Abstract

Income supplementation benefits aim to provide additional financial support to low-income municipal residents for expenses insufficiently covered by their primary income sources. In the Netherlands, the non-take-up of these benefits is particularly high and relatively underexamined. This study investigates factors influencing the decision not to claim income supplementation benefits, by surveying approximately 3500 low-income residents of a Dutch municipality. Using hypothetical scenarios where all participants are considered potentially eligible for certain local welfare benefits, the research explores the impact of shared scheme characteristics, trust in government, and the fear of reclaims and fines. The findings reveal that stringent requirements, such as extensive proof of financial need and restrictions on spending autonomy, are likely barriers to participation. Additionally, a lack of trust in the government and concerns about potential reclaims or penalties further discourage participation. These insights underscore the need for policies to improve the accessibility of income supplementation schemes.

Introduction

The Dutch social support system is composed of various national and local schemes that address different aspects of social welfare, including healthcare, childcare, unemployment, disability and old age pensions. Nearly all support schemes (local and national) are selective, meaning that benefits are distributed on the basis of individual need, as determined by a test of income and – often – assets.

Around six million households in the Netherlands are dependent on one or more social support schemes (Algemene Rekenkamer, 2019). However, as in many other countries, non-take-up of benefits poses a significant problem. Non-take-up refers to the proportion of those eligible for a benefit (in cash or in kind) or other provision who do not receive it. In the Netherlands, non-take-up is highest for the income supplementation benefits offered by most municipalities. These local income supplementation benefits are designed to provide low-income residents of the municipalities with extra support for particular expenses that are not covered adequately by their main source of income. While non-take-up levels vary between different schemes and municipalities, on average the level of non-take-up is between 30 and 80% (Slagman et al., 2023).

There are hundreds of income supplementation schemes, and many are unique to the individual municipalities that provide them. However, they do share several important characteristics. First, the benefit amounts are usually relatively modest (a few hundred euros at the most), often one-time payments, either monetary or in kind. Second, almost all of these schemes are means-tested and require applicants to prove their eligibility by providing evidence (such as bank statements). Third, the income supplementation benefits are almost always exclusively targeted at the most vulnerable groups in society, such as people who are structurally dependent on welfare or who have had a very low income for a number of years. Fourth, most income supplementation schemes are meant as an income supplement for very specific expenses, for example to replace a broken washing machine, stove, or refrigerator (so-called ‘white goods’); to buy a laptop or tablet computer for children going to school; to help pay for sports and cultural activities, etc.

Some might argue that the non-take-up of these additional income support measures is a relatively unimportant issue, as they merely provide extras to low-income residents. However, while these support measures are not meant to provide access to goods and services as necessary for survival as housing or healthcare, they could potentially play an important role in enhancing the quality of life of beneficiaries. The small additional benefits are specifically intended to offer low-income residents – and their children – the means to participate in social and public life as normally as possible. In addition, even missing out on a few very modest additional income support measures would add up to a significant amount of money that remains unclaimed.

The Dutch National Ombudsman, among others, sees the current crisis of trust as the cause of citizens’ avoidance of social support schemes offered by the government. This lack of trust is often attributed, in part, to the childcare benefit scandal. In 2021, the Dutch government resigned over a scandal involving child benefits, in which more than 26,000 families were wrongly accused of benefit fraud by the tax authority. Many fear that this scandal has made people distrustful of the government and therefore more hesitant to apply for benefits (NOS, 2023).

In this paper, I address two possible explanations for the high levels of non-take-up of local income supplementation benefits: the characteristics that most of these schemes share and the level of trust of citizens in the government. I am interested in a specific type of non-take-up, in the factors that influence the decision to claim or not claim an income supplementation benefit, when a potential applicant is faced with circumstances that may warrant such a claim (such as a high energy bill, a broken appliance, or having to pay a membership fee for a child who wants to participate in a sports team) and knows of the existence of such a scheme.

The paper is structured as follows. In the following section, I give a succinct overview of the available literature on the drivers of chosen non-take-up and the hypotheses I have derived from this literature. I then explain the methods I employed to test my hypotheses. The next section presents the results of the study, then finally I present my conclusions, including the limitations of the study and directions for future research.

Drivers of chosen non-take-up

The literature on non-take-up of government social support shows that there are different levels of factors to consider when trying to understand non-take-up. For example, relevant determinants of non-take-up include: (a) the personal characteristics and the decision-making processes of potential beneficiaries; (b) the design of schemes; (c) the way in which the schemes are implemented; and (d) the social context of potential beneficiaries (Janssens and Van Mechelen, 2022; Van Oorschot, 1996). Reijnders (2020) also proposes a four-level framework as a mere starting point for investigation of the non-take-up of social support: (a) the individual level – the potential welfare recipient; (b) the organisational level – the third sector providers (and their representatives); (c) the social service system; and (d) the social policy design.

In this paper, I examine what is referred to by Van Oorschot (1994) as ‘primary non-take-up’: the decision not to claim. Non-take-up in that respect refers to a situation in which the potential claimant is aware of the existence of a scheme and his/her eligibility, but decides not to claim (for more on the different types of non-take-up, see: Goedemé and Janssens, 2020).

