Abstract

Parents are increasingly providing financial support to their adult children. At the same time, it is often taking young people into their 30s to convert educational credentials into career outcomes, establish independent households, and marry or form partnerships. While the role of the so-called ‘bank of mum and dad’ in assisting with entry into home ownership is well established, its effects are potentially far wider, for example affecting young adults’ employment pathways. This article contributes to emerging research on extended intergenerational support using longitudinal data from Australia to explore which young people are receiving this support during their 20s and into their early 30s. Drawing on our findings, we contend that financial transfers as people enter their mid-20s and beyond appear to be used both to manage hardship and precarity, and to enable speculation on positive employment futures.

Introduction

Academics and policy makers in many countries are beginning to discuss the potential societal consequences of the ‘great wealth transfer’ due in coming decades. Over this period the Baby Boomer cohort, who have generally experienced positive (although unequally shared) opportunities for wealth accumulation, are set to reach the end of their lives and pass on inheritances to their children and other younger relatives. However, there is evidence that this wealth transfer has already begun, as parents are increasingly making inter-vivos (while living) transfers to support their children well into young adulthood, potentially reducing their own wellbeing and financial security in doing so (Maroto, 2017; Woodman, 2022). In Australia those aged 18–34 are in a weaker financial position than any living generation at a similar age (Productivity Commission, 2020), 1 and similar patterns are seen in other countries (see Chetty et al., 2017). This is due to low wage growth and young adults’ relative difficulty, compared to previous generations, with beginning to build assets.

In this environment youth researchers in Australia and across similar countries (primarily in the Global North) have shown that it is more often taking people into their 30s to convert educational credentials into career outcomes, to establish independent households and to build adult relationships (Bessant et al., 2017; Settersten Jr & Ray, 2010; Tanner & Arnett, 2017; Woodman & Wyn, 2015). Significantly, most people in Australia now receive direct financial support from parents at some point during their 20s and 30s, with transfers to the 25–34 age group growing most rapidly (Productivity Commission, 2020). Over 80% of 18- to 21-year-old Australians now live in the family home, up from 51% in 2001. Indeed, even by their late 20s, 30% of Australians live with at least one parent, up from 15% in 2001, saving approximately $20,000 (AUD) a year compared to living independently (Wilkins et al., 2019).

Many of the intergenerational supports once associated with teenage years now continue further along the life course for a greater number of people (Woodman & Wyn, 2015). It is established that these financial transfers influence people's housing trajectories (Cook, 2021; Troy et al., 2023), but the effects of the ‘bank of mum and dad’ are likely to be far wider, potentially affecting career, relationship, and health and wellbeing outcomes, for example through minimising the effects of employment precarity (Woodman, 2022). Researchers are beginning to attend to this extension of parental support well into people's 20s and 30s (Maroto, 2017). This is crucial given this period of young adulthood is increasingly central to significant housing, relationship and career transitions, affecting both young people and their parents (Woodman, 2022).

Using the Life Patterns project, a unique mixed-methods dataset that has tracked Australians from the end of high school when they were in their late teens, through their 20s and into their 30s, in this article we identify who among the participants is receiving this intergenerational support at different ages. We begin by considering existing research on how parental resources can support successful education to employment transitions. We then consider how the relationship between intergenerational assistance and life outcomes has been conceptualised in recent work on the ‘asset economy’, highlighting how our study builds on and augments this research. We move on to present the methods, findings and discussion. We ultimately contend that financial transfers are provided to these Australian young people for reasons beyond assistance with home ownership, that patterns of receipt change as young adults age, and that they are provided both to assist young adults to ‘get ahead’, and to mitigate experiences of precarity or financial insecurity.

The impact of parental resources on young adults

The link between qualifications and employment outcomes has become increasingly complex in recent years. Although the labour market in Australia is currently strong, driven by an increase in economic activity following the pandemic, part-time and casual employment has been embedded as a common employment status for people in their 20s for several decades, including for many with higher degrees (Venn et al., 2016). Many highly sought-after educational trajectories, as well as prestigious and (in some cases) highly remunerated career outcomes, are linked to extended periods of seeming insecurity (Friedman & Laurison, 2020; Morgan & Nelligan, 2018;). Support from parents during young people's 20s and 30s may be of increasing importance not just for alleviating the effects of employment with poor conditions and providing access to networks, but also for navigating extended career trajectories with the potential for high rewards in relation to status, remuneration and autonomy (Woodman, 2022).

In addition to extended periods of time spent in insecure employment, the average rate of home ownership has decreased over time for young adults: those aged 30–34 had an ownership rate of 50% in 2021, compared to 64% in 1971, and those aged 25–29 had a rate of 36% in 2021, compared to 50% in 1971 (AIHW, 2023). Additionally, according to the 2021 Australian Census, the median age of parents at the birth of their child is at its highest level since records began (31.7 for mothers and 33.7 for fathers) (ABS, 2022a), and the average age of first marriage was 34 for those aged 25–39 in 2021, compared to 27 for those of the same age in 1991 (ABS, 2022b). Income insecurity and insecurity of housing tenure has been linked with difficultly establishing and maintaining couple relationships and with conflictual parent–child relationships (Strazdins et al., 2006). Parental support may mediate the impact of insecurity on young people's relationship patterns – including which young people can pursue potentially high-reward career paths with extended insecurity while being able to build adult relationships and make family formation decisions at the same time (Woodman, 2022). An emerging literature also suggests that norms and practices of intergenerational financial assistance may be gendered, with daughters more likely to receive support (Goodsell et al., 2015; Tisch & Gutfleisch, 2022) in the context of enduring gender pay gaps.

The sociological study of young people's trajectories into adulthood has a substantial history. Famously, Bourdieu (1979) showed how, through the mid-20th century in France, social and cultural transfers grew in importance relative to direct financial inheritance in explaining the reproduction of social positions. In the 21st century in many countries, including Australia, it is clear that family financial support is becoming a more important resource in a context marked by a narrowing of government support for young people, growing employment precarity, and extended uncertainty in other areas of life (Taylor, 2023). However, questions remain about who is receiving this support at different points in the life course and in different contexts. Focusing on young people in Australia, we seek to address these questions in the present article.

The relationship between assets and employment

Recent research has addressed the relationship between assets and life outcomes, with a particular focus on members of younger generations. Much of this work finds its genesis in Piketty's (2014) claim that growth in income from employment has not kept pace with growth in rates of return on assets over recent decades, returning to an older pattern that weakened during the mid-20th century. Standing's (2016) recent work has built upon this account by articulating a new class schema which accounts for both employment and assets. Adkins et al. (2020, 2021) have similarly sought to develop a class schema that elevates the significance of asset ownership over that of employment in determining one's social class, and ultimately one's life chances. Notably, unlike Standing (2016), Adkins et al. (2020, 2021) do not include occupations in their class schema, and only consider employment in relation to whether an individual receives income from wages (as opposed to returns on investments). Adkins et al. (2021) also highlight not only asset ownership but also proximity to asset ownership, as a significant factor shaping life chances; for instance, receiving ‘in kind’ transfers by living rent free in a property owned by someone else (typically a parent).

