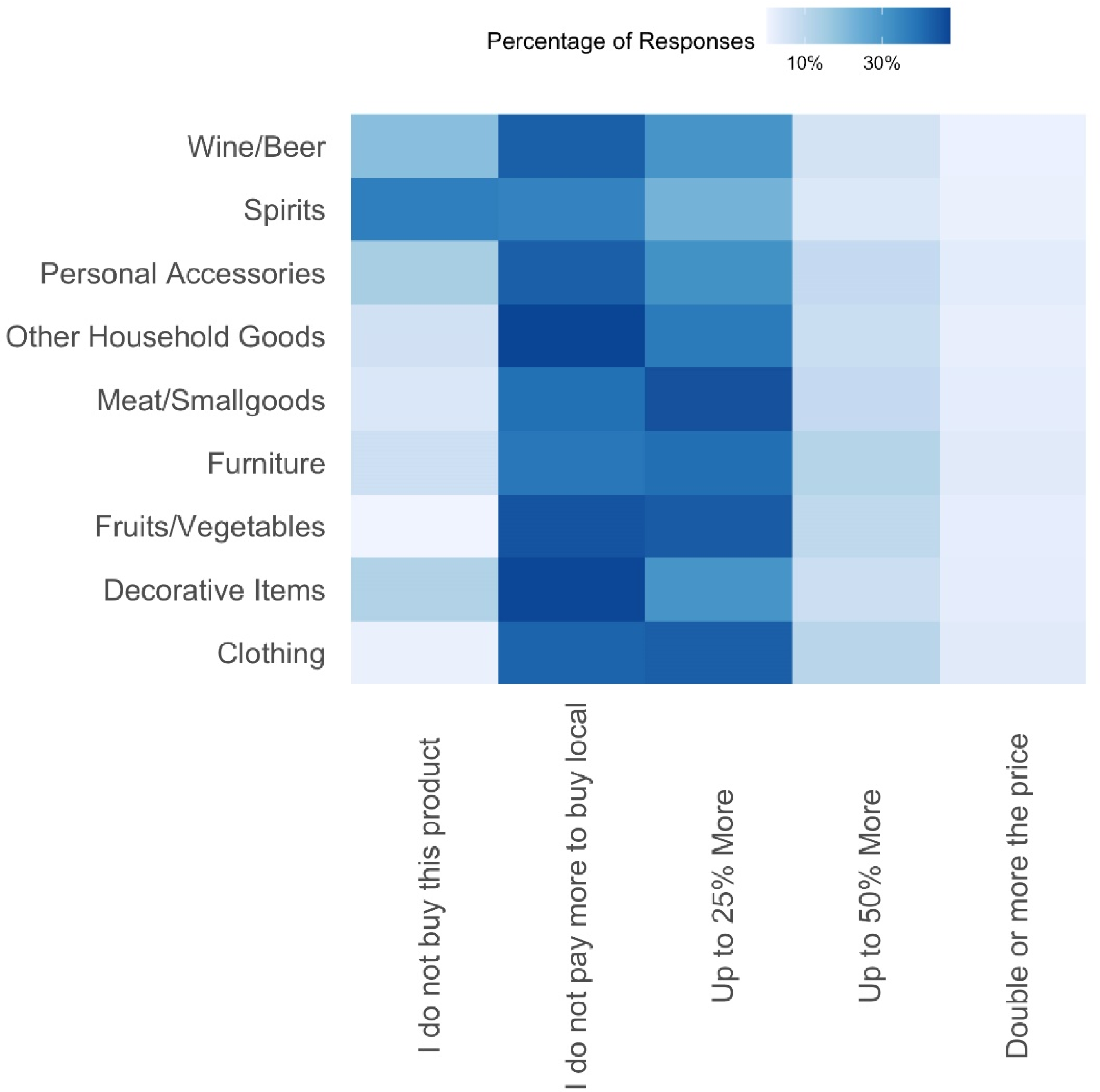

Looking at the responses to Q1 and behaviours around buying local, clear differences around whether the ‘local’ is sought out for various product groupings were apparent (see Figure 1). While there was a general trend to buy at least Australian across product categories, price point was also important in some instances. The results demonstrated that, across all categories, an average of 31.2% of respondents mostly considered buying products ‘produced anywhere in Australia’. Alternatively, 29.9% responded that they prioritised ‘the best price and/or availability’ and 19.9% responded ‘produced as locally as possible’. Some 10.2% stated ‘I do not buy this product’. For perishable food items there was a strong preference for ‘Buying as locally as possible’ (especially fruits and vegetables), or ‘anywhere in Australia’ (meat and smallgoods). Overall, there was a 50/50 split for ‘willing to pay more’ and ‘not willing to pay more’ for locally produced goods, which appeared relatively consistently across categories (see dichotomised results in Figure 2). The price point was the most important consideration for clothing, decorative items, furniture, other household items and personal accessories, reflecting the more limited availability and frequently (much) higher price point of these kinds of goods when made locally. In Figure 2, ‘produced as locally as possible’ is combined with ‘produced anywhere in Australia’ as ‘Prioritises Local Produce’ and all other options are indicated by ‘Does Not Prioritise’.

Summary of Q1 Responses Across Product Categories.

Summary of Dichotomised Q1 Responses Across Product Categories.

Who prioritises buying as locally as possible?