While multilevel theoretical frameworks might offer a fuller explanation of the decision not to claim, their complexity makes them difficult to apply fully in a single study. Arguably, the dominant way of thinking about the decision not to claim a benefit is founded on the assumptions of the rational actor model (Reijnders, 2020). In essence, the rational actor has stable, coherent and well-defined preferences rooted in self-interest and utility maximisation; he accurately reflects on the costs and benefits of various strategies and choices, pursuing the correct path to maximise his preferences and the expected utility value (McMahon, 2015).

In the rational model, a choice – such as applying for income supplementation benefits - is guided by objective, clear-cut measures of costs and (expected) benefits. However, few will accept the rational actor as a fully realistic description of the decision-making processes involved in the claiming of income support measures. Firstly, there are many behavioural barriers that stand in the way of ‘optimal’ rational decisions (Janssens and Van Mechelen, 2022). For example, people often appear to be too optimistic about finding a job or about how much money they will have left at the end of the month, while they actually underestimate the likelihood of the need for (financial) support (Bhargava and Manoli, 2015). Secondly, if potential beneficiaries of income support measures were completely rational, we would not expect non-take-up levels to be nearly as high as they are. For example, even if the application process for claiming 400 euros to purchase a new washing machine were to take a full 8 h and significant effort, few would consider it rational not to claim, as the people who are entitled to such a benefit would likely not earn 50 euros an hour.

Non-take-up as a result of a cost-benefit calculation

From a rational choice perspective, simply put, the choice not to avail oneself of an income supplementation benefit offered by the government is made after weighing the expected costs and benefits of various alternatives (e.g. not applying, waiting a while before applying or applying immediately). Hernanz et al. (2004) identify several different kinds of costs involved in applying for income support: information costs (costs related to, for example, obtaining more information about the benefit and the application procedure); administrative costs (e.g. the duration and complexity of the application process).

Besides these more or less objective sources of costs, perceived or felt social and psychological costs can also play a role in explaining non-take-up. For example, people might refrain from seeking help because this does not fit with the image they have of themselves (‘I should be able to take care of myself/my family’). Because of this, the ‘threat to self-esteem’ model proposes that help-seeking can lead to feelings of failure, dependency and inferiority (Wang, 2002). Likewise, claiming a benefit could also lead to the fear that others will view them as inferior (Baumberg, 2016; Baumberg et al., 2021; Bertrand et al., 2000; Hümbelin, 2019; Markussen and Roed, 2015; Stuber and Schlesinger, 2006).

I expect the psychological costs to be particularly relevant for the non-take-up of small additional income support measures. This is firstly because nearly all local income supplementation schemes are extensively means-tested. The process of means-testing is often linked to higher psychological costs for potential beneficiaries and therefore to a higher likelihood of non-take-up (see Mitton, 2004 for an extensive overview of the available literature). In addition, potential applicants might view the process of means-testing for small income supplementation schemes to be particularly invasive and stigmatising, as the benefit that is being claimed is small, especially compared to the general social assistance schemes. Moreover, as the benefits involved are relatively modest in amount, relying on them could lead to especially strong feelings of failure and inferiority. Most people would likely be less hesitant to ask for a loan of 100,000 euros to buy a house than they would be asking for a loan of 50 euros to buy a washing machine. Likewise, the fact that the small additional support measures act as a safety net below the actual safety net (such as general welfare or the state pension), might exacerbate the feeling among potential applicants that they are even less self-reliant than others if they apply for these additional benefits. Finally, because the benefits are themselves modest in amount, from a rational choice perspective, the costs involved in claiming outweigh the benefits far sooner than might be the case with social assistance schemes that offer bigger ‘rewards’.

On the outcome side of the rational actor equation, uncertainty about whether the benefit can be claimed at all may also contribute to non-take-up, as this dampens the expected utility of the decision to claim. This can be the case if, for example, the administrative body has a large degree of discretion when determining the right to a benefit – for example, when vague criteria are used – so that it is not clear to an applicant whether he or she is entitled and/or to what extent. The more uncertain the applicant's assessment of whether a benefit can be claimed successfully, the higher the likelihood of non-take-up (Behrendt, 2002). Something similar also applies to the nature of the benefit that is offered. For example, income support that is provided with spending autonomy is considered more ‘useful’ than a provision in kind or with no spending autonomy.

Two outcome-related factors seem to be relevant to the non-take-up of income supplementation schemes. Obviously, as the benefit amounts are modest, from a rational actor perspective potential applicants will only be willing to endure modest costs to receive the benefit. However, it is also important to consider that potential applicants have a choice between several alternative options to solve a particular problem (e.g. to replace a broken laptop). They could borrow some money from family, friends or other lenders to purchase a second-hand laptop for a child. By contrast, there is not really a viable alternative to applying for general welfare (which, in the Netherlands, amounts to roughly 17,000 euros per year for as long as it is needed).