This work has highlighted important recent shifts in the relationship between assets and employment, bringing attention to the relationship not only between asset ownership and life chances, but also between proximity to assets and life chances. However, scholarship has yet to provide much direct guidance on the mechanisms by which proximity to assets may strengthen life chances. Where this topic has been addressed, discussion has focused on intergenerational wealth transfers provided to aid members of younger generations with entry into property ownership (Adkins et al., 2020), a topic that has received empirical treatment both in Australia (Cook, 2021) and other countries (see Manzo et al., 2019; Suh, 2020). The literature has remained comparably silent on the question of how these transfers shape or interact with other life outcomes, especially for young adults who are no longer at the age at which they are likely to receive family financial assistance with the costs associated with being in higher education. 2 While the work of Piketty, Standing and Adkins, Cooper and Konings has been critiqued eslewhere based on its treatment of employment – with Christophers (2021, 2022) contending that these authors have given less consideration than required to the significance of assets owned by corporations – in this article we consider the relationship between proximity to assets and employment in a somewhat different way. Specifically, we consider whether receipt of family financial assistance corresponds with statuses other than home ownership for a cohort of Australian young adults. In doing so we contribute to providing a fuller picture of the role of proximity to assets (gauged through receipt of family financial assistance) in shaping young adults’ life chances.

Methods

This article investigates who is receiving financial transfers from parents at different ages and the characteristics of these young people, drawing on a longitudinal dataset tracing the lives of participants who finished secondary school in 2006 across three states and one territory in Australia. The study uses both repeated survey questionnaires and qualitative interviews and this article draws on data from both, using the interviews to inform two illustrative case studies. The cohort of school leavers who we focus on in this article began with a sample of 3977 participants. The sampling strategy was designed to recruit a sample that was representative of the cohort of students in year 11 in 2005 in relation to gender and school sector (i.e. public, independent or Catholic). In service of this aim, a stratified cluster selection process took place in which schools were selected at random within the relevant state and sector cluster. The whole year cohort within the selected schools were invited to participate. Additionally, a top-up sample of 348 students enrolled at Technical and Further Education (TAFE) institutions in NSW and Victoria were recruited into the sample in 2009 in response to higher levels of attrition among men and those who were not pursuing university study in the original sample.

As is common in youth transition studies, there has been significant attrition and, despite this top-up, the sample now includes an over-representation of women and people with tertiary qualifications. While some datasets available in Australia, such as the Household, Income and Labour Dynamics in Australia (HILDA) Survey and the Longitudinal Study of Australian Youth (LSAY), are more representative, the benefit of the Life Patterns project is a high number of participants in the relevant age groups and data that extends further through the life course than most longitudinal studies of youth (for instance, LSAY stops collecting data at the age of 25). Additionally, HILDA asks about gifts from family, but does not include loans. This is problematic for research on family financial assistance, in which the difference between loans and gifts is indistinct and subject to change over time (Heath & Calvert, 2013). Notably, the Life Patterns project includes questions about both gifts and loans.

While the Life Patterns project only collects data about those receiving family financial assistance – rather than those providing it – we use data collected from participants about their parents in conjunction with findings from existing research to extrapolate about this group. Specifically, existing studies have found that parents are far more likely than any other family member to provide financial assistance (Suh, 2020). For this reason, although the survey question that we draw on asks whether the respondent received a ‘gift from family’ or ‘loan from family’ in the previous 12 months, we are confident in assuming that the majority of our respondents likely received ‘family financial assistance’ from parents. Additionally, in support of our aim of better understanding how proximity to assets is translated into advantages for young people, we use data collected from the respondents about their parents to support our assumption that they are likely to be asset holders. This is based on home ownership rates of 75–82% among these parents’ age cohorts (depending on their year of birth) (AIHW, 2023), as well as their high rates of tertiary qualifications (more than double the national rate for their age cohort; ABS, 2022c) and professional occupations, each of which are correlates of higher lifetime earnings for members of their age cohort (Daly et al., 2015).