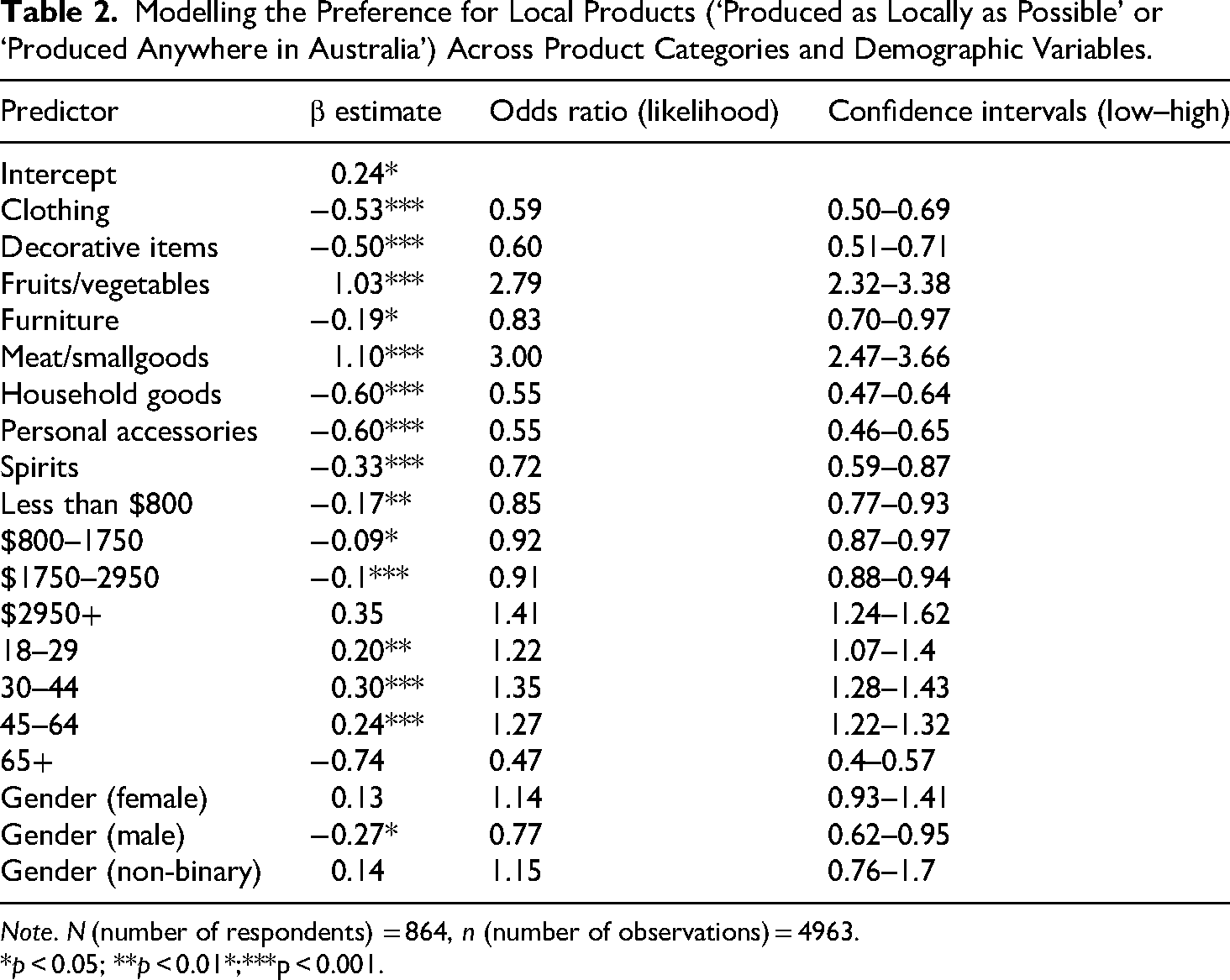

Drilling down into these Q1 responses more deeply, to understand how different demographic factors were associated with attitudes to buying local produce, we conducted binomial logistic regressions predicting a respondent's selection of either ‘produced as locally as possible’ and ‘produced anywhere in Australia’ (versus all other non-local options) by product category, age, income and gender. To restrict the sample to active consumers, ‘I do not buy this’ responses were removed from analysis. The model's results are depicted in Table 2. The results showed significant effects for product category (χ2 (8) = 455.53, p < 0.001), income (χ2 (3) = 36.54, p < 0.001), age (χ2 (3) = 186.54, p < 0.001) and gender (χ2 (2) = 40.05, p < 0.001).

Modelling the Preference for Local Products (‘Produced as Locally as Possible' or ‘Produced Anywhere in Australia’) Across Product Categories and Demographic Variables.

Note. N (number of respondents) = 864, n (number of observations) = 4963.

*p < 0.05; **p < 0.01*;***p < 0.001.

In regard to the former (‘product category’), this reiterates that the respondents were significantly more likely to consider buying as locally as possible for fruits/vegetables and meat/smallgoods and less likely to consider buying as locally as possible for clothing, decorative items, furniture (aligning with the relative lack of domestic manufacturing, hence the generally high price point for Australian-made furniture), other household goods, personal accessories and spirits (despite the burgeoning artisanal distilling sector in Australia), when compared to the overall mean. In terms of income, aligning with the perceptions of exclusivity around localised consumption often found in the literature, those in lower income brackets were significantly less likely to purchase locally. With regard to gender, those identifying as male were significantly less likely to consider locally produced purchases. Notably however, respondents in the 65+ age group were less likely to consider buying produce as locally as possible, when compared to the overall mean. Purchasing local products was reportedly considered less often by all three lower income categories (but interestingly, this was not mirrored in willingness to pay more, as will be seen shortly).