To conclude, from a rational choice perspective, it is possible that the small additional income support measures suffer from especially high levels of non-take-up because they (a) usually involve one-time, relatively small amounts but (b) still require applicants to endure significant administrative, information and psychological costs.

Trust and regret: fear of reclaims and fines

In the Netherlands, non-take-up of social support has been explicitly linked to a lack of trust in the government. Trust, and its impact on decision-making processes, is frequently considered in psychological, sociological, economic, political and organisational science literature.

While the precise conceptualisation of trust differs between areas of study, it is generally accepted that trust particularly influences behaviour and decision-making when there is a lack of objective information (uncertainty) about outcomes and the intentions of others. This, in turn, creates vulnerability for the individual in question, and the risk that a decision or behaviour will not result in the desired outcome or may even have adverse effects.

In that sense, the role of trust in decision making is closely related to the notion of (anticipated) regret. Regret is an emotion or feeling that is experienced when people realize or imagine that their present situation would have been better had they decided differently in the past. Regret can be experienced about past (‘retrospective regret’) and future (‘anticipated or prospective regret’) decisions. Zeelenberg and Pieters (2007) assert that people tend to be regret averse, meaning they ‘are motivated to avoid regret from happening and when it happens they engage in ameliorative behaviors (e.g. reverse the decision or undo the consequences)’. Like trust, the role of anticipated regret in explaining certain behaviour has been extensively researched in other domains, such as health-related behaviour (smoking, drinking, etc.), psychology and economics.

By and large, trust and anticipated regret are inversely related to each other. When trust in the other party (e.g. the government) is low, individuals often perceive higher risks associated with their decisions, leading to higher levels of anticipated regret (Luhmann, 2017). If anticipated regret is high, this impacts the subsequent evaluation of potential outcomes and subsequent behaviour (Zeelenberg and Pieters, 2007).

Why would someone anticipate regret when applying for income supplementation measures from the government? Besides a loss of autonomy and self-reliance and perhaps the fear of facing degrading treatment during the application process, the Dutch childcare benefits scandal is an especially dramatic example, which shows that relying on government support is by no means free of risk. Between 2012 and 2018, the Dutch Tax Authority wrongly labelled an estimated 26,000 recipients of childcare benefits as perpetrators of deliberate fraud. Benefit recipients were unlawfully subjected to a ruthless enforcement policy in the form of repayments (tens of thousands of euros in many cases) and fines of up to 100% of the amount of fraud detected. Many parents were driven into financial and emotional destitution by the Tax Authority's zero-tolerance approach, based on forced repayments and rigid sanctioning (Haitsma and Bouwmeester, 2023). This stringent fraud policy has permeated most aspects of the Dutch social assistance system: if a benefit has been claimed unduly, it has to be repaid in full and a fine is imposed, even if there is little fault on the part of the claimant.

The fear of reclaims and/or sanctions is sometimes mentioned as a potential inhibitor of participation in welfare schemes (Reeves and Loopstra, 2017; Wright et al., 2020). In a qualitative study among low-income households in the Netherlands, Simonse et al. (2023) found that the fear of reclaims was the main reason respondents refrained from welfare participation. However, in a later quantitative study, Simonse et al. (2023) found that fear of reclaims explains only a small part of the non-take-up of healthcare benefits and child support benefits.

Considering the amount of publicity surrounding the childcare benefit scandal, it is not hard to imagine why Dutch people in particular would be hesitant to apply for an income supplementation measure. Why would someone choose to apply for a modest benefit, relegating autonomy and financial self-reliance, incur information, administrative and psychological costs, if he or she believes that there is a significant likelihood of having to repay the benefit and incur a fine? Would potential claimants willingly engage in such high-risk, low-reward behaviour?

To sum up, viewed from a rational choice perspective, the choice not to claim from an income supplementation scheme could be the result of two interrelated factors. The application process for small, means-tested benefits is often arduous, requiring extensive evidence of eligibility. This not only places administrative and informational burdens on potential applicants, but also enforces the negative feelings associated with claiming. Moreover, past examples of stringent fraud policies may exacerbate fears of the potentially severe consequences of making mistakes. This fuels anticipated regret related to potential reclaims and fines, in particular for people with low levels of trust in the government, making claiming the benefit even more unappealing.

Hypotheses

My premise, based on the available literature, is that the ‘choice’ to apply for income supplementation benefits is partly a rational one based on evaluations of the costs and benefits associated with the claiming process. The cost-benefit ratio could be improved by decreasing application costs and/or increasing the expected utility. My first hypothesis is:

The likelihood of non-take-up is lower with income supplementation measures that have a more favourable cost-to-benefit ratio.

The income supplementation benefits that are central to this study share four main characteristics: the benefit amounts are usually relatively modest; they are meant as a supplement for very specific expenses; they are extensively means and asset tested; and they require applicants to prove their eligibility with evidence. How could these characteristics be altered so that the odds of non-take-up are lower?