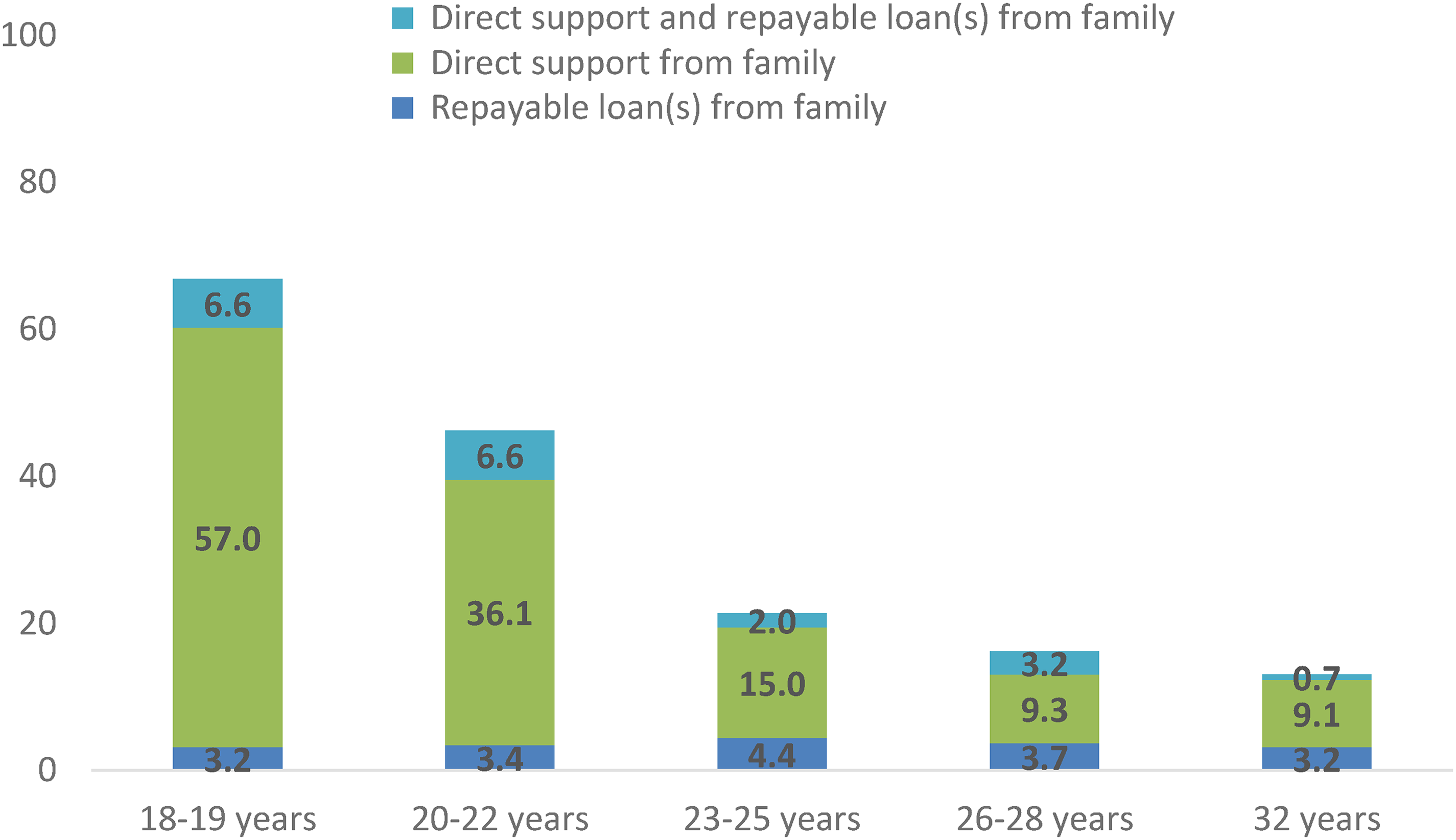

Our analysis combines descriptive statistics to identify broad patterns in practices of intergenerational financial assistance and statistical modelling to estimate the strength of association between different social characteristics and receipt of financial support from family at different points in time in young people's transitions. The descriptive analysis allows us to estimate how common conditional and non-conditional forms of intergenerational transfers (i.e. loans and gifts) are (see Figure 1). It also allows us to hint at the relationship between access to financial support from family and other dimensions of economic life, such as home ownership and financial (in)security (see Figures 2 and 3).

Probability of receiving different forms of family financial support, by age (%).

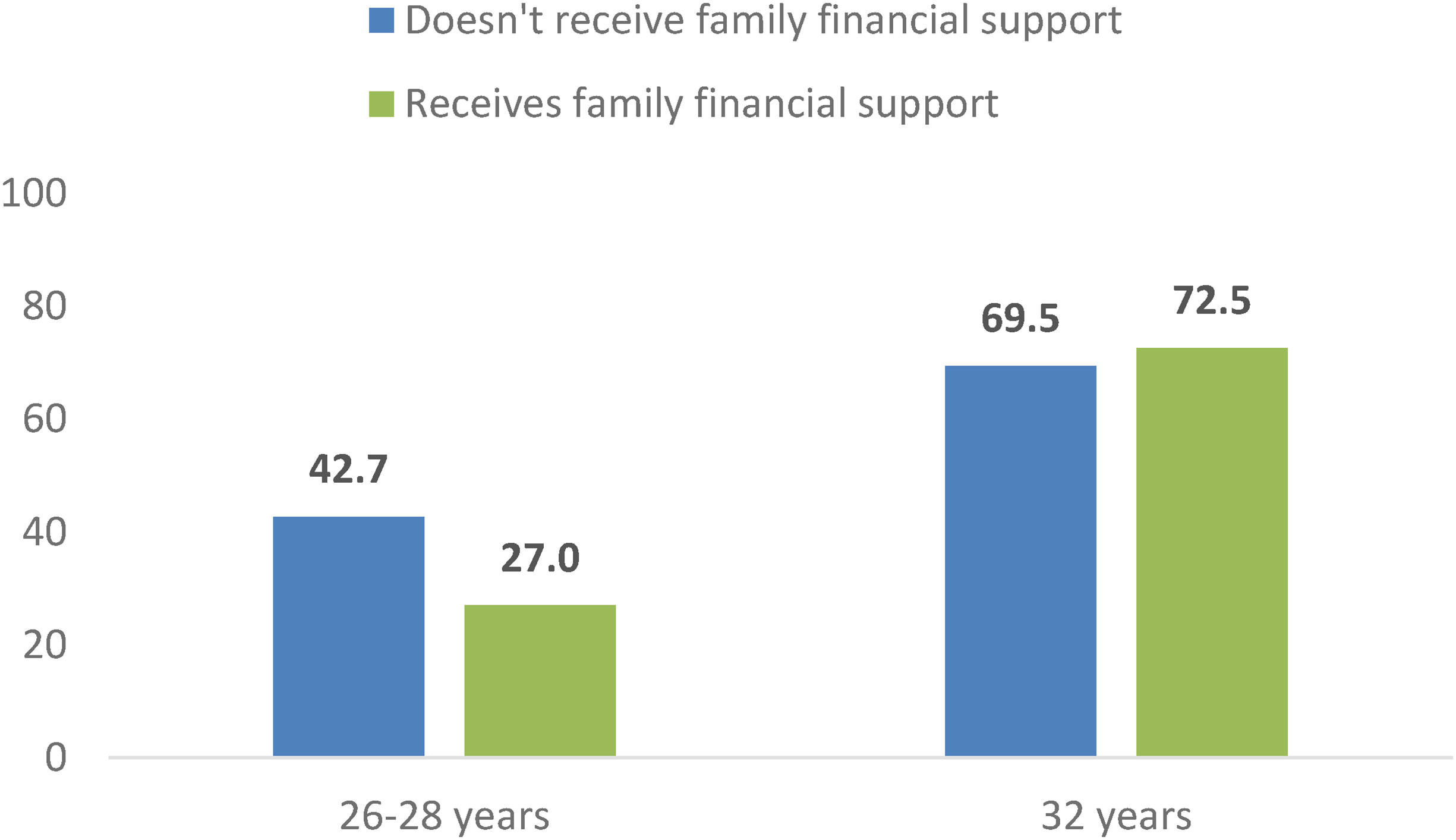

Home ownership rate among those who do and do not receive family financial support, by age 32 (%).