In the tables in this section, beta estimates (ß) demonstrate the effect of a category on the log-odds of considering local produce (with the intercept reflecting the overall mean inclusive of all conditions). This information can be more easily interpreted using the odds ratio (the exponential of the beta estimate). Here, odds ratios above 1 indicate greater odds of considering local produce while odds ratios below 1 demonstrate a decreased likelihood. Confidence intervals show where the likely ‘true’ odds are, estimated using the current sample. While the final categorical variable coefficients typically demonstrate redundant information within the models, they have been included here (in italics) to demonstrate the pattern of responses across all individuals.

Willingness to pay more for locally made

To establish how much more individuals are willing to pay for locally produced goods, we asked respondents to reflect upon how much their ‘household is willing and able to spend’ on local varieties of different products (Q5). The percentage of responses to each category is shown in Figure 3. The results demonstrated that, across all categories, a sizeable average of 48% of respondents would not pay more to buy local. Of the remaining, across all categories just over half of respondents were willing to pay more for locally produced goods, with the majority of them (41%) not willing to pay more than 25% more for locally made products, while 9% responded they would pay up to 50% more and only 2% responded they would pay ‘Double or more the price’. Some 11.3% responded ‘I do not buy this product’. It is notable that, among the items respondents reported not being willing to pay more for if they are locally produced, were decorative items and other household goods, which are parts of the Australian consumer market that have expanded rapidly over the last couple of decades with the arrival of relatively cheap mass-produced goods in these categories. This compares with clothing, likewise a sector that has seen a rapid expansion in the trade and affordability of goods as a result of the opening of global markets, but which has also been subject to increased scrutiny over both labour practices and the environmental impact of fast fashion (we explore consumer motivations in greater detail below). Due to the dichotomous nature of the findings (whereby most respondents either responded with ‘I do not pay more to buy local’ or ‘up to 25% more’), we recoded willingness to pay more as ‘1’ and unwillingness as ‘0’ for subsequent analyses.

Summary of Q5 Responses for Willingness to Pay More Across Product Categories.