First, by not requiring evidence of means and assets from applicants, both perceived administrative as well as psychological costs might be decreased. It would require less effort for potential applicants to submit an application, as no documents need to be gathered (Janssens and Van Mechelen, 2022; Moynihan et al., 2015), and moreover, the feeling that the burden of proof is minimal possibly reduces the feeling of stigmatisation and shame among potential applicants.

If the decision whether or not to submit an application is the result of a (limited) rational choice process, the expected utility of applying also plays a role in the decision. Obviously, increasing the actual amount of the benefit dramatically will likely reduce non-take-up. However, other less expensive alternatives are also possible. First, governments can opt for a fixed benefit (instead of a variable and therefore uncertain amount) and clearly describe the inclusion criteria, in order to reduce uncertainty about expected outcomes. Second, governments can offer applicants spending autonomy, as this allows these applicants to allocate the allotted funds where they are most needed. Likewise, spending autonomy might lead to lower levels of perceived dependence and loss of autonomy.

In sum, I expect modest benefit amounts and lack of spending autonomy to negatively impact the expected utility of claiming, thereby increasing the odds of non-take-up. The process of means-testing in general, and requiring evidence of means in particular, increases the costs to clients (information, process, or stigma), thereby increasing the odds of non-take-up.

The second element of my model revolves around the role of trust and, related to this, anticipated regret. Based on the literature discussed earlier, I expect people with low trust in the government to experience higher levels of anticipated regret when deciding whether or not to claim a benefit. This anticipated regret likely revolves around the risk of having to repay the benefit and being fined if a mistake is discovered by the administrative body. This will impact claimants’ decision whether or not to apply for an income supplementation benefit by lowering the expected utility of the decision to claim. My hypothesis is therefore:

The likelihood of non-take-up is lower if the citizen’s trust in the government is higher.

It is likely that potential applicants’ anticipated regret will have a lot to do with the perceived risk of the benefit having to be repaid if it is received unduly. Therefore, not explicitly mentioning the possible risk of having to repay the benefit if it turns out to have been received unjustly might reduce this anticipated regret (and reduce the expected utility of the decision to claim); a reference to this risk might exacerbate it. This leads to the final hypothesis:

The likelihood of non-take-up is higher if the possibility of a reclaim and/or fine if the benefit is claimed unduly is explicitly mentioned.

Methods

I tested my hypotheses by conducting an online vignette study coupled with a short web survey. A vignette study is a research method used to explore how individuals perceive and respond to hypothetical scenarios or descriptions of situations. In such studies, participants are presented with written or verbal vignettes describing particular situations, often involving social interactions, decision-making dilemmas, or policy scenarios. These vignettes make it possible to manipulate the variables or conditions of interest. In my case, the research question is how people expect to react when they read certain information about an income supplementation scheme from the municipality of Groningen. The vignettes then vary with regard to the various characteristics of income supplementation schemes that I mentioned earlier. It is completely random which text is seen by each respondent. This method enables a relatively precise determination of the effect that each unique characteristic of an income supplementation measure might have on non-take-up rates.

To gain access to potential respondents, I collaborated with the municipality of Groningen, the largest city in the northern part of the Netherlands (+/- 240,000 inhabitants). The municipal authorities were willing to send out an invitation to low-income residents of the city, asking them to participate in the study. The authorities agreed to do so, because they are themselves concerned with the non-take-up of their income supplementation schemes and have taken steps to reduce it. For example, the municipality simplified the application procedure for several income supplementation measures in the first quarter of 2023. In particular, applicants are no longer required to provide evidence of means and assets. Applicants merely indicate what their (financial) situation is by means of box-ticking and short answers to simple questions. A completed application form is then compared by municipal employees with data from the municipal and national systems. If no questions arise from the comparison, the resident receives a decision on his application. When information provided by the resident does not match the data retrieved from the systems, the municipality contacts the resident to ask what the reason for the difference may be. If necessary, supporting documents are requested from the applicant during the process, but this is not usually the case.

The municipality has contact information (home address, phone number and/or e-mail) for most people who have received benefits or income supplementation in the past. The income supplementation scheme most widely used by the municipality is the so-called ‘energy allowance’. In 2022, the municipality granted this benefit to a large group of low-income residents, either ex officio (i.e. without a claim from the citizen) or after an application, in order to alleviate the financial effects of the surge in energy prices. The energy allowance involved a one-time payment of 800 euros. The measure was intended for all households who – at the time – were on a low income (no more than 120% of the welfare level).

To include as many people as possible in the study, all past recipients of the energy allowance were asked by the municipality of Groningen to take part. The group of potential respondents therefore also includes people who at the moment do not receive any social support (such as welfare) and people who may never have applied for income supplementation benefits themselves (as the energy allowance was granted automatically to many people).

I designed the invitation letter and the survey. The municipality distributed it to residents who had received an energy allowance in the past. In total, just over 10,000 invitations were sent by the municipality, both by regular mail and by email. The invitation included a hyperlink and a QR-code that led respondents to the online survey. The survey could only be filled out anonymously, which was explicitly stated in the invitation to participate. No personal information on the potential respondents was shared between myself and the municipality.