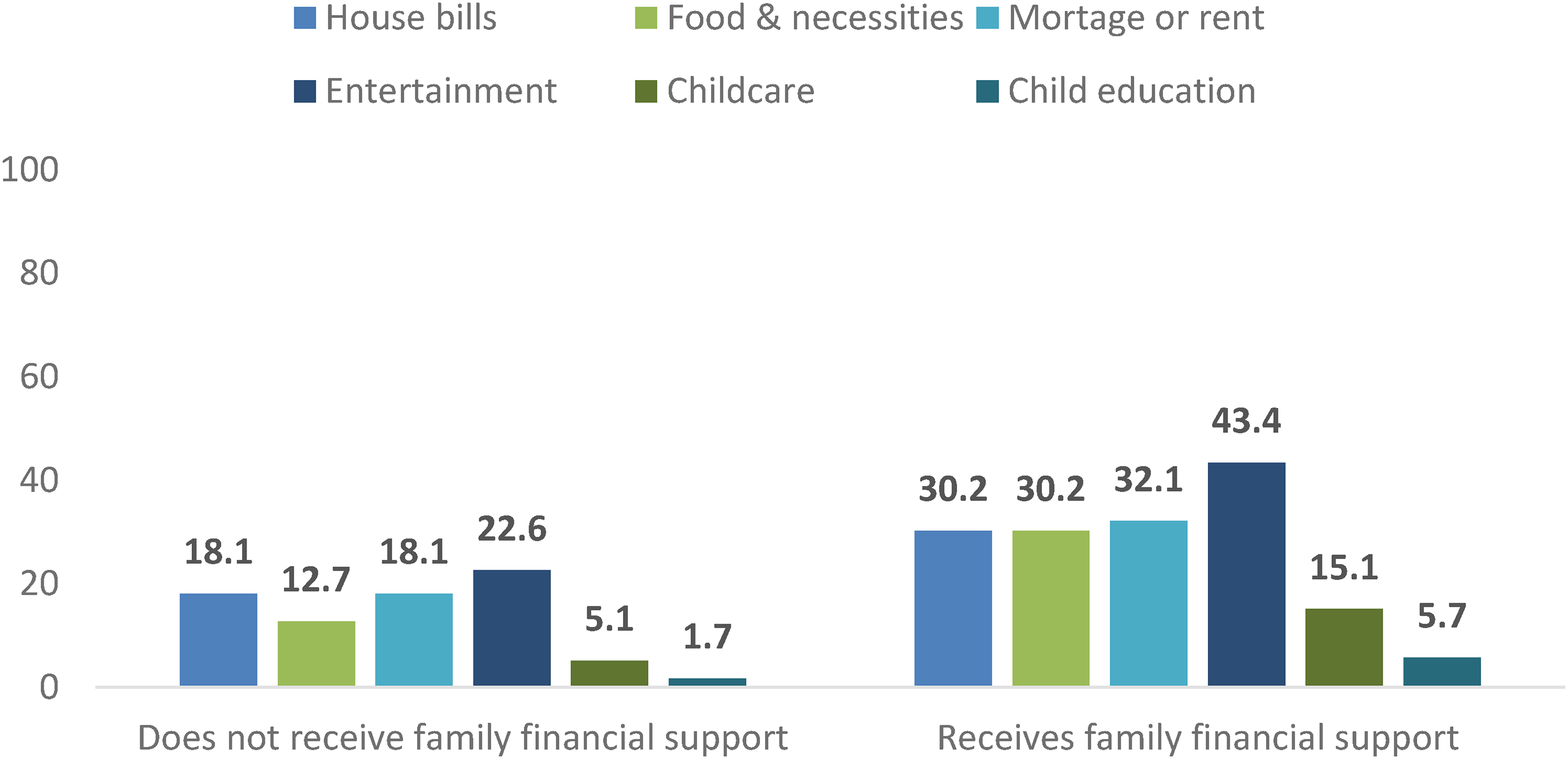

Probability of reporting difficulty paying bills, by receipt of intergenerational financial support and expenditure category (32-year-olds, %).

For the statistical modelling, in order to jointly examine the relationship between age, various social characteristics and intergenerational transfers from family, we conduct a longitudinal analysis of the likelihood of receiving financial support from family. The analysis focuses on respondents aged 20–32 years. The analysis is conducted using four time points to enable a more granular analysis than would be the case when using two basic categories, for example younger youth (e.g. under 25 years of age) and early adults (e.g., over 25 years of age). For the first three time points (i.e. ages 21 years, 24 years and 27 years), we pool responses from consecutive waves (t-1, t and t + 1) in order to minimise the risk of type II error, that is, missing occurrences of intergenerational transfers taking place between these time points. For each of these three time points, we code as receiving support all respondents who report receiving support in at least one of the three pooled waves. The final time point is based on a single wave to focus specifically on the most recent available survey data, with a three-year gap for ages 29 to 31 years, when questions about financial support from family were not included in the surveys. Given the dichotomous nature of the dependent variable (intergenerational financial transfers/support based on a ‘yes/no’ question) and its availability across multiple waves of the study, we use a repeated measures logistic regression to estimate the relationship between this outcome and a range of predictors.

In fitting the model, we include both time-varying and time-invariant predictors. Seven categories of variables are included in the former group: relationship status (dummy coded), living arrangements (three categories), parenting status (dummy coded), highest qualification level (three categories), work (one dummy-coded variable: experience of joblessness), access to economic resources (three dummy-coded variables: full-time income, part-time income and savings); and a health variable (with self-reported mental health scored from 1 (lowest) to 5 (highest)). Three categories of variables are included in the latter group: gender (dummy coded); parental education (dummy coded as having at least one parent who graduated from university); and geographical origins (three categories).