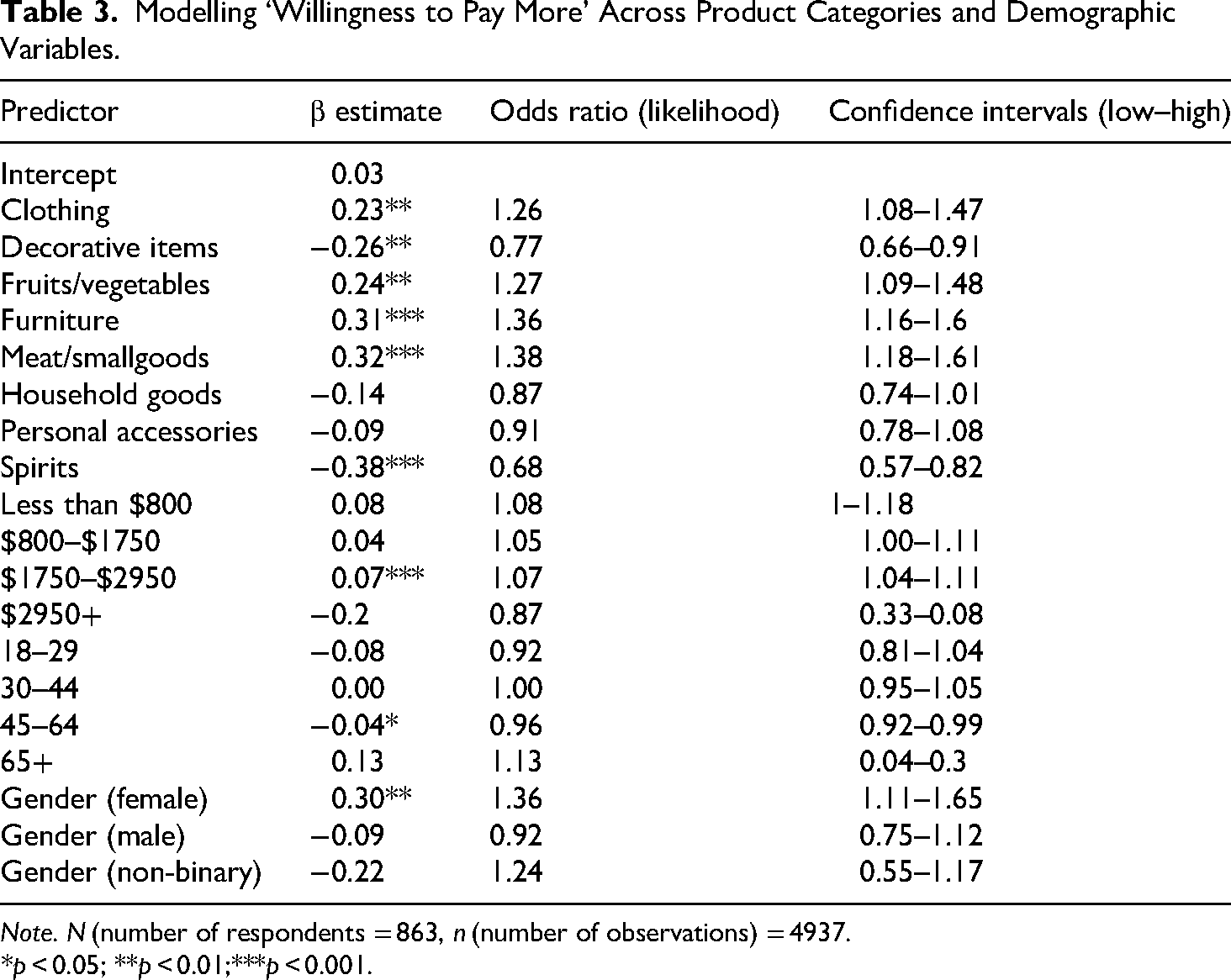

In order to understand how different product categories and demographic factors related to willingness to pay more, we conducted binomial logistic regressions predicting willingness to pay more by product category, age, income and gender. The model's results are depicted in Table 3. The results showed significant effects for product category (χ2 (8) = 76.91, p < 0.001), income (χ2 (3) = 19.77, p < 0.001) and gender (χ2 (2) = 46.15, p < 0.001). Here, the respondents were significantly more likely to be willing to pay more for locally sourced or produced clothing, fruits/vegetables, furniture, or meat/smallgoods but were significantly less likely to be willing to pay more for spirits and decorative items, when compared to the overall mean response. A significant effect of income was observed, where those in the second highest income category ($1750–2950 a week) were more likely to respond with willingness to pay more, compared to the overall mean. More broadly though, the responses demonstrated a trend in which those in the lower income brackets were more often willing to pay more, whereas those in the highest income bracket rarely reported being willing to pay more. For gender, females were significantly more likely to be willing to pay more, when compared to the overall mean. For age, those in the 45–64 age bracket were less likely to be willing to pay more, when compared to the overall mean.

Modelling ‘Willingness to Pay More’ Across Product Categories and Demographic Variables.

Note. N (number of respondents = 863, n (number of observations) = 4937.

*p < 0.05; **p < 0.01;***p < 0.001.

What consumer motivations underpin buying ‘local’?