The questionnaire was accessible between 13 July 2023 and 31 August 2023, and was partially completed by +/- 5000 people. Just over 3500 people completed the questionnaire in full, which is a good response rate for a web survey (Daikeler et al., 2020). I did not conduct a non-response bias survey, so do not know how representative the sample is of all low-income residents of the municipality who were approached to participate in the study. There are also no publicly available data comparing the sample with the population of low-income residents of the municipality of Groningen. However, scientific inference does not require the general or target population to be representative in order to be valid, as the study does not focus on prevalence rates but rather on the impact of manipulated variables (Rothman et al., 2013).

Measurements

Level of trust. To measure trust in the government, I asked two questions used by Statistics Netherlands (CBS), the statistics agency of the Dutch national government, to measure institutional trust. Institutional trust relates to a number of social and political institutions and organisations. To keep the survey as brief as possible, I only included two institutions: the ‘national government’ and the ‘municipality of Groningen’. CBS uses ‘a lot of trust’, ‘quite a lot of trust’, ‘not that much trust’ and ‘no trust at all’ as the answer categories. I chose to measure responses on a scale between 1 (I have no trust at all in…) and 10 (I trust …. completely). The following two questions were posed: How much trust do you have in the government? – I have (1) no trust at all… (10) complete trust. How much trust do you have in the municipality of Groningen? – I have (1) no trust at all… (10) complete trust.

Control variables. As control variables I first included the respondents’ main source of income (a paid job; welfare; (state) pension; self-employed/business). I asked respondents to select their main source of income, so that the categories are mutually exclusive. Due to the fact that income source serves merely as a control variable in my analysis, I opted not to examine differences between specific categories (e.g. paid employment vs. welfare).

In addition, I asked respondents to indicate on a scale of 1 to 10 how satisfied they are with their financial situation (1 = very dissatisfied, 10 = very satisfied). Finally, I asked them to indicate whether they thought their financial situation would worsen, remain the same or improve in the short term. I recoded this item into two dummy variables: the first to measure the effect of an expected deterioration in the financial situation on non-take-up, the second to measure the effect of an expected improvement in the financial situation on non-take-up. Both variables use the neutral (remain the same) as a reference category. I also measured respondents’ attitudes to financial help from the government. That statement read: The government should help people with little money.

The response options were designed as a five-point Likert scale, ranging from ‘strongly disagree’ to ‘strongly agree’. A higher score indicates that the respondent has a more positive view of government income support.

The design of the income supplementation scheme. After the first part of the questionnaire, respondents were shown the following text:

‘The municipality wants to know how it can help people with a low income. Unfortunately, the schemes it has for this are underused. The University of Groningen and the municipality wish to know why that is. You can help us with this. Below you will read a short text about an idea for an income supplementation measure from the municipality. Once you have read the text, would you like to answer a question about it?’

I then presented a single vignette text. The vignette I presented consisted of five characteristics, each with two options. This means that a respondent was shown one of 25 different vignettes. The various factors are shown below:

Inclusion criterion: specific or general

- If you had a low income in the past year (maximum €1434 for a single person, maximum €2049 for married or cohabiting) you can apply for a benefit. - If you had a low income in the past year, you can apply for a benefit. Amount of the benefit: variable or fixed

- The amount is 600 euros. - The amount of the benefit depends on your income and expenses. Spending autonomy or not

- If you are entitled to the benefit, we will deposit it in your bank account. - You may only use the benefit to pay a bill approved by the municipality. Evidence: necessary or not

- You must prove that you are entitled to the benefit. This is why we ask for copies of bank account statements from the last 12 months. - You do not need to send any supporting documents. We will check if the information you entered is correct. Risk of regret

- Unduly received benefits must be repaid. Have you deliberately given us incorrect information? Then you may also be fined. - Nothing is mentioned.

Non-take-up

At the end of the vignette text, I asked the question: What is the likelihood that you would apply for this benefit? 0% likelihood = definitely will not apply, 100% likelihood = will definitely apply. Respondents could select any value between 1 and 100. Because I am interested in non-take-up (instead of take-up), I subtracted the given score from 100. I used that final score in the subsequent analyses. Higher scores indicate that the self-reported likelihood of non-take-up is higher. Of course, this subjective estimate of the likelihood of non-take-up does not necessarily perfectly reflect actual non-take-up. I consider this limitation in the discussion.