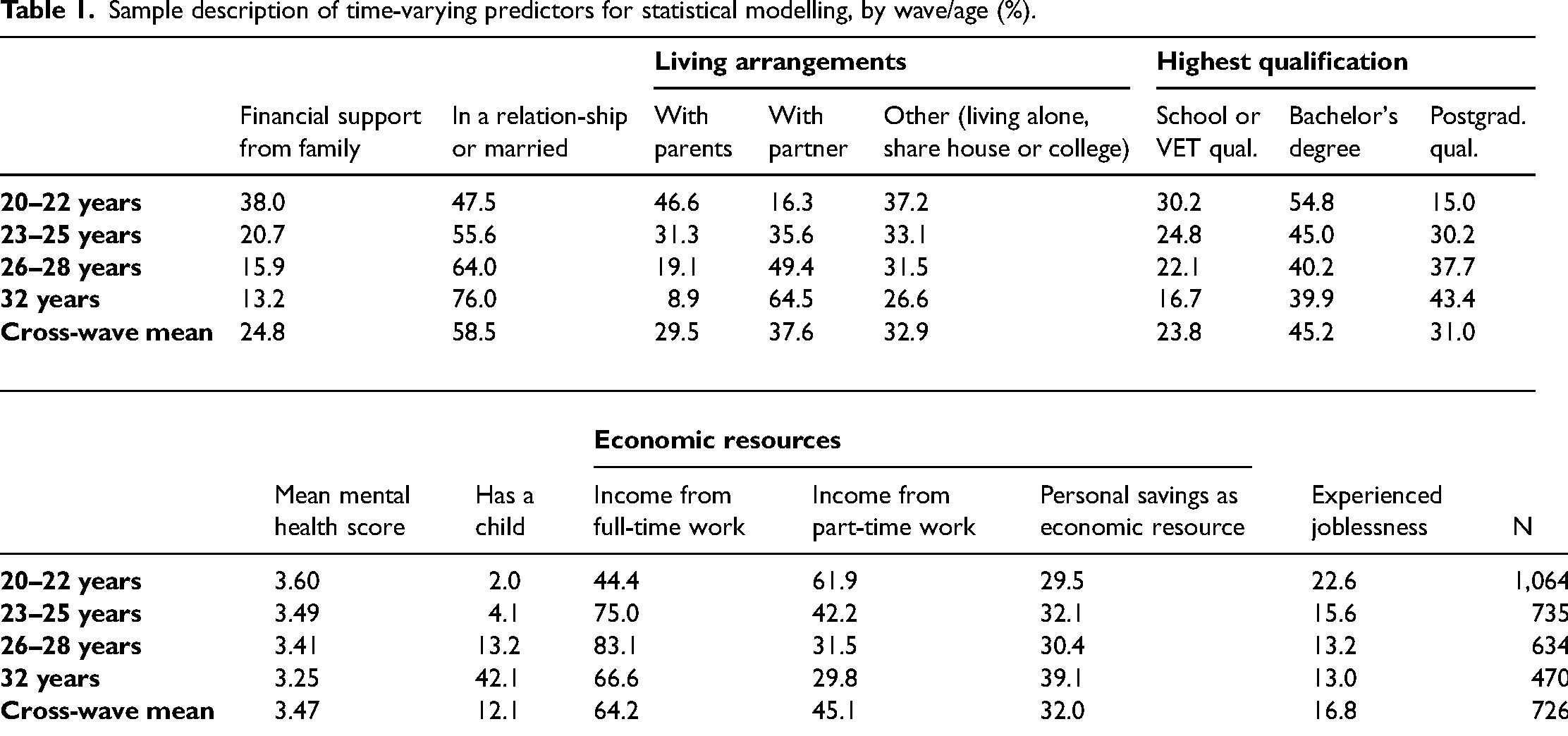

The regression model is fitted to a dataset of four time points corresponding to the following respondent ages: (1) 20–22 years, (2) 23–25 years, (3) 26–28 years, and (4) 32 years. The model uses data from a total of 679 respondents, with an average of 550 valid responses per wave for variables included in the model. The sample characteristics for time-varying predictors are described in Table 1. As regards time-invariant predictors, the sample includes 68.9% of young women and 31.1% of young men; 51.9% of respondents with at least one parent who graduated from university; and 42.4% of respondents from a capital city, 28.6% from a regional town and 29.0% from rural Australia. With these methods, the central focus of the analysis is on the kinds and temporality of financial assistance rather than on the level of financial assistance, which is not asked about in the survey. Future research focusing on this latter dimension would help to further explore the relationship between family support and attributes such as class and gender, especially in the context of enduring gender pay gaps in the Australian labour force (WGEA, 2022).

Sample description of time-varying predictors for statistical modelling, by wave/age (%).

The participants who informed the two illustrative case studies were chosen because they exemplified tendencies that emerged in the quantitative analysis in relation to experiences of family financial assistance. In this sense they are best understood as what Flyvbjerg (2006) has termed ‘paradigmatic cases’ in his work on the role of case studies in social science research, referring to cases that highlight the general characteristics of the phenomena that are in question. The first case highlights the types and experiences of family support that were common among the portion of the sample who received support in order to invest in their education or future career. The second case reflects the types of support and experiences that were common among those who received financial support to alleviate disadvantage of some kind. The data for these case studies are drawn from the participants’ annual survey responses (which include open text responses that provide context to multiple choice answers), and from interviews conducted with these specific participants in 2018 (at the age of 30), which focused on their experiences of family financial support since reaching adulthood.

The findings of our analysis are best interpreted as a window into the lives of young people who, in the conjuncture of earlier generations, would have been considered as established or securely in the middle class.

Results

From their late teens to their early 30s, both gifts (hereafter direct support) and loans (hereafter conditional support) figure among the forms of intergenerational financial support provided to our participants. The most common type is direct support, with a small proportion of young people receiving both conditional and direct support. Overall, two thirds of our cohort received financial support in their late teens. This percentage steadily decreased until the early 30s but remained significant for a minority of the cohort even at this age. Over 4 in 10 young people received financial support in their early 20s, most often linked to study. One in five young people received support in their mid-20s. By age 32 years, 13% of our cohort (i.e. one in eight young people) still received financial support. For complete interpretation, these findings need to be considered in relation to other economic resources (also presented in Table 1).

Table 1 shows that, overall, the likelihood of receiving intergenerational financial transfers from family decreases with age as young people from the Life Patterns project cohort move from their early 20s to their early 30s. This is associated with multiple changes in young people's lives that correspond with their transition to young adulthood, including: a significant increase in access to income from full-time work (from 44.4% to 83.1% throughout young people's 20s, with a dip to 66.6% by age 32 years as some respondents take on parenting roles) and a corresponding decline in income from part-time work (from 61.9% to 29.8%); a relative decline in experiences of joblessness (from 22.6% at age 20–22 to 13.0% at age 32); the growth in postgraduate university qualification attainment (almost tripling from 15.0% at ages 20–22 years to 43.4% at age 32), with a corresponding decline in the proportion of respondents with lower qualification levels; a steady decline in self-rated mental health; the generalisation of relationship formation, from 47.5% at ages 20–22 to 76.0% at age 32; the sharp decline in parental household living replaced by living with a partner and other living arrangements; and the rise of parenting. Alongside these changes, other fluctuations in participants’ lives are evident, although the shifts are less clearly directional. This is the case for the use of personal savings as an economic resource, for instance.