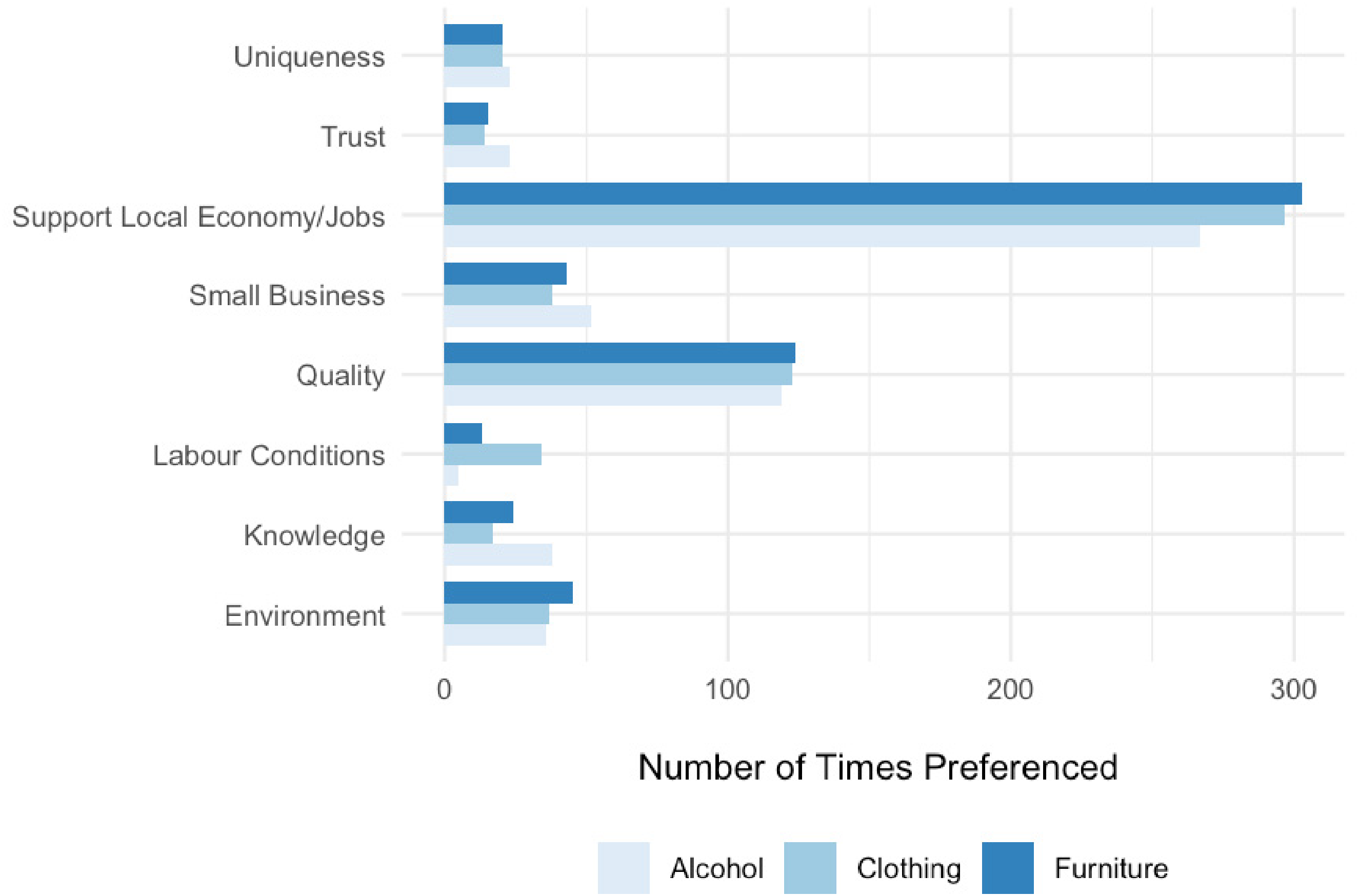

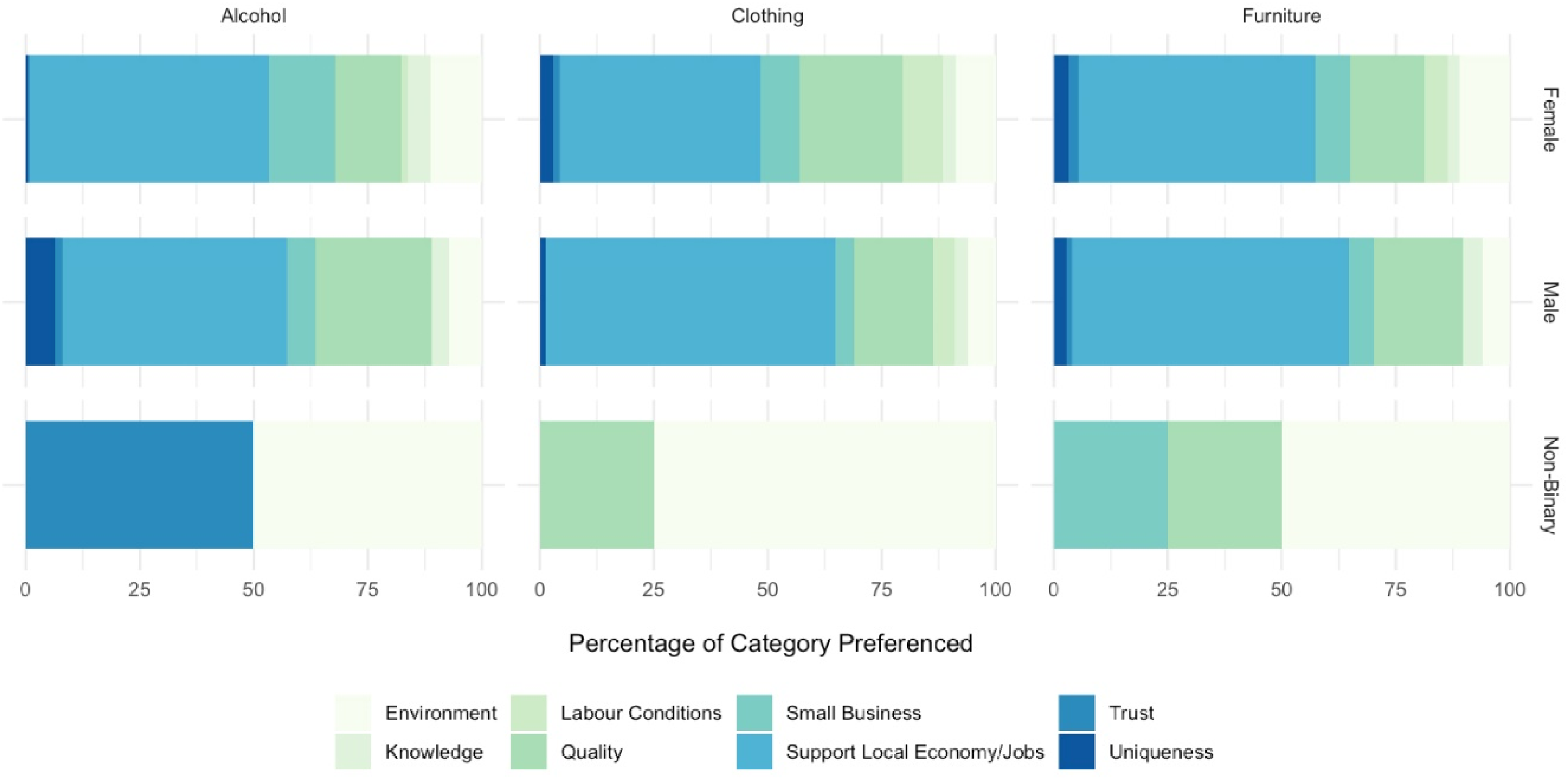

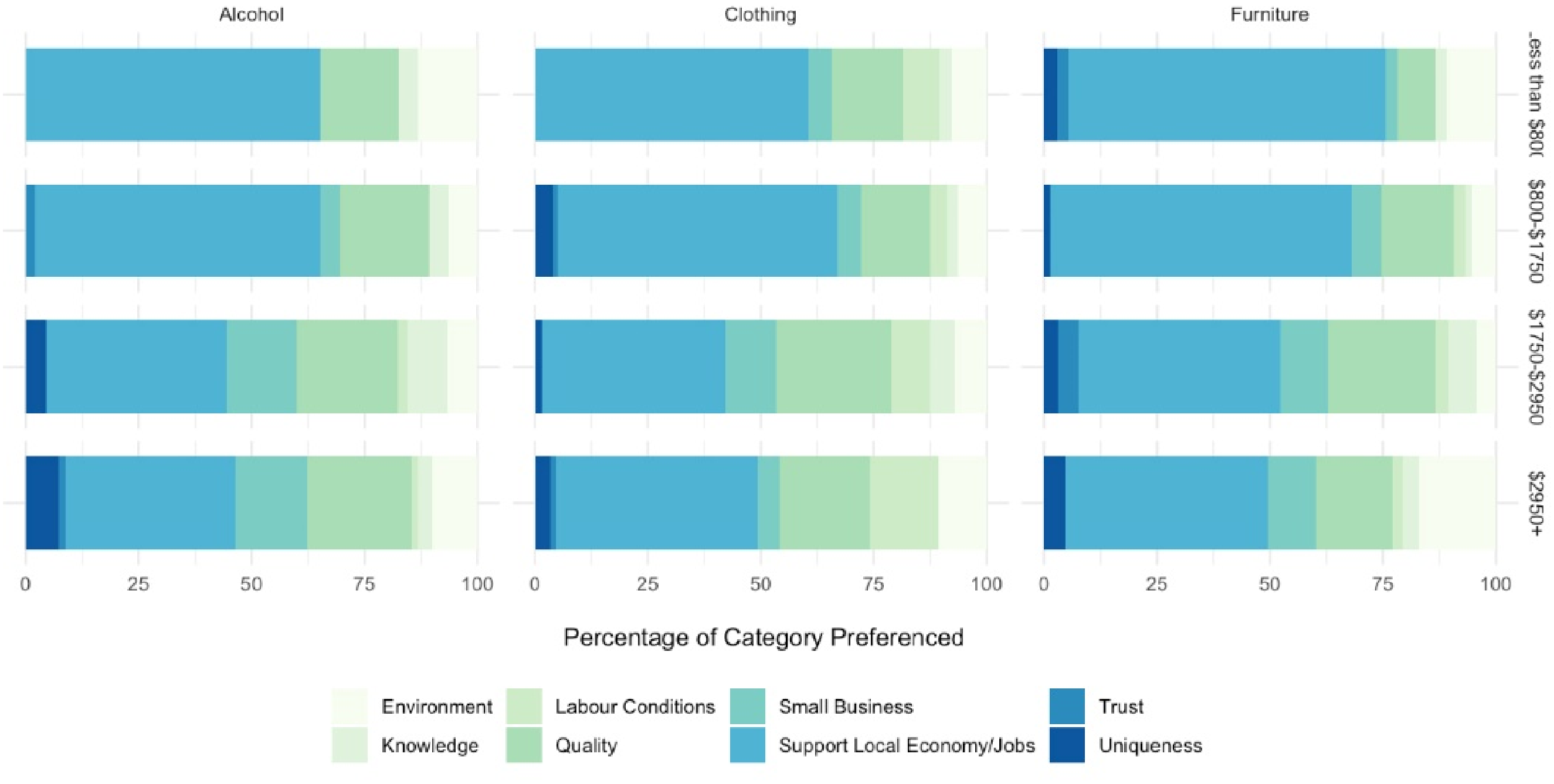

To understand the motivations behind buying local, we asked the respondents to identify the top-three reasons they would choose to buy local (Q2, Q3 and Q4). Figure 4 summarises the number of times each motivation was ranked as the first preference across each of the product categories of interest. The data demonstrated that ‘support local economy and jobs’, ‘quality’ and ‘small business’ were the three most chosen primary motivations when buying local. Notably, they were also the most commonly chosen second and third options, and thus motivations overall. This was consistent across all levels of product categories (alcohol, furniture and clothing). However, while the figures were largely consistent, building upon the trend emerging above whereby the respondents seemed to be more willing to pay more for locally made clothing, it was therefore salient that the option ‘labour conditions’ was most likely to be chosen for clothing. This contrasted with the response ‘I like to know where and how it is produced’ (‘knowledge’), which was chosen more often for alcoholic beverages. Interestingly, processes of visibility (or their absence) within local production economies, especially the small-scale or artisanal, seem to be in play here. Educating customers, foregrounding maker stories, cellar/brewery/distillery open doors and conducting tours are key parts of the promotional strategies and market points of difference for local alcoholic beverage producers. Likewise, the exploitative labour practices within the global (fast) fashion industry have achieved greater mainstream visibility, especially following the Rana Plaza disaster of April 2013 when 1134 were killed and many injured in the collapse of a building in Bangladesh, most of them garment workers producing clothing for well-known fast fashion brands.

Summary of Primary Motivations for Buying Local Across the Three Product Categories of Interest (Alcohol, Clothing, Furniture).

What motivations drive the willingness to pay more?

As a final, more exploratory analysis, we focused on our respondents who were willing to pay more (whether 25%, 50% or double the price; Q5) and investigated their first-ranked considerations for buying local across the three key product categories (Q2, Q3, Q4). We plotted these counts by income, gender and age, to understand how demographic factors were related to key considerations that paralleled individuals reporting a willingness to pay more. We note that these counts had smaller sample sizes than the above figures, as the observations relied on individuals successfully and accurately responding to the specific demographic questions, as well as providing responses for the subsequent combination of questions (alcohol n = 239, clothing n = 365, furniture n = 345).