Results

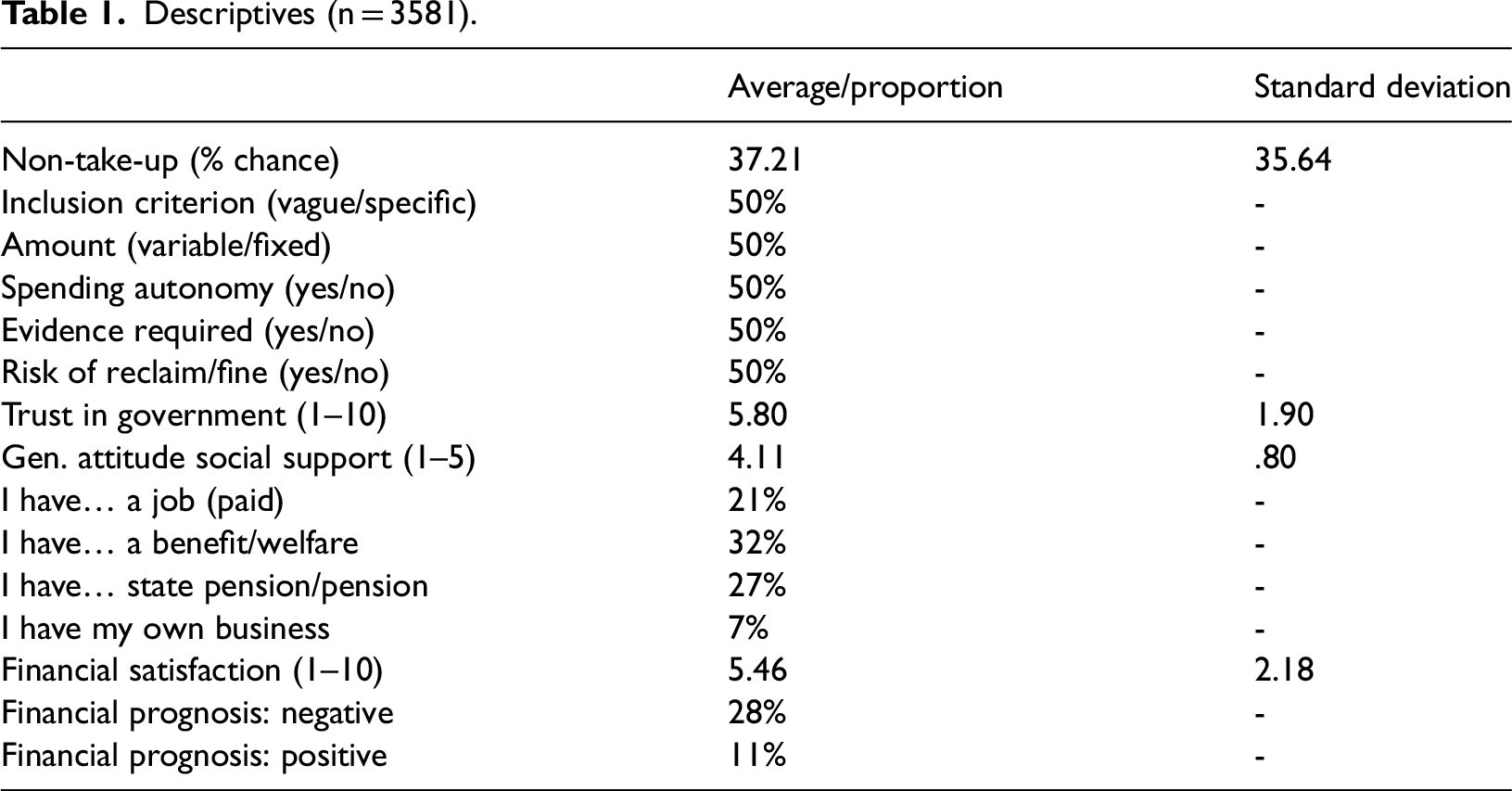

The descriptive statistics of the variables in the model can be seen below in Table 1.

Descriptives (n = 3581).

First of all, it can be seen that the respondents are generally neither very trusting nor very distrustful of the government. This corresponds quite well with the Dutch national trust figures over the past 15 years (De Blok, 2022). Respondents are also neither very satisfied nor very dissatisfied with their financial situation: on average they give it 5.5 out of 10. Nearly a third (28%) of respondents foresee their financial situation deteriorating in the near future, while only 11% foresee an improvement. A significant portion of our respondents have a paid job (21%). Likewise, our sample also includes a fair number of relatively old people (67+), as 27% currently receive a (state) pension. The average self-reported probability of non-take-up is 37%.

As the dependent variable in the model is measured at the interval level and our model contains multiple independent variables, I use a multiple linear regression analysis to test my hypotheses. As trust, financial satisfaction and general attitude towards social support were included in the regression as continuous variables, a positive regression coefficient (B) related to these variables indicates that a higher value, taking into account the other variables in the model, was associated with a higher self-reported probability of non-take-up. The other explanatory variables in my model are category-based and have two levels. The regression coefficient should be interpreted as the average difference in the self-reported probability of non-take-up between the two categories, controlling for the other variables in the model. The regression table shows which score has been assigned to which level of the factor in the vignette.

The independent variables were added to the regression hierarchically: the first step included only the various characteristics of the income supplementation scheme; the second step included the degree of trust in the government, the third step included the control variables.