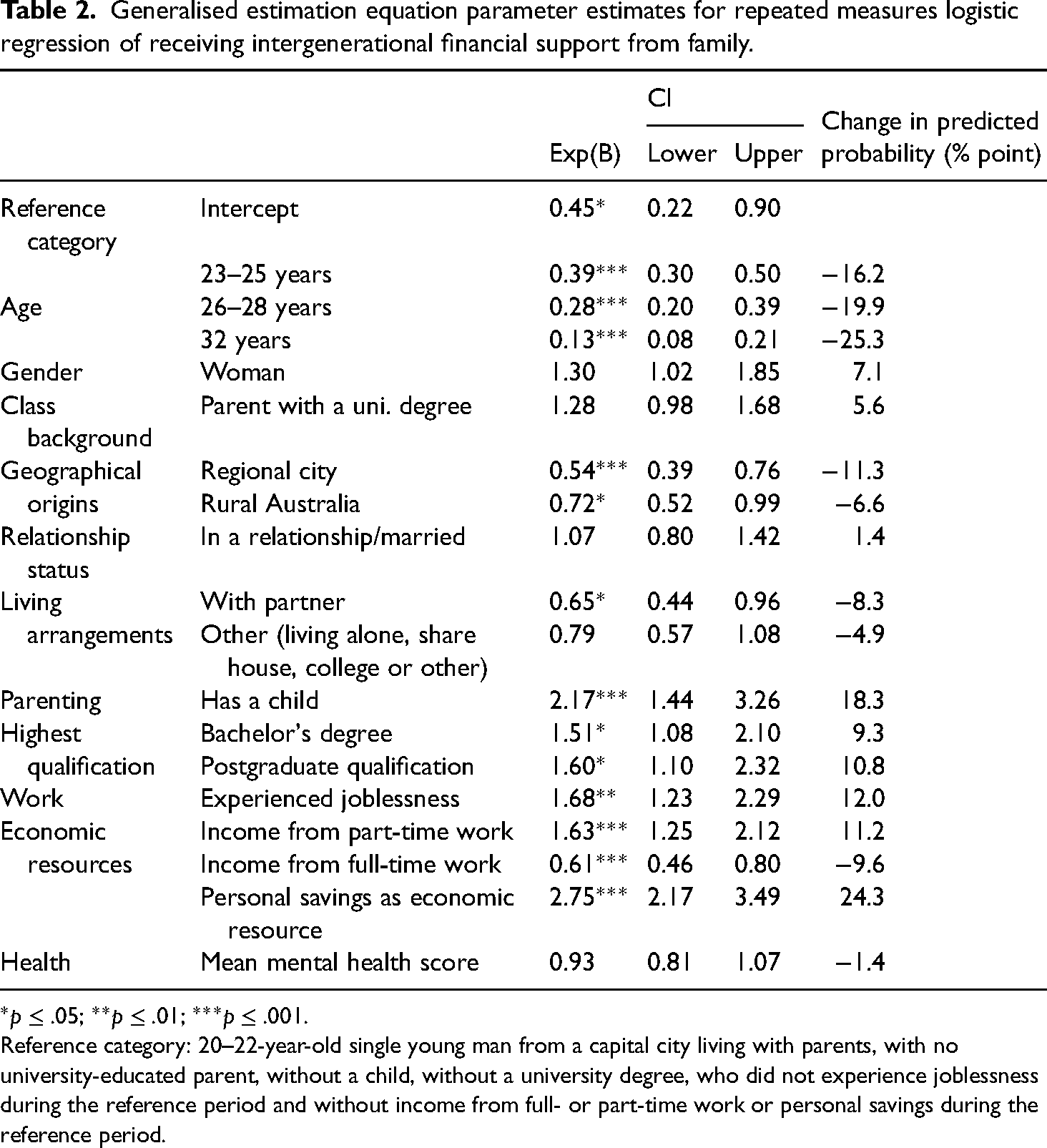

Table 2 reports the parameters of the generalised estimation equation for repeated measures logistic regression fitted to analyse the variation of practices of intergenerational transfer, by age and other social characteristics. The change in odds ratio associated with independent variables is compared to the odds ratios for the reference category (see Table 2 note). Given the categorical nature of predictors (except for self-reported mental health), the relative magnitude of the estimates can be compared to ascertain the characteristics most strongly associated (positively or negatively) with the likelihood of receiving intergenerational financial transfers.

Generalised estimation equation parameter estimates for repeated measures logistic regression of receiving intergenerational financial support from family.

*p ≤ .05; **p ≤ .01; ***p ≤ .001.

Reference category: 20–22-year-old single young man from a capital city living with parents, with no university-educated parent, without a child, without a university degree, who did not experience joblessness during the reference period and without income from full- or part-time work or personal savings during the reference period.

The estimated probability of a young person in the reference category (see Table 2 note) reporting receiving financial support from family when aged 20–22 is almost one in three, at 30.9%. At the same time, the chances of receiving intergenerational financial support are highly socially variable among young Australians, with some groups being significantly more likely and others significantly less likely to receive financial transfers from family. There is a transition effect evidenced in these findings. Compared to the reference category (see Table 2 note), young people's age appears to be most significantly associated with variation in the probability of receiving this form of financial support: compared to their 20–22-year-old selves, people aged 23–25 are 16.2 percentage points less likely to receive family financial support. The gap grows to 19.9 points less likely for 26–28-year-olds, and to 25.3 points less likely for 32-year-olds. However, there are approximately 3 in 20 young people in this sample still receiving transfers once they have reached the age of 32.

Alongside age, three other attributes are associated with a statistically significant decline in the probability of receiving financial transfers from family: coming from outside of Australia's capital cities (−11.3% for regional city origins, and −6.6% for rural origins); having access to income from full-time work (−9.6 percentage points) and living with a partner (−8.3 points). The negative relationship observed between full-time work and intergenerational financial transfers suggests that, in many instances, this form of family assistance is used to compensate for the poorer economic prospects of young people unable to access full-time employment. Meanwhile, the negative relationship observed between living outside of Australia's capital cities and access to intergenerational financial assistance suggests that the economic circumstances and ethos associated with growing up in different localities contribute to shaping practices of family transfer.

In contrast to these characteristics, other attributes are associated with a statistically significant increase in the probability of receiving intergenerational financial assistance. Chief among these is the use of personal savings as a source of financial support, which is associated with a 24.3 percentage point increase in the probability of receiving parental support. While we initially questioned whether the use of personal savings alongside receipt of family financial assistance may be a sign of financial hardship, and perhaps a financial shock such as job loss, we found that respondents who reflected this experience were no more likely to be unemployed than the wider sample and were actually slightly more likely to be in full-time work. This suggests two things within the context of our mostly university-qualified and middle-class sample. First that, when it occurs, access to intergenerational transfers is generally part of a broader spectrum of financial resources young people access, rather than being the sole non-labour economic resource. Second that, for young Australians, intergenerational transfers may be used for purposes other than meeting basic economic needs. This can be inferred by the positive relationship observed between (1) family transfers and access to savings, on one hand, and (2) between family transfers and university qualifications on the other. Taken together, these two relationships highlight that intergenerational transfers can be associated with relatively stable, secure and/or established individual and family circumstances.