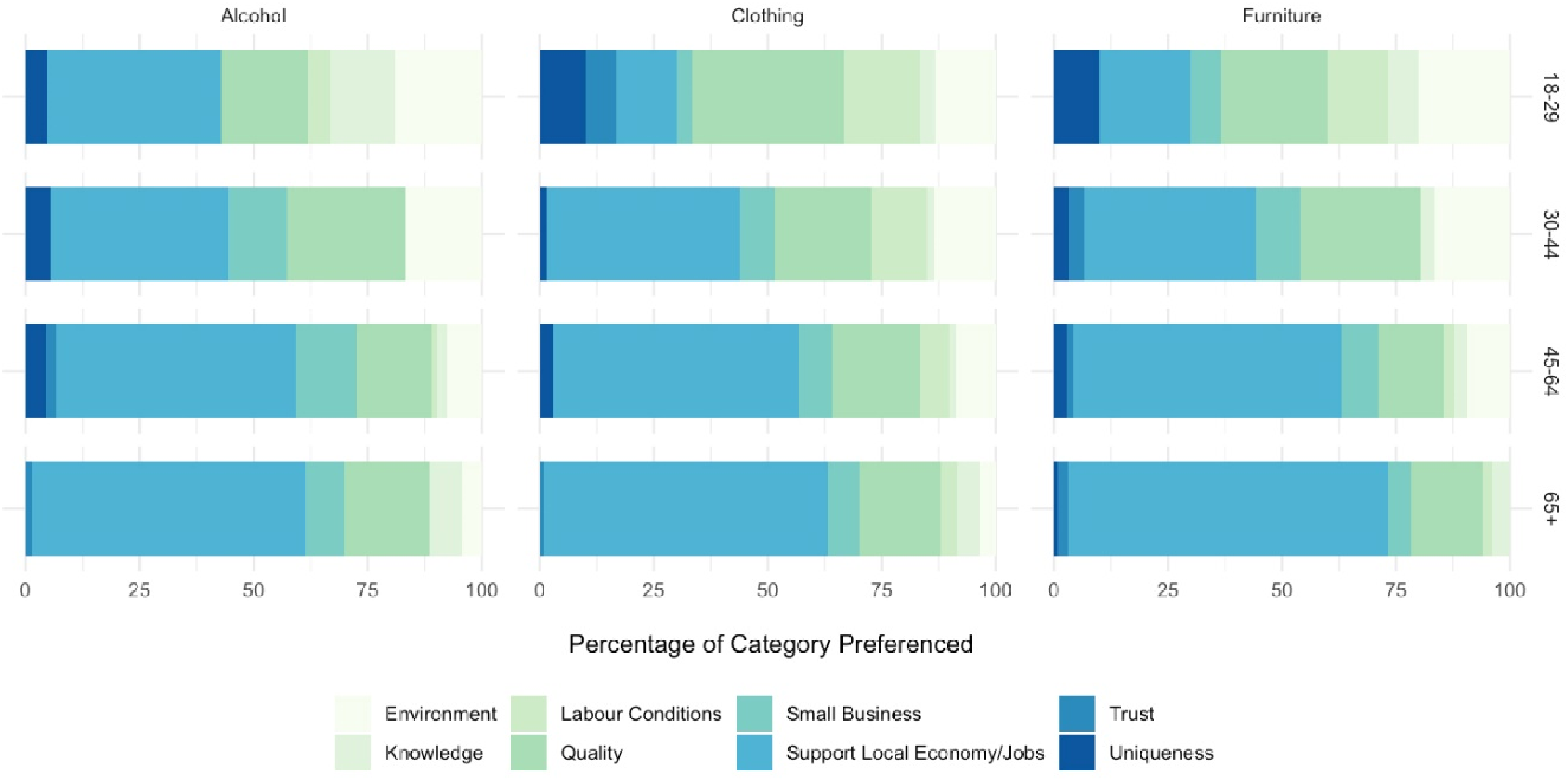

As above, the key consideration of ‘support local economy and jobs’ was relatively consistent, with small changes across younger age categories, non-binary respondents and higher income earners. Clearly the emphasis on supporting the local economy and jobs diminished across all product categories for younger respondents (Figure 5), as well as non-binary respondents (Figure 6) and higher income earners (Figure 7), and with other considerations (such as labour conditions and quality) being noted more frequently, when compared to other demographic categories. The data in this study has revealed micro-practices of difference, for example, young people being more concerned about the environment, and labour conditions being a stronger driver of decision-making for younger and female respondents when it comes to buying clothing and personal accessories. However, the increased importance of economic motivations for older respondents, combined with the reduced importance given to ethical or values-based considerations, suggest that prioritising ‘the local’ was not primarily a niche activity of those we might identify as from more liberal or (perceived) progressive demographic cohorts, as the literature can often suggest, but also included conservative motivations that reflected recent trends towards a more defensive consumer nationalism, as we discuss below.

Summary of Motivations for Self-Reported Willingness to Pay More Across the Three Product Categories of Interest (Alcohol, Clothing, Furniture) for Age Categories.

Summary of Motivations for Self-Reported Willingness to Pay More Across the Three Product Categories of Interest (Alcohol, Clothing, Furniture) for Gender Categories.

Summary of Motivations for Self-Reported Willingness to Pay More Across the Three Product Categories of Interest (Alcohol, Clothing, Furniture) for Income Categories.