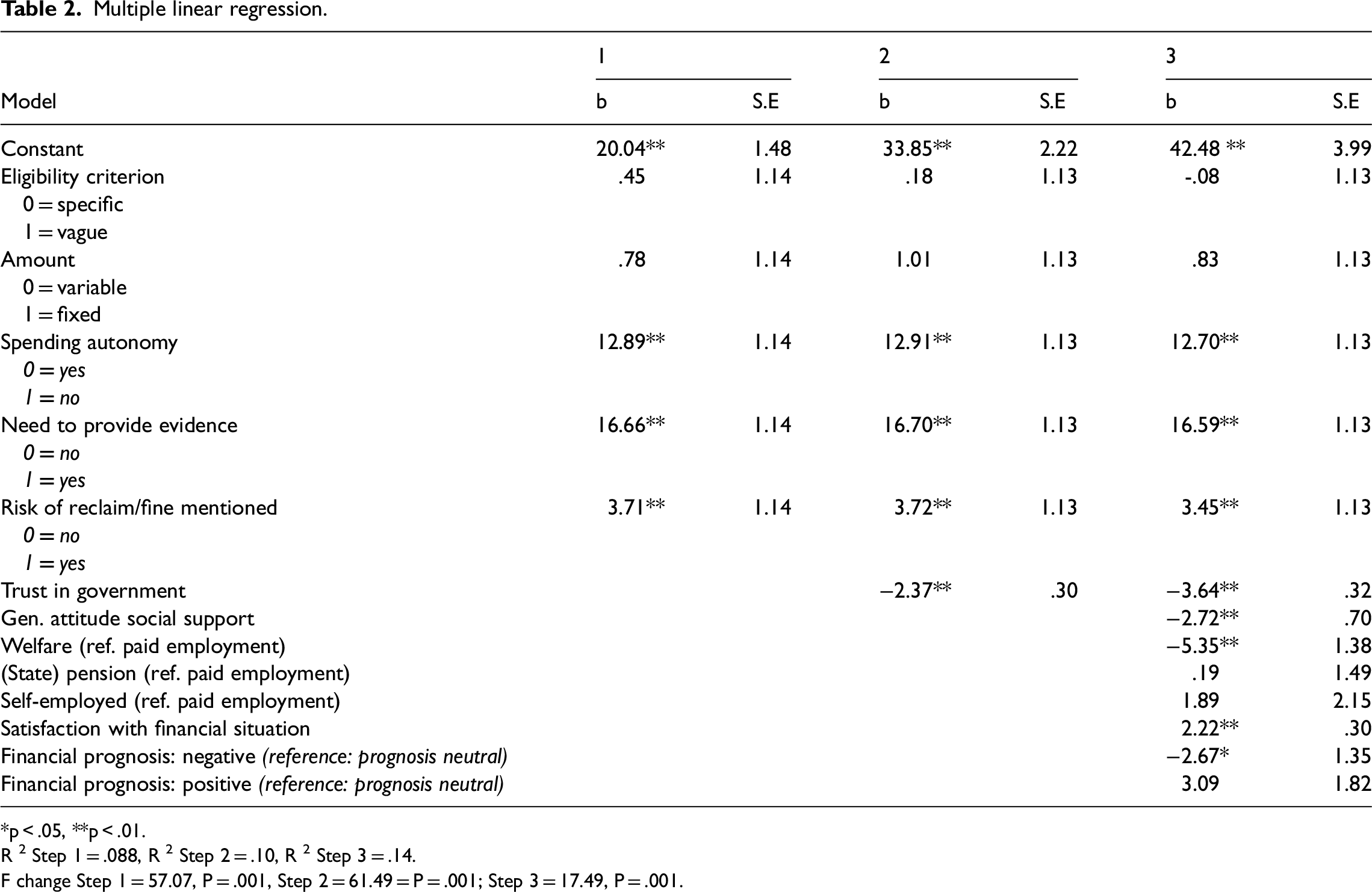

Table 2 below shows the results of the multiple regression analysis.

Multiple linear regression.

*p < .05, **p < .01.

R 2 Step 1 = .088, R 2 Step 2 = .10, R 2 Step 3 = .14.

F change Step 1 = 57.07, P = .001, Step 2 = 61.49 = P = .001; Step 3 = 17.49, P = .001.

Table 2 shows that approximately 14% of the variation in the self-reported probability of non-take-up can be explained by all of the variables in our model. About half of the total explained (8.5%) variance can be attributed to the five characteristics of the benefit scheme included in the model. Only three of those five were statistically significant: the absence of spending autonomy and the need to provide evidence of eligibility were associated with a higher self-reported likelihood of non-take-up. These findings support hypothesis 1. Explicitly mentioning the risk of having to repay the benefit and incurring a possible fine in case of fraud was also associated with a higher likelihood of self-reported non-take-up. This confirms hypothesis 3.

The second regression model includes the level of trust in the government. The table shows that the level of trust in the government is related to the reported likelihood of non-take-up. Respondents with less trust in the government considered themselves less likely to apply for a benefit – regardless of the specific characteristics of the benefit presented to them – than respondents with higher levels of trust in the government. More specifically, respondents with relatively low levels of trust (one standard deviation below the mean, +/- 4 out of 10) on average reported approximately a 9% higher likelihood of non-take-up than respondents with a relatively high degree of trust (+ one standard deviation above the mean, approximately 7. 8 out of 10). Hypothesis 2 is confirmed by our data, as the level of trust does seem to be associated with non-take-up, albeit not to the level I perhaps expected.