Yet, this does not tell the whole story of social practices of intergenerational transfers. Indeed, the results from Table 2 illustrate how complex and multi-faceted a social practice intergenerational financial assistance is. It can occur not only to help fulfil aspirations through augmenting income alongside other resources (such as personal savings), as we have seen, but also to meet basic needs or provide support in times of changing individual circumstances. The second point is illustrated by young people who report experiencing joblessness also being more likely to report having received financial support from their family (by 12.0 points). Meanwhile, the last point is illustrated by respondents with a child being 18.3 percentage points more likely to report receiving financial support from their family, net of the other attributes considered in the analysis. Altogether, the results highlight the need to refuse ascribing a single social meaning to these practices (be it as a response to precarious conditions or as a means to reproduce intergenerational social advantage), as well as the difficulty of grasping the social significance of such practices through basic statistical categories.

The multi-modal nature of intergenerational transfer: illustrations

Intergenerational transfers, asset economy and age

For young people, access to home ownership is an important element to consider when studying intergenerational financial assistance. But this relationship is age dependent and must be considered within the various temporalities of young people's trajectories toward independent living.

At age 26–28, the rate of home ownership is significantly lower among those who receive family financial support (27% versus 43%). By age 32, however, the rate of home ownership is comparable for the two groups, amid a decline in the proportion of the cohort receiving intergenerational financial support. This suggest that an important reason for these intergenerational transfers may be the acquisition of real estate, as has been found in existing research (Cook, 2021; Manzo et al., 2019; Suh, 2020).

Intergenerational transfers and enduring precarity

For those in in their early 30s, intergenerational transfers are at times a response to enduring financial instability or economic precarity. This is evident when comparing the rate of intergenerational transfers for those who do and do not report difficulties paying for various expenses.

Across all types of expenditures, those who receive intergenerational financial assistance in their early 30s are more likely to report financial insecurity or difficulties. By that stage in young adults’ lives, intergenerational assistance becomes associated more with financial insecurity than with capital accumulation in the asset economy. The gap is consistent across expenditure types, which suggests that intergenerational transfers are more linked to overall financial circumstances of young adults than with punctual support for targeted/specific activities or types of expenditures. By examining the respondents’ occupations at each point in time we also find some changes over time that may be related to the changing purpose of family financial assistance. In the initial waves, at which the participants were aged 20–22, many are in service sector positions, reflecting the fact that they are likely to be studying and undertaking paid work on a casual or part-time basis. However, in the final two points in our analysis, at which the participants are aged 26–28 and 32, another pattern emerges. While some of the participants are unemployed or in relatively stable professional occupations, some are also employed in fields and industries associated with long-term job or pay insecurity. Most of the participants who fall into this category are in fields related to the creative arts, such as illustration or dance, and identify that they are self-employed. We explore the implications of this finding in the discussion.

Qualitative case studies

We now turn to two qualitative case studies that exemplify these two tendencies, drawn from interviews with members from the sample used for the above analysis.

Katrina

While completing her undergraduate degree in Canberra, Katrina lived in the family home rent free (thus receiving in-kind assistance from her parents) and undertook minimal paid work to ensure that she could maintain high grades. Upon finishing her undergraduate degree, she relocated to Brisbane with her partner for a year, living rent free in a property owned by her grandmother, who was travelling at the time. Katrina then returned to Canberra with her partner to undertake an additional (Honours) year of advanced undergraduate study. During this time, she was employed casually as a research assistant and received direct financial assistance from her parents. This assistance continued the following year when she commenced a four-year medical program and bought a house in Canberra with her partner. The house was bought outright by Katrina's parents, with the intention that a portion of it would be repaid either once Katrina had started working, or when they sold the house. This arrangement was suggested by Katrina's parents because Katrina and her partner could not be approved for a mortgage loan that would cover the costs of the type of property that they were interested in due to their relatively low income at the time. Katrina was advised that it would not be feasible for her to work while studying medicine, so her partner's income was used to cover general household expenses but was not sufficient to cover mortgage repayments. The intention of buying a house at this time was in large part to provide stability to Katrina while she undertook a competitive and intense medical program that required a large time commitment. In this sense, it was a way for Katrina's parents to invest in her future earning potential, as medical doctors undertake long periods of training but have above-average lifetime earnings. By helping Katrina to cover her living expenses and ensuring a stable living situation for her during her medical degree, Katrina's parents essentially helped her to achieve a career outcome that she may have struggled to attain without this assistance while building equity in a home at the same time. This arrangement continued until Katrina completed her medical program and internship, after which the property was sold, and a portion of the funds were returned to Katrina's parents, leaving Katrina and her partner with enough equity to purchase another property.

Amanda

In contrast to Katrina, who received financial assistance to help her to achieve her goal of becoming a medical doctor, Amanda received assistance when she experienced hardship. Amanda remained in the family home until she was aged 26, even after she completed her tertiary education and began working as a primary school teacher. She did not pay rent during this time, and instead saved for a deposit for a house and land package in an estate 15 minutes from her parent's house. Although Amanda paid the deposit for the property and serviced the loan herself, her parents guaranteed the loan so that she would not be required to pay lender's mortgage insurance (which is generally required when the purchaser has a loan to deposit ratio (LDR) of over 80%). Soon after moving into the property Amanda invited her boyfriend to live with her, and they had a baby within the next year. Amanda's boyfriend became abusive and controlling soon after her daughter was born, and when her daughter was six months old, she left the home and stayed in a refuge with her daughter until her former partner could be evicted by police. When Amanda returned to her home with her daughter, she received significant practical and financial support from her parents, who helped to supplement her income while she was on maternity leave and provided care for her daughter during this time and after she had returned to her job as a teacher. The assistance that Amanda received did not help her to ‘get ahead’ in the same way as Katrina experienced. Instead, this assistance helped to alleviate a situation of precarity.

Discussion

For this sample of young people in Australia, intergenerational transfers are generally part of a broader spectrum of financial resources young people access, rather than being their sole non-labour economic resource. While some receive intergenerational transfers to meet basic economic needs, or even in response to significant hardship (as experienced by Amanda), many do not. These findings suggest that intergenerational financial transfers are made for multiple reasons. Analytically, these transfers seem to be given for at least two reasons: to combat financial insecurity/instability and to ‘get ahead’ and acquire asset/financial stability (including but not limited to housing). This is true even within this largely middle-class sample, and the trend identitifed here may be heightened in research that can pursue these questions within a wider spectrum of socio-economic positions.