Discussion

Writing pre-pandemic but post-global financial crisis, Currid-Halkett argues that, for what she refers to as the aspirational class, ‘the choice of particular fabrics, wood, or foodstuffs has to do with acquiring knowledge of what is superior, more environmentally friendly, and more humane’ (2017, p. 56). But the desire to ‘buy local’ is not dominated by any one section of the demographic spectrum, although the reasons and motivations change for different groups. The tendency in the literature to find that women are more likely than men to support buying local was also borne out here, but the fact that male respondents were far more likely than female respondents to seek out Australian-made beer, wine and/or spirits, as they saw them as ‘better quality’ and as ‘safer and more trustworthy’, perhaps points to the greater status that men can gain from alcohol purchases with perceived ‘authenticity’ markers (as opposed to more everyday household goods) (Thurnell-Read, 2019), as well as reflecting potentially less progressive motivators for buying local, including perhaps racist assumptions around the quality, safety and trustworthiness of goods made ‘elsewhere’ (see Pham, 2022). It was also significant that economic motivations – a desire to support the local economy and jobs – increased and other ethical and values-based motivations decreased as respondents aged, perhaps indicating a more ‘defensive’ form of localism that scholars have identified as elitist, exclusionary (particularly due to the generally higher price point of locally produced goods), and as appealing to ‘nativist sentiments’ (Hinrichs, 2003, p. 37; see also Goodman et al., 2014). Such responses should be understood in the context of growing calls for the reintroduction of tariffs and supporting local production, as well as calls to halt or significantly curtail immigration, which are finding some support across different parts of the electorate in countries such as the United States, the UK and Australia. The AuSSA asks respondents about their views on political parties, immigration and gender, and these responses were cross-referenced with various respondent demographics. The most notable and clear finding from this was that the primary motivation among older respondents in the survey to buy local in order to support local economy and jobs was simultaneously associated with more negative views about immigration.

The survey responses further revealed that the greater the income, the less motivations for buying local were focused on the local economy. Instead, local products were chosen for their ‘better quality’ and as a way to ‘minimise environmental impact’ (Figure 7). When considering potential reasons for this, it could be that people with the highest incomes may feel the consequences of local economic downturns less directly, and hence may be able to direct their purchasing towards personal (or wider ethical or status) motivations. It may also be that those in the lowest income brackets are in professions (e.g. hospitality, retail) that feel most directly the consequences of a thriving (or not) local economy. Note also the proximity of Australians in general to small business – ABS figures indicate that around 66% of the Australian private sector workforce is employed in small- or medium-sized enterprises (SMEs) (Phillipov et al., 2025) – which means that a large percentage of the population has had direct experience of SMEs having it tough during the COVID pandemic and then the subsequent cost of living crisis. It is also important here to note that income level does not necessarily map onto age, as within the sample there was a sizeable proportion of younger people with high incomes. This challenges assumptions that young people, on the whole, are not in a position to pay more for locally made, ethically sourced household items. Indeed, age-related trends around purchasing behaviours driven by concern for the environment were evident. Climate-focused considerations were a relative minor motivation for buying local across the sample, however, where they were apparent, this choice was a much stronger driver for younger age groups, and not even a top-three motivator among older respondents (Figure 5), likely reflecting Australian young people's greater environmental awareness and support for action on climate change (Colvin & Jotzo, 2021) and a perception that the simpler, more direct supply chains associated with local purchasing can assist with this.

Conclusion

The wider research project this survey emerged out of commenced in 2022 and was interested in examining the medium- to long-term impacts of the turn to local provisioning necessitated by the pandemic. In the Australian context, much of the media's initial focus during the pandemic, when both state and national borders were closed, was on encouraging consumer support for hyper-local artisanal levels of making, as distinct from the more highly impacted larger scale production that is more reliant on complex, international supply chains (Phillipov et al., 2023). Certainly, the time period of the survey (2022–2023) perhaps captures a shift away from the more progressive, community-focused, COVID-era support for buying local (Phillipov et al., 2023), towards not so much a defensive localism but, given the national scale of ‘buy local’ discourses in Australia, a potentially defensive nationalism. Indeed, overall, the picture that emerges here is a nuanced but generally consistent one. There was a strong desire across the survey respondents to buy local, with ‘to support local economy and jobs’ by far the dominant motivation. However, precisely because this was the case across the survey, what is clear is that there is no specific political alignment of buying local as the sole preserve of those identified as having left-leaning political views. For while ‘localism’ may have been more associated with progressive individuals and communities in the early adopter moment of initiatives such as farmers markets, what is clear in this data is that post-COVID consumer motivations to buy local are just as likely to be shared across the political spectrum. How the local is understood here varies across consumer items, but what is unambiguous in the case of this Australian study is that it almost always involves buying from within the country itself. This is in contrast to most international studies where ‘local’ is generally perceived to be a smaller unit than ‘country’ (e.g. Brune et al., 2023; Carfora & Catellani, 2023; Dukeshire et al., 2011; Schoolman, 2020). There has long been an active national ‘Buy Australian’ campaign to advocate buying ‘local’ in response to the removal of tariff protections for local production and the subsequent off-shoring of much manufacturing as part of wider patterns of economic globalisation (Phillipov et al., 2025). Therefore, it is interesting to look at this data when, at the time of writing, the decades-long moment of so-called free trade is being disrupted transnationally by the imposition of tariffs on imported goods by the United States and subsequent calls by impacted trade-partner countries to not buy US goods. Australia has not been immune to this budding global ‘trade war’ and, while the Australian government has not joined other countries in imposing counter-tariffs, there have been high-profile calls including from the Prime Minister to buy Australian to support ‘Team Australia’ (Crowley, 2025). Combined with a growing anti-immigration sentiment that has also been occurring simultaneously, culminating in anti-immigration ‘March for Australia’ rallies in all Australian capital cities in 2025, we need to be attentive to the ways in which the desire to support local products and economies can become a space in which more progressive environmental goals and growing xenophobia can potentially become political bedfellows obscured under homogenous notions of ‘community’ (see Goodman et al., 2014, p. 21).

Footnotes

Ethics approval

This research has Human Research Ethics Committee approval from both the University of Adelaide (H-2022-043) and University of South Australia (204603).

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Australian Research Council (Grant no. DP220100110).

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.