The third regression model contains all my variables of interest, including the control variables. Concerning the control variables, respondents’ attitude towards social assistance in general also contributed to the regression of the self-reported likelihood of non-take-up. Respondents with higher levels of support for social assistance in general, reported a lower likelihood of non-take-up. It can also be seen that the current level of satisfaction with one’s financial situation is associated with a higher self-reported likelihood of non-take-up: respondents who are more satisfied with their current financial situation on average reported a higher likelihood of non-take-up. Likewise, if respondents foresee a deterioration of their financial situation in the future, the self-reported probability of non-take-up is slightly lower, compared to respondents in the neutral category. However, the opposite does not apply: a positive financial prognosis does not seem to be associated with a higher likelihood of non-take-up compared to respondents in the neutral category. Finally, people who listed ‘welfare’ as their main source of income, on average reported a lower likelihood of non-take-up, compared to respondents who reported a paid job as their main source of income.

Conclusion and discussion

In this paper I addressed two possible explanations for the high levels of non-take-up of local income supplementation benefits: the characteristics shared by most of these schemes and the level of trust of citizens in the government.

From a rational choice perspective, potential applicants weigh the potential advantages of applying for an income supplementation benefit against the associated (objective, social and psychological) costs. The application process for small, means-tested benefits is often perceived as arduous, requiring applicants to provide the municipality with extensive evidence of eligibility. This not only places administrative and informational burdens on potential applicants, but also enforces the negative feelings associated with claiming. Moreover, examples of stringent fraud policies may have damaged people’s trust in the government and have exacerbated fears of the potentially severe consequences of mistakes, as well as anticipated regret linked to the decision to claim.

By and large, the results confirm these assumptions. The choice to apply for a benefit offered by the government seems to depend – to a certain extent – on the expected costs and benefits associated with an application. Requiring extensive evidence from applicants and denying them autonomy on how to spend the benefit were both associated with higher levels of non-take-up. Our study provides only limited support for the hypothesis of the Dutch National Ombudsman, who sees the lack of trust in the government as the cause of citizens’ avoidance of governmental social support schemes. The level of trust of respondents in the government seems (in terms of the estimated B value) to be only moderately relevant for non-take-up. Similarly, highlighting the possibility that a benefit will have to be repaid if it is received unduly and that, in case of fraud, a fine is imposed was associated with only a (slightly) higher risk of non-take-up.

The relatively moderate effect of trust on non-take-up observed in this study reflects the complex and multifaceted nature of the decision-making process involved in claiming benefits. While trust in institutions is indeed relevant, other practical factors – such as the complexity of application procedures, the stigma associated with claiming benefits, or the perceived risk of having to repay them – may play a more immediate and decisive role. Moreover, individuals may prioritise more explicit, tangible, costs and benefits over broader concerns about trust when deciding whether to engage with these schemes.

Explicitly mentioning the possibility of a reclaim and a fine was only associated with a slightly higher likelihood of self-reported non-take-up. This could be interpreted as meaning that those anticipated risks are not a very relevant factor in the decision to claim an income support measure. However, it could also be that our respondents expect this to be the case. For over 20 years, the focus of the Dutch system of social support has been on the prevention and punishment of fraud. One would not expect (not) mentioning this well-known fact to have any significant impact on non-take-up.

Limitations and directions for future research

While there is much value in collecting data from vignette studies, further testing of my findings is required using a different type of design. For example, while I based the vignettes on actual income supplementation benefits, they are still artificial constructs, and participants may respond differently to hypothetical situations than to real-life scenarios. This can lead to issues with the external validity of the findings, as the responses may not accurately reflect how individuals would behave in actual situations. It is therefore difficult to determine the actual impact of benefit characteristics and trust on non-take-up based on a vignette study. For example, not asking applicants to provide evidence of means might make more people start an application process, but does not take away from the fact that there can be all sorts of additional reasons for not following through with one.

Non-take-up is a difficult problem to tackle effectively, as there are many moving parts that explain potential beneficiaries’ decisions to refrain from applying. My model, which only considers a few variables of interest, may only account for a small portion of the variance in the self-reported likelihood of non-take-up.

However, while this study has several limitations that warrant consideration, including the potential that unmeasured confounding factors may influence the observed associations, the findings highlight three characteristics commonly associated with income supplementation benefits, which appear to play a role in beneficiaries’ decisions not to claim income supplementation benefits: these benefits are extensively means-tested, often restrict spending autonomy, and carry the (perceived) risk of repayment and/or fines. These characteristics may collectively contribute to non-take-up, though further research is needed to confirm and refine these observations in light of potential confounders.

Governments seeking to address the issue of non-take-up of income supplementation schemes could explore strategies such as relaxing the burden of proof required from applicants and granting beneficiaries greater spending autonomy. While these measures may reduce some barriers to participation, non-take-up is influenced by a complex interplay of factors, and it is likely that this issue will persist to some degree. Even with such measures in place it seems very likely that non-take-up will remain a problem that plagues income supplementation benefits.