In terms of how these transfers are conceptualised within current debates about the extension of youth, and about inequality in the context of the increasing centrality of the ‘asset economy’ (Adkins et al., 2021), these two reasons for transfers interact in interesting ways, pointing to the interplay of the reproduction of inequalities and generational change (Woodman & Wyn, 2015). Assets and their intergenerational inheritance are an increasing focus in the study of the economic and sociological aspects of inequality (Adkins et al., 2021; Piketty, 2014;). There is a renewed role for inheritance and financial support given inter vivos for family members in countries where its role was at least somewhat reduced during the mid-20th century (Albertini & Kohli, 2012). While family wealth transfer is an enduring feature of social stratification, the mid-century mix of slower asset appreciation and even depreciation, higher taxes and relatively more generous government support for young people meant that forms of inheritance other than direct transfer came to play a greater role, as highlighted by Bourdieu's (1979) work on the importance of cultural capital inheritances in France at this time. This was a period of relatively early transition to financial independence in Australia and countries with similar economies and welfare state regimes. The contemporary moment is sometimes presented as one of delayed transitions to adulthood masking the mechanisms of intergenerational class reproduction that were experienced by previous generations (France & Roberts, 2015). Yet the embedding of debt, speculation and asset accumulation as the logic driving economic life across the class structure, with profound consequences for the life course and its generational dimensions (Adkins et al., 2020), mean that a new dynamic is at play.

Woodman (2022) has suggested that a speculative attitude to life, with the risks mitigated by potential or actual financial transfers from parents, is increasingly central to being able to leverage social and cultural capital in career building. The parents who can most readily provide this support are those who have themselves accrued substantial assets due to a mix of their own starting class position, an elevator effect of education and economic change moving people into the middle class for their generation and the substantial asset accumulation that their cohort on average experienced due to economic, tax system and housing market changes during their working lives. In countries like Australia, accessing this was easier to achieve through wages alone (even on a relatively modest salary) for this cohort, who through these processes were catapulted into a substantively higher wealth bracket (Adkins et al., 2021).

It is recognised that accessing this housing pathway to asset wealth is now more difficult and increasingly requires financial support from family in Australia (Wood & Griffith, 2019), negotiated in complex ways between generations (Cook, 2021). However, as identified earlier in this article, less attention has so far been paid to the potential impact of financial transfers (often facilitated through young adults’ proximity to assets owned by parents) on other areas of young adults’ lives, particularly employment. Those born since the 1980s are sometimes categorised as members of ‘the precariat’ because of these changes to the labour market and housing (Standing, 2011). However, others highlight that not all young people are in insecure work and that only some who are in this type of work are truly precarious, with some doing so only for spending money while they are studying or otherwise supported by their parents (Antonucci, 2018; MacDonald, 2016).

Yet this debate – focused as it is on whether young people as a cohort are, or are not, structurally disadvantaged by currentl levels of insecure employment, or whether instead it is simply the reproduction of class across cohorts as before – underplays the complex role of employment and work experience in asset accumulation and speculation on the future. For example, this complexity is evident in the trajectories of young people undertaking employment that is objectively precarious alongside tertiary and increasingly postgraduate study and internships, while having parental support as a safety net. A related example is those young people embarking, with family support, on career trajectories that may lead to substantial rewards in remuneration, autonomy and prestige but also with a somewhat higher risk of long-term insecurity, such as media, academia, journalism or acting (Friedman & Laurison, 2020).

The intergenerational transfers tracked here as young people move through their 20s and into their early 30s appear to be playing several different roles. As well as supporting housing investment, as has been identified, and somewhat protecting the more privileged from the effects of insecure employment, these transfers may be facilitating a speculation on the future at work, alongside other forms of asset accumulation, including housing. By demonstrating that transfers are not used only for entering the property market and are not only received by those who are in a position to service a mortgage loan (and are thus relatively financially stable), our findings contribute to understanding the specific way that transfers (and, by extension, proximity to assets) can interact with young people's lives in areas other than home ownership. In so doing they highlight some of the ways in which proximity to assets may improve life chances for young adults.

This study is, however, subject to limitations. Key among them is that the dataset underpinning this study does not provide information about how much money is received, from whom specifically, in what way (e.g. a lump sum or payments over time), and how it is used. The dataset also only collects data from individual young people, meaning that it is unable to provide insight into the experiences and perspectives of those who are providing them with financial support. As we discuss below, these are key areas for further research.

Conclusion

The ‘bank of mum and dad’ has been identified as a growing source of support for young people, not primarily in the form of inheritances after parents are deceased, which tend to occur when the receivers are well into middle age, but via transfers from living parents to their young adult children. Many of the intergenerational supports, including financial support, once associated with teenage years now appear to be extending further into young adulthood.

This research suggests that transfers between parents and their youing adult children are a complex social practice, with a complex relationship to insecurity: they are given both to combat financial insecurity/instability and so that young adult children can ‘get ahead’ and acquire assets/financial stability. By highlighting the prevalence of financial transfers occurring even into our participants’ 30s and suggesting some of the characteristics of those who receive them, this study opens several questions for future research and areas for conceptual development. Key areas for future research include consideration of how much money is changing hands, how it is provided, what the funds are used for, how they are experienced and negotiated by parents and their children, the gendered dynamics at play in the provision and receipt of financial assistance, and whether there is a different culture of intergenerational transfers in regional and urban areas or differences at the edges of the class structure. Additionally, as the transfers that we have focused on occur while parents are still living, and indeed while they may still be relatively young given the age of our participants, this study suggests the need to further focus on the impact of these transfers on the retirement planning and general financial wellbeing of those who are providing them (Maroto, 2017). This is particularly urgent in light of growing awareness of financial elder abuse in the context of intergenerational transfers for the purpose of home ownership. Conceptually, the multi-modal nature of transfers and their potential effects on broad aspects of young adults’ lives, including education, employment, relationships, and health and wellbeing, opens questions about the likely far-reaching impact of family financial assistance on young adults’ life courses and family dynamics.

While the present study has begun to explore the multiple reasons for these transfers, it also opens up a future research agenda. Even as there remains a clear transitional effect in these transfers, being more common for 18-year-olds than 32-year-olds, the lack of research into the extension of parental support well into people's 20s and even into their 30s is a critical gap given that these older periods of ‘youth’ appear to be becoming increasingly central to crucial life outcomes.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Australian Research Council, (grant number DP0557902, DP1094132, DP160101611, DP210100445).

Notes

Author biographies

Dan Woodman is TR Ashworth Professor in Sociology at the University of Melbourne and a co-Chief Investigator on the on the Australian Research Council (ARC) funded Life Patterns project.

Quentin Maire is a Senior Research Fellow in the Melbourne Graduate School of Education working on the ARC-funded Life Patterns project.

Julia Cook is Senior Lecturer in Sociology at the University of Newcastle, Australia, an ARC DECRA Fellow and a co-Chief Investigator on the on the ARC-funded Life Patterns